‘Bombardier Business Aircraft Seminar’ - ASA Appraisers · ‘Bombardier Business Aircraft...

75

Introduction – Mr. James Perry – Director Structured Finance Welcome to the ABACE 2014 ‘Bombardier Business Aircraft Seminar’ April 2014

Transcript of ‘Bombardier Business Aircraft Seminar’ - ASA Appraisers · ‘Bombardier Business Aircraft...

Introduction – Mr. James Perry – Director Structured Finance

Welcome to the ABACE 2014

‘Bombardier Business Aircraft Seminar’

April 2014

Introduction – David Crick, ASA, Partner, Lloyds Asset Services Background & Experience

! Accredited Senior Appraiser of the American Society of Appraisers

! Current President of the ASA Australian Chapter

! Serves on the Finance & Leasing Committee of the HAI

! Over 19 years of specialised valuation and consulting experience

! Corporate valuations for financial reporting, mortgage security assessments, insurance & liquidation disposals

! Appraisals for finance and leasing, aviation sales, mergers and acquisitions, insurance disputes, and expert witness for the legal fraternity

! A Partner with Lloyds Asset Services, an Australian company providing international valuation services for aviation assets

! Appraises both fixed wing & rotary aviation assets in Asia Pacific, the USA and various countries in Europe & the Middle East.

April 2014

Introduction – Richard Berkemeier, ASA, MTS Education Chair Background & Experience

! Accredited Senior Appraiser of the American Society of Appraisers in Machinery and Equipment and Appraisal Review and Management

! Current American Society of Appraisers Education Chair for

! Machinery and Equipment and ARM

! Former Vice President of Citigroup Investment Bank

! Over 30 years experience in Banking and Leasing

! Partner with CB Appraisal Review and Management Group

! Appraisals for finance and leasing of Aircraft, and complex leasing structures.

! Appraises both fixed wing & rotary aviation assets globally for Banks, Leasing, Insurance and End Users

April 2014

Introduction – Jeff Dorrough, ASA, Bombardier Pre-Owned Sales Background & Experience

! Accredited Senior Appraiser of the American Society of Appraisers

! Currently chief appraiser with Bombardier’s Pre-Owned group

! Is a member of ASA, NAFA, NARA, NBAA, GAMA

! Over 12 years of specialised valuation, diminution and residual value forecasting experience

! Assisted in creating corporate trade language

! Assisted in creation of the valuation policy for Bombardier

! Actively tracks market activity for Bombardier products world wide

April 2014

WHERE IS THE GLOBAL APPRAISAL PROFESSION

HEADED TODAY

Richard A. Berkemeier, ASA MTS Education Chair American Society of Appraisers [email protected]

April 2014

Important Points

n Education

n Continuing Education

n Accreditation

n Standards

n Ethics

n Online Education

n Delivery

n Politics and Global Convergence

April 2014

What Is the American Society of Appraisers (ASA)?

n The American Society of Appraisers, founded in 1936, is a non-profit

organization of appraisal professionals dedicated to the education, development

and growth of the appraisal profession Continuing Education

n ASA is international in structure and is the oldest and only major appraisal

organization representing all of the disciplines of appraisal specialists Standards

April 2014

About ASA – Our Mission

The American Society of Appraisers’ (ASA) international mission is to provide its members with education, accreditation and services to ensure exemplary ethics and competency across all disciplines of property appraisal, management and consulting services toward the goal of a unified profession; and to the betterment of the public interest.

April 2014

The ASA Appraisal Disciplines

Machinery and Technical Specialties (MTS):

§ Perform market or liquidation value appraisals for purposes such as sales, acquisition, ad valorem taxes, eminent domain, collateralization, insurance or residual forecasting

§ Appraise general machinery and equipment, aircraft, cost surveys, marine survey (commercial and yachts), mines and quarries, oil and gas, and public utilities

April 2014

The ASA Appraisal Disciplines (Continued)

Appraisal Review and Management (ARM):

§ (ARM) specialists concentrate on managing and reviewing appraisal assignments

§ Geared toward those individuals who may not perform appraisals on a regular basis, but who are responsible for approving appraisals or authenticating the valuation conclusions

April 2014

The ASA Appraisal Disciplines (Continued)

