BOARD OF REVISION - Supreme Court of Ohio and the Ohio ... Rite Aid of Ohio, Inc. v ... revealed a...

23

t^Frm np'`"^^ IN THE SUPREME COURT OF OHIO LOWE'S HOME CENTERS, INC., Appellant, V. Case No. 2014-0843 Appeal from Ohio Board of Tax Appeals BTA Case No. 2011-1664 WASHINGTON COIJNTY BOARD OF REVISION, et al., Appellees. BRIEF OF APPELLEES WASHINGTON COUNTY AUDITOR AND WASHINGTON COUNTY BOARD OF REVISION Kelley A. Gorry (0079210) COUNSE.L OF RECORD James R. Gorry (0032461) Rich & Gillis Law Group, LLC 6400 Riverside Drive, Suite D Dublin, OH 43017 PH: (614) 228-5822 FAX: (614) 540-7476 [email protected] Attorneys for Appellees Washington County Auditor and Board of Revision The Honorable Michael DeWine (0009181) Ohio Attorney General 30 East Broad Street, 17th Floor Cohimbus, OH 43215 PH: (614) 466-4986 AttoNney for Appellee Ohio Tax Commissioner Ryan J. Gibbs (0080331) Geoffrey N. Byrne (0090906) The Gibbs Firm, LPA 2355 Auburn Avenue Cincinnati, OH 45219 PH: (513) 381-3890 FAX: (866) 796-3717 Attorneys for Appellant Lowe 's Home Centers, Inc. O'1.EIR , K OF a/ f^,y^l^^i ji rqit'^8fo.. n; ' tt%^.u ^^ : 5 :^ ,G.,'c?5 #^%•^%i^.'^3v.^f,±,, P.^ i 'c.% <a'{ : ,i i :^?

Transcript of BOARD OF REVISION - Supreme Court of Ohio and the Ohio ... Rite Aid of Ohio, Inc. v ... revealed a...

t^Frm np'`"^^

IN THE SUPREME COURT OF OHIO

LOWE'S HOME CENTERS, INC.,

Appellant,

V.

Case No. 2014-0843

Appeal from Ohio Board of Tax AppealsBTA Case No. 2011-1664

WASHINGTON COIJNTY BOARD OFREVISION, et al.,

Appellees.

BRIEF OF APPELLEES WASHINGTON COUNTY AUDITOR ANDWASHINGTON COUNTY BOARD OF REVISION

Kelley A. Gorry (0079210)COUNSE.L OF RECORDJames R. Gorry (0032461)Rich & Gillis Law Group, LLC6400 Riverside Drive, Suite DDublin, OH 43017PH: (614) 228-5822FAX: (614) [email protected] for Appellees WashingtonCounty Auditor and Board of Revision

The Honorable Michael DeWine (0009181)Ohio Attorney General30 East Broad Street, 17th FloorCohimbus, OH 43215PH: (614) 466-4986AttoNney for Appellee Ohio TaxCommissioner

Ryan J. Gibbs (0080331)Geoffrey N. Byrne (0090906)The Gibbs Firm, LPA2355 Auburn AvenueCincinnati, OH 45219PH: (513) 381-3890FAX: (866) 796-3717Attorneys for Appellant Lowe 's HomeCenters, Inc.

O'1.EIR, K OF a/ f^,y^l^^i

jirqit'^8fo..

n;'tt%^.u ^^ : 5 :^

,G.,'c?5#^%•^%i^.'^3v.^f,±,,

P.^

i

'c.%<a'{ : ,i i :^?

TABLE OF CONTENTS

Table of Authorities •......................................................................>................................,.,............. iig

Statement of the Case and Facts ......................................................................................................1

Law and Argument ..........................................................................................................................5

Intro duction . . . ... . . . . ... . .. . . .. .. . . . . . . . . . . . . . . .. .. . . . . . . . . .. . . . . . .. . . . . . . .. . .. . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . .. . . .. . .. . . .. .. . . . . . . . .. . . . . . .. .. . 5

Reply to Proposition of Law No. 1 ..................................................................................................6

Lowe's "leased fee" argument was rejected in Meijer and no adjustment isrequired for "leased fee" sales ..........................................................................................6

Reply to Proposition of Law No. 2 ..................................................................................................9

The BTA's decision does not violate the Equal Protection Clause ................................9

Reply to Proposition of Law No. 3 .......................... ...................................................................... 10

Ms. Blosser did not violate USPAP or state law regarding the preparation ofthe Blosser Report ............................................................................................................10

Reply to Proposition of Law No. 4 ................................................................................................11

The BTA was not required to independently determine value as it properlyadopted the Blosser Report as competent and probative evidence of value ...............11

Conclusion .....................................................................................................................................13

App endix . ... . . .. .. . . . . .. .. . . . . . .. . . . .. . . . . . . . . . . .. . . . . . . . . . . .. . . . . . . . . . . . . .. . . . . . . . .. . . .. . .. • . .. . . .. . . . . . . .. . . .. . ... ... . ... . .. . . . . . . .. . .. . . . .. . . . .1

ii

TABLE OF AUTHORITIES

Statutes:

R.C. 4763.01 .. ........................................................................................................................11

R.C. 5713.03 .......... ...........................................................................................................................9

Cases:

AEI Net Lease Income & Growth Fund v. Erie County Board of Revision,

119 Ohio St. 3d 563, 2008-Ohio-5203, 895 N.E.2d 830 ................................................. 7-8

Cardinal Fed. S. & L. Assn. v. Cuyahoga Cty. Bd of Revision,

44 Ohio St. 2d 13, 336 N.E.2d 433 (1975) ........................................................................12

Columbus City Schools v. Franklin Cty. Bd of Revision,

134 Ohio St. 3d 529, 2012-Ohio-5680, 983 N.E.2d. 1285 ...................................................9

Cummins Property Services, L.L.C. v. Franklin County Board ofRevision,117 Ohio St. 3d 516, 2008-OQhio-1473, 885 N.E.2d 222 .....................................................7

