BMEI 2017 Full Report English 19APR - pressroom home sheet/BM… · MISCELLANEOUS CHEMICAL PRODUCTS...

39

2017

Transcript of BMEI 2017 Full Report English 19APR - pressroom home sheet/BM… · MISCELLANEOUS CHEMICAL PRODUCTS...

2017

Index

P.01 1. General Overview

P.01 2. Objectives

P.01 3. Sample: sectors, selection criteria and composition

P.01 3.1 Sectors evaluated for survey and regional trade flows

P.03 3.2 Geographic breakdown

P.03 3.3 Profile of importers selected for the survey

P.05 3.4 Type of executive interviewed

P.05 4. Methodology

P.06 5. Main FindingsP.06 5.1 Main highlights

P.07 5.2 Searching for new international suppliers

P.08 5.3 Contacting new international suppliers

P.13 5.4 Making purchasing decisions

P.18 5.5 Finalizing the purchase

P.22 5.6 Import process: supply chain

P.31 6. Sector specific highlights

P.31 6.1 Propensity to import by sector

P.32 6.2 Apparel

P.33 6.3 Automotive

P.34 6.4 High-tech

P.35 6.5 Industrial Manufacturing

P.36 7. Conclusions: highlights and insights

AnnexesAnnex 1: Apparel sector report

Annex 2: Automotive sector report

Annex 3: High-tech sector report

Annex 4: Industrial manufacturing sector report

1. General Overview

UPS Business MonitorTM Export Index Latin America 2017 is the result of interviews with 2,170

small and medium-sized importers throughout the Americas conducted to study their

online/offline purchasing behavior. The study’s focus on importers (buyers) reveals strategically

useful information that will help exporters to sell and supply goods in international markets.

2. Objectives

The BMEI 2017’s assessment of the purchasing behavior of small and medium-sized importers

in the Americas addresses several objectives:

• Identify importer’s preferred online and offline means of contact when evaluating new

suppliers and the criteria used to assess product, to enable exporters to adjust their international

promotion.

• Assess and estimate the magnitude of import transactions conducted over the Internet, broken

down by the four selected industries.

• Detect the critical factors in the supply chain that influence an importer’s purchasing

decisions.

• Track importer behavior from the closing of the transaction to handling of damaged products,

identifying critical issues in order to identify opportunities for improvement in the process.

3. Sample: sectors, selection criteria and composition

3.1 Sectors evaluated for the BMEI 2017

Four industries were chosen for the BMEI 2017: industrial manufacturing, automotive, apparel

and high-tech.

These four export sectors were identified based on a cross section of the following four

variables:

1. High participation in US trade

2. High participation in intra-regional Latin American trade

3. Demand/use of express courier services

4. Estimated density of exporters

In order to determine the levels of participation in intra-regional Latin American and US trade

flows, the main imports into the United States from Latin America and the main Latin American

imports from other Latin American countries were analyzed. Table 1 and Table 2 on the

following page highlight trade flows for the 15 main products in each market.

01

SectorsUS Imports: Latin

American origin in USD

billions

ALL PRODUCTS 452.88

FUELS 92.37

AUTO PARTS AND VEHICLES 69.02

MACHINERY, ELECTRICAL EQUIPMENT AND PARTS 66.56

MACHINERY AND MECHANICAL DEVICES 47.78

FOOD 35.82

APPAREL AND FOOTWEAR 17.50

INSTRUMENTS, OPTICAL INSTRUMENTS, MEASUREMENT, PHOTOGRAPHY

AND CINEMATOGRAPHY13.87

JEWELRY 13.79

MATERIALS ELSEWHERE NOT SPECIFIED 13.52

FURNITURE AND FIXTURES 10.06

BEVERAGES 9.99

IRON AND STEEL 7.22

PLASTICS AND ARTICLES MADE OF PLASTICS 5.70

ARTICLES OF CAST IRON OR STEEL 5.10

Source: International Trade Center (Trade Map) based on the latest official data available, 2014 for the US.

SectorsLATAM Imports: Latin American

origin in USD billions

ALL PRODUCTS 213.92

FUELS 43.39

FOOD 36.90

AUTO PARTS AND VEHICLES 29.49

MACHINERY, ELECTRICAL EQUIPMENT AND PARTS 12.50

MACHINERY AND MECHANICAL DEVICES 11.73

PLASTICS AND ARTICLES MADE OF PLASTICS 8.79

APPAREL AND FOOTWEAR 6.99

PHARMACEUTICAL PRODUCTS 5.18

IRON AND STEEL 4,95

ESSENTIAL OILS AND RESINOIDS; PREPARATION OF PERFUMERY,

SOAPS4.04

PAPER, CARDBOARD, PRODUCTS MADE FROM PULP, PAPER,

CARDBOARD3.70

COPPER AND COPPER MANUFACTURED PRODUCTS 3.50

MISCELLANEOUS CHEMICAL PRODUCTS 3.36

ORGANIC CHEMICAL PRODUCTS 3.34

Table 2: Latin American imports 2013 (Latin American origin) by sector

Table 1: US imports 2014 (Latin American origin) by sector

Source: International Trade Center (Trade Map) based on the latest official data available, 2013 for Latin America.

02

The following table presents Latin American importers’ annual US dollar (USD)

purchases of 15 Latin American products broken down by sector.

The following table presents US importers’ annual US dollar (USD) purchases of

15 Latin American products broken down by sector.

COUNTRIESINDUSTRIAL

MANUFACTURINGAUTOMOTIVE APPAREL HIGH TECH TOTAL

UNITED STATES 250 84 50 50 434

MEXICO 146 50 50 50 296

BRAZIL 90 50 50 50 240

COLOMBIA 50 50 50 50 200

CHILE 50 50 50 50 200

PERU 50 50 50 50 200

COSTA RICA 50 50 50 50 200

DOMINICAN REP. 50 50 50 50 200

PANAMA 50 50 50 50 200

3.2 Geographic breakdown:

With the main industries of interest

defined based on trade flows and other

critical factors, UPS chose to focus on

nine specific markets: Brazil, Chile,

Colombia, Costa Rica, Dominican

Republic, Mexico, Panama, Peru and the

United States.

To analyze the import/export behavior in

each one of the countries selected for this

study, a sample per country was defined

based on the size ratio between each

market with a margin of error between

+/- 4.7% and +/- 9.1%.

3.3 Profile of importers selected for the survey

Furthermore, as part of the selection criteria, the study interviewed small and medium-

sized enterprises (SME) because this segment represents the lion’s share of foreign trade

transactions in the Americas. An additional criterion applied to the sample was that all

selected importers had to have performed at least five import transactions in the 12

months prior to the interview.

As a result, 2,170 importers were identified and interviewed, for an overall margin of

error +/- 2.3 %, according to the Calculation of the Probability of a Sample used in this

type of research.

Table 3: Sample broken down by country and sector

03

-

Dominican

Republic

US

TYPES OF COMPANIES %

DISTRIBUTOR 38%

MANUFACTURER 24%

WHOLESALER 12%

STORE/RETAILER 7%

OTHER 16%

TOTAL 97%*

TYPES OF PRODUCTS IMPORTED %

FINISHED GOODS FOR RESALE 61%

FINISHED GOODS FOR IN-HOUSE USE 15%

RAW MATERIALS FOR PRODUCTION 15%

SEMI-MANUFACTURED FOR PRODUCTION 6%

OTHER 3%

TOTAL 100%

2,170interviews

INDUSTRIAL

MANUFACTURING

36%

AUTOMOTIVE

22%

APPAREL

21%

HIGH-TECH

21%

Table 4: Sample summary(Percentages may not total 100 due to rounding.)

