Booms and Systemic Banking Crises

64

Booms and Systemic Banking Crises F. Boissay, F. Collard and F. Smets NBB Conference, October 2012 Boissay - Collard - Smets Booms and Systemic Banking Crises NBB Conference, October 2012 1 / 50

Transcript of Booms and Systemic Banking Crises

Booms and Systemic Banking Crises

F. Boissay, F. Collard and F. Smets

NBB Conference, October 2012

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 1 / 50

Disclaimer

The views expressed in this presentation are our own and do notnecessarily reflect those of the European Central Bank or the Eurosystem

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 2 / 50

Motivation/Objective

Better understand the joint dynamics of regular business cycles andsystemic banking crises (SBCs)

Account for the few features common to SBCs (Reinhart and Rogoff,2009; Jordà et al., 2011; Claessens et al., 2011; Schularick andTaylor, 2012):

Key Fact #1: SBCs are rare events —on average 1 every 40 years inOECD countries

Key Fact #2: Recessions that follow SBCs are deeper and last longer—output loss during a SBC is 60% largerKey Fact #3: SBCs are "credit booms gone wrong"

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 3 / 50

Motivation/Objective

Better understand the joint dynamics of regular business cycles andsystemic banking crises (SBCs)

Account for the few features common to SBCs (Reinhart and Rogoff,2009; Jordà et al., 2011; Claessens et al., 2011; Schularick andTaylor, 2012):

Key Fact #1: SBCs are rare events —on average 1 every 40 years inOECD countriesKey Fact #2: Recessions that follow SBCs are deeper and last longer—output loss during a SBC is 60% larger

Key Fact #3: SBCs are "credit booms gone wrong"

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 3 / 50

Motivation/Objective

Better understand the joint dynamics of regular business cycles andsystemic banking crises (SBCs)

Account for the few features common to SBCs (Reinhart and Rogoff,2009; Jordà et al., 2011; Claessens et al., 2011; Schularick andTaylor, 2012):

Key Fact #1: SBCs are rare events —on average 1 every 40 years inOECD countriesKey Fact #2: Recessions that follow SBCs are deeper and last longer—output loss during a SBC is 60% largerKey Fact #3: SBCs are "credit booms gone wrong"

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 3 / 50

Motivation/Objective

In most DSGE models with financial frictions banking crises are bignegative shocks amplified

Can explain Key Facts #1 & #2Cannot explain Key Fact #3 ← SBCs are not random

Explaining Key Fact #3 requires to model the economic dynamicsleading to SBCs

From a policy perspective, our framework is a step forward towards:

DSGE—based crisis prevention policy analysisDSGE—based early warning signals

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 4 / 50

Motivation/Objective

In most DSGE models with financial frictions banking crises are bignegative shocks amplified

Can explain Key Facts #1 & #2

Cannot explain Key Fact #3 ← SBCs are not random

Explaining Key Fact #3 requires to model the economic dynamicsleading to SBCs

From a policy perspective, our framework is a step forward towards:

DSGE—based crisis prevention policy analysisDSGE—based early warning signals

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 4 / 50

Motivation/Objective

In most DSGE models with financial frictions banking crises are bignegative shocks amplified

Can explain Key Facts #1 & #2Cannot explain Key Fact #3 ← SBCs are not random

Explaining Key Fact #3 requires to model the economic dynamicsleading to SBCs

From a policy perspective, our framework is a step forward towards:

DSGE—based crisis prevention policy analysisDSGE—based early warning signals

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 4 / 50

Motivation/Objective

In most DSGE models with financial frictions banking crises are bignegative shocks amplified

Can explain Key Facts #1 & #2Cannot explain Key Fact #3 ← SBCs are not random

Explaining Key Fact #3 requires to model the economic dynamicsleading to SBCs

From a policy perspective, our framework is a step forward towards:

DSGE—based crisis prevention policy analysisDSGE—based early warning signals

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 4 / 50

Motivation/Objective

In most DSGE models with financial frictions banking crises are bignegative shocks amplified

Can explain Key Facts #1 & #2Cannot explain Key Fact #3 ← SBCs are not random

Explaining Key Fact #3 requires to model the economic dynamicsleading to SBCs

From a policy perspective, our framework is a step forward towards:

