BMO Multi-Manager Informed investor - Global · showing a rise in US wages. This rise suggests that...

12

Review of world markets Investment strategy Portfolio breakdowns What we learnt on a recent research trip around Asia Postcard from Asia Keeping you up-to-date with your F&C Multi-Manager investment Informed investor BMO Multi-Manager Issue 21 | Spring 2018

Transcript of BMO Multi-Manager Informed investor - Global · showing a rise in US wages. This rise suggests that...

Review of world markets Investment strategy Portfolio breakdowns

What we learnt on a recent research trip around Asia

Postcard from Asia

Keeping you up-to-date with your F&C Multi-Manager investment

Informed investor

BMO Multi-Manager

Issue 21 | Spring 2018

2 Informed investor | Issue 21 | Spring 2018

Informed investor

Anthony WillisInvestment Manager, BMO Multi-Manager team

Sept 2017 – Feb 2018

Retu

rn %

IA £ Corporate Bond NR IA £ High Yield NR IA Global Bonds NR IA Property NR

-4.0-3.5-3.0-2.5-2.0-1.5-1.0

-0.50.00.51.01.52.02.5

09/17 02/1810/17 11/17 12/17 01/18

Percentage growth, total return 01.09.17 to 23.02.18, in sterling, source: Lipper.

Fixed income and property – a subdued period for bonds and property

Retu

rn %

IA Global Emerging Markets NRIA Asia Pacific Excluding Japan NR IA Japan NRS&P 500 TRFTSE All-Share TR FTSE AW Developed Europe ex UK TR GBP

-6

-3

0

3

6

9

12

15

09/17 02/1810/17 11/17 12/17 01/18

Percentage growth, total return 01.09.17 to 23.02.18, in sterling, source: Lipper.

Equities – progress dampened by February sell-off

Fixed income

Corporate bonds (both high yield and investment grade) received support from a broadly positive economic backdrop, robust corporate performance and demand from investors looking for income. Government bond prices eased (yields rose) as higher inflation increased the chance of interest rate rises.

Our view – valuations, the prospect of higher inflation, rising interest rates and issues around liquidity (the ability to buy and sell) remain some of the reasons we are still cautious on fixed income. We continue to favour funds with the flexibility to target those areas where opportunities do exist.

Economies and markets

Past performance should not be seen as an indication of future performance.

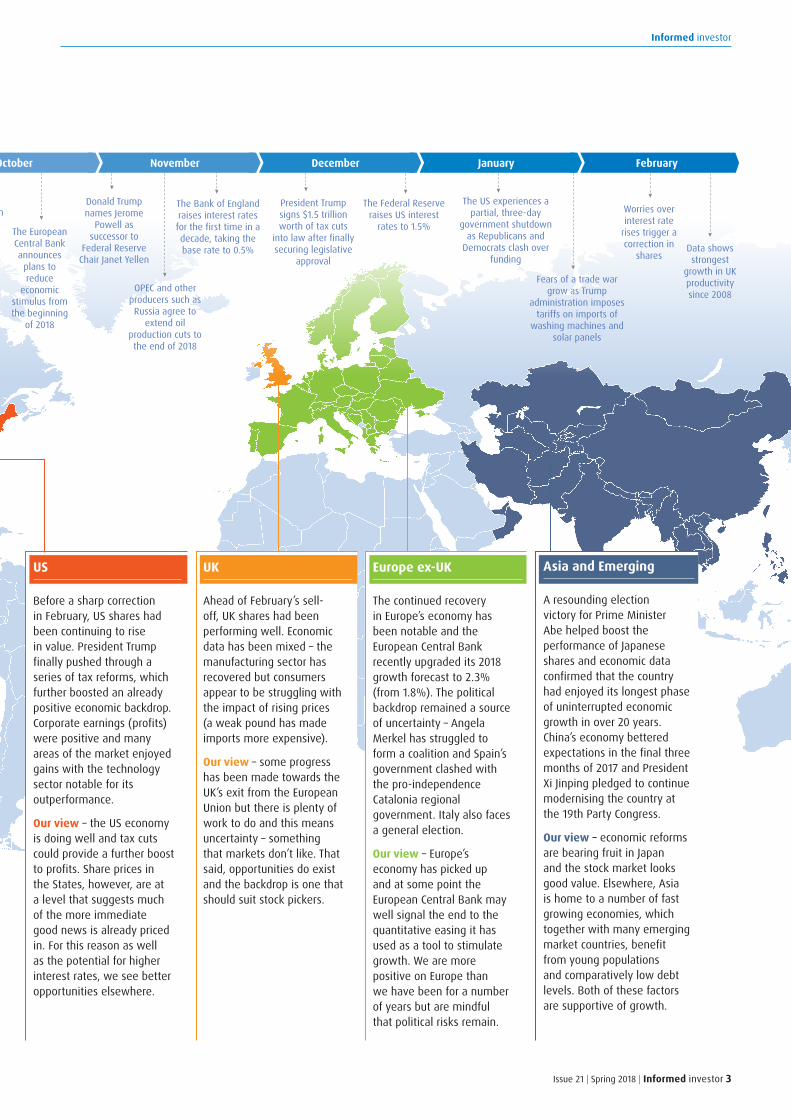

Here we look at some of the key events and themes making an impression on markets around the world as well as offering a summary of our views.

