BLACKROCK FUNDS III BlackRock Cash Funds: Prime · BLACKROCK FUNDS III BlackRock Cash Funds: Prime...

91

BLACKROCK FUNDS III BlackRock Cash Funds: Prime (the “Fund”) Supplement dated February 23, 2017 to the Prospectuses, Summary Prospectuses and Statements of Additional Information each dated October 11, 2016 On February 23, 2017, the Board of Trustees of BlackRock Funds III (the “Trust”) approved a proposal to close the Fund to new purchases and thereafter to liquidate the Fund. Accordingly, effective 3:00 p.m. (Eastern time) on April 24, 2017, the Fund will no longer accept purchase orders. On or about April 28, 2017 (the “Liquidation Date”), all of the assets of the Fund will be liquidated completely, the shares of any shareholders holding shares on the Liquidation Date will be redeemed at the 3:00 p.m. (Eastern time) net asset value per share and the Fund will then be terminated as a series of the Trust. Shareholders may redeem their Fund shares or exchange their shares into an appropriate class of shares of another money market fund advised by BlackRock Advisors, LLC or its affiliates, at any time prior to the Liquidation Date. The Fund may not achieve its investment objective as the Liquidation Date approaches. Shareholders should consult their personal tax advisers concerning their tax situation and the impact of the liquidation or exchanging to a different fund on their tax situation. Shareholders should retain this Supplement for future reference. PR2SAI-CFPRI-0217SUP

-

Upload

truongduong -

Category

Documents

-

view

242 -

download

4

Transcript of BLACKROCK FUNDS III BlackRock Cash Funds: Prime · BLACKROCK FUNDS III BlackRock Cash Funds: Prime...

BLACKROCK FUNDS IIIBlackRock Cash Funds: Prime

(the “Fund”)

Supplement dated February 23, 2017 to theProspectuses, Summary Prospectuses and Statements of Additional Information

each dated October 11, 2016

On February 23, 2017, the Board of Trustees of BlackRock Funds III (the “Trust”) approved a proposal toclose the Fund to new purchases and thereafter to liquidate the Fund.

Accordingly, effective 3:00 p.m. (Eastern time) on April 24, 2017, the Fund will no longer accept purchaseorders. On or about April 28, 2017 (the “Liquidation Date”), all of the assets of the Fund will be liquidatedcompletely, the shares of any shareholders holding shares on the Liquidation Date will be redeemed at the3:00 p.m. (Eastern time) net asset value per share and the Fund will then be terminated as a series of the Trust.

Shareholders may redeem their Fund shares or exchange their shares into an appropriate class of shares ofanother money market fund advised by BlackRock Advisors, LLC or its affiliates, at any time prior to theLiquidation Date. The Fund may not achieve its investment objective as the Liquidation Date approaches.

Shareholders should consult their personal tax advisers concerning their tax situation and the impact of theliquidation or exchanging to a different fund on their tax situation.

Shareholders should retain this Supplement for future reference.

PR2SAI-CFPRI-0217SUP

BBIF Money Fund

BBIF Treasury Fund

BIF Money Fund

BIF Treasury Fund

BlackRock Allocation Target SharesBATS: Series A PortfolioBATS: Series C PortfolioBATS: Series E PortfolioBATS: Series M PortfolioBATS: Series P PortfolioBATS: Series S Portfolio

BlackRock Balanced Capital Fund, Inc.

BlackRock Basic Value Fund, Inc.

BlackRock Bond Fund, Inc.BlackRock Total Return Fund

BlackRock California Municipal Series TrustBlackRock California Municipal OpportunitiesFund

BlackRock Capital Appreciation Fund, Inc.

BlackRock CoRI FundsBlackRock CoRI 2015 FundBlackRock CoRI 2017 FundBlackRock CoRI 2019 FundBlackRock CoRI 2021 FundBlackRock CoRI 2023 Fund

BlackRock Emerging Markets Fund, Inc.

BlackRock Equity Dividend Fund

BlackRock EuroFund

BlackRock Financial Institutions Series TrustBlackRock Summit Cash Reserves Fund

BlackRock Focus Growth Fund, Inc.

BlackRock FundsSM

BlackRock All-Cap Energy & ResourcesPortfolioBlackRock Alternative Capital Strategies FundBlackRock Commodity Strategies FundBlackRock Developed Real Estate Index FundBlackRock Disciplined Small Cap Core FundBlackRock Emerging Markets Dividend FundBlackRock Emerging Markets Equity StrategiesFund

BlackRock Emerging Markets Long/ShortEquity FundBlackRock Energy & Resources PortfolioBlackRock Exchange PortfolioBlackRock Flexible Equity FundBlackRock Global Long/Short Credit FundBlackRock Global Long/Short Equity FundBlackRock Global Opportunities PortfolioBlackRock Health Sciences OpportunitiesPortfolioBlackRock Impact Bond FundBlackRock Impact U.S. Equity FundBlackRock International Opportunities PortfolioBlackRock Mid-Cap Growth Equity PortfolioBlackRock Midcap Index FundBlackRock Min Vol EAFE Index FundBlackRock Min Vol USA Index FundBlackRock Money Market PortfolioBlackRock MSCI Asia ex Japan Index FundBlackRock MSCI World Index FundBlackRock Multifactor International Index FundBlackRock Multifactor USA Index FundBlackRock Multi-Manager AlternativeStrategies FundBlackRock Real Estate Securities FundBlackRock Science & TechnologyOpportunities PortfolioBlackRock Short Obligations FundBlackRock Short-Term Inflation-ProtectedSecurities Index FundBlackRock Small Cap Growth Equity PortfolioBlackRock Small/Mid Cap Index FundBlackRock Tactical Opportunities FundBlackRock Total Emerging Markets FundBlackRock Total Stock Market Index FundBlackRock USA Momentum Factor Index FundBlackRock USA Quality Factor Index FundBlackRock USA Size Factor Index FundBlackRock USA Value Factor Index FundBlackRock U.S. Opportunities Portfolio

BlackRock Funds IIBlackRock 20/80 Target Allocation FundBlackRock 40/60 Target Allocation FundBlackRock 60/40 Target Allocation FundBlackRock 80/20 Target Allocation FundBlackRock Core Bond PortfolioBlackRock Credit Strategies Income FundBlackRock Dynamic High Income PortfolioBlackRock Emerging Markets FlexibleDynamic Bond PortfolioBlackRock Floating Rate Income PortfolioBlackRock Global Dividend PortfolioBlack GNMA PortfolioBlackRock High Yield Bond Portfolio

BlackRock Inflation Protected Bond PortfolioBlackRock LifePath® Smart Beta 2020 FundBlackRock LifePath® Smart Beta 2025 FundBlackRock LifePath® Smart Beta 2030 FundBlackRock LifePath® Smart Beta 2035 FundBlackRock LifePath® Smart Beta 2040 FundBlackRock LifePath® Smart Beta 2045 FundBlackRock LifePath® Smart Beta 2050 FundBlackRock LifePath® Smart Beta 2055 FundBlackRock LifePath® Smart Beta RetirementFundBlackRock Low Duration Bond PortfolioBlackRock Managed Income FundBlackRock Multi-Asset Income PortfolioBlackRock Strategic Income OpportunitiesPortfolioBlackRock U.S. Government Bond Portfolio

BlackRock Funds IIIBlackRock Cash Funds: InstitutionalBlackRock Cash Funds: PrimeBlackRock Cash Funds: TreasuryBlackRock CoreAlpha Bond FundBlackRock Disciplined International FundBlackRock Large Cap Index FundBlackRock LifePath® Dynamic RetirementFundBlackRock LifePath® Dynamic 2020 FundBlackRock LifePath® Dynamic 2025 FundBlackRock LifePath® Dynamic 2030 FundBlackRock LifePath® Dynamic 2035 FundBlackRock LifePath® Dynamic 2040 FundBlackRock LifePath® Dynamic 2045 FundBlackRock LifePath® Dynamic 2050 FundBlackRock LifePath® Dynamic 2055 FundBlackRock LifePath® Index Retirement FundBlackRock LifePath® Index 2020 FundBlackRock LifePath® Index 2025 FundBlackRock LifePath® Index 2030 FundBlackRock LifePath® Index 2035 FundBlackRock LifePath® Index 2040 FundBlackRock LifePath® Index 2045 FundBlackRock LifePath® Index 2050 FundBlackRock LifePath® Index 2055 FundBlackRock LifePath® Index 2060 FundBlackRock S&P 500 Index FundBlackRock Total International ex U.S. IndexFundBlackRock U.S. Total Bond Index Fund

BlackRock Global Allocation Fund, Inc.

BlackRock Global SmallCap Fund, Inc.

BlackRock Index Funds, Inc.BlackRock International Index FundBlackRock Small Cap Index Fund

BlackRock Large Cap Series Funds, Inc.BlackRock Event Driven Equity FundBlackRock Large Cap Core FundBlackRock Large Cap Growth FundBlackRock Large Cap Value FundBlackRock Large Cap Value RetirementPortfolio

BlackRock Latin America Fund, Inc.