DSGE—based crisis prevention policy analysisDSGE—based early warning signals

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 4 / 50

Motivation/Objective

In most DSGE models with financial frictions banking crises are bignegative shocks amplified

Can explain Key Facts #1 & #2Cannot explain Key Fact #3 ← SBCs are not random

Explaining Key Fact #3 requires to model the economic dynamicsleading to SBCs

From a policy perspective, our framework is a step forward towards:

DSGE—based crisis prevention policy analysis

DSGE—based early warning signals

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 4 / 50

Motivation/Objective

In most DSGE models with financial frictions banking crises are bignegative shocks amplified

Can explain Key Facts #1 & #2Cannot explain Key Fact #3 ← SBCs are not random

Explaining Key Fact #3 requires to model the economic dynamicsleading to SBCs

From a policy perspective, our framework is a step forward towards:

DSGE—based crisis prevention policy analysisDSGE—based early warning signals

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 4 / 50

Outline

Stylized facts

Comparison with the literature

RBC model with systemic banking crises

Quantitative analysis

Concluding remarks

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 5 / 50

Stylized factsSBCs are rare and bring about deep and long recessions

Frequency, magnitude, and duration of systemic banking crises

Frequency Magnitude Duration(%) (%) (Years)

from peak to trough

All banking crises 4.49 — —Systemic Banking Crises (SBC) 2.42 — —

All recessions 10.20 4.86 (5.91) 1.85Recessions with SBC (A) 23.86 6.74 (6.61) 2.59Recessions w/o SBC (B) 76.13 4.27 (5.61) 1.61Test A 6=B, p-value (%) — 2.61 0.00

Source: Schularik et al. (2011), data for 14 OECD countries, 1870-2008

Crises defined as in Laeven and Valencia (2008)

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 6 / 50

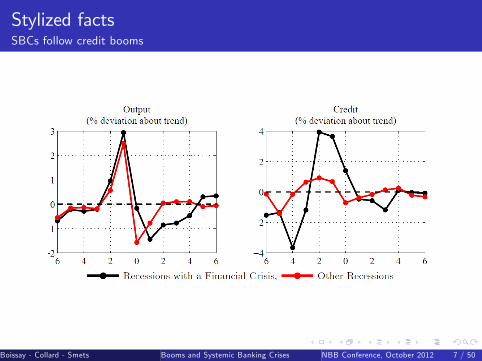

Stylized factsSBCs follow credit booms

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 7 / 50

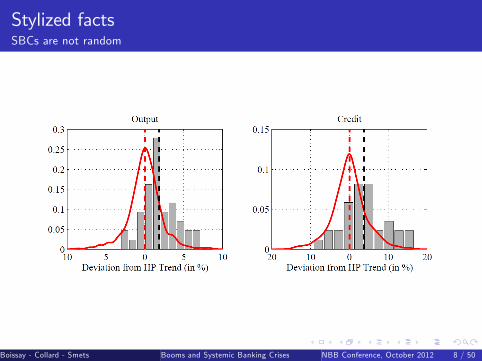

Stylized factsSBCs are not random

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 8 / 50

Our Framework

Textbook stochastic optimal growth model (RBC)

Heterogenous banks endowed with intermediation and storagetechnologies

Interbank market subject to MH and AI

A Systemic Banking Crisis is an inter-bank market freeze

Spill-over effects between the interbank market, the retail corporateloan market, and the real economy

Boissay - Collard - Smets ()Booms and Systemic Banking Crises NBB Conference, October 2012 9 / 50

Main Results

1 Model features a (small) financial accelerator in normal times;calibrated to generate financial crises every 40 years

2 The typical banking crisis follows upon an unusually longsequence of small, positive, transitory productivity shocks –Not a large negative financial shock

3 Financial recessions follow credit booms. They are deeper and lastlonger because they come with a credit crunch

4 The likelihood, depth, and length of a financial recession increasewith the intensity of the credit boom that precedes it

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 10 /

50

Main Results

1 Model features a (small) financial accelerator in normal times;calibrated to generate financial crises every 40 years

2 The typical banking crisis follows upon an unusually longsequence of small, positive, transitory productivity shocks –Not a large negative financial shock

