BLEKINGE INSTITUTE OF TECHNOLOGY (BTH) School of ...€¦ · BLEKINGE INSTITUTE OF TECHNOLOGY (BTH)...

48

BLEKINGE INSTITUTE OF TECHNOLOGY (BTH) School of Management Sweden Master Thesis in Business Administration, 10 credits Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model Author: Mauricio Aracena Kovacevic Supervisor: Dr. Klaus Solberg Søilen Submission Date: 20 th June, 2007

Transcript of BLEKINGE INSTITUTE OF TECHNOLOGY (BTH) School of ...€¦ · BLEKINGE INSTITUTE OF TECHNOLOGY (BTH)...

BLEKINGE INSTITUTE OF TECHNOLOGY (BTH)

School of Management

Sweden Master Thesis in Business Administration, 10 credits

Key Success Factors for Ericsson Mobile Platforms

using Porter's Value Chain model

Author: Mauricio Aracena Kovacevic Supervisor: Dr. Klaus Solberg Søilen Submission Date: 20th June, 2007

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

Abstract Title Key Success Factors for Ericsson Mobile Platforms using Porter's Value

Chain model Author Mauricio Aracena Kovacevic Supervisor Dr. Klaus Solberg Søilen Institution School of Management, Blekinge Institute of Technology Course Master Thesis in Business Administration, 10 credits Purpose The purpose of this study is to extract the Key Success Factors for

Ericsson Mobile Platforms (EMP) by analyzing its value chain and possible areas of improvements. Furthermore, the aim of this study is to test the Value Grid concept as tool for strategic planning using the analysis of EMP’s value chain.

Methodology This master thesis is a case study of Ericsson Mobile Platforms (EMP)

from an inside-out perspective. The data is collected from documentation and from semi-structured interviews with people from EMP. The theoretical framework is a combination of traditional theories such as value chain analysis and newer approaches like value networks and added-value chain.

Conclusions The value chain analysis and the research model used in this study

demonstrated to be useful to identify the KSFs for EMP. Four KSFs were identified for EMP: ability to bring TTM cost-optimized platform with new technology; ability to integrate, test and deliver stable complex technology solutions in short time; excellent competence in radio technology; and finally, to have customers that generate high volumes. The KSFs for EMP resides in the fact that it has managed to define correctly the boundaries of the value chain activities, that is, it only does activities where it has core competences. After a deep analysis of the value chain and value system, the Value Grid concept proved to be an heuristic tool for finding opportunities of improvements for EMP. Finally, Value Grid framework seems to be suitable for firms who have value chains built on modular activities that can be re-used independently for creating other types of products.

Keywords Value chain, added-value chain, value networks, key success factors,

Value Grid, strategy, mobile phone, mobile platform industry.

2

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

Acknowledgments I would like to thank Dr. Klaus Solberg Søilen, my supervisor, for his guidance and support on how to conduct this study. Further, I would like to thank Martin E. Jönsson, Robert Puskaric, Linda Werneman, Fredrik Dahlgren and Pär Stigmer, all people from Ericsson Mobile Platforms who willingly accepted to collaborate in this study.

Last, but not least, I would like to thank my wife Fabiola for encouraging me to take this MBA study. Moreover, without her love and support I could have not managed to succeed in finishing this two years MBA program.

3

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

Table of Contents Abstract .............................................................................................. 2 Acknowledgments............................................................................. 3 List of figures..................................................................................... 6 1 Introduction .............................................................................. 7

1.1 Background .................................................................. 7 1.2 Aim ............................................................................... 7 1.3 Delimitations................................................................. 7 1.4 Outline of the study....................................................... 8

2 Theoretical Foundations.......................................................... 9 2.1 The Value Chain and the Value System....................... 9 2.1.1 Introduction................................................................... 9 2.1.2 Value chain................................................................... 9 2.1.3 Linkages ..................................................................... 10 2.1.4 Drivers in Competitive Advantages ............................ 10 2.1.5 Competitive scope in the value chain ......................... 12 2.1.6 The Value System ...................................................... 12 2.2 Value Network ............................................................ 12 2.3 The Added-value Chain.............................................. 13 2.4 The Value Grid ........................................................... 15 2.4.1 Value Grid framework................................................. 15 2.4.1.1 The vertical dimension................................................ 16 2.4.1.2 The horizontal dimension ........................................... 17 2.4.1.3 The diagonal dimension ............................................. 17 2.5 Key Success Factors (KSF) ....................................... 17 2.6 Research Model ......................................................... 18

3 Methodology ........................................................................... 20 3.1 Research Design........................................................ 20 3.1.1 Scientific motivations behind this research design ..... 20 3.1.2 Case Study................................................................. 20 3.1.3 Qualitative research.................................................... 21 3.1.4 Methodological Reflections......................................... 21 3.1.5 Critique on Source of Information............................... 21

4 Empirical findings .................................................................. 23 4.1 The Mobile platform Industry ...................................... 23 4.2 Ericsson Mobile Platforms (EMP)............................... 25 4.2.1 The EMP’s Value Chain and Value System ............... 29

5 Analysis................................................................................... 35 5.1 Value Chain Analysis.................................................. 35 5.2 Test of Value Grid....................................................... 39 5.2.1 Vertical Dimension...................................................... 39 5.2.2 Horizontal Dimension ................................................. 40 5.2.3 Diagonal Dimension ................................................... 40 5.2.4 Summary and Analysis of EMP’s Value Grid ............. 41 5.3 Key Success Factors for EMP.................................... 41

6 Conclusions............................................................................ 43

4

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

7 Suggestion for further research ........................................... 44 8 References .............................................................................. 45 9 Appendix ................................................................................. 47

9.1 Questionnaire ............................................................. 47 9.2 Terminology................................................................ 48

5

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

List of figures Figure 1: The Value Chain (Porter, 1985)........................................................................................9 Figure 2: The Value System (Porter, 1985) ...................................................................................12 Figure 3: The added-value chain (McPhee & Wheeler, 2006) ......................................................14 Figure 4: The Value Grid (Pil and Holweg, 2006).........................................................................16 Figure 5: The research model.........................................................................................................18 Figure 6: Traditional Value chain for a complete mobile phone manufacture (Anderson & Jönsson, 2006).. ..............................................................................................................................23 Figure 7: The value system for the mobile phone industry (Anderson & Jönsson, 2006).............24 Figure 8: System Architecture of EMP Products (Kornby, 2005) .................................................26 Figure 9: Main parts of an EMP Hardware platform. ...................................................................27 Figure 10: EMP’s business Model (Source: Ericsson)...................................................................28 Figure 11: EMP’s ecosystem (source: Ericsson, Dawidson & Karlsson, 2005) ............................29 Figure 12: EMP’s Value Chain ......................................................................................................34

6

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

1 Introduction

1.1 Background Mobile phones are becoming more complex every day. They do not just offer voice services, but a set of other services such as data communication and multimedia services. The mobile phone industry has become much more intricate then it was before, several parties and industries are involved in the design of a mobile phone: network operators who provide the network infrastructure and put requirements on mobile phones, mobile manufactures, mobile platforms providers and other players who provide more specific components such as memories and displays. The evolution of the mobile phone industry has experience changes in the past years. Originally, the process of making a complete mobile phone used to belong to a single company, however, as it occurred with the PC industry, the value chain for making a mobile phone started to be fragmented to a more stratified approach (Anderson & Jönsson, 2006). Consequently, new companies have appeared in the industry where they provide technology in different parts of the value chain. Companies like Ericsson Mobile Platforms and Qualcomm are examples of this change in the industry. They provide technology solutions for mobile manufactures that allow them to build a new phone in a faster way without having the core knowledge of making complex technologies like radio access technologies. However, this new landscape in the mobile industry makes it complex to analyze competitive advantages for companies such as Ericsson Mobile Platform and Qualcomm, since they group different activities of the value chain for making a mobile phone. For instance, Qualcomm is regarded as a fabless company that makes the whole hardware design for a mobile platform, but it does not manufacture the phone. On the other hand, Ericsson Mobile Platforms does partly the hardware design (but with a more reduced number of employees compare to Qualcomm) and leaves to suppliers to do the rest of the hardware design. This difference makes it hard to evaluate what are the competitive advantages for each company, since the level of vertically integration does not necessarily means a direct competitive advantage in this complex industry. As technology becomes more complex, companies have started to outsource more from the suppliers. Nowadays, companies may not have any physical flow in their value chain and may depend more on intangible factors such as relationship with suppliers. Thus the traditional concept of value chain may not be sufficient for today’s firms.