Regional equity markets have trodden a similar path over the last six months – trending gradually upwards until early February then falling sharply in response to data showing a rise in US wages. This rise suggests that US interest rates are likely to rise quicker and higher than previously expected – something that financial markets will need to potentially adjust to. At the time of writing, they have regained some of the lost ground.

Informed Investor is a marketing communication and should not be considered as advice or a recommendation to buy, sell or hold investments. As with all investments, capital is at risk.

Donald Trump names Jerome

Powell as successor to

Federal Reserve Chair Janet Yellen

The Bank of England raises interest rates for the first time in a decade, taking the base rate to 0.5%

EU leaders agree to allow Brexit talks to move

on to the trade negotiation

phase

Prime Minister Theresa May

proposes a two-year transition after the UK leaves the EU

in 2019Angela Merkel faces difficult

coalition negotiations following the inconclusive

German elections

The European Central Bank announces

plans to reduce

economic stimulus from the beginning

of 2018

The Federal Reserve raises US interest

rates to 1.5%

The US experiences a partial, three-day

government shutdown as Republicans and

Democrats clash over funding

President Trump signs $1.5 trillion worth of tax cuts

into law after finally securing legislative

approval

Fears of a trade war grow as Trump

administration imposes tariffs on imports of

washing machines and solar panels

Worries over interest rate

rises trigger a correction in

shares Data shows strongest

growth in UK productivity since 2008

OPEC and other producers such as Russia agree to

extend oil production cuts to the end of 2018

Japan´s equity market rallies on strong election win for Prime Minister Abe

Dot-com bubble bursts

FSA becomesUK regulator

Pensions A-day FCA replaces FSA

Financial ServicesAct 1986 came into effect

Black Monday UK exits exchange rate mechanism

Asian financial crisis

Russianfinancial crisis

Depolarisation, SIPPs launched

RDRCredit crunch Eurozone crisis starts

Pension reforms

1985 1986 1987 1988 19891980 1981 1982 1983 1984 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2005 2006 2007 20082003 2004 2009 2010 2013 2014 2015 20162011 2012

Moody´s downgrades China´s credit rating for the first time in

around 30 years, citing concerns over slowing growth and rising debt

The UK general election results in a hung parliament

Oil prices fall below the $50 per barrel mark

The Federal Reserve raises interest rates

from 0.75% to 1%

The UK triggers Article 50 to begin

the process of leaving the European

Union

Far-right party led by Geert Wilders is

defeated in the Dutch general

election

Data shows US economic growth

slowed sharply in the first 3 months of 2017

UK economic growth slows to just 0.2% for the first quarter, but inflation jumps

to 2.7% in April

The Federal Reserve increases interest rates

from 1% to 1.25%

US Congress votes in favour of further sanctions against

Russia

Global equities reach fresh record highs as Chinese growth beats

expectations

Escalation of US/North Korea

tensions

The US Dow Jones index breaks

through 22,000 10 years since the start of the Global

Financial Crisis

March April May June July August

September October November December January February

Emmanuel Macron beats ultra-right

candidate Marine Le Pen in the French

presidential election

The UK government calls a snap

general election for

8 June

Issue 21 | Spring 2018 | Informed investor 3

Informed investor

Sept 2017 – Feb 2018

US

Before a sharp correction in February, US shares had been continuing to rise in value. President Trump finally pushed through a series of tax reforms, which further boosted an already positive economic backdrop. Corporate earnings (profits) were positive and many areas of the market enjoyed gains with the technology sector notable for its outperformance.

Our view – the US economy is doing well and tax cuts could provide a further boost to profits. Share prices in the States, however, are at a level that suggests much of the more immediate good news is already priced in. For this reason as well as the potential for higher interest rates, we see better opportunities elsewhere.

UK

Ahead of February’s sell-off, UK shares had been performing well. Economic data has been mixed – the manufacturing sector has recovered but consumers appear to be struggling with the impact of rising prices (a weak pound has made imports more expensive).

Our view – some progress has been made towards the UK’s exit from the European Union but there is plenty of work to do and this means uncertainty – something that markets don’t like. That said, opportunities do exist and the backdrop is one that should suit stock pickers.

Europe ex-UK

The continued recovery in Europe’s economy has been notable and the European Central Bank recently upgraded its 2018 growth forecast to 2.3% (from 1.8%). The political backdrop remained a source of uncertainty – Angela Merkel has struggled to form a coalition and Spain’s government clashed with the pro-independence Catalonia regional government. Italy also faces a general election.

Our view – Europe’s economy has picked up and at some point the European Central Bank may well signal the end to the quantitative easing it has used as a tool to stimulate growth. We are more positive on Europe than we have been for a number of years but are mindful that political risks remain.

Asia and Emerging

A resounding election victory for Prime Minister Abe helped boost the performance of Japanese shares and economic data confirmed that the country had enjoyed its longest phase of uninterrupted economic growth in over 20 years. China’s economy bettered expectations in the final three months of 2017 and President Xi Jinping pledged to continue modernising the country at the 19th Party Congress.

Our view – economic reforms are bearing fruit in Japan and the stock market looks good value. Elsewhere, Asia is home to a number of fast growing economies, which together with many emerging market countries, benefit from young populations and comparatively low debt levels. Both of these factors are supportive of growth.