3 Financial recessions follow credit booms. They are deeper and lastlonger because they come with a credit crunch

4 The likelihood, depth, and length of a financial recession increasewith the intensity of the credit boom that precedes it

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 10 /

50

Main Results

1 Model features a (small) financial accelerator in normal times;calibrated to generate financial crises every 40 years

2 The typical banking crisis follows upon an unusually longsequence of small, positive, transitory productivity shocks –Not a large negative financial shock

3 Financial recessions follow credit booms. They are deeper and lastlonger because they come with a credit crunch

4 The likelihood, depth, and length of a financial recession increasewith the intensity of the credit boom that precedes it

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 10 /

50

Main Results

1 Model features a (small) financial accelerator in normal times;calibrated to generate financial crises every 40 years

2 The typical banking crisis follows upon an unusually longsequence of small, positive, transitory productivity shocks –Not a large negative financial shock

3 Financial recessions follow credit booms. They are deeper and lastlonger because they come with a credit crunch

4 The likelihood, depth, and length of a financial recession increasewith the intensity of the credit boom that precedes it

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 10 /

50

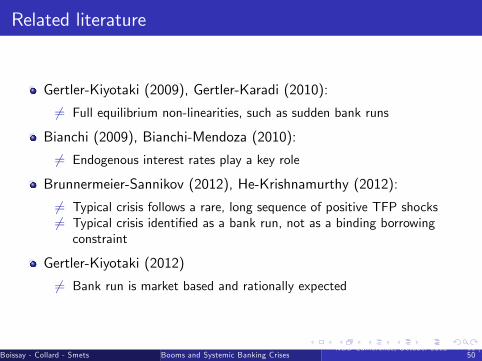

Related literature

Gertler-Kiyotaki (2009), Gertler-Karadi (2010):

6= Full equilibrium non-linearities, such as sudden bank runs

Bianchi (2009), Bianchi-Mendoza (2010):

6= Endogenous interest rates play a key role

Brunnermeier-Sannikov (2012), He-Krishnamurthy (2012):

6= Typical crisis follows a rare, long sequence of positive TFP shocks6= Typical crisis identified as a bank run, not as a binding borrowingconstraint

Gertler-Kiyotaki (2012)

6= Bank run is market based and rationally expected

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 11 /

50

Model setupOverview

RepresentativeHousehold

RepresentativeEntrepreneur

Bank deposits/equity at

CorporateLoans kt

Loan paymentsRtkt

Return on savingsrtat

Banking sector

Intermediation cost

Financial flows at the beginning of period t (“core activity”)

Financial flows at the end of period t (“core activity”)

Financial flows at the end of period t1 (“core activity”)

Financial flows at the beginning of period t (“noncore activity”)

Financial flows at the end of period t (“noncore activity”)

Banks are heterogeneous w.r.t. their financial intermediation costs

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 12 /

50

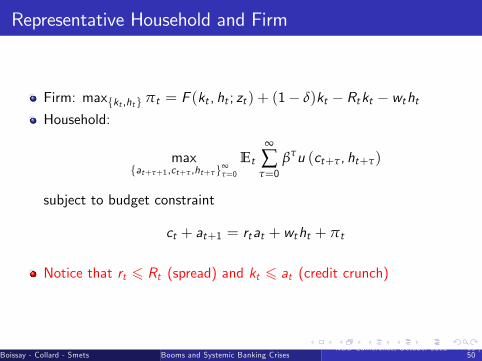

Representative Household and Firm

Firm: max{kt ,ht} πt = F (kt , ht ; zt ) + (1− δ)kt − Rtkt − wthtHousehold:

max{at+τ+1,ct+τ ,ht+τ}∞

τ=0

Et

∞

∑τ=0

βτu (ct+τ, ht+τ)

subject to budget constraint

ct + at+1 = rtat + wtht + πt

Notice that rt 6 Rt (spread) and kt 6 at (credit crunch)

