BNM Annual Report 2010 & Financial Stability and Payment Systems Report 2010 · 2014-12-10 · BNM...

42

1 by Dato' Muhammad bin Ibrahim Deputy Governor 23 March 2011 BNM Annual Report 2010 & Financial Stability and Payment Systems Report 2010 Briefing to Analysts & Fund Managers

Transcript of BNM Annual Report 2010 & Financial Stability and Payment Systems Report 2010 · 2014-12-10 · BNM...

1

byDato' Muhammad bin Ibrahim

Deputy Governor

23 March 2011

BNM Annual Report 2010 & Financial Stability and Payment

Systems Report 2010

Briefing to Analysts & Fund Managers

2

Briefing to cover:

• Economic and financial developments in 2010

• Prospects for 2011

• Policy Direction

3

Malaysian economy expanded strongly by 7.2% in 2010

• Growth driven mainly by robust domestic demand and primarily by private sector activity

• Public sector continued to play a crucial role in supporting the domestic economy in 2010

• External demand, which rebounded strongly in the first half of the year, moderated in the second half-year in tandem with the moderation in global trade

Annual change (%) 2009 2010p

Domestic demand -0.5 6.3

Private consumption 0.7 6.6

Public consumption 3.1 0.1

Gross fixed capital formationPrivate investmentPublic investment

-5.6-17.28.0

9.413.85.5

Net exports 5.0 -24.2

Exports of G&S -10.4 9.8

Imports of G&S -12.3 14.7

Real GDP -1.7 7.2

Source: Department of Statistics, Malaysia

p preliminary

4

Strong growth in all sectors, in line with the robust

domestic demand and rebound in exports

Annual change (%) 2009 2010p

Agriculture 0.4 1.7

Mining -3.8 0.2

Manufacturing -9.4 11.4

Construction 5.8 5.2

Services 2.6 6.8

Real GDP -1.7 7.2

Source: Department of Statistics, Malaysia

p preliminary

5

2009 2010p

RM billionCurrent Account 112.1 90.5

% of GNI 17.5 12.2Goods 141.7 136.6Services 4.7 0.9Income -14.6 -25.2Capital Account -0.2 -0.2Financial Account -80.2 -21.9

Direct Investment -22.9 -15.0In Malaysia 5.0 27.6Abroad -27.9 -42.6

Portfolio Investment -1.7 44.9Financial Derivatives 2.5 -0.8Other Investment -58.1 -51.1

E & O -17.9 -71.1Rev. Gain (+)/Loss (-) 10.7 -32.6

Overall Balance 13.8 -2.6Reserves (USD billion equivalent)

331.396.7

328.6106.5

… negligible e/ estimate

Overall balance of payments remained strong in 2010

• Current account surplus narrowed to 12.2% of GNI

• Financial account recorded smaller net outflow due to higher portfolio and FDI inflows