BlackRock Liquidity FundsCalifornia Money FundFederal Trust FundFedFundMuniCashMuniFundNew York Money FundTempCashTempFundT-FundTreasury Trust Fund

BlackRock Long-Horizon Equity Fund

BlackRock Mid Cap Value Opportunities Series,Inc.

BlackRock Mid Cap Value Opportunities Fund

BlackRock Multi-State Municipal Series TrustBlackRock New Jersey Municipal Bond FundBlackRock New York Municipal OpportunitiesFundBlackRock Pennsylvania Municipal Bond Fund

BlackRock Municipal Bond Fund, Inc.BlackRock High Yield Municipal FundBlackRock National Municipal FundBlackRock Short-Term Municipal Fund

BlackRock Municipal Series TrustBlackRock Strategic Municipal OpportunitiesFund

BlackRock Natural Resources Trust

BlackRock Pacific Fund, Inc.

BlackRock Series Fund, Inc.BlackRock Balanced Capital PortfolioBlackRock Capital Appreciation Portfolio

- 2 -

BlackRock Global Allocation PortfolioBlackRock Government Money MarketPortfolioBlackRock High Yield PortfolioBlackRock Large Cap Core PortfolioBlackRock Total Return PortfolioBlackRock U.S. Government Bond Portfolio

BlackRock Series, Inc.BlackRock International FundBlackRock Small Cap Growth Fund II

BlackRock Strategic Global Bond Fund, Inc.

BlackRock Value Opportunities Fund, Inc.

BlackRock Variable Series Funds, Inc.BlackRock Basic Value V.I. FundBlackRock Capital Appreciation V.I. FundBlackRock Equity Dividend V.I. FundBlackRock Global Allocation V.I. FundBlackRock Global Opportunities V.I. FundBlackRock Government Money Market V.I.FundBlackRock High Yield V.I. FundBlackRock International V.I. FundBlackRock iShares® Alternative Strategies V.I.FundBlackRock iShares® Dynamic Allocation V.I.FundBlackRock iShares® Dynamic Fixed IncomeV.I. FundBlackRock iShares® Equity Appreciation V.I.FundBlackRock Large Cap Core V.I. FundBlackRock Large Cap Growth V.I. FundBlackRock Large Cap Value V.I. Fund

BlackRock Managed Volatility V.I. FundBlackRock S&P 500 Index V.I. FundBlackRock Total Return V.I. FundBlackRock U.S. Government Bond V.I. FundBlackRock Value Opportunities V.I. Fund

FDP Series, Inc.FDP BlackRock Franklin Templeton TotalReturn FundFDP BlackRock Invesco Value FundFDP BlackRock Janus Growth FundFDP BlackRock MFS Research InternationalFund

Funds For Institutions SeriesBlackRock Premier Government InstitutionalFundBlackRock Select Treasury StrategiesInstitutional FundBlackRock Treasury Strategies InstitutionalFundFFI Government FundFFI Treasury Fund

Managed Account SeriesBlackRock U.S. Mortgage PortfolioGlobal SmallCap PortfolioMid Cap Value Opportunities Portfolio

Ready Assets Government Liquidity Fund

Ready Assets U.S.A. Government Money Fund

Ready Assets U.S. Treasury Money Fund

Retirement Series TrustRetirement Reserves Money Fund

(each, a “Fund” and collectively, the “Funds”)

Supplement dated February 6, 2017 to the Statement of Additional Information of each Fund

Each Fund’s Statement of Additional Information is amended as follows:

The list in the section entitled “Purchase of Shares — Additional Payments by BlackRock — C. ServiceOrganizations Receiving Additional Payments”, “Miscellaneous — Additional Payments by BlackRock —C. Service Organizations Receiving Additional Payments”, “Investment Advisory Arrangements —Additional Payments by BlackRock — C. Service Organizations Receiving Additional Payments” or“Investment Adviser and Other Service Providers — Additional Payments by BlackRock — C. ServiceOrganizations Receiving Additional Payments” in Part II, as applicable, of each Fund’s current Statementof Additional Information is deleted in its entirety and replaced with the following:

Access Control AdvantageAccuTech Systems CorporationADP Broker-Dealer, Inc.

AIG Advisor Group, Inc.Allianz Life Financial Services, LLCAllianz Life Insurance Company of New York

- 3 -

Allianz Life Insurance Company of North AmericaAmerican Enterprise Investment Services, Inc.American Fidelity Assurance CompanyAmerican Fidelity Securities, Inc.American General Life Insurance CompanyAmerican United Life Insurance CompanyAnnuity Investors Life Insurance CompanyAon HewittAscensus Broker Dealer Services, Inc.Ascensus, Inc.AssetMark Trust CompanyAXA Advisors, LLCAXA Equitable Life Insurance CompanyBank of America, N.A.Bank of New York Mellon, TheBarclays Capital Inc.BB&T Retirement & Institutional ServicesBenefit Plans Administrative Services, Inc.Benefit Trust CompanyBlackRock Advisors, LLCBMO Capital Markets Corp.BMO Harris BankBNP Paribas Investment Partners UK LimitedBNY Mellon, N.A.BOKF, N.A.Broadridge Business Process Outsourcing, LLCBrown Brothers Harriman & Co.Capital One, N.A.Cetera Advisor Networks LLCCetera Advisors LLCCetera Financial GroupCetera Financial Specialists LLCCetera Investment Services LLCCharles Schwab & Co., Inc.Chicago Deferred Exchange Company LLCChicago Mercantile Exchange Inc.CitiBank, National AssociationCitigroup Global Markets, Inc.Citizens Business BankCME Shareholder Servicing LLCCMFG Life Insurance CompanyComerica BankComerica Securities, Inc.Commonfund Securities Inc.Commonwealth Financial NetworkCompanion Life Insurance CompanyComputershare Trust CompanyCredit Suisse First BostonCredit Suisse Securities (USA) LLCCSC Trust Company of DelawareDelaware Life Insurance CompanyDelaware Life Insurance Company of New York

Deutsche Bank AGDeutsche Bank Securities Inc.Deutsche Bank Trust Company AmericasDigital Retirement Solutions, Inc.Edward D. Jones & Co., L.P.Empire Fidelity Investments Life Insurance

CompanyExpertPlan, Inc.Federal Deposit Insurance CorporationFidelity Brokerage Services LLCFidelity Investments Institutional Operations

Company, Inc.Fidelity Investments Life Insurance CompanyFifth Third Securities, Inc.First Allied Securities, Inc.First Clearing, LLCFirst Hawaiian BankFirst Mercantile Trust CompanyFirst MetLife Investors Insurance CompanyFirst Security Benefit Life Insurance and Annuity

Company of New YorkFirst Symetra National Life Insurance Company of

New YorkFIS Brokerage & Securities Services LLCForethought Life Insurance CompanyFSC Securities CorporationGenworth Life and Annuity Insurance CompanyGenworth Life Insurance Company of New YorkGirard Securities, Inc.Global Atlantic Distributors, LLCGoldman Sachs & Co.Great-West Financial Retirement Plan Services, LLCGreat-West Life & Annuity Insurance CompanyGreat-West Life & Annuity Insurance Company of

New YorkGuardian Insurance & Annuity Company, Inc., TheGWFS Equities, Inc.Hartford Life and Annuity Insurance CompanyHartford Life Insurance CompanyHartford Securities Distribution Company, Inc.Hazeltree Fund Services, Inc.Hightower Securities, Inc.Hilltop Securities Inc.HSBC Bank USA, N.A.Huntington Investment Company, TheInstitutional Cash Distributors, LLCIntegrity Life Insurance CompanyINVEST Financial CorporationInvestment Centers of America, Inc.Investors Capital CorporationJ.P. Morgan Securities LLCJefferies LLC

- 4 -

Jefferson National Life Insurance CompanyJefferson National Life Insurance Company of New

YorkJohn Hancock Life Insurance CompanyJohn Hancock Life Insurance Company of New YorkJPMorgan Chase Bank, N.A.KeyBanc Capital Markets Inc.KeyBank, N.A.Ladenburg Thalmann Advisor Network LLCLegend Equities CorporationLincoln Financial Advisors CorporationLincoln Financial Distributors, Inc.Lincoln Financial Securities CorporationLincoln Life & Annuity Company of New YorkLincoln National Life Insurance CompanyLincoln Retirement Services LLCLPL Financial LLCM&T Securities Inc.Manufacturers and Traders Trust CompanyMassachusetts Mutual Life Insurance CompanyMembers Life Insurance CompanyMercer HR Services, LLCMerrill Lynch, Pierce, Fenner & Smith IncorporatedMetavante CorporationMetLife Insurance Company USAMetropolitan Life Insurance CompanyMid Atlantic Capital CorporationMidland Life Insurance CompanyMinnesota Life Insurance CompanyMizuho Securities USA Inc.MML Distributors, LLCMML Investors Services, LLCMorgan Stanley & Co. LLCMorgan Stanley Smith Barney LLCMSI Financial Services, Inc.MUFG Union Bank, National AssociationMy Treasury LimitedNational Financial Services LLCNational Integrity Life Insurance CompanyNational Life Insurance CompanyNational Planning CorporationNational Planning Holdings, Inc.Nationwide Financial Services, Inc.Nationwide Fund Distributors LLCNationwide Retirement SolutionsNCB Federal Savings BankNew England Pension Plan Systems, LLCNew York Life Insurance and Annuity CorporationNewport Retirement Services, Inc.Northbrook Bank & Trust CompanyNorthwestern Mutual Investment Services, LLCNYLife Distributors LLC

