Boa Offshore April 2013 Helge Kvalvik, CEO presentation is made by Boa Offshore ... is making any...

31

Boa Offshore April 2013 Helge Kvalvik, CEO

-

Upload

truongdien -

Category

Documents

-

view

218 -

download

3

Transcript of Boa Offshore April 2013 Helge Kvalvik, CEO presentation is made by Boa Offshore ... is making any...

Boa Offshore April 2013

Helge Kvalvik, CEO

This presentation is made by Boa Offshore (or the ”Company”). The information contained herein

include statements that are ”forward-looking” in their nature. These forward-looking statements include

all matters that are not historical facts and are based on the Company’s current intentions, believes

and expectations about among other things, the Company’s results of operations, financial condition,

prospects, growth, strategies and the industry in which the Company operates. Such forward-looking

information and statements reflect current views with respect to future events. The Company cannot

give any assurance as to the correctness of information and statements related to such future events.

Furthermore, these forward-looking statements involve known and unknown risks, uncertainties and

other factors that are in many cases beyond the Company’s control that could cause the actual results

of operations, financial condition, liquidity and the development of the industry in which the Company’s

businesses operate to differ materially from the impression created by the forward-looking statements

contained herein, because they relate to events and depend on circumstances that may or may not

occur in the future. Although the Company believes that its intentions, beliefs and expectations, and

the statements in this presentation, are based on reasonable assumptions as of today, the Company

can not give any assurance that the actual results will be as set out in this presentation. Financing the

Company involves risks, and several factors could cause the actual results, performance or

achievements of the Company to be materially different from the impression created by the forward-

looking statements contained herein. Neither the Company, nor any company within the Boa Offshore

Group, is making any representation or warranty (express or implied) as to the accuracy, reliability or

completeness of the information and statements in this presentation, and neither the Company, any

company within the Boa Group, nor any of their directors, officers or employees will have any liability

to any persons resulting from the possible use of information in the presentation.

Disclaimer

2

5 Market overview and outlook

3 Financials

2 Boa Offshore overview

4 Boa Offshore Subsidiaries

Contents

3

1 Boa Offshore summary

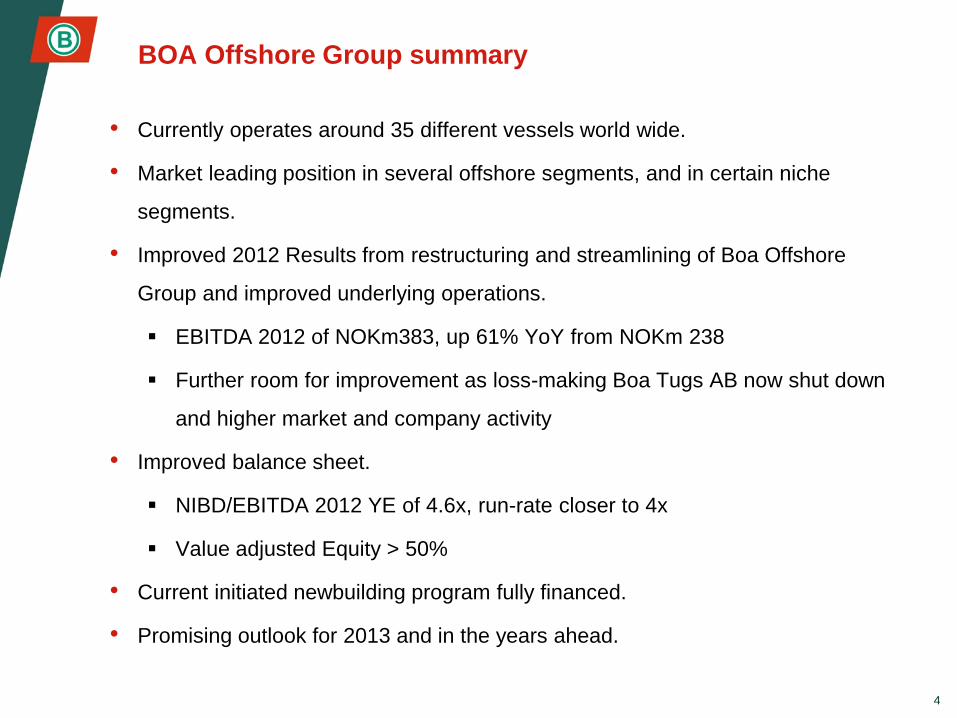

BOA Offshore Group summary

• Currently operates around 35 different vessels world wide.

• Market leading position in several offshore segments, and in certain niche

segments.

• Improved 2012 Results from restructuring and streamlining of Boa Offshore

Group and improved underlying operations.

EBITDA 2012 of NOKm383, up 61% YoY from NOKm 238

Further room for improvement as loss-making Boa Tugs AB now shut down

and higher market and company activity

• Improved balance sheet.