Dublin City Schools Bd of Edn. v. Franklin Cty. Bd of Revision,139 Ohio St. 3d 212, 2014-Ohio-1940, 11 N.E.2d 222 .....................................................12

EOP-BP Tower, L.L.C. v. Cuyahoga Cty. Bd of Revision,

106 Ohio St. 3d 1, 2005-Ohio-3096, 829 N.E.2d 686 .......................................................12

Fawn Lake Apts. v. Cuyahoga Cty. Bd of Revision,

75 Ohio St. 3d 601, 665 N.E.2d 194 (1996) ......................................................................12

Health Care REIT, Inc. v. Cuyahoga Cty. Bd. of Revision,

140 Ohio St. 3d 30, 2014-Ohio-2574, 14 N.E.3d 1009 .................................................9, 10

!lleijer Stores Limited Partnership v. Fi°anklin County Board of Revision,122 Ohio St. 3d 447, 2009-Ohio-3479, 912 N.E.2d 560 ...................

AIeyer et al. v. Cuyahoga Cty. Bd of Revision,

58 Ohio St. 2d 328, 334, 390 N.E.2d 796 (1979) .........................

Olmstead Falls Bd of Edn. v. Cuyahoga Cty. Bd of Revision,122 Ohio St. 3d 134, 2009-Ohio-2461, 909 N.E.2d 597 .................

...................... infra

.................................9

............................9

iii

Rite Aid of Ohio, Inc. v. Washington Cty. Bd of Revision,

BT'A No. 2011-1760, 2014 Ohio Tax LEXIS 2541 (Apr. 22, 2014), unreported .........9, 10

Southern Railway Co. v. yVatts,260 U.S. 519 (1923) ...........................................................

iv

..........................................9

STATEMENT OF THE CASE AND FACTS

Appellant Lowe's Home Centers, Inc. ("Lowe's") filed a complaint with the Washington

County Board of Revision (the "BOR") for tax year 2010 seeking a reduction in value on that

certain real property it owns located at 842 Pike Street in Marietta, OH and identified as

Auditor's Parcel Numbers 23-00-84565.001, 24-00-84563.001, 24-00-84570.002, 24-00-

84566.001, 24-00-84566.004, and 24-00-84566.720 (the "Subject Property"). The Subject

Property is improved with a 142,446 square foot freestanding retail home improvement store

constructed in 2002 which was owner-occupied by Lowe's as of the applicable lien date of

January 1, 2010.

At the hearing before the BOR, Lowe's presented an owner's opinion of value containing

comparable sales but did not present an appraisal. See BOR Hearing Record, Record. The BOR

declined to grant a reduction in value from the Auditor's original valuation and Lowe's appealed

to the Ohio Board of Tax Appeals (the "BTA").

At the hearing before the BTA, both Lowe's and the County Auditor and BOR

(collectively, the "County Appellees") presented appraisals. Lowe's presented an appraisal of

Patricia Costello of the Robert Weiler Company with an effective date of January 1, 2010 (the

"Costello Report"). See Costello Report, Record. Ms. Costello utilized both the sales

comparison and income approaches to value. Regarding her sales comparison approach, Ms.

Costello selected all vacant or second-generation sales. The rationale for such rejection was

expressed in her appraisal as well as her testimony before the BTA. Page 37 of the Costello

Report reads as follows, in its relevant part:

We are aware of a number of sales that have occurred that involve first generationleases that are based upon the costs of construction of big box facilities plus a

1

profit to the developer that builds the facilities. All costs of construction,including land, are included in this lease rate. These costs are amortized over anagreed upon period, typically fifteen to twenty years. There may be additionalrenewal periods.

Essentially, these leases represent a financing mechanism for the occupant. Theymay also contain amortized tenant improvements and personal property, whichare not real estate and are not relevant. They are not considered to representmarket rents. When these properties are sold on the open market, although the"lease rates" may or may not be significantly above those noted in secondgeneration space, the terms of the leases are much longer than are typically notedin the general marketplace, i.e. three to seven years. Additionally, thecreditworthiness of these tenants far exceeds that of the tenants that would beanticipated to occupy the subject's space upon its releasing. Therefore, sales ofthese first generation big box facilities were considered in our analysis of thesubject property; however, they do not represent the considerations of the mostlikely purchasers of the subject property, and they have not been utilized in ouranalysis.

Costello Report at p. 37-38. Moreover, Ms. Costello admitted on cross-examination before the

BTA that she was intentionally valuing the property as if Lowe's was not the occupant as of the

applicable lien date. BTA Hearing Record ("H.R.") at p. 49:18-22. In selecting her sales

comparables, she excluded all first-generation sales and selected sales of stores older than the

subject. When questioned regarding the availability of newer big box stores, she admitted that

she was unable to locate such stores as due to the subject's age of 8 years old, the first-generation

user that built the store usually had not vacated the property as of this date. Id. at p. 50:13-19.

The selected comparables included two former Wal-Marts, a former Lowe's, and a second-

generation Garden Ridge. See Costello Report at pp. 40-47. Such sales, before adjustments,

revealed a range of value of $10.54 per square foot to $43.04 per square foot. Id After adjusting

for location, condition and age, visibility, size and quality of construction, Ms. Costello

concluded at a value of $40.00 per square foot, or $5,700,000, via the sales comparison

approach.