DISTRIBUTOR 38%FINISHED GOODS 61%

04

* 3% of surveyed participants did not respond to this question.

COUNTRIES US MX BR CO CHI PE CR DR PA TOTAL

MANUFACTURER 36% 39% 33% 25% 10% 11% 10% 13% 20% 24%

DISTRIBUTOR 39% 39% 25% 34% 39% 41% 50% 35% 36% 38%

WHOLESALER 8% 8% 12% 15% 16% 11% 15% 14% 12% 12%

RETAILER 3% 1% 14% 2% 7% 6% 9% 19% 7% 7%

OTHER 5% 12% 16% 22% 26% 27% 14% 18% 20% 16%

NO RESPONSE 9% 1% 0% 2% 2% 4% 2% 1% 5% 3%

3.4 Type of executive interviewed

Finally, in order to achieve the study’s objectives, the individuals responsible for

international purchases were interviewed. The import decision makers were asked a series

of questions based on a semi-structured questionnaire for a quantitative and qualitative

result.

4. Methodology

The semi-structured questionnaire broke down the typical import process into five distinct

stages—search for new international suppliers; contacting new international suppliers;

making purchasing decisions; finalizing the purchase; import process: supply chain.

The participating importers were contacted and asked the questions over the telephone

using a CATI system (computer-assisted telephone interviewing).

Table 5: Sample broken down by country and type of importer

05

Note: Percentages may not total 100 due to rounding.

5. Main Findings

5.1 Highlights

UPS Business MonitorTM Export Index Latin America 2017 identifies clear trends among the

region’s importers that extend across four industries in nine countries.

The main trends identified were:

ü Propensity (i.e., willingness) to import by country and by sector;

ü Digital versus traditional behavior when searching for new suppliers;

ü Value assigned to an exporter’s website;

ü Online purchasing behavior;

ü Main attributes other than price and quality that importers value the most when assessing

potential vendors;

ü Use of promotional tools supplied by the exporter;

ü Main importing barriers.

Among the greatest similarities found were the attributes that importers value the most when

assessing potential vendors; their preferred online and offline channels used to search for

suppliers; and the main importing barriers faced.

The findings also reveal industry-specific and country-specific insights in addition to the

general trends identified. For example, in the case of online purchases, the BMEI 2017

revealed that 57% of importers (from the total sample) do not purchase their imported

products online from start to finish. However, when the results were analyzed by industry,

considerable differences were found. For example in the automotive sector, 74% of

respondents indicated that they do not purchase imported products online. In analyzing

responses for a particular sector in specific countries, additional insight was revealed, e.g.,

80% of apparel importers in Brazil and Costa Rica do not purchase imported products online.

This report presents the main findings for the entire sample of SMEs interviewed, highlighting

the most relevant insights for each sector and individual countries.

In addition to the general findings in this report, there is an index of the propensity to import

for each of the four industries analyzed –see pages 31-35.

06

5.2 Searching for new suppliers

In the first part of the questionnaire, importers

were asked if they are currently searching for

new international suppliers. The objective of

the question was to determine the current

demand for new suppliers in the Americas.

Almost half (47%) of the importers

interviewed responded that they are actively

seeking new international suppliers, which

suggests that there is an opportunity for

exporters to find new buyers and increase their

sales in the region.

Variations by industry were slight. The

percentage of those seeking new suppliers is

the highest in the high-tech sector (49%

versus 47% on average), not surprising, given

Is your company currently

searching for new international

suppliers? (Simple response)

47%

52%

1%

Yes No Na/Dk No response

that it is an industry marked by dynamic product development. In turn, the propensity to

import is the lowest among industrial manufacturers (45%).

In terms of the geographical breakdown of the results, the responses were very consistent

throughout the region. In most of the countries surveyed, the responses were almost evenly

divided 50:50, leaning slightly higher toward not searching for new suppliers in every case

except Costa Rica, which was the only country out of the nine where the tables were turned

with 56% seeking new suppliers. In the US, 60% of all importers responded that they are not

currently seeking new suppliers, the highest level recorded.

Not surprisingly, in the case of those importers seeking a new supplier (47% of the total

sample), two out of three (67%) indicated that finding suppliers is the most important aspect

07

Achieving a long-lasting relationship in foreign trade is based on several

factors that exporters can control, such as ensuring a consistent supply of

product and stable business conditions (replacement and warranty policies,

flexible payment terms and financing). These factors all weighed in heavily

when importers were asked to evaluate different aspects of potential

suppliers, and what emerged was a profile of the supplier that importers are

either seeking—or believe they have found.

of the supply chain, whereas less than half (49%) of those not seeking new suppliers (52%

of the total sample), indicated it as such.

In turn, two out of every three (66%) importers not looking for new suppliers do not purchase

their imported products online, which is slightly higher than the average of the total sample

(57%).

5.3 Contacting new international suppliers

After determining that one out of every two (47%) importers are looking for new

international suppliers, they were asked to indicate their preferred offline and online channels

for conducting their search.

Industry fairs and trade shows were named as the most widely used offline channel for

finding new suppliers (28%). Trade missions were named as the second most frequently used

channel.

What offline channels does your company use to contact new

international suppliers? (Multiple responses)

28%

21%

17%

10% 9% 7% 6%

2% 0%

5%

10%

15%

20%

25%

30%

Industry fairs and

trade shows

I don’t contact

them; they contact me.

Trade mission to country of

origin

Traditional advertising

(print, radio,

television)

Telephone directories

Other Dk/Na No response

08

There was a high percentage of importers who indicated that they do not actively search for

suppliers via offline channels, but rather they expect potential suppliers to contact them

(21%).

A breakdown by country revealed two exceptions to the average throughout the region:

Brazilians were the most proactive, with only 5% indicating that they do not contact new

suppliers but rather wait to be contacted. Whereas, importers in the US were the least

proactive, with one out of three (31%) indicating that they do not contact suppliers.

The passive and permissive attitude of the 21% of respondents who indicated that they

expect suppliers to contact them (combined with the 52% who indicated that they are not

seeking new suppliers) reflects the importance of focused and well-researched business

proposals. The same indicator highlights the opportunity for proactive exporters who reach

out to buyers directly via email or over the telephone.

The analysis of the means by which importers find suppliers included their use of online

channels.

What online channels does your company use to contact new

international suppliers? (Multiple responses)

Top three responses.

09

32%22%

10%

Search engines

(Google, Yahoo, etc.)

Suppliers

contact me

via email

B2B portals and

e-commerce

marketplaces

10

Note: Anti-spam regulations vary by country and an exporter should review them in the market of interest.

The most widely used online channels for searching for new suppliers cited were search

engines (32% of total responses), followed by the importer’s response to contact initiated by

the vendor via email (22%) and supplier advertising received by email (10%).

Interestingly, the percentage of respondents who indicated that they do not contact new

suppliers dropped to 7% in the case of online channels, down from 21% in the case of offline

channels. On the one hand, this indicates the greater ease of contact that the Internet offers,

making it possible to overcome barriers that face-to-face or telephone conversations may

pose (language, geography, time differences). On the other, there was also an overwhelming

number of importers who indicated that sellers are contacting them via email (personalized

emails and supplier advertising) for a combined total of 32% of responses, the same as search

engines.

