Blame the northeast for low natural gas prices

25

Blame the Northeast for Low Natural Gas Prices Bloomberg Intelligence Vincent Piazza and Gurpal Dosanjh Analysts

-

Upload

bloomberg-lp -

Category

Economy & Finance

-

view

33 -

download

0

Transcript of Blame the northeast for low natural gas prices

Blame the Northeast forLow Natural Gas Prices

Bloomberg IntelligenceVincent Piazza and Gurpal Dosanjh

Analysts

The secular growth in hydrocarbon output from the prolific Northeast collides with the cyclical, seasonal demand for natural gas -- yielding a structural imbalance.

While the imbalance will narrow and prices should improve over time, volume should continue to challenge the pace of infrastructure build out, continuing to pressure basis differentials in a market that once was a premium priced region.

Northeast gas boom may hurt prices nationwide through 2017

Prodigious production of natural gas and liquids such as ethane and propane in the U.S. Northeast will keep pressure on gathering, processing and transportation infrastructure into 2017, even amid a steady expansion of capacity.

Prices in the region may be depressed by these bottlenecks, and other hubs will also be affected as Marcellus and Utica production displaces natural gas transported to the northeast. Incremental output flowing to the southeast and midwest will compete with gas produced in those areas.

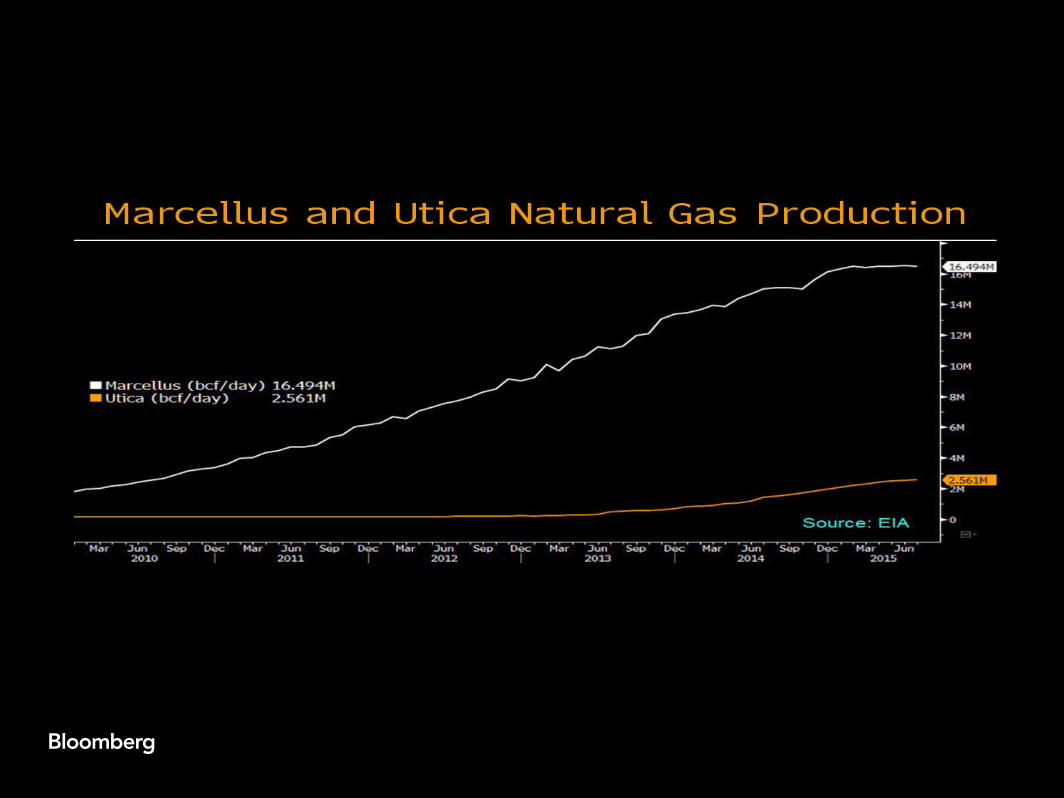

Marcellus, Utica gas output will displace other regions’ volumes

Natural gas volume growth in the U.S. Northeast is likely to slow through 2017 as production rises faster than pipeline capacity, pressuring price differentials across the region. Operators have sought out new markets to absorb the excess volume, helping to dilute seasonal supply and demand imbalances and boost prices.