2

For her income approach, Ms. Costello also deliberately excluded consideration of any

rents resulting from "build-to-suit" arrangenlents, explaining the basis for such rejection as:

We considered a number of leases of retail facilities in the Ohio area that aresimilar in age and in utility to the subject property. The lease rates in thesefacilities are based upon the costs of constructing such facilities, including thecost of acquiring the sites, which may vary significantly from location to location,and are inclusive of a profit to the developer. These costs, often termed build tosuit or custom construction costs, are amortized over an agreed upon lease term.These leases are not considered. to represent market rent. They are not based onopen market negotiations but rather are negotiated exclusively with the owner of apredetermined site on terms that provide a return on the site owner's investment.These facilities have not been exposed to the open market for competitive biddingfrom prospective tenants. The amortized lease terms are typically fifteen totwenty years, much longer than typical lease terms which range from three toseven years. Consequently, we have not utilized these leases in our analysis ofmarket rent.

Id at p. 19. For her lease comparables, she selected a former Value City Furniture, a Value City

Furniture and inline space for three retail shopping centers. Id. at pp. 20-29. The size of such

comparables ranged from 20,000 to 81,548 square feet, in contrast to the subject's size of

1.46,442 square feet. After adjustments, Ms. Costello selected a "market" rent of $4.00 per

square foot on a triple net basis. She selected market expenses upon review of three expense

comparables. Id. at pp. 33-34. After including a replacement reserve, she arrived at a net

operating income of $503,190 which she capitalized at a rate of 9.5% and concluded to a value

of $5,295,000 via the income approach. Id. at p. 35. In reconciling both approaches and placing

primary reliance upon the sales comparison approach as "a majority of these facilities sell on a

vacant basis" for a final value of $5,700,000 for the Subject Property as of January 1, 2010. Id. at

p. 49.

In contrast, the County Appellees submitted an appraisal of Karen Blosser, MAI, of US

Realty Consultants with an effective date of January 1, 2010 (the "Blosser Report"). Ms. Blosser

3

also utilized the sales comparison and income approaches to value. For her sales comparison

approach, Ms. Blosser looked primarily to sales of big box facilities of 90,000 square feet or

larger in size. She surveyed all transactions occur.ring in Ohio between January 2006 and

December 2011 and noted that the average sale price of those sales which she was able to

confirm was $76.31 per square foot. See Blosser Report at p. VI-1. From those sales, she

selected six sales, consisting of three first-generation occupied facilities, one second-generation

occupied facility, and two vacant former first-generation facilities. Id at pp. VI-4-VI-12. For her

adjustments, she considered conditions of sale, property rights conveyed, market conditions,

location, size, age/condition/quality, and occupancy. While recognizing that the Subject

Property was located in a rural area, although on the main commercial corridor of Marietta,

Ohio, she specifically considered traffic counts for main and secondary access streets, population

and median household income around a 5-mile radius of each comparable. Id. at pp. VI-15-VI-

17. After adjustments, the comparables revealed a range of value from $21 per square foot to

$87 per square foot. In selecting a valuation in the middle of such range at $50 per square foot,

or $7,100,000, Ms. Blosser concluded as follows:

The subject was constructed for a first generation user with that user, Lowe'sHome Improvement, still in place. We have taken this fact in addition to thepossibility of vacancy at the subject into consideration in our conclusion of value.The subject is located in a relatively small market with a slightly decliningpopulation basis. It is noted, however, that the subject area has a high trafficcount that draws from surrounding areas. Based on the above, it is our opinionthat the subject falls within the middle of the adjusted range.

Blosser Report at p. VI-19.

For her income approach, she selected four first-generation big box leases ranging in size

from 94,731 square feet to 156,013 square feet, including a Wal-Mart, Sam's Club, Lowe's and a

4

Giant Eagle. Id. at p. 111-8. After adjustments, including the specific location adjustments

applied to the comparable sales, the rent comparables revealed a market rent range of $5.00 per

square foot to $9.00 per square foot. From these comparable rents and conversations with local

market participants, Ms. Blosser selected a rental rate of $5.75 per square foot, triple net. Id. at p.

111-8. She included minimal expenses for a management fee, replacement reserve, and general

expenses in time of vacancy, and arrived at net operating income of $668,036. Id. at p. V-3.

When capitalizing the net operating income at a capitalization rate of 9.25%, Ms. Blosser

concluded to a total value of $7,200,000 via the income approach. Id. at p. V-5. Ms. Blosser

relied primarily upon the income approach, noting that the income approach "is considered to

provide a meaningful indication of value since retail buildings such as the subject are often

income-producing properties purchased with the intent of realizing future profits," for a final

value of $7,200,000 for the Subject Property. Id. at p. VII-1.

On April 22, 2014, the BTA issued its decision accepting the Blosser Report as "more

persuasive" of the Subject Property's value for tax year 2010. As support for its determination,

the BTA held that Ms. Costello's analysis was "potentially skewed" as she deliberately excluded

all first-generation used-occupied and long-term leases build to suit properties. See BTA

Decision, Record, at p. 2. Moreover, it recognized Ms. Blosser's comparables as more

appropriate, particularly when the subject was located in a "high trafficked area which draws

from a regional market." Id. at p. 3. Lowe's timely appealed to the Court.

LAW AND ARGUMENT

INTRODUCTION

At issue in this appeal is whetlier the BTA abused its discretion in adopting the Blosser

5

Report over the Costello Report in accordance with this Court's decision in Me^er Stores

Limited Partnership v. Franklin County Board of Revision, 122 Ohio St. 3d 447, 2009-Ohio-

3479, 912 N.E.2d 560. Lowe's primary argument is foreclosed by Meijer and the BTA correctly

declined to adopt the Costello Report deliberately excluding any "build-to-suit" or "leased fee"

sales or rents, and valuing the property as if vacant. Just as in Meijer, Lowe's failed to meet its

burden of proof on appeal to this Court and the BTA's decision must be affirmed.

REPLY TO PROPOSITION OF LAW NO . 1:

Lowe's "leased fee" argument was rejected in Meijer and no adjustment isrequired for "leased fee" sales.