Donald Trump names Jerome

Powell as successor to

Federal Reserve Chair Janet Yellen

The Bank of England raises interest rates for the first time in a decade, taking the base rate to 0.5%

EU leaders agree to allow Brexit talks to move

on to the trade negotiation

phase

Prime Minister Theresa May

proposes a two-year transition after the UK leaves the EU

in 2019Angela Merkel faces difficult

coalition negotiations following the inconclusive

German elections

The European Central Bank announces

plans to reduce

economic stimulus from the beginning

of 2018

The Federal Reserve raises US interest

rates to 1.5%

The US experiences a partial, three-day

government shutdown as Republicans and

Democrats clash over funding

President Trump signs $1.5 trillion worth of tax cuts

into law after finally securing legislative

approval

Fears of a trade war grow as Trump

administration imposes tariffs on imports of

washing machines and solar panels

Worries over interest rate

rises trigger a correction in

shares Data shows strongest

growth in UK productivity since 2008

OPEC and other producers such as Russia agree to

extend oil production cuts to the end of 2018

Japan´s equity market rallies on strong election win for Prime Minister Abe

Dot-com bubble bursts

FSA becomesUK regulator

Pensions A-day FCA replaces FSA

Financial ServicesAct 1986 came into effect

Black Monday UK exits exchange rate mechanism

Asian financial crisis

Russianfinancial crisis

Depolarisation, SIPPs launched

RDRCredit crunch Eurozone crisis starts

Pension reforms

1985 1986 1987 1988 19891980 1981 1982 1983 1984 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2005 2006 2007 20082003 2004 2009 2010 2013 2014 2015 20162011 2012

Moody´s downgrades China´s credit rating for the first time in

around 30 years, citing concerns over slowing growth and rising debt

The UK general election results in a hung parliament

Oil prices fall below the $50 per barrel mark

The Federal Reserve raises interest rates

from 0.75% to 1%

The UK triggers Article 50 to begin

the process of leaving the European

Union

Far-right party led by Geert Wilders is

defeated in the Dutch general

election

Data shows US economic growth

slowed sharply in the first 3 months of 2017

UK economic growth slows to just 0.2% for the first quarter, but inflation jumps

to 2.7% in April

The Federal Reserve increases interest rates

from 1% to 1.25%

US Congress votes in favour of further sanctions against

Russia

Global equities reach fresh record highs as Chinese growth beats

expectations

Escalation of US/North Korea

tensions

The US Dow Jones index breaks

through 22,000 10 years since the start of the Global

Financial Crisis

March April May June July August

September October November December January February

Emmanuel Macron beats ultra-right

candidate Marine Le Pen in the French

presidential election

The UK government calls a snap

general election for

8 June

Informed investor

4 Informed investor | Issue 21 | Spring 2018

strong team9

Why is it important to meet management companies and managers on their own doorsteps? Plenty of Asian and Japanese fund managers promote their funds by visiting London so it is possible to meet them in our offices – something we do on a regular basis. Doing so, however, often doesn’t give us the full picture and actually visiting the region and seeing the economy in action is a great way to get a clearer perspective and pick up on local views.

It is also key to meet other people working behind the scenes on the funds in which we invest (or are considering) on your behalf. Alongside every fund manager there is usually a team of analysts rolling up their sleeves and researching businesses in order to identify investment ideas. This bottom-up work is key to a fund’s performance potential and really getting to know what makes the broader team tick, and crucially, work together effectively, is key.

How do investors on the ground view the prospects for the region? Over the course of a hectic five-day trip, we visited both Hong Kong and Singapore, meeting 17 fund managers and seeing 22 analysts. It is always interesting to talk to local investors

and mostly they were upbeat in their assessment of the future prospects for Asian economies and markets. Importantly, there was a real and growing sense that confidence across the region was picking up and a feeling that its fortunes were less dependent on global growth than has historically been the case.

What are your views and how are the portfolios positioned?Last year was one in which Asia and the emerging markets were among our favoured markets – a stance that proved positive for the performance of our portfolios. Heading into 2018, that remains the case with valuations still looking reasonable – especially relative to areas like the US – and many companies appear to be in good shape and well-positioned for the future. In terms of underlying holdings, we have selectively increased exposure to a number of our favoured managers and funds, where appropriate.

years combined investment experience180

Informed investor

"It is also key to meet other people working behind the scenes on the funds in which we invest (or are considering) on your behalf."

Having returned from a research trip to Asia towards the end of last year, Scott Spencer discusses the insights gained from the team’s trip to the region.

On the road: Asia trip

The BMO Multi-Manager team in numbers: +

years in fund selection120

Issue 21 | Spring 2018 | Informed investor 5

Informed investor

Scott SpencerInvestment Manager, BMO Multi-Manager team

What are the prospects for growth in Asia?In years gone by an investment in funds accessing China and other Asian countries largely meant investing in exporters selling goods around the world. As the region has developed that has changed and investing in an Asian fund can now be much more about tapping into themes like the growing spending power of an expanding and increasingly affluent middle class. With prospects for economies in the region increasingly driven by internal factors, it is important to consider how the likes of China are faring domestically. Lower borrowing and a reduction in government stimulus means that it does seem likely that China’s economy will slow a little but evidence suggests that it will still grow in the region of 6 to 6.5% in 2018. On a global perspective, this is still an impressive number.

What are your thoughts specifically on Japan?We have liked Japan for a while and still believe it to be attractive from an investment viewpoint. Prime Minister Shinzo Abe was re-elected in October 2017 – a sweeping victory that signalled a continuation of his program of economic and corporate reforms. Many companies are increasing their focus on effectively managing their finances and prioritising the needs of their shareholders, something that is evident in rising dividend payments. As investors, we naturally think this is good news. Additionally, many shares look reasonably valued and the domestic economy is continuing to strengthen.