1.2 Aim The aim of this study is to identify the Key Success Factors (KSF) for Ericsson Mobile Platforms by analyzing its value chain and possible areas of improvements. Further, the aim is to test the Value Grid as a tool for strategic planning from the empirical data extracted in this research.

1.3 Delimitations A proper analysis of the KSF for EMP, would have been to do benchmarking with other companies from the same Industry. This is the ideal case since it is possible to define in a better manner EMP’s strategic advantages. However due to time limitations, and in part availability of

7

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

information, this research focuses only on an inside-out perspective. This study is also limited, for the same reason, to test the concept of the Value Grid using one source of empirical data (i.e. a single case study).

1.4 Outline of the study The remaining of this master thesis is organized as follows: chapter 2 presents the theoretical foundations used in this study for analyzing the competitive advantages of EMP. Chapter 3, describes the methodology used in this master thesis for extracting the empirical data. Chapter 4 presents the empirical findings concerning mobile platform industry, the EMP company and its value chain. The analysis is this master thesis is conducted in chapter 5, here the theoretical foundations are tested using the empirical data. Finally, the conclusions and suggestion for future work are found in chapter 6 and 7 respectively.

8

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

2 Theoretical Foundations

2.1 The Value Chain and the Value System

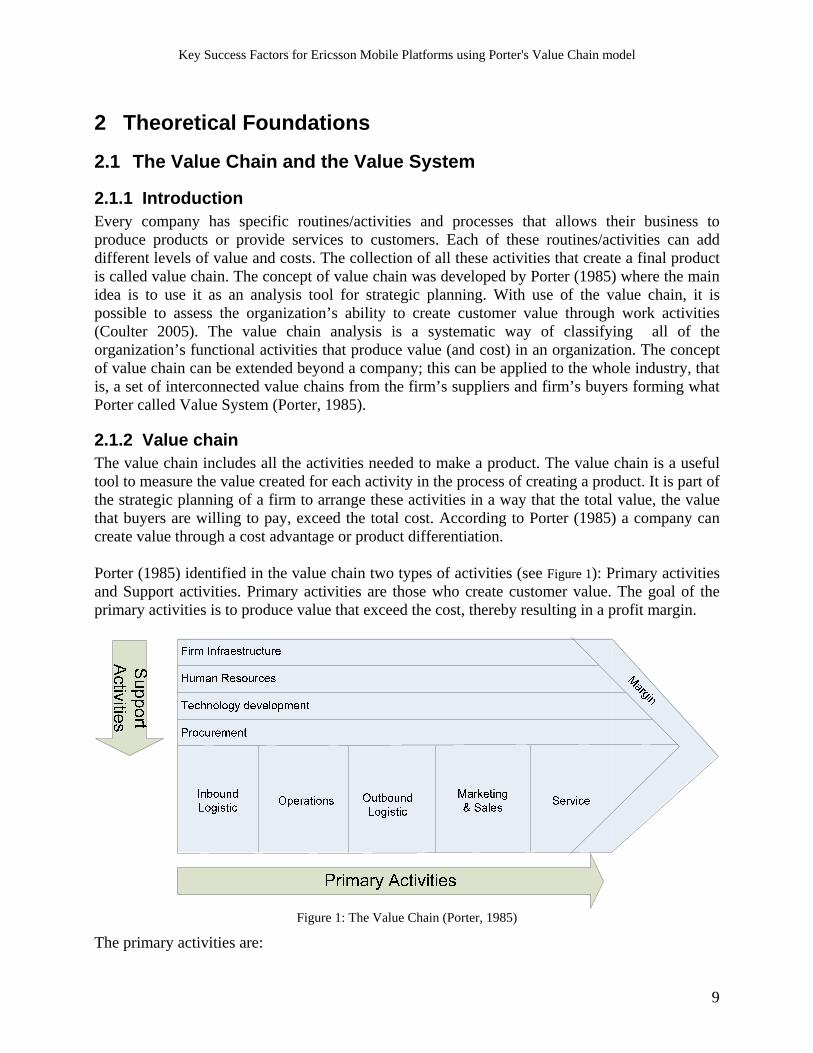

2.1.1 Introduction Every company has specific routines/activities and processes that allows their business to produce products or provide services to customers. Each of these routines/activities can add different levels of value and costs. The collection of all these activities that create a final product is called value chain. The concept of value chain was developed by Porter (1985) where the main idea is to use it as an analysis tool for strategic planning. With use of the value chain, it is possible to assess the organization’s ability to create customer value through work activities (Coulter 2005). The value chain analysis is a systematic way of classifying all of the organization’s functional activities that produce value (and cost) in an organization. The concept of value chain can be extended beyond a company; this can be applied to the whole industry, that is, a set of interconnected value chains from the firm’s suppliers and firm’s buyers forming what Porter called Value System (Porter, 1985).

2.1.2 Value chain The value chain includes all the activities needed to make a product. The value chain is a useful tool to measure the value created for each activity in the process of creating a product. It is part of the strategic planning of a firm to arrange these activities in a way that the total value, the value that buyers are willing to pay, exceed the total cost. According to Porter (1985) a company can create value through a cost advantage or product differentiation. Porter (1985) identified in the value chain two types of activities (see Figure 1): Primary activities and Support activities. Primary activities are those who create customer value. The goal of the primary activities is to produce value that exceed the cost, thereby resulting in a profit margin.

Figure 1: The Value Chain (Porter, 1985)

The primary activities are:

9

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

• Inbound logistic: The receiving and warehousing of the raw materials and distributing

the activities involves the process of transforming the input

he

and customer

he primary activities are assisted by the support activities. The support activities are classified

• Procurement: This refers to purchasing the right quantity of input materials used by the

al Development: This refers to technologies that improves the processes of

These activities involve recruiting, hiring, training, development and

ts the total value chain, this refers to the organizational

2.1.3 Linkages alue chain are not independent. Linkages may exist between activities, that

he value chain analysis can also be focused on the linkage between companies’ value chains.

2.1.4 Drivers in Competitive Advantages

lue through a cost advantage (Porter, 1985). By analyzing the value chain and

inputs to the products. • Operations: These are

products into finished product or services. That is, machining, assembling, testing, etc. • Outbound logistics: These are the activities that collects and physically distribute t

products to the buyers, like warehousing, inventory control and scheduling delivering. • Marketing and Sales: Marketing the goods and services to the customers. • Customer Service: This involves installation, maintenance, after sales

support. Tinto four areas:

company. A simple approach would be to purchase repetitively the same materials from different suppliers. A more complex approach would be to find long term partners to lower cost.

• Technologicproducing a product by reducing cost of production or technologies that support value creating activities.

• Human Resources:compensation of all personnel.

• Firm Infrastructure: This affecstructure of the company, financial, planning, control systems, management, etc.

The activities in the vis, one process may affect the cost and performance of others. Linkage can exist between primary activities, as well as, between primary and support activities. Therefore, competitive advantages can be also derived from the linkages between activities. TInterrelationships between suppliers and buyers of the firm also play an important role in creating competitive advantages. By connecting various activities between the players in the value system, it is possible to optimize and coordinate in a more efficient manner. The channel linkage (between the firms and buyer) can performs activities such as sales and advertisement, where having a good coordination between the parties can reduce cost and increase competitive advantages, in this case, the company products become part of the buyer’s value chain.

Cost advantages A firm can gain vathe distribution of the cost in each activity, the firm can reconfigure its activities to reduce cost. If

10

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

a firm manages to reduce the total cost to a level that it is lower than its competitors then the firm has reached a cost advantage. Porter identified ten cost drivers (Porter, 1985):

• Economies of scale: Companies can increase efficiency in cost with volume production. • Learning: The labor improve the efficiency of doing an activity by gaining experience,

this may reduce the cost of this activity. • Pattern of capacity utilization: An activity that has a high fix cost associated, it cost will

be affected by capacity of utilization. • Linkages among activities: Linkages between activities can create the opportunity to

lower the cost of connected activities. • Interrelationships among activities: A more integrated value chain in a firm leads to better

the possibilities to reduce cost among activities. • Interrelations among business units: Interrelationship between business units of a firm can

affect the cost. The cost can be lowered when these activities are synchronized. • Degree of vertical integration: The level of integration of a firm may influence the cost of

their activities, e.g. if a firm can produce raw materials instead of buying them, the cost of the activities that transform them in to final products may become lower.