NIBD/EBITDA 2012 YE of 4.6x, run-rate closer to 4x

Value adjusted Equity > 50%

• Current initiated newbuilding program fully financed.

• Promising outlook for 2013 and in the years ahead.

4

5 Market overview and outlook

3 Financials

2 Boa Offshore overview

4 Boa Offshore Subsidiaries

Contents

5

1 Boa Offshore summary

Boa Offshore in short

• Boa Group and Boa Offshore is controlled by Ole T. Bjørnevik and his family.

• Boa Offshore currently operates and manages a fleet of approximately 35 units in various segments.

• Performs the technical, commercial and operational tasks on behalf of all its subsidiaries, with approximately 350 employees.

• Main activities/exposure include:

Subsea installation and construction (OCV/BMSI)

Seismic EM vessel operations (SBL)

Sea transportation and load-out and launching of heavy objects (Barges/BMSI)

Rig moves (NFDS/AHTS)

Harbor and costal towage (Tugs)

Salvage operations (Tugs)

• Global presence and operations.

• Leading player in the global market for heavy lift barges.

• Head Office in Trondheim/Norway, and offices in Houston/USA and Gdynia/Poland.

• Fleet value of NOKbn 3.6 YE 2012 (Excl newbuilds).

• YE 2012 NIBD NOKbn 1.8.

6

7

Boa office

Geographical presence

Houston

, USA

Trondheim,

Norway

• OCVs on contract in West Africa

and Asia/Australia

• Tugs located in North Europe

• Two heavy lift, semi submersible

barges in GoM

• Two large heavy lift, semi

submersible barges in Australia

• SBL EM vessels in Brazil & Asia

Site offices,

China

Gdynia,

Poland

Global presence

Overview of business segments

Tugs Barges Offshore Vessels

• 1 voith escort tug

• 4 ASD escort tugs

• 4 harbour / towage tugs

• 2 harbour tugs

• 8 semisubmersible barges

• 7 deck cargo barges

• 2 other barges

• Options for more new barges

• OCV – Boa Sub C

• OCV – Boa Deep C

• SBL – Boa Thalassa

• SBL – Boa Galatea

• New building program

Mid-Norway and North Sea operations

Tugs has been the primary business of Boa since inception

Revitalization of this business segment with a substantial fleet renewal 2010-2012

World Wide operations

Leading player in the global heavy lift market

Continuous new building program since 1999

World wide operations

Ongoing modernization of the fleet, incl NFDS

Successfully owns and operates two of the world’s most high spec OCVs

Tonnage provider and solution/ project provider for:

• Salvage operations

• Turn key towage / transport / handling operations

Tonnage provider, also solution/ project provider for:

• All engineering related to barges. In house design

• Turn key transportation projects

• Load out and launching

• Dry docking operations

• Float over

BMSI, also solution/ project provider for:

• SURF (subsea, umbilicals, risers and flowlines)

• IRM (inspection, repair and maintenance) of platforms

• Floater moves and installations

• Also use of 3rd party vessels

8

Assets

D

escri

pti

on

/op

era

tio

ns

76%

Boa Offshore organizational structure*

• Boa OCV owns and operates the offshore construction

vessels Boa Deep C and Boa Sub C.

• Boa SBL owns two modern seismic vessels Boa Galatea

and Boa Thalassa.

• Boa Shipping owns and/or operates several barges and

tugs with a regional focus. The tugs operate as harbor tugs,

salvage tugs, costal and deep sea towage tugs. Boa

Shipping also owns the below subsidiaries:

Boa Barges: World leading barge operator with a fleet

of 10/17 barges (including two newbuilds), also

performing associated project engineering and

management

Taubåtkompaniet: Owns 4 Rampart tugs (operated by

Boa Shipping)

Boa PSV: Owns the two to MPSV newbuilds; Boa

Heron and Boa Pelican, estimated delivery in 2Q and

4Q 2014

NFDS Offshore 1 AS (NOFF 1 AS) is the owner of the

newbuild AHTS Boa Bison to be delivered in 1Q 2014

• Det Nordenfjeldske Dampskibsselskap AS: At present

holding company for NOFF 1 AS. Will consider new vessel

investments with external investors going forward.

• Boa Offshore LLC is a company used for operating vessels

in the US Gulf (Boa Deep C).

Boa Marine Services Inc. (BMSI) is an engineering

and turnkey operator in the Americas

9

Boa Offshore AS

Org. # 926265156

Norway

Boa OCV AS

Org. # 984158939 Norway

Boa SBL AS

Org. # 990899576 Norway

Boa Shipping AS

Org. # 981395697 Norway

Boa Barges AS

Org. # 992982950 Norway

BOA GALATEA BOA THALASSA

Taubåtkompaniet AS

Org. # 992982985 Norway

Boa PSV AS

Org. # 997265459 Norway

Other**

Boa Offshore LLC

US

Boa Marine Services Inc

US

* All companies are 100% owned unless otherwise specified ** See appendix for full details

Det Nordenfjeldske

Dampskibsselskap AS

Org. # 999327826 Norway

NFDS Offshore 1 AS

Org. # 999255108 Norway

76% 100%

of

voting

shares

5 Market overview and outlook

3 Financials

2 Boa Offshore overview

4 Boa Offshore Subsidiaries

Contents

10

1 Boa Offshore summary

Boa Offshore consolidated historical financials

• Boa Offshore has streamlined its

business model, which is now showing

results.

