Blue Strategy

22

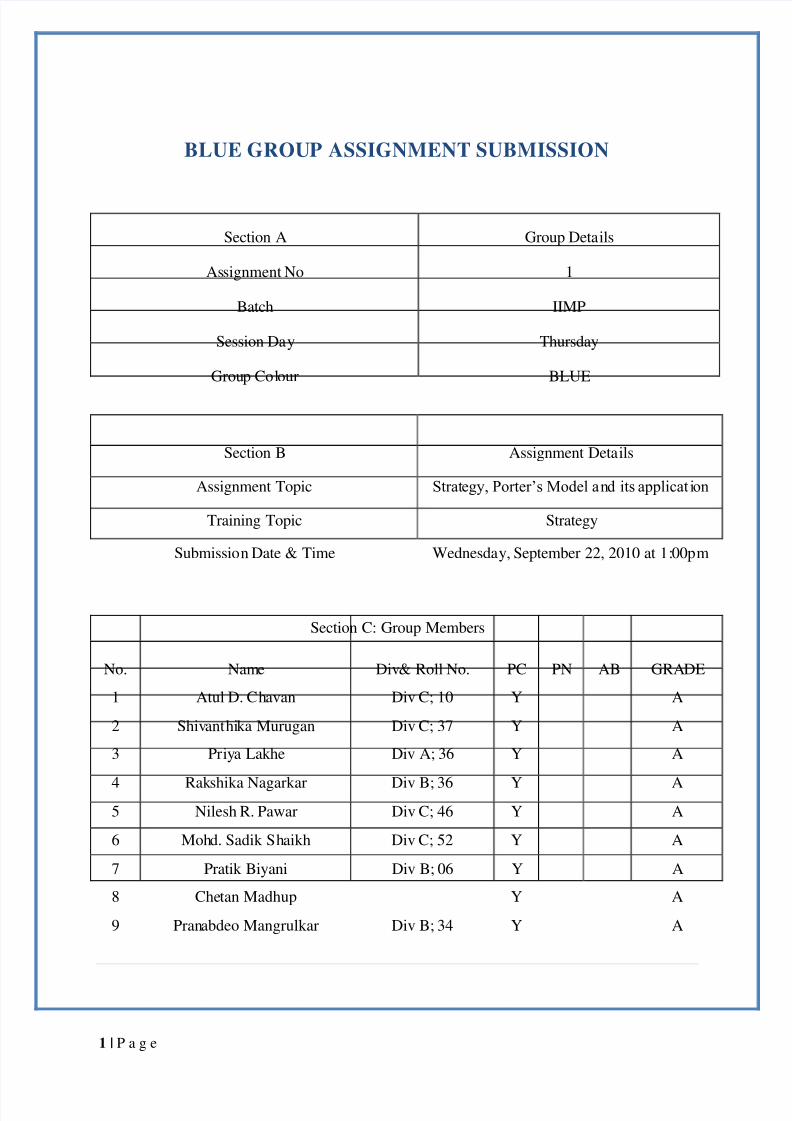

1 | Page BLUE GROUP ASSIGNMENT SUBMISSION Section A Group Deta ils As signment No 1 Batch IIMP Session Da y Thursday Grou p Co l our BLUE Section B Assignment Deta ils Assignment Topic Strat egy, Porter’s Model a n d its applicat i on Training Topic Strategy Submissio n Date & Time Wednesda y, September 22, 2010 at 1 : 00p m Section C: Group Members No. Nam e Div & Roll No. PC PN AB GRADE 1 Atul D. C h avan Div C; 10 Y A 2 Shiv ant hi ka Murugan Div C; 37 Y A 3 Pr iy a Lakhe Div A; 36 Y A 4 Rakshika Nagarkar Div B; 36 Y A 5 Nilesh R. Pawar Div C; 46 Y A 6 Mohd. Sadik S h aikh Div C; 52 Y A 7 Pratik Biyani Div B; 06 Y A 8 Che tan Madhup Y A 9 Pran abdeo Mangrulkar Div B; 34 Y A