Business Valuation (BV):

§ Value specific intangible business assets such as patents, trademarks, employment agreements, copyrights, securities and goodwill

§ Prepare financial studies such as merger and acquisition studies, employee stock ownership plan feasibility analyses

§ May appraise for estate and gift tax returns, buy-sell agreements, securities litigation, equitable distribution in matrimonial matters and others

April 2014

The ASA Appraisal Disciplines (Continued)

Gems and Jewelry (GJ):

§ Specialize in diamonds and unmounted colored gemstones, contemporary jewelry, designer jewelry, Native American or other collectible ethnic jewelry, antique and period jewelry, gemstone carvings or mineral specimens

§ Familiar with all levels of the jewelry marketplace

§ Trained in market research and analysis

April 2014

The ASA Appraisal Disciplines (Continued)

Personal Property (PP): § Have specialized knowledge to competently produce appraisals for purposes such as

insurance, estate tax, damage claims, donation, sale, dissolution of marriage and equitable distribution

§ Personal property is defined as tangible, movable property that is utilitarian, collectible, decorative or a combination of the three

§ Appraise in specialties including antiques and decorative arts; fine arts; antique firearms, antique furniture; books; photography; Oriental rugs; sports collectibles and memorabilia; and many more

April 2014

The ASA Appraisal Disciplines (Continued)

Real Property (RP): § Analyze and value real property including:

§ Residential dwellings

§ Agricultural properties

§ Commercial properties (including shopping centers, office buildings, hospitals,

hotels, etc.)

§ Industrial plants

§ Timber and timberland; mineral rights, etc.

April 2014

ASA’s Education Program

Education

n ASA provides post-‐baccalaureate education in valuation through Principles of Valuation (POV) courses and higher level specialty courses

n Courses are taught by highly skilled practitioners who are well versed in the

intricacies of today’s workplace

n ASA courses are offered worldwide, on site at places of employment, at regular

course sites with the U.S. and at various U.S. universities and colleges

n Self-‐study options make ASA courses convenient and available for the busy

professional

April 2014

What Does ASA Do?

ASA offers education, testing and accreditation in the following disciplines:

n Appraisal Review and Management

n Business Valuation

n Gems and Jewelry

n Machinery and Technical Specialties

n Personal Property

n Real Property

April 2014

n Minimum Requirement of four 30 hour courses with Exams

n Completion of a Standards Course

n Completion of an Ethics Course

n Continuing Education Minimum 100 hours every 5 years

April 2014

Minimum Global Education Requirements Over The Next 5 Years

Consist of:

n 1. Courses in your discipline or expertise

n 2. Education Webinars

n 3. Attending Conference

n 4. Developing Education Intellectual Properties

April 2014

Continuing Education

To practice in the appraisal Industry you will need to have accreditation by a global organization recognized and accepted by the Government Regulating Bodies, Banking and Insurance Industry at the very minimum

April 2014

Accreditation

We have a myriad of Global Standards bodies including:

n 1. USPAP – Uniform Standards of Professional Appraisal Practice. This was

established based upon use in the US, Canada and Mexico (Rules Based)

n 2. IVS – International Valuation Standards as English Based and developing

global traction (Principles Based)

n 3. IBAPE - Brazilian Institute of Appraisals and Engineering Reports

n 4.China Appraisal Society Standards (CAS)

April 2014

Standards

n Need for Ethics

n Course Development

n Sign on the dotted line that you are doing this appraisal in compliance with the

Ethic Standard of the Society

April 2014

Ethics

n Education will move to an online delivery and format to save cost and time

April 2014

Online Education & Delivery

n Global Convergence of Education

n Global Convergence of Standards

n Politics involved in the process

n Why is the Appraisal Process so important and who cares?

n What is the relationship between the appraiser and the aircraft stakeholders.

n Appraisal is a snapshot in time.