Lowe's advances a similar (if not ideritical) argument made by Meijer in Meijer that the

Blosser Report should be rejected as valuing the "leased fee" rather than "fee simple" interest in

the Subject Property. Furthermore, while Lowe's acknowledges that consideration of "leased

fee" sales is appropriate pursuant to Meijer, it suggests that such sales must be adjusted to

account for the subject's owner-occupied "fee simple" status as of the applicable lien date.

Taken either separately or together, both of these arguments are foreclosed by Meijer.

In Meijer, this Court considered the valuation of a newly constructed Meijer store with

competing appraisals presented by Meijer and the board of education that bear striking

similarities to the appraisals at issue herein. Meijer, supra, at ¶ 1. Meijer's appraiser valued the

property as vacant or as occupied by a second-generation user whereas the board of education's

appraiser valued it as if Meijer was occupying it. Id. at ¶¶ 7-8. The Court aptly summarized the

differences between each appraiser's selection of comparables in the sales comparison and

income approaches as follows:

The selection of other properties as comparables bears out this general point of

6

contrast. For his sales comparison approach, Lorms [Meijer's appraiser] usedeight properties that included four Kmarts that had been abandoned by that entityduring its bankruptcy, two Ames stores that had also been abandoned duringbankruptcy, a WalMart abandoned by the retailer when it moved into a newsupercenter, and a Sam's Club that `went dark' in 1995 and took five years to sell.On the other hand, Koon's [the board of education's appraiser] comparableproperties included seven properties, four of which were purchased subject tolong-term leases. Koon opined that the value of the Meijer store is `at some pointwhich lies somewhere between selling prices of properties which are leased tofirst generation users *** and prices of properties which are vacant and availablefor occupancy.

Similar differences pervade the rent comparables used by the two appraisers.Lorms used a`market rent' approach that deliberately excluded data derived frombuild-to-suit leases and newly developed discount stores because under Lorm'stheory, the rent in such cases reflected values other than the market rent thatpertained to the fee-simple estate. Koon took the contrary approach: by viewingMeijer itself as the potential lessee of the property, Koon justified using sevenfirst-generation properties and five second-generation properties as rentcomparables. The first-generation comparables were all build-to-suit properties.

Id. at ¶¶ 9-10.

The Court rejected Meijer's two principal arguments: that the board of education's

appraiser valued the "leased fee" rather than the "fee simple" estate; and that such appraisal

constituted a constitutionally prohibited "value-in-use" appraisal. Regarding the "leased fee"

argument that Lowe's raises here, the Court recognized that Meijer was owner-occupying the

property without a lease as of the applicable lien date. Id. at ^ 23. It rejected Meijer's contention

that the valuation of the "fee simple" estate required valuing the property as vacant:

Although Meijer's property is currently not encumbered with a lease, Meijer'scontention that its property cannot be compared to build-to-suit properties ismistaken. As recent cases have demonstrated, the possibility of encumbering aproperty like the one at issue here constitutes - as a purely factual matter - onemethod of realizing the value of legal ownership of the property. See CumminsPropeNty Servs., L.L.C. v. Franklin CtJ>. Bd of Revisi.on, 117 Ohio St. 3d 516,2008-Ohio-1473, 885 N.E.2d 222, ^ 27 ("encumbering property typicallyrepresents an owner's attempt to realize the full value of the property"); AEI NetLease Income & Growth Fund, 119 Ohio St. 3d 563, 2008-Ohio-5203, 895

7

N.E.2d 830, ¶ 21 (sale-leaseback, in its totality, constituted an arm's-lengthtransaction in which seller/lessee and buyer/lessor each pursued the objective torealize value of the realty). Moreover, by drawing the distinction between `feesimple' and `leased fee,' Meijer predicates its argument on a legal premise thatour cases have rejected. We have held that a recent aYna's-length sale priceshould not be adjusted to remove the economic effect ofsuch encumbrances whenthey exist. And we have also determined that a sale price does not have to beadjusted to remove the effect of above-fnarket rent paid by a creditworthy tenant.It follows that an appraiser, when determining the value of a Meijer's store, maytake into account the possibility that at some point, the store could be held as arental property subject to an above-market lease that would enhance its value.

Id. (emphasis added). Moreover, the Court specifically rejected the distinction between "leased

fee" and "fee simple" invoked by appraisers and appraisal methodology:

The distinction between the `fee simple' and `leased fee' is one drawn in thecontext of appraisal practice. See Appraisal Institute, The Appraisal of Real Estate(13' Ed. 2008). The appraisal industry uses the term `fee simple' to refer tounericumbered property - or to property appraised as if it were unencumbered. Id.This distinction is not one recognized by the law, however. A`fee simple' maybe absolute, conditional, or subject to defeasance, but the mere existence ofencumbrances does not affect its status as fee simple. Black's Law Dictionary (8^'Ed. 2004) 648-649.

Id at¶23,n.4.

Here, Lowe's alleges that Ms. Blosser should have adjusted any "leased fee" or "build-to-

suit" comparables utilized in her report since the Subject Property was not leased to Lowe's as of

the applicable lien date. But as this Court directly held in Meijer, such adjustment is not

warranted by law, even if required by appraisal methodology. Id. at ¶ 23. Since this Court has

held that sales need not be adjusted to remove the economic effect of encumbrances, or above-

market leases, Ms. Blosser was not required to adjust her sales or rents as she was authorized to

consider "the possibility, that at some point, the store could be held as a rental property subject to

8

an above-market lease that would enhance its value."I Id. Accordingly, Lowe's first proposition

of law is without merit.

REPLY TO PROPOSI'I'ION OF LAW NO. 2:

The BTA's decision does not violate the Equal Protection Clause.

Next, Lowe's contends that the BTA's decision violates its equal protection rights under

the Ohio and Federal Constitutions because the decision appears facially inconsistent with

another recent decision in Rite Aid of Ohio, Inc. v. Washington Cty. Bd of Revision, BTA No.