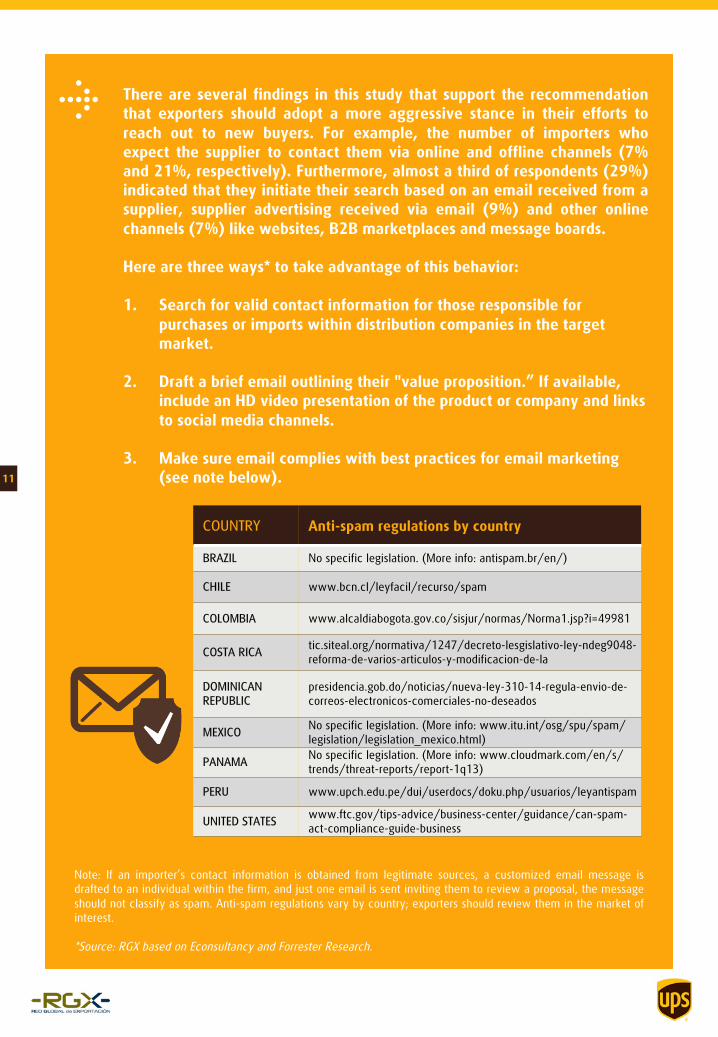

There are several findings in this study that support the recommendation

that exporters should adopt a more aggressive stance in their efforts to

reach out to new buyers. For example, the number of importers who

expect the supplier to contact them via online and offline channels (7%

and 21%, respectively). Furthermore, almost a third of respondents (29%)

indicated that they initiate their search based on an email received from a

supplier, supplier advertising received via email (9%) and other online

channels (7%) like websites, B2B marketplaces and message boards.

Here are three ways* to take advantage of this behavior:

1. Search for valid contact information for those responsible for

purchases or imports within distribution companies in the target

market.

2. Draft a brief email outlining their "value proposition.” If available,

include an HD video presentation of the product or company and links

to social media channels.

3. Make sure email complies with best practices for email marketing

(see note below).

COUNTRY Anti-spam regulations by country

BRAZIL No specific legislation. (More info: antispam.br/en/)

CHILE www.bcn.cl/leyfacil/recurso/spam

COLOMBIA www.alcaldiabogota.gov.co/sisjur/normas/Norma1.jsp?i=49981

COSTA RICAtic.siteal.org/normativa/1247/decreto-lesgislativo-ley-ndeg9048-

reforma-de-varios-articulos-y-modificacion-de-la

DOMINICAN

REPUBLIC

presidencia.gob.do/noticias/nueva-ley-310-14-regula-envio-de-

correos-electronicos-comerciales-no-deseados

MEXICONo specific legislation. (More info: www.itu.int/osg/spu/spam/

legislation/legislation_mexico.html)

PANAMANo specific legislation. (More info: www.cloudmark.com/en/s/

trends/threat-reports/report-1q13)

PERU www.upch.edu.pe/dui/userdocs/doku.php/usuarios/leyantispam

UNITED STATESwww.ftc.gov/tips-advice/business-center/guidance/can-spam-

act-compliance-guide-business

Note: If an importer’s contact information is obtained from legitimate sources, a customized email message is

drafted to an individual within the firm, and just one email is sent inviting them to review a proposal, the message

should not classify as spam. Anti-spam regulations vary by country; exporters should review them in the market of

interest.

*Source: RGX based on Econsultancy and Forrester Research.

11

Today, search engines are a way for exporting SMEs to gain greater

visibility at a relatively low cost. They can increase the possibility

of potential buyers finding them. Based on the findings, it is

important that exporters maximize the number of visitors to their

websites by ensuring that their site appears high on the list of

search engine results, also known as search engine optimization

(SEO).

Table 6: Online channels used by importers to contact new suppliers. Results broken down by

country (multiple response)

A breakdown by country reveals that in Mexico, Panama, Peru, Dominican Republic and the US,

there is a high incidence of suppliers contacting importers via email.

In the case of Panama, the response tied with search engines as the main means of

communication when initially establishing contact with a new supplier (28%).

Brazil and Dominican Republic were the two markets where the highest percentage of importers

(15% in both cases) indicated B2B portals and e-commerce marketplaces as a preferred online

channel for contacting importers.

12

B2B ande-commercesites

Searchengines

Sector-specific directories

Social media

Supplier advertising(via email)

I don’t contact them; they contact me

Suppliers contact me via email

Other

DK

Unanswered

Brazil Chile Colombia Costa Rica Mexico Panama Peru Dominican Rep. US

Source: Stella Tomasi and Xiaolin Li. 2015. Influences of Search Engine Optimization on Performance of SMEs: A Qualitative Perceptive.

J. Electron. Commer. Organ. 13, 1 (January 2015), 27-49. DOI=http://dx.doi.org/10.4018/jeco.2015010103

5.4 Making purchasing decisions

The main factors that impact an

importer’s purchasing decisions were

assessed based on participants’ responses

to four questions:

1. Does a supplier’s website influence

your company's assessment of an

international supplier?

2. What are the website sections or

content that you value the most?

3. What are the most important factors

when evaluating a potential vendor?

4. What are the most important product

attributes?

As part of the analysis of the factors that

importers take into account when making

a purchasing decision, they were first

asked whether a supplier’s website

influenced their decision to do business

with a particular vendor. As can be seen

in the figure to the right, six out of every

ten (59%) respondents said that an

international supplier’s website does

influence their decision.

Does a supplier’s website influence

your company's assessment of an

international supplier? (Single

response)

59%

39%

2%

Yes No Dk/Na

Based on the study’s finding regarding the value that buyers assign to

websites, it is recommended that exporters review and revise their website

content to ensure that the information addresses a potential buyer’s need for

information, communicating the product’s attributes in a clear manner in the

buyer’s language.