• Timing: first movers may impact the cost of the activities. • Location: The cost can be affected by the geographical location of the activities related in

other places. • Institutional factors: Government regulation, taxes and other financial incentives

constitute a cost driver in the final parts of the value chain. Differentiation A firm can gain value through product differentiation (Porter, 1985). Porter identified several drivers of uniqueness:

• Policies and decisions: Firm can choose what activities to perform and how to perform them in order to make them unique.

• Linkages among activities: A firm can have linkages that make some activities to perform better that competition.

• Timing: First movers of placing a new product in the market make them unique. • Location: By placing units/production/sales in critical locations may lead to uniqueness. • Interrelationships: Sharing activities between sister business units, like sharing sales

forces, can make the firm unique by offering better services. • Learning: An activity can be unique as a result of the learning process within a firm. • Integration: A higher degree of integration in a value chain can make a firm unique

because it has better control of more activities. • Scale: A firm can get an activity to perform in a unique way when producing large

volumes. • Institutional factors can lead a firm to be unique, such as building a good relationship with

the union. (Porter, 1985).

11

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

2.1.5 Competitive scope in the value chain There are four dimensions of competitive scope that affect the value chain (Porter, 1985). They are segment scope, degree of integration, geographical scope and industry scope. A firm with a broad scope can benefit from performing more activities internally, while a firm with a narrow scope can adapt their value chains to a specific market segment.

• Segment Scope: A firm can differentiate their products in order to serve different needs or market segments. If a firm provides a unique product that it is needed for a specific market segment then it can lead this market and reach a competitive advantage, in this case, differentiation favors narrow scope. A firm can also use the interrelationships between value chains that serves different segments to favor a broad scope (Porter, 1985), that is, a firm that uses different value chains that produce different products but it shares many value activities.

• Degree of Integration: The division of activities between a firm and its suppliers, channels and buyers is defined by the degree of vertical integration in the value chain (Porter, 1985). A firm that can produce raw material rather than buying from external suppliers may have a better control of the cost in the activities in the value chain.

• Geographic scope: A firm can share or coordinate value activities in one place to produce a product, but it sells them in different geographical areas

• Industry scope: A firm compete with a coordinated strategy in a range of related industries (Porter, 1985).

2.1.6 The Value System Porter (1985) extends the concept of the value chain; a firm’s value chain is part of an interconnected value chains between suppliers and buyers called Value System. The value system includes the value chain of the upstream suppliers and downstream channels and customers, see Figure 2.

Figure 2: The Value System (Porter, 1985)

The total margin available is spread across suppliers, distributors and customers (Recklies, 2001) in the value system. The amount of how much part of this margin is received by each member depends on its market positions and negotiation power (Recklies, 2001). A firm who has higher degree of vertical integration has a better position in coordinate its upstream and downstream activities (therefore get a higher margin), however a company who has less degree of vertical integration can also get high margins if it can succeed in having agreements between suppliers and partners to achieve better coordination (netMBA.com, 2002-2007)

2.2 Value Network Value chain and the Five Forces Model of Porter (1980, 1985) have been widely used for more than 30 years. These tools strongly focus on the tangible aspects of the organization and they tend

12

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

to isolate the organization’s activities from its environment (Middendorp, 2005). Moreover, the value that can be extracted from the organization activities is measured in terms of financial value (margin) but ignore the fact that intangible assets such as competencies, internal structures and relationship with the environment are the driving factors behind the financial results (Sveiby, 1997). New methods have appeared to take into consideration the intangible assets. Value Network Analysis (Allee, 2003) is a “method that combines tools that analyze strategy with insight into complexity of interactions among people” (Middendorp, 2005). This analysis is based on the intangible assets should be considered as negotiable and exchangeable. Peppar and Rylander (2006) introduced the Network Value Analysis (NVA) method as “a way to analyze competitive ecosystems” (Peppar and Rylander, 2006). They argue that the traditional value chain analysis is inappropriate, since it focuses only in the end product and in the internal firm’s activities that generate the product (which are suitable for physical products) and it does not consider the strong co-operative behavior and relationships between the different parties that show today’s industries (Peppar and Rylander, 2006). In the value network concept, “value is co-created by a combination of player in the network” (Peppar and Rylander, 2006). With this method companies “focus not the company or the industry, but the value creating system itself” (Peppar and Rylander, 2006) that includes the different economic actors: suppliers, partners, allies and customers. Value networks are composed of a set of nodes and links, each node is an autonomous unit that can be managed independently, where services are delivered from one node to another through these links. The key of this model is that tries to understand how value is created in relationships, then value networks tries to view the relationships as a network of interdependent relationships. Consequently, this method looks how a firm can create value within the context of the network (Peppar and Rylander, 2006), in order to understand the competitive environment in the network economy. Therefore, firms must build relationships among the different players in the industry so they can cultivate an ecosystem, a set of firms that can co-create value (Peppar and Rylander, 2006). Firms that “understand the sources of value in the network and are able to exploit them will be the winners” (Peppar and Rylander, 2006).

2.3 The Added-value Chain According to McPhee and Wheeler (2006), from a traditional value chain perspective, focusing on the internal core activities of a firm is not enough to derive value in today’s firms. Successful firms are now “replacing from an internally focused strategy-development models to alternatives that allow a broader view of the firm a part of the world around it” (McPhee and Wheeler, 2006). In this context, firms should include, as well, the activities that creates value through external relationships (McPhee and Wheeler, 2006). McPhee and Wheeler (2006) proposed an added-value chain model where it includes a set of expanded business activities from different business models and a re-definition of value that incorporates brand, reputation, and relationship-based value drivers of the firm. Thus this model encompasses three new ideas: firstly, a new definition of value that includes intangible assets, secondly, it moves from a centric view to view the firms as part of a broader community, and finally, it adds activities that involves cross-functional teams of employees from across several areas. (McPhee and Wheeler, 2006).

13

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

The proposed added-value model (McPhee and Wheeler, 2006) is showed in Figure 3.

Figure 3: The added-value chain (McPhee and Wheeler, 2006)

Margin and Brand Equity In the added-value chain model, the definition of value incorporates profit margin and intangible assets like leadership quality, innovate capability, brand equity and competences in strategic-alliance development. This new value definition gives to the firms the ability to evaluate how their strategy affect both “hard” and “soft” assets of the firms (McPhee and Wheeler, 2006). Expanded Activities The added-value chain includes three new primary activities and one new support activities from the original value chain from Porter (1985); they are: Supply Chain Management, Product use, End of Primary Use and External Networks, see Figure 3. Supply chain Management As in the Porter’s value chain (1985), the supply chain remains outside the added-value chain. However, it includes the activities that involves the interaction of the firm with suppliers such as product quality, R&D, product development partnerships, and sharing of production knowledge (McPhee and Wheeler, 2006). Product use The idea is to include the customer interaction into the firm’s value chain (not just the responsibility of the sales and service departments as in the traditional value chain). This involves activities related to how customers use the product: managing customer networks, product testing and development and outsourcing (McPhee and Wheeler, 2006). By including product usage intelligence in the value chain (as means of informing product development) (McPhee and Wheeler, 2006), firms can think from a value network perspective and can co-create value with customers (Prahalad and Ramaswamy, 2004).

14

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

End of primary use The added-value chain incorporates the value of capturing some of product’s residual value after the customer is finished with it. These activities are leasing management, product take-back, management of secondary markets and recycling (McPhee and Wheeler, 2006). External Networks This set of activities include the management of external networks and other firms, that is, customer, suppliers, vendors, institutions, peer associations and stakeholders (McPhee and Wheeler, 2006). In corporate strategy, this topic is considered as potentially important component, as for example when firms are members of technology cluster (Porter, 1998). According to Porter (1998) firms that participate actively with academic players can create a competitive advantage, that is, building value from activities derived from their external networks. When firms include the analysis into the added-value chain, they can decide how to determine their relationship with external networks that influence most to increase their value proposition; for instance, using the external networks to build value through innovation, knowledge capture, and reputation-building (McPhee and Wheeler, 2006).

2.4 The Value Grid The value chain created by Porter (1985) represents a sequence of activities that add value to the final product. The traditional concept of value chain consists in that raw materials are transformed into final products, stored, distributed, sold and serviced. From the value chain, strategic planners can identify activities where they can improve to gain strategic advantages in cost or product differentiation (Porter, 1985). However, the concept of value chain is not without critics; the value chain has become inappropriate today as a tool to analyze industries and to uncover source of value (Peppar and Rylander, 2006), due to more products and services become dematerialized. New researchers, such as, Pil and Holweg (2006) argue that this approach “it can also put a stranglehold on innovation at a time when the greatest opportunities for value creation (and the most significant threats to long-term survival) often originate outside the traditional, linear view”. Pil and Holweg (2006) developed an evolved concept of Value Chain called Value Grid.