• Boa Offshore 2012 EBITDA increased

61% YoY to NOKm 383.

Corresponding to EBITDA margin of

37%, up from 25% in 2011

Sale of loss making vessels

negatively impacting 2011

2H 12 EBITDA of NOKm 204., up

from NOKm 179. in 1H 12

• Margins excluding loss making Boa Tugs

AB in mid 40s.

Boa Tugs AB now shut down, will

positively impact EBITDA in 2013

and onwards

• Several segments performing very well

with sustained high EBITDA margins.

• Gross interesting bearing debt slightly

reduced to less than NOK 2 bn. and

NIBD maintained at NOK 1.8 bn. despite

payments for newbuilding program during

2012.

11

Boa Offshore key P&L items NOK mill.

Boa Offshore key balance sheet items NOK mill.

Note: NGAAP reported figures

4,138

1,446 1,576

4,134

1,758 1,274

3,9761,768

1,363

0

1,000

2,000

3,000

4,000

5,000

Total assets NIBD Equity

NO

K m

ill.

2010

2011

2012

891

381

167

956

238

(152)

1,038

383100

-200

0

200

400

600

800

1,000

Sales EBITDA Net profit

NO

K m

ill.

2010

2011

2012

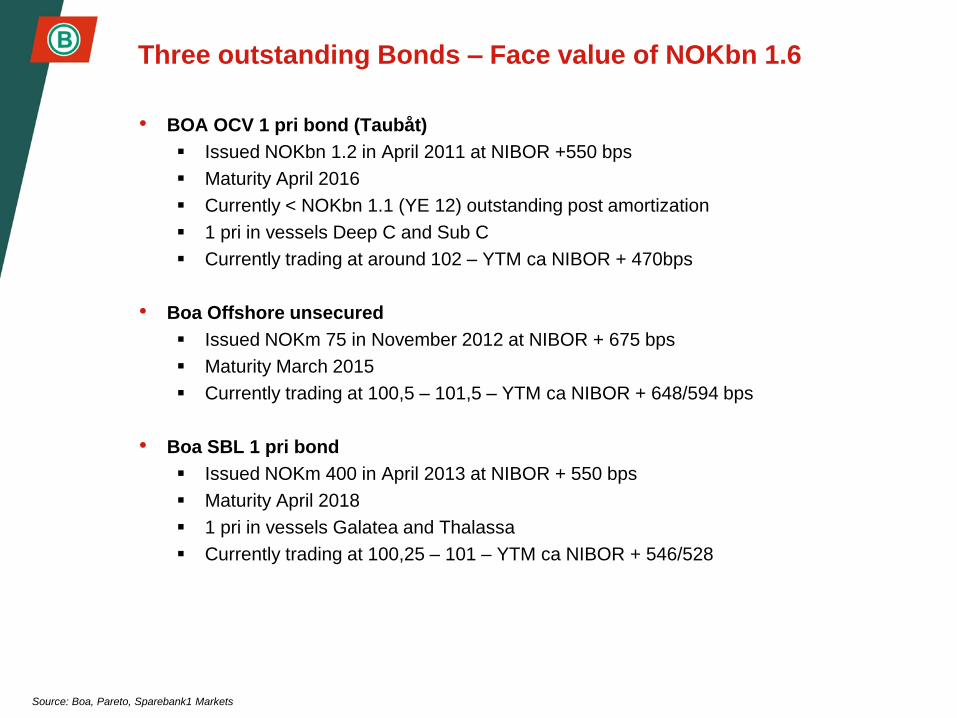

Three outstanding Bonds – Face value of NOKbn 1.6

• BOA OCV 1 pri bond (Taubåt)

Issued NOKbn 1.2 in April 2011 at NIBOR +550 bps

Maturity April 2016

Currently < NOKbn 1.1 (YE 12) outstanding post amortization

1 pri in vessels Deep C and Sub C

Currently trading at around 102 – YTM ca NIBOR + 470bps

• Boa Offshore unsecured

Issued NOKm 75 in November 2012 at NIBOR + 675 bps

Maturity March 2015

Currently trading at 100,5 – 101,5 – YTM ca NIBOR + 648/594 bps

• Boa SBL 1 pri bond

Issued NOKm 400 in April 2013 at NIBOR + 550 bps

Maturity April 2018

1 pri in vessels Galatea and Thalassa

Currently trading at 100,25 – 101 – YTM ca NIBOR + 546/528

Source: Boa, Pareto, Sparebank1 Markets

Key Figures (NIBD/EBITDA, ROA)

• Boa Offshore consolidated with

NIBD/EBITDA 2012 YE of 4.6x.