2011-1760, 2014 Ohio Tax LEXIS 2541 (Apr. 22, 2014), unreported. In the real property

taxation context, the Court has recognized that the Equal Protection Clause is violated when

property within the same class is undervalued, and that such undervaluation was "intentional and

systematic." Meyer et al. v. Cuyahoga Cty. Bd. of Revision, 58 Ohio St. 2d 328, 334, 390 N.E.2d

796 (1979), citing Southern Railway Co. v. Watts, 260 U.S. 519 (1923). Regarding consistency

between the BT'A's decisions, the Court recently stated:

We have hrmly rejected arguments that the BTA must act consistently whenevaluating evidence of value, even when the evidence goes to value of the sameproperty in different tax years. See Olmstead Falls Bd. of Edn. v. Ctayahoga Cty.Bd of Revision, 122 Ohio St. 3d 134, 2009-Ohio-2461, 909 N.E.2d 597, ¶ 24-25.Although `consistency in the manner of evaluating evidence is desirable,' `theconcern for consistency is overridden by the imperative that the BTA correctlydetermine value in the case before it." Id. at ¶25.

Health Care REIT, Inc. v. Cuyahoga Cty. Bd of Revision, 1.40 Ohio St. 3d 30, 2014-Ohio-2574,

14 N.E.3d 1009, ¶ 49 (emphasis in original).

1 To the extent that Lowe's is arguing that the recent revisions to R.C. 5713.03 to value the "unencumbered" feesimple require the Court to value the Subject Property as vacant; the revisions do not apply to this tax year 2010case when Lowe's filed the complaint in 2011 and the General Assembly had not yet enacted the revisions. SeeColurnbus City Schools v. Franklin Cty. Bd. af Revision, 134 Ohio St. 3d 529, 2012-Ohio-5680, 983 N.E.2d 1285, ¶28 (applying version of R.C. 5713.03 in effect "when the case arose"). Even if they did apply, the Court has alreadyrejected the appraisal industry's use of the term that Lowe's relies upon here. See Meyer, supra, at ¶ 23.

9

Here, Lowe's equal protection and consistency argument fails for a number of reasons.

First, the BTA's decision in Rite Aid, supra, is not a final decision and is currently pending in the

Court on appeal. See Rite Aid of Ohio, Inc. v. Washington Cty. Bd of Revision, Case No. 2014-

0828 (filed May 21, 2014). Second, even if it was a final decision, the BTA need not act

consistently wlien evaluating different appraisals for different properties, even if such appraisals

are similar. Health Care REIT, supra, at ¶ 49. Although the Costello Report is similar to Rite

Aid's appraisal, it is not identical. Ms. Costello intentionally and deliberately excluded sales and

rent cornparables of all frst-generation big boxes whereas Mr. Hatcher included (although

admittedly did not rely upon) several first-generation Rite Aid rents in neighboring West

Virginia. Finally, Lowe's falls well short of establishing a violation of the Equal Protection

Clause. Aside from failing to establish any "intentional or systematic" action of the BTA, it is

not alleging undervaluation resulting from the BTA's decision in. Rite Aid, but instead is alleging

proper valuation that should be applied here. Accordingly, Lowe's second proposition of law

must be rejected.

REPLY TO PROPOSITION OF LAW NO. 3:

Ms. Blosser did not violate USPAP or state law regarding the preparation ofthe Blosser Report.

In its third proposition of law, Lowe's alleges that Ms. Blosser violated the Uniform

Standards of Appraisal Practice ("USPAP") or state law in preparing her report with assistance

of a licensed real estate appraiser assistant and by conducting a telephone conversation with a

market participant without a current real estate broker's or salesperson's license. Such

allegations are unfounded.

Ms. Blosser did not violate USPAP in permitting the assistance of a licensed real estate

10

appraiser assistant in authoring the Blosser Report. Pursuant to R.C. 4763.01, a "state-registered

real estate appraiser assistant means any person, other than a state-certified general real estate

appraiser, state-certified residential real estate appraiser, or a state-licensed residential real estate

appraiser, who satisfies the registration requirements of this chapter for participating in the

development and preparation of real estate appraisals and who holds a current and valid

registration or renewal registration issued to the person pursuant to this chapter." R.C.

4763.01(0) (emphasis added). Ms. Blosser testified at the BT'A hearing that Ms. Hamilton, in

addition to being a registered real estate appraiser assistant, was in the process of obtaining her

state certification as an appraiser and was very close to obtaining certification. See BTA H.R. at

p. 113:19-25; 114:1-3. Additionally, Ms. Blosser directly supervised Ms. Hamilton and

confirmed that Ms. Hamilton did not engage in any activities outside of the scope of her license

as a registered assistant. Id. at p. 142:20-25; 143:1-6.

Furthermore, Lowe's failed to cite any provision of USPAP or the Revised Code that

requires a state-certified general real estate appraiser to conduct market participant interviews

with licensed real estate brokers or salespersons. Ms. Blosser testified that it was not typical for

an appraiser to conduct research regarding the licensure of a market participant and that she had

no reason to believe that such persons were not knowledgeable of the local market or that their

opinions were inaccurate or incorrect. Id. at p. 143:12-21. Accordingly, Lowe's third proposition

of law must be rejected.

REPLY TO PROPOSITION OF LAW NO. 4:

The BTA was not required to independently determine value as it properlyadopted the Blosser Report as competent and probative evidence of value.