2.4.1 Value Grid framework According to the Pil and Holweg (2006), the Value Grid has a variety of new paths to enhanced performance, resulting in a three dimensional grid. They are: the vertical, the horizontal and the integrative diagonal dimensions, see Figure 4.

15

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

Figure 4: The Value Grid (Pil and Holweg, 2006)

The Value Grid concept emerge from thinking nonlinearity within the value chain. Within the vertical dimension, companies seek for nonlinear opportunities in the traditional value chain by looking in to the upstream and downstream from the adjacent players. Within the horizontal dimension firms look for opportunities in parallel value chains. On the other hand in the diagonal dimension, companies take an integrative approach to explore more widely in other levels and value chains for opportunities to create value and reduce risk.

2.4.1.1 The vertical dimension - Nonlinearity thinking Firms are seeking for competitive advantages with the value chain by reducing cost, reducing lead time between activities and increasing coordination between supplier and customers (Pil and Holweg, 2006). However, how the benefits are distributed across the value chain depends on the balance power between suppliers and manufactures. Pil and Holweg (2006) said that “the strategy focus needs to shift from lead-time reduction to the power dynamics between the company and other players in the chain”. Therefore companies needs to focus on three areas:

• Opportunities to influence customer demand both upstream an downstream. In this case companies are looking for ways to control who drives the purchase decision in the supply chain, for instance by influencing demand from some intermediate products. If the firm cannot influence the customer directly, the firm can explore the value chain in a more broad perspective by identifying or “inserting levers that will shift decisions from one point to another” (Pil and Holweg, 2006).

• Opportunities to modify information access in either direction. Companies can shift the buying decision when they are able to link information with control. For example, companies can control their suppliers by forcing them to choose an specific second-tier supplier. The suppliers sees this level of control as part of their interest. (Pil and Holweg, 2006)

• Opportunities to explore penetration points in multiple tiers that are not immediately adjacent. In this case companies assume multiple positions in the value chain in order to diversify demand and limit a particular buyer’s power. (Pil and Holweg, 2006).

16

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

2.4.1.2 The horizontal dimension – Exploring Parallel Value chains This dimension provides opportunities for companies to move across value chains, in order to leverage economies of scale across multiple sources of demand (Pil and Holweg, 2006). For instance, if a supplier is able to produce flexible components that can be re-used in more than one type of products, then the suppliers are able to generate sales and spread its cost. The potential of this dimension is that enable companies to (Pil and Holweg, 2006):

• Manage risk: the firms can spread demand and development risk for a component across multiple value chains and level demand by operating in value chains with orthogonal demand and risk (Pil and Holweg, 2006).

• Seize existing value: The firms can supply special products or components (with advance technology that differentiate to the rest of the components in the market) to competitors. In this case, firms not only gain economies of scale but also they can establish and control the future development of this particular component (Pil and Holweg, 2006).

• Integrate sources of existing value: The firms can generate value by joining or integrating value across different value chains. (Pil and Holweg, 2006).

• Explore new ways to create value: The horizontal thinking allows viewing parallel value chains from different industries, in this way companies can integrate these parallel value chains to offer package or price combinations that with a single value chain approach cannot be done.

2.4.1.3 The diagonal dimension – Exploiting Value Chains Across Tiers With this dimension, firms explore the grid in an integrative fashion, in order to increase the control over inputs and customers. Firms looks at the upstream and downstream of other value chains for controlling the supply chain of critical components and uncovering new ways of boosting customer demands (Pil and Holweg, 2006). Pil and Holweg described two strategies that take advantages from this dimension:

• Pursuing Pinch-Point mapping: In this case companies shall monitor key component supplies and negotiate alternative source of components.

• Defining Demand enablers: Companies who have a particular expertise in a given value chain, can examine other value chains in other industries that can leads to new opportunities to leverage key competitive advantages (Pil and Holweg, 2006).

2.5 Key Success Factors (KSF) Critical Success Factors (CSFs or denoted sometimes as Key Success Factors, KSF) are “the limited number of areas in which satisfactory results will ensure successful competitive performance for the individual, department or organization. CSFs are the few key areas where "things must go right for the business to flourish and for the manager's goals to be attained” (Bullen & Rockart, 1981). However, in the literature Key Success Factors has different meanings depending how it is used. According to Grunert and Ellegaard (1992), KSFs can be used in 4 different ways: “as a necessary ingredient in a management information system, as a unique characteristic of a company, as a heuristic tool for managers to sharpen their thinking and finally,

17

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

as a description of the major skills and resources required to be successful in a given market”. In this master thesis, the last view will be used. Thus, KSF in this study is defined the same as in Ghosh, et. al (1998), “as factors which are critical for excellent performance of the company, rather than just survival…”. Grunnert and Ellegard (1992) defined Key Success Factors as the skills or resources of a company that provide competitive advantages in value and/or cost in any market. KSF can be distinguished in the degree of how easy competitors can emulate them, that is, in their level of changeability (Grunnert and Ellegard, 1992). Key Success Factors also differ if they are conjunctive or compensatory. The former, are the necessary factors conditions for superior performance and, the latter, are the factors that open up for choices of areas of excellence and hence formation of strategic groups (Grunnert and Ellegard, 1992). There are several techniques for identifying Key Success Factors, Leidecker and Bruno (1984) proposed the following: environmental scanning, industry structure analysis, industrial expert’s opinions, competitor’s analysis, best practice analysis, assessment of the company’s internal feeling or judgment, intuitive factors and gathered data of profit impact and market strategy. In this master thesis, a mix between internal assessment of a firm and from industrial expert’s opinions will be used. This internal assessment technique focuses into explore what the firm does well and not so well while with the experts’ opinions technique, the KSF are extracted from people who have excellent knowledge and experience in the industry.

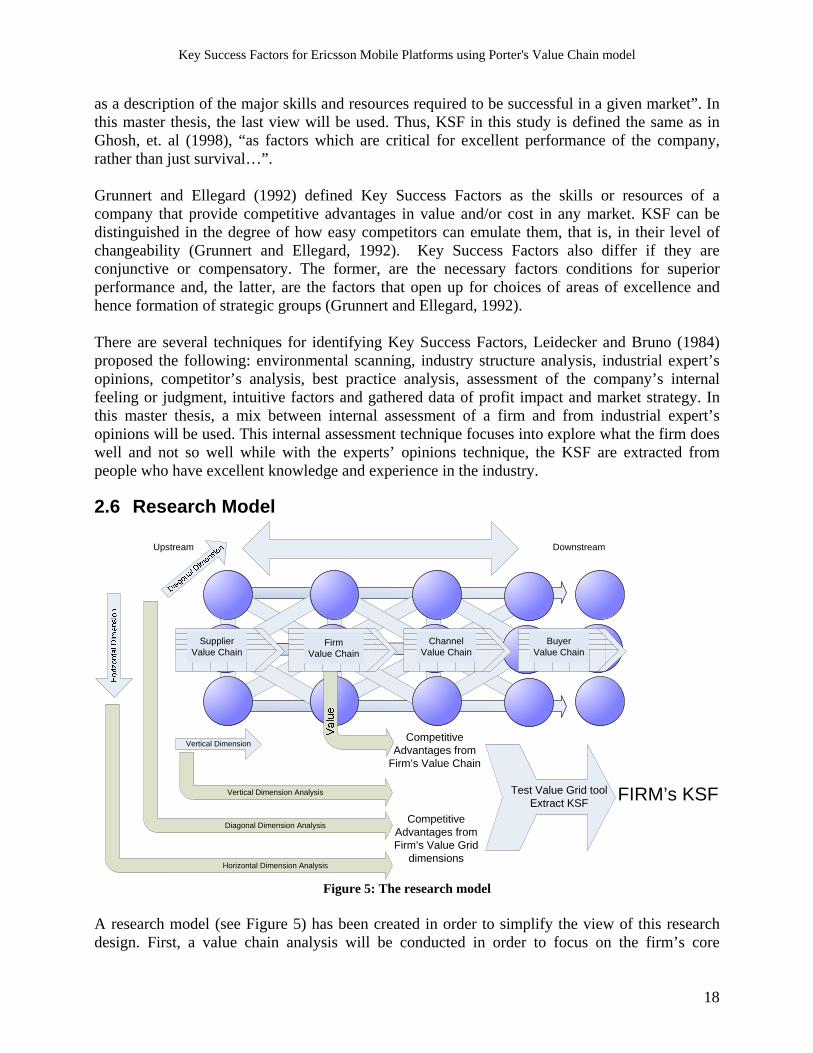

2.6 Research Model

Upstream Downstream

Supplier Value Chain

Firm Value Chain

Channel Value Chain

BuyerValue Chain

Competitive Advantages from

Firm’s Value Chain

Vertical Dimension

Competitive Advantages fromFirm’s Value Grid

dimensions

Test Value Grid toolExtract KSF FIRM’s KSF

Diagonal Dimension Analysis

Vertical Dimension Analysis

Horizontal Dimension Analysis

Figure 5: The research model A research model (see Figure 5) has been created in order to simplify the view of this research design. First, a value chain analysis will be conducted in order to focus on the firm’s core

18

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

competences from an inside perspective. In parallel, the firm’s value chain will be positioned into the value system of the industry, in order to identify adjacent players and external linkages and determine firm’s ecosystem. An analysis of the Value Chain is conducted in order to identify competitive advantages. From the Value System and the ecosystem, the Value Grid framework is used to identify competitive advantages from its three dimensions. The outcomes from Value chain and Value Grid are analyzed to test the Value Grid and to extract the KSF for EMP.