• Reserves remained high at USD110.4 billion at 15 March 2011

p preliminary Source: Department of Statistics, Malaysia

6

Higher foreign direct investment and direct investment abroad in 2010

• Higher FDI inflows

- Improved global and domestic economic conditions

- Better corporate earnings

-5

5

15

25

35

45

55

2008 2009 2010p

RM billion

• Direct investment abroad (DIA) was also higher

- Malaysian companies continued to tap profitable opportunities in other regions

- Outflows into services, oil and gas and manufacturing

… negligible e/ estimate

Source: Department of Statistics, Malaysia

p preliminary

Net FDI

Net DIA

7

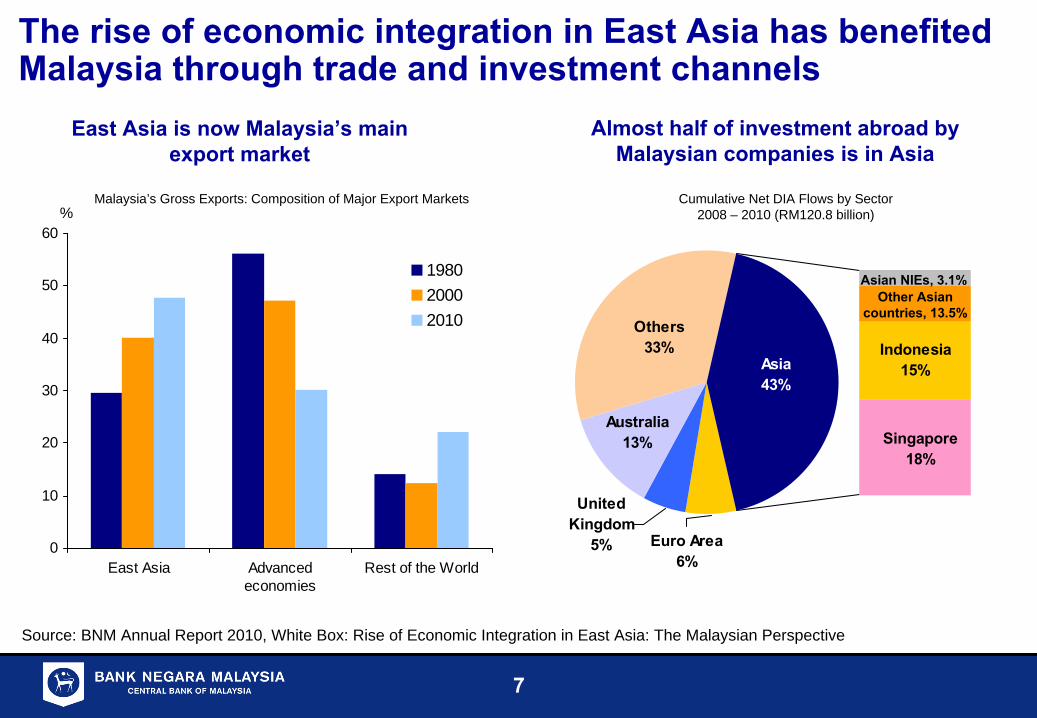

The rise of economic integration in East Asia has benefited Malaysia through trade and investment channels

Others33% Indonesia

15%

Singapore18%

Euro Area6%

United Kingdom

5%

Australia13%

Asia43%

0

10

20

30

40

50

60

East Asia Advancedeconomies

Rest of the World

%

198020002010

Almost half of investment abroad by Malaysian companies is in Asia

East Asia is now Malaysia’s main export market

Malaysia’s Gross Exports: Composition of Major Export Markets

Source: BNM Annual Report 2010, White Box: Rise of Economic Integration in East Asia: The Malaysian Perspective

Other Asian countries, 13.5%

Asian NIEs, 3.1%

Cumulative Net DIA Flows by Sector 2008 – 2010 (RM120.8 billion)

8

External debt remained low

• External debt declined to RM226.3 billion (equivalent to 30.2% of GNI)

• Lower medium- and long- term debt due to:

- revaluation gains following appreciation of ringgit and;

- net repayment position of the private sector

• Short-term debt increased but remains manageable

end-Dec 2009

end-Dec 2010

RM billionTotal External Debt 233.1 226.3

(USD bn equiv.) 67.4 72.6

Medium- and long-term 155.4 146.9

Short-term 77.8 79.4

%

External Debt/GNI 35.1 30.2

Short-Term Debt /Reserves 23.5 24.2

… negligible e/ estimate

Source: Ministry of Finance, Malaysia and Bank Negara Malaysia

9

Labour market conditions improved in 2010 following

strong gains in employment

239179

44

153

3.2

3.73.33.2

0

50

100

150

200

250

300

2007 2008 2009 2010e0

1

2

3

4

Net job creation Unemployment rate (RHS)

No. of jobs ('000) % of labour force

Source: Economic Planning Unit and Ministry of Human Resources

Higher net job creation & lower unemployment rate in 2010

While retrenchments declined significantly

0

5

10

15

20

25

30

2007 2008 2009 2010

Total retrenchments Mfg Non-mfg

Person (‘000)

10

Inflation was modest in 2010

Contribution to Inflation

-2 -1 0 1 2

All Items

Food & non-alco bev

Transport

Housing, water, elec, gas

Misc. goods & services

Alco bev & tobacco

Recreation serv & culture

Restaurants & hotels

Education

Furnishings & household eq.