13

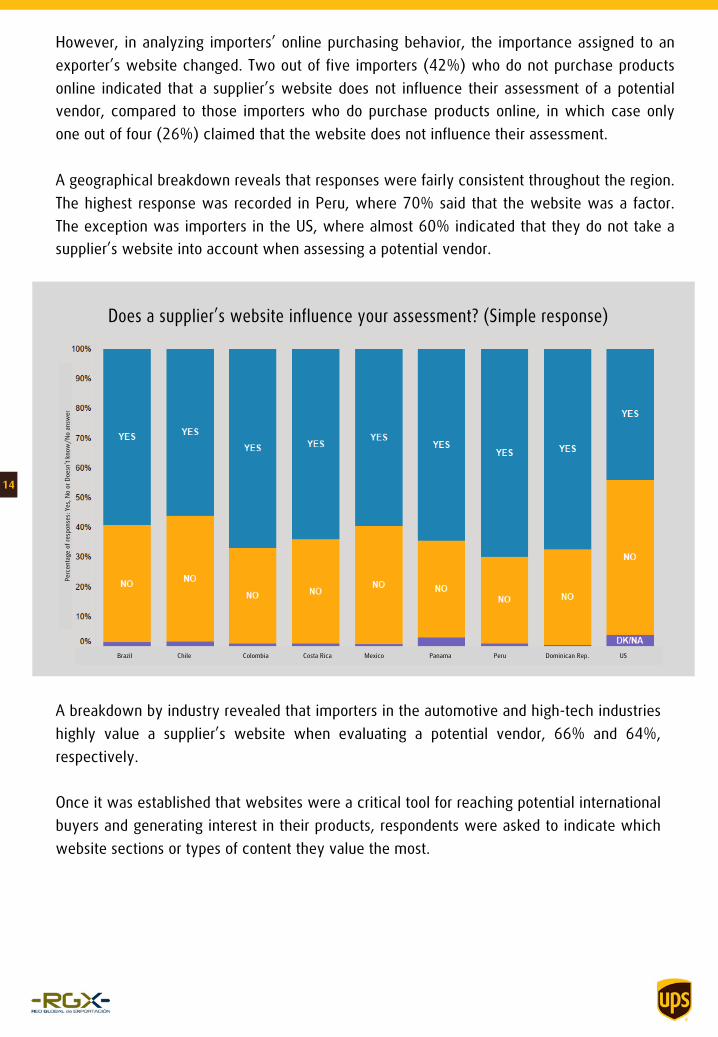

However, in analyzing importers’ online purchasing behavior, the importance assigned to an

exporter’s website changed. Two out of five importers (42%) who do not purchase products

online indicated that a supplier’s website does not influence their assessment of a potential

vendor, compared to those importers who do purchase products online, in which case only

one out of four (26%) claimed that the website does not influence their assessment.

A geographical breakdown reveals that responses were fairly consistent throughout the region.

The highest response was recorded in Peru, where 70% said that the website was a factor.

The exception was importers in the US, where almost 60% indicated that they do not take a

supplier’s website into account when assessing a potential vendor.

A breakdown by industry revealed that importers in the automotive and high-tech industries

highly value a supplier’s website when evaluating a potential vendor, 66% and 64%,

respectively.

Once it was established that websites were a critical tool for reaching potential international

buyers and generating interest in their products, respondents were asked to indicate which

website sections or types of content they value the most.

14

Perc

enta

ge o

f re

sponse

s: Y

es,

No o

r D

oesn

’t k

now

/N

o a

nsw

er

Does a supplier’s website influence your assessment? (Simple response)

Brazil Chile Colombia Costa Rica Mexico Panama Peru Dominican Rep. US

Three out of four respondents (73%) across all four industries in all nine countries surveyed

named at least four types of website content as highly important:

• Technical specifications of products

• Product certifications/Product warranty

• “Who we are/About Us” section (company experience, history, etc.)

• Product-specific export information (trade terms, freight information, etc.)

Of the different types of website content, technical specifications and product

warranty/certifications were consistently cited as the most important in all nine countries.

15%

8%

6%

2%

2%

18%

10%

52%

73%

76%

87%

88%

0% 20% 40% 60% 80% 100%

Client opinions, testimonials

Product-specific export information (Trade Terms, freight information, etc.)

“Who we are/About Us” section (company experience, history, etc.)

Product certifications/product warranty

Technical specifications of products

Highly important

Fairly important

Not important

11%

19%

How important are the following website sections/content to your assessment

of an international supplier? (Multiple responses)

Furthermore, the two types of website content most highly valued by importers are closely

linked to the perception of product quality, which was consistently named as the main factor

that the respondents took into consideration when deciding to make a purchase (see the

graph on page 16).

15

33%

When asked about the main factors taken into account when evaluating a potential supplier,

importers indicated that they look at several aspects, from the product itself to the services a

seller may offer to facilitate purchases. Product quality and price were the two top responses,

followed by seller services, such as, more flexibility in payment terms and after-sales services.

Interestingly, the majority of respondents cited several factors as highly important.

Three out of every four respondents (74%) cited five factors as highly important: price, quality,

logistics services, flexible payment terms and after-sales services, with no single one heavily

outweighing the others. Logistics tracking tools and promotional tools were still rated as highly

important by over half of all respondents.

How important are each of the following factors to your company when deciding to

purchase from an international supplier? (Multiple responses)

97% 88%

78% 78% 74%

61% 58%

3% 10%

18% 18% 20%

30% 29%

0% 2% 4% 4% 5% 9%

13%

0%

20%

40%

60%

80%

100%

120%

Product quality Price Shipping and logistics services

offered

Flexible payment terms

After-sales service Logistics tracking tools

Promotional support/tools

Highly important

Fairly important

Not at all important16

*Percentages may not total 100 due to rounding.

Given that the product itself is the main

component assessed by importers when

deciding whether to make a purchase

from a particular vendor, importers were

asked which product attributes influence

their purchasing decision the most.

Not surprisingly, the top two results were

quality and price (see table below),

which is in line with the overwhelming

response regarding product quality and

price in the previous question. In regard

to product attributes, suitability in terms

of local demand and certified

manufacturing processes tied as the most

influential factors after price and quality.

Interestingly, one out of every two

importers (48%) named at least six

factors that influence the company’s

decision to purchase a particular product.

With respect to the materials that you import, which of the following product

attributes influence your company’s purchasing decision? (Multiple responses)

According to ISO, an

independent, non-governmental global

organization with a membership of 162

national standards bodies, international

standards “are instrumental in facilitating

international trade.”

ISOhaspublishedmorethan21,000standards, coveringalmosteveryindustry.Industry-specificstandardsinclude:

Automotive: ISO/TS16949

Apparel and footwear: ISO9001/WRAP

High-tech and industrial manufacturing:

ISO 9001

For more information, visit: www.iso.org17

What type of products (other than office supplies) does your company typically import

and what online or offline instruments do you use to formalize/complete the purchasing

process in the majority of cases? (Multiple responses)

5.5 Finalizing the purchase

The following block of questions examines the means by which importers realize or formalize

their purchases, with the objective of identifying the preferred type of instrument used (from

less formal options, i.e., a telephone call, email or a supplier’s website to more traditional

options, such as the physical exchange of documents via fax or mail).

The first question in this block identifies the types of goods imported by the companies and the

means by which they formalize their sales agreements. The study’s insights revealed that the

vast majority of importers buy finished goods for resale and the preferred instrument for

formalizing their purchases is email.

The offline instrument most frequently used to formalize a sale agreement is a written contract:

27% on average in all nine countries.

18Finished goods Finished goods for Others Raw materials Semi-manufactures

for resale in-house use for production for production

In analyzing importers’

purchases, the objective was

to find out how many are

buying imported products

over the Internet and on what

types of sites they are making

those purchases. The results

indicate that four out of ten

importers (42%) are currently

buying products online. Of

those importers that said they

purchase imported products

online, 67% do so directly,

going through the website of

their international suppliers.

Do you purchase any of the products that you

import over the Internet?

(Simple response)

The predominant preference for email as the preferred means for formalizing a sale exposes

parties to a possible legal vacuum. An alternative is to sign contracts sent via email using an

internationally recognized digital signature system (e.g., VeriSign). In the event of a dispute,

the authenticity of the parties and the international sales contract can be verified.

Nearly one-quarter of respondents (23%) cited the use of B2B platforms as Alibaba, Amazon

and eBay, among others.

19

On what types of websites do you make your online purchases from?

(Multiple response)

*Percentages may not total 100 due to rounding.