19

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

3 Methodology

3.1 Research Design A research design provides a framework for the collection and analysis of data (Bryman & Bell, 2003), where a research method is the technique for collecting data (Bryman & Bell, 2003). In this master thesis, it has been chosen to use a case study approach in a single organization, Ericsson Mobile Platforms, where the data collection is based both from existing available source of information and from qualitative interviews.

3.1.1 Scientific motivations behind this research design According to Esterby-Smith, et al. (2002), it is important to understand the philosophical issues behind the research design. It helps to: clarify the research design, recognize which designs will work or not and finally, it can help the researcher to identify or even create designs that may be outside of the researcher experience (Esterby-Smith, et al. 2002). The philosophical issues consist of ontological and epistemological questions about the nature of the research. Ontology is defined as “assumptions that we make about the nature of reality” (Esterby-Smith, et al. 2002) and epistemology is defined as “general set of assumptions about the best ways of inquiring into the nature of the world” (Esterby-Smith, et al. 2002). From epistemological point of view, this research design is based on social constructionism, where “the reality is determined by people rather than by objective or external factors” (Esterby-Smith, et al. 2002). In this master thesis, the purpose is to understand what the EMP’s competitive advantages (reality) are by asking the people who work in this organization. As the social constructivism stances, here the observer (author) is part of what is being observed (employee of the EMP organization) and the extraction of the data incorporates the perspective of the stakeholders, that is, the interviewees. Moreover, the conclusions will be induced from the analysis of the interviews. From an ontological point of view, this research assumes a representationalist position, where it is desired to obtain “an accurate reflection of reality” (Esterby-Smith, et. al. 2002). In this case, to identify the Key Success Factors for EMP. Based on the ontological and epistemological positions described above, it can be concluded that a case method based using a qualitative approach through interviews is suitable to understand the EMP’s competitive advantages.

3.1.2 Case Study A case study is a method where entails the analysis of a single case (Bryman & Bell, 2003), in this master thesis the case is a single organization: EMP. Yin (2003) suggests that a case study is “an empirical inquiry that investigates a phenomenon within its real-life context”. Through this case, it is intended to evaluate the Value Grid theory as a tool to analyze the EMP’s strategy and to identify Key Success Factors.

20

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

3.1.3 Qualitative research The ontological and epistemological position stated above that a qualitative method would be logical to fulfill the purpose of this master thesis. A qualitative research “emphasizes words rather than quantification in the collection and analysis of data” (Bryman and Bell, 2003). From a quality research it can be inducted the relationship between theory and research (Bryman and Bell, 2003). Qualitative methods lead to a more in-depth analysis (Estherby-Smith, et. al. 2002) and it requires a small sample of data. Therefore personal interviews with key persons at EMP was considered to be the best alternative. Data Collection For this research, it has chosen to collect data from semi-structured interview, where the interviewer has a specific list of topics to be covered (Bryman and Bell, 2003). The advantage of this method is that the interviewer has the flexibility to reformulate the questions or simply ask new questions that may appear as a result of the answer of the interviewee (Bryman and Bell, 2003). According to Grunert and Ellegaard (1992), perceived KSF can be measured by this type of interview with business decision makers. Since the author of this master thesis is an employee of the company in study, it was easy to have access to documentation related to the company strategy and the industry. Moreover, to get access to key persons inside the EMP’s organization was rather simple as well. Five key persons were chosen for an interview from EMP. Robert Puskaric, head of EMP, Martin Jönsson, from Product Portfolio Management, Fredrik Dalhgren Deputy Director of System Management, Pär Stigmer from Sourcing and Supply and Linda Wenerman from Product Management.

3.1.4 Methodological Reflections Different criteria need to be considered in order to evaluate the quality of the research design. They are reliability and validity. Reliability refers to if the study is “transparent in how sense was made from the raw data” (Estherby-Smith, et. al. 2002), while validity refers to if this research study “gain access to the experiences of those in the research setting” (Estherby-Smith, et. al. 2002). In this study internal reliability was verified by comparing the results directly from the opinion of the respondents when they were asked about what are the Key Success Factors and from a deep analysis of EMP’s value chain made by the author of this master thesis. Internal validity was verified by comparing the outcomes from the different theories used in this thesis: value chain, Value Grid and KSF theory.

3.1.5 Critique on Source of Information All the information was collected from documentation provided by Ericsson and from the informants in the interviews. It was chosen to not use a tape recorder during the interviews; the reason was to avoid the distraction for the interviewees in order to let the interviewees to speak freely and secure. One could argue that lot of information could have been missing due to the

21

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

interviewer may have not been able to write down or memorize all the conversation, however, since interviewer is an EMP’s employee, he could easily focus in extracting only the relevant information concerning to this study, due to that he is very familiar with the concepts and definitions used inside EMP.

22

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

4 Empirical findings

4.1 The Mobile platform Industry Since the first handheld mobile phones entered the market, mobile phones have evolved from voice centric devices to data and multimedia devices allowing mobile phones to handle a set of non-voice content such as music, videos and games (Kornby, 2005). As a consequence, mobile phones do not only include radio technology (such as GSM, GPRS, EDGE and WCDMA), but several other technologies have been incorporated to support these new type of multimedia services; some of them are color displays, mega-pixel cameras, music players, web browsers and e-mail clients (Kornby, 2005). Kornby (2005) says today’s industry challenges for 3G mobile phone manufactures are: first, to face the growing development in 3G technology to provide a stable commercial product and second, to compete in technology in terms of size, cost and power consumption. During the late 80’s and 90’s, companies like Ericsson, Motorola and Siemens used to manufacture the complete phone, that is, they had the complete control of the design, production and marketing of the mobile phone, see Figure 6 for a description of a traditional value chain.

Figure 6: Traditional Value chain for a complete mobile phone manufacture (Anderson & Jönsson, 2006). Traditionally phone manufactures had a highly vertically integrated value chain.

23

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

However, in the last decade the mobile handset industry has changed from a vertical specialization to a more horizontally stratified structure (Andersson & Jönsson, 2006, see Figure 7). Andersson and Jönsson (2006) say that the main drivers for this trend has been: “Latent gains from trade companies who are able to sell technology across firm boundaries” and “emerging capabilities differences amongst firms in the industry driven by increased multidimensional technology complexity as phones become more sophisticated”. Several companies has started to specializing in specific hardware components such as radio chips, audio components and key peripheral such as display, camera modules, memory and batteries. Thus mobile phone manufactures are now focusing in the activities within the value chain where they have the core competence and outsource the rest (Andersson & Jönsson, 2006).

Figure 7: The value system for the mobile phone industry (Anderson & Jönsson, 2006). The value system shows a more horizontally stratified structure. The traditional value chain has been split, now there are more parties involves in the process of making a mobile phone. Each party focuses in areas of the value chain where they have their core competence. Many companies focus more in the design of the phone (service domain) while others focus on the manufacture and assembly of the product (physical domain).