April 2014

Moving Forward

1. Valuation methodology of the residual value of a Business aircraft vs commercial aircraft from a financier point of view

n 1a. Commercial vs Corporate comparisons

n 1b. Static curve vs business cycle

n 1c. Asset management

n 1d. RV expectation at term

n 1e. OLV considerations

April 2014

1a. Commercial versus Corporate Comparables Commercial Valuations

n Commercial aircraft primary purpose is income generation

n Aircraft are highly homogenous with little variance between aircraft

n Avionics are often functional for the theatre in which they operate

n Utilization is often high and not a component of value

n Utilization is a not major component of value n Engines are the primary source of value and

programs are not greatly used.

n Damage is not a primary consideration n Log books are often incomplete with varying

degrees of clarity

n Swapping of parts is acceptable and not a driver in value

Corporate Valuations n Corporate aircraft primary purpose is for

convenience or status reasons.

n Aircraft are often highly customized and differ greatly from one aircraft to another.

n Avionics are often state of the art, and differ from one aircraft to another, and from region to another.

n Utilization is often low and a major component of value.

n Engines are a primary source of value and programs are greatly used.

n Damage is regarded as a value degradation.

n Log books must have accurate and complete data.

n Swapping of parts is not acceptable.

April 2014

1b. Static curve vs business cycle Residual Value curves - The residual value could be defined as an estimated amount that an

entity can obtain when disposing of an asset after its useful life has ended. When doing this the estimated costs of disposing of the asset should be deducted.

Business Cycle - The fluctuations in economic activity that an economy experiences over a period of time. A business cycle is basically defined in terms of periods of expansion or recession.

n Residual Value curves are an effective tool in the prediction of future value during predictive markets, and factoring costs associated with owning the aircraft.

n Residual value curves never forecast price appreciation.

n Residual values must exhibit strict assumptions to predict value – utilization, asset life, residual value at the end of term.

n Residual Value curves do not take into account the seasonality of the business cycle.

n At any given point the residual value curve will most likely be different than the actual market conditions.

April 2014

1c. Asset Management

Asset Management

n The Asset Management Team is the cross- functional group responsible for managing the asset management process

n The Asset Management Plan defines goals, objectives, and strategies involving all functions of aircraft leasing.

n Each asset has an Asset Plan that defines the activities required by that asset — maintenance, refurbishments, and ultimate replacement.

n Asset Condition Monitoring is the ongoing process of measuring asset condition. This is not just to determine if the asset should be replaced or repaired — the process helps evaluate the frequencies and activities involved in normal operation and is used to update the Asset Plans.

n Periodic Audits — The asset management process includes periodic audits of all aircraft to ensure the aircraft meet the overall objective.

April 2014

1d. RV Expectation at term RV expectation can best be defined as the culmination and proper estimation of

all forms of obsolescence on a given aircraft at some future point in time combined with forecasted economic conditions.

n Functional Obsolescence - Functional obsolescence is defined as a form of depreciation resulting in a loss in value caused by conditions within the property such as changes in design, materials, or process and resulting in inadequacy, lack of utility, or excess operating expenses.

n Physical Obsolescence - defined as the loss in value due to physical wear and tear during usage and/or from the forces of nature.

n Economic Obsolescence - Economic obsolescence is defined as a form of depreciation, or an incurable loss in value, caused by unfavorable conditions external to the property, such as the government regulations, economics of the industry, availability of financing,

April 2014

Engine Technology

The Passport features some of today's most innovative aviation technology. With more than $1 billion in research and development invested annually in engines like the GEnx, F136 and LEAP-X, GE's leading-edge engineering and ingenuity have culminated in the development of the Passport. With our history of existing on-the-shelf technology, GE is poised to deliver outstanding next-generation business aviation power for decades to come.

April 2014

The GE Passport sets a new standard for performance of ultra-long range business aircraft. Developed as an Integrated Propulsion System (IPS), the Passport is designed to meet the requirements of the business aviation operator with low cabin noise, emissions and fuel consumption. As a result of rigorous testing and improvements across GE's military and commercial platforms, the Passport is poised to deliver enhanced performance, reliability and efficiency.