Pacific Life & Annuity CompanyPacific Life Insurance CompanyPacific Select Distributors, Inc.Park Avenue Securities LLCPershing LLCPFPC Inc.PFS Investments Inc.Piper Jaffray & Co.PNC Bank, National AssociationPNC Capital Markets LLCPNC Investments LLCPrimerica Shareholder Services, Inc.Principal Life Insurance CompanyPruco Life Insurance CompanyPruco Life Insurance Company of New JerseyPrudential Annuities Distributors, Inc.Prudential Insurance Company of AmericaPurshe Kaplan Sterling InvestmentsRaymond James & Associates, Inc.RBC Capital Markets, LLCRegions BankReliance Trust CompanyReliastar Life Insurance CompanyReliastar Lire Life Insurance Company of New YorkRiverSource Distributors, Inc.RiverSource Life Insurance Co. of New YorkRiverSource Life Insurance CompanyRobert W Baird & Co IncorporatedRoyal Alliance Associates, Inc.SagePoint Financial, Inc.Sammons Retirement Solutions, Inc.Saturna Trust CompanySecurity Benefit Life Insurance CompanySecurity Financial Resources, Inc.Security Life of Denver Insurance CompanySEI Private Trust CompanySG Americas Securities, LLCSI Trust ServicingSII Investments, Inc.Standard Insurance CompanyState Farm VP Management Corp.State Street Global Markets, LLCStifel, Nicolaus & Company, IncorporatedSummit Brokerage Services, Inc.SunTrust BankSVB Asset ManagementSymetra Life Insurance CompanySyntal Capital Partners, LLCT. Rowe Price Retirement Plan Services, Inc.TD Ameritrade Clearing, Inc.TD Ameritrade Trust CompanyTD Ameritrade, Inc.

- 5 -

Teachers Insurance and Annuity Association ofAmerica

TIAA-CREF Tuition Financing, Inc.Transamerica Advisors Life Insurance CompanyTransamerica Financial Life Insurance CompanyTreasury BrokerageTrust Company of AmericaTrust Management NetworkU.S. Bancorp Investments, Inc.U.S. Bank, National AssociationUBATCO & Co.UBS AGUBS Financial Services, Inc.UBS Securities LLCUMB Bank, National AssociationUnited of Omaha Life Insurance CompanyUnited States Life Insurance Company in the City of

New York, TheVALIC Retirement Services Company

Vanguard Group, Inc., TheVanguard Marketing CorporationVoya Financial Advisors, Inc.Voya Financial Partners, LLCVoya Institutional Plan Services, LLCVoya Insurance and Annuity CompanyVoya Investments Distributor, LLCVoya Retirement Insurance and Annuity CompanyVSR Financial Services, Inc.Wells Fargo Advisors, LLCWells Fargo Bank, N.A.Wells Fargo Investments, LLCWells Fargo Securities, LLCWilmington Trust Retirement and Institutional

ServicesWilmington Trust, National AssociationWoodbury Financial Services, Inc.Xerox HR Solutions, LLCZB, National Association

Shareholders should retain this Supplement for future reference.

SAI-GLOBAL-0217SUP

- 6 -

BLACKROCK FUNDS IIIBlackRock Cash Funds: Institutional

BlackRock Cash Funds: PrimeBlackRock Cash Funds: Treasury

(each a “Fund,” and collectively, the “Funds”)

Supplement dated December 22, 2016 to theStatements of Additional Information of the Funds dated October 11, 2016

The Funds have received an order from the Securities and Exchange Commission (the “Order”) grantingexemptions from certain provisions of the Investment Company Act of 1940, as amended, and rules thereunder,including a provision requiring that certain borrowings be made only from banks. Pursuant to the Order, theFunds may participate in an interfund lending program (the “Interfund Lending Program”) under which eachFund may lend money directly to and borrow money directly from certain other open-end BlackRock funds,including the Funds, for temporary purposes, to the extent consistent with its investment objectives, restrictions,policies, limitations and organizational documents, and subject to the conditions of the Order.

Effective immediately, the Funds’ Statements of Additional Information are amended to add the followingas a new subsection under “Investment Risks”:

Interfund Lending Program. Pursuant to an exemptive order granted by the SEC (the “IFL Order”), an open-endBlackRock fund (referred to as a “BlackRock fund” in this subsection), including a Fund, to the extent permittedby its investment policies and restrictions and subject to meeting the conditions of the IFL Order, has the abilityto lend money to, and borrow money from, other BlackRock funds pursuant to a master interfund lendingagreement (the “Interfund Lending Program”). Under the Interfund Lending Program, BlackRock funds may lendor borrow money for temporary purposes directly to or from other BlackRock funds (an “Interfund Loan”). AllInterfund Loans would consist only of uninvested cash reserves that the lending BlackRock fund otherwisewould invest in short-term repurchase agreements or other short-term instruments. Although the Funds may, tothe extent permitted by their investment policies, participate in the Interfund Lending Program as borrowers orlenders, they typically will not need to participate as borrowers because the Funds are money market funds andare required to comply with the liquidity provisions of Rule 2a-7 under the 1940 Act.

If a BlackRock fund has outstanding bank borrowings, any Interfund Loans to such BlackRock fund would:(a) be at an interest rate equal to or lower than that of any outstanding bank loan, (b) be secured at least on anequal priority basis with at least an equivalent percentage of collateral to loan value as any outstanding bank loanthat requires collateral, (c) have a maturity no longer than any outstanding bank loan (and in any event not overseven days), and (d) provide that, if an event of default occurs under any agreement evidencing an outstandingbank loan to the BlackRock fund, that event of default will automatically (without need for action or notice bythe lending BlackRock fund) constitute an immediate event of default under the interfund lending agreement,entitling the lending BlackRock fund to call the Interfund Loan immediately (and exercise all rights with respectto any collateral), and cause such call to be made if the lending bank exercises its right to call its loan under itsagreement with the borrowing BlackRock fund.

A BlackRock fund may borrow on an unsecured basis through the Interfund Lending Program only if itsoutstanding borrowings from all sources immediately after the borrowing total 10% or less of its total assets,provided that if the BlackRock fund has a secured loan outstanding from any other lender, including but notlimited to another BlackRock fund, the borrowing BlackRock fund’s borrowing will be secured on at least anequal priority basis with at least an equivalent percentage of collateral to loan value as any outstanding loan thatrequires collateral. If a borrowing BlackRock fund’s total outstanding borrowings immediately after an InterfundLoan under the Interfund Lending Program exceed 10% of its total assets, the BlackRock fund may borrowthrough the Interfund Lending Program on a secured basis only. A BlackRock fund may not borrow under theInterfund Lending Program or from any other source if its total outstanding borrowings immediately after theborrowing would be more than 33 1/3% of its total assets or any lower threshold provided for by the BlackRockfund’s investment restrictions.

No BlackRock fund may lend to another BlackRock fund through the Interfund Lending Program if the loanwould cause the lending BlackRock fund’s aggregate outstanding loans through the Interfund Lending Programto exceed 15% of its current net assets at the time of the loan. A BlackRock fund’s Interfund Loans to any oneBlackRock fund shall not exceed 5% of the lending BlackRock fund’s net assets. The duration of InterfundLoans will be limited to the time required to receive payment for securities sold, but in no event more than sevendays, and for purposes of this condition, loans effected within seven days of each other will be treated as separateloan transactions. Each Interfund Loan may be called on one business day’s notice by a lending BlackRock fundand may be repaid on any day by a borrowing BlackRock fund.

The limitations described above and the other conditions of the IFL Order permitting interfund lending aredesigned to minimize the risks associated with interfund lending for both the lending BlackRock fund and theborrowing BlackRock fund. However, no borrowing or lending activity is without risk. When a BlackRock fundborrows money from another BlackRock fund under the Interfund Lending Program, there is a risk that theInterfund Loan could be called on one day’s notice, in which case the borrowing BlackRock fund may have toborrow from a bank at higher rates if an Interfund Loan is not available from another BlackRock fund. InterfundLoans are subject to the risk that the borrowing BlackRock fund could be unable to repay the loan when due, anda delay in repayment to a lending BlackRock fund could result in a lost opportunity or additional lending costs.No BlackRock fund may borrow more than the amount permitted by its investment restrictions.