24

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

As an example of this, Ericsson Mobile Communications (a complete phone manufacture) split into Ericsson Mobile Platforms and the Swedish-Japanese join venture company Sony Ericsson. Under these circumstances, Ericsson Mobile Platforms started to sell its technology to several companies, for instance, Sony Ericsson and LG Electronics. Now these companies can differentiate their products with different applications and functionality into different market segments by having basically the same technology inside. Today, there are many mobile phone platforms actors in the world, in addition to Ericsson we can mention Qualcomm and Freescale. The network operator industry has also faced changes in the way how they receive revenues. Network operators have increased the available bandwidth by upgrading their networks to 3G, thus, they can offer more data services. That is, they have evolved from offering voice telephony services to a variety of multimedia services, such as downloadable ring tones, short messaging services (SMS), multimedia messaging services (MMS) and data transfers services such as streaming and web browsing (Kornby, 2005). Moreover, network operators are starting to require a standardized platform in the handset so they can put their own application software in the phones they sell regardless of the phone manufacture (Kornby, 2005). This leads operators to substantial cost saving opportunities in areas as device verification, service creation, device provisioning, customer care and training (Andersson & Jönsson, 2006).

4.2 Ericsson Mobile Platforms (EMP) Ericsson Mobile Platforms is a business unit within the Ericsson Group. It was founded in September 1, 2001 as a result of a split from the Ericsson mobile handset division, Ericsson Mobile Communications. This split ended up in Ericsson Mobile Platforms (EMP) and the joint-venture Sony Ericsson Mobile Communications. Before that time, Ericsson produced mobile platforms for in-house use only. Through EMP, Ericsson started to license open-standard 2.5G and 3G technology platforms to others mobile phone manufacturers and other mobile communication devices. Thus, Ericsson could still keep the development of platform technology and sell it to established and new entrant vendors. Today, EMP has approximately, 1800 employees in seven global sites: Sweden (headquarter in Lund), Norway, China, USA, Japan, South Korea, Taiwan and Germany. EMP products EMP offers stable platform deliveries that include ASICs and development boards (hardware), platform software, reference design, development and testing tools, training, support and documentation (source: Ericsson). The EMP platforms contain integrated circuits and software needed to build a GPRS, EDGE and/or WCDMA phone. It provides all the system functionality such as Network Signaling, Data communications and Multimedia services. EMP products consist on three main entities (Kornby, 2005):

• A reference design, a well tried-and-tested blueprint where all the EMP functionality has been tested, allowing the customers to only focus in writing their applications and product differentiation.

• An EMP integrated circuit, that contains all the key hardware components • The platform software, that contains all the interfaces to control the software and

hardware.

25

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

Platform Software The system architecture of EMP is a modular design that is built on a use case analysis (Kornby, 2005). Examples of use cases are: imagining, video telephony, voice call, multimedia streaming, call handling, audio and video. The system architecture design (both software and hardware) consist on the following service stacks (see Figure 8):

Figure 8: System Architecture of EMP Products (Kornby, 2005)

• Middleware Services, which contains all the JAVA support and a set of Application

Program Interfaces (API) called OPA (Open API) to control the software platform. • Network Access Services, which contains all the network access stack for GSM, GPRS,

EDGE, WCDMA and HSPA. • Data Communication Services, which contains all local connectivity, such as Bluetooth,

USB, WLAN and protocol stacks such is TCP/IP. • Man-Machine Interface (MMI) Services, which contains support for accessing the user

interface devices such as camera interfaces and acoustic components. It also contains all the multimedia features such as Video and Audio codecs.

• Application Platform Services, which provides support for data storage and management, such as phone book, positioning, clock, message transport and cell broadcast applications.

• Operation Services, which provides basic control support like Operating Systems, platform security, battery and power management, SIM services and platform start-up and shutdown.

The following criteria have been taken into account to develop this system architecture (Kornby, 2005): complete platform software (not only protocols), stability, flexibility, scalability to different market segments, adaptable to customer software applications, one single architecture for different mobile systems (GPRS, EDGE, WCDMA), maximum reuse of components and customer applications between software; and backward compatibility in software over the time.

26

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

Customers builds their applications on top of EMP platform software stack. Examples of customers applications are: multimedia players, phone call applications, web browsers, etc. EMP also supply a suite of core applications where customers can use a starting point for building their applications. Application Suite EMP also provides a complete application suite to support customers who do not build their own applications. This is especially for customers that want to focus in the low end market. The goal of the EMP’s Application Suite is to reduce time-to-market for customers in launching their phones. Hardware The EMP hardware consists on three main parts: a Radio Frequency device (RF) that handle the radio communication for GSM, GPRS, WDCMA, HSPA and EDGE, a Digital Base Band (DBB) circuit, that contains the phone processors or CPUs and a Mixed Signal circuit or Analog Base Band (ABB) which converts signals from analog to digital and vice versa. In addition, the platform contains peripheral components such as displays, cameras modules, memory and batteries, where customers chose which type of device to use, see Figure 9. Moreover, EMP provides a flexible hardware solution that allows customers to add external hardware components to enhance the features and capabilities of the phone. Customer can add external application CPU processors for running other operating system than provided by EMP, such as SymbianTM and Windows MobileTM and add companion chips to enhance concurrency use cases capabilities in the platform. This extensibility of the platform allows customers to differentiate even further their products.

Digital Base Band (DBB)

Analog Base Band (ABB)Radio Frequency (RF)

Peripherals

Convert Analog signals to Digital Signal and vice versa

Displays, Cameras, batteries, etc.

CPUs and external Phone processors (customers)

WCDMA, GSM/GPRS, EDGE

EMPCPU 1

EMPCPU 2

External CPU (customers) Companion

Chip

Figure 9: Main parts of an EMP Hardware platform.

27

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

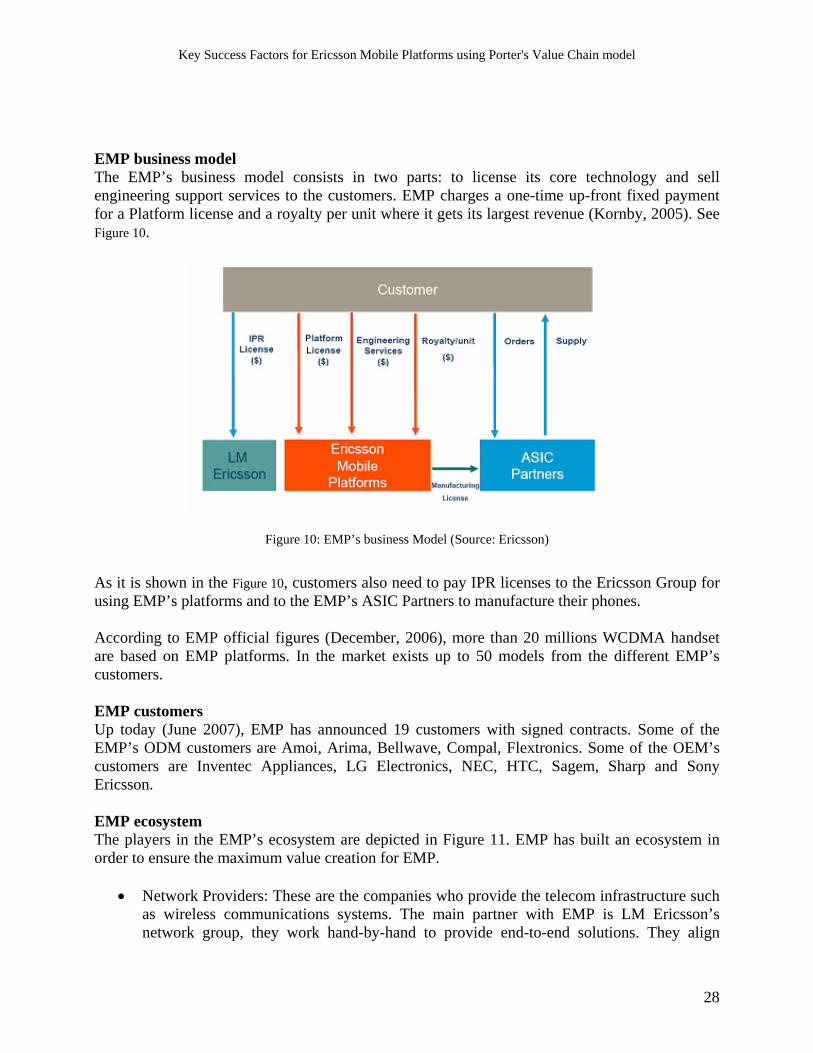

EMP business model The EMP’s business model consists in two parts: to license its core technology and sell engineering support services to the customers. EMP charges a one-time up-front fixed payment for a Platform license and a royalty per unit where it gets its largest revenue (Kornby, 2005). See Figure 10.