Health

Communication

Clothing & footwear

percentage points

2009

2010

• Inflation edged to 1.7% in 2010 (2009: 0.6%), reflecting increases in the food and transport

Malaysia CPI, %

-15

-10

-5

0

5

10

15

20

Jul-0

7

Oct

-07

Jan-

08

Apr-

08

Jul-0

8

Oct

-08

Jan-

09

Apr-

09

Jul-0

9

Oct

-09

Jan-

10

Apr-

10

Jul-1

0

Oct

-10

Annual growth, %

Headline inflation

Core inflation

Supply-related inflation

11

Financing conditions expected to remain favourable

Net financing growth sustained…

3

6

9

12

15

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep

-09

Nov

-09

Jan-

10

Mar

-10

May

-10

Jul-1

0

Sep

-10

Nov

-10

Annual change (%)

Loan growth: 12.7%

Net financing growth: 11.3%

Total Financing

30

40

50

60

70

80

90

100

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

BusinessesHouseholds

Loans Applications by Businesses and Households

RM billion

20102009

…supported by robust demand for loans from businesses and households

12

Domestic equity market had sustained growth in line with regional trends

KLCI and Bursa Malaysia sectoral indices

80

100

120

140

160

180

200

220

Jan-

09M

ar-0

9

May

-09

Jul-0

9

Sep

-09

Nov

-09

Jan-

10M

ar-1

0M

ay-1

0

Jul-1

0

Sep

-10

Nov

-10

Jan-

11M

ar-1

1

Index (Jan 2009=100)

Finance

Industrial

KLCI

Plantation

Construction

Performance of Major Indices (% growth)

87.0

63.2

63.0

49.7

45.2

23.5

64.5

78.3

22.1

52.0

19.0

46.1

40.6

37.6

21.9

19.3

12.8

10.1

9.6

9.0

5.3

-3.0

-20 0 20 40 60 80 100

Indonesia

Thailand

Philippines

Korea

Msia

US

Singapore

Taiwan

UK

HK

Japan

%

2010

2009

13

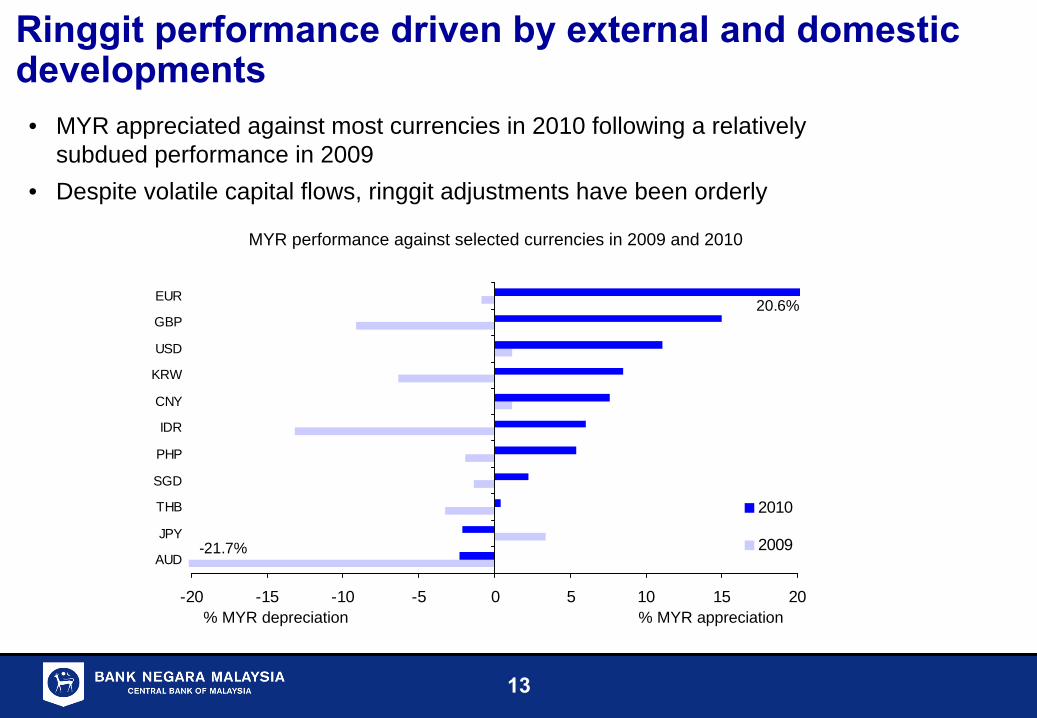

-20 -15 -10 -5 0 5 10 15 20

AUD

JPY

THB

SGD

PHP

IDR

CNY

KRW

USD

GBP

EUR

2010

2009-21.7%

20.6%

Ringgit performance driven by external and domestic developments• MYR appreciated against most currencies in 2010 following a relatively

subdued performance in 2009• Despite volatile capital flows, ringgit adjustments have been orderly