"With prospects for economies in the region increasingly driven by internal factors, it is important to consider how the likes of China are faring domestically."

manager meetings annually400 +

Informed investor

6 Informed investor | Issue 21 | Spring 2018

Strategic perspectives

Gary PotterCo-head, BMO Multi-Manager team

We have been working together as a nine-strong investment team for over 21 years now. Over that time, we have developed a sensible approach based on common sense investment principles. Above all, we try to keep things simple in what can seem an overly complex investment world. We do not believe that it is possible to predict the future direction of markets with any accuracy or consistency and we are certainly sceptical about those claiming any ability to predict the actions of central bankers or politicians - especially these days!

We also recognise that it is impossible for us to be experts in every part of the market so we focus our efforts on identifying people that are. We think that with the right research tools, contacts and experience it is possible to find talented people working in the right conditions for their skills to flourish. Indeed, picking managers has always been the key driver of your portfolio’s composition and its performance – something we expect to remain the case. You can see the funds we have selected on your behalf in the portfolio breakdowns on pages 8 to 11.

Of course, we are cognisant of the broader economic, political and market backdrops and make modest adjustments to the portfolios accordingly. Our trip to Asia (read more on pages 4 and 5) for example, reinforced a positive view on investment prospects for the region – potential we hope to access through the best managers we can find.

Manager skill can be important in all conditions. We enter 2018 after another year of impressive returns in many areas.

Who would have predicted such a recovery from the depths of the global financial crisis that the world found itself in not even 10 years ago? Today, markets reflect years of unprecedented central bank and government stimulus, a relatively buoyant and growing global economy and healthy corporate profits.

Our expectation is for this broadly supportive backdrop to be maintained but we do recognise that we may well be in an environment in which managers need to work harder for returns, be flexible enough to respond to swift changes and importantly, work to protect capital as and when we hit bumps in the road. Just a matter of weeks before I wrote this update, for example, shares endured a sharp sell-off after higher-than-expected inflation figures spooked investors into thinking significant interest rate rises were on the way. Up to the point of writing, they seem to have regained their poise and recouped some of the lost ground.

Fixed income is one area that brings this dynamic clearly into focus. Bond markets – like others – have generated bumper returns over the last decade but looking forward, rising inflation and the gradual withdrawal of stimulus by central banks are not likely to be overly supportive to many fixed income assets. Proven skill, insight and flexibility are watchwords for us as we seek out bond funds capable of performing in such an environment.

Whatever the asset class, we aim to offer our clients access to a well-diversified and dynamically managed portfolio of the very best available options.

We manage portfolios with a clear focus – helping people achieve their long-term investment goals by aiming to generate inflation-beating returns. We seek to achieve this by building portfolios from the best available talent.

Informed investor

Issue 21 | Spring 2018 | Informed investor 7

Outcomes matter :talking income

Sensible steps to income

Diversification - reducing risk and volatility (short-term fluctuations) by investing across a variety of assets.

Natural income - yield (or income) generated by an investment without drawing down the underlying capital value.

*Historic yield reflects distributions declared over the previous 12 months as a percentage of the share price as at 31 January 2018. Source: Lipper for Investment Management.

The Financial Conduct Authority – the UK’s financial regulator – is keen that asset managers like ourselves are clear in explaining what ‘outcomes’ the products we manage are aiming to deliver. We think this is a good thing and the portfolios we create on our clients’ behalf are designed to meet specific objectives.

Income investing is one area in which the desired ‘outcome’ – an attractive and reliable yield – is obvious and of course, despite the prospect of a modest rise in interest rates over the next 12 to 18 months returns from cash-based savings look set to remain relatively lacklustre. As a result, many people are having to reassess their willingness to accept additional risk to their capital in return for income. As well as the level of income, the consistency of the flow is key – a characteristic that is often at odds with the inconsistent world in which we live and invest.

To counter this paradox we believe it makes sense to adopt an approach that centres on sound long-term investment principles. For example, we deliberately diversify across asset types, geographies, management companies and underlying funds with the objective of delivering a consistent and less volatile income ‘outcome’. Diversifying is a recognised way of reducing investment risk but investors still need to be mindful that the value of investments and any income derived from them can go down as well as up as a result of market or currency movements and that they may not get back the original amount invested. Time can help here and evidence suggests that the longer you invest for the less the likelihood of suffering a capital loss.

Investment income can take many forms. Traditional sources of yield include dividends from equities, coupons from bonds or rent from property. There are plenty of other alternatives and in our F&C MM Navigator Distribution Fund, which is currently yielding 4.6%*, we also hold funds offering access to income from the likes of infrastructure projects, student accommodation, aircraft leasing and holiday parks to name just a small selection.

Whilst the sources of income in the portfolio are diverse, there is one characteristic we believe they share – the ability to generate yield ‘naturally’. To us that means without putting too much pressure on the value of capital. There are a number of reasons why we think this is important. First, maintaining capital is crucial in ensuring the long-term sustainability of an income strategy. If the value of capital is eroding, then the level of income it can generate will surely fall over time. Second, we recognise that markets do experience ups and downs, which in turn affect capital values. Seeking out sources of natural income can help keep the level of income much more consistent, even as underlying capital values fluctuate.