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 13 /

50

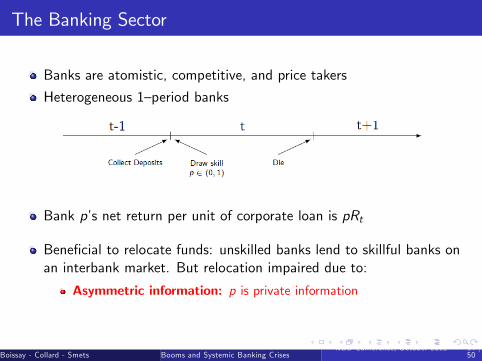

The Banking Sector

Banks are atomistic, competitive, and price takers

Heterogeneous 1—period banks

Bank p’s net return per unit of corporate loan is pRt

Beneficial to relocate funds: unskilled banks lend to skillful banks onan interbank market. But relocation impaired due to:

Asymmetric information: p is private informationMoral hazard: bank p may borrow φt and run away

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 14 /

50

The Banking Sector

Banks are atomistic, competitive, and price takers

Heterogeneous 1—period banks

Bank p’s net return per unit of corporate loan is pRt

Beneficial to relocate funds: unskilled banks lend to skillful banks onan interbank market. But relocation impaired due to:

Asymmetric information: p is private information

Moral hazard: bank p may borrow φt and run away

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 14 /

50

The Banking Sector

Banks are atomistic, competitive, and price takers

Heterogeneous 1—period banks

Bank p’s net return per unit of corporate loan is pRt

Beneficial to relocate funds: unskilled banks lend to skillful banks onan interbank market. But relocation impaired due to:

Asymmetric information: p is private informationMoral hazard: bank p may borrow φt and run away

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 14 /

50

The Banking Sector

Bank p has 4 options:

1. Lend to other banks on the market =⇒ ρt2. Store goods =⇒ γ3. Raise funds φt from market and lend to firm =⇒ pRt (1+ φt )4. Raise funds φt from market and walk away =⇒ γ (1+ θφt )

Notice that the incentive to divert depends on corporate loan RtThe higher Rt , the lower the incentive to divert

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 15 /

50

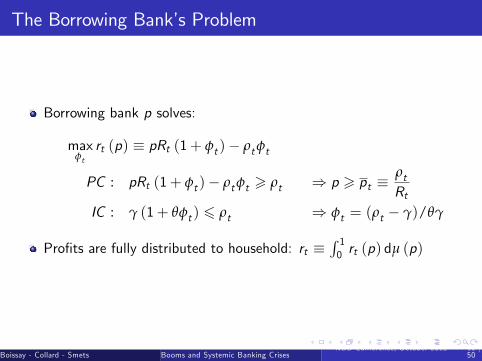

The Borrowing Bank’s Problem

Borrowing bank p solves:

maxφtrt (p) ≡ pRt (1+ φt )− ρtφt

PC : pRt (1+ φt )− ρtφt > ρt ⇒ p > pt ≡ρtRt

IC : γ (1+ θφt ) 6 ρt ⇒ φt = (ρt − γ)/θγ

Profits are fully distributed to household: rt ≡∫ 10 rt (p) dµ (p)

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 16 /

50

Interbank Market EquilibriumInterbank market clearing condition

Supply (+)︷ ︸︸ ︷µ (pt ) =

Demand bends backward (+ or −)︷ ︸︸ ︷(1− µ (pt ))︸ ︷︷ ︸

"extensive margin" (−)

× φt︸︷︷︸"intensive margin" (+)

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 17 /

50

Interbank Market EquilibriumTrade takes place when the corporate loan rate is high

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 18 /

50

Interbank Market EquilibriumTrade is impossible when the corporate loan rate is low

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 19 /

50

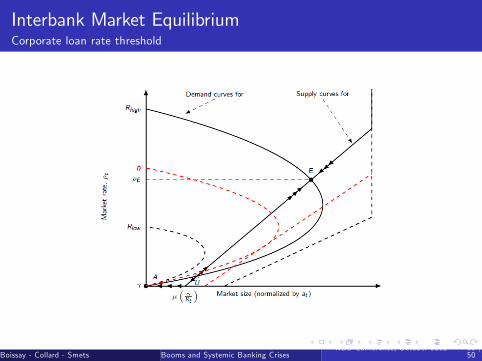

Interbank Market EquilibriumCorporate loan rate threshold

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 20 /

50

The Banking SectorReturn on equity and corporate loan supply

Return on equity:

rt =

Rt∫ 1ptp dµ(p)1−µ(pt )

, if an equilibrium with trade exists

Rt(

γRt

µ(

γRt

)+∫ 1

γRtp dµ (p)

), otherwise.