-

Upload

shivanthika -

Category

Documents

-

view

221 -

download

0

Transcript of Blue Strategy

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 1/22

1 | P a g e

BLUE GROUP ASSIGNMENT SUBMISSION

Section A Group Details

Assignment No 1

Batch IIMP

Session Day Thursday

Group Colour BLUE

Section B Assignment Details

Assignment Topic Strategy, Porter’s Model and its applicat ion

Training Topic Strategy

Submission Date & Time Wednesday, September 22, 2010 at 1:00pm

Section C: Group Members

No. Name Div& Roll No. PC PN AB GRADE

1 Atul D. Chavan Div C; 10 Y A

2 Shivanthika Murugan Div C; 37 Y A

3 Priya Lakhe Div A; 36 Y A

4 Rakshika Nagarkar Div B; 36 Y A5 Nilesh R. Pawar Div C; 46 Y A

6 Mohd. Sadik Shaikh Div C; 52 Y A

7 Pratik Biyani Div B; 06 Y A

8 Chetan Madhup Y A

9 Pranabdeo Mangrulkar Div B; 34 Y A

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 2/22

2 | P a g e

BLUE GROUP-IIMP

ASSIGNMENT NO. 1

‘HOW COMPETITIVE FORCES SHAPE

STRATEGY’

CAREER DEVELOPMENT PROGRAM

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 3/22

3 | P a g e

PART A

MICHAEL PORTER’S MODEL AND ITS APPLICATION ON

THE TRAINING INDUSTRY

Part A

1) Introduction of training industry

2) Michael Porter’s Five Forces Model

3) Application of the model to Training Industry

4) SWOT Analysis

5) Conclusions

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 4/22

4 | P a g e

Introduction of training industry

With the world-wide expansion of companies and changing technologies, IndianOrganizations have realized the importance of corporate training. Training is considered as

more of retention tool than a cost.

Today, human resource is now a source of competitive advantage for all organizations.

Therefore, the training system in Indian Industry has been changed to create a smarter

workforce and yield the best results. With increase in competitio n, every company wants to

optimize the utilization of its resources to yield the maximum possible results.

Training is required in every field be it Sales, Marketing, Human Resource, Relationship

building, Logistics, Production, Engineering, etc. It is now a business effective tool and is

linked with the business outcome.

Michael Porter’s Five Forces Model

The model of the Five Competitive Forces was developed by Michael E. Porter in his book,

Competitive Strategy: Techniques for Analyzing Industries and Competitors― in 1980. Since

that time it has become an important tool for analyzing an organizations industry structure in

strategic processes.

Porter’s model is based on the insight that a corporate strategy should meet the opportunities

and threats in the organizations external environment.

Especially, competitive strategy should base on and understanding of industry structures and

the way they change. Porter has identified five competitive forces that shape every industry

and every market.

These forces determine the intensity of competition and hence the profitability and

attractiveness of an industry. The objective of corporate strategy should be to modify these

competitive forces in a way that improves the position of the organization. Porters model

supports analysis of the driving forces in an industry.