Aircraft Navigation Technology

n Automatic Dependent Surveillance (ADS-B)

n Wide Area Augmentation System (WAAS) Also called Space Based Augmentation System (SBAS)

Compared to Local Area Augmentation System (LAAS)

l Localizer Performance with Vertical Guidance (LPV)

l Required Navigation Performance (RNP)

n Controller-Pilot Data Link Communication (CPDLC) l Protected Mode CPDLC (PM-CPDLC)

n Automatic Dependent Surveillance-Broadcast (ADS-B)

n Future Air Navigation System (FANS) l FANS 1/A

l FANS 2

n Traffic Collision Avoidance System (TCAS) 7.1 These Acronyms Used Extensively in the Industry

April 2014 Data generously provided by Honeywell Aerospace

Technology for Safer and More Efficient Skies

New Technology Changes Aircraft Values

Technology is moving fast. It is hard to think that the ubiquitous Smart Phone wasn’t even here 7 years ago.

Aircraft are in an increasingly faster technology change as consumer technology advances drives changes. The advance to software based features has enabled huge transitions with easier to modify equipment.

1990 2010 2030 Understanding these advances is key to mapping the value of aircraft.

April 2014 Data generously provided by Honeywell Aerospace

ADS-B “Out” Regulatory Timeline

Hudson Bay Improved Access, (DO-260) FL 350 to 400

FAA* Retrofit, (DO-260B) January 1, 2020

ADS-B “In” Mandates-

Europe Retrofit, (DO-260B) December 7, 2017

Australia* Retrofit, FL 290+, (DO-260) December 2, 2013

No known Regulations

Gulf of Mexico ADS-B Out (DO-260A) Improved Access

= Preliminary Date

= Published Date

*Note – Australia and FAA Mandates Also Require “SA Aware” GPS Receiver (i.e. WAAS)

April 2014 Data generously provided by Honeywell Aerospace

What is SBAS, LAAS, WAAS, and LPV?

Space Based Augmentation Systems increase GPS position accuracy within a particular region

Local Area Augmentation Systems (ground based) at an airport or local airports

-------- Wide Area Augmentation System is the SBAS system that

covers North America

SBAS utilizes ground stations to measure errors in the GPS signal for the region and provides corrections to GPS receivers

These corrections dramatically increase the accuracy and integrity of GPS position thereby enabling precision-like LPV Approaches with a decision height as low as 200 feet

Parameter GPS SBAS/GPS LAAS/GPSCat III

Horizontal Position Accuracy 10 m 1-2 m < 1 m

Vertical Position Accuracy 15 m 2-3 m < 1 m

(LPV Stand for Localizer Performance with Vertical Guidance)

April 2014 Data generously provided by Honeywell Aerospace

WAAS/LPV Compatible with Other SBAS Systems

Currently in Service – WAAS – Wide Area Augmentation System (US, Canada, Mexico)

– EGNOS – European Geostationary Navigation Overlay Service (Europe)

Coming in the Future – MSAS – Multifunctional Satellite Augmentation System (Japan)

– SDCM – System for Differential Corrections and Monitoring (Russia)

– GAGAN – GPS Aided Geostationary Augmented Navigation (India)

– SNAS – Satellite Navigation Augmentation System (China)

– SACCSA – Soluciόn de Aumentaciόn para Caribe, Centro y Sudamérica (South America)

April 2014 Data generously provided by Honeywell Aerospace

Benefits of RNP/SBAS/LAAS Procedures

Allows for curved flight paths to accommodate terrain, obstacles, airspace or noise footprint

Saves time and fuel through optimum routing

Less reliance on ground navaids such as VORs and ADFs

Increased safety through stabilized vertical path on approaches (no step-downs)

Improved airport access through lower VNAV minima

Terrain E.g. Juneau, Alaska

Airspace E.g. Washington National

Stabilized Path

It’s All About Limiting Variance

RNP AR RNAV (RNP)

RNP RNAV (GPS)

SBAS LPV WAAS

GBAS LAAS

April 2014 Data generously provided by Honeywell Aerospace

What is Controller Pilot Data Link Communication ?