Although somewhat puzzling, Lowe's appears to suggest in its fourth proposition of law

11

that the BTA was required to perform an independent valuation of the Subject Property. The

Court's decision in Dublin City Schools Bd. of Edn. v. Franklin Cty. Bd. of Revision, 139 Ohio

St. 3d 212, 2014-Ohio-1940, 11 N.E.2d 222, is inapposite. Both parties here presented

appraisals at the BTA on appeal and neither party seeks reinstatement of the Auditor's original

valuation, Regarding the BTA's duty to review competing appraisals, the Court has held:

The weighing of evidence and the granting of credibility as regards both of theappraisals are the statutory job of the BTA. Fawn Lake Apts. v. Cuyahoga Cty.Bd ofRevision, 75 Ohio St. 3d 601, 603, 665 N.E.2d 194 (1996). When it reviewsappraisals, the BTA is vested with wide discretion in determining the weight to begiven to the evidence and the credibility of the witnesses that come before it.Cardinal Fed. S. & L. Assn. v. Cuyahoga Cty. Bd. qf Revision, 44 Ohio St. 2d 13,336 N.E.2d 433 (1975), at syllabus ¶ 3. This court determined in R.R.Z. Assoc. v.Cuyahoga Cty. Bd of Revision, 38 Ohio St.3d 198, 201, 527 N.E.2d 874 (1988),that `[t]he BTA need not adopt any expert's valuation.'

EOP-BP Tower, L.L.C. v. Cuyahoga Cty. Bd, of Revision, 106 Ohio St. 3d 1, 2005-Ohio-3096,

829 N.E.2d 686, ¶ 9.

As vested with wide discretion in reviewing competing appraisals for the Subject

Property, the BTA properly adopted the Blosser Report. It concluded that the Blosser Report

was more probative of value as it included "leased fee" and "build-to-suit" properties with proper

adjustment for location. See BTA Decision at p. 2; see also Meijer, supra, at ¶ 23. By

"intentionally excluding first-generation users and long-term leased build-to-suit properties

within her two approaches, Costello has not properly analyzed the market, potentially skewing

her analysis." Id. This finding is entitled to the Court's deference and will not be overturned on

appeal unless such finding was so unreasonable that it constitutes an abuse of the BTA's

discretion. For the aforementioned reasons, the BTA did not abuse its discretion in adopting the

Blosser Report.

12

CONCLUSION

The BTA's decision should be affirmed as Lowe's failed to meet its burden to prove that

the BTA abused its discretion in adopting the Blosser Report. The Costello Report does not

comply with Meijer in its deliberate exclusion of "leased fee" and "build-to-suit" properties that

are appropriate for valuing a first-generation big box property, which the Subject Property was as

of the applicable lien date. Lowe's arguments are without merit and must be rejected.

Therefore, the County Appellees respectfully request that this Honorable Court affirm the BTA's

decision for tax year 2010 and carried forward according to law.

Respectfully Submitted,

Ke11ey A. Gorry ( 079210)James R. Gorry (0032461)Rich & Gillis Law Group, LLC6400 Riverside Drive, Suite DDublin, OH 43017PH: (614) 228-5822FAX: (614) 540-7476kgorry c,r richgillislawgroup.comAttorneys for Appellees Washington CountyAuditor and Board of Revision

CERTIFICATE OF SERVICE

I hereby certify that a true and complete copy of the foregoing Merit Brief was served, byregular U.S. Mail, postage prepaid, upon: Ryan J. Gibbs, Esq., The Gibbs Firm, LPA, 2355Auburn Ave., Cincinnati, OH 45219; and the Honorable Michael DeWine, Esq., Ohio AttorneyGeneral, 30 East Broad Street, 17th Floor, Columbus, OH 43215, this 27th day of Octfiftr, 2014.

13

Attorney for Appellees

IN 1 IIE SUPREME COUI2 T®E OHIO

LOWE'S HOME CENTERS, INC.,

Appellant,

V.

WASHINGTON COUNTY BOARD OFREVISION, et al.,

Appellees.

Case No. 2014-0843

Appeal from Ohio Board of Tax AppealsBTA Case No. 2011-1664

APPENDIX

Kelley A. Gorry (0079210)COUNSEL OF RECORDJames R. Gorry (0032461)Rich & Gillis Law Group, LLC6400 Riverside Drive, Suite DDublin, OH 43017PH: (614) 228-5822FAX: (614) 540-7476kgorry(̂7a,richgillislawgroup.comAttorneys for Appellees WashingtonCounty Auditor and Board of Revision

Ryan J. Gibbs (0080331)Geoffrey N. Byrne (0090906)The Gibbs Firm, LPA2355 Auburn AvenueCincinnati, 01-145219PH: (513) 381-3890FAX: (866) 796-3717Attorneys for AppelZant Lowe 's HomeCenters, Inc.

The Honorable Michael DeWine (0009181)Ohio Attorney General30 East Broad Street, 17 th FloorColumbus, OH 43215PH: (614) 466-4986Attorney for Appellee Ohio TaxCommissioner

TABI.E OF CONTENTS

Notice of Appeal .....................

BTA Decision .........................

BOR Decision .........................

Statutes:

R. C . 47610101 ...... . . .. ... ... . .. ..... .. .

R.C. 5713.03 ......:.....................

........................................._.....................see Appellant's Appendix

............................................................... see Appellant's Appendix

......................................................................................................3