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 5/22

5 | P a g e

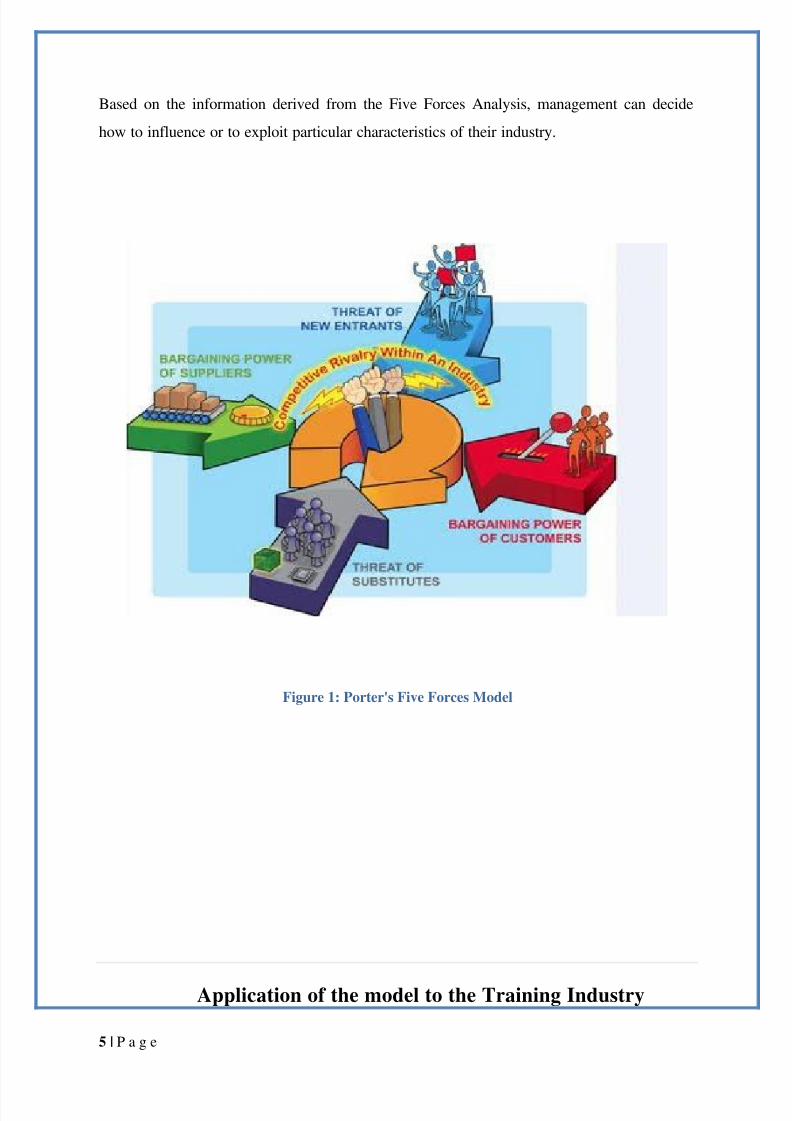

Based on the information derived from the Five Forces Analysis, management can decide

how to influence or to exploit particular characteristics of their industry.

Figure 1: Porter's Five Forces Model

Application of the model to the Training Industry

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 6/22

6 | P a g e

THREAT OF NEW ENTRANTS

Power is also affected by the ability of people to enter your market. If it costs little in

time or money to enter your market and compete effectively, if there are few economies of

scale in place, or if you have little protection for your key technologies, then new competitors

can quickly enter your market and weaken your position. If you have strong and durable

barriers to entry, then you can preserve a favorable position and take fair advantage of it.

It is not only the existing firms that can create rivalry but there exists a threat of new

entrants as well. New entrants bring new capacity, the desire to gain market share and

substantial resources.

Easy to enter if there is:

Common technology

Little brand franchise

Assess to distribution channel

Difficult to enter if there is:

Patented

Difficulty in brand switching

Restricted distribution channel

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 7/22

7 | P a g e

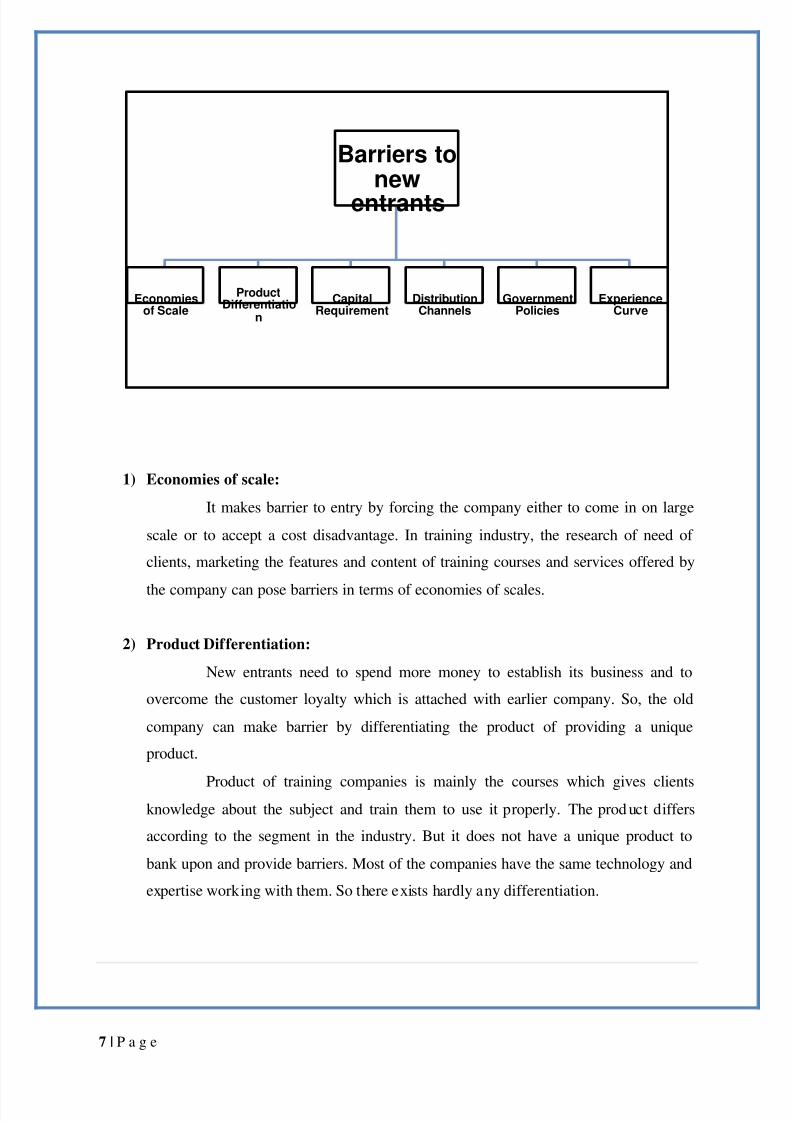

1) Economies of scale:

It makes barrier to entry by forcing the company either to come in on large

scale or to accept a cost disadvantage. In training industry, the research of need of

clients, marketing the features and content of training courses and services offered by

the company can pose barriers in terms of economies of scales.

2) Product Differentiation:

New entrants need to spend more money to establish its business and to

overcome the customer loyalty which is attached with earlier company. So, the old

company can make barrier by differentiating the product of providing a unique

product.

Product of training companies is mainly the courses which gives clientsknowledge about the subject and train them to use it properly. The prod uct differs

according to the segment in the industry. But it does not have a unique product to

bank upon and provide barriers. Most of the companies have the same technology and

expertise working with them. So there exists hardly any differentiation.

Barriers tonew

entrants

Economiesof Scale

ProductDifferentiatio

n

CapitalRequirement

DistributionChannels

GovernmentPolicies

ExperienceCurve

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 8/22

8 | P a g e

3) Capital Requirement:

New entrants need to invest a huge amount of financial resources to compete

with established ones which creates barriers to entry. Large amount of money is

needed to invest to tap the customers in training industry. Many corporate clients has

familiarity with some established ones. So, to break this and compete with them new

entrants need to advertise and carry out promotional activities which require high

capital investment.

4) Distribution Channel:

The well organized distribution channel of established companies can be

barrier for new comers. In training industry, this factor provides barrier for new

entrants. Old companies have well established distribution channel in the form of

structure and more number of centers providing the training facilities compared to

new ones. So, new entrants need to set up distribution channel which is again costly

and it provides barrier to entry.

5) Experience Curve:

According to the concept of experience curve, unit cost in industries decline

with ―Experience‖. Such Cost decline creates barrier to entry because new companies

with no experience face problems such as higher cost of operations. Experience curve

acts as entry barrier in training industry. The established training companies have cost

advantage due to more efficient workforce, facilities, technology support.

6) Government Policies:

Government can limit the entry to industries with controls like licensing,

standards and regulations. National Institute for Small Industry Extension Training

(NISIET), an autonomous arm of the Ministry of Small Scale Industries (SSI), the

Institute strives to achieve its objectives through operations ranging from training,

consultancy, research and education, to extension and information services. It offers

an easy and effective means of achieving broad based ownership of industry, the

diffusion of enterprise and initiative in the industrial field.

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 9/22

9 | P a g e

THREAT OF SUBSTITUTES

Substitutes to the training industry can be

1) Distance education Programs:

The students enroll themselves to distance education programs and they are

provided with notes and other study materials. The students interaction

between the Faculty and peers is minimal.

2) Self learning kits:

People nowadays use the self learning kits which are available in the markets.

Their advantage is that the learning can be done at the pace at which they are

comfortable. E.g.: Personal Finance for dummies, Magic for Dummies etc.

3) Virtual Classrooms:

A virtual classroom is a learning environment created in the virtual space. The

objectives of a virtual classroom are to improve access to advanced

educational experiences by allowing students and instructors to participate inremote learning communities using personal computers; and to improve the

quality and effectiveness of education by using the computer to support a

collaborative learning process.

4) Hypertext courses:

Structured course material is used as in a conventional distance education

program. However, all material is provided electronically and can be viewed

with a browser. Hyperlinks connect text, multimedia parts and exercises in a

meaningful way.

5) Video-based courses:

They are like face-to- face classroom courses, with a lecturer speaking and

Powerpoint slides or online examples used for illustration. Video- streaming

technologies is used. Students watch the video by means of freeware or plug-ins.