CPDLC is simply “text messaging” between the pilot and ATC for aircraft control instead of using voice communication

Pilot can request and/or acknowledge changes to aircraft speed, altitude and route using standard ATC phraseology

Functionality contained in Flight Management Computer and/or Communications Management Unit

Utilize both SATCOM and VHF Data Links

PM-CPDLC is Protected Mode (encrypted) European Mandate

Reduces Comm Cost, Language and Static Barriers

April 2014 Data generously provided by Honeywell Aerospace

Data Link Recording & CPDLC Regulatory Timeline

Eurocontrol PM-CPDLC Retrofit Required February 5, 2015

Eurocontrol PM-CPDLC Non-Compliant A/C can’t fly in Europe January 1, 2017

Eurocontrol PM-CPDLC End of Exemption with FANS-1/A January 1, 2014

FAA CVR CPDLC Recording Part 135 (CPDLC installed) December 6, 2010

FAA CVR CPDLC Recording Part 91 (CPDLC installed) April 6, 2012

= Preliminary Date

= Published Date

North Atlantic Tracks - FANS 1/A February 2013 - Tentative 2015

April 2014 Data generously provided by Honeywell Aerospace

1e. OLV Considerations OLV is defined as an opinion of the gross amount, expressed in terms of money,

that typically could be realized from a liquidation sale, given a reasonable period of time to find a purchaser (holding costs), with the seller being compelled to sell on an as-is, where-is basis, as of a specific date.

OLV is used by financial institutions to ascertain the value in which the bank could exit a lease with no financial impact to the banks portfolio. It is a moving target that needs to be calculated on a regular basis.

n Seek 3rd party valuations periodically for market

n Factor any STC or other import export costs

n Factor the costs to return the aircraft to a normalized condition

April 2014

2. What are the major factors which impact the residual value of a business aircraft?

n 2a. Aircraft time

n 2b. Condition

n 2c. Maintenance

n 2d. Damage

n 2e. Programs

n 2f. Markets / Economy

April 2014

2a. Airframe Time

n The benchmark utilization for most business aircraft is between 300 and 450 annually

n Higher airframe times have a punitive impact on aircraft value

n Lower airframe times have a beneficial impact on aircraft value

n Each aircraft will have a major airframe inspection due

April 2014 Data generously provided by Bombardier Inc

2b. Condition Adjustments n Condition adjustments represent aesthetics of the aircraft and the acceptance in the market

place.

n Paint

l Average paint is every 5 to 7 years

l Costs can range from $50K to $300K depending on the size of the aircraft.

l The most common paint scheme is Matterhorn white base with 2 stripes

n Interior

l Average interior refurb is every 5 to 7 years

l Costs can range from $65K to $1.2M

l Cabin configuration has a dramatic affect on value

l The common cabin configuration is based on the type of aircraft

n Each aircraft will have a major airframe inspection due

April 2014

2c. Maintenance Adjustments n Maintenance is broken down into scheduled and unscheduled. Scheduled maintenance can

be based on hourly, cycle, or calendar. n Unscheduled maintenance occurs when a random part breaks at random time intervals.

n Scheduled maintenance is either manufacturer or aircraft specific. Each aircraft will have a major inspection at regular intervals l Airframe – are usually performed on a hourly basis l Control Surfaces – are generally both hourly and cycle driven l Landing gears – are usually performed on a cycle basis l Engines - are generally both hourly and cycle driven l APU (Auxilary Power Unit) - are generally both hourly and cycle driven

n Maintenance schedules can be based on high utilization (HUMP), low utilization (LUMP), or Chapter 5 (most common)

n Maintenance costs vary widely and require the aircraft to be out of use for long periods of time

April 2014

2d. Damage History n Damage is a very subjective matter and is best described as two parts – Curable and non-

curable

n Curable damage constitutes damage to a specific portion of the aircraft that has been fixed.

l A winglet is damaged – part-off, part-on

l From an engineering perspective the aircraft is repaired to a status that is as good, or better than prior to the incident.

n Non-curable damage constitutes the stigma associated with the damage event, log book entries and marketability of the aircraft.

l From a re-sale aspect even though the aircraft has been repaired, it may suffer in price degradation due to poorly written log entries, or overall market perception of the incident.