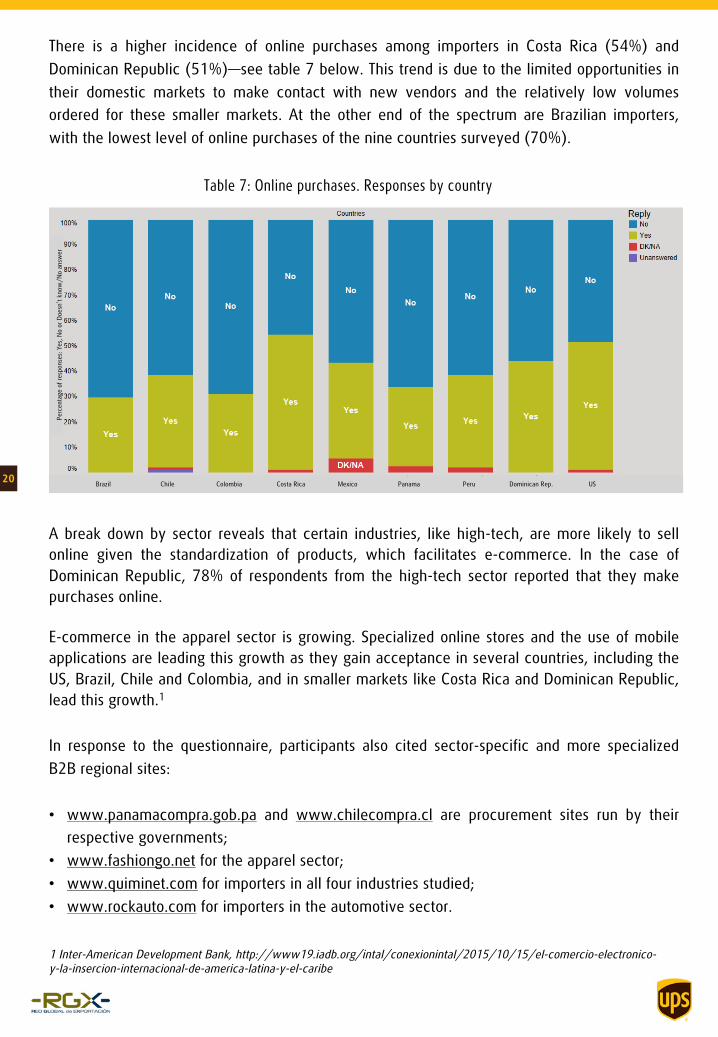

There is a higher incidence of online purchases among importers in Costa Rica (54%) and

Dominican Republic (51%)—see table 7 below. This trend is due to the limited opportunities in

their domestic markets to make contact with new vendors and the relatively low volumes

ordered for these smaller markets. At the other end of the spectrum are Brazilian importers,

with the lowest level of online purchases of the nine countries surveyed (70%).

Table 7: Online purchases. Responses by country

20Brazil Chile Colombia Costa Rica Mexico Panama Peru Dominican Rep. US

Perc

enta

ge o

f re

sponse

s: Y

es,

No o

r D

oesn

’t k

now

/N

o a

nsw

er

A break down by sector reveals that certain industries, like high-tech, are more likely to sell

online given the standardization of products, which facilitates e-commerce. In the case of

Dominican Republic, 78% of respondents from the high-tech sector reported that they make

purchases online.

E-commerce in the apparel sector is growing. Specialized online stores and the use of mobile

applications are leading this growth as they gain acceptance in several countries, including the

US, Brazil, Chile and Colombia, and in smaller markets like Costa Rica and Dominican Republic,

lead this growth.1

In response to the questionnaire, participants also cited sector-specific and more specialized

B2B regional sites:

• www.panamacompra.gob.pa and www.chilecompra.cl are procurement sites run by their

respective governments;

• www.fashiongo.net for the apparel sector;

• www.quiminet.com for importers in all four industries studied;

• www.rockauto.com for importers in the automotive sector.

1 Inter-American Development Bank, http://www19.iadb.org/intal/conexionintal/2015/10/15/el-comercio-electronico-y-la-insercion-internacional-de-america-latina-y-el-caribe

The study also includes response from importers about the promotional support they receive from

their suppliers. As shown below, nearly half (44%) of importers indicated that they do not use any

promotional tools provided by suppliers, a response that is mainly attributable to an overall lack of

awareness about the availability of these tools.

Meanwhile, earlier in the survey, when asked about whether they value promotional tools (see

page 16), 58% of all respondents rated them as highly important and 23% as fairly important.

What promotional tools provided by your international supplier(s) does your

company use to promote and sell the products you import? What are they?

(Multiple responses)

Table 8: Types of websites used for online purchases by country

21

Brazil Chile Colombia Costa Rica Mexico Panama Peru Dominican Rep. US

5.6 Import process: supply chain

The closing section of the questionnaire

assesses importers’ perceptions in terms of

critical factors along the supply chain. The

line of questioning explores the main

obstacles that they face when importing,

pinpointing the type of assistance exporters

can offer their buyers throughout the import

process.

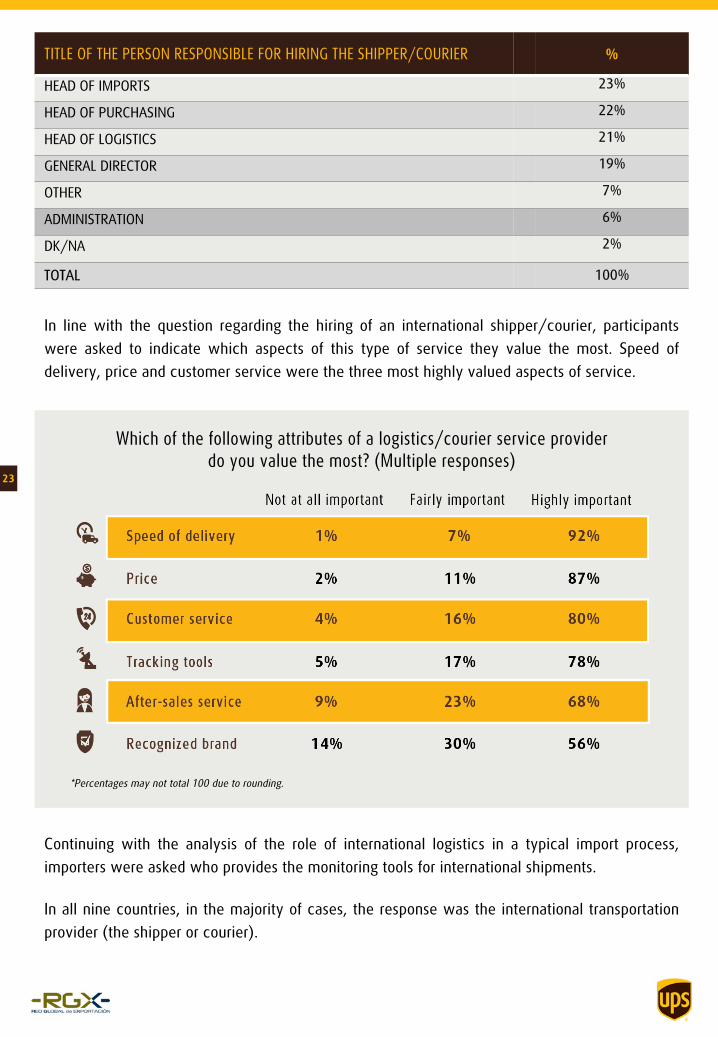

Participants were asked who makes the

decision regarding the hiring of an

international shipper or courier once they

have purchased the product. Almost one-

third (31%) of the buyers interviewed

said that they leave the decision to their

supplier (i.e., the exporter) and two-thirds

(66%) said that they decide and hire their

international shipper.