Corporate loan supply

kst =

at , if an equilibrium with trade exists(1− µ

(γRt

))at , otherwise

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 21 /

50

The Banking SectorCrisis and credit crunch

Proposition 2 (Interbank loan market freeze): The interbank loanmarket is at work if and only if at 6 at ≡ f −1k (R + δ− 1; zt ), andfreezes otherwise.

Proposition 3 (Credit crunch): An interbank market freeze isaccompanied with a sudden fall in the supply of corporate loans kst(i.e. given zt , limat↘at k

st < limat↗at k

st ), as well as by a sudden

increase in the interest rate spread Rt/rt (i.e. given zt ,limat↘at Rt/rt > limat↗at Rt/rt).

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 22 /

50

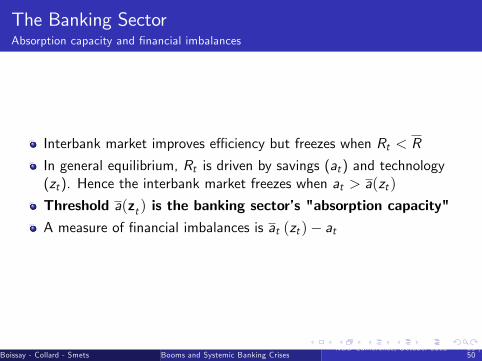

The Banking SectorAbsorption capacity and financial imbalances

Interbank market improves effi ciency but freezes when Rt < R

In general equilibrium, Rt is driven by savings (at) and technology(zt). Hence the interbank market freezes when at > a(zt )

Threshold a(zt ) is the banking sector’s "absorption capacity"A measure of financial imbalances is at (zt )− at

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 23 /

50

The Banking SectorInterest rates

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 24 /

50

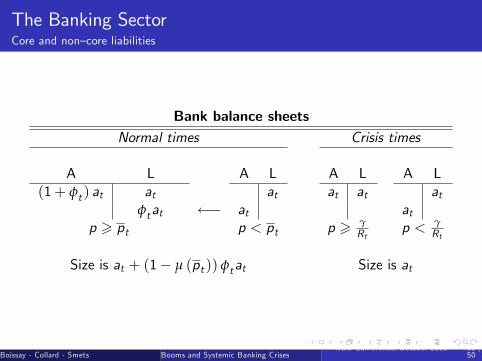

The Banking SectorCore and non—core liabilities

Bank balance sheetsNormal times Crisis times

A L A L A L A L(1+ φt ) at at at at at at

φtat ←− at atp > pt p < pt p > γ

Rtp < γ

Rt

Size is at + (1− µ (pt )) φtat Size is at

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 25 /

50

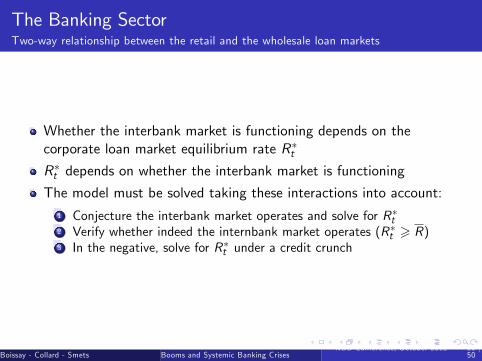

The Banking SectorTwo-way relationship between the retail and the wholesale loan markets

Whether the interbank market is functioning depends on thecorporate loan market equilibrium rate R∗tR∗t depends on whether the interbank market is functioning

The model must be solved taking these interactions into account:1 Conjecture the interbank market operates and solve for R∗t2 Verify whether indeed the internbank market operates (R∗t > R)3 In the negative, solve for R∗t under a credit crunch