MYR performance against selected currencies in 2009 and 2010

% MYR appreciation% MYR depreciation

14

The impact of ringgit appreciation on the economy has been manageable

0%

5%

10%

15%

20%

25%

30%

35%

40%

Favourable Neutral Unfavourable0%

5%

10%

15%

20%

25%

30%

35%

40%

Favourable Neutral Unfavourable

Quarterly sectoral

survey* 4Q 2010Impact of ringgit appreciation on profit margins

Impact on profit margin thus far Impact on profit margin if ringgit appreciates further

* Based on a survey of 177 companies, of which 109 are manufacturing, 43 non-financial services and 25 Constructions

15

Measures undertaken to allow more efficient management of foreign financial transactions

To allow more efficient management of foreign transactions, several measures have been undertaken, including:

• Allow settlements in local currencies

• Facilitate hedging activities by residents

• Allow unlimited holding of foreign currency accounts

• Allow settlement of transactions in foreign currency by exporters and importers

16

Prospects for 2011

17

Global growth projection for 2011

Challenge for global economy going into 2011 is sustaining growth with job creation

Source: National authorities, IMF World Economic Outlook, January 2011 Update

2009 2010 2011f

Annual change (%)

World GDP -0.6 5.0 4.4World Trade -10.7 12.0 7.1

US -2.6 2.8 3.0

Euro area -4.1 1.7 1.5

Japan -6.3 3.9 1.6

Developing Asia 1/ 7.0 9.3 8.4

China 9.2 10.3 9.6

ASEAN-5 2/ 1.7 6.7 5.5

Note: Forecasts for 2011 are IMF’s projections1/ IMF: Asia ex-NIEs2/ IMF: Indonesia, Malaysia, Philippines, Thailand and Vietnam

• Significant improvement in 2010

• Continued recovery in advanced economies although growth remains slow

• Strong growth in emerging economies, particularly in Asia underpinned by domestic demand and recovery in world trade

• More recently, rising commodity and energy prices are leading to higher global inflation

18

Global growth mainly from EMEs in 2011

-4-3-2-1012345678

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

f

-80-60-40-20020406080100120140160Advanced economies EM: Africa

EM: Asia EM: Eastern EuropeEM: Middle East EM: Latin AmericaEM: CIS EME contribution to global growth (RHS)

Contribution to world growth, p.p. share of world growth. %

Source: IMF World Economic Outlook Note: CIS is the Commonwealth of Independent States, formerly Soviet republics

While accounting for 47% of global economy, emerging economies expected to contribute more than 70% of global growth

19

3

5

7

9

11

Dec

-07

Mar

-08

Jun-

08S

ep-0

8D

ec-0

8M

ar-0

9Ju

n-09

Sep

-09

Dec

-09

Mar

-10

Jun-

10S

ep-1

0D

ec-1

0

0

1

2

3

4

5

6

US Euro area UK Japan (RHS)

%%-14

-12

-10

-8

-6

-4

-2

0

22001 2003 2005 2007 2009

-12

-10

-8

-6

-4

-2

0

% of GDP % of GDP

Advanced economies still need to address structural problems

-10

-5

0

5

10

15

Dec

-07

Mar

-08

Jun-

08S

ep-0

8D

ec-0

8M

ar-0

9Ju

n-09

Sep

-09

Dec

-09

Mar

-10

Jun-

10S

ep-1

0D

ec-1

0

-4

-3

-2

-1

0

1

2

3

4

5

6%%

Restrained credit conditionsHigh unemployment rate High fiscal deficit1 32

Source: National authorities, Haver, IMF

Unemployment rate (%) Fiscal deficit, % of GDP Credit to private sector, growth

20

0

1

2

3

4

5

6

Dec

-07

Mar

-08

Jun-

08S

ep-0

8D

ec-0

8M

ar-0

9Ju

n-09

Sep

-09

Dec

-09

Mar

-10

Jun-

10S

ep-1

0D

ec-1

0

Index

0

1

2

3

4

5

6

7Index

Korea Singapore Hong KongChina C. Taipei (RHS) Thailand (RHS)

