Bonds and Mutual Funds Savings Accounts and Credit Scores – The future of your savings!

49

Bonds and Mutual Funds Savings Accounts and Credit Scores – The future of your savings!

-

Upload

naomi-wood -

Category

Documents

-

view

218 -

download

0

Transcript of Bonds and Mutual Funds Savings Accounts and Credit Scores – The future of your savings!

Bonds and Mutual FundsBonds and Mutual FundsSavings Accounts and Credit Scores – The future of your savings!

What is a bond?

• A bond is an IOU to a government or to a corporation.

• When you loan your money to a corporation, government or a government agency the ISSUER promises to pay you back with INTEREST .

Bonds

• Issuers promise to pay you back a specific rate of interest called the COUPON RATE.

• You are usually paid interest then on a quarterly time rate for the life of the bond.

Life of the bond?

• The period of time the issuer has to pay back the investor.

• The issuer also promises to pay back the FACE VALUE of the bond when the bond MATURES.

Face Value

• ALSO called PAR VALUE or the PRINCIPAL.

Why invest in bonds?

• USUALLY doesn’t take much money to start.

• “Safer” investment– Tax-free and risk-free

return.• THAT IS THE CHEERY

PICTURE

Opportunity Costs of Bonds

• What happens if INFLATION goes higher than the value of your bond?– Interest on bond is 4%

but inflation goes to 6%.

• What happens if the rating on your bond goes south?

How do you know if a bond is a good one?

• Seek Investment Grade Bonds – Highest rated by

MOODY’S – a service that rates companies and government bonds.

– Investment Grade – least chance of missing interest payments

• Other good rating services for bonds include Fitch and Standard & Poor.

Grading Bonds

• AAA – PRIME BONDS.

• AA+ or AA or AA- or Aa1, Aa2 or Aa3 = HIGH GRADE BONDS.

• A+ to BBB- = UPPER GRADE TO MID GRADE BONDS

ANYTHING BB rated or below

•JUNK BONDS– These are high risk

bonds.• More chance of

DEFAULTING – not paying you back!

– Often called HIGH-YIELD offering higher interest rates at the same maturity of Investment Grade Bonds.

• Also sometimes called Subprime bonds.

4 Types of Bonds

• Corporate• Municipal• Agency• Government

Corporate Bonds

• Major source of corporate borrowing

• Debentures – most common type of bond, backed by the general credit of the corporation.

• Asset Based – backed by specific property or equipment of the corporation.

What are the best corporate bonds?

• According to Moody’s– AAA+ =

• ZERO!

– AAA = • JNJ• GE• PFE• MRK• UPS• XOM• ADP

WORST Corporate Bonds?

• Downgrades of investment-grade companies shot up by 153 percent from the year-ago quarter to a record 96, while downgrades of junk-rated companies surged by 147 percent to 287. – Moody's downgraded $1.76

trln U.S. corp debt in Q1– Wed Apr 1, 2009

• SBUX is now rated BB• BRK-A is now just AA

QOD: Why would someone say…

• “Provided the economy doesn't crash, junk bonds may be a great buy.”

Municipal Bonds

• Issued by states and local governments to raise money.

• General Obligation: Backed by full faith and credit of the issuer.– Revenue Bonds: Based

on income produced by a specific project.

• Kearney’s Archway• Lincoln’s proposed $250-

million arena / convention center.

Municipal Bonds

• Why would Moody’s and Goldman Sachs urge people NOT to buy bonds in the highlighted states?– BTW: Nebraska Bond

Rating is downgraded to AA+

– Omaha – AAA– Lincoln – AA+– California - BBB

Municipal Bonds

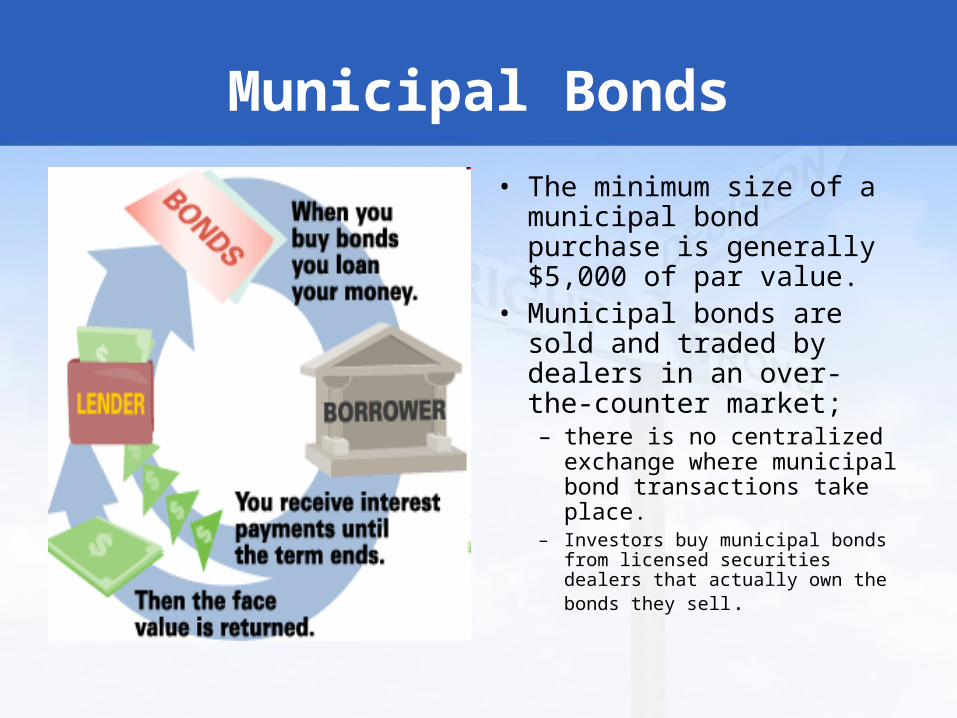

• The minimum size of a municipal bond purchase is generally $5,000 of par value.