Once your company makes a

purchase, who is in charge of

hiring the international

shipper/courier?

(Single response)31%

66%

3% Supplier/Exporter

Our company (buyer)

DK/NA

Table 9: Decision to hire a courier by country

22

Brazil Chile Colombia Costa Rica Mexico Panama Peru Dominican Rep. US

In line with the question regarding the hiring of an international shipper/courier, participants

were asked to indicate which aspects of this type of service they value the most. Speed of

delivery, price and customer service were the three most highly valued aspects of service.

TITLE OF THE PERSON RESPONSIBLE FOR HIRING THE SHIPPER/COURIER %

HEAD OF IMPORTS 23%

HEAD OF PURCHASING 22%

HEAD OF LOGISTICS 21%

GENERAL DIRECTOR 19%

OTHER 7%

ADMINISTRATION 6%

DK/NA 2%

TOTAL 100%

Which of the following attributes of a logistics/courier service provider

do you value the most? (Multiple responses)

Continuing with the analysis of the role of international logistics in a typical import process,

importers were asked who provides the monitoring tools for international shipments.

In all nine countries, in the majority of cases, the response was the international transportation

provider (the shipper or courier).

23

*Percentages may not total 100 due to rounding.

In international transactions, monitoring tools add value for three main

reasons:

1. According to the International Chamber of Commerce (ICC), one of the

most frequently used sales clauses is the Incoterm free on board (FOB)—

meaning the seller's liability for ensuring safe shipment and payment of

shipping fees terminates upon delivery of the goods to the chosen carrier.

From the importer’s perspective, having an eye on their shipment at all

times is highly valued (78% of all respondents in this study indicated as

much). For this reason, offering customers access to monitoring tools to

track shipments forms part of the recommended action to build loyalty

among importers.

2. In the BMEI 2017, delivery delays were cited as the greatest obstacle

faced by importers. Monitoring systems or tracking tools keep importers

abreast of shipping status, contributing to a better organization of the

reception of international purchases. It also allows them to prepare and

submit supporting documentation in a timely manner to avoid delays.

3. Since most of the importers interviewed in the study indicated that they

import finished goods for resale (61%), monitoring tools can also give retail

customers or end consumers access to shipping information, thereby

allowing importers to provide a better service to their customers.

Who provides the monitoring tool for shipments? (Multiple responses)

24

Brazil Chile Colombia Costa Rica Mexico Panama Peru Dominican Rep. US

Participants indicated the attributes that they value the most when selecting a logistics service

provider. The highest ranking attribute cited was speed of clearance. In second place,

compliance and the level of trust/relationship established tied. Quality of information provided

and price were also cited as highly important.

How important are each of the following attributes to your company

when choosing a customs broker? (Multiple responses)

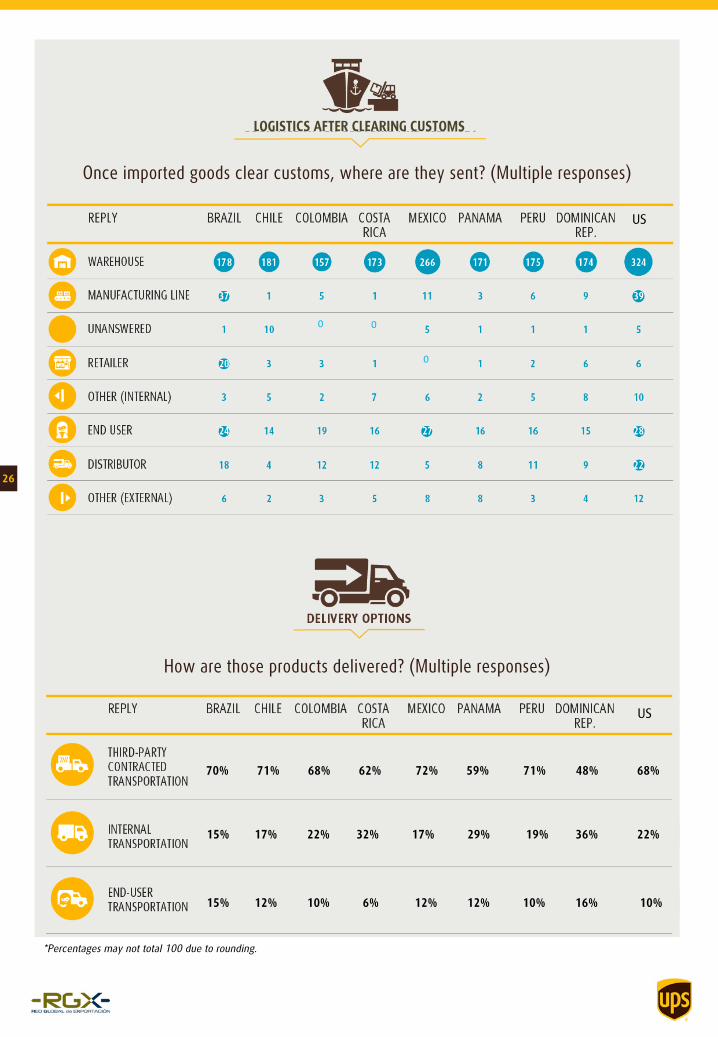

In anticipation of the next steps involved in a typical import transaction, participants were

asked about their logistics needs once their products are released from customs at the

destination.

The findings revealed that four out of every five importers (83%) send the imported goods to

their own warehouse. Of those respondents, 64% use third-party transportation services, while

22% use their own services. These findings are in line with the profile of the importer

interviewed for this study as seen on page 6, which illustrates that two out of every five (38%)

are distributors and over half (61%) are importing finished goods for resale.

25

Once imported goods clear customs, where are they sent? (Multiple responses)

How are those products delivered? (Multiple responses)

26

70% 71% 68% 62% 72% 59% 71% 48% 68%

15% 17% 22% 32% 17% 29% 19% 36% 22%

15% 12% 10% 6% 12% 12% 10% 16% 10%

US

US

LOGISTICS AFTER CLEARING CUSTOMS

*Percentages may not total 100 due to rounding.

0 0

0

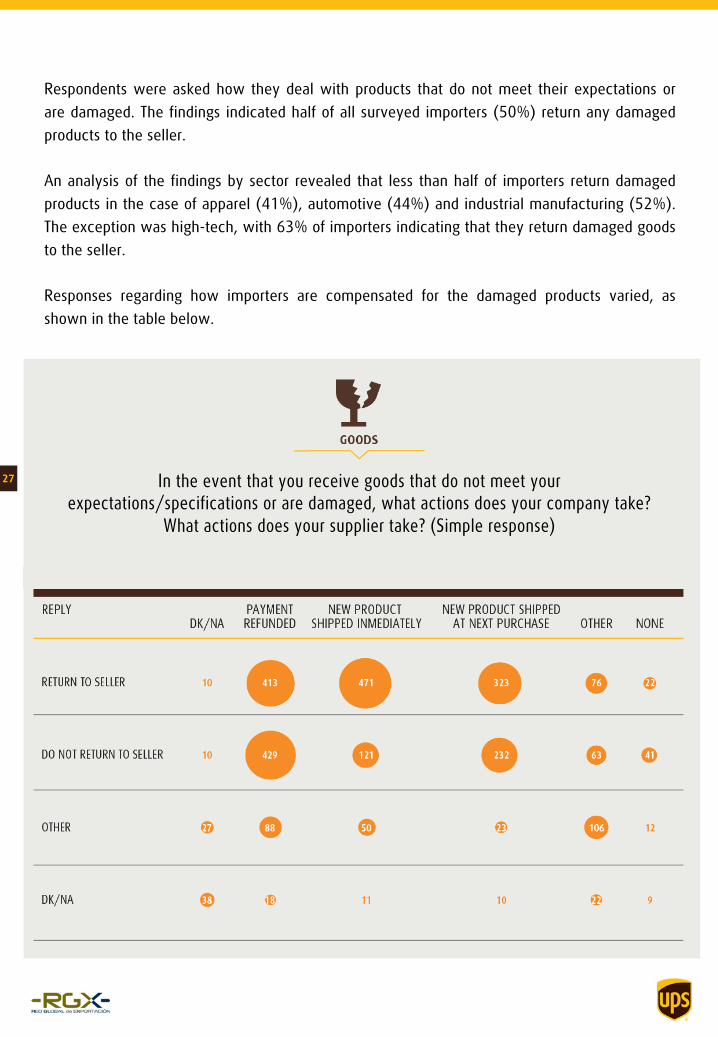

Respondents were asked how they deal with products that do not meet their expectations or

are damaged. The findings indicated half of all surveyed importers (50%) return any damaged

products to the seller.