A reversal of typical Northeast flow will hurt basis prices across the U.S. in the long term. Marcellus and Utica output may surpass 19 billion cubic feet a day in September, about 25% of U.S. volume.

Marcellus output growth will slow from historical highs, yet volume will remain robust and likely continue to outrun pipeline capacity. Growth in the Utica is also pipeline-constrained. Range, Cabot, EQT, Exxon Mobil, Chevron, Southwestern and Chesapeake are significant producers in the region.

Plethora of Northeast gas pressures other markets into 2017

The price spread between cheap Northeast U.S. natural gas and more expensive Henry Hub gas will stay wide through at least 2017, when additional pipeline capacity comes online. The Northeast, historically a region with premium pricing that imports gas during high seasonal demand, is now more reliant on its own lower-cost output. However, limited intermittent takeaway capacity has reduced prices.

With more takeaway, its gas will find new markets and differentials may improve while prices elsewhere are pressured.

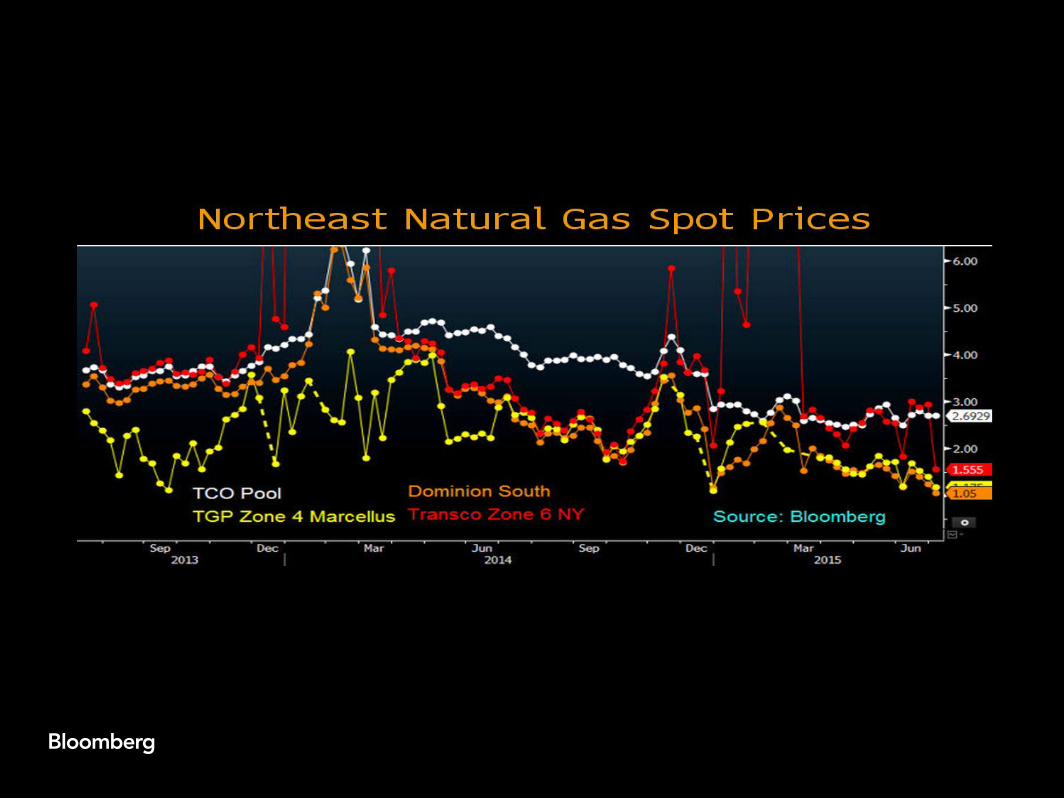

Northeast U.S. gas pipeline additions may affect regional prices

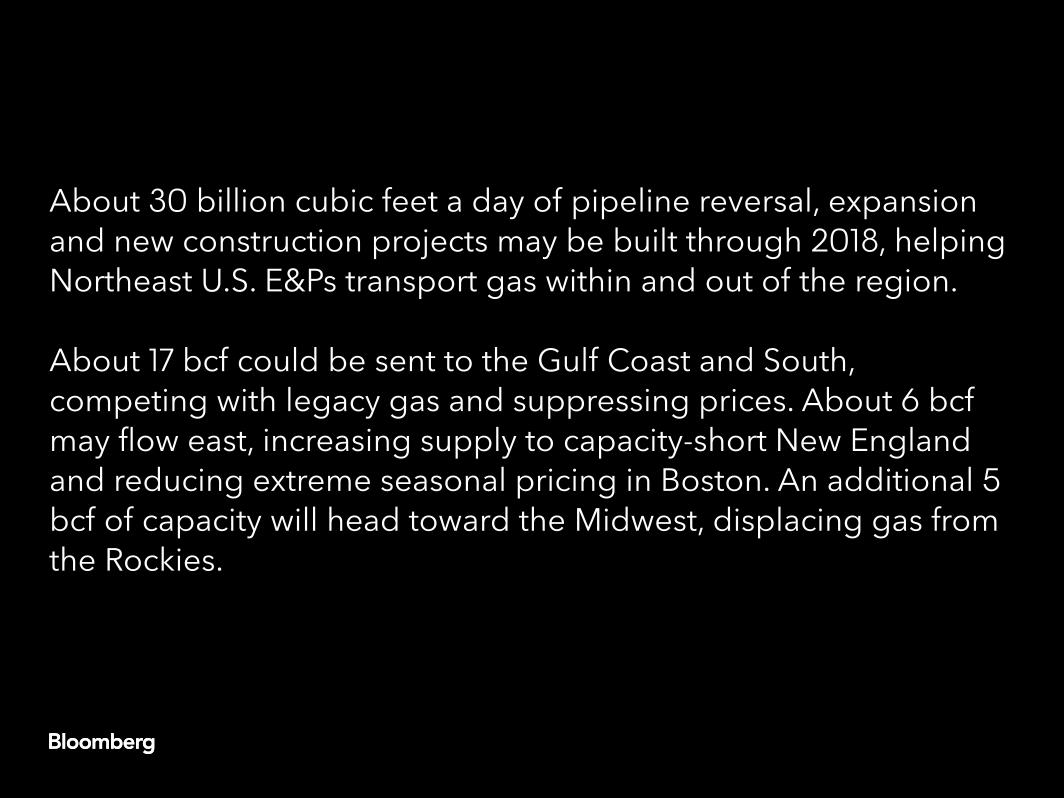

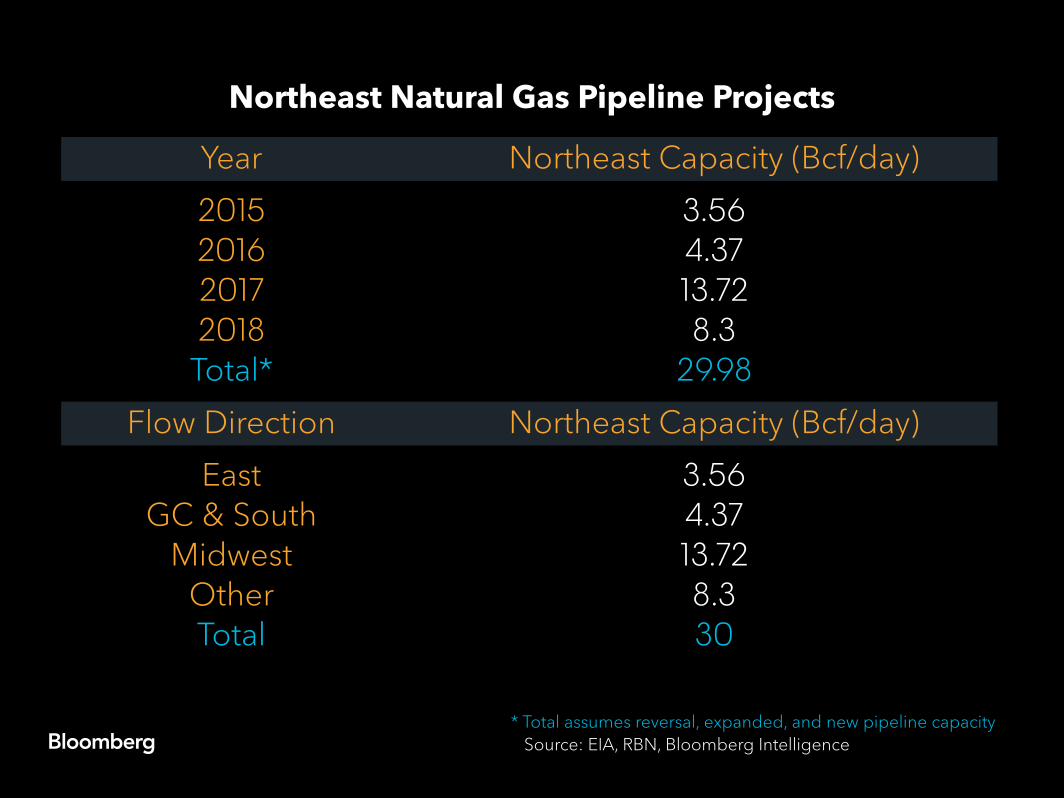

About 30 billion cubic feet a day of pipeline reversal, expansion and new construction projects may be built through 2018, helping Northeast U.S. E&Ps transport gas within and out of the region.

About 17 bcf could be sent to the Gulf Coast and South, competing with legacy gas and suppressing prices. About 6 bcf may flow east, increasing supply to capacity-short New England and reducing extreme seasonal pricing in Boston. An additional 5 bcf of capacity will head toward the Midwest, displacing gas from the Rockies.

Expanded pipeline infrastructure should ease bottlenecks in the Marcellus and Utica plays for producers with natural gas exposure such as Range Resources, Cabot, EQT, Southwestern, Hess, Anadarko and Chesapeake Energy. Added capacity should also help ease wide Northeast pricing differentials.

Northeast Natural Gas Pipeline Projects

Year

Flow Direction

* Total assumes reversal, expanded, and new pipeline capacitySource: EIA, RBN, Bloomberg Intelligence

2015201620172018Total*

EastGC & South

MidwestOtherTotal

Northeast Capacity (Bcf/day)

Northeast Capacity (Bcf/day)

