Book of Greeks

135

The Book of Greeks Edition L1 0 Rahul Bhattacharya CFE School, Risk Latte Company Limited, Hong Kong 2011

-

Upload

nicolas-lefevre-laumonier -

Category

Documents

-

view

228 -

download

0

Transcript of Book of Greeks

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 1/135

The

Book

of GreeksEdition L1 0

Rahul Bhattacharya

CFE School, Risk Latte Company Limited, Hong Kong

2011

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 2/135

2

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Dedicated to my father, Chandranath Bhattacharya

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 3/135

3

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

What Industry Practitioners have to say about this book?

Rahul Bhattacharya has composed an indispensable collection of notes on Quantitative

Finance with an astonishingly broad coverage. The book familiarizes the reader with awide array of models used in the industry with tips on implementation in Excel™. Excel™is an excellent pedagogical tool and the material in the book invites the reader to

implement the models. The book also contains an extensive coverage of structures traded

across asset classes and even the most seasoned professional will find something new in it.

This is more than a study aid; this is an excellent reference that should be kept within reachon any derivatives desk.

Boris MangalFX Options TraderRBC Capital Markets, Tokyo

The Book of Greeks is an amazingly useful compendium. Rahul Bhattacharya has produced

an easy-reference compilation of the main results in quantitative finance, with just enough

write-ups to be able to apply them in practice, and spanning the entire field from basic stochastic processes to equity, credit, and rates, as well as exotic payoffs and numerical

methods. It distils the key results from an entire library of books, periodicals, and academic

papers into a single short volume that will save practitioners a lot of time and effort .

James de Castro

Former Head of Trading, Asia-Pacific (ex-Japan)

Merrill Lynch, Hong Kong

The Book of Greeks is a perfect companion for any risk manager, quant or derivatives

trader. It manages to have a unique blend of practical application through it's reference to

excel whilst giving the reader all the technical and academic detail he could ever require.

It takes time to give background to the world of modern derivatives and describes the

origins of advanced techniques and models we all take for granted. Everything from

pricing today's exotic derivatives to simple black-scholes greeks are covered. No one

should ever be at their desk without it.

Richard Kendrick

Market Risk ManagementGoldman SachsLondon

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 4/135

4

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Foreward

The Book of Greeks is an excellent compendium of formulae, models and quantitative

techniques that should be in the repertoire of any derivatives trader, hedge fund manager,

derivatives structurer, academic or student of financial engineering.

Often when we work on trading desks or while structuring derivatives, we wish that we had

a book that had the answers and solutions to the myriad financial products that we have to

price or trade. Well, "The Book of Greeks" is the answer to our prayers. A wonderful, well

compiled book, it offers both the practitioner as well as the academic a one stop source of

mathematical techniques used in the world of financial engineering.

I have enjoyed going through this book and am delighted to be able to recommend it to

anyone who has an interest in quantitative finance and financial engineering.

Rajat BhatiaCEO, Neural CapitalFormer SVP, Citibank Global Asset Management, London& former VP, Lehman Brothers International, London.

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 5/135

5

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

First Few Words

This book is a collection of lecture notes that I’ve used for my CFE classes over the past 2years. These notes are intended to help the reader navigate through various formulas,

equations and algorithms that are used in the four modules of our Certificate in FinancialEngineering (CFE) course. Also, these notes will help all those students taking our CFEExam to better understand the landscape of the entire subject. However, by no means dothese notes present a comprehensive or an exhaustive list of formulas and equations that areused in the study of financial engineering and quantitative finance. At best, it is a miniscule portion of the entire discipline. If anything, these notes aim to provide to the reader aglimpse of the giant canvas on which the subject of Quantitative Finance is written.

All formulas and equations that are used in these notes are meant to be implemented on anExcel™ spr eadsheet. In our CFE course, we implement all these formulas and equations inExcel/VBA and then build quantitative models of financial derivatives and asset portfolio

pricing and risk analysis.

Financial Engineering or Quantitative Finance (and we shall use both these termsinterchangeably) is neither just physics nor applied mathematics, and much more than thesum total of the two. Quantitative Finance is concerned with the application of all those physics-like theories and advanced mathematical concepts and methodologies for thedevelopment of mathematical models and algorithms with which financial derivatives andfinancial asset portfolios can be traded, valued and their risks can be analyzed. However,such is not possible unless all those complex and abstract formulas and equations aretransformed into simpler workable format and implemented on a platform. And that platform has to be something that is very simple to understand and work on.

For our CFE course that platform is the Microsoft Excel™ spreadsheet.

These notes are exclusively meant for supplementing the knowledge and skills imparted inthe CFE course and helping students take the CFE examination. Other than that, this bookhas no other objective or pretense. This book should not be seen as an alternative orsupplement to any textbook on the subject of quantitative finance, a partial list of which isgiven at the end in the reference section. There are no substitutes for the great bookswritten by Jamil Baz, George Chacko, John Hull, Jim Gatheral, Rebonato Riccardo, PaulWilmott, to name only a few.

Rahul Bhattacharya

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 6/135

6

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Contents

Page

Chapter

The Journey: From U of Chicago to CBOE 10

0.1 Backgroud0.2 Two Physics problems0.3 A Very Brief History of Quant Finance0.4 Timelines0.5 Black-Scholes Era0.6 Heston Era

0.7 Post-Heston Era0.8 Volatility as a Financial Asset

Chapter M

Applied Mathematics and Numerical Methods in Finance 17

Part A: Matrices & Applications

M.1 Fun with Matrices: From Quantum Mechanics to Quant FinanceM.2 Types of Matrices

M.3 Eigenvalues and EigenvectorsM.4 Cholesky matrixM.5 Finding Square Root of MatrixM.6. Applications in Quantitative Finance

Part B: Probability & Probability Distributions

M.7 Probability and Measure TheoryM.8 Is Call Option price a Probability Measure?M.9. Expectations and Jensen’s Inequality

M.10 Moments of a DistributionM.11 Gaussian distributionM.12 Skew and Fat Tails

M.13 Change of MeasureM.14 Correlation and Covariance

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 7/135

7

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Part C: Binomial & Trinomial Trees

M.15 Cox-Ross-Rubinstein (CRR) TreeM.16 Trinomial Tree

M.17 Trinomial Tree with CRR parametersM.18 Other kinds of Binomial Trees

Part D: Black-Scholes Diffusion Equaiton & Green’s Function

M.19 Valution of Vanilla OptionsM.20 Valuation of Exotic Options

Part E: Numerical Integrals & Monte Carlo Integration

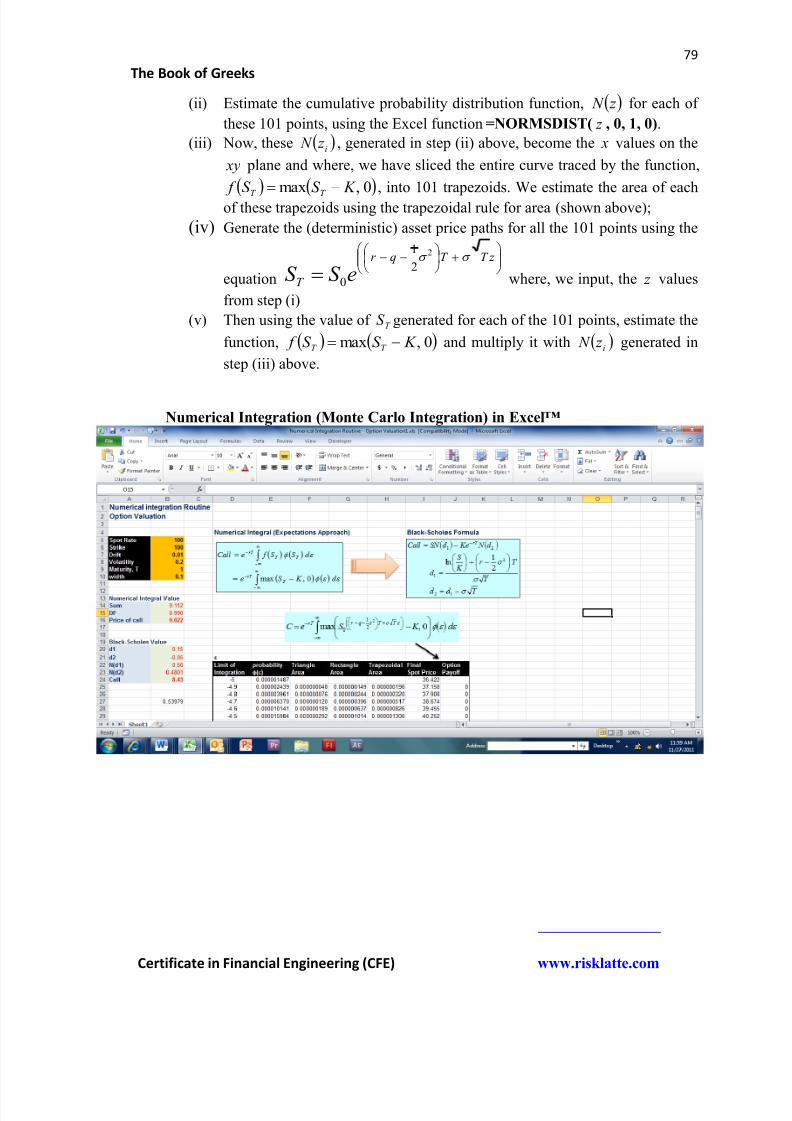

M.14 Trapezoidal and other rules for Numerical IntegrationM.15 Gaussian Quadrature MethodsM.15 Monte Carlo Integration to value Non-path Dependent OptionsM.16 Routine for Implementation in Excel™