Shareholders should retain this Supplement for future reference.

SAI-CF-1216SUP

2

STATEMENT OF ADDITIONAL INFORMATION

BLACKROCK FUNDS IIIBLACKROCK CASH FUNDS: INSTITUTIONAL

BLACKROCK CASH FUNDS: PRIME

BLACKROCK CASH FUNDS: TREASURY

400 Howard Street, San Francisco, California 94105 • Phone No. (800) 441-7762

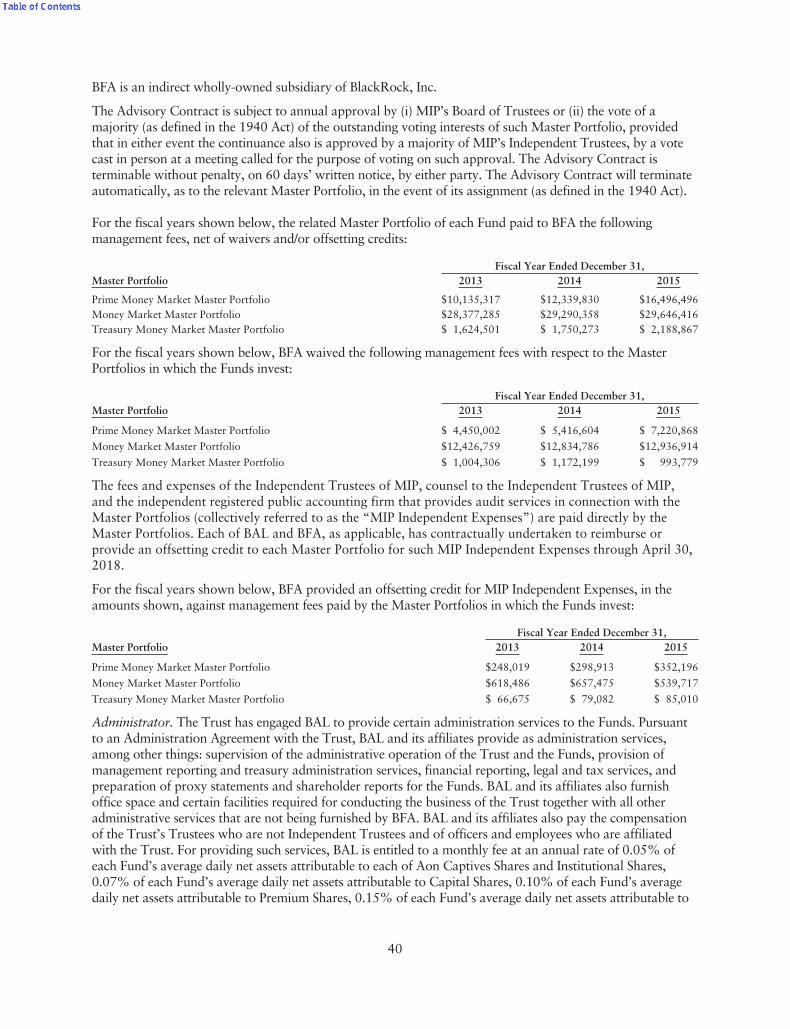

This combined Statement of Additional Information (“SAI”) of BlackRock Funds III (the “Trust”) is not aprospectus and should be read in conjunction with each of the current prospectuses of the Trust datedOctober 11, 2016, as they may from time to time be supplemented or revised, for: (i) Capital, Institutional,Premium, Select and Trust Shares of BlackRock Cash Funds: Institutional, BlackRock Cash Funds: Prime andBlackRock Cash Funds: Treasury (together with BlackRock Cash Funds: Institutional and BlackRock CashFunds: Prime, each a “Fund” and collectively, the “Funds”); and (ii) Aon Captives Shares of BlackRock CashFunds: Institutional. No investment in shares should be made without reading the appropriate prospectus. Allterms used in this SAI that are defined in the prospectuses have the meanings assigned in the prospectuses.This SAI is incorporated by reference in its entirety into each prospectus for Aon Captives, Capital,Institutional, Premium, Select and Trust Shares. Copies of the prospectuses and Annual Report and Semi-Annual Report for each of the Funds may be obtained, without charge, by writing to State Street Corporation,Institutional Transfer Agency, P.O. Box 5493, Boston, Massachusetts 02206, or by calling 1-888-204-3956(toll free). The audited financial statements of each of the Funds are incorporated into this SAI by reference tothe Funds’ 2015 Annual Report. The unaudited financial statements of each of the Funds are incorporatedinto this SAI by reference to the Funds’ 2016 Semi-Annual Report.

References to the Investment Company Act of 1940, as amended (the “1940 Act”), or other applicable law, willinclude any rules promulgated thereunder and any guidance, interpretations or modifications by the Securities andExchange Commission (the “SEC”), SEC staff or other authority with appropriate jurisdiction, including courtinterpretations, and exemptive, no-action or other relief or permission from the SEC, SEC staff or other authority.

The Trust is an open-end, series management investment company. The Funds have an additional share classwhich is described in a separate prospectus and a separate SAI. Each Fund seeks to achieve its investmentobjective by investing all of its assets in a master portfolio of Master Investment Portfolio (“MIP”). BlackRockCash Funds: Institutional invests in Money Market Master Portfolio; BlackRock Cash Funds: Prime invests inPrime Money Market Master Portfolio; and BlackRock Cash Funds: Treasury invests in Treasury MoneyMarket Master Portfolio (each, a “Master Portfolio” and collectively, the “Master Portfolios”). MIP is anopen-end, series management investment company. BlackRock Fund Advisors (“BFA” or the “InvestmentAdviser”) serves as investment adviser to each Master Portfolio. References to the investments, investmentpolicies and risks of a Fund, unless otherwise indicated, should be understood to include references to theinvestments, investment policies and risks of such Fund’s Master Portfolio.

BLACKROCK FUND ADVISORS — INVESTMENT ADVISER

BLACKROCK INVESTMENTS, LLC — DISTRIBUTOR

The date of this Statement of Additional Information is October 11, 2016

Fund and Share Class Ticker Symbol

BLACKROCK CASH FUNDS: INSTITUTIONAL

Aon Captives Shares AOCXX

Capital Shares BCIXX

Institutional Shares BGIXX

Premium Shares BSSXX

Select Shares BGLXX

Trust Shares BGTXX

BLACKROCK CASH FUNDS: PRIME

Capital Shares BCPXX

Institutional Shares BPIXX

Premium Shares BPSXX

Select Shares BPLXX

Trust Shares BPEXX

BLACKROCK CASH FUNDS: TREASURY

Capital Shares BCYXX

Institutional Shares BRIXX

Premium Shares BSPXX

Select Shares BRSXX

Trust Shares BYTXX

TABLE OF CONTENTS

Page

History of the Trust . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Description of the Funds and their Investments and Risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Investment Objectives and Policies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Master/Feeder Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Investment Restrictions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Fundamental Investment Restrictions of the Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Non-Fundamental Investment Restrictions of the Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Investments and Risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Asset-Backed and Commercial Mortgage-Backed Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Bank Obligations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Commercial Paper and Short-Term Corporate Debt Instruments . . . . . . . . . . . . . . . . . . . . . . . . . 6

Asset-Backed Commercial Paper . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Floating-Rate and Variable-Rate Obligations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Forward Commitments, When-Issued Purchases and Delayed-Delivery Transactions . . . . . . . . . 7

Funding Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Illiquid Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Investment Company Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Letters of Credit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Loans of Portfolio Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Loan Participation Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Medium-Term Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Mortgage Pass-Through Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Mortgage Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Municipal Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Non-U.S. Obligations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Participation Interests . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Regulation Regarding Derivatives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Repurchase Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Restricted Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Unrated Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