Figure 10: EMP’s business Model (Source: Ericsson)

As it is shown in the Figure 10, customers also need to pay IPR licenses to the Ericsson Group for using EMP’s platforms and to the EMP’s ASIC Partners to manufacture their phones. According to EMP official figures (December, 2006), more than 20 millions WCDMA handset are based on EMP platforms. In the market exists up to 50 models from the different EMP’s customers. EMP customers Up today (June 2007), EMP has announced 19 customers with signed contracts. Some of the EMP’s ODM customers are Amoi, Arima, Bellwave, Compal, Flextronics. Some of the OEM’s customers are Inventec Appliances, LG Electronics, NEC, HTC, Sagem, Sharp and Sony Ericsson. EMP ecosystem The players in the EMP’s ecosystem are depicted in Figure 11. EMP has built an ecosystem in order to ensure the maximum value creation for EMP.

• Network Providers: These are the companies who provide the telecom infrastructure such as wireless communications systems. The main partner with EMP is LM Ericsson’s network group, they work hand-by-hand to provide end-to-end solutions. They align

28

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

roadmaps and ensure that EMP platforms can support the new network functionality offered by Ericsson (Kornby, 2005).

• Customers: EMP has a closer relationship with the customers to ensure that new customer requirements are collected in right time in order to implement new functionality as early as possible.

• Network Operators: Operators are the ones who provide the services to the end-users (subscribers). They also purchase phones from mobile manufactures that are sold to the operators’ subscribers. Many times operators request to mobile manufacture to use a specific mobile platform (Kornby, 2005). Thus EMP has built an important relationship with them in order to understand future operators’ requirements to secure that new functionality is available in the EMP’s platform.

• Standardization Bodies: EMP and LM Ericsson are very active to work with the standardization bodies such as 3GPP, OMA, JCP and OMPT. This is done in order to ensure interoperability of EMP’s mobile platforms worldwide.

• Suppliers: EMP has a very active work towards ASIC, peripheral, IP and software suppliers in order to get fair prices for building EMP products.

Figure 11: EMP’s ecosystem (source: Ericsson, Dawidson and Karlsson, 2005)

4.2.1 The EMP’s Value Chain and Value System The EMP’s value chain and Value System are depicted in Figure 12. The direct activities of EMP’s value chain are: Supply Chain Management, Hardware design activity, Software development and integration activity, a system reference design activity, a System Test and Interoperability

29

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

Test (IOT), Product Use, External Networks and finally a customization activity. EMP has also a prototype unit which builds prototype phones for testing early functionality. Supply Chain Management EMP basically does not have any regular material flow, but it outsource software and hardware through licenses. The task of the sourcing and supply department is to act as an internal consultant at EMP for deciding whether to buy an IP or develop hardware/software in-house. The sourcing department works tightly with the product definition and the R&D organization; they work proactively to ensure fair prices. The decisions are based on three aspects: 1) cost, if it is cheaper to buy than develop it, 2) it assess the risk of buying and finally, 3) evaluate the total value by developing in-house. For example, for getting a new IP in the platform, the sourcing department evaluate the total cost that consist in: 1) cost of getting the IP from the supplier, 2) cost of using the IP (license) per ASIC (in this case customers pay the license directly, see Figure 10), 3) cost of integrating an IP into the suppliers’ ASIC (a supplier may have already the knowledge of adding this IP, thus it becomes cheaper) and finally 4) the cost of the final integration into the platform (how difficult is to make drivers and APIs to control the IP). The sourcing and supply department acts differently depending of what wants to outsource. For IPs, the negotiations are based on case, for ARM and DSP cores it builds long term relationship with the suppliers, and for a specific components such as Image Signal Processor (ISP) is chooses from the best price in the market. Since ASICs are costly, EMP co-develop the design with suppliers and builds long term relationship. Hardware design (HW) In this activity EMP only designs and specifies requirements for the different hardware components in the platform. As it is shown in the Figure 12, ASIC suppliers (or fabs, see Exhibit 2) are the ones who test and manufacture the hardware. EMP only does the verification of the hardware components when it builds the reference design. The design of the HW is divided into two main parts, Front-End and Back End design (see Exhibit 1). For the Radio Frequency (RF) hardware EMP does the Front-End and Back-End design. For the Digital Base Band (DBB) EMP only does the front-end design. Finally, the analog base band (ABB) ASIC, EMP only specifies the hardware requirements and leaves to the ASICs suppliers to do the rest.

30

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

Basic Concepts for designing Hardware Designing HW is very similar to designing SW, however, the languages and tools are different. The design process can be divided in two main parts:

• Front-End design: Here it is developed a high level description for the logic. This design process is independent of the target technology and it is programmed using VHDL (or Verilog). The first step is the logical synthesis. A tool produces Register Transfer Level (RTL) code from the VHDL description. The RTL code is a standardized description format for digital logic which is independent of vendor or technology.

• Back-End design: This is a target dependent technology. The elements available (e.g. multiplexers, gates, etc) for a specific silicon vendor (technology specific) are defined in the vendor cell library. This process involves the physical synthesis. Here it is mapped the RTL code to a technology specific representation using the vendor library. The next step is to position the elements in to the ASIC that defines the “layout view”. In this process is also involved simulation of the design to verify if the implementation is correct.

Note: Processors (CPUs) are the most performance demanding design. The processors are optimized independently and they are introduced in the Back-end design as a black box.

Exhibit 1: Basic concepts for designing Hardware.

The digital base band (DBB) ASIC is the most expensive device in the platform, consequently it determines the cost effectives of the platform offering. The cost of the DBB is based on several factors: Die size in mm2, (being the most important), Logic cores, CPUs and DSPs, Maturity of technology node, package and test time. Therefore, a high amount of the margin is transferred to the ASIC manufactures.

Software development and Integration This activity consist in developing software solutions for the different stacks in the software platform architecture described in section 4.2. This activity involves developing EMP (in-house) software stacks such as Network Signaling protocols for WCDMA, GSM/GPRS and EDGE; data communication protocols such as, TCP/IP, RTP, and IMS; multimedia protocols for streaming music and video; develop a set of application platform interfaces to control the software platform and hardware. Implementation of low level drivers to control hardware components inside the mobile platform like DBB, ABB, RF, peripheral, etc. This activity also involves the integration of third party proprietary software components such as, music codecs (like MP3 and Windows media player), operating systems, etc. This activity consist also in testing the software at different levels: module tests, regression tests and integration tests.

31

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

Reference design In this activity EMP builds reference boards and real-size reference phones. These non-commercial phone are produced in small quantities that are internally used for development of software and hardware verification, interoperability test and as first test of hardware for customers. System Test and Interoperability test The system test consist of the verification of the complete reference design. The tests are conducted in lab, with network vendors and interoperability test with major live networks operators in the world. This is a very costly task and it is done to uncover ambiguities in the basic standards and specification. It also covers informal type approval test for the phone (Kornby, 2005).

Customization This activity is the main interface between EMP and the customers. This activity is driven by the Customer Project Organization (CPO). A customer project consist of the following activities: delivery definition of the project, customization of the platform, integration and test, delivery, maintenance and support. Product Use In this activity EMP coordinates with customers about new customers’ requirements, it discusses technical matters about product development for the current projects and future platforms. It also includes meetings with customers for discussing and sharing new ideas that can be implemented in future products, and finally, if it is possible, customers and EMP shares roadmaps in order to build a common understanding of what is needed in the future. External Networks In this support activity EMP interacts with the different players in its ecosystem (see Figure 11). As it was described in section 4.2, EMP interacts with the network operators to take their requirements, which affect the software design (e.g. network signaling stack, multimedia protocols, etc, see Figure 8) or if there is some specific requirements that EMP needs to fulfill for the application suite in order to be compliant to changes in the markets demands. Finally, EMP keeps a close interaction with operators. EMP and operators perform IOT test with the EMP’s platforms in order to solve ambiguities in the standard and specifications. EMP participates actively with the different standardization bodies that affects the design of EMP’s platforms. The goal is to secure that EMP’s goes hand-by-hand with the development of new technology standards, such as HSPA and Long Term Evolution (LTE) access technologies. Finally, EMP has a strong collaboration with LM Ericsson. Both parties secure that EMP’s platforms can work in Ericsson Networks, an at the same time, LM Ericsson uses EMP’s handsets to test its new network functionality, for example, MBMS, IMS services, etc.