Part F: Differential Equations & Finite Difference Methods

M.17 Ordinary Differential Equations in FinanceM.18 Stochastic Differential Equations in FinanceM.19 Partial Differential Equations in FinanceM.20 Finite Difference MethodsM.21 Laplace Transform

Chapter S

Stochastic Processes for Asset Price Modeling 84 (Monte Carlo Simulation on Excel™ spreadsheet)

S.1 Stochastic Process and a Markov ProcessS.2 Random WalkS.3 Geometric Brownian motion

S.4 S.5 Reimann Zeta Function and the Brownian motionS.6 Girsanov’s Theorem S.7 Brownian motion for the Inverse of the Asset PriceS.8 Brownian motion with defaultS.9 Stochastic Process for the Relative Process of Two AssetsS.10 Arithmetic Brownian motionS.11 Mean Reverting Brownian motion

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 8/135

8

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

S.12 Brownian Bridge ProcessS.13 Cox-Ross Square Root ProcessS.14 Ornstein-Uhlenbeck ProcessS.15 Vasicek Process

S.16 Cox-Ingersoll-Ross ProcessS.17 Black Derman Toy (BDT) ProcessS.18 Black Karisinski ProcessS.19 Poisson Jump Diffusion ProcessS.20 Kou’s Double Exponential Process S.21 Heston Stochastic Volatility ModelS.22 Double Mean Reverting Process for VarianceS.23 Constant Elasticity of Variance (CEV) ProcessS.24 Stochastic Alpha Beta Rho (SABR) ModelS.25 Longstaff’s Double Square Root Model

S.26 Stochastic Local Volatility (SLV) ProcessS.27 SLV Bloomberg ModelS.28 GARCH Diffusion ProcessS.29 Gibson & Schwarz Stochastic Convenience Yield ProcessS.30 Stochastic Correlation ProcessS.31 Mixture of Normals ProcessS.32 Variance Gamma (VG) ProcessS.33 Monte Carlo Simulation for VG ProcessS.34 Displaced Diffusion ModelS.35 Libor Market Model (LMM)

S.36 Homogenous Poisson ProcessS.37 Monte Carlo Simulation for Valuation of Single Asset optionsS.38 Multi-asset Stochastic ProcessS.39 Cholesky DecompostionS.40 Eigenvalue decompositionS.41 Monte Carlo Simulation of Valuation of Multi-asset optionsS.42 Cleaning Correlation MatricesS.43 Quantum Random Walk

Chapter E

Financial Products and Product Engineering (Structuring) 132

E.1 Vanilla OptionsE.2 Straddles and zero beta straddlesE.3 Binary OptionsE.4.Outperformance Digital optionsE.5 Money back options

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 9/135

9

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

E.6 Fixed and Floating Strike Lookback OptionsE.7 Arithmetic Average OptionsE.8 Chooser OptionsE.9 Symmetric and Asymmetric Power Options

E.10 Forward Starting and Cliquet OptionsE.11 Reverse Cliquet OptionsE.12 Napoleon OptionsE.13 Exchange OptionsE.14 Amortizing OptionsE.15 Pyramid and Madonna OptionsE.16 Basket OptionsE.17 Best of and Worst of OptionsE.18 Himalaya, Altipano and Everest OptionsE.19 Capped Bull Note

E.20 Principal Protected Bull NoteE.21 Principal Protected Bear NoteE.22 Principal Protected Mixed NoteE.22 Equity Linked Basket NoteE.23 Note with a Short Put option embeddedE.24 Perpetual Capped Call Note (American style) with no maturityE.25 Decomposition of Structured Product through Payoff DiagramE.26 Convertible Bonds and Reverse Convertible BondsE.27 Caplet and Snowball optionsE.28 Sycurve Options

Chapter V

Volatility and Correlation 166

Part A: Implied Volatility & Volatility Surface

V.1 Numerical Estimation of Implied VolatilityV.2 Leland’s Formula V.3 Brenner-Subrahmanyam Approximations

V.4 Corrado Miller ApproximationV.5 Steven Li’s Approximation V.6 SABR VolatilityV.7 CEV VolatilityV.8 Volatility SkewV.9 Implied Volatility Surface and Interpolating Implied VolatilityV.10 Vanna Volga Methodology

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 10/135

10

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

V.11 Local VolatilityV.12 Local Volatility in presence of Default

Part A: Historical Volatility

V.13 Historical Volatility using close to close priceV.14 Parkinson’s Number V.15 Garman-Klass EstimatorV.16 EWMA VolatilityV.17 GARCH Process

Part C: Model Free Volatility and Variance Swaps

V.18 Log Contract

V.19 Britten-Jones & Neuberger ModelV.20 Variance SwapV.21 VIX IndexV.22 Volatility SwapV.23 Correlation and Implied CorrelationV.24 Correlation SkewV.25 Dispersion

Chapter O

Options and Financial Derivatives Valuation 195

O.1 Vanilla Options using Black-Scholes ModelO.2 Put-Call Parity and Put-Call SymmetryO.3 Straddle OptionsO.4 Option pricing using Displaced Diffusion modelO.5 Power OptionO.6 Exchange OptionO.7 Binary OptionO.8 Barrier OptionO.9 One Touch Option

O.9 Double Barrier (Binary) OptionO.10 Fixed and Floating Strike Lookback optionsO.11 Arithmetic Average optionO.12 Forward Starting optionO.13 Caps and FloorsO.14 Swaption Valuation using Black’s formulaO.15 SYCURVE Options

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 11/135

11

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

O.16 Bond Option pricing using Black’s formulaO.17 Options on Zero Coupon Bond using Vasicek’s Model O.18 Options on Variance

Chapter G

Greeks for Vanilla & Exotic Options 221

G.1 Call and Put DeltaG.2 Call and Put GammaG.3 Vega of OptionsG.4 Hedging Error due to Volatility SmileG.5 Theta and Rho of Vanilla optionsG.6 Binary Call and Put DeltaG.7 Dirac Delta Function and the Binary

G.8 Binary Gamma and VegaG.9 Variance Swap Greeks

Chapter P

Portfolio Analysis & Asset Allocation 230

P.1 Sharpe Ratio, Treynor Ration and Jensen’s Alpha P.2 Portfolio VolatilityP.3 Expected Return for Stocks and BondsP.4 Volatility of Spreads

P.5 Probability of Stocks Outperforming BondsP.6 Mean-Variance Optimization for a Total Return ObjectiveP.7 Mean-Variance Optimization by maximizing Sharpe RatioP.8 Sharpe’s Algorithm for Efficient Frontier P.9 Portfolio InsuranceP.10 Constant Proportion Portfolio Insurance (CPPI)P.11 Capital Asset Pricing Model (CAPM)P.12 Minimization of Risk and MCR AlgorithmP.13 Statistical ArbitrageP.14 Triangular Arbitrage

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 12/135

12

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Chapter 0

The Journey From the University of Chicago to Chicago Board Options Exchange……

Background

Before we talk about Quantitative Finance, talk about its brief history and then plungeourselves into the thick of this discipline with formulas, equations and theory, it isworthwhile to understand the background in which this discipline originated some 50 to 60years ago. That background is physics. The foundations of quant finance were laid based ontheories and models of physics. The twin concepts of “equilibrium” and “linearity” whichunderlie almost all of early theories and models of quant finance are both borrowed from physics, as is most of the math and the rationale.

Two Physics problems and the Birth of Quant Finance

I. Albert Einstein and the Random Walk (Diffusion) Problem

Diffusion is one of the fundamental physical processes by which material in nature moves. Itis found in biology, chemistry, geology, engineering, and above all in physics. The processfirst originated in physics in the form of Brownian motion and was studied by none other thefamous physicist Albert Einstein in 1905. Diffusion arises due to the constant thermal motionof atoms, molecules, and particles and causes material to move from areas of highconcentration to low concentration. Therefore, the final outcome of diffusion would be astate of constant concentration across space. Take a bottle of deodorant or perfume and sprayit heavily inside a small closed room. Eventually the smell spreads across the room and the

entire room starts to smell nice. This is an example of diffusion. Take an iron rod and heatone end of it. Eventually, the other end becomes hot as well, because heat was transferredfrom the hot end to the cold end.

Actually, Albert Einstein had solved the Black-Scholes problem long ago. While studyingBrownian motion of particles to complete his Ph.D. thesis, he realized that the randommotion of the molecules at the microscopic level is ultimately responsible for the process ofdiffusion that occurs at the macroscopic level. Physicists had long studied the macroscopic phenomenon of diffusion and established the governing partial differential equation, PDE,( see below for more details on what is a PDE ). However, it took Einstein’s genius to realizethat the constant coefficient of diffusion in the governing PDE of the diffusion process is

actually the same as the volatility parameter, , of the microscopic random process of themolecules.

Note: Fischer Black and Myron Scholes, while formulating the option pricing problem inearly 1970s, followed more or less the same rationale and thought process as Einstein. Themath and the physics was exactly the same. Only the context was different and certain broad

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 13/135

13

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

(and sweeping) assumptions were made about the economy and the investors in relating the problem in physics to that in financial economics.