3.564.3713.728.3

29.98

3.564.3713.728.330

NGL price pressure to remain as Northeast adds to oversupply

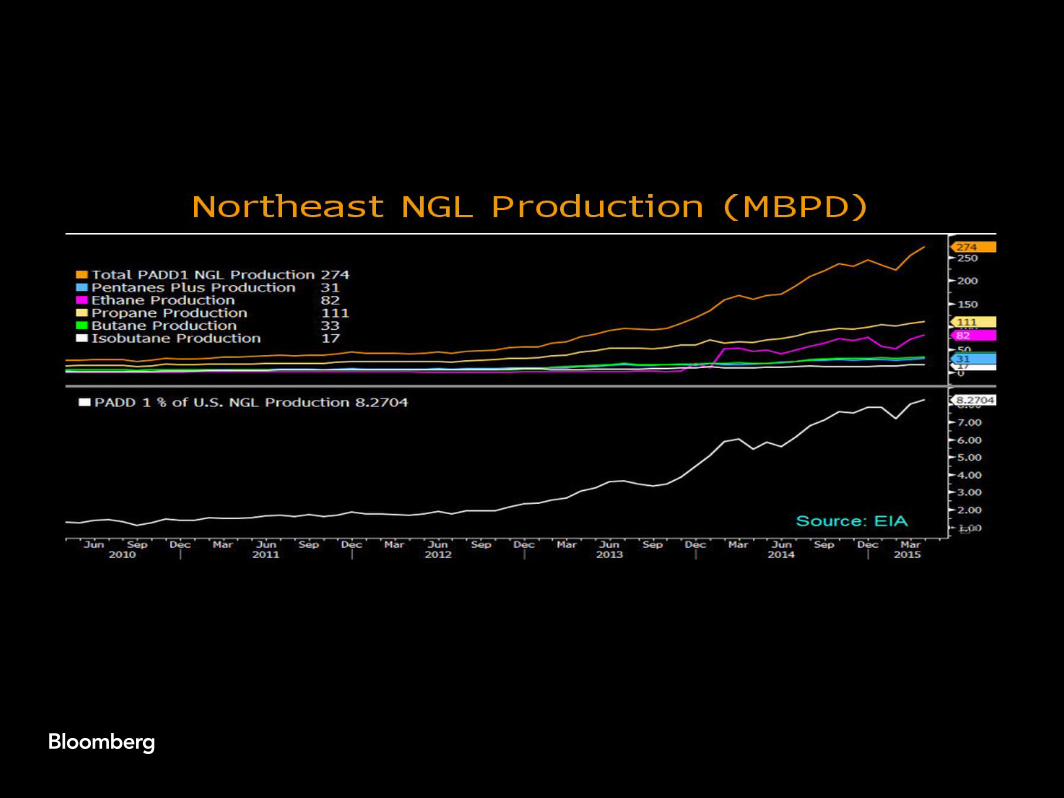

The Marcellus output glut that’s straining infrastructure is also depressing prices of natural gas liquids. NGL supply has surged 12-fold in the past five years.

While output growth will be more subdued, demand will lag behind rising volume, forcing producers to leave ethane, the largest NGL component, in the gas stream. Projects such as Mariner East and West will allow ethane exports from the Northeast U.S. While Enterprise’s propane connector will join East and West Coast flows, domestic oversupply will remain.

Natural gas liquids, also referred to as “wet gas,” may be extracted from a well’s hydrocarbon stream. Range Resources, Chesapeake, Gulfport, Chevron, Hess and EQT have exposure to Northeast plays such as the Marcellus and Utica that have wet gas, condensate and dry gas windows.

Natural gas, NGL flows rebalance, yet weak prices will persist

Abundant natural gas liquids from the three key U.S. oil plays, along with stout natural gas volume from the Northeast, will maintain pressure on regional gas and NGL prices even with potential export demand. Volume will converge along the Gulf Coast and Southeast as flows rebalance.

Associated gas from the main oil plays accounts for about 20% of total domestic output, while Northeast gas makes up 25%. Less drilling will narrow the supply and demand imbalance, though expected demand may weaken if exports don’t materialize.

Gas and NGL prices will remain depressed in the long term given the output glut balanced against demand. Export potential may narrow imbalances as well as less liquids drilling. Exxon Mobil, Range, Southwestern, Chesapeake, Devon, Anadarko and EOG Resources are large companies with gas exposure.

Spreading successful Utica tests don’t bode well for gas prices

Operators have successfully tested in the Utica across Ohio, West Virginia and Pennsylvania with varying levels of success. Drilling and completion methods in the play, which lies below the Marcellus, have extended the potential of the Appalachian Basin.

Should Utica operators lower their costs, the basin will be awash with cheaper natural gas. Similarly, the transition from exploration to full-scale development and exploitation of the Marcellus brought prolific output and lower unit costs.

Bloomberg Intelligence offers valuable insight and company data, interactive charting and written analysis with government, credit insights from a team of independent experts, giving trading and investment professionals deep insight into where crucial industries start today and where they may be heading next.