F&C MM Navigator Distribution Fund

F&C MM Navigator Moderate Fund

Portfolio breakdown %UK 9.90Schroder Income Maximiser 6.04J O Hambro Capital Management UK Equity Income Fund 4.76

Majedie UK Income Fund 3.06MI Chelverton UK Equity Income Fund 2.61FTSE 100 Index Futures -6.57Fixed Income 29.89Ashmore SICAV Emerging Markets Total Return Fund 4.65

MI TwentyFour Dynamic Bond Fund 4.52Henderson Strategic Bond Fund 4.48Schroder Strategic Credit Fund 4.21Active Funds ICAV - Global High Income Bond Fund 2.17

Angel Oak Multi-Strategy Income Fund 2.00GCP Infrastructure Investments Limited 1.93TwentyFour Income Fund Limited 1.49P2P Global Investments plc 1.26Starwood European Real Estate Finance Limited 1.18

Carador Income Fund plc 0.79Ranger Direct Lending Fund plc 0.61UK Mortgages Limited 0.60North America 3.38Hamlin High Dividend Equity UCITS Fund 3.33BNY Mellon U.S. Equity Income Fund 2.03S&P 500 Index Futures -1.98Europe 8.40Schroder European Alpha Income Fund 4.62Blackrock Continental European Income Fund 3.01Polar Capital Funds plc - European Ex UK Income Fund 2.77

Euro Stoxx 50 Index Futures -2.01Japan 2.47CC Japan Income & Growth Fund 2.47Asia 5.98Schroder Asian Income Maximiser 4.51Prusik Asian Equity Income Fund 1.48Emerging Markets 2.61JPM Emerging Markets Income Fund 2.61Specialist (Non Equity) 9.29Darwin Leisure Property Fund 3.41Amedeo Air Four Plus Limited 1.94GCP Student Living plc 1.92Blue Capital Alternative Income Fund Limited 0.81SQN Asset Finance Income Fund Limited 0.69SQN Asset Finance Income Fund Limited C Share 0.51

Specialist (Equity) 16.03RWC Global Enhanced Dividend Fund 3.89Artemis Global Income Fund 3.64Veritas Global Equity Income Fund 2.98Fidelity Global Enhanced Income Fund 2.95Aptus Global Financials Fund 2.58Cash 12.04Total 100.00

Portfolio breakdown %UK 12.44Majedie UK Focus Fund 6.08Old Mutual UK Dynamic Equity Fund 3.25GVQ UK Focus Fund 2.93J O Hambro Capital Management UK Growth Fund 2.56

Man GLG Undervalued Assets Fund 2.54FTSE 100 Index Futures -4.93Fixed Income 26.86Henderson Strategic Bond Fund 4.71Invesco Perpetual Tactical Bond Fund 4.54Legg Mason Western Asset Macro Opportunities Bond Fund 4.10

Active Funds ICAV - Global High Income Bond Fund 2.97

GCP Asset Backed Income Fund Ltd 2.55MI TwentyFour Dynamic Bond Fund 2.48Barings Emerging Markets Debt Blended Total Return Fund 1.95

GCP Infrastructure Investments Limited 1.81Hermes Multi Strategy Credit Fund 1.75North America 4.00Artemis US Extended Alpha Fund 4.00Conventum - Lyrical Fund 1.98S&P 500 Index Futures -1.98Europe 9.01Memnon European Fund 4.05Schroder European Alpha Plus Fund 3.72Blackrock Continental European Income Fund 3.25Euro Stoxx 50 Index Futures -2.02Japan 4.43Schroder International Selection Fund - Japanese Opportunities 2.43

CC Japan Alpha Fund 2.00Asia 6.32Prusik Asian Equity Income Fund 2.32TT Asia-Pacific Equity Fund 2.02BGF Asian Growth Leaders Fund 1.98Emerging Markets 2.92Hermes Global Emerging Markets Fund 2.92Specialist (Equity) 5.11Ardevora Global Equity Fund 3.07Aptus Global Financials Fund 2.04Specialist (Non Equity) 18.31Majedie Asset Management Tortoise Fund 4.82Old Mutual UK Specialist Equity Fund 4.08Darwin Leisure Property Fund 2.90Man GLG UK Absolute Value Fund 2.03iShares Physical Gold ETC 1.93Amedeo Air Four Plus Limited 1.47Custodian REIT 1.08Cash 10.60Total 100.00

Informed investor

8 Informed investor | Issue 21 | Spring 2018

F&C MM Navigator Funds

Our range of traditional multi-manager return-focused funds are actively managed portfolios of what we believe to be the best available funds blended to achieve defined investment objectives, with a flexible approach to asset allocation.

"We think that with the right research tools, contacts and experience it is possible to find talented people working in the right conditions for their skills to flourish."

Source: BMO Global Asset Management. Data as at 31.01.18

F&C MM Navigator Progressive Fund

F&C MM Navigator Select Fund

F&C MM Navigator Boutiques Fund

Portfolio breakdown %UK 21.32Majedie UK Focus Fund 5.97J O Hambro Capital Management UK Growth Fund 4.47

Man GLG Undervalued Assets Fund 4.51Old Mutual UK Dynamic Equity Fund 4.12GVQ UK Focus Fund 3.99River and Mercantile UK Micro Cap Investment Company Limited 1.75

FTSE 100 Index Futures -3.50Fixed Income 11.43Legg Mason Western Asset Macro Opportunities Bond Fund 3.54

Henderson Strategic Bond Fund 2.69Barings Emerging Markets Debt Blended Total Return Fund 1.83