Current run-rate figure closer to 4x

• The lowest multiple in the Norwegian

supply vessel sector.

• Sector average of around 7x.

NB: 2012 EBITDA figure includes > NOKm 35 P&L

expensed provision for class/periodical maintenance

(NGAAP)

NIBD/EBITDA 2012 Return on Assets* 2012

• Boa Offshore consolidated Return on

Assets* (ROA) on active fleet of >10%.

• Highest in the Norwegian supply vessel

sector.

• Sector average of around 6%.

* = EBIT/ Fixed Tangible Assets adj for newbuilds on

balance sheet

Source: Boa, Company Reports

Boa Offshore initiated newbuild program - fully financed

14

Boa Heron/Pelican MPSV VS 495

Delivery/

Vessel type Design Yard status Debt financing Ownership Other

AHTS #1 – Boa Bison

28,000 bhpVS 491

Norwegian/

China hull1Q 2014

60% commitment from bank,

SpareBank1 SMN/GIEK

NFDS Offshore 1 AS with

24% external investors

600t winch

ROV hangar

AHTS #2

28,000 bhpVS 491

On hold until financing

is in placeBoa Shipping AS

MPSV #1 – Boa Heron VS 495 Chinese 2Q 2014 70% bank, CDB & Sinosure Boa PSV ASTargeted for light construction/

IMR market

MPSV #2 - Boa Pelican VS 495 Chinese 4Q 2014 70% bank, CDB & Sinosure Boa PSV ASTargeted for light construction/

IMR market

Boabarge 34 Boa Chinese Delivered Jan. 2013 SpareBank1 SMN Boa Barges AS 140 m Semi submersible

Boabarge 43 Boa Chinese 2Q 2013 SpareBank1 SMN Boa Barges AS 300 feet Flat top

Boabarge 44 Boa Chinese 2Q 2013 SpareBank1 SMN Boa Barges AS 300 feet Flat top

NFDS AHTS #1 VS 491

5 Market overview and outlook

3 Financials

2 Boa Offshore overview

4 Boa Offshore Subsidiaries

Contents

15

1 Boa Offshore summary

Boa OCV: BOA DEEP C

• BOA DEEP C is a specialized offshore

construction vessel designed by Vik-

Sandvik (VS 4201) and built at the

Factorias Vulcano Yard in Spain in 2003.

• The vessel is equipped with:

Two WROV hangars

Anchor handling winch

Two secondary winches

Two cranes

Heli-deck

• The vessel has proved operational

excellence with close to full utilization.

• MV estimated at NOKm 900-950.

• Contract till August 2013.

Length overall 120 m

Breadth 27 m

Positioning DP-III

Deck Space 1150 m2

Deck Strength 15 t/m2

Main Crane 250 t

Crane Depth 2000 m

Main Winch 500 t

Bollard Pull 229 t

Accommodation 90-100

Particulars

Source: Boa Offshore, Shipbroker Reports/Valuation 16

Boa OCV: BOA SUB C

• BOA SUB C is a specialized offshore

construction vessel designed for sub sea

construction, including pipe laying.

• The vessel has enhanced capabilities to

manage difficult assignments in particularly

demanding or harsh environments.

• Gross tonnage of 16,500 tons, VS 4201

design, delivered in 2007.

• The vessel is equipped for the following

operations:

Anchor handling (>3000 m dept)

Towing (3 winches at 6/5/500 t)

Mooring

ROV operations (2 ROV hangars)

Heavy lift up to 400 tons (3 cranes)

Helicopter operations

Multifunctional subsea services

• MV estimated at NOKm 1,050-1,150.

• Contract till July 2015 + options.

Length overall 138.5 m

Breadth 30.6 m

Positioning DP-III

Deck Space (free) 1885 m2

Deck Strength 20 t/m2

Main Crane 400 t

Crane Depth 3000 m

Main Winch 600 t

Bollard Pull 220 t

Accommodation 135

Particulars

Source: Boa Offshore, Shipbroker Reports/Valuation 17

SBL 14%

OCV 59%

Barges, tugs

and other 27%

SBL 17%

OCV 56%

Barges, tugs

and other 27%

Boa OCV AS – Summary and key financials

• Account for > 50% of Boa Offshore

values and EBITDA.

• Both vessels are on contracted to EMAS

AMC.

• 2012 EBITDA of NOKm 240.

• NOKm 1,088 gross debt 2012 YE

NIBD NOKm 973

• Shipbrokers average valuation per

December 2012 of NOKm 2,020 for both

vessels.

• LTV year end 2012 of 54/48%.

• Strong outlook for subsea construction

vessels.

• Identified several attractive possibilities

for Deep C from contract expiry August

2013.

• Few vessels in same segment with

matching capacities: crane, deck-space,

DP3, and winch/bollard pull.