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 10/22

10 | P a g e

6) Audio-based courses

They are similar but instead of moving pictures only the sound track of the lecturer is

provided. Often the course pages are enhanced with a text transcription of the lecture.

7) Animated courses:

This is Enhancing the text or audio course material by animations to make it more

interesting .Animations are created using Macromedia Flash or similar technologies.

These animations help understand key concepts and also allow for better retention of

learning.

8) Web-supported textbook: These courses are based on specific textbooks. Students read and reflect on the

chapters by themselves. Review questions, topics for discussion, exercises, case

studies, etc. are given chapterwise on a website and discussed with the lecturer. Class

meetings may be held to discuss matters in a chatroom, for example.

9) Peer-to-peer courses :

These courses are taught "on-demand" and without a prepared curriculum.

COMPETITIVE RIVALRY WITHIN AN INDUSTRY

1. The major threat to the T&D industry comes from the emergence of new low cost

providers into the industry.

2. There are numerous institutes coming up in cities, which provide Corporate training

and skills like Communication, English Speaking, Personality building etc, at a very

low cost compared to highly professional training courses.

3. The current professional training institutes are continuously trying to gain competitive

advantage and hence are becoming more competitive.

4. Free enormous amount of data and information available on the internet is another

major rival to the T&D industry

5. Concepts like Distance learning/Correspondence courses also pose a challenge, as it

drastically cuts down the number of people that would take up the trainings

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 11/22

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 12/22

12 | P a g e

2. Is the product offered unique or at least differentiated, or if it has built up

switching costs?

Many trainers are available in the market specialized in the same field. Hence

in general, the services offered by the trainers are not much differentiated.

There are very few trainers who are known for their experience & knowledge.

For such trainers the organization is known by their name & not vice versa. These

trainers have built up switching costs for them.

3. Are the suppliers obliged to contend with other products for sale to the industry?

There are many suppliers working in the same field. So many a times there is

more than one supplier who would like to serve the industry. At such times the

supplier has to compete with others.

4. Do the suppliers pose a credible threat of integrating forward into the industry’s

business?

Trainers who have gained sufficient experience, knowledge and who are

renowned in the industry do pose a threat of forward integration. These trainers over

the period of years develop a strong goodwill and network in the market. Due to

which it becomes easy to start up a training institute.

5. Is the Training Industry not an important customer of the supplier group?

Majority of the trainers belong to this industry only. Their main profession is

teaching. So they don’t pose any threat.

Nowadays many working professionals have entered into the training market

as freelancers. These professionals have a job in some other industry but they are also

interested in being a part of training industry. For these trainers the training industry is

not the only customer for their skills & knowledge. If there are trainers in this

category who have built up a switching cost for themselves then they do pose a threat.

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 13/22

13 | P a g e

Looking at these questions, we can say that:

1. Suppliers in the training industry are not that powerful.

2. Most of the suppliers are undifferentiated.

3. Very few of them have built up a switching cost for themselves.

4. Those who have built up a switching cost for themselves do pose a threat of forward

integration in the industry.

5. Training Industry is more concentrated and more powerful than the suppliers.

BARGAINING POWER OF BUYERS/ CUSTOMERS

The more options the buyer has to choose from, the more power the buyer has. New

substitutes and new entrants erode the monopoly that traditional colleges and universities

have enjoyed. Buyer power is also increased to the extent that firms themselves become

suppliers of higher education, as they introduce lifelong learning programs for employees,

reducing the ability of the universities to capture value.

The bargaining power of customers is also described as the market of outputs: the ability of

customers to put the firm under pressure, which also affects the customer's sensitivity to price

changes.

Power of Buyers - This is how much pressure customers can place on a business. If one

customer has a large enough impact to affect a company's margins and volumes, then the

customer hold substantial power. Here are a few reasons that customers might have power:

• Small number of buyers

• Purchases large volumes

• Switching to another (competitive) product is simple

• The product is not extremely important to buyers; they can do without the product for

a period of time

• Customers are price sensitive

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 14/22

14 | P a g e

When analyzing the training industry, some factors may indicate high buyer bargaining

power and some may indicate low buyer bargaining power. It plays an important role in

determining the profit potential.