II. Richard Feynman’s “Path Integrals” and Feynman-Kac Approach

In 1948, Richard Feynman, another eminent physicist of the twentieth century made a simpleand stunning discovery. He found out that the Schrodinger’s partial differential equation(another example of a PDE) in quantum mechanics could be solved by some kind ofaveraging over the paths. This led to the reformulation of the entire quantum mechanicaltheory in physics in terms of what is known as “path integrals”. Mark Kac, a mathematicianand a colleague of Feynman at Cornell, immediately realized that the concept of “averagingof paths” could be applied to the solution of heat equation with boundary conditions andother kinds of diffusion equations in physics. In short, a diffusive partial differential equationcan be solved as an expectation, under a certain probability measure, of a function thatcontains a Brownian motion. This expectation approach has come to be known as the

Feynman-Kac solution.

Note: The expectations approach, developed by latter day quants and still used extensively by practicing quants in the banks and the academic theorists, to solve the pricing problem forvanilla and exotic options is exactly like Feynman and Kac’s approach. In f act, even quantscall it the Feynman-Kac approach. Everywhere, in finance textbooks, research papers and

other technical documents, you’ll see the expectation operator, E written as .Q E and inside

the brackets you’d see an option payoff. This is nothing but Feynman-Kac approach.

A Very Brief History of Quant Finance

The history of Quantitative Finance is essentially a history of the conquest of "Volatility".The story is about how a few exceptionally talented men across both sides of the Atlanticgrappled with the concept of volatility and ultimately tamed it. The story starts off in 1952with volatility being a statistical measure of financial risk and ends in the present day with it becoming a financial asset. That’s pretty much all there is to quantitative finance. Rest is justdetails and an awful lot of very advanced math and computer programming.

It all started in Chicago in 1952 with Harry Markowitz and ended in Chicago sometimearound 2003 when the new VIX was introduced. In that sense we may be living in the post-historical period.

Timeline

This timeline outlines how Volatility got transformed from being a measure of financial riskto financial asset. If we were to take a Jurassic Park style tour of Quant Finance then we’d betaken through the following periods:

Black-Scholes Era (1952 – 1987)

Heston Era (1988 – 2007)

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 14/135

14

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Post Heston (2007 – Present)

The History tour of Quant Finance

Black-Scholes Era (1952 – 1987)

Black Scholes era began when in 1952, Harry Markowtiz, during the course of completinghis Ph.D. dissertation realized that volatility is a statistical concept and in fact, is the same asthe concept of standard deviation. And mathematically speaking, this is the proxy forfinancial “risk”.

Constant Volatility

It was in 1973, when Fischer Black and Myron Scholes presented their seminal – perhaps,the most famous paper in all of quantitative finance – on option pricing. This could be

considered a formal beginning of the discipline of quant finance.

Here are the defining characteristics and landmarks of this era

In 1973 Black-Scholes option pricing model was introduced which modeled asset prices as following a geometric Brownian motion – a Gaussian diffusion process – with a fixed volatility parameter and option prices are determined as functions of theunderlying asset price. This fixed volatility parameter was important as this is thesame parameter that appears in the partial diffusion equation (PDE) for the option price as the “coefficient of diffusion”.

The physics of the problem was this: asset price is like the molecule following a

random walk suspended in a medium, where the “molecule” was the stock (asset) andthe “medium” was the volatility.

The fact that volatility is constant is extremely important in a Black-Scholes world, because it simplifies life enormously. Constant volatility implies and causes thefollowing:

(i) A market consisting of a stock and an interest-bearing bond is “complete”, inthe sense that all derivative payoffs can be replicated by a dynamic portfolioconsisting of the stock and the bond only.

(ii) Corollary to the above point is that the principle of no arbitrage leads to aunique equivalent martingale measure that can be used to price derivatives.

(iii) The Black-Scholes PDE (with boundary conditions) can be solved exactly as aheat equation and a neat formula for option price can be extracted (this is theBlack-Scholes option pricing formula).

In 1977 Oldrich Vasicek presented the mean reverting random walk model for asset price. This has now come to be known as the Vasicek model and over the years thismodel has found wide applications in interest rate derivatives valuation.

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 15/135

15

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

In 1976 John Cox and Steven Ross presented their risk-neutral argument andintuitively one of the most curious facts of the Black-Scholes model, that is, as to whythe drift term in the asset price equation of random walk drops out of the option pricing equation and the Black-Scholes formula.

Cox and Ross also presented the square root diffusion model of asset price which onceagain opened up new ways at looking at the option pricing problem. Closely related tothe Cox-Ross model was the Cox-Ingersoll-Ross (CIR) model of asset prices, anothermean reverting, arithmetic Brownian motion model of asset price. This model alsofound wide applications in interest rate modeling. More importantly, CIR model wouldform the basis for the stochastic volatility model developed by Heston in the early1990s.

Black-Scholes era came to an end with the stock market crash of 1987 when investorsrealized that volatility is not constant. The notion of volatility smile (skew) – a varyingimplied volatility across strike prices – was born and Wall Street started becoming a very

comfortable place for the quants. Strangely, as the physics was getting out of the way ofquantitative finance and making way for something far more complex (at least in terms ofcomprehension and conceptualization), more and more physicists started getting hired onWall Street.

Heston Era (1988 – 2007)

In my opimion the Heston era began around the time when John Hull and Alan White published their one factor stochastic volatility model in 1987. But this was still not a gamechanger. The real paradigm shift happened when Steven Heston came up with his two factorstochastic volatility model. This was the first break with physics like models.

Stochastic Volatility Here are the defining characteristics and landmarks of this era

Heston postulated that not only the asset price but volatility associated with that asset price is stochastic. In other words, both the asset price and the volatility of that asset price evolve randomly over time. Even though the asset price in Heston’s modelfollows the same geometric Brownian motion, i.e. a Gaussian diffusion process, as theBlack-Scholes model, the volatility is assumed to follow a square root diffusion process, more popularly known as the Cox-Ingersoll-Ross (CIR) process. Thus, the

probability distribution of the asset price was Gaussian (Log-normal) but that of thevolatility was not.

Volatility, which varies stochastically, is also mean reverting;

And above all, the stochastic processes for the asset and the volatility are correlated.This is where there was a paradigm shift in the world view. For, there was no parallelof such a process in physics. Imagine, Einstein thinking about a diffusion process of amolecule which follows a random walk in a “medium” which is itself vibrating in arandom manner.

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 16/135

16

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Since volatility was not a tradable asset – by which we mean, an explicitly tangibletradable asset – a random volatility would give rise to a situation where a riskless portfolio cannot be constructed to replicate the option price; hence we would end up ina state where markets would no longer be complete.

And the PDE for the option got far more complex. Fortunately, Heston’s model generated a closed form solution – a formula, if you will

– with which option prices could be calculated.

And last but certainly not the least, Heston, during the course of his work on stochasticvolatility, introduced the use of Fourier transform into the quant finance domain (thistechnique would be later utilized to solve various option pricing problem extensively by many quants, most notably Peter Carr).

However, ironically, even though Heston introduced a revolutionary way of visualizingvolatility and the option pricing problem and, advertently or inadvertently, made a decisive break with physics-like models of quant finance, much of the Heston era was dominated by

the other type of volatility models, i.e. the volatility surface and local volatility. It was onlyfrom 2003 onwards that banks started using Heston’s model extensively and quants andtraders started recognizing the utility of this model.

In fact, to be precise, both concepts of “volatility surface” and “local volatility” do not meritthe addition of the word “model” after them. Vol surface and Local Vol are not reallymodels. They are just another way of looking at stochastic volatility.

Anyway, as things stand today Heston’s stochastic volatility model has become a veryimportant and essential tool in the repertoire of most quants and traders in the banks aroundthe world. This change has come about in the last 8 to 9 years.

Volatility Surface

As noted that with the demise of the Black-Scholes world view after the crash of 1987,investors and option traders discovered the volatility smile.

It was observed in the market that implied volatility of options varied across strike prices for a given maturity. From 1987 onwards, it was observed that at least forequity index options, almost always, implied volatilities increase with decreasingstrike – that is, out-of-the-money puts trade at higher implied volatilities than out-of-the-money calls. This feature is often referred to as a “negative” skew, where

skew is just another characterization of smile. It was observed that there is a term structure of volatility, i.e. implied volatility

varied across different maturities; another key observation was that long-termimplied volatilities exceed short-term implied volatilities

From this, the notion of volatility surface was born. This was a surface – a twodimensional matrix – where implied volatility was plotted against strike pricesand time to maturity. From this surface, implied volatility of any arbitrary optioncan be interpolated.

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 17/135

17

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Local Volatility in a Stochastic Volatility world

In 1994, Emanuel Derman, Iraz Kani and Bruno Dupire noted that under the condition of riskneutrality there is a unique diffusion process that is consistent with the distribution of market

prices of the European options. Derman and Kani, then at Goldman Sachs, presented thisargument using a discrete time binomial tree whereas, Dupire, working separately, presentedthe continuous time version of the same argument. Their work was based on the earlier workof Breeden and Litzenberger done in 1978.

The import of their arguments was a simple modification in the way we looked at volatility.Rather than thinking of volatility as a constant coefficient of a diffusion process, as given bythe Black-Scholes model, they assumed that volatility was now a state dependent function

expressed as: t S L , , where, the subscript L stood for the word local. The volatility

was now a function of S , the asset price and time, t . This shift in the way how volatility wasdefined by Dupire, Derman and Kani (DDK), based on what was observed in the market as

well as that of theoretical foundations of Breeden and Litzenberger’s work, presented acomplexity. How exactly can we define “local volatility”? This is a question that many seniorquants and traders in banks will have difficulty answering.