April 2014

Damage Issues – Interior

April 2014

Damage Issues – Exterior

April 2014

2e. Programs – Airframe There are many programs from many different suppliers. These programs help the

owner in flattening his exposure to events over time, and allows the owner to better forecast costs. Some popular programs are:

n Airframe/Parts – Covers the costs associated with part changes, however does not usually cover labor costs

l JSSI – Tip to tail – All manufacturers

l Smart Parts – Bombardier product

l PlaneParts – Gulfstream product

l Pro Parts – Cessna product

l Falcon care – Falcon product

April 2014

2e. cont. Programs – Engines & Other

n Engines/APU – Cover a range of options depending on level of coverage

l MSP – Honeywell engines

l ESP – Pratt & Whitney engines

l Rolls Royce Corporate Care – Rolls Royce engines

l GE On Point – GE Engines

l TAP Elite – Williams Engines

l JSSI – All Engine makes

n Avionics

l HAAP – Honewell avionics suites

April 2014

2f. Markets and Economy n The aircraft marketplace and overall economy have

a major impact on aircraft values.

n Saturation – The count of aircraft available for sale divided by the count of total aircraft in operation for any aircraft model.

l 12% saturation is commonly viewed as normalized markets, meaning an equal number of buyers and sellers.

u Nominal depreciation is observed l 0% to 10% is commonly viewed as a good

market, meaning more buyers than sellers.

u Little to no depreciation is observed l 15% or more is commonly viewed as a

depressed market, meaning more sellers than buyers.

u Greater amounts of depreciation are observed, often greater than 10% per quarter.

April 2014 Data generously provided by Bombardier Inc

Business Jet Market Performance 1966-2013

'66 '68 '70 '72 '74 '76 '78 '80 '82 '84 '86 '88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12'13

0%

20%

40%

60%

80%

-20%

-40%

-60%

(% Change YoY)

$0

$5

$10

$15

$20

$25(Deliv eries in '14 $ Bns)

Market Change YoY Value of Deliveries

April 2014 Data generously provided by The Teal Group Corporation

April 2014 Data generously provided by The Teal Group Corporation

April 2014 Data generously provided by The Teal Group Corporation

April 2014 Data generously provided by The Teal Group Corporation

April 2014 Data generously provided by The Teal Group Corporation

This was a severe downturn, but it only hit half the OEM market.

Large aircraft performed well, for everyone else, the effect and uncertainty have been quite long-

lasting.

Good chance that the bottom half starts recovering this year.

OEMs in the bottom half of the market face a structurally altered industry.

Worldwide Business Aircraft Market Information

April 2014

Drivers of World Aircraft Prices

n Percentage of Active Fleet For Sale

n Percentage/Number of Aircraft Selling

n Average Asking/Selling Prices

April 2014

Worldwide Business Aircraft Resale Market Aircraft Size Groupings • Turbo-Props • Light Jets - < 20,000lbs MTOW • Medium Jets – 20-40,000lbs MTOW • Large Jets – 40,000lbs + MTOW

• “Newer” – <=10 years old • “Mid Age” – >10 years, <=20 years old • “Old” – >20 years old

Aircraft Age Segments

Market Parameters • % Active Fleet For Sale • Resale Retail Transactions (as % of active fleet) • Average Asking Prices $

Data generously provided by AMSTAT April 2014

Business Aircraft Resale Market Percentage of Active Fleet For Sale or Lease

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Turbo-‐Props Light Jets Medium Jets Large Jets

Data generously provided by AMSTAT April 2014

2006 2007 2008 2009 2010 2011 2012 201312.4% 11.2% 12.3% 17.5% 15.1% 13.8% 13.5% 13.2%

Jets1Available1for1Sale1as1%1of1World1Fleet1(as1of1July11)

!11,969!! !12,876!! !13,703!! !13,729!!!14,818!! !15,561!! !16,110!! !16,621!!

!1,697!! !1,617!!!1,925!! !2,909!!

!2,638!! !2,492!! !2,518!!!2,518!!

0%#2%#4%#6%#8%#10%#12%#14%#16%#18%#20%#

!-!!!!

!5,000!!

!10,000!!

!15,000!!

!20,000!!

!25,000!!

2006! 2007! 2008! 2009! 2010! 2011! 2012! 2013!

%!of!Fleet!fo

r!Sale!

Aircra;!(Units)!

Business!Jets!for!sale!-!July!1,!2006-2013!

Aircra;!not!for!sale! Aircra;!for!sale! %!Aircra;!for!sale!