-30

-20

-10

0

10

20

30

40

50

Dec

-07

Apr

-08

Aug

-08

Dec

-08

Apr

-09

Aug

-09

Dec

-09

Apr

-10

Aug

-10

Dec

-10

-15

-10

-5

0

5

10

15

20

25

Regional economies supported by resilient domestic demand

-10

0

10

20

30

40

Dec

-07

Mar

-08

Jun-

08S

ep-0

8D

ec-0

8M

ar-0

9Ju

n-09

Sep

-09

Dec

-09

Mar

-10

Jun-

10S

ep-1

0D

ec-1

0

-8

-4

0

4

8

12

16yoy,%

Continued access to creditRising retail salesUnemployment trending down1 32

Source: National authorities, Haver

Unemployment rate Lending growth *

Note: * Refers to loans as reported in banks’ balance sheet, except for Indonesia which refers to loans outstanding

Indonesia

yoy,%Retail salesyoy,% yoy,%

21

-3

-2

-1

0

1

2

3

4

5

6

7

8

2003

2004

2005

2006

2007

2008

2009

2010

2011

Rising commodity prices have increased the risk to higher global inflation

0

50

100

150

200

250

300

350

400

450

500

2003

2004

2005

2006

2007

2008

2009

2010

2011

Metals

Crude oil

Food

US

Euro

UK

East Asia-9

…driving up inflation in most economies

Index (Jan ’03 = 100) Yoy (%)

Rising commodity prices amid supply disruptions and geopolitical tensions…

22

Different degrees of monetary policy response

0

2

4

6

8

10

2008 2009 2010 2011

PR China

Thailand

Indonesia

Korea

%

Malaysia

Ch Taipei

0

1

2

3

4

5

6

2008 2009 2010 2011

%

US

Euro area

UKJapan

…while most regional economies have started to normalise

or tighten since 2010Some advanced economies are expected

to begin to normalise

rates this year…

Key interest rates, % Key interest rates, %

23

Global shifts in liquidity: Volatile capital flows…Large capital inflows driven by growth differentials and the search for yield…

0 4 8 12 16 20

C. Taipei

Thailand

India

Malaysia

Singapore

Philippines

Korea

Indonesia

PR China

20092010

Total flows into equity and bond markets

USD billionSource: EFPR

0 50 100 150 200

Hong Kong

P.R China

Malaysia

Singapore

Korea

C. Taipei

Philippines

Thailand

Indonesia

Stock market

Property prices

% change from end-2008 till end-2010

Stock market and property price performance

…driving stock and property prices higher

1

1/ till 3Q 10 for property pricesSource: Haver and Bloomberg

24

…prompting measures to manage these flows

Measures introduced in the region to manage capital flows

Hong Kong SAR & Singapore

Philippines

Indonesia

Thailand

Chinese Taipei

Korea

PR China

Limit capital inflows – capital account measures

Prudential & liquidity measures (macroprudential)

Greater flexibility for capital outflows (liberalisation)

Administrative measures (real estate)

25

The Malaysian economy is projected to grow by 5% −

6% in 2011

-2

-1

0

1

2

3

4

5

6

7

8

2005

2006

2007

2008

2009

2010

p

2011

f

Annual change (%)

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

5.0%

6.0%7.2%

p preliminary f forecast

• Slower growth in 1H 2011 – High base in 1H 2010, particularly

for exports and investment– Lower demand for electronic

exports

• Growth is expected to improve in 2H– Stronger expansion of domestic

demand, particularly, private consumption and investment

– Higher exports

26

Strong growth in domestic demand to be driven by private sector activity

2010p 2011f 2010p 2011f

Annual change (%)

Contribution to growth (p.p)