...........................4

......... ...................6

2

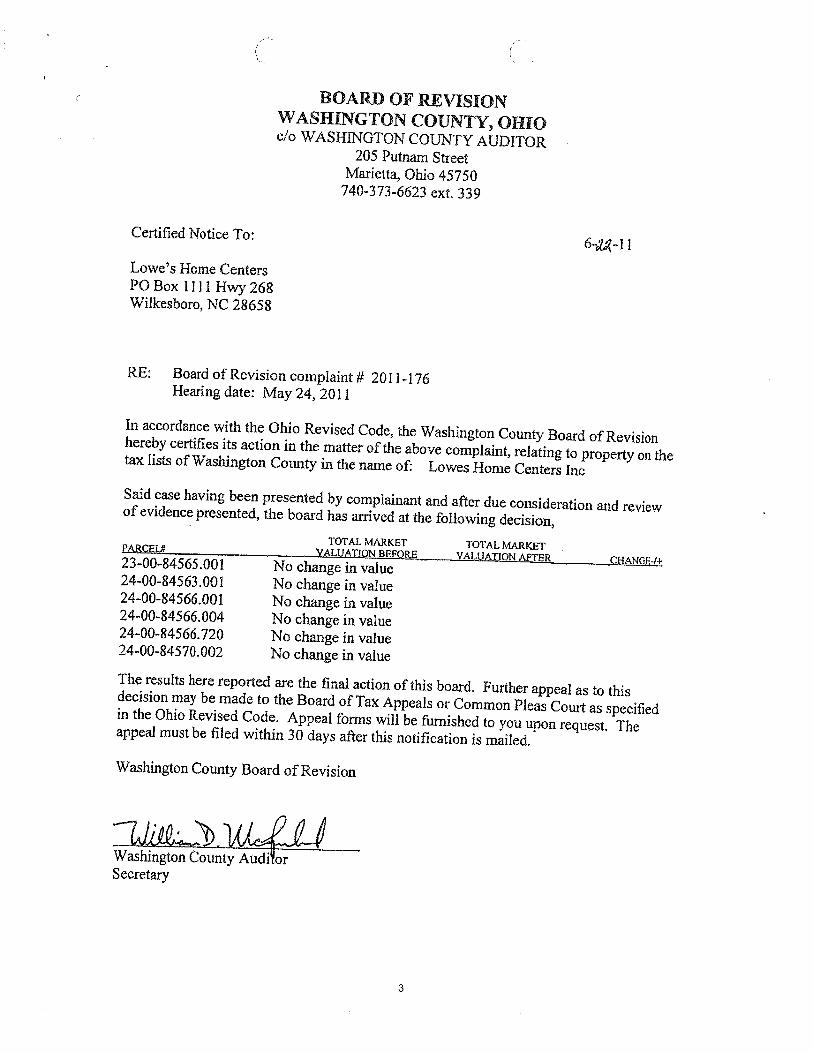

BOARD OF REVISIONWASHINGTON COUNT" i y OHIOc!o WASHINGTON COUNTY AUDITOR

205 Putnam StreetMarietta, Ohio 45750

740-373-6623 ext. 339

Certified Notice To:

Lowe's Home CentersPO Box IIII Hwy 268Wilkesboro, NC 28658

RE: Board of Revision complaint # 2011-176Hearing date: May 24, 2011

6 -dA -11

In accordance with the Ohio Revised Code, the Washington County Board of Revisionhereby certifies its action in the matter of the above complaint, relating to property on thetax lists of Washington County in the name of- Lowes Home Centers Inc

Said case having been presented by complainant and after due consideration and reviewof evidence presented, the board has arrived at the following decision,

TOTAL MARKET TQTAL RRARKETpAR EL4 vALUATIQ BEFC}RE VALUATI®N AFTER23-00-84565.001 No change in value cnArrcE-i+24-00-84563.001 No change in value24-00-84566.001 No change in value24-00-84566.004 No change in value24-00-84566.720 No change in value24-00-84570.002 No change in value

The results here reported are the final action of this board. Further appeal as to thisdecision may be made to the Board of Tax Appeals or Common Pleas Court as specifiedin the Ohio Revised Code. Appeal forms will be furnished to you upon request. Theappeal must be filed within 30 days after this notification is mailed.

Washington County Board of Revision

Washington County Audi orSecretary

Lawriter - ORC - 4763.0I Real estate appraiser definitions.

4763.01 Real estate appraiser definiti ns.

As used in this chapter:

Page 1 of 2

(A) "Real estate appraisal" or "appraisal" means an analysis, opinion, or conclusion relating to the

nature, quality, value, or utility of specified interests in, or aspects of identified real estate that isclassified as either a valuation or an analysis.

(8) "Valuation" means an estimate of the value of real estate.

(C) "Analysis" means a study of real estate for purposes other than valuation.

(D) "Appraisal report" means a written communication of a real estate appraisal, appraisal review, or

appraisal consulting service or an oral communication of a real estate appraisal , appraisal review, or

appraisal consulting service that is documented by a writing that supports the oral communication.

(E) "Appraisal assignment" means an engagement for which a person iicensed or certified undar this

chapter- is employed , retained, or angaged to act, or would be perceived by third parties or the public

as acting, as a disinterested third party in rendering an unbiased real estate appraisal.

(F) "Specialized services" means all appraisal services, other thari appraisal assignments, including,

but not limited to, valuation and analysis given in connection with activities such as real estate

brokerage, mortgage banking, real estate counseling, and real estate tax counseling, and specializedmarketing, financing, and feasibility studies.

(G) "Real estate" has the same meaning as in section 4735.01 of the Revised Code.

(H) "Appraisal foundation" means a nonprofit corporation incorporated under the laws of the state of

Illinois on fVovember 30, 1987, for the purposes of establishing and improving uniferm appraisal

standards by defining, issuing, and promoting ti-iose standards; establishing appropriate criteria for the

certification and recertification of qualified appraisers by defining, issuing, and promoting the

qualification criteria and disseminating the qualification criteria to others; and developing or assisting

in development of appropriate examinations for qualified appraisers.

(I) "Prepare" means to develop and communicate, whether through a personal physical inspection or

through the act or process of critically studying a report prepared by another who made the physical

inspection, an appraisal, analysis, or opinion, or specialized service and to report the results. If the

person who develops and communicates the appraisal or specialized service does not make the

personal inspection, the name of the person who does make the personal inspection shall be identifiedon the appraisal or specialized service reported.

(1) "Report" means any communication, written, oral, or by any other means of transmission of

information, of a real estate appraisal, appraisal review, appraisal consulting service, or specialized

service that is transmitted to a client or employer upon completion of the appraisal or service.