U.S. Government Obligations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

U.S. Treasury Obligations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

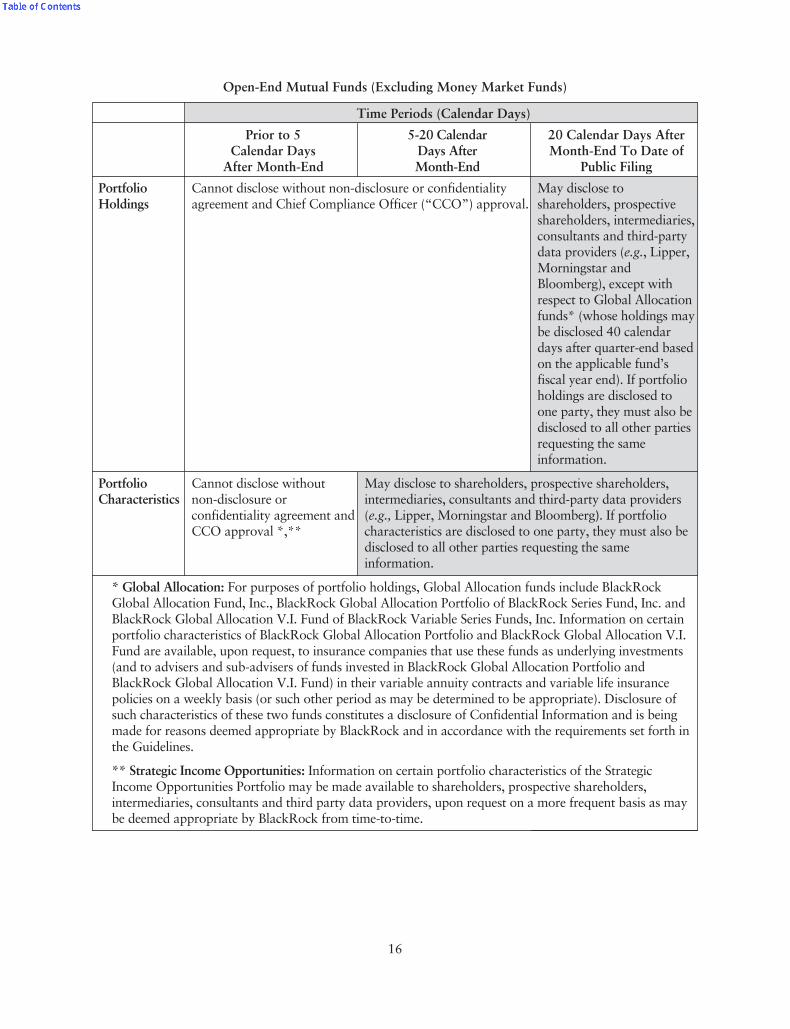

Disclosure of Portfolio Holdings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Share Ownership Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Ownership of Securities of Certain Entities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

i

Page

Compensation of Trustees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Codes of Ethics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Proxy Voting Policies of the Master Portfolios . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Shareholder Communication to the Board of Trustees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Potential Conflicts of Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Control Persons and Principal Holders of Securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Investment Adviser and Other Service Providers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Investment Adviser . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Advisory Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Administrator . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Distributor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

BlackRock Cash Funds: Institutional — Aon Captives Shares Distribution Plan . . . . . . . . . . . . . 42

Shareholder Servicing Agents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Other Payments by the Fund . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

Additional Payments by BlackRock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

Custodian . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Transfer and Dividend Disbursing Agent . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Independent Registered Public Accounting Firm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Determination of Net Asset Value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Purchase, Redemption and Pricing of Shares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

Terms of Purchase and Redemption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

In-Kind Purchases . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

Suspension of Redemption Rights or Payment of Redemption Proceeds . . . . . . . . . . . . . . . . . . . 53

Declaration of Trust Provisions Regarding Redemptions at Option of Trust . . . . . . . . . . . . . . . 53

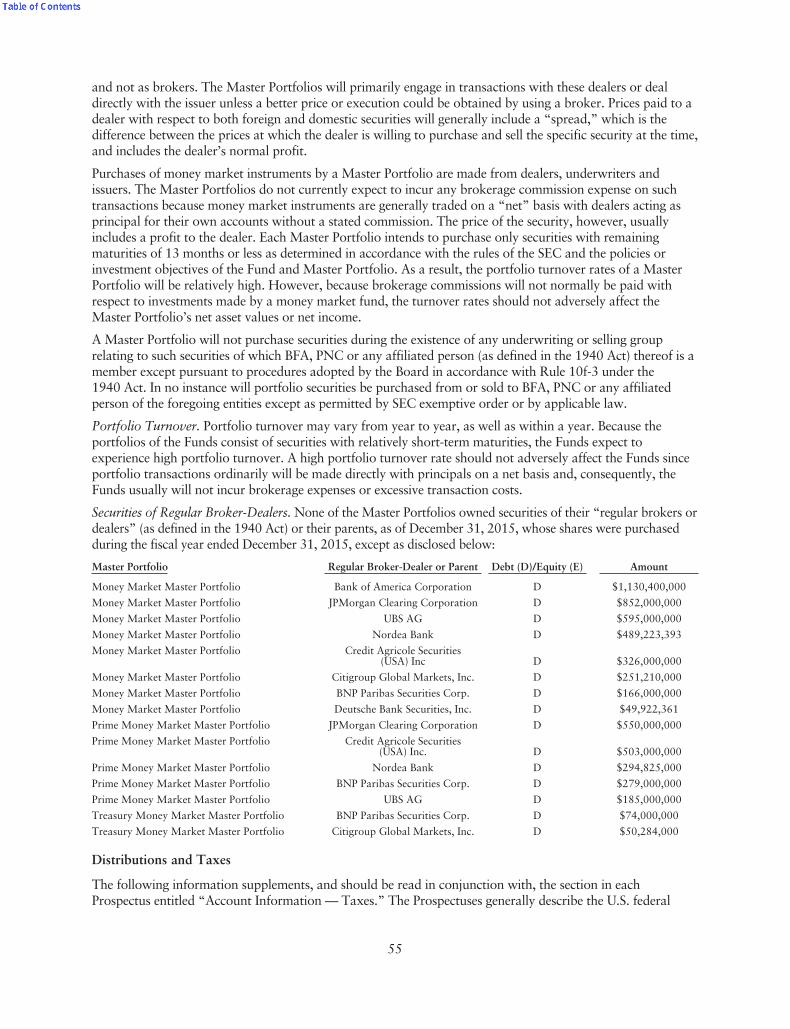

Portfolio Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

General . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

Portfolio Turnover . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

Securities of Regular Broker-Dealers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

Distributions and Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

Qualification as a Regulated Investment Company . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

Excise Tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

Capital Loss Carry-Forwards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

Investment Through the Master Portfolios . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

Taxation of Fund Investments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

Taxation of Distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

Sales of Fund Shares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

Foreign Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

ii

Page

Federal Income Tax Rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

Back-Up Withholding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

Tax-Deferred Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

Foreign Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

Foreign Account Tax Compliance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

Capital Stock . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

Voting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Dividends and Distributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Master Portfolios . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

Additional Information on the Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

Appendix A . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-1

iii

History of the Trust

BlackRock Funds III (the “Trust”) was organized on December 4, 2001 as a statutory trust under the laws ofthe State of Delaware under the name Barclays Global Investors Funds. The Trust was originally organized asa Maryland corporation named Barclays Global Investors Funds, Inc. (the “Maryland corporation”). OnAugust 21, 2001, the Board of Directors of the Maryland corporation approved a proposal to redomicile theMaryland corporation in Delaware as a Delaware statutory trust (the “Redomiciling”). Shareholders of theMaryland corporation approved the Redomiciling on November 16, 2001. The Trust was established withmultiple series corresponding to, and having identical designations as, the series of the Maryland corporation.The Redomiciling was effected on January 11, 2002, at which time the Trust assumed the operations of theMaryland corporation and adopted the Maryland corporation’s registration statement. Shortly thereafter, theMaryland corporation was dissolved.

On December 1, 2009, the Trust was renamed BlackRock Funds III and certain of its series were alsorenamed. Prime Money Market Fund was renamed BlackRock Cash Funds: Prime. Institutional MoneyMarket Fund was renamed BlackRock Cash Funds: Institutional. Treasury Money Market Fund was renamedBlackRock Cash Funds: Treasury.

The Trust consists of multiple series, including BlackRock Cash Funds: Prime, BlackRock Cash Funds:Institutional and BlackRock Cash Funds: Treasury (each, a “Fund” and collectively, the “Funds”). Each Fundissues shares in multiple classes, currently including SL Agency, Premium, Capital, Institutional, Select andTrust Shares, and with respect only to BlackRock Cash Funds: Institutional, Aon Captives Shares. SL AgencyShares are discussed in a separate Statement of Additional Information. On August 14, 2002, the Trust’sboard of trustees (the “Board of Trustees” or the “Board”) approved changing the name of BlackRock CashFunds: Institutional Distributor Shares to the “Aon Captives Shares.”

Each Fund invests all of its assets in a master portfolio (each, a “Master Portfolio” and collectively, the“Master Portfolios”) of Master Investment Portfolio (“MIP”) (as shown below), which has substantially thesame investment objective, policies and restrictions as the related Fund.

Fund Master Portfolio in Which the Fund Invests

BlackRock Cash Funds: Prime Prime Money Market Master Portfolio

BlackRock Cash Funds: Institutional Money Market Master Portfolio

BlackRock Cash Funds: Treasury Treasury Money Market Master Portfolio

The Trust’s principal office is located at 400 Howard Street, San Francisco, California 94105.

Description of the Funds and their Investments and Risks

Investment Objectives and Policies. The Trust is an open-end, series management investment company.

Each of BlackRock Cash Funds: Prime and BlackRock Cash Funds: Institutional is a non-retail, non-government money market fund under Rule 2a-7 under the 1940 Act (each an “Institutional Fund”). Each ofMoney Market Master Portfolio and Prime Money Market Master Portfolio is a non-retail, non-governmentmoney market fund under Rule 2a-7 (each an “Institutional Master Portfolio”). Each of BlackRock CashFunds: Treasury and Treasury Money Market Master Portfolio is a government money market fund underRule 2a-7.