Buyer Power is High/Strong if Buyer Power is Low/Weak if

Buyers are more concentrated than

sellers

No Buyers are less concentrated than

sellers

Yes

Buyer switching costs are low No Buyer switching costs are high Yes

Threat of backward integration is

high

No Threat of backward integration is

low

Yes

Buyer is price sensitive No Buyer is not price sensitive Yes

Buyer is well-educated regarding

the product

Yes Buyer is uneducated regard ing the

product

No

Buyer purchases product in high

volume

No Buyer purchases product in low

volume

Yes

Buyer purchases comprise large

portion of seller sales

No Buyer purchases comprise small

portion of seller sales

No

Product is undifferentiated No Product is highly differentiated Yes

Substitutes are availableNo Substitutes are unavailable Yes

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 15/22

15 | P a g e

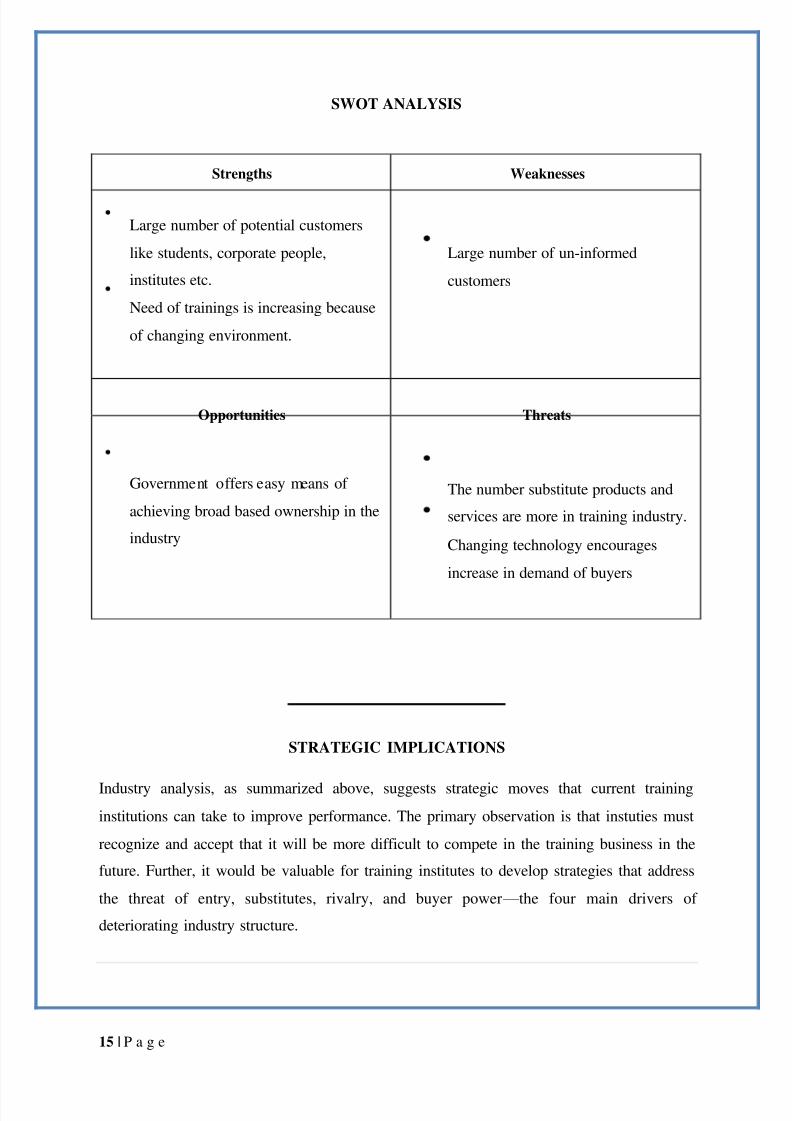

SWOT ANALYSIS

Strengths Weaknesses

Large number of potential customers

like students, corporate people,

institutes etc.

Need of trainings is increasing because

of changing environment.

Large number of un-informed

customers

Opportunities Threats

Government offers easy means of

achieving broad based ownership in the

industry

The number substitute products and

services are more in training industry.

Changing technology encourages

increase in demand of buyers

STRATEGIC IMPLICATIONS

Industry analysis, as summarized above, suggests strategic moves that current training

institutions can take to improve performance. The primary observation is that instuties must

recognize and accept that it will be more difficult to compete in the training business in the

future. Further, it would be valuable for training institutes to develop strategies that address

the threat of entry, substitutes, rivalry, and buyer power — the four main drivers of

deteriorating industry structure.