And few available before mid 2014

18

Boa OCV AS share of EBITDA* 2012

Boa OCV AS share of fleet value December 2012

Note: NGAAP reported figures *EBITDA before eliminations

Boa SBL - The vessels

• Boa SBL owns two modern seismic vessels

being the world’s first custom built vessels

for electromagnetic seismic; “EM”

• On long term contracts to EMGS

Thalassa firm until December 2014 +

2x12 months options (first option

exercised)

Galatea firm until July 2014 + 3x12

months options

• Total construction costs NOKm 325 each

and average market value (charter free) of

NOKm 305* today.

• Estimated newbuild price today assumed

20% above historical construction cost.

• Although purpose built for EMGS, vessel

design is generic (MT 6000 series) and

vessels can be converted into:

Traditional 3D seismic

OBN/OBC seismic

Survey/ROV support

IMR/light construction

Offshore Wind Farm support 19

Main specifications vessels

Design MT 6007 (Marin Teknikk AS)

Type EM seabed logging vessels

Length (m) 80.35

Beam (m) 16.40

DWT (t) 3,000

Max speed 17 knots

Accommodation 57 persons

DP-system Rolls-Royce DP II

Delivered December 2008 and July 2009 respectively

Yard Bergen Group Fosen, Norway

Class Det Norske Veritas

Flag Cayman Islands

* Source: According to average of two independent shipbroker valuations

Boa SBL - Historical financials

• Boa SBL reported EBITDA of NOKm

57 in 2012.

• Corresponding figures for 2010 and

2011 were NOKm 99 and NOKm 45

respectively.

• The 2010 number was positively

impacted by currency gains, and the

2011 number was negatively impacted

by higher than expected class provision

(level is now adjusted for going

forward).

• Net profit 2012 reported at NOKm 13

• Debt to credit institutions YE 2012

reduced by NOK 47 mill. YoY to NOK

289 mill. Cash reported at NOK 26 mill.

NIBD of NOKm 263

• LTV of 47/43%

• Recently issued April 2013 new NOKm

400 bond to re-finance debt.

20

Boa SBL key P&L items NOK mill.

Boa SBL key balance sheet items NOK mill.

-40

0

40

80

120

160

Sales EBITDA Net profit

NO

K m

ill.

2010

2011

2012

0

100

200

300

400

500

600

700

Total assets NIBD Equity

NO

K m

ill.

2010

2011

2012

21

Boa Barges AS – The barge experts

• BOA has since 1998 had continuous new

building program for barges in China.

• Today operates 10/17 barges of different

size.

• Built up an in-house engineering capacity

that is unique in the industry.

• As from 2002 BOA developed its own in-

house design, giving substantial cost

savings.

• Boa can offer in additional to “the steel”:

• Total turn key projects for

transportation or dry docking

operations by barges

• All engineering services related to

barges

• Hydrostatics & Hydrodynamics

• Structural & Operational

• Engineering and project management

performed from Trondheim and Houston.

Source: Boa Offshore

Boa Tugs and Barges – Summary and key financials

• Boa owns and operates 31 tugs and

barges (including 2 other vessels) in

various subsidiaries within the group.

• 2012 EBITDA for Boa Offshore other

segments at NOKm 108, from NOKm 51

in 2011.

• Shipbrokers valuation per YE 2012 of

NOKm 996.

• Excluding equity paid in AHTS #1 and

MPSV # 1 and 2.

• LT Debt per YE 2012 of NOKm 601.

NIBD of NOKm 533

• Indicative LTV around 60/54%.

• Contracts for most subsidiaries and

assets in the other segments of Boa

Offshore are of a short to medium term

character.

• Market outlook for all of the other

segments are stable to positive.