The Funds and the Master Portfolios in which they invest are diversified funds as defined in the 1940 Act.Each Fund’s investment objective is set forth in its Prospectuses. Each Fund’s investment objective isnon-fundamental and can be changed by the Trust’s Board of Trustees without shareholder approval. Theinvestment objective and investment policies of a Fund determine the types of portfolio securities in which theFund invests, the degree of risk to which the Fund is subject and, ultimately, the Fund’s performance. Therecan be no assurance that the investment objective of any Fund will be achieved.

Master/Feeder Structure. Each Fund seeks to achieve its investment objective by investing all of its assets in thecorresponding Master Portfolio of MIP. The Trust’s Board of Trustees believes that under normal

1

circumstances, none of the Funds or their shareholders will be adversely affected by investing Fund assets in aMaster Portfolio. However, if a mutual fund or other investor redeems its interests from a Master Portfolio, theeconomic efficiencies (e.g., spreading fixed expenses over a larger asset base) that the Trust’s Board of Trusteesbelieves may be available through a Fund’s investment in such Master Portfolio may not be fully achieved. Inaddition, although unlikely, the master/feeder structure may give rise to accounting or operational difficulties.

The fundamental policies of each Master Portfolio cannot be changed without approval by the holders of amajority (as defined in the 1940 Act) of a Master Portfolio’s outstanding interests. Whenever a Fund, as aninterestholder of a Master Portfolio, is requested to vote on any matter submitted to interestholders of theMaster Portfolio, a Fund will either hold a meeting of its shareholders to consider such matters and cast itsvotes in proportion to the votes received from its shareholders (shares for which a Fund receives no votinginstructions will be voted in the same proportion as the votes received from the other Fund shareholders) orcast its votes, as an interestholder of the Master Portfolio, in proportion to the votes received by the MasterPortfolio from all other interestholders of the Master Portfolio.

Certain policies of the Master Portfolios that are non-fundamental may be changed by vote of a majority ofMIP’s Trustees without interestholder approval. If a Master Portfolio’s investment objective or fundamentalor non-fundamental policies are changed, a Fund may elect to change its objective or policies to correspond tothose of the related Master Portfolio. Each Fund may redeem its interests from its Master Portfolio only if theTrust’s Board of Trustees determines that such action is in the best interests of the Fund and its shareholders,for this or any other reason. Prior to such redemption, the Trust’s Board of Trustees would consideralternatives, including whether to seek a new investment company with a matching investment objective inwhich to invest or retain its own investment adviser to manage the Fund’s portfolio in accordance with itsinvestment objective. In the latter case, a Fund’s inability to find a substitute investment company in which toinvest or equivalent management services could adversely affect shareholders’ investments in the Fund.

Investment Restrictions

Fundamental Investment Restrictions of the Funds. The Funds are subject to the following investmentrestrictions, all of which are fundamental policies. Each Fund may not:

(1) Purchase the securities of issuers conducting their principal business activity in the same industry if,immediately after the purchase and as a result thereof, the value of the Fund’s investments in that industrywould equal or exceed 25% of the current value of the Fund’s total assets, provided that this restriction doesnot limit the Fund’s: (i) investments in securities of other investment companies, (ii) investments in securitiesissued or guaranteed by the U.S. Government, its agencies or instrumentalities, or (iii) investments inrepurchase agreements collateralized by U.S. Government securities; and further provided that, with respect toBlackRock Cash Funds: Prime and BlackRock Cash Funds: Institutional, the Fund reserves the right toconcentrate in the obligations of domestic banks (as such term is interpreted by the Securities and ExchangeCommission (“SEC”) or its staff);

(2) Purchase the securities of any single issuer if, as a result, with respect to 75% of the Fund’s total assets,more than 5% of the value of its total assets would be invested in the securities of such issuer or the Fund’sownership would be more than 10% of the outstanding voting securities of such issuer, provided that thisrestriction does not limit the Fund’s cash or cash items, investments in U.S. Government securities, orinvestments in securities of other investment companies;

(3) Borrow money or issue senior securities, except to the extent permitted under the 1940 Act, including therules, regulations and any orders obtained thereunder;

(4) Make loans to other parties, except to the extent permitted under the 1940 Act, including the rules,regulations and any orders obtained thereunder. For the purposes of this limitation, entering into repurchaseagreements, lending securities and acquiring any debt securities are not deemed to be the making of loans;

(5) Underwrite securities of other issuers, except to the extent that the purchase of permitted investmentsdirectly from the issuer thereof or from an underwriter for an issuer and the later disposition of such securitiesin accordance with the Fund’s investment program may be deemed to be an underwriting; and provided

2

further, that the purchase by the Fund of securities issued by an open-end management investment company,or a series thereof, with substantially the same investment objective, policies and restrictions as the Fund shallnot constitute an underwriting for purposes of this paragraph;

(6) Purchase or sell real estate unless acquired as a result of ownership of securities or other instruments (butthis shall not prevent the Fund from investing in securities or other instruments backed by real estate orsecurities of companies engaged in the real estate business); and

(7) Purchase or sell commodities, provided that: (i) currency will not be deemed to be a commodity forpurposes of this restriction, (ii) this restriction does not limit the purchase or sale of futures contracts, forwardcontracts or options, and (iii) this restriction does not limit the purchase or sale of securities or otherinstruments backed by commodities or the purchase or sale of commodities acquired as a result of ownershipof securities or other instruments.

With respect to the fundamental policy relating to concentration set forth in paragraph (1) above, the 1940 Actdoes not define what constitutes “concentration” in an industry and it is possible that interpretations ofconcentration could change in the future. Accordingly, the policy in paragraph (1) above will be interpreted torefer to concentration as that term may be interpreted from time to time. In this respect, and in accordance withSEC staff interpretations, the ability of BlackRock Cash Funds: Prime and BlackRock Cash Funds: Institutionalto concentrate in the obligations of domestic banks means that these Funds are permitted to invest, withoutlimit, in bankers’ acceptances, certificates of deposit and other short-term obligations issued by (a) U.S. banks,(b) U.S. branches of foreign banks (in circumstances in which the U.S. branches of foreign banks are subject tothe same regulation as U.S. banks), and (c) foreign branches of U.S. banks (in circumstances in which the Fundswill have recourse to the U.S. bank for the obligations of the foreign branch). A Fund may invest in otherinvestment companies that may concentrate their assets in one or more industries. A Fund may consider theconcentration of such other investment companies in determining compliance with the Fund’s concentrationpolicy.

The Trust has delegated to BlackRock Fund Advisors (“BFA” or the “Investment Adviser”), an affiliate ofBlackRock, Inc. (together with its affiliates, “BlackRock”), the ability to determine the methodology used bythe Master Portfolios to classify issuers by industry. BFA defines industries and classifies each issuer accordingto the industry in which the issuer conducts its principal business activity pursuant to its proprietary industryclassification system. In classifying companies by industry, BFA may draw on its credit, research andinvestment resources and those of BlackRock Institutional Trust Company, N.A. (“BTC”) or its otheraffiliates, and BFA may (but need not) consider classifications by third-party industry classification systems.BFA believes that its system is reasonably designed so that issuers with primary economic characteristics thatare materially the same are classified in the same industry. For example, asset-backed commercial paper maybe classified in an industry based on the nature of the assets backing the commercial paper, and foreign banksmay be classified in an industry based on the region in which they do business if BFA has determined that theforeign banks within that industry have primary economic characteristics that are materially the same.

A fund that invests a significant percentage of its total assets in a single industry may be particularly susceptibleto adverse events affecting that industry and may be more risky than a fund that does not concentrate in anindustry. To the extent BFA’s classification system results in broad categories, concentration risk may bedecreased. On the other hand, to the extent it results in narrow categories, concentration risk may be increased.

With respect to paragraph (3) above, the 1940 Act currently allows each Fund to borrow up to one-third ofthe value of its total assets (including the amount borrowed) valued at the lesser of cost or market, lessliabilities (not including the amount borrowed) at the time the borrowing is made. With respect to paragraph(4) above, the 1940 Act and regulatory interpretations currently limit the percentage of each Fund’s securitiesthat may be loaned to one-third of the value of its total assets.

Non-Fundamental Investment Restrictions of the Funds. The Funds have adopted the following investmentrestrictions as non-fundamental policies. These restrictions may be changed without shareholder approval bya majority of the Trustees of the Trust at any time.