Jim Gatheral has presented a unique interpretation of this concept in his book Volatility andCorrelation. He doubts if the proponents of DDK local volatility model visualized this as amodel of evolution of volatility. In fact, he doesn’t believe that “local volatility” should forma separate class of models. Gatheral’s interpretation is that “local volatility” can be thoughtof as an average of all possible instantaneous volatilities in a stochastic volatility world .Gatheral has actually demonstrated this notion, using sophisticated mathematics, in his book.

As David de Rosa (64) points out it is important to note that even though local volatility is afunction of a stochastic variable, i.e. the asset price, in itself it is not stochastic. Thisdistinction is important to capture the essence of local volatility. Local volatility isn’t somemeasure of stochastic volatility, rather, given the existence of vanilla option prices in themarket it is a process through which quants make some simplifying assumptions to priceexotic options that are consistent with the prices of the vanilla options traded in the market.

Post Heston (2007 – Present)

One can say that the post-Heston era started with the financial crisis of 2007-2008. Duringthe ensuing market turmoil the stochastic volatility models more or less broke down. This is a

period that witnessed big spikes in volatility in many FX options market, such as the Dollar-Yen market, it caused serious problems for traders. What was really troubling, and perhaps bewildering at the same time, was the observation that somehow volatility has acquired a lifeof its own independent of that of the underlying asset. Is such a thing possible? Is it possiblefor volatility to have the freedom to rise or fall on its own accord without any change in theunderlying asset, say, the FX rate?

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 18/135

18

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Enter a new class of models known as the Stochastic Local Volatility (SLV) models. Themost important development came with the publication of a stochastic local volatility model by Ren, Madan, and Qian in 2007. As we shall see later on in these notes, this modelincorporated an independent stochastic component in the volatility process that would change

the dynamics of the process significantly. Grigore Tataru and Travis Fisher at Bloombergalso developed an SLV model in 2010 for pricing barrier options. Tataru and Fisher make akey observation in their paper, which perhaps explains the motivation for the development ofSLV models and what we have argued in the above paragraph. The authors note that pricesof barrier and path dependent options mostly depend on the dynamics of the market. Vanillaoption prices don’t matter that much for their pricing. What is important is how the market behaves and, in particular, how volatility rises and falls with the arrival of information and passage of time. SLV models try to matching this extra market dimension to obtain goodexotic option prices.

Volatility as a Financial Asset

Right from the onset in early 1970s when option trading began on the Chicago Board,investors bought or sold options for its value which was captured, mainly, by the volatility ofthe underlying asset. Therefore, implicitly at least, investors were buying and sellingvolatility via options. But this trade was an imperfect trade in volatility. Volatility in itselfwas not a tradable asset. Still, traders and sophisticated investors used various optionstrategies to create as perfect a trade as possible to trade only the volatility of the asset.

During the Heston era two fundamental developments happened that would transformvolatility into a “nearly tangible” asset. The first was the development of variance swaps (andvolatility swaps). In 1994, Anthony Neuberger introduced the Log contract. A keymathematical ingredient in the variance swap pricing mechanism was this Log contract.Variance swaps were developed mainly by Derman and his colleagues at Goldman Sachs,though many others, like Jim Gatheral, contributed to the understanding and development ofthe pricing of this product, and other related products such as volatility swaps. Varianceswap was first instrument in the history of quant finance which allowed investors to trade“pure” volatility, as if it were an asset.

The second development was the creation of the new VIX index by the Chicago BoardOptions Exchange (CBOE) in 2003. The construction of this volatility index would not have been possible without the introduction of the variance swaps. Through this new VIX indexvolatility became an exchange traded commodity and options on this VIX index have now been developed.

From being just the standard deviation of asset returns to becoming an exchanged tradedasset is the story of volatility; which, as I said before, is pretty much the story of quantitativefinance. From the University of Chicago in 1952, when Harry Markowitz had to defend hisnovel concept of risk to Milton Friedman, to the Chicago Board Options Exchange in 2003,when the new VIX was introduced, is a very short distance. But it’s been a long andfascinating journey in time.

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 19/135

19

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Chapter M Applied Mathematics and

Numerical Methods in Finance

Part A

Matrices & Applications

Fun with Matrices

From Quantum Mechanics to Quantitative Finance - I

Matrices are extremely important in the study of Quantitative Finance and they areubiquitous. While studying quant finance we come across Volatility matrix, correlation

matrix, Variance-covariance matrix, etc. Just like quantum mechanics in physics, the study ofquantitative finance would not be possible without matrices. Matrices can be easily handledand understood and most of the time they are fun to deal with. So what are matrices?

We all know what a matrix is. A 2 x 2 matrix is an arrangement of rows and columns, or inother words, arrays. A typical 2 x 2 matrix looks like:

20

11 A

The above matrix has 2 rows and 2 columns and hence its dimension is 2 x 2. A typical 3 x 3matrix will look like:

631

435.0

001

B

The above matrix has 3 rows and 3 columns and hence its dimension is 3 x 3. Matrices canalso have imaginary numbers as its components. For example, a 2 x 2 matrix can look like:

00i

i

In the above is a 2 x 2 matrix i is an imaginary number that appears on the second cell of the

first column and the first cell of the second column. The value of i is 1i . The matrix is

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 20/135

20

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

designated as , which is called the “sigma” (in capital) in Greek. The above matrix forms part of something very important in quantum mechanics in physics and is known as one ofthe Pauli matrices. The above matrices are all square matrices. Why “square”? That is because the number of rows is equal to the number of columns. A 2 x 2, 3 x 3, 8 x 8 or an N

x N matrix are all examples of square matrices. In quantitative finance we only deal withsquare matrices.

Of course, non-square matrices do exist and they do have applications in other fields ofstudy, such as Cryptography. But we shall not talk about them here.

The cool thing about matrices – and from now on we only mean “square” matrices – is thatthey don’t commute. What does that mean? Take the numbers 3 and 8. Multiply 3 by 8 andyou’ll get 24. If instead, you multiply 8 by 3 you’d still get 24. It does not matter whether wemultiply 3 by 8 or 8 by 3. The result is the same 24.

248338

In algebra, if we measure a quantity by x and another by y then:

0 yx xy yx xy

If you take y time x and then subtract that quantity from x times y then result would be

zero. Any junior school student would tell you that.

However, this does not happen in the case of matrices. If a quantity is measured by say, a 2 x2 matrix (such as a correlation matrix for a two asset portfolio or for any two random

variables), P and another quantity is measured by another 2 x 2 matrix, Q then:

0 QP PQ .

Take any arbitrary square matrices, P and Q .

If

04

13 P and

80

01Q then if you multiply P with Q , you’d get

04

83 PQ .

Now, if you multiply Q with P , you’d get:

032

13QP . Therefore, the value of the

quantity given by PQ is different from the value of the quantity given by QP . How is this

possible? School algebra tell us that x times y is always equal to y times x . Yes, but that is

what we call commutative algebra. Matrices form, what we call, non-commutative algebra.

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 21/135

21

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

It may seem trivial to many of you but this simple, non-commutative property of matrices,

i.e. the fact that 0 QP PQ gave physicists the first glimpse into the world of Quantum

Mechanics.

Fun with MatricesFrom Quantum Mechanics to Quantitative Finance - II

There is a beautiful book – perhaps, one of the best in its field – titled Quantum Mechanics in

Simple Matrix Form by Thomas F. Jordan. This article is inspired from that book.

Let us consider three special matrices:

01

101

,

0

02

i

i ,

10

013

These matrices are known as Pauli matrices in quantum mechanics and form one of the building blocks of that discipline in physics. But why do we need to know about them? Wedon’t really have to know about them, except that if we combine the Pauli matrices with an

Identity matrix, I , where

10

01 I , then we can express any arbitrary 2 x 2 matrix using

them. In that sense, we can say that Pauli matrices are the fundamental building blocks of all2 x 2 matrices in the universe.

Let’s take an arbitrary 2 x 2 matrix, A, where A is given by:

2221

1211

aa

aa A . Now take four

complex numbers, 0 z , 1 z , 2 z and 3 z . In fact, these complex numbers can be thought to be

some sort of unique complex numbers associated with every 2 x 2 matrix.

Now, given the Pauli matrices above and the Identity matrix, I we can write the matrix, A,as:

3021

2130

2221

1211

3210

2221

1211

3322110

10

01

0

0

01

10

10

01

z z iz z

iz z z z

aa

aa

z i

i z z z

aa

aa

z z z I z A

Therefore, we can express the unique complex numbers as:

221131221212211221102

1,

2

1,

2

1,

2

1aa z aai z aa z aa z

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 22/135

22

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

As an example, take a 2 x 2 correlation matrix, M . This could be the correlation between thereturns of two stock indices. Say, one stock index is 70% correlated with the other. Then, M can be expressed as:

17.0

7.01 M

Therefore, we can now express this 2 x 2 correlation matrix in terms of the unique complexnumbers associated with it:

10 z 7.01 z , 02 z , 03 z

Every correlation matrix can be decomposed into its unique complex numbers derived fromPauli matrices.

Types of Matrices and their Applications

1. Square Matrix

In a square matrix the number of rows is equal to the number of columns. It is generally

nn mn written as matrix, where, . A matrix is a square matrix with 3 rows and 3

columns. All matrices used in financial engineering and quantitative finance are square

33 matrices. An example of a matrix would be:

320

841

102

P

An example of a square matrix in finance is the correlation matrix of asset returns. Acovariance matrix of asset returns is also an example of a square matrix.

2. Identity Matrix

I An Identity Matrix, denoted by, , has one on its diagonal and zeros in the off-diagonals.