Pre-Owned Business Jet Inventory

Data generously provided by JETNET iQ April 2014

Pre-Owned Business Jet and Turboprop Inventory

0%#

2%#

4%#

6%#

8%#

10%#

12%#

14%#

16%#

18%#

20%#

#)####

#500##

#1,000##

#1,500##

#2,000##

#2,500##

#3,000##

#3,500##

2006# 2007# 2008# 2009# 2010# 2011# 2012# 2013#

Business#Jets#and#Turboprops#for#sale#Jul#2006#)##Jul#2013#

##of#Jets#for#sale# ##of#Turboprops#for#sale# %#of#Jets#for#sale# %#of#Turboprops#for#sale#

2006 2007 2008 2009 2010 2011 2012 2013Business/Jets 12.4% 11.2% 12.3% 17.5% 15.1% 13.8% 13.5% 13.2%Turboprop 9.0% 8.2% 9.0% 12.0% 10.9% 10.3% 8.9% 7.7%

Jets/Available/for/Sale/as/%/of/World/Fleet/(as/of/July/1)

Data generously provided by JETNET iQ April 2014

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%

2008 2009 2010 2011 2012 2013

Turbo-‐Props Light Jets Medium Jets Large Jets

Business Aircraft Resale Market Resale Retail Transactions (RRT) As Percentage of Active Fleet

All RRT Q1 + Q2 2008 2009 2010 2011 2012 2013

% 5.5% 3.3% 4.0% 4.6% 4.8% 4.7%

Data generously provided by AMSTAT April 2014

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

2008 2009 2010 2011 2012 2013

Older Jets Mid-‐Age Jets Newer Jets

Business Jet Resale Market – by Age Resale Retail Transactions As Percentage of Active Fleet

All Jets Q1 + Q2 2008 2009 2010 2011 2012 2013

% 5.1% 3.2% 4.0% 4.7% 4.9% 4.8%

Data generously provided by AMSTAT April 2014

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Jet BR Turbo-‐Prop BR

Business Aircraft Resale Market Burn Rate

Burn Rate – The number of months it would take, at the current average monthly resale retail transaction rate, to sell the current inventory. Calculated by dividing the current inventory count by the average number of resale retail transactions for the respective quarter.

Data generously provided by AMSTAT April 2014

Business Large Jet Resale Market Average Asking Prices

$8,000,000

$10,000,000

$12,000,000

$14,000,000

$16,000,000

$18,000,000

$20,000,000

Data generously provided by AMSTAT April 2014

3. Aircraft asset portfolio protection

n 3a. Rule of 15

n 3b. Utilization Controls

n 3c. Maintenance event controls

n 3d. Avoiding Risks with programs

n 3e. Charter risk

n 3f. Damage clauses

n 3g. Personalization Issues

April 2014

3a. Rule of 15

n Traditionally was called the rule of 25, however, due to the recent financial crisis it has been modified to exclude a larger group of aircraft.

n Rule of 15 simply states that the sum of the aircraft age and finance term cannot exceed 15 years.

l Minimal amounts down – 5%-10% l Most attractive rates l Most minimally invasive return conditions

n Outside of the rule of 15 you may not be able to get financing, or it is more cumbersome. l Higher amounts down – 20% or more l Higher rates l Most invasive return conditions

April 2014

3b. Utilization Controls

n Utilization controls can help maintain the value of you asset, and assist you accurately forecasting future values.

n Know your customers utilization profile

April 2014

3c. Maintenance Event Controls

Major maintenance events occur throughout the aircrafts life with some being very costly.

n Know the events so as to accurately forecast future residual values

n Mandate aircraft to be on all programs to minimize the costs of each event

n Ensure favorable return conditions so the bank isn’t left holding the costs of the

event.