22

Boa Tugs and Barges share of EBITDA* 2012E

Boa Tugs and Barges share of fleet value Dec. 2012

Note: NGAAP reported figures *EBITDA before eliminations

SBL 14%

OCV 59%

Barges, tugs

and other 27%

SBL 17%

OCV 56%

Barges, tugs

and other 27%

5 Market overview and outlook

3 Financials

2 Boa Offshore overview

4 Boa Offshore Subsidiaries

Contents

23

1 Boa Offshore summary

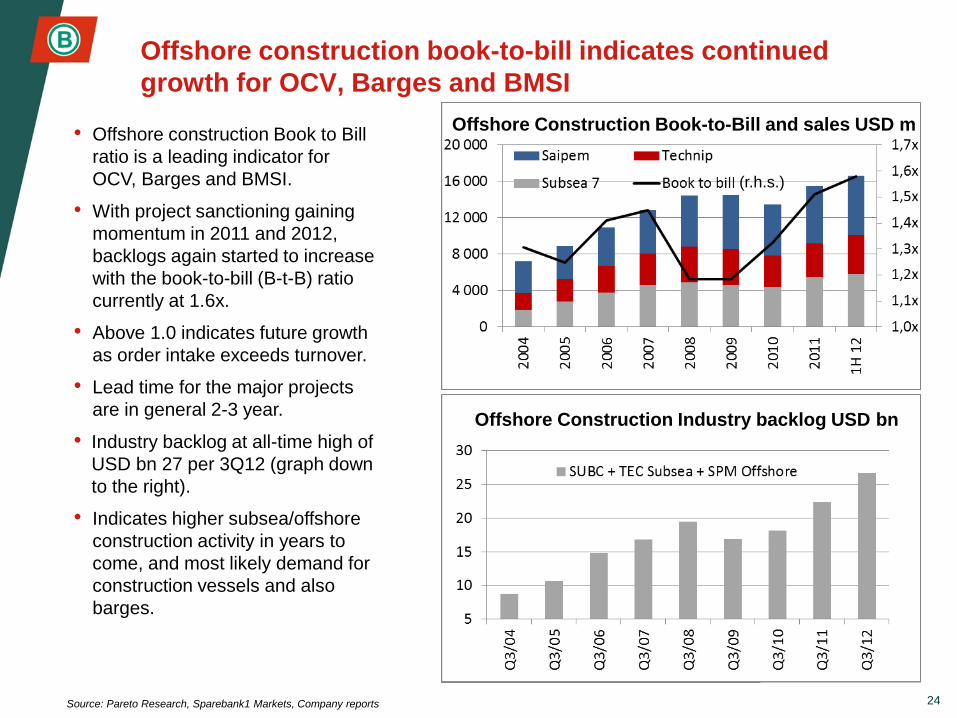

Offshore construction book-to-bill indicates continued

growth for OCV, Barges and BMSI

• Offshore construction Book to Bill

ratio is a leading indicator for

OCV, Barges and BMSI.

• With project sanctioning gaining

momentum in 2011 and 2012,

backlogs again started to increase

with the book-to-bill (B-t-B) ratio

currently at 1.6x.

• Above 1.0 indicates future growth

as order intake exceeds turnover.

• Lead time for the major projects

are in general 2-3 year.

• Industry backlog at all-time high of

USD bn 27 per 3Q12 (graph down

to the right).

• Indicates higher subsea/offshore

construction activity in years to

come, and most likely demand for

construction vessels and also

barges.

24 Source: Pareto Research, Sparebank1 Markets, Company reports

Offshore Construction Book-to-Bill and sales USD m

Offshore Construction Industry backlog USD bn

(r.h.s.)

25 Source: ODS/IHS, Boa Offshore, Sparebank1 Markets, FMC Technologfies/Quest

Strong growth in subsea wells and FPSOs expected:

OCV, BMSI

Subsea tree awards World Wide

• Subsea tree awards and estimated subsea tree installations is a key indicator for vessel activity.

• Number of tree installations likely to increase from an average of around 300 p.a. in 2010-2012 to 500+ within 3-5 years.

• Normally on average 12-24 months lead time from award to installation

• Most important markets are North Sea, Brazil, and West Africa with US GoM and Australia as runners up.

2x

FPSO installations World Wide

• OCV: Boa Sub C and Boa Deep C also well suited for FPS installation due to bollard pull capacity.

• Average number of FPS installations p.a. has been around 20 last 5 years, but was down to 14/18 in 2011/2012.

• Prospect list indicate > 40 per year next five years. Some projects will be postponed/turned down.

• However, 25-30 per year 2013-2016 looks very achievable at present.

• Includes FPSO, FSRU, FSO, Semi, TLP and Spars.