(K) "State-certified general real estate appraiser" means any person who satisfies the certification

requirements of this chapter relating to the appraisal of all types of real property and who holds a

current and valid certificate or renewal certificate issued to the person pursuant to this chapter.

(L) "State-certified residential real estate appraiser" rneans any person who satisfies the certification

requirements only relating to the appraisal of one to four units of single-family residential real estate

4iittp://codes.ohio.bov/orc/4763.01 10/24/2014

Lawriter -OR.C - 4763.01 Real estate appraiser definitions. Page 2 of 2

without regard to transaction value or complexity and who holds a current and valid certificate or

renewal certificate issued to the person pursuant to this chapter.

(M) "State-licensed residential real estate appraiser" means any person who satisfies the licensure

requirements of this chapter relating to the appraisal of noncomplex one-to--four unit single-family

residential real estate having a transaction value of less than one million dollars and complex one-to-

four unit single-family residential real estate having a transaction value of less than two hundred fifty

thousand dollars and who holds a current and valid license or renewal license issued to the personpursuant to this chapter.

(N) "Certified or licensed real estate appraisal" means an appraisal preparec, and reported by a

certificate holder or licensee under this chapter acting within the scope of certification or iicensu,-e andas a disinterested third party.

(0) "State-registered real estate appraiser assistant" means any person, other than a state-certified

general real estate appraiser, state-certified residential real estate appraiser, or a state-licensed

residential real estate appraiser, who satisfies the registration requirements of this chapter for

participating in the development and preparation of real estate appraisals and whc3 holds a current and

valid registration or renewal registration issued to the person pursuant to this chapter.

(P) "Institution of higher education" rneans a state university or college, a private college or university

located in this state that possesses a certificate of authorization issued by the 0•hiQ board of regents

pursuant to Chapter 1713. of the Revised Code, or an accredited college or university located outside

this state that is accredited by an accrediting organization or professional ac:crediting association

recognized by the Ohio board of regents.

(Q) "Division of real estate" may be used interchangeably with, and for all purposes has the same

meaning as, "division of real estate and professional licensing."

(R) "Superintendent" or "superintendent of real estate" means the supe-intendent of the division of

real estate and professional licensing of this state . Whenever the division or superintendent of real

estate is referred to or designated in any statute, rule, contract, or other docurnent, the reference or

designation shall be deemed to refer to the division or superintendent of real estate and professional

licensing, as the case may be.

(S) "Appraisal review" means the act or process of developing and communicati.pg an opinion about

the quality of another appraiser's work that was performed as part of an appraisal, appraisal review, or

appraisal consultina assignment.

(T) "Appraisal consulting" means the act or process of developing an analysis, recommendation, oropiniori to solve a problem related to real estate.

(U) "Work file" means documentation used during the preparation of an appraisal report or necessary

to support an appraiser's analyses, opinions, or conciusions.

Amended by 128th General AssemblyFile No.9, HB 1, §101.01, eff. 10/16/2009.

Effective Date: 06-30-1997

5

http://codes.ohio.gov/orc/47b3.01 10/24/2014

Lawriter - ORC -5713.03 County auditor to determine taxable value of real property. Page 1 of 1

5713v03 County auditor to determine taxab1e value of r°ealproperty.

The county auditor, from the best sources of information available, shall determine, as nearly as

practicable, the true value of the fee simple estate, as if unencumbered but subject to any effects from

the exercise of police powers or from other governmental actions, of each separate tract, lot, or parcel

of real property and of buildings, structures, and improvements located thereon and the current

agricultural use value of (and valued for tax purposes in accordance with section 5713.31 of the

Revised Code, in every district, according to the rules prescribed by this chapter and section 5715.01

of the Revised Code, and in accordance with the uniform rules and methods of valuing and assessing

real property as adopted, prescribed, and promuigated by the tax commissioner. The auditor shall

determine the taxable value of all real property by reducing its true or current agricultural use value by

the percentage ordered by the commissioner. In determining the true value of any tract, lot, or parcel

of real estate under this section, if such tract, lot, or parcel has been the subject of an arm's length

sale between a willing seller and a willing buyer within a reasonable length of time, either before or

after the tax lien date, the auditor may consider the sale price of such tract, lot, or parcel to be the

true value for taxation purposes. However, the sale price in an arm's length transaction between a

willing seller and a willing buyer shall not be considered the true value of the property sold ifsubsequent to the sale:

(A) The tract, lot, or parcel of real estate loses value due to some casualty;

(B) An improvement is added to the property. Nothing in this section or section 5713.01 of the Revised

Code and no rule adopted under section 5715.01 of the Revised Code shall require the county auditor

to change the true value in money of any property in any year except a year in which the tax

commissioner is required to determine under section 5715.24 of the Revised Code whether theproperty has been assessed as required by law.

The county aiaditor shall adopt and use a real property record approved by the commissioner for each

tract, lot, or parcel of real property, setting forth the true and taxable value of land and, in the case ofland valued in accordance with section 5713.31 of the Revised Code, its current agricultural use value,ttie number of acres of arable land, permanent pasture !and, woodland, and wasteland in each tract,

lot, or parcel. The auditor shall record pertinent information and the true and taxable value of each

building, structure, or improvement to land, which value shall be included as a separate part of thetotal value of each tract, lot, or parcel of real property.

Amended by 129th General AssemblyFile No.186, HB 510, §1, eff. 3/27/2013.

Amended by 129th General AssemblyFile No.127, HB 487, §101.01, eff. 9/10/2012.

Effective Date: 09-27-1983

Related Legislative Provgscone See 129th General AsserrmblyFile No.186, HB 510, §3

See 129th General AssemblyFile No.127, NB 487, §757.51.

6

http://codes.ohio.gov/orc/5 713.03 10,%24/2014