April 2014

3d. Avoiding Risks With Programs

Many aircraft Lessors are caught unaware of mitigating end of term risk. Simple steps can be taken to ensure this risks are minimized.

n Tripartite Agreements

n Ensure AD’s & SB’s are current

n Confirmation of Program currency

April 2014

3e. Charter Risk Controls

Many aircraft owners supplement annual usage with charter to offset the costs of borrowing.

n Attempt to not allow supplemental charter as it decreases your value through

utilization and condition adjustments through wear and tear.

n Know your customers utilization profile you can minimize the amount he is able

to charter.

n Beware of the danger of ‘grey’ charter which would negate insurance profiles

and other jurisdictional requirements

April 2014

3f. Damage Clauses

Many aircraft suffer some form of damage in its life. Types of damage can range from hanger rash to controlled crashes.

n Institute periodic visits to the aircraft and conduct log book reviews.

n Create language that allows the bank to assess any event that occurs to the

aircraft.

n Use a third party appraiser to assess the market impact

April 2014

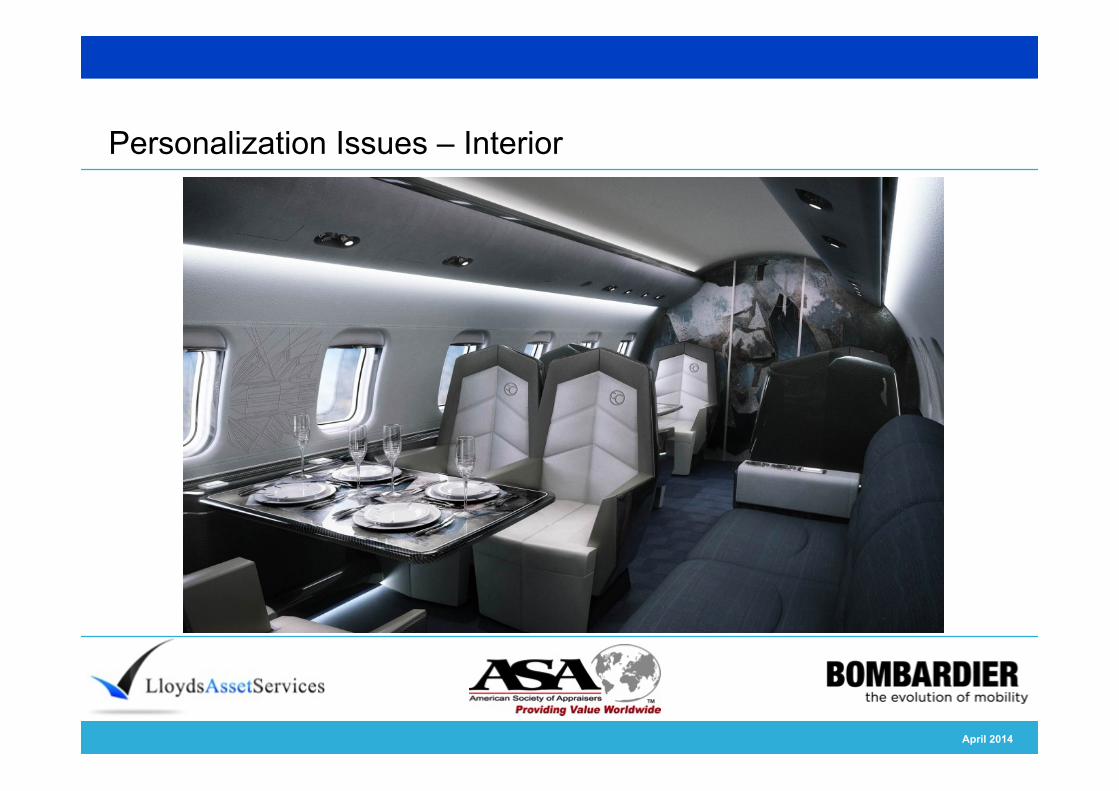

3g. Personalization Issues

Many aircraft owners wish to personalize their aircraft either with logo’s, customized paint, or interiors. While re-painting the aircraft can be relatively easy the removal of vinyl logo’s can damage the undersurface of the paint requiring a subsequent re-paint.

Interiors do not have to be exotic to justify a customized interior and create costs at the time of sale.

n Institute periodic visits to the aircraft and conduct log book reviews.

n Create language that allows the bank to assess any event that occurs to the

aircraft.

n Use a third party appraiser to assess the market impact of such an event

n Factor the costs to return the aircraft to a normalized condition

April 2014

Personalization Issues – Exterior

April 2014

Personalization Issues – Exterior

April 2014

Personalization Issues – Interior

April 2014

Aircraft Valuation from Manufacturer point of view

n Market Expectations – Pre-Owned Aircraft

April 2014