GCP Infrastructure Investments Limited 1.79MI TwentyFour Dynamic Bond Fund 1.59North America 10.16Artemis US Extended Alpha Fund 5.20Conventum - Lyrical Fund 4.68Findlay Park American Fund 2.22S&P 500 Index Futures -1.95Europe 12.86Memnon European Fund 4.72FP Crux European Special Situations Fund 3.97Schroder European Alpha Plus Fund 3.73Edinburgh Partners European Opportunities Fund 2.46

Euro Stoxx 50 Index Futures -2.01Japan 6.22Schroder International Selection Fund - Japanese Opportunities 3.73

CC Japan Alpha Fund 2.49Asia 5.53BGF Asian Growth Leaders Fund 2.78Prusik Asian Equity Income Fund 2.75Emerging Markets 5.55TT Asia-Pacific Equity Fund 2.02TT Emerging Markets Unconstrained Fund 1.77Hermes Global Emerging Markets Fund 1.76Specialist (Equity) 4.85Ardevora Global Equity Fund 2.83Aptus Global Financials Fund 2.02Specialist (Non Equity) 12.39Majedie Asset Management Tortoise Fund 5.01Old Mutual UK Specialist Equity Fund 3.52Man GLG UK Absolute Value Fund 1.93iShares Physical Gold ETC 1.91Cash 9.69Total 100.00

Portfolio breakdown %UK 14.02Majedie UK Focus Fund 4.95The Heronbridge United Kingdom Equity Fund 3.47Old Mutual UK Dynamic Equity Fund 2.77GVQ UK Focus Fund 2.53River and Mercantile UK Micro Cap Investment Company Limited 2.26

J O Hambro Capital Management UK Growth Fund 1.90

FTSE 100 Index Futures -3.85Fixed Income 3.61Legg Mason Western Asset Macro Opportunities Bond Fund 2.19

Barings Emerging Markets Debt Blended Total Return Fund 1.42

North America 15.21Artemis US Extended Alpha Fund 5.77Conventum - Lyrical Fund 5.55Findlay Park American Fund 3.76Edgewood L Select US Select Growth Fund 2.06S&P 500 Index Futures -1.93Europe 14.65Memnon European Fund 4.95Schroder European Alpha Plus Fund 4.44FP Crux European Special Situations Fund 4.43Edinburgh Partners European Opportunities Fund 2.82

Euro Stoxx 50 Index Futures -1.99Japan 8.85Schroder International Selection Fund - Japanese Opportunities 3.31

CC Japan Alpha Fund 3.21CF Morant Wright Nippon Yield Fund 2.33Asia 12.07BGF Asian Growth Leaders Fund 3.96Hermes Asia ex-Japan Equity Fund 3.49Prusik Asian Equity Income Fund 2.61TT Asia-Pacific Equity Fund 2.01Emerging Markets 4.54TT Emerging Markets Unconstrained Fund 2.51Hermes Global Emerging Markets Fund 2.03Specialist (Equity) 4.92Ardevora Global Equity Fund 2.92Aptus Global Financials Fund 2.00Specialist (Non Equity) 13.02Majedie Asset Management Tortoise Fund 4.80Old Mutual UK Specialist Equity Fund 4.34Man GLG UK Absolute Value Fund 2.02iShares Physical Gold ETC 1.86Cash 9.11Total 100.00

Portfolio breakdown %UK 7.87Majedie UK Focus Fund 2.92Old Mutual UK Dynamic Equity Fund 2.51The Heronbridge United Kingdom Equity Fund 2.44North America 41.52Artemis US Extended Alpha Fund 7.68Conventum - Lyrical Fund 7.34Findlay Park American Fund 6.60William Blair U.S. Small-Mid Cap Growth Fund 5.74Majedie Asset Management US Equity Fund 5.01Hamlin High Dividend Equity UCITS Fund 4.83Edgewood L Select US Select Growth Fund 4.33Europe 20.80Memnon European Fund 6.47FP Crux European Special Situations Fund 5.65Edinburgh Partners European Opportunities Fund 4.89

DNCA European Select Equity Fund 3.79Japan 8.97CC Japan Alpha Fund 3.06Alma Capital Investment Funds – Alma Eikoh Japan Large Cap Equity Fund 2.97

CF Morant Wright Nippon Yield Fund 2.94Asia 10.26Prusik Asian Equity Income Fund 3.94TT Asia-Pacific Equity Fund 3.21Hermes Asia ex-Japan Equity Fund 3.12Emerging Markets 4.63TT Emerging Markets Unconstrained Fund 4.63Specialist (Equity) 2.05Aptus Global Financials Fund 2.05Specialist (Non Equity) 3.99Majedie Asset Management Tortoise Fund 1.77Man GLG UK Absolute Value Fund 1.30iShares Physical Gold ETC 0.92Cash -0.10Total 100.00

Informed investor

Issue 21 | Spring 2018 | Informed investor 9

Source: BMO Global Asset Management. Data as at 31.01.18

Informed investor

F&C MM Lifestyle Foundation Fund

F&C MM Lifestyle Defensive Fund

Portfolio breakdown %UK 10.79F&C FTSE All-Share Tracker Fund 2.28Majedie UK Income Fund 2.11Man GLG Undervalued Assets Fund 2.04River and Mercantile UK Equity Income Fund 2.01Jupiter UK Smaller Companies Fund 1.75River and Mercantile UK Equity Long Term Recovery Fund 1.57