An analysis of the findings by sector revealed that less than half of importers return damaged

products in the case of apparel (41%), automotive (44%) and industrial manufacturing (52%).

The exception was high-tech, with 63% of importers indicating that they return damaged goods

to the seller.

Responses regarding how importers are compensated for the damaged products varied, as

shown in the table below.

In the event that you receive goods that do not meet your

expectations/specifications or are damaged, what actions does your company take?

What actions does your supplier take? (Simple response)

27

What are the most important aspects of the supply chain for your business? (Multiple responses)

What are the main operating barriers that your company faces when importing? (Multiple responses)

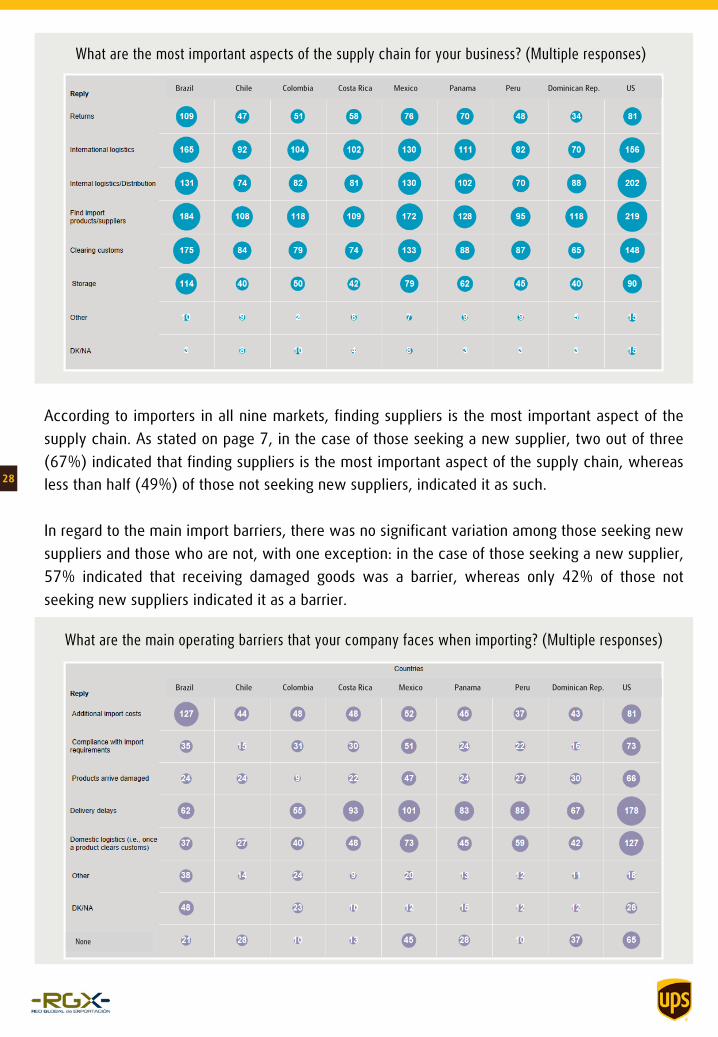

According to importers in all nine markets, finding suppliers is the most important aspect of the

supply chain. As stated on page 7, in the case of those seeking a new supplier, two out of three

(67%) indicated that finding suppliers is the most important aspect of the supply chain, whereas

less than half (49%) of those not seeking new suppliers, indicated it as such.

In regard to the main import barriers, there was no significant variation among those seeking new

suppliers and those who are not, with one exception: in the case of those seeking a new supplier,

57% indicated that receiving damaged goods was a barrier, whereas only 42% of those not

seeking new suppliers indicated it as a barrier.

28

Brazil Chile Colombia Costa Rica Mexico Panama Peru Dominican Rep. US

Brazil Chile Colombia Costa Rica Mexico Panama Peru Dominican Rep. US

None

As seen in section 5.2, in response to the first question, 971

importers said that they are looking for new suppliers, whereas

1,158 indicated that they are not. (Furthermore, there were 41

respondents who either responded that they didn’t know if the

company was looking or refrained from answering (DK/NA), so

they may or may not be looking.) In this section of the

questionnaire, 1,251 respondents (58%) indicated that finding

new suppliers is the most important aspect of their supply chain,

which appears incongruous with the results for the first question.

However, the fact that they are not actively looking does not make

it any less of a critical point along the supply chain.

In turn, with the exception of Brazil and Chile, delivery delays were indicated as the main

obstacle that importers face during the import process. In Brazil, the main obstacle cited was

additional import costs, followed by delivery delays in second place. Chilean importers also

named additional import costs as the top obstacle faced, followed by domestic logistics. In the

case of the US, Peru and Mexico, domestic logistics was the second most commonly cited

barrier.

Both of the above questions regarding the most important aspects of the supply chain and the

main import barriers reveal the challenges inherent in each market, highlighting countries’

different degrees of permeability regarding imports crossing their borders.

If an exporter can meet demanding commercial and non-tariff requirements, it is advisable that

they focus on markets with low tariff barriers and greater potential demand, such as the US,

Mexico and Brazil.

For those companies that are not prepared to respond to requests from countries with strict

commercial and non-tariff requirements, there are more suitable destinations with lower non-

tariff requirements and trade agreements or reduced-tariff agreements in effect to facilitate the

entry of their products.

29

Level of difficulty of entry to the countries surveyed

Importers face two types of trade barriers: tariff barriers and non-tariff barriers.

The first table shows the degree of permeability in each market in relation to

the exporter’s country of origin, based on the levels of import taxes in each

destination (tariff barriers).

The second table reflects the level of commercial and non-tariff requirements in

each of the countries analyzed.

Based on both tables, an exporter must analyze the convenience of choosing

one market over another.

Table A: Level of difficulties of entry in nine countries based on tariff barriers

Table B: Level of difficulty of entry based on commercial and non-tariff requirements: i.e., required

quantities, quality standards, certifications, flexible payment terms and after-sales services.

Low: Existing trade agreements.

Average: Tariff reduction agreements in effect.

High: No trade agreements in effect.

30

6. Sector specific highlights

6.1 Propensity to importIn an effort to understand the different countries’ propensity to import, an analysis was

conducted to determine if there is a positive correlation between an importer’s response to

whether it is currently searching for new suppliers (i.e., the percentage of importers seeking a

new provider vs. those who are not) and the evolution in recent years of imports of the more

representative tariff items in each of the four industries analyzed.

Import statistics in each industry over the past five years were examined to see if they had

increased, decreased or remained stable, and how this behavior related to the propensity to

import found in the study.