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 16/22

16 | P a g e

Threat of New Entrants Competitive Rivalry

Threat of New Entry

Supplier

Buyers

Power

Power

Supplier Power Buyer Power

Threat of Substitute

Threat of Substitute

The following framework can give a detailed competitive study of the

training industry. By studying each force, we can conclude how strong the force is.For example, the force: threat of new entrants, the conclusion is new entry is quiteeasy. So we have put “+“(Positive sign) indicating the threat of new entrants do not

exists. Similarly we can apply the same to other forces.

Expensive to enter

into the industry.

Experience needed

Some Economiesof scale

No technologybarriers

High barriers

New entry quite

hard.

The number of

buyers is more

Competition in the

industry is more

Customers

considers the

value proposition

Give more

preference to word

of mouth

Buyer power is

more

Geographical

constraints

Need to use

expensive high-end

technology

language barriers

Resources and

budgets

Distant Learning

Self Learning Kit

Virtual Class rooms

Peer-peer Courses

Threat of

Substitutes exists

Undifferentiatedsuppliers

Suppliers not so

powerful Switching cost is

high

Competitive

Rivalry

+

-

-+

-

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 17/22

17 | P a g e

CONCLUSION

In response to their changing environment, training institutes should identify the full set of

functions, or products and services they offer — Sales, Marketing, Human Resource,

Relationship building, Logistics, Production, Engineering, etc.

The traditional strategic prescription would be to participate only in markets where an

institution’s strengths continue to offer a competitive advantage.

This would lead to concession of entire market segments to new entrants exploiting new

technologies, and a retreat to core educational products that cannot readily be imitated or

substituted.

On the other hand, it could be argued that institutions should embrace the new technologies,

delivery systems, and customer needs that the changing environment is generating by

entering new markets such as distance learning.

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 18/22

18 | P a g e

PART B

Application of Industry Attractiveness Questionnaire to the

Telecom Industry

Part B:

1) Application of model to Telecom industry

2) Conclusion

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 19/22

19 | P a g e

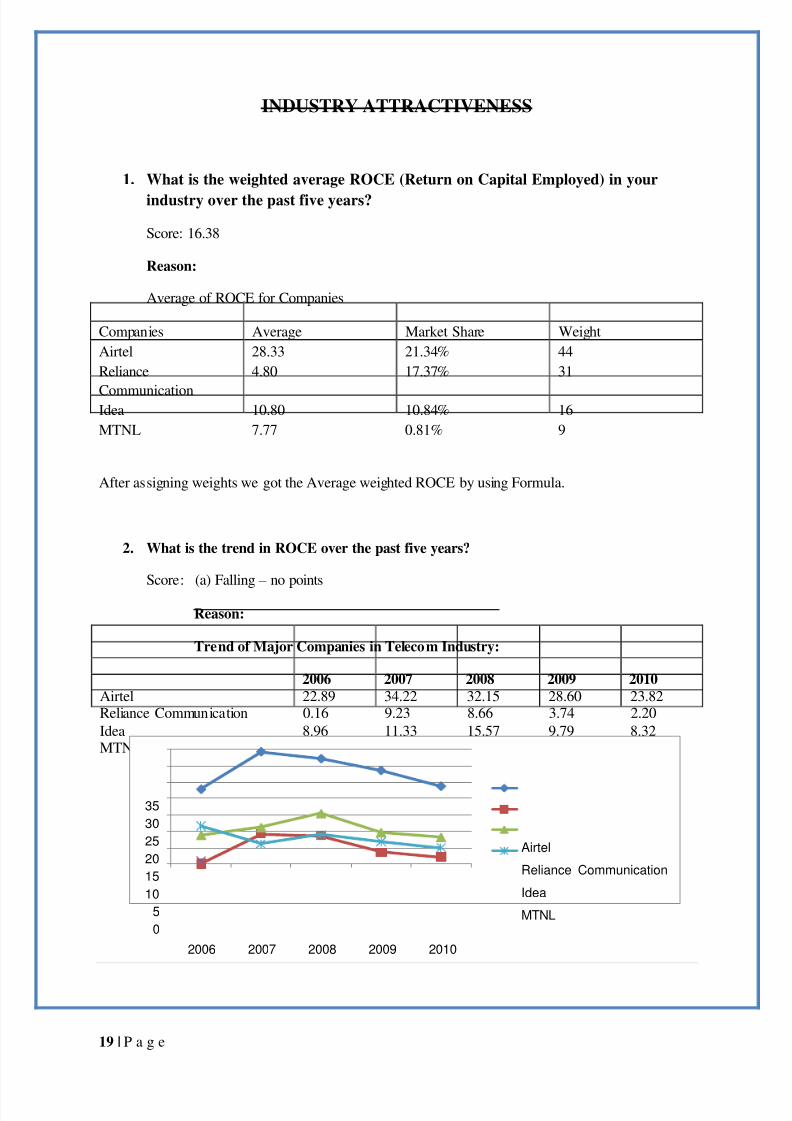

INDUSTRY ATTRACTIVENESS

1. What is the weighted average ROCE (Return on Capital Employed) in your

industry over the past five years?