Domestic demand 6.3 6.7 5.6 6.0Private sector 7.8 7.4 4.9 4.7

Consumption 6.6 6.9 3.6 3.7Investment 13.8 9.7 1.4 1.0

Public sector 2.5 5.1 0.6 1.3Consumption 0.1 7.2 0.0 1.0

Investment 5.5 2.7 0.6 0.3Net exports -24.2 2.3 -3.3 0.2

Exports of G&S 9.8 2.7 10.5 3.0Imports of G&S 14.7 2.8 13.8 2.8

Real GDP 7.2 5.0~6.0 7.2 5.0~6.0

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

p preliminary f forecast

• Private domestic demand to be the main growth driver

- Strong private consumption

- Rising investment activity

• Public sector to remain supportive of growth

27

Strong expansion in private consumption

Stronger expansion in consumer spending supported by:

– Favourable labour market conditions

– Rising disposable incomes

– Sustained consumer confidence

– Continued access to credit

p preliminary f forecast

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

Real private consumption

9.1

6.8

8.5

0.7

6.9

10.5

6.6

0

2

4

6

8

10

12

2005 2006 2007 2008 2009 2010p 2011f

Annual change (%)

28

Household expenditure on discretionary items has increased in recent years

0 2 4 6 8 10 12 14

Miscellaneousgoods &services

Restaurants &hotels

Communication

Recreation &culture

% of total household consumption

2005-092000-04

• The changing patterns of household spending reflected mainly growing affluence, supported by

- Steady rise in disposable income

- Accumulation of wealth

• Other key factors- Favourable demographic (i.e.

young and large working-age population)

- Increased financial deepening and inclusion

- Technological developments

Source: Department of Statistics, Malaysia

29

Labour market conditions expected to remain

favourable in 2011

3.23.5

3.3

3.2 3.3

3.7

3.2

0

1

2

3

4

2005 2006 2007 2008 2009 2010e 2011f0

1

2

3

4

5

Annual change (%)

Unemployment rate (% of labour force)

Source: Economic Planning Unit

• Unemployment rate to remain stable at 3.2% in 2011

- supported mainly by growth in domestic-oriented sectors

e Estimate f Forecast

Employment (RHS)

Labour

force (RHS)

Unemployment rate

30

Strong performance in private investment

Annual change (%) 2009 2010p 2011f

Real private investment -17.2 13.8 9.7• Increased capital spending in all

economic sectors- Key sectors: services,

manufacturing and mining

• Factors supporting private investment:

- Expansion of new growth areas- Strengthening domestic demand- Implementation of Government

initiatives- Sustained business confidence

Nominal Private Investment

0

10

2030

40

50

6070

80

90

2006 2007 2008 2009 2010p 2011f

RM billion

Agriculture Mining ManufacturingConstruction Services

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

62.1

76.6 79.8

65.2

76.9

86.9

p

preliminary f forecast

31

FDI to increase further in 2011

• Higher net inflows of FDI in 2011

- Better corporate earnings

- Rising business confidence

- Further improvement in global FDI flows

- Liberalisation

- Implementation of Government ETP projects

• Inflows channeled mainly into the manufacturing, services, and oil and gas sectors

Net FDI inflows into Malaysia

29.5

24.1

5.0

27.632.4

0

10

20

30

40

50

2007 2008 2009 2010p 2011f

RM billion

p preliminary f forecast

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

32

Positive trends in private investment are expected to continue moving forward

Source: Department of Statistics, Malaysia, Bank Negara Malaysia

Two distinct changes can be observed in the recent decade

• Increasing diversity in the investment spending across the various economic sectors

• More capital expenditure channelled into higher value-added, technologically-intensive projects across the different sectors of the economy

- Manufacturing: Renewable energy, high- end electronic products, machinery and equipment, medical devices industry

- Services: Shared services and outsourcing, communication and transport & storage infrastructure