FTSE 100 Index Futures -0.98Gilts 10.23iShares UK Gilts 0-5yr UCITS ETF 6.23iShares UK Gilts UCITS ETF 4.00UK Index Linked Bonds 7.03iShares £ Index-Linked Gilts UCITS ETF 7.03International Bonds 10.05M&G Global Macro Bond Fund 3.63Legg Mason Western Asset Macro Opportunities Bond Fund 3.60

Barings Emerging Markets Debt Blended Total Return Fund 2.81

Europe ex UK 1.93Oyster - Continental European Selection 1.93Japan 4.42Eastspring Investments – Japan Dynamic Fund 1.98Baillie Gifford Japanese Fund 1.22Tokio Marine Japanese Equity Focus Fund 1.21Pacific Ex Japan 2.46BGF Asian Growth Leaders Fund 2.46North America 4.53Majedie Asset Management US Equity Fund 2.83HSBC S&P 500 UCITS ETF 1.70Property 5.79Darwin Leisure Property Fund 1.93GCP Student Living plc 1.46F&C Real Estate Securities Fund 1.29Custodian REIT 1.12UK Corporate Bonds 17.43Royal London Sterling Credit Fund 6.46Henderson Strategic Bond Fund 4.48Invesco Perpetual Tactical Bond Fund 3.99MI TwentyFour Monument Bond Fund 2.50Absolute Return 4.92 Majedie Asset Management Tortoise Fund 2.63Man GLG UK Absolute Value Fund 2.29Commodities 1.43iShares Physical Gold ETC 1.43Cash 18.99Total 100.00

Portfolio breakdown %UK 15.82F&C FTSE All-Share Tracker Fund 3.45Man GLG Undervalued Assets Fund 3.05Majedie UK Income Fund 2.98River and Mercantile UK Equity Income Fund 2.79Jupiter UK Smaller Companies Fund 2.61River and Mercantile UK Equity Long Term Recovery Fund 2.14

FTSE 100 Index Futures -1.20Gilts 5.80iShares UK Gilts 0-5yr UCITS ETF 3.29iShares UK Gilts UCITS ETF 2.51UK Index Linked Bonds 3.77iShares £ Index-Linked Gilts UCITS ETF 3.77International Bonds 4.61Legg Mason Western Asset Macro Opportunities Bond Fund 2.25

M&G Global Macro Bond Fund 1.37Barings Emerging Markets Debt Blended Total Return Fund 0.98

Europe ex UK 3.97Oyster - Continental European Selection 1.96Schroder European Alpha Plus Fund 2.00Japan 6.46Eastspring Investments – Japan Dynamic Fund 2.97Tokio Marine Japanese Equity Focus Fund 2.00Baillie Gifford Japanese Fund 1.49Pacific Ex Japan 6.49 BGF Asian Growth Leaders Fund 1.97Hermes Asia ex-Japan Equity Fund 2.28TT Asia-Pacific Equity Fund 2.24North America 8.44 Majedie Asset Management US Equity Fund 4.74HSBC S&P 500 UCITS ETF 3.70Property 5.78Darwin Leisure Property Fund 1.99GCP Student Living plc 1.41Custodian REIT 1.14F&C Real Estate Securities Fund 1.25UK Corporate Bonds 18.55Royal London Sterling Credit Fund 6.01Henderson Strategic Bond Fund 4.51Invesco Perpetual Tactical Bond Fund 3.52MI TwentyFour Monument Bond Fund 3.09Allianz Strategic Bond Fund 1.42Absolute Return 4.97 Majedie Asset Management Tortoise Fund 2.66Man GLG UK Absolute Value Fund 2.31Global High Yield Bonds 1.02 Hermes Multi Strategy Credit Fund 1.02Commodities 1.52 iShares Physical Gold ETC 1.52Cash 12.81Total 100.00

10 Informed investor | Issue 21 | Spring 2018

F&C MM Lifestyle Funds

Our range of risk-targeted multi-manager funds with strategic asset allocations are designed to deliver returns appropriate for five specific attitudes to risk. The funds are rebalanced on a regular basis to ensure they match your attitude to risk at the time you invest and on an ongoing basis.

"Picking managers has always been the key driver of your portfolio’s composition."

Source: BMO Global Asset Management. Data as at 31.01.18

Informed investor

F&C MM Lifestyle Cautious Fund

F&C MM Lifestyle Balanced Fund

F&C MM Lifestyle Growth Fund

Portfolio breakdown %UK 22.64F&C FTSE All-Share Tracker Fund 5.48Majedie UK Income Fund 4.17Man GLG Undervalued Assets Fund 4.12River and Mercantile UK Equity Income Fund 3.96Jupiter UK Smaller Companies Fund 3.37River and Mercantile UK Equity Long Term Recovery Fund 2.73

FTSE 100 Index Futures -1.19Gilts 3.02iShares UK Gilts UCITS ETF 3.02Europe ex UK 3.89Oyster - Continental European Selection 1.95Schroder European Alpha Plus Fund 1.94Japan 8.40Eastspring Investments – Japan Dynamic Fund 3.95Tokio Marine Japanese Equity Focus Fund 2.48Baillie Gifford Japanese Fund 1.98Pacific Ex Japan 6.77BGF Asian Growth Leaders Fund 2.00Hermes Asia ex-Japan Equity Fund 2.25Macquarie Fund Solutions – Macquarie Asian All Stars Fund 0.00