Score: 16.38

Reason:

Average of ROCE for Companies

Companies Average Market Share Weight

Airtel 28.33 21.34% 44

Reliance

Communication

4.80 17.37% 31

Idea 10.80 10.84% 16

MTNL 7.77 0.81% 9

After assigning weights we got the Average weighted ROCE by using Formula.

2. What is the trend in ROCE over the past five years?

Score: (a) Falling – no points

Reason:

Trend of Major Companies in Telecom Industry:

2006 2007 2008 2009 2010

Airtel 22.89 34.22 32.15 28.60 23.82Reliance Communication 0.16 9.23 8.66 3.74 2.20

Idea 8.96 11.33 15.57 9.79 8.32MTNL 11.65 6.25 9.02 6.90 5.03

0

5

10

15

20

25

30

35

2006 2007 2008 2009 2010

Airtel

Reliance Communication

Idea

MTNL

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 20/22

20 | P a g e

3. How substantial are the barriers stopping new entrants to the industry?

Score: (d) Very high barr iers – 10 points

Reason:

Huge License Fees to be paid upfront & High gestation period.

Infrastructure Setup Cost – High.

Rapidly changing technology.

Setting of towers at various locations is very difficult.

Highly Skilled labours are required.

4. What is your best estimate of the next five years’ average annual market

growth?

Score: (d) Over 10 % - 10 points

Reason:

Yearly cell phone addition 178.25 million Jan-Dec 2010.

Monthly cell phone addition 17 million (July-2010)

Current Teledensity - 58.17%

Expected Teledensity – 84% i.e., 1 billion by 2012

5. What is the current balance in the industry between customer demand, and the

total industry capacity?

Score: (a) There is serious industry over capacity, and no plans to remove it – minus 20

points

Reasons:

Service Providers started offering Sim cards for free.

Individuals started owning 2-3 Sim cards without any problem.

No shortage by network providers irrespective of the demand. Excess focus on urban market, which led to untapped customer base of rural

areas.

6. What is the threat from substituting products, services or technologies?

Score: (d) Threats do not appear to exist & unlikely – no points

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 21/22

21 | P a g e

7. What relative bargaining power do the industry’s suppliers have?

Score: (d) The industry is more concentrated and more powerful than suppliers and can

dictate terms to them – 10 points

Reason:

Network Outsourcing and Maintenance

Vast number of Service Provider.

Not much distinction between the products or services provided by the supplier.

Outsourcing Deals - Call Centres, Tower Business

8. What relative bargaining power do the industry’s customers have?

Score: (a) The customers are more concentrated and powerful: no points

Reason:

Low Switching Costs

Cut throat Competition

Lack of differentiation among Service Providers

Easy availability of the product.

Conclusion:Total Score: 26.38Thus,

Score (26 to 50): The industry is not very attractive, but it is possible for segment leaders and

very well run firms to make a living

Range Of Scores:

Negative Score (-1 to -40): try to get out of the industry. If you are still reporting profits or any one isfoolish enough to buy the business, sell.

Score (0 to 25): This is an unattractive industry. If you are not the market leader, sell the business.

Score (26 to 50): The industry is not very attractive, but it is possible for segment leaders and very

well run firms to make a living

Score (51 to 60): The industry is slightly attractive or unattractive. Competitive position is all.

Score (61 to 75): The industry is attractive. If you are in it, consolidate your position and gain or

maintain leadership. If not, consider entry if it is adjacent to your business and you have the expertise

or can share costs with your existing business.

8/8/2019 Blue Strategy

http://slidepdf.com/reader/full/blue-strategy 22/22

22 | P a g e

Score (over 75): The industry is unusually attractive. If you are in it, invest heavily for leadership. If

you are not in it, you may find it difficult to enter without acquisition, but if there is a suitable way in,

take it with both