Nominal Private Investment

0%

20%

40%

60%

80%

100%

2000 2010p/Agriculture Mining ManufacturingConstruction Services

25.5

1.1

64

3.26.1

30.7

% share

3.6

54.7

6.64.4

Sectoral

distribution of private investment has become more diversified

33

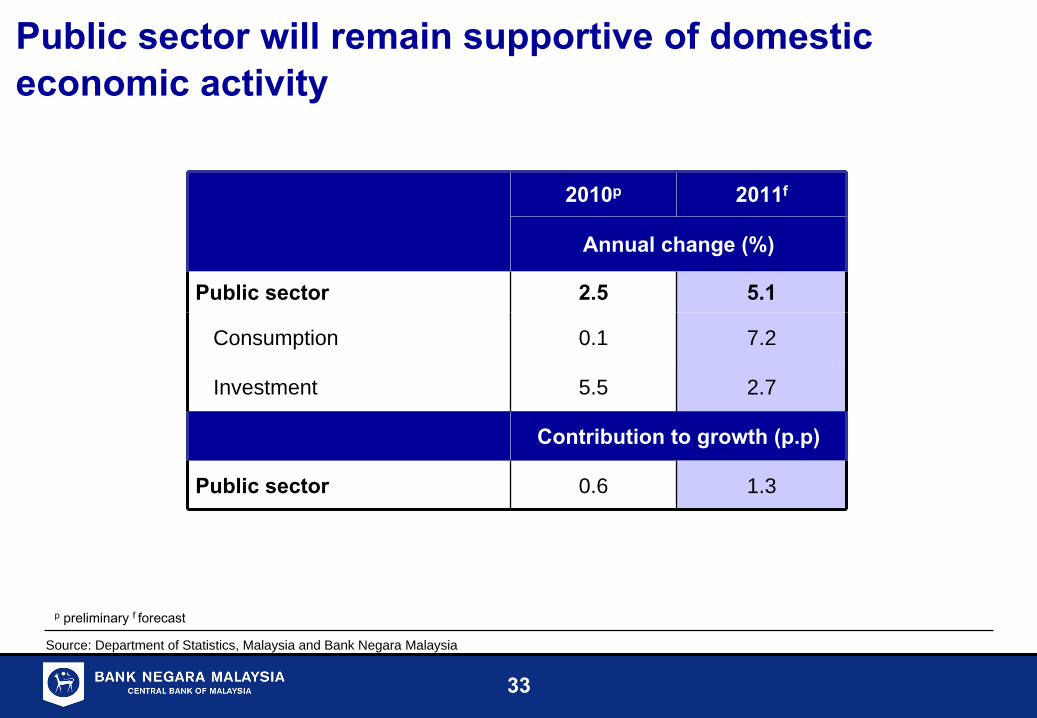

Public sector will remain supportive of domestic economic activity

2010p 2011f

Annual change (%)

Public sector 2.5 5.1

Consumption 0.1 7.2

Investment 5.5 2.7

Contribution to growth (p.p)

Public sector 0.6 1.3

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

p

preliminary f forecast

34

External trade to expand in 2011

• Exports– Moderation from the high base

of 2010, particularly in manufactured exports

– But, strong support from commodity exports due to higher prices and sustained regional demand

• Imports– Modest growth in intermediate

imports– Growth in capital and

consumption imports reflects strong domestic demand

Annual change (%) 2010p 2011f

Gross exports 15.6 5.4Manufactured 13.0 4.4

E&E 9.9 3.7

Non-E&E 17.3 5.2

Commodities 26.9 10.1Agriculture 30.8 12.4

Minerals 23.4 8.0

Gross Imports 21.7 5.7Capital 16.2 10.3

Intermediate 22.1 5.3Consumption 10.1 8.4

Trade balance (RM bn) 110.2 114.6

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

p

preliminary f forecast

35

Current account to remain in surplus

• Larger trade surplus supported by higher commodity exports

• Services surplus, benefiting from higher tourism receipts

• Lower income deficit

- Higher earnings by Malaysian companies investing abroad

- Lower repatriation of profits and dividends by MNCs

Widening current account surplus

-50

-20

10

40

70

100

130

160

190

220

2007 2008 2009 2010p 2011f

RMb

-5

0

5

10

15

20% GNI

Goods ServicesIncome Current transfersCurrent Account, % GNI (RHS)

12.5%12.2%RM90.5b RM100.7b

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

p

preliminary f forecast

36

Annual change (%) 2010p 2011f

Agriculture 1.7 3.4

Mining 0.2 2.0

Manufacturing 11.4 5.7

Construction 5.2 5.4

Services 6.8 5.9

Real GDP 7.2 5.0 ~ 6.0

Broad-based growth across all sectors

• Supported mainly by the continued growth of domestic economic activity

• Trade-related services and export-oriented manufacturing industries to record slower growth in line with the expected moderation in external demand

Source: Department of Statistics, Malaysia and Bank Negara Malaysia

p preliminary f forecast

37

Headline inflation to range between 2.5 – 3.5% in 2011

Inflation Forecast 2011

0

1

2

3

4

5

6

2005 2006 2007 2008 2009 2010 2011/f

Annual growth (%)

2.5 –

3.5%

• Driven mainly by higher global commodity and energy prices, inflation is expected to increase in 2011.