33 It is the equivalent of number 0 in number theory. An example of a identity matrix

is:

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 23/135

23

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

100

010

001

I

3. Diagonal Matrix

A diagonal matrix is one whose diagonals have non-zero values and the off-diagonalshave zeros. An identity matrix is a special case of a diagonal matrix. An example of a

33 diagonal matrix is:

200

060

003

D

Say, we have a three asset portfolio (1, 2, 3) with asset (return) volatilities of 15%, 10%and 12%. Then, we can write the volatilities as a diagonal matrix:

12.000

010.00

0015.0

V

4. Triangular Matrices

A triangular matrix is one where all elements above or below the diagonal are zeros. If allelements above the diagonal are zero then the matrix is known as lower triangular matrixwhereas if all elements below the diagonal are zero then the matrix is known as upper

33 triangular. Examples of lower and upper triangular matrices are:

Lower Triangular

829

011

002

L

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 24/135

24

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Upper Triangular

400

530681

U

5. Symmetric Matrix: Correlation & Variance-Covariance Matrices

A symmetric matrix is one where all elements above the diagonal are mirror images of

nn Athe elements below the diagonal. In other words, for any symmetric matrix, , theT Atranspose of the matrix, , is the matrix itself. The following relationship holds:

A AT

A transpose operation flips the rows of any matrix into columns and columns into rows.

33 Consider a correlation matrix of asset returns, which is a symmetric matrix:

125.055.0

25.0165.0

55.065.01

M

M All elements of below the diagonal are mirror images of the elements below thediagonal. That is obvious in the case of asset correlation matrix. The correlation of asset 1with that of asset 2 is the same as the correlation of the return of asset 2 with that of asset

12 21 1. If is the correlation of asset 1 with asset 2 then is the correlation of asset 2

2112 with asset 1 such that .

M The transpose of the asset correlation matrix, , above is given by:

M M T

125.055.0

25.0165.0

55.065.01

If we have three assets (1, 2, 3) in a portfolio then the symmetric, 33 asset correlation

matrix is given by:

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 25/135

25

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

1

1

1

3231

2321

1312

M

If the volatilities of the three assets (1, 2, 3) are given by 1 , 2 and 3 respectively

then the symmetric, 33 asset covariance matrix is given by:

2

332233113

2332

2

22112

13311221

2

1

6. Volatility, Correlation and Variance-Covariance (VCV) Matrix of a Portfolio(Three Asset Case)

1 2 3 Given three assets (1, 2 and 3) with volatilities of , and respectively. Then the

volatility matrix can be expressed as a diagonal matrix:

3

2

1

00

00

00

V

M Given a correlation matrix of these three assets as , where,

1

1

1

3231

2321

1312

M

M jiij Where, in the matrix , we have . Then the Variance-Covariance matrix of the

three asset portfolio would be given by:

MV V T

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 26/135

26

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

2

323321331

2332

2

21221

13311221

2

1

3

2

1

3231

2321

1312

3

2

1

00

00

00

1

1

1

00

00

00

7. Transpose of a Matrix

As explained above a transpose operation flips the rows of any matrix into columns and

33 columns into rows. Consider the following matrix.

2.030

5.021

041

B

BThe transpose of would be given by

2.05.00

324

011T B

In Excel™, the formula for Transpose is given by =TRANSPOSE(.).

8. Determinant of a Matrix

Determinant symbolizes the area or the volume enclosed by the row vectors of anymatrix. It is a scalar quantity (a single number). Determinants exist only for square

22 matrices. Consider a matrix below:

31

12C

C C C detThe determinant of this matrix, , denoted by or is given by:

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 27/135

27

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

7)1(13231

12

C

33 For a matrix the determinant is calculated as:

251

203

121

E

E The determinant of would be given by:

9

15182101

51

03

)1(21

23

225

20

1

E

Why are determinants important?

(i) They are essential for calculating the inverse of a matrix. In fact, a determinant tellsus if a matrix can be inverted or not.

(ii) They are related to the eigenvalues and eigenvectors of a symmetric matrix(iii) They measure the area or the volume of shape defined by the row vectors of a

matrix.

Why the Determinant of a VCV or a Correlation Matrix should be Positive?

Interpretation #1

Let’s look at a simple 2 x 2 correlation matrix. The geometrical interpretation ofdeterminant is that – in a 2 x 2 framework (2 x 2 matrix) – it measures the area that isspanned by the two column vectors of the 2 x 2 correlation matrix. If both the vectorsare aligned, which means one of the vectors is linearly dependent on the other, then thedeterminant is zero. The value of the determinant becomes maximum when the angle between the vectors is 90 degrees which is equivalent to the area under a rectangleformed by the two vectors. If the determinant is a measure of the area then how can thearea of a surface outlined by two vectors be negative? Therefore, a negative determinant,though possible for any arbitrary square matrix, is geometrically incomprehensible for asymmetric, correlation or covariance matrix.

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 28/135

28

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Interpretation #2

The determinant of a VCV matrix is a measure of “generalized variance”, which is inessence a measure of the spread of the observations in the data set. The determinant for

a 2 x 2 VCV measures the overall information in the matrix, i.e. the total variance ofeach variable less whatever correlation (covariance) there is between the variables.Here again, a negative generalized variance cannot be defined and therefore, if thevalue of the determinant of a VCV (or correlation) matrix is negative then we are in therealm of the nonsense. And a zero variance will only apply to constants, i.e. no spreadin the observations in the data set. Therefore, zero variance is meaningless because thiswould mean all observations in the data set are same.

Determinants and Eigenvalues of a Matrix( For more on eigenvalues and eigenvectors see Chapter S, Part B)

For a symmetric variance-covariance (VCV) or Correlation matrix, the determinant of the Amatrix is equal to the product of the eigenvalues of the matrix. If is a square,

mn n m mn Asymmetric matrix with dimension ( rows and columns, with ), is the

A ....,,, 321 n Adeterminant of and are eigenvalues of then the following

relationship holds:

n A ......321

Since calculation of the determinant is much easier (and faster) than the estimation ofeigenvalues of a matrix, as a rule of thumb, a quant should always check first if the

determinant of a VCV or a correlation matrix of asset returns is positive. If it is, then thechances are good that all eigenvalues of the matrix are positive – though not necessarilyso – and hence there is a good chance that the matrix would be “valid” and not“nonsensical” (i.e. the matrix would be positive semi-definite). Of course, even with a positive determinant, a correlation matrix can be nonsensical if 2 or 4 or other evennumber of eigenvalues is negative.

In Excel™, the formula for the determinant of a matrix is given by =MDETERM(.).

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 29/135

29

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

9. Inverse of a Matrix

A 1 A A 1 AThe inverse of a matrix, , is defined as where, multiplied by is equal to the

I I AA 1identity matrix, . Mathematically, we can write, .The inverse of a matrix is

calculated as:

A

Aadj A 1

If the determinant of a matrix is zero then the inverse of the matrix will not exist. We saythat the matrix is non-invertible. Such matrices are known as Singular matrices.

In Excel™, the formula for the inverse of a matrix is given by =MINVERSE(.).

10. Matrix Multiplication

Two matrices can be multiplied to produce a third matrix. However, two matrices canonly be multiplied if the column of the first matrix is equal to the row of the secondmatrix. The dimension of the third matrix, which is the product of the first and the secondmatrix, would be the rows of the first matrix and the columns of the second matrix.

22 A BIf we have two matrices, and given as follows

2221

1211

2221

1211

bb

bb B

aa

aa A

B A Then the product of the two matrices, is given by

2222122121222121

2212121121121111

2221

1211

2221

1211

babababa

babababa

bb

bb

aa

aa B AC

Say, we have a three asset portfolio (1, 2, 3) with asset (return) volatilities of 10%, 15%

33 and 12% respectively and expressed as a diagonal matrix as:

12.000

015.00

0010.0

V

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 30/135

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 31/135

31

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Then, the Trading Covariance matrix in Dollars per share is given by the followingmatrix multiplication:

m

T

m

mn

m

m

mm

T

p

p

p

p

p

p

P M P

00

00

00

00

00

00

1

1

1

00

00

00

00

00

00

2

1

2

1

21

221

112

2

1

2

1

12. Power of a Matrix

One of the problems of matrices is that they cannot be raised to non-integer powers. Wecan raise a square matrix to a power of 2, 3, 4….. but we cannot raise a matrix to the power of 0.5 (half) or 0.75. Thus we cannot find the square root of a matrix. Consider the

33 following matrix:

651

113

012

X

If we want to find the square of the matrix we simply multiply the matrix with itself(same as raising the matrix to the power of 2).

313623

718

137

651

113

012

651

113

0122 S S S

S 3 2S S Similarly we can raise the matrix to the power of by multiplying with ; and so

S on for higher powers of

S However, if we want to raise the matrix, , to the power of half (0.5), i.e. if we want to

S S find the square root of the matrix , we cannot do it. Square roots of the matrix, exists but they are very different from the notion of a square root that we have from number

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 32/135

32

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

theory. In fact, a square matrix can have numerous square roots, something that we don’t

3 3see in number theory. The number, has a unique square root given by, .

13. Eigenvalues and Eigenvectors of a Matrix

Let A be an nn square matrix. There exists a number that is said to be the

eigenvalue of A if there exists a non-zero solution vector, W to the linear system ofequations:

W AW

The solution vector, W , is said to the eigenvector of A corresponding to the particular

eigenvalue, .