• Municipal bonds are sold and traded by dealers in an over-the-counter market; – there is no centralized

exchange where municipal bond transactions take place.

– Investors buy municipal bonds from licensed securities dealers that actually own the bonds they sell.

Agency Bonds

• Some government sponsored but privately owned corporations.– Freddie Mac / Fannie

Mae

• Sometimes specific projects that government wants to fund.

Agency Bonds

• Often issue bonds to raise funds either to make loan money available or pay off a new project.

• No! Not that bond either!

US Treasury Bonds

• Backed by full faith and credit of the US government.

• When government doesn’t collect enough in taxes it issues notes, bills, and bonds to make up the difference. – Bonds = at least ten years

to maturity– Bills= less than two years

to maturity.

Current Bond Rates

• EE bonds = .7%• HH bonds = 1.5%• NEW rates will be

announced on November 1.

Why have US Savings Bonds?

• $50, $75, $100, $200, $500, $1,000, $5,000 and $10,000.

• Series EE Savings Bonds are purchased at half their face value. – A face-value $100 EE

bond is purchased for $50.

Why have US Savings Bonds?

• These EE bonds will increase in value every month instead of every six months. Interest is compounded semiannually.

What are the Opportunity Costs of US Savings Bonds?

• Could the US be “over leveraged”?

What happens if the US defaults?

• If new people – or countries – won’t buy our debt (bonds) – what then?

Final Note on Bonds

• Bonds are considered FIXED INCOME INVESTMENTS.– Fixed amount of

interest to the bondholder for the use of their money

Another type of purchase with the game – MUTUAL FUNDS

• A collection of stocks, bonds, and other securities owned by a group of investors and managed by a professional investment advisory firm.

Mutual Funds

• The investment firm pools money from investors and invests it.

Mutual Funds and Risk

• Some funds are CONSERVATIVE and others are more SPECULATIVE.

Mutual Funds

• Help to DIVERSIFY a portfolio.– DIVERSIFICATION:

Reducing risk by combining different investments so they aren’t going to be in step with one another.

– Mutuals Cannot:• Buy on margin• Short-sell stock

Mutual Funds: Types

• Value Funds – Only invest in stocks that the managers believe are UNDERVALUED.

• Socially Responsible Funds – only invest in companies that have “social responsibility.”– www.socialfunds.com

Vocabulary with Mutuals

• Open-end Funds – – Funds that sell as

many shares as investors want to buy.

• If you sell your shares, you sell them back to the fund.

• Closed-end Funds – – You buy these as

shares, like stock.

Vocabulary for Mutuals

• Large-Cap– Generally a company with

at least $5-billion in value of market capitalization.

• Mid-Cap– $1-$5 billion in market

capitalization (value of the company or stock)

• Small Cap– $250-million to $1-billion

• MICRO-CAP: less than $250 million.

The Best of Mutuals

Large Cap Value Fund 1yr. 5yrs. Expenses (as % of assets) American Funds American Mutual A -20.3 -0.4 0.60 Sound Shore -25.3 -0.7 0.92 T. Rowe Price Equity Income -24.9 -1.7 0.71 Vanguard Windsor II -24.4 -1.4 0.39

To find out more about Mutual Funds

• Morningstar.com

Why do you save money?

• Major purchases• Annual or

semiannual bills• Unexpected

expenses• Major long-term

expenses.• Amass wealth

What are the benefits of putting your money in a bank?

• Security• Interest

– Money cannot be lost.

Types of Savings Accounts

• Regular Savings Account– OB: require only a

small deposit.– OB: LIQUIDITY: can

be converted to cash with little or no loss in interest payments.

– OC: Most banks charge fees if balance too low.

Types of Savings Accounts

• Money Market Deposit Accounts:– OB: Generally

higher interest rates offered. Depends on t-bill interest rates.

– OB/OC: Fairly easy to withdraw.

– OC: Interest rate might be lower than regular savings.

Time Deposits

• CDs (Certificates of Deposit) – required to leave money in account for a specific amount of time.

• Maturity – When you can have your money back.

Time Deposits

• USUALLY the longer in, the more interest earned. – Depends on interest

rates!

• Interest rate is established when the CD is purchased.

• Require minimum deposit.

QOD

• If you had $1000 – how would you save it? – CD?– Savings Account?– Money Market?– Bonds?– Stocks?

Terms to Know:

• Compound Interest: Interest added to the PRINCIPAL at regular intervals.

• Subsequent interest is based on the original principal and the interest!

• $1000 at 5% = $1005• Compounded: $1000 at

5% = $1157.63

Terms to Know

• Simple Interest: Interest calculated at regular intervals based SOLELY ON THE PRINCIPAL.

• $1000 at 5% = $1050 a year.

• 3 years, $1150

Terms to Know

• Rule of 72: A way to calculate how long it takes your investment to double in value IF the interest rate is constant.

• 72/ interest rate = time it takes to double.

• EXAMPLE: 12 years for money to double at 6%.

Terms to Know

• 401K – A retirement plan that has employees AND employers contributing. Funds grow TAX-FREE until you withdraw them!

TERMS TO KNOW

• IRA – Individual Retirement Account: A personal savings account for retirement that is tax-free until you withdraw from the account.

• Variety of ways to set up the account to save for you!– DIVERSIFY!

Terms to Know

• Estate Plans: Life insurance, house – having a will to transfer funds and property.– Can be big bucks to

the taxman!