3

(1) Each Fund may invest in shares of other open-end management investment companies, subject to thelimitations of Section 12(d)(1) of the 1940 Act, including the rules, regulations and exemptive orders obtainedthereunder;

(2) Each Fund may not invest more than 5% of its net assets in illiquid securities. For this purpose, illiquidsecurities include, among others, (i) securities that are illiquid by virtue of the absence of a readily availablemarket or legal or contractual restrictions on resale, (ii) fixed time deposits that are subject to withdrawalpenalties and that have maturities of more than seven days, and (iii) repurchase agreements not terminablewithin seven days;

(3) Each Fund may lend securities from its portfolio to brokers, dealers and financial institutions, in amountsnot to exceed (in the aggregate) one-third of a Fund’s total assets. Any such loans of portfolio securities will befully collateralized based on values that are marked-to-market daily; and

(4) Each Fund may not make investments for the purpose of exercising control or management; provided thata Fund may invest all of its assets in a diversified, open-end management investment company, or a seriesthereof, with substantially the same investment objective, policies and restrictions as the Fund, without regardto the limitations set forth in this paragraph.

BlackRock Cash Funds: Treasury has adopted the following investment restrictions as additionalnon-fundamental policies:

(1) The Fund invests at least 99.5% of its total assets in cash, U.S. Treasury bills, notes and other directobligations of the U.S. Treasury, and repurchase agreements secured by such obligations or cash.

(2) The Fund will invest, under normal circumstances, at least 80% of its net assets, plus the amount of anyborrowings for investment purposes, in U.S. Treasury bills, notes and other obligations of the U.S. Treasury,and repurchase agreements secured by such obligations. This policy will not be changed without providingshareholders with at least 60 days’ prior notice of any change in the policy.

BlackRock Cash Funds: Prime and BlackRock Cash Funds: Institutional have adopted the followinginvestment restrictions as additional non-fundamental policies:

(1) Each Fund may not purchase interests, leases, or limited partnership interests in oil, gas, or other mineralexploration or development programs.

(2) Each Fund may not write, purchase or sell puts, calls, straddles, spreads, warrants, options or anycombination thereof, except that the Fund may purchase securities with put rights in order to maintainliquidity.

(3) Each Fund may not purchase securities on margin (except for short-term credits necessary for the clearanceof transactions) or make short sales of securities.

Notwithstanding any other investment policy or restriction (whether or not fundamental), each Fund may(and does) invest all of its assets in the securities of a single open-end management investment company withsubstantially the same fundamental investment objective, policies and limitations as the Fund.

The fundamental and non-fundamental investment restrictions for each Master Portfolio are identical to thecorresponding investment restrictions described above for the Fund that invests in such Master Portfolio,except that, in the case of Treasury Money Market Master Portfolio, industry concentration restriction (1),proviso (iii) does not limit investments in repurchase agreements collateralized by securities issued orguaranteed by the U.S., its agencies or instrumentalities.

Investment Risks

To the extent set forth in this SAI, each Fund, through its investment in the corresponding Master Portfolio,may invest in the securities described below. To avoid the need to refer to both the Funds and the MasterPortfolios in every instance, the following sections generally refer to the Funds only.

4

The assets of each Fund consist only of obligations maturing within 397 calendar days from the date ofacquisition (as determined in accordance with the regulations of the SEC). The dollar-weighted averagematurity of a Fund may not exceed 60 days and the dollar-weighted average life of a Fund may not exceed120 days. The securities in which each Fund invests may not yield as high a level of current income as may beachieved from securities with less liquidity and less safety. There can be no assurance that a Fund’s investmentobjective will be realized as described in its Prospectuses.

BlackRock Cash Funds: Treasury invests at least 99.5% of its total assets in cash, U.S. Treasury bills, notesand other direct obligations of the U.S. Treasury, and repurchase agreements secured by such obligations orcash. Practices described below relating to illiquid securities, investment company securities, loans of portfoliosecurities and repurchase agreements also apply to BlackRock Cash Funds: Treasury.

BlackRock Cash Funds: Prime and BlackRock Cash Funds: Institutional may invest in any of the instrumentsor engage in any practice described below.

Asset-Backed and Commercial Mortgage-Backed Securities. BlackRock Cash Funds: Institutional andBlackRock Cash Funds: Prime may invest in asset-backed and commercial mortgage-backed securities. Asset-backed securities are securities backed by installment contracts, credit-card receivables or other assets.Commercial mortgage-backed securities are securities backed by commercial real estate properties. Both asset-backed and commercial mortgage-backed securities represent interests in “pools” of assets in which paymentsof both interest and principal on the securities are made on a regular basis. The payments are, in effect,“passed through” to the holder of the securities (net of any fees paid to the issuer or guarantor of thesecurities). The average life of asset-backed and commercial mortgage-backed securities varies with thematurities of the underlying instruments and, as a result of prepayments, can often be shorter or longer (as thecase may be) than the original maturity of the assets underlying the securities. For this and other reasons, anasset-backed and commercial mortgage-backed security’s stated maturity may be shortened or extended, andthe security’s total return may be difficult to predict precisely. The Funds may invest in such securities up tothe limits prescribed by Rule 2a-7 and other provisions of or under the 1940 Act. Changes in liquidity of thesesecurities may result in significant, rapid and unpredictable changes in prices for credit-linked securities. Alsosee “Mortgage Pass-Through Securities” and “Mortgage Securities.”

Bank Obligations. BlackRock Cash Funds: Institutional and BlackRock Cash Funds: Prime may invest inbank obligations, including certificates of deposit (“CDs”), time deposits, bankers’ acceptances and othershort-term obligations of domestic and foreign banks, foreign subsidiaries of domestic banks, foreign branchesof domestic banks, foreign branches of foreign banks, and domestic branches of foreign banks, domesticsavings and loan associations and other banking institutions. Certain bank obligations may benefit fromexisting or future governmental debt guarantee programs.

CDs are negotiable certificates evidencing the obligation of a bank to repay funds deposited with it for aspecified period of time.

Time deposits (“TDs”) are non-negotiable deposits maintained in a banking institution for a specified periodof time at a stated interest rate. TDs that may be held by the Funds will not benefit from insurance from theBank Insurance Fund or the Savings Association Insurance Fund administered by the Federal DepositInsurance Corporation (“FDIC”).

Bankers’ acceptances are credit instruments evidencing the obligation of a bank to pay a draft drawn on it bya customer. These instruments reflect the obligation both of the bank and of the drawer to pay the faceamount of the instrument upon maturity. The other short-term obligations may include uninsured, directobligations bearing fixed-, floating- or variable-interest rates.

Domestic commercial banks organized under federal law are supervised and examined by the Comptroller ofthe Currency and are required to be members of the Federal Reserve System and to have their deposits insuredby the FDIC. Domestic banks organized under state law are supervised and examined by state bankingauthorities and are members of the Federal Reserve System only if they elect to join. In addition, state bankswhose CDs may be purchased by the Funds are insured by the FDIC (although such insurance may not be of

5

material benefit to a Fund, depending on the principal amount of the CDs of each bank held by the Fund) andare subject to federal examination and to a substantial body of federal law and regulation. As a result of federalor state laws and regulations, domestic branches of domestic banks whose CDs may be purchased by the Fundsgenerally are required, among other things, to maintain specified levels of reserves, are limited in the amountsthat they can loan to a single borrower and are subject to other regulations designed to promote financialsoundness. However, not all of such laws and regulations apply to the foreign branches of domestic banks.

Obligations of foreign branches of domestic banks, foreign subsidiaries of domestic banks and domestic andforeign branches of foreign banks, such as CDs and TDs, may be general obligations of the parent banks inaddition to the issuing branch, or may be limited by the terms of a specific obligation and/or governmentalregulation. Such obligations are subject to different risks than are those of domestic banks. These risks includeforeign economic and political developments, foreign governmental restrictions that may adversely affectpayment of principal and interest on the obligations, foreign exchange controls and foreign withholding andother taxes on amounts realized on the obligations. These foreign branches and subsidiaries are not necessarilysubject to the same or similar regulatory requirements that apply to domestic banks, such as mandatoryreserve requirements, loan limitations, and accounting, auditing and financial record keeping requirements. Inaddition, less information may be publicly available about a foreign branch of a domestic bank or about aforeign bank than about a domestic bank.

Obligations of U.S. branches of foreign banks may be general obligations of the parent bank in addition to theissuing branch, or may be limited by the terms of a specific obligation or by federal or state regulation, as wellas governmental action in the country in which the foreign bank has its head office. A domestic branch of aforeign bank with assets in excess of $1 billion may be subject to reserve requirements imposed by the FederalReserve System or by the state in which the branch is located if the branch is licensed in that state.

In addition, federal branches licensed by the Comptroller of the Currency and branches licensed by certainstates may be required to: (1) pledge to the appropriate regulatory authority, by depositing assets with adesignated bank within the relevant state, a certain percentage of their assets as fixed from time to time bysuch regulatory authority; and (2) maintain assets within the relevant state in an amount equal to a specifiedpercentage of the aggregate amount of liabilities of the foreign bank payable at or through all of its agenciesor branches within the state.