To solve for we set up the characteristic equation as follows:

00

0

I AW I A

W AW

Where, I A represents the determinant of I A . This characteristic equation

yields a closed form real or complex solution for the eigenvalues, . The eigenvalues, will be the solution of the polynomial (quadratic, cubic, etc.) equation generated by the

characteristic equation above. If A is a 22 matrix then there would be 2 values of , (

1 and 2 ). If A is a 33 matrix then there would be 3 values of , ( 1 , 2 and 3 )

and so on. Eigenvalues are scalar quantities and are simply real or complex numbers.

Once the eigenvalues of the matrix, A are determined then the eigenvectors, W aredetermined. Except for very rare instances, closed form solutions do not exist for

eigenvectors and the eigenvectors, W , corresponding to each eigenvalue is estimatediteratively using numerical algorithms.

If A is an nn square matrix (i.e. n rows and n columns) then there would be n

eigenvectors and W would be expressed as an nn square matrix. If A is 22 then

even W would be 22 in dimension and if A is 33 then even W would be 33 in

dimension. The matrix A and W have the same dimensions.

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 33/135

33

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

For any arbitrary square matrix, A given by:

nnnn

n

n

aaa

aaa

aaa

A

21

22221

11211

We have the corresponding eigenvalues are n ,....,, 21 and the matrix of

eigenvectors W is given as:

nnnn

n

n

www

www

www

W

21

22221

11211

Here,

nw

w

w

W

1

12

11

1

is the eigenvector corresponding to the eigenvalue 1 ,

2

22

12

2

nw

w

w

W

is

the eigenvector corresponding to the eigenvalue 2 and so on.

14. Square Root of a Matrix

K A square matrix can have many square roots. A matrix is said to be the square root of

M M M K 22 a matrix, , if the product equals to . For example, consider a matrix B

as given by

3721

2816 B

This matrix has many square roots. One of the square roots of this matrix is a matrix given

53

42 R B R R by because, .

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 34/135

34

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

15. Methods of Finding the Square Root of a Matrix( Please see the Eigenvalues and Eigenvectors of a Matrix to understand this part fully)

th N There are many methods for finding the square root or the root of a square matrix.One of the most common and robust ways of finding the square root of a matrix is via thediagonalization method using the eigenvalues and the eigenvectors of the matrix.

X jk W If is a square matrix of dimension given by and is the matrix of the

X jk eigenvectors of with the same dimension of and is a diagonal matrix of the

X X eigenvalues of then can be decomposed as:

1 W W X

th N X Then, the root of the matrix is given by:

1

1

ˆ W W X N

th N Where, is a diagonal matrix with the diagonal elements being the root of the

k .......,,, 21 33 individual eigenvalues, . For a matrix we get the following.

33 X

333231

232221

131211

x x x

x x x

x x x

X If we have a matrix, , given by:

W And if the matrix of eigenvectors, , and the diagonal matrix of the eigenvalues, , aregiven by:

333231

232221

131211

www

www

www

W

3

2

1

00

00

00

and

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 35/135

35

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

16. Cholesky Matrix

(See Part B, Chapter S for more on Cholesky matrix)

Cholesky is a lower triangular matrix that is obtained using the following

M nn Atransformation. If is a correlation or a variance-covariance matrix and isthe Cholesky matrix of same dimension then the Cholesky matrix is obtained by:

M AAT

The Cholesky is an important matrix in quantitative finance. A correlation matrix (or avariance-covariance matrix) of asset returns is valid, i.e. workable and usable, if andonly if the Cholesky of that matrix exists. This is related to the condition of positivesemi-definiteness. A correlation matrix is positive semi-definite if all its eigenvaluesare positive and the Cholesky of that matrix exists. If the Cholesky of a correlationmatrix does not exist then the correlation matrix is commonly known as “nonsensical”.

17. Solution of a System of Linear Equations using Matrices

Matrices can be used to solve a system of linear equations. Consider the followingsystem of three linear equations:

22

1

03

z y x

z y x

z y x

Using matrices, we can write the above as:

2

1

0

211

111

113

z

y

x

B AX The above can be written as: where,

21

0

211111

113

B z y

x

X A

The solution can be obtained using matrix multiplication and using the concept of the

B A X B AX 1inverse of a matrix:

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 36/135

36

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

8.0

1.0

3.0

2

1

0

211

111

113 1

z

y

x

X

3.0 x 1.0 y 8.0 z Thus, , and

Applications of Matrices in Quantitative Finance

I. Hedging an Option Portfolio

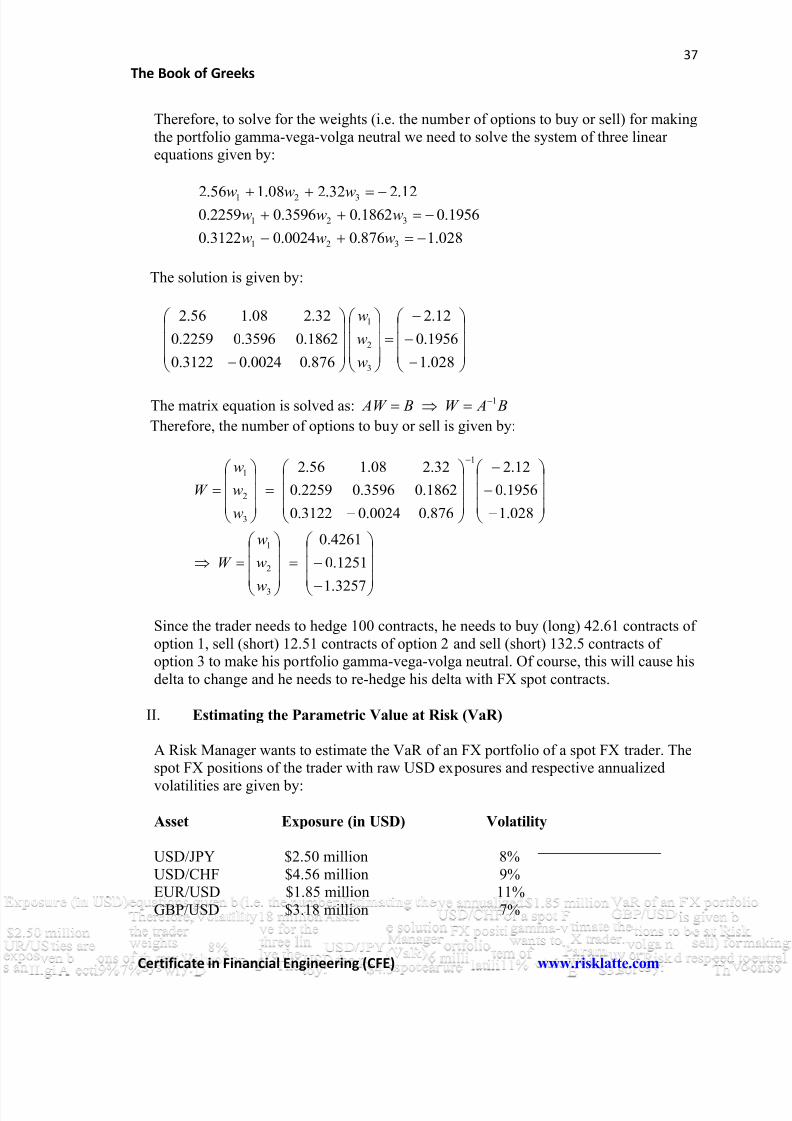

An FX options trader wants to hedge a short position of 100 contracts in an OTC FXoption position that he is running that has a Gamma of 2.12, Vega of 0.1956 and a Volga

of 1.028 such that his overall portfolio (original position plus the hedge) is gamma-vega-volga neutral. He identifies three traded options in the market with the following greeks:

Option 1 Option 2 Option 3

Gamma 2.56 1.08 2.32

Vega 0.2259 0.3596 0.1862

Volga 0.3122 -0.0024 0.876

How many of each of these three traded options should he buy or sell to make his portfolio gamma-vega-volga neutral?

For gamma neutrality the equation would be:

12.232.208.156.2 321 www

For vega neutrality the equation would be:

1956.01862.03596.02259.0 321 www

For volga neutrality the equation would be:

028.1876.00024.03122.0 321 www

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 37/135

37

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Therefore, to solve for the weights (i.e. the number of options to buy or sell) for makingthe portfolio gamma-vega-volga neutral we need to solve the system of three linearequations given by:

12.232.208.156.2 321 www 1956.01862.03596.02259.0 321 www

028.1876.00024.03122.0 321 www

The solution is given by:

028.1

1956.0

12.2

876.00024.03122.0

1862.03596.02259.0

32.208.156.2

3

2

1

w

w

w

The matrix equation is solved as: B AW B AW 1

Therefore, the number of options to buy or sell is given by:

3257.1

1251.0

4261.0

028.1

1956.0

12.2

876.00024.03122.0

1862.03596.02259.0

32.208.156.2

3

2

1

1

3

2

1

w

w

w

W

w

w

w

W

Since the trader needs to hedge 100 contracts, he needs to buy (long) 42.61 contracts ofoption 1, sell (short) 12.51 contracts of option 2 and sell (short) 132.5 contracts ofoption 3 to make his portfolio gamma-vega-volga neutral. Of course, this will cause hisdelta to change and he needs to re-hedge his delta with FX spot contracts.