TT Asia-Pacific Equity Fund 2.52North America 10.51 Majedie Asset Management US Equity Fund 5.90HSBC S&P 500 UCITS ETF 4.62Property 4.82Darwin Leisure Property Fund 1.73GCP Student Living plc 1.15Custodian REIT 0.89F&C Real Estate Securities Fund 1.05UK Corporate Bonds 18.53Royal London Sterling Credit Fund 6.01Henderson Strategic Bond Fund 4.52Invesco Perpetual Tactical Bond Fund 3.70MI TwentyFour Monument Bond Fund 3.01Allianz Strategic Bond Fund 1.29Absolute Return 4.95 Majedie Asset Management Tortoise Fund 2.64Man GLG UK Absolute Value Fund 2.31Global High Yield Bonds 1.94 Hermes Multi Strategy Credit Fund 1.94Emerging Markets 5.84Hermes Global Emerging Markets Fund 3.04TT Emerging Markets Unconstrained Fund 2.79Commodities 1.41iShares Physical Gold ETC 1.41Cash 7.29Total 100.00

Portfolio breakdown %UK 27.64F&C FTSE All-Share Tracker Fund 6.64Majedie UK Income Fund 5.09Man GLG Undervalued Assets Fund 4.81River and Mercantile UK Equity Income Fund 4.68Jupiter UK Smaller Companies Fund 4.18River and Mercantile UK Equity Long Term Recovery Fund 3.25

FTSE 100 Index Futures -1.01Europe ex UK 4.84Oyster - Continental European Selection 2.42Schroder European Alpha Plus Fund 2.42Japan 9.35Eastspring Investments – Japan Dynamic Fund 4.60Tokio Marine Japanese Equity Focus Fund 2.73Baillie Gifford Japanese Fund 2.02Pacific Ex Japan 9.78TT Asia-Pacific Equity Fund 3.52Hermes Asia ex-Japan Equity Fund 3.26BGF Asian Growth Leaders Fund 3.00North America 10.43Majedie Asset Management US Equity Fund 5.84HSBC S&P 500 UCITS ETF 4.59Property 2.96Darwin Leisure Property Fund 1.23F&C Real Estate Securities Fund 1.05Custodian REIT 0.68UK Corporate Bonds 12.80Royal London Sterling Credit Fund 5.49Invesco Perpetual Tactical Bond Fund 3.67Henderson Strategic Bond Fund 3.64Absolute Return 4.93 Majedie Asset Management Tortoise Fund 2.60Man GLG UK Absolute Value Fund 2.33Global High Yield Bonds 1.93Hermes Multi Strategy Credit Fund 1.93Emerging Markets 8.78TT Emerging Markets Unconstrained Fund 3.05Hermes Global Emerging Markets Fund 3.01iShares Emerging Markets Equity Index Fund 2.72Commodities 1.30iShares Physical Gold ETC 1.30Cash 5.26Total 100.00

Portfolio breakdown %UK 31.90F&C FTSE All-Share Tracker Fund 7.47Majedie UK Income Fund 5.90Man GLG Undervalued Assets Fund 5.70River and Mercantile UK Equity Income Fund 5.61Jupiter UK Smaller Companies Fund 4.46River and Mercantile UK Equity Long Term Recovery Fund 3.54

FTSE 100 Index Futures -0.78Europe ex UK 4.89Oyster - Continental European Selection 2.46Schroder European Alpha Plus Fund 2.43Japan 9.80Eastspring Investments – Japan Dynamic Fund 4.61Tokio Marine Japanese Equity Focus Fund 2.90Baillie Gifford Japanese Fund 2.29Pacific Ex Japan 14.87BGF Asian Growth Leaders Fund 4.79Hermes Asia ex-Japan Equity Fund 5.02TT Asia-Pacific Equity Fund 5.06Macquarie Fund Solutions – Macquarie Asian All Stars Fund 0.00

North America 8.55Majedie Asset Management US Equity Fund 4.88HSBC S&P 500 UCITS ETF 3.67Property 2.94Darwin Leisure Property Fund 1.25F&C Real Estate Securities Fund 1.01Custodian REIT 0.69UK Corporate Bonds 1.53Henderson Strategic Bond Fund 1.53Absolute Return 4.98Majedie Asset Management Tortoise Fund 2.63Man GLG UK Absolute Value Fund 2.35Global High Yield Bonds 2.95Hermes Multi Strategy Credit Fund 2.95Emerging Markets 14.85Hermes Global Emerging Markets Fund 5.01TT Emerging Markets Unconstrained Fund 5.09iShares Emerging Markets Equity Index Fund 4.74Commodities 1.31iShares Physical Gold ETC 1.31Cash 1.42Total 100.00

Issue 21 | Spring 2018 | Informed investor 11

Source: BMO Global Asset Management. Data as at 31.01.18

© 2018 BMO Global Asset Management. All rights reserved. BMO Global Asset Management is a trading name of F&C Management Limited, which is authorised and regulated by the Financial Conduct Authority. CM15766 (03/18). UK

If you have any queries about your investment please contact us. Please remember to quote your account number on all communications with us.

0330 123 3798 (weekdays 9am-5pm, calls may be recorded for training and monitoring purposes)

F&C Fund Management Limited PO Box 9040 Chelmsford Essex CM99 2XH

Contact us

For existing investors only. Articles in this newsletter are only intended to provide a general outline of the subject and should not be considered comprehensive nor a sufficient basis for making decisions. It is not investment research and has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. Investors requiring advice on their individual circumstances should consult their financial adviser. Prospective investors should consult the Prospectus and Key Investor Information Document for the relevant share class available from their financial adviser or BMO Global Asset Management.