Commercial Paper and Short-Term Corporate Debt Instruments. The Funds may invest in commercial paper(including variable amount master demand notes), which consists of short-term, unsecured promissory notesissued by corporations to finance short-term credit needs. Commercial paper is usually sold on a discountbasis and usually has a maturity at the time of issuance not exceeding nine months. Variable amount masterdemand notes are demand obligations that permit a Fund to invest fluctuating amounts, which may changedaily without penalty, pursuant to direct arrangements between a Fund, as lender, and the borrower. Theinterest on these notes varies pursuant to the arrangements between the Fund and the borrower. Both theborrower and the Fund have the right to vary the amount of the outstanding indebtedness on the notes. BFAmonitors on an ongoing basis the ability of an issuer of a demand instrument to pay principal and interest ondemand.

The Funds also may invest in non-convertible corporate debt securities (e.g., bonds and debentures) with notmore than thirteen months remaining to maturity at the date of settlement. A Fund will invest only in suchcorporate bonds and debentures that are deemed appropriate by BFA in accordance with Rule 2a-7 under the1940 Act. Subsequent to its purchase by a Fund, an issue of securities may cease to be rated or its rating maybe reduced. BFA will consider such an event in determining whether the Fund should continue to hold theobligation. To the extent the Fund continues to hold the obligation, it may be subject to additional risk ofdefault.

Asset-Backed Commercial Paper. A Fund may also invest in asset-backed commercial paper. Asset-backedcommercial paper is a type of securitized commercial paper product used to fund purchases of financial assetsby special purpose finance companies called conduits. The financial assets may include assets such as pools oftrade receivables, car loans and leases, and credit card receivables, among others. Asset-backed commercial

6

paper is typically tracked and rated by one or more credit rating agencies. Some asset-backed commercialpaper programs maintain a back-up liquidity facility provided by a major bank, which is intended to be usedif the issuer is unable to issue new asset-backed commercial paper.

Floating-Rate and Variable-Rate Obligations. The Funds may purchase debt instruments with interest ratesthat are periodically adjusted at specified intervals or whenever a benchmark rate or index changes. Thefloating-rate and variable-rate instruments that the Funds may purchase include certificates of participation insuch instruments. The interest rate adjustments generally limit the increase or decrease in the amount ofinterest received on the debt instruments. Floating-rate and variable-rate instruments are subject to interestrate risk and credit risk.

The Funds may purchase floating-rate and variable-rate demand notes and bonds, which are obligationsordinarily having stated maturities in excess of thirteen months, but which permit the holder to demandpayment of principal at any time, or at specified intervals not exceeding 397 days, as defined in accordancewith Rule 2a-7 and the 1940 Act. Variable-rate demand notes including master demand notes are demandobligations that permit a Fund to invest fluctuating amounts, which may change daily without penalty,pursuant to direct arrangements between a Fund, as lender, and the borrower. The interest rates on thesenotes fluctuate from time to time. The issuer of such obligations ordinarily has a corresponding right, after agiven period, to prepay in its discretion the outstanding principal amount of the obligations plus accruedinterest upon a specified number of days’ notice to the holders of such obligations. The interest rate on afloating-rate demand obligation is based on a known lending rate, such as a bank’s prime rate, and is adjustedautomatically each time such rate is adjusted. The interest rate on a variable-rate demand obligation isadjusted automatically at specified intervals. Frequently, such obligations are secured by letters of credit orother credit support arrangements provided by banks.

These obligations are direct lending arrangements between the lender and borrower. There may not be anestablished secondary market for these obligations, although they are redeemable at face value. Accordingly,where these obligations are not secured by letters of credit or other credit support arrangements, a Fund’sright to redeem is dependent on the ability of the borrower to pay principal and interest on demand. Suchobligations frequently are not rated by credit rating agencies. BFA considers on an ongoing basis thecreditworthiness of the issuers of the floating-rate and variable-rate demand obligations in a Fund’s portfolio.

Forward Commitments, When-Issued Purchases and Delayed-Delivery Transactions. A Fund may purchaseor sell securities that it is entitled to receive on a when issued basis. A Fund may also purchase or sell securitieson a delayed delivery basis or through a forward commitment (including on a “TBA” (to be announced)basis). These transactions involve the purchase or sale of securities by a Fund at an established price withpayment and delivery taking place in the future. The Fund enters into these transactions to obtain what isconsidered an advantageous price to the Fund at the time of entering into the transaction. When a Fundpurchases securities in these transactions, the Fund segregates liquid securities in an amount equal to theamount of its purchase commitments.

Pursuant to recommendations of the Treasury Market Practices Group, which is sponsored by the FederalReserve Bank of New York, beginning January 1, 2014, a Fund or its counterparty generally will be requiredto post collateral when entering into certain forward-settling transactions, including without limitation TBAtransactions.

There can be no assurance that a security purchased on a when issued basis will be issued or that a securitypurchased or sold on a delayed delivery basis or through a forward commitment will be delivered. Also, thevalue of securities in these transactions on the delivery date may be more or less than the price paid by theFund to purchase the securities. The Fund will lose money if the value of the security in such a transactiondeclines below the purchase price and will not benefit if the value of the security appreciates above the saleprice during the commitment period.

If deemed advisable as a matter of investment strategy, a Fund may dispose of or renegotiate a commitmentafter it has been entered into, and may sell securities it has committed to purchase before those securities aredelivered to the Fund on the settlement date. In these cases the Fund may realize a taxable capital gain or loss.

7

When a Fund engages in when-issued, TBA or forward commitment transactions, it relies on the other partyto consummate the trade. Failure of such party to do so may result in the Fund’s incurring a loss or missing anopportunity to obtain a price considered to be advantageous.

The market value of the securities underlying a commitment to purchase securities, and any subsequentfluctuations in their market value, is taken into account when determining the market value of a Fund startingon the day the Fund agrees to purchase the securities. The Fund does not earn interest on the securities it hascommitted to purchase until they are paid for and delivered on the settlement date.

Funding Agreements. The Funds may invest in short-term funding agreements. A funding agreement is acontract between an issuer and a purchaser that obligates the issuer to pay a guaranteed rate of interest on aprincipal sum deposited by the purchaser. Funding agreements will also guarantee the return of principal andmay guarantee a stream of payments over time. A funding agreement has a fixed maturity and may haveeither a fixed-, variable- or floating-interest rate that is based on an index and guaranteed for a fixed timeperiod. The Funds will purchase short-term funding agreements only from banks and insurance companies.The Funds may also purchase Guaranteed Investment Contracts.

The secondary market, if any, for these funding agreements is limited; thus, such investments purchased by theFunds may be treated as illiquid. If a funding agreement is determined to be illiquid it will be valued by eachInstitutional Fund at its fair market value as determined by procedures approved by the Board of Trustees.Valuation of illiquid indebtedness involves a greater degree of judgment in determining the value of eachInstitutional Fund’s assets than if the value were based on available market quotations.

Illiquid Securities. Each Fund may invest in securities as to which a liquid trading market does not exist,provided such investments are consistent with its investment objective. Such securities may include securitiesthat are not readily marketable, such as privately issued securities and other securities that are subject to legalor contractual restrictions on resale, floating-rate and variable-rate demand obligations as to which the Fundcannot exercise a demand feature on not more than seven days’ notice and as to which there is no secondarymarket, and repurchase agreements providing for settlement more than seven days after notice.

Investment Company Securities. Each Fund may invest in shares of open-end investment companies, includinginvestment companies that are affiliated with the Funds and BFA, that invest exclusively in high-quality short-term securities to the extent permitted under the 1940 Act, including the rules, regulations and exemptiveorders obtained thereunder; provided, however, that a Fund, if it has knowledge that its beneficial interests arepurchased by another investment company investor pursuant to Section 12(d)(1)(G) of the 1940 Act, will notacquire any securities of registered open-end management investment companies or registered unit investmenttrusts in reliance on Section 12(d)(1)(F) or 12(d)(1)(G) of the 1940 Act. Other investment companies in whicha Fund invests can be expected to charge fees for operating expenses, such as investment advisory andadministration fees, that would be in addition to those charged by the Fund. A Fund may also purchase sharesof exchange listed closed-end funds to the extent permitted under the 1940 Act. Under the 1940 Act, a Fund’sinvestment in investment companies is limited to, subject to certain exceptions, (i) 3% of the total outstandingvoting stock of any one investment company, (ii) 5% of the Fund’s total assets with respect to any oneinvestment company, and (iii) 10% of the Fund’s total assets with respect to investment companies in theaggregate. To the extent allowed by law or regulation, each Fund may invest its assets in securities ofinvestment companies that are money market funds, including those advised by BFA or otherwise affiliatedwith BFA, in excess of the limits discussed above.

Letters of Credit. Certain of the debt obligations (including municipal securities, certificates of participation,commercial paper and other short-term obligations) that the Funds may purchase may be backed by anunconditional and irrevocable letter of credit issued by a bank, savings and loan association or insurancecompany that assumes the obligation for payment of principal and interest in the event of default by theissuer. Only banks, savings and loan associations and insurance companies that, in the opinion of BFA, are ofcomparable quality to issuers of other permitted investments of the Funds may be used for letter of credit-backed investments.

8