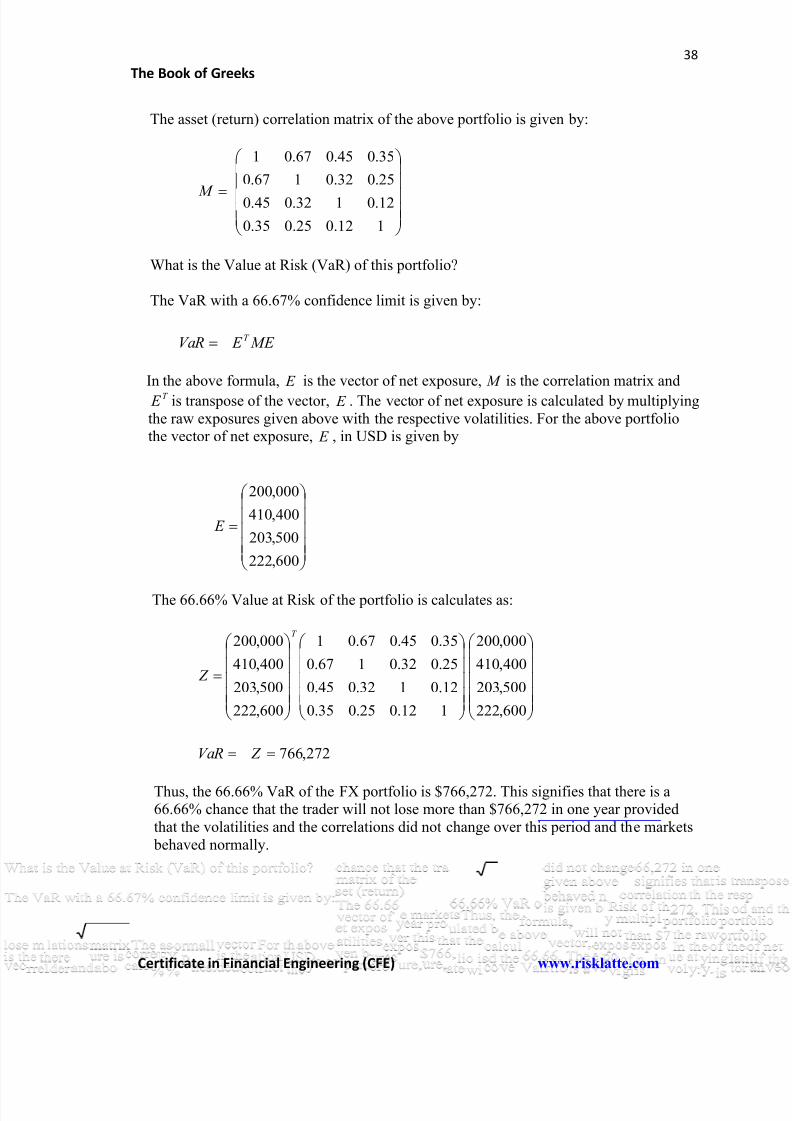

II. Estimating the Parametric Value at Risk (VaR)

A Risk Manager wants to estimate the VaR of an FX portfolio of a spot FX trader. Thespot FX positions of the trader with raw USD exposures and respective annualized

volatilities are given by:

Asset Exposure (in USD) Volatility

USD/JPY $2.50 million 8%USD/CHF $4.56 million 9%EUR/USD $1.85 million 11%GBP/USD $3.18 million 7%

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 38/135

38

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

The asset (return) correlation matrix of the above portfolio is given by:

112.025.035.0

12.0132.045.0

25.032.0167.0

35.045.067.01

M

What is the Value at Risk (VaR) of this portfolio?

The VaR with a 66.67% confidence limit is given by:

ME E VaR T

E M In the above formula, is the vector of net exposure, is the correlation matrix andT E E is transpose of the vector, . The vector of net exposure is calculated by multiplying

the raw exposures given above with the respective volatilities. For the above portfolio E the vector of net exposure, , in USD is given by

600,222

500,203

400,410

000,200

E

The 66.66% Value at Risk of the portfolio is calculates as:

600,222

500,203

400,410

000,200

112.025.035.0

12.0132.045.0

25.032.0167.0

35.045.067.01

600,222

500,203

400,410

000,200 T

Z

272,766 Z VaR

Thus, the 66.66% VaR of the FX portfolio is $766,272. This signifies that there is a66.66% chance that the trader will not lose more than $766,272 in one year providedthat the volatilities and the correlations did not change over this period and the markets behaved normally.

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 39/135

39

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

III. Portfolio Optimization: Strategic Asset Allocation Problems

Linear equations also appear in portfolio optimization problems (mean-variance

optimization) that appear in strategic asset allocation models used by fund managers toallocate funds between various asset classes and individual securities within assetclasses.

See Chapter P for more details on this.

IV. Applications in Algorithmic Trading (Minimization of MCR)

Matrices are also used to solve complex mathematical algorithms used by algorithmicand high frequency traders to buy and sell stocks and other assets. A particular exampleis the minimization of the Marginal Contribution of Risk (MCR) to determine the

number of stocks to buy and/or sell in a trade list.

See Chapter P for more details on this.

V. Estimating the Variance-Covariance (VCV) Matrix from Market Data

Quantitative equity analysts, fund managers and risk managers in bank need to have thevariance covariance (VCV) matrix of asset returns almost on a real time basis. How dowe estimate the VCV matrix from market data of stock (asset) prices?

The best, and the easiest way, to extract the VCV matrix from the market data is toestimate it via excess return. From a time series of stock price data we can calculate themean return of the stock and hence determine the excess return for a particular period,

i.e. the return of a particular period less the mean return. Let’s say that we have K riskyassets (stocks or stock indices, etc.) and for each of these assets we have price data

(which we can easily obtain in real time from Bloomberg) for N periods (say, 12months, 52 weeks or 5 years, etc.)

Then, here’s the algorithm for obtaining the VCV matrix of the portfolio of K assets:

1. Estimate the return on each of these assets over N periods; ideally, all percentage asset returns should be annualized

2. Calculate the mean return for each of the assets (stocks);

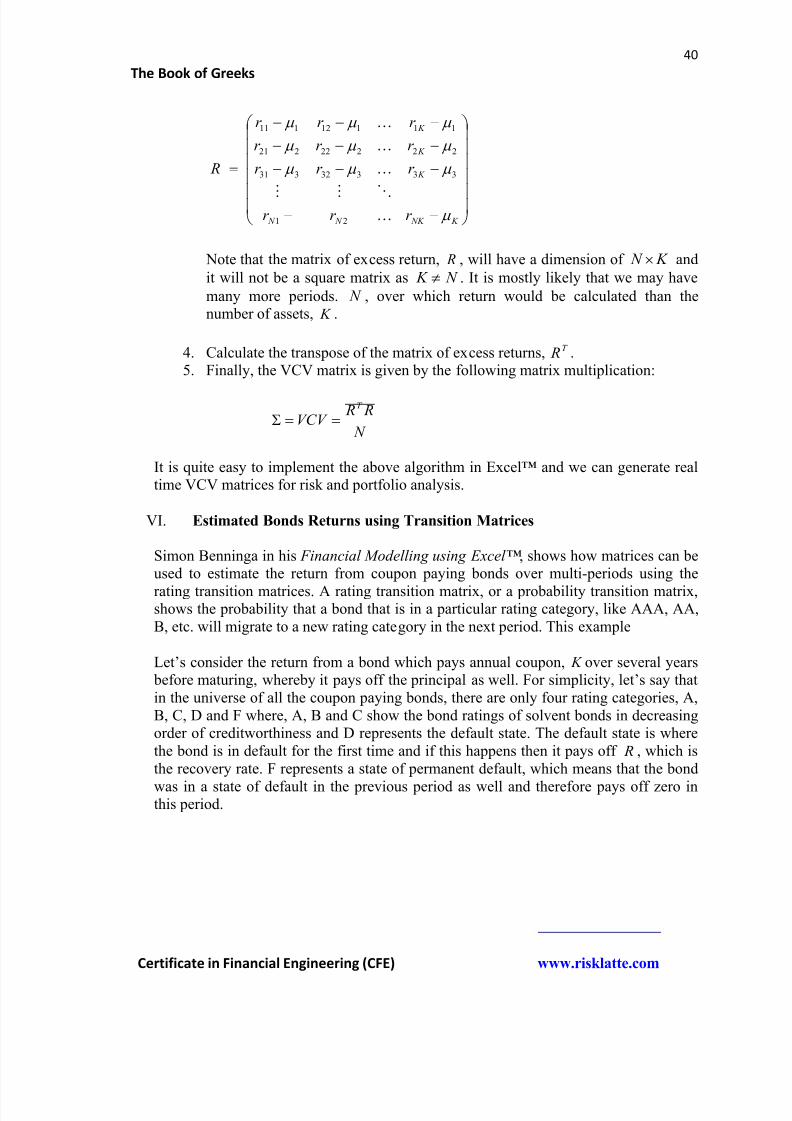

3. Estimate the excess return matrix; the matrix of excess returns, Rˆ is given by:

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 40/135

40

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

K NK N N

K

K

K

r r r

r r r

r r r

r r r

R

21

33332331

22222221

11112111

ˆ

Note that the matrix of excess return, R , will have a dimension of K N and

it will not be a square matrix as N K . It is mostly likely that we may have

many more periods. N , over which return would be calculated than thenumber of assets, K .

4. Calculate the transpose of the matrix of excess returns, T Rˆ .5. Finally, the VCV matrix is given by the following matrix multiplication:

N

R RVCV

T ˆˆ

It is quite easy to implement the above algorithm in Excel™ and we can generate realtime VCV matrices for risk and portfolio analysis.