26 Source: ODS/IHS, Boa Offshore, UNO

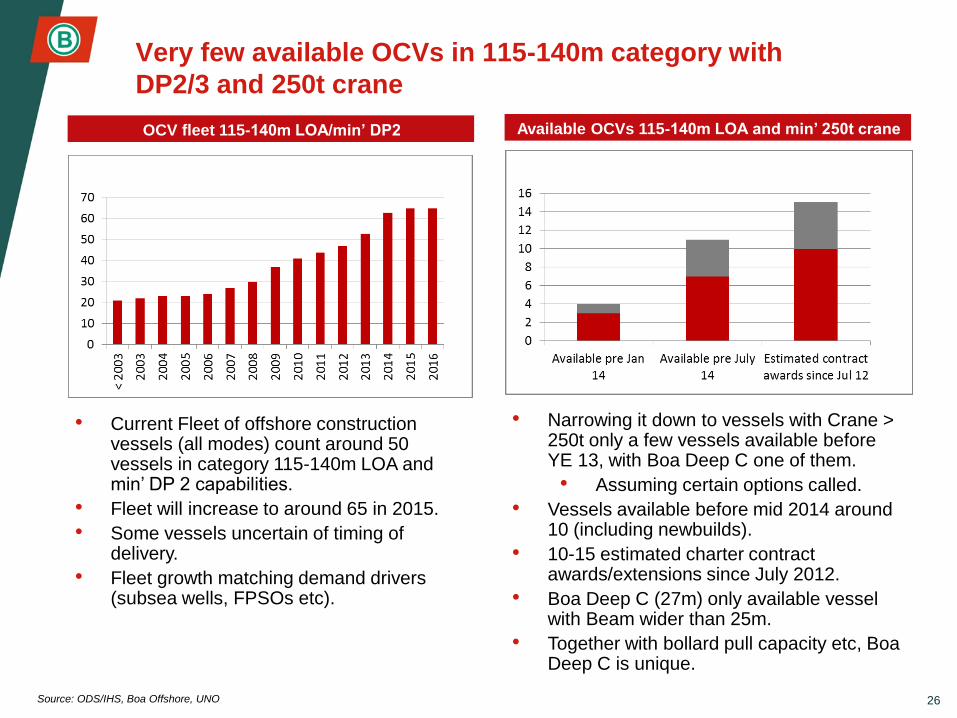

Very few available OCVs in 115-140m category with

DP2/3 and 250t crane

OCV fleet 115-140m LOA/min’ DP2

• Current Fleet of offshore construction vessels (all modes) count around 50 vessels in category 115-140m LOA and min’ DP 2 capabilities.

• Fleet will increase to around 65 in 2015.

• Some vessels uncertain of timing of delivery.

• Fleet growth matching demand drivers (subsea wells, FPSOs etc).

Available OCVs 115-140m LOA and min’ 250t crane

• Narrowing it down to vessels with Crane > 250t only a few vessels available before YE 13, with Boa Deep C one of them.

• Assuming certain options called.

• Vessels available before mid 2014 around 10 (including newbuilds).

• 10-15 estimated charter contract awards/extensions since July 2012.

• Boa Deep C (27m) only available vessel with Beam wider than 25m.

• Together with bollard pull capacity etc, Boa Deep C is unique.

27

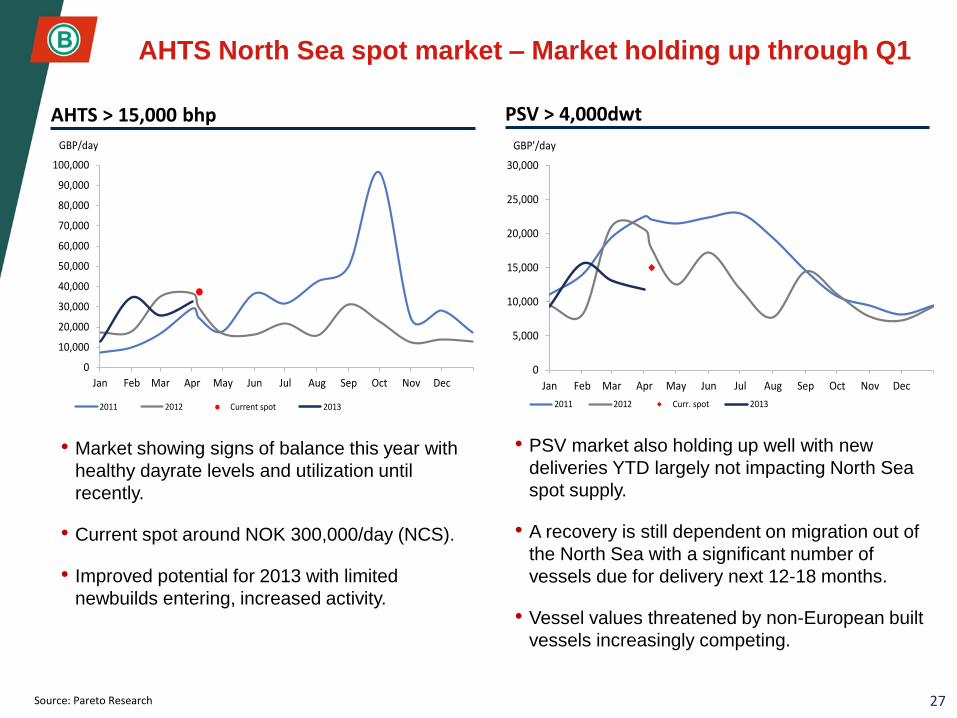

AHTS North Sea spot market – Market holding up through Q1

Source: Pareto Research

AHTS > 15,000 bhp PSV > 4,000dwt

• Market showing signs of balance this year with

healthy dayrate levels and utilization until

recently.

• Current spot around NOK 300,000/day (NCS).

• Improved potential for 2013 with limited

newbuilds entering, increased activity.

• PSV market also holding up well with new

deliveries YTD largely not impacting North Sea

spot supply.

• A recovery is still dependent on migration out of

the North Sea with a significant number of

vessels due for delivery next 12-18 months.

• Vessel values threatened by non-European built

vessels increasingly competing.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2011 2012 Current spot 2013

GBP/day

0

5,000

10,000

15,000

20,000

25,000

30,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2011 2012 Curr. spot 2013

GBP'/day

28

Despite……

Source: IHS/ODS Petrodata, Boa

• No large FPSOs to support (ref 2011 and 3Q12).