As a result, an index was created of the nine countries’ propensity to import in the four industries

studied. On the next four pages, there is a table for each industry that reflects the percentage of

importers seeking new suppliers and the findings related to their online activity and overall

digital behavior.

For the purposes of this study, an importer’s digital behavior or “e-focus” is defined by a

respondent’s positive responses to three questions: Do you search online for new suppliers? Do

you make online purchases? Do you highly value exporters’ websites?

31 -

6.2 Apparel

• The three countries with the highest percentage of respondents looking for new suppliers in

the apparel sector are the US (54%), Costa Rica (58%) and Chile (52%), which are markets

that exporters looking for new markets to develop should consider.

• In the case of the US, the most widely used means to seek new suppliers were international

fairs (49% of total responses) and Internet search engines (47% of total responses). In Chile

and Costa Rica, responses were similar, although trade missions are growing in importance.

• International fairs and trade missions are consolidated as the two preferred offline channels

used to contact new potential suppliers in all nine countries.

• In all nine countries, of those respondents who said they make purchases online, the

percentage of apparel importers who buy directly through their international supplier’s

website (73%) was higher than the average of the study (67%).

32 Apparel importers’ digital attributes and propensity to import by country

6.3 Automotive

• Colombia (54%) and Costa Rica (52%) were the two countries with the highest percentage

of importers looking for new suppliers, which is in line with the positive trend in imports seen

in the table on page 31.

• The majority of Colombian importers interviewed use search engines to find new suppliers.

• In turn, in Dominican Republic, there is a similar proportion of importers buying online

directly through the supplier’s site (44%) and those buying on B2B platforms (37%).

Furthermore, it is the country where importers use and prefer online means of contact, as

well as online purchasing methods, so it is important that exporters evaluate an online

strategy when targeting Dominican importers in this sector.

• Domestic logistics was cited as the second largest importing obstacle for this sector (19%)

following delivery delays with 28% of total responses.

33

Automotive importers’ digital attributes and propensity to import by country

6.4 High-tech

• The study’s findings indicate that the highest level of online activity in import processes is

found in the high-tech sector. This is explained by importers’ preference for online searches

for new suppliers, the high number of respondents carrying out purchases completely online

(50% of respondents), as well as the more frequent and varied use of online promotional

tools.

• In Dominican Republic, nearly eight out of ten respondents (78%) said that they purchase

products online.

• Warranty policies and product certifications were named as the most valued content on a

potential supplier’s website.

34

-

High-tech importers’ digital attributes and propensity to import by country

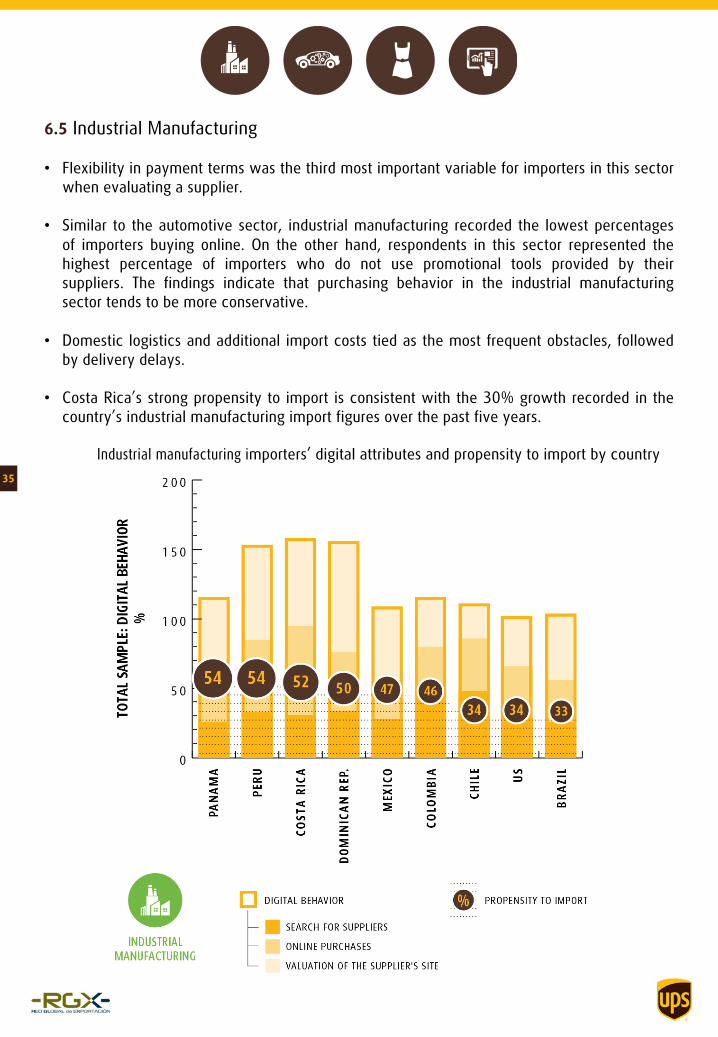

6.5 Industrial Manufacturing

• Flexibility in payment terms was the third most important variable for importers in this sector

when evaluating a supplier.

• Similar to the automotive sector, industrial manufacturing recorded the lowest percentages

of importers buying online. On the other hand, respondents in this sector represented the

highest percentage of importers who do not use promotional tools provided by their

suppliers. The findings indicate that purchasing behavior in the industrial manufacturing

sector tends to be more conservative.

• Domestic logistics and additional import costs tied as the most frequent obstacles, followed

by delivery delays.

• Costa Rica’s strong propensity to import is consistent with the 30% growth recorded in the

country’s industrial manufacturing import figures over the past five years.

35

Industrial manufacturing importers’ digital attributes and propensity to import by country

36

7. Conclusions: highlights and insights

This study takes an in-depth look at the purchasing behavior of small and medium-sized

importers in the Americas and, in particular, at their preferences and actions throughout the

import process. As a result of the responses received, several opportunities have been

identified for Latin American small and medium-sized exporters.

Four out of ten companies (42%) surveyed said that they purchase imported products over

the Internet. This trend represents an opportunity to increase sales for those exporters with

the capability to sell products online. Small and medium-sized exporters can also exploit the

advantages of organic positioning in search engines, online marketing tools and a presence

in online B2B platforms to reach more customers.

The study also highlights the importance that importers place on the quality of the products

that they buy. Exporting SMEs in the region must invest in their production processes and

work to ensure that the product they deliver meets or exceeds industry standards.

Furthermore, exporters must clearly communicate their business attributes, services,

qualifications and certifications on their companies’ websites. According to the findings,

these attributes influence importers’ purchasing decisions.

Although the results were consistent throughout the nine countries surveyed in all four

sectors—reflecting the fairly homogenous foreign trade conditions in the region—a closer

look at the behavior of importers makes it possible to make several recommendations. These

recommendations are based on:

• the percentage of importers seeking new suppliers (page 7)

• their propensity to use online channels in their import processes (pages 19 – 20)

• the permeability of the import country (page 30)

Two windows of opportunity were identified for exporting SMEs to win over and retain

international customers. The first is associated with the lack of online promotional support

that importers receive from their current suppliers.

37

Exporting SMEs can build customer loyalty by assisting buyers with their promotional efforts

through the use of tools like search engine advertising and “buy now” buttons on social

media platforms.

The second opportunity for exporters is to offer customers solutions that address one of the

main obstacles cited by importers: delays in clearing customs. Exporters can ensure that

their customers have all of the proper documentation to present in customs. They can also

provide solutions based on new technologies, such as e-commerce, online customer support

and shipment tracking tools. These solutions will be key differentiators from existing

competitors.