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 26 /

50

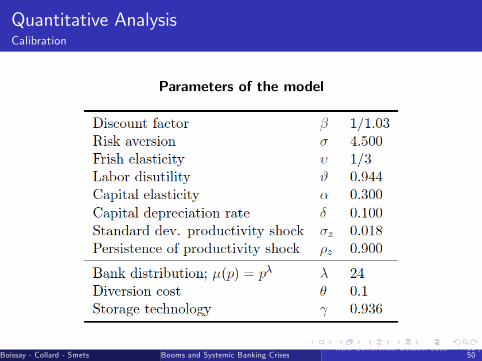

Quantitative AnalysisCalibration

Production function: F (kt , ht ; zt ) ≡ ztkαt h1−αt with α ∈ (0, 1)

Utility function: u (ct , ht ) = 11−σ

(ct − ϑ h

1+υt1+υ

)1−σ

Cdf of bank skills: µ(p) = pλ

Real economy: standard calibration on US (annual) post—WWII data

Financial sector (γ, θ, λ) is calibrated so that:

Crisis probability is 2.5%Average interest rate spread is 1.71%Average corporate loan rate of 4.35%

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 27 /

50

Quantitative AnalysisCalibration

Parameters of the model

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 28 /

50

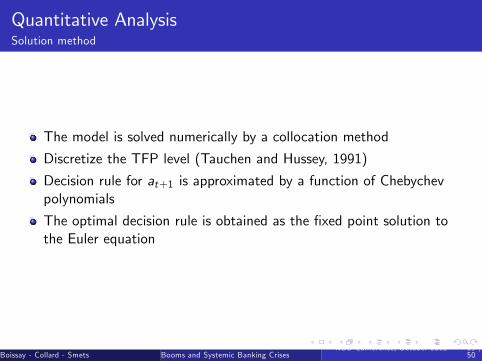

Quantitative AnalysisSolution method

The model is solved numerically by a collocation method

Discretize the TFP level (Tauchen and Hussey, 1991)

Decision rule for at+1 is approximated by a function of Chebychevpolynomials

The optimal decision rule is obtained as the fixed point solution tothe Euler equation

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 29 /

50

Quantitative AnalysisOptimal savings rule: exogenous versus endogenous crises

at

at+1

Crisis originates withan unusually largenegative shock

Average TFP

Crisis originates withan unusually longsequence of positiveshocks

Low TFP

High TFP

S

O

U

Variety of crises: shock—driven (S) and credit boom—driven (U)

History suggests that credit—boom driven crises prevail

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 30 /

50

Quantitative AnalysisOptimal savings rule: exogenous versus endogenous crises

at

at+1

Crisis originates withan unusually largenegative shock

Average TFP

Crisis originates withan unusually longsequence of positiveshocks

Low TFP

High TFP

S

O

U

Variety of crises: shock—driven (S) and credit boom—driven (U)

History suggests that credit—boom driven crises prevail

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 30 /

50

Quantitative AnalysisIntuition behind endogenous SBCs

1 At the beginning, a positive shock brings TFP above its mean

Credit demand rises. Return on savings goes up. The householdaccumulates assets for consumption smoothingThe credit boom is initially demand—driven

2 TFP goes down back to mean but remains above it for a long time

Credit demand decreases, while the household keeps on accumulatingsavingsThe credit boom becomes supply—driven

3 The household accumulates assets for precautionary motives, whichworks to reduce interest rates and to raise further the likelihood of acrisis

4 A SBC breaks out as the corporate loan rate crosses its threshold

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 31 /

50

Quantitative AnalysisTypical path to crisis

Typical path

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 32 /

50

Quantitative AnalysisTypical path to crisis

Financial variables dynamics along typical path

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 33 /

50

Quantitative AnalysisTypical path to crisis

Real variables dynamics along typical path

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 34 /

50

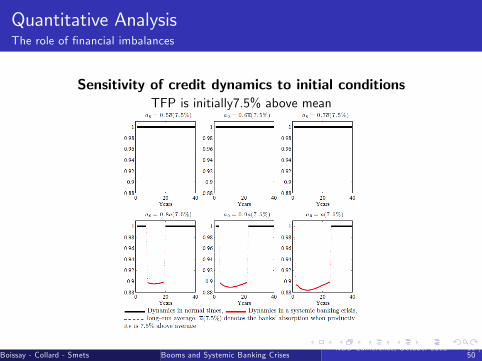

Quantitative AnalysisThe role of financial imbalances

Sensitivity of output dynamics to initial conditionsTFP is initially7.5% above mean