• This trend is similar to other regional economies

Regional Countries Headline Inflation Forecast

3.8%

3.3%

1.7%

2.8%

3.0-5.0%3.0-5.0%

2.5-3.5%

3.0-4.0%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Singapore Malaysia Thailand Phillippines

Annual growth (%)

2010 2011 forecast

Note: Inflation forecast refer to the central bank official forecast

38

Malaysia has adopted a comprehensive approach to manage inflationary pressures from commodity prices

In addition to macroeconomic policies, other measures taken are

• Increasing food production and its distributional efficiency

• Promoting greater energy efficiency by households and industry

• A more gradual subsidy rationalisation programme

• Providing income support to targeted groups

39

Monetary policy in 2011 will remain supportive of growth, while managing risks to inflation

2.75%

2.50%

2.0%

3.5%

2.25%

1.5

2.0

2.5

3.0

3.5

4.0

Jun-

08A

ug-0

8O

ct-0

8D

ec-0

8Fe

b-09

Apr

-09

Jun-

09A

ug-0

9O

ct-0

9D

ec-0

9Fe

b-10

Apr

-10

Jun-

10A

ug-1

0O

ct-1

0D

ec-1

0

% Overnight Policy Rate (OPR)

• Given improved economic outlook, the OPR was adjusted in 2010 to

– Normalise monetary conditions

– Prevent the risk of financial imbalances

• For 2011, focus of monetary policy is to manage the risk of a more modest growth and higher inflation

– Monetary policy has the flexibility to remain accommodative

– The degree of accommodation may however, need to be reviewed to ensure sustainable economic growth

40

Two-way capital flows expected to continue

• In 2010, the capital inflows to Malaysia went into both the bond and equity markets• Strong economic fundamentals and positive prospects will continue to attract portfolio inflows• But this is likely to be interrupted by intermittent reversals driven by external events

-15

-10

-5

0

5

10

15

20

25

Q1 Q2 Q32009

Q4 Q1 Q2 Q32010

Q4

Net Portfolio Investment into MalaysiaRM billion

Source: Department of Statistics Malaysia

Cumulative net equity fund flows (since Jan 07)

-40

0

40

80

120

160

200

Dec

-06

Apr

-07

Aug

-07

Dec

-07

Apr

-08

Aug

-08

Dec

-08

Apr

-09

Aug

-09

Dec

-09

Apr

-10

Aug

-10

Dec

-10

USD billion

-0.5

0.0

0.5

1.0

1.5

2.0

2.5USD billion

All Emerging Markets (LHS)Malaysia (RHS)

07

Source: Emerging Portfolio Fund Research Global

41

Large inflows have also led to increases in international reserves

Net International Reserves(Jan’08 - Mar’11)

110.4

130.5

80

90

100

110

120

130

140

Jan-

08

Apr

-08

Jul-0

8

Oct

-08

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

USD bn

Deleveraging activities by international investors

Resumption of capital inflows

Source: BNM

• Large inflows have led to increases in international reserves

– Since the resurgence of capital inflows in 2H 2009, net international reserves at USD110.4 bn in 15 March-11.

– During previous episode in Aug- 08: USD130.5 bn

42

Capital flows currently well intermediated

• More diversified and developed financial system has helped to intermediate the capital flows

• Managed float regime has the necessary flexibility for the exchange rate to adjust to changing conditions

• Wider range of instruments for effective monetary operations

• Rigorous surveillance and information systems

• Stronger fundamentals and a healthy level of international reserves

• Closer cooperation and communication among central banks

Large inflows have increased liquidity in the domestic financial

system but, this has been well managed