32

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

The Role of EMP’s Prototype Unit The EMP’s prototype unit was created in order to test and try new functionality in a phone-sized device. The prototype unit takes an EMP platform from the latest development stages of a release program (project) and adds new functionality (e.g. new access technologies such as LTE). The final product is used for testing the new functionality with Ericsson new network functionality. The goal of this unit is also to participate in public demonstrations and conferences such as 3GSM. A final goal is to give feedback and lessons learned of implementing new technology so EMP can have an easier developing process for making a cost-effective device.

What is a Foundry (Fab) company? “In the microelectronics industry, a foundry (also called a fab for fabrication plant) is a factory where devices like integrated circuits are manufactured. When the term "Foundry" is applied to a fab, it means that there are many devices being made at that fab for one or more customers. A fab that only has one product, or just one customer is generally not called a foundry.” (source: www.wikipedia.org, accessed 2007-05-20) What is a Fabless semiconductor company? A fabless semiconductor company specializes in the design and sale of hardware devices implemented on semiconductor chips. It achieves an advantage by outsourcing the fabrication of the devices to a specialized semiconductor manufacturer called a semiconductor foundry or "fab." A fabless company may concentrate its research and development resources on the end market without being required to invest resources in staying current in semiconductor technology. For this reason they are also known as IP firms, because their primary product consists of licenses in patents, trade secrets, mask works, and other forms of intellectual property. (source: www.wikipedia.org, accessed 2007-05-20)

Exhibit 2: Definitions from the semiconductor industry.

33

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

Figure 12: EMP’s Value Chain

34

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

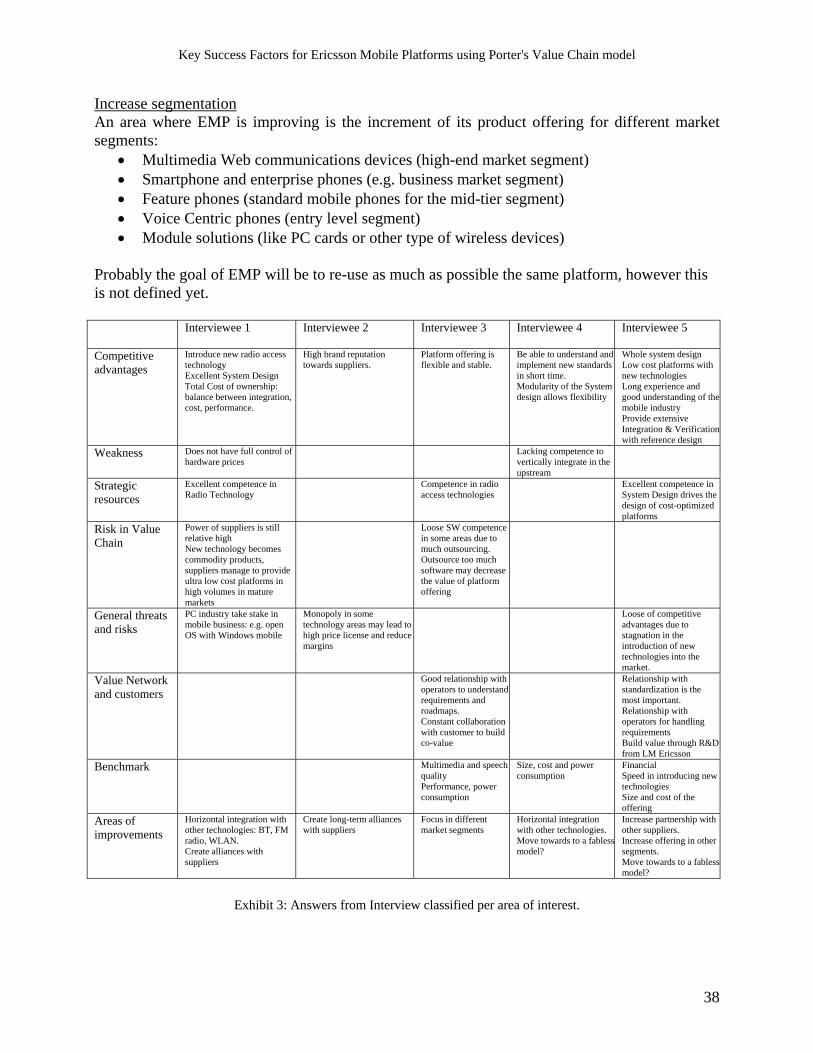

5 Analysis

5.1 Value Chain Analysis The aim of this section is to analyze the EMP’s value chain and evaluate the theoretical framework. The answers from the interviews are summarized and classified per area of interest in Exhibit 3. The analysis of the value chain is divided into eight areas: competitive advantages, weaknesses, strategic resources, risk in the value chain, general threats and risk, value networks and customers, benchmark and finally a discussion in areas of improvements. Competitive Advantages According to the theoretical framework a company can generate competitive advantages by analyzing the different activities in the value chain. EMP’s value chain basically works only in the service domain, that is, it licenses its platform solutions and let the customers to manage the manufacturing process with EMP’s suppliers, thus the EMP’s core activities are design (both in hardware and software), integration and testing of the platform (of the whole system). Integration is a complex task due to the huge amount of functionality that it is implemented in the platform. EMP’s advantage is that it has designed a holistic system architecture which it makes easy to develop and test independently the functionality, this saves considerable amount of time at the integration phase. Moreover, the system is designed to be flexible and scalable, so it is easy re-use and add new functionality. Therefore, EMP’s main strength is that it successfully manages to develop, integrate and test very complex new technologies to deliver a stable low cost-effective platform solution when technology development is not in a mature phase. This does not really means that EMP become first in the market; other competitors may offer the solution before EMP, but it is normally costly and not suitable for the mass market. EMP main competitive advantage is to be the leader in providing cost-effective solutions for the mass market when the new technologies are emerging. Another interested strength is that the brand image of Ericsson plays an important role when it comes to meet new suppliers. The reputation of Ericsson corporation is transferred to EMP and it facilitates the starting of new agreements and businesses. Weaknesses The value chain is an analysis tool that helps to find value in each activity, this can be also used for finding weakness and areas of improvements. From the value chain we can identify two main weaknesses. First, the base band ASICs are the most costly part in the platform, despite that EMP says that has managed to get fair licenses prices for the ASICs, still the power of the suppliers is relative high, thus EMP cannot have full control of the hardware prices. It seems that high margins still go to ASIC manufactures. Second, at this moment, EMP does not have the competence and the resources to vertically integrate in the upstream value chain. See “areas of improvement” for a more detailed discussion.

35

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model

Strategic Resources According to the interviewees, the most strategic resource at EMP resides on personnel’s competence in the area of radio access technology and in the skills for designing a flexible and low cost system. These two competences are the drivers for providing a cost-optimized mobile platforms. Risk in the Value Chain The main risks in the value chain comes from the supplier side. When technology reach a mature market, there is a risk that the technology become a commodity product and thus, suppliers can gain knowledge on how to implement these technologies in their own ASICs, this will imply that ASIC manufactures can produce ultra low cost platforms, due to they can control the price of the hardware. Another identified potential risk is the fact of how much EMP should outsource, as it is shown in the value chain (Figure 12), EMP outsource a number of software components. An indiscriminate software outsourcing may lead to loose some competences inside EMP value chain, such as signal processing knowledge1 and thus, reducing the value of the platform offering. General Threat and Risk Other players from other industries, like PC industry, may decide to enter the mobile platforms business. There is a threat that new players may take a stake in market share, for instance, by proving open OS phones like Windows Mobile operating systems. If customers start to demand to incorporate technologies in to the EMP platforms that are monopolized, this would increase the power of the suppliers and therefore increase the license cost of the platform. The greatest risk that it could happen is the stagnation of introducing new technologies in to the market. According to all the interviewees, one of the EMP’s competitive advantage is that is bringing constantly TTM cost-effective solutions of new technologies. If this development stops, EMP would be caught by its competitors and ultra low cost suppliers when the market reach maturity. Value Network and Customers The value-added chain framework introduces external networks and product use as new value activities in the value chain. As it can be seen this activities do add value for EMP. According to the interviewees, it is extremely important that EMP has a good relationship with the customers. EMP interacts constantly with the customers for discussing technical issues, future requirements and feedback. For EMP is important to have a close relationship with the operators, since they are the ones who rollout and enable new functionalities in the network infrastructure (such as Video Telephony).

1 Digital signal processing is used to develop algorithms that can for instance, enhance speech quality in voice call. Echo cancellers and noise suppressor are examples of speech processing algorithms. If EMP starts to outsource to much in this area it may finally loose this competence and become completely dependent on external suppliers.

36

Key Success Factors for Ericsson Mobile Platforms using Porter's Value Chain model