VI. Estimated Bonds Returns using Transition Matrices

Simon Benninga in his Financial Modelling using Excel™ , shows how matrices can beused to estimate the return from coupon paying bonds over multi-periods using the

rating transition matrices. A rating transition matrix, or a probability transition matrix,shows the probability that a bond that is in a particular rating category, like AAA, AA,B, etc. will migrate to a new rating category in the next period. This example

Let’s consider the return from a bond which pays annual coupon, K over several years before maturing, whereby it pays off the principal as well. For simplicity, let’s say thatin the universe of all the coupon paying bonds, there are only four rating categories, A,B, C, D and F where, A, B and C show the bond ratings of solvent bonds in decreasingorder of creditworthiness and D represents the default state. The default state is wherethe bond is in default for the first time and if this happens then it pays off R , which isthe recovery rate. F represents a state of permanent default, which means that the bond

was in a state of default in the previous period as well and therefore pays off zero inthis period.

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 41/135

41

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

A sample transition matrix is given by:

10000

10000

0

0

0

CDCC CBCA

BD BC BB BA

AD AC AB AA

p p p p

p p p p

p p p p

Q

If the bond in consideration pays a coupon, K and if R denotes the recovery rate shouldthis bond default then the payoff vector (a column vector, in array notation) of the bond

at any time, t before maturity, T (where, T t ) and at maturity, T are given by

0

R

K

K

K

T t L and

0

1

1

1

R

K

K

K

T t L

The state vector (a row vector) of the bond will be defined as the current rating state thatit is in. If A, B, C, D and F are arranged in the decreasing order in a row and if the bondin consideration is in rating category C then its state vector will be given by:

00100S

Whereas, if the bond is currently in the rating category A, then its state vector will begiven by:

00001S

Therefore, the expected payoff of the bond is given by the following row vector:

t L J S t L E t

In the above, S is the state vector (row) of dimension 1 5, t J is the transition matrix

raised to the power of t of dimension 5 5 and t L is the bond payoff vector (column)

of dimension 5 1. The dimension of t L E is 1 5.

The expected return of the bond can be found out by calculating the Internal Rate ofReturn (IRR) using the initial investment of $1 and the expected bond payoff vector

t L E .

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 42/135

42

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

VII. Fibonacci Numbers and the Golden Ratio – An Eigenvalue problem

Fibonacci Numbers and the Golden Ratio are used quite extensively by technical

analysts to predict stock and currency market moves. However, even though both theFibonacci numbers and the Golden Ratio are staple diet for technical analysts inanalyzing stock and currency charts, many would have trouble grasping the relationship between these two mathematical constructs.

What is the relationship between Fibonacci numbers and the Golden Ratio? As it turnsout Golden Ratio is one of the eigenvalues of a Fibonacci matrix.

A Fibonacci sequence of numbers is given by:

0, 1, 1, 2, 3, 5, 8, 13, 21, ………………

Where, each number, except for zero and one, is the sum of the previous two numbers.

In general they can be written as, with seed values, 00 f and 11 f :

21 k k k f f f

Golden Ratio is the irrational number 1.6180339……. It is generally denoted by the

Greek alphabet (psi) and is an extremely important ratio that is found in mathematics,

nature and the world of arts. Some mathematicians, represent it as:2

51 . And

interestingly, many Renaissance artists believed that the Golden Ratio was a “divine proportion”.

We can write a Fibonacci sequence (of two successive Fibonacci numbers) as a 2 x 1column vector such as:

k

k

k

k k

k

k

f

f

f

f f

f

f 1

1

1

1

2

01

11

As can be seen the above equation represents an eigenvalue problem where A is theFibonacci matrix.

01

11 A

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 43/135

43

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

It can be easily shown that one of the eigenvalues, 1 , of A is equal to the Golden

Ratio, 1.6180339…..

Setting up the characteristic equation as 0 I A where, is the eigenvalue of A

we get the quadratic equation:

012

Solving the above, we get:2

51 where:

......6180339.12

511

and .....6180339.0

2

512

Hence, one of the eigenvalues of A, 1

is equal to the irrational number 1.6180339…which is the Golden Ratio.

A whole New Branch of Study

Random Matrices

From Nuclear Physics to Quantitative Finance - I

Matrices are arrays – an arrangement of rows and columns – of numbers. These numberscan be real or complex. For example, a 3 x 3 symmetric correlation matrix we have the pair

correlation between two variables. Say, if we have three financial assets, A, B and Carranged as A, B and C on both rows and columns, and their correlation matrix, M, is given by:

135.075.0

35.0165.0

75.065.01

M

In the above matrix, all elements are real numbers and each element represents thecorrelation between two variables. For example, 0.65 is the correlation between A and B

and 0.35 is the correlation between B and C. The matrix is symmetric because all elementsabove the diagonal are equal to all elements below the diagonal (which is how a correlationmatrix should be).

Now say a smart but a lazy quant in a bank wants to estimate the correlation matrix of thesethree financial assets. Rather than do historical analysis on the time series of the prices ofA, B and C or try to find out the correlation from the options market, he simply generates aset of uniform random numbers between 0 and 1 (using Excel spreadsheet or some other

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 44/135

8/12/2019 Book of Greeks

http://slidepdf.com/reader/full/book-of-greeks 45/135

45

The Book of Greeks

Certificate in Financial Engineering (CFE) www.risklatte.com

Ever since then random matrices and Random Matrix Theory have been applied to variousdisciplines including electrical engineering, quantum mechanics, sociology, econometricsand even quantitative finance.

Random MatricesFrom Nuclear Physics to Quantitative Finance - II

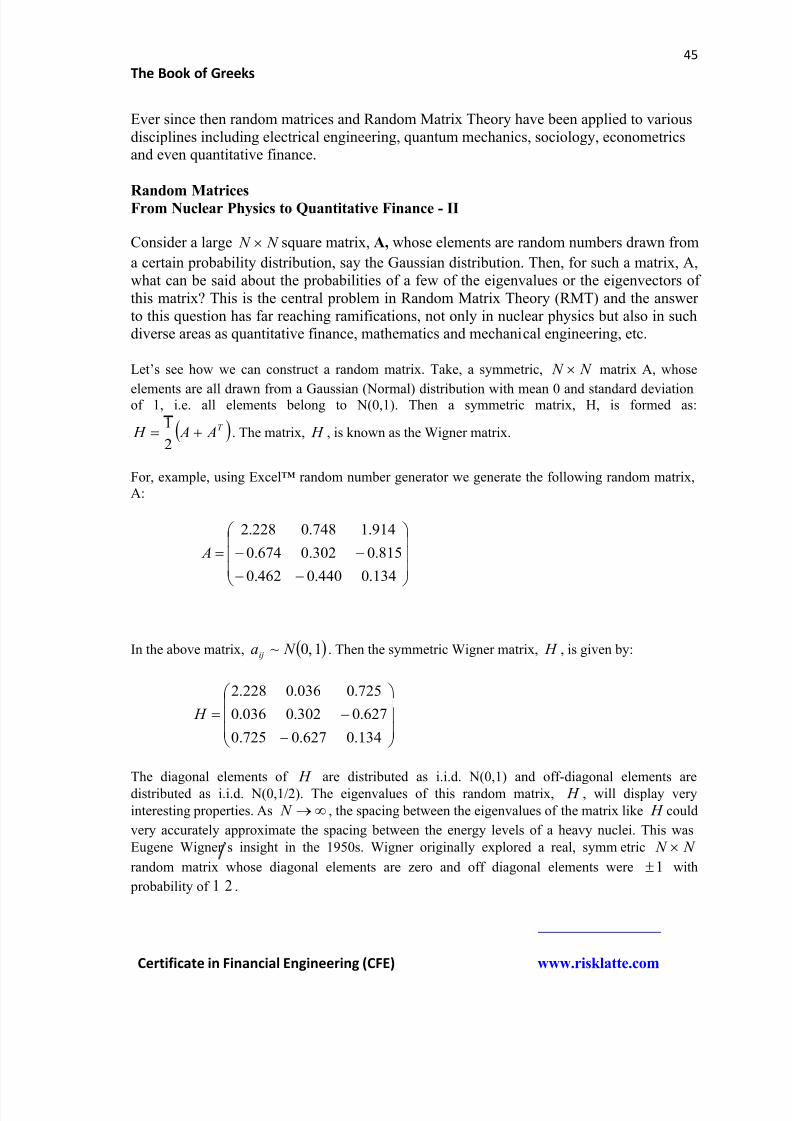

Consider a large N N square matrix, A, whose elements are random numbers drawn from

a certain probability distribution, say the Gaussian distribution. Then, for such a matrix, A,what can be said about the probabilities of a few of the eigenvalues or the eigenvectors ofthis matrix? This is the central problem in Random Matrix Theory (RMT) and the answerto this question has far reaching ramifications, not only in nuclear physics but also in suchdiverse areas as quantitative finance, mathematics and mechanical engineering, etc.

Let’s see how we can construct a random matrix. Take, a symmetric, N N matrix A, whose

elements are all drawn from a Gaussian (Normal) distribution with mean 0 and standard deviationof 1, i.e. all elements belong to N(0,1). Then a symmetric matrix, H, is formed as:

T A A H 2

1. The matrix, H , is known as the Wigner matrix.

For, example, using Excel™ random number generator we generate the following random matrix,A:

134.0440.0462.0

815.0302.0674.0

914.1748.0228.2

A

In the above matrix, 1,0~ N aij . Then the symmetric Wigner matrix, H , is given by:

134.0627.0725.0

627.0302.0036.0

725.0036.0228.2

H

The diagonal elements of H are distributed as i.i.d. N(0,1) and off-diagonal elements are