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 35 /

50

Quantitative AnalysisThe role of financial imbalances

Sensitivity of credit dynamics to initial conditionsTFP is initially7.5% above mean

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 36 /

50

Quantitative AnalysisThe role of financial imbalances

Sensitivity of the frequency of SBCs to initial conditionsTFP is initially7.5% above mean

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 37 /

50

Quantitative AnalysisThe role of savings behaviour

Sensitivity of the frequency of SBCs to initial conditionsTFP is initially7.5% above mean

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 38 /

50

Quantitative AssessmentSBCs are rare and bring about deep and long recessions

Frequency, magnitude, and duration of systemic banking crises

Frequency Magnitude Duration(%) (%) (Years)

from peak to troughSystemic Banking Crises (SBC) 2.69 — —

All recessions 10.00 12.08 (7.30) 2.08Recessions with SBC (A) 13.00 17.87 (10.50) 2.62Recessions w/o SBC (B) 87.00 10.04 (6.73) 1.90

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 39 /

50

Quantitative AssessmentSBCs follow credit booms

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 40 /

50

Quantitative AssessmentSBCs are not random

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 41 /

50

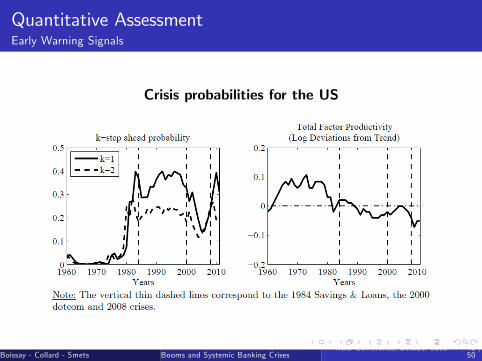

Quantitative AssessmentEarly Warning Signals

Crisis probabilities for the US

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 42 /

50

Sensitivity Analysis

Changes in standard parameters

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 43 /

50

Bank Leverage, Bank Defaults

Absent frictions between banks and household, bank leverage isundeterminate and bank default is not defined

Two more assumptions to pin down leverage:

Bank deposits are safe assets (non state contingent return)Bank managers are risk neutral (unlike household)

One more assumption to introduce defaults:

Household (bank shareholder) has partial liability

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 44 /

50

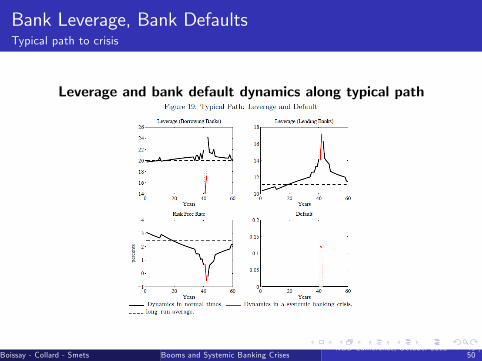

Bank Leverage, Bank DefaultsTypical path to crisis

Leverage and bank default dynamics along typical path

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 45 /

50

Concluding Remarks

Develop a simple DSGE model with SBCs

SBCs are not caused by large, negative, financial shocks but rather bylong sequences of small, positive, productivity shocks

Highlight the role of financial imbalances, consumption smoothing,and precautionary savings

From a policy making perspective:

Framework for both crisis management and crisis preventionDSGE-based probability of a crisis

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 46 /

50

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 47 /

50

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 48 /

50

The Model in a Nutshell

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 49 /

50

The Banking SectorA reduced form

Interest rate spread:

Rt − rt ={

∆nt if at6at (zt )∆ct otherwise

, with ∆ct > ∆nt > 0

Credit crunch:

at − kt ={

ψnt = 0 if at6at (zt )ψct > 0 otherwise

Notice that all this is micro-founded

Boissay - Collard - Smets ()Booms and Systemic Banking CrisesNBB Conference, October 2012 50 /

50