• Few very large Field Developments/construction

projects.

• Competition from PSVs (increased fleet).

• Less exploration wells.

• Total number of spot AHTS fixtures for period

Jan-March up 30% from 2011 to 2013.

• Number of spot fixtures for Rig Moves up 80%

from 2011 to 2013.

• Other spot fixtures down 10% last two years.

* Updated per mid march

Term demand down significantly AHTS 15k+ Also seen in spot market*

29

Drilling activity to pick up significantly in 2013 and onwards

Source: Pareto

0

10

20

30

40

50

60

Q1

'05

Q3

'05

Q1

'06

Q3

'06

Q1

'07

Q3

'07

Q1

'08

Q3

'08

Q1

'09

Q3

'09

Q1

'10

Q3

'10

Q1

'11

Q3

'11

Q1

'12

Q3

'12

Q1

'13

Q3

'13

Q1

'14

Q3

'14

Q1

'15

Q3

'15

UK Norway

# of working rigsOther supportive demand factors:

Increased subsea/FPSO activity, particularly in 2014

More frontier drilling with Barents Sea and Greenland up y/y in 2013

At least one, likely two and potentially three drilling campaigns offshore Greenland in 2014

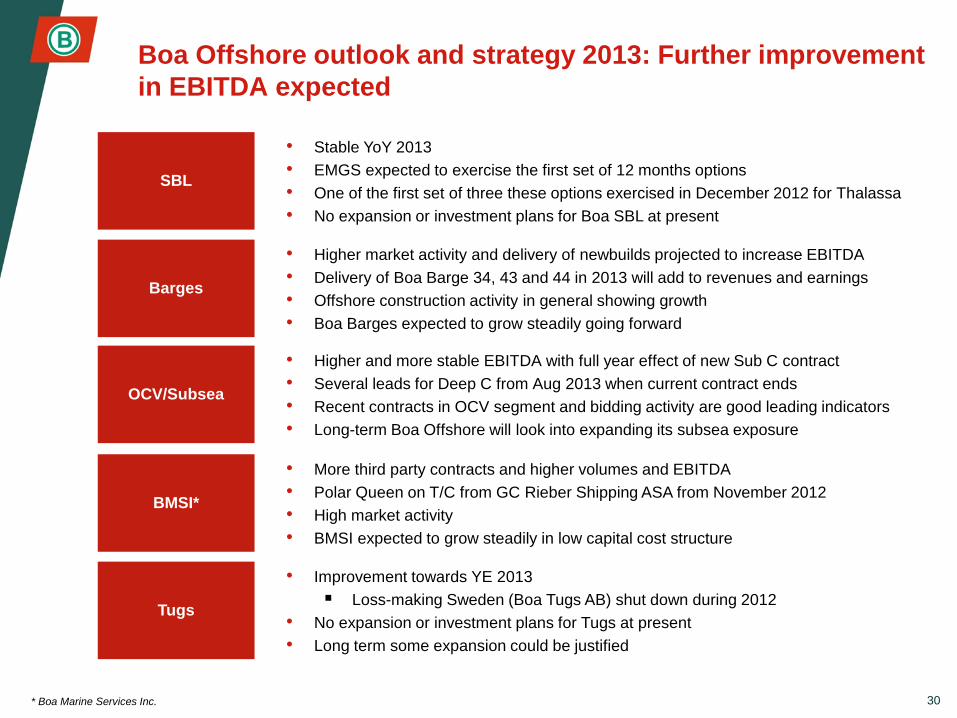

Boa Offshore outlook and strategy 2013: Further improvement

in EBITDA expected

30

• Higher and more stable EBITDA with full year effect of new Sub C contract

• Several leads for Deep C from Aug 2013 when current contract ends

• Recent contracts in OCV segment and bidding activity are good leading indicators

• Long-term Boa Offshore will look into expanding its subsea exposure

• Higher market activity and delivery of newbuilds projected to increase EBITDA

• Delivery of Boa Barge 34, 43 and 44 in 2013 will add to revenues and earnings

• Offshore construction activity in general showing growth

• Boa Barges expected to grow steadily going forward

• Stable YoY 2013

• EMGS expected to exercise the first set of 12 months options

• One of the first set of three these options exercised in December 2012 for Thalassa

• No expansion or investment plans for Boa SBL at present

• More third party contracts and higher volumes and EBITDA

• Polar Queen on T/C from GC Rieber Shipping ASA from November 2012

• High market activity

• BMSI expected to grow steadily in low capital cost structure

• Improvement towards YE 2013

Loss-making Sweden (Boa Tugs AB) shut down during 2012

• No expansion or investment plans for Tugs at present

• Long term some expansion could be justified

OCV/Subsea

Barges

SBL

BMSI*

Tugs

* Boa Marine Services Inc.