AP18 - Southwest Baking Company: Applying FactoryTalk Batch For Flexibility and Modularity

BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0

Business Plan

Medium Term plan outlining growth opportunities and strategies for optimising growth over the next 3 to 5 years.

Prepared: September 2016

By: Craigie Mains Ltd

Contact: Harriet Hastings

Biscuiteer Baking Company Ltd 18 Stannary Street, London, SE11 4AA +44 (0) 8704 588 358 [email protected]

Biscuiteer Baking Company Ltd

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 2 of 32

Important notice The contents of this Circular have not been approved by an authorised person. Such approval is required by section 21 Financial Services and Markets Act 2000 unless an exemption applies. This communication is directed only at "Investment Professionals" within the meaning of article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001 (i.e. in broad terms, directed only at persons having professional experience in matters relating to investments).

These persons are most likely to be:

1. Persons whose ordinary activities involve them, as principal or as agent, in acquiring, holding, managing or disposing of investments for the purposes of a business carried on by them;

2. Persons whose ordinary business involves the giving of advice which may lead to another person acquiring or disposing of an investment or refraining from so doing; and

3. Persons whose ordinary business involves making arrangements with a view to another person acquiring or disposing of investments.

If you do not fall within the above categories you should return this document immediately to the Company at the following address: Biscuiteers Baking Company Ltd, 18 Stannary Street, London, SE11 4AA

If the addressee is in any doubt about the proposals contained in this Circular they should consult an authorised person specialising in advising on investments of the kind in question. Any reliance on the Circular for the purpose of engaging in any investment activity may expose the addressee to a significant risk of losing the value of their investments in the Company.

The information in this document, which does not purport to be comprehensive, has been provided by the management of Biscuiteer Baking Company Ltd and has not been independently verified. No representation or warranty, express or implied, is given by Biscuiteer Baking Company Ltd or the Directors of Biscuiteer Baking Company Ltd as to the accuracy of the information or the opinions contained in this document or any other written or oral information made available to any interested party. No liability (whether in negligence or otherwise) is accepted for any such information or opinions (save in the case of fraud).

No information set out in this document or referred to, or any other written or oral information supplied to any interested party will form the basis of any contract. Any prospective purchaser of new shares issued by Biscuiteer Baking Company Ltd will be required to acknowledge in an investment contract that he has not relied on or been induced to enter such agreement by any representation or warranty, save as expressly set out in such agreement.

This document is being made available only to those parties who have signed and returned a non-disclosure agreement and recipients are therefore bound by the agreement in respect of all information in this document and any other information provided subsequently. This document must not be distributed, published or reproduced in whole or in part or disclosed by recipients to any other person.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 3 of 32

DISCLAIMER

This Circular, which is not a prospectus, is issued by Biscuiteer Baking Company Ltd and is for use only by Biscuiteer Baking Company Ltd or the person to whom it is addressed.

This Circular should not be considered as a recommendation by Biscuiteer Baking Company Ltd or its directors, officers, agents or employees to enter into the Shareholders Agreement. It will be assumed that you have carried out your own enquiries and inspections and have considered all the relevant information. Your attention is drawn to the contents of section headed "Risk Factors".

Neither the issue of this Circular nor any part of its contents is to be taken as any form of commitment on the part of Biscuiteer Baking Company Ltd to proceed with any of the Proposals envisaged in this Circular and the right is reserved without advance notice to change the procedure for the acceptance of the Proposals or to terminate any negotiations with any prospective investors at any time. In no circumstances will Biscuiteer Baking Company Ltd be responsible for any costs or expenses incurred in connection with any appraisal or investigation of Biscuiteer Baking Company Ltd or for any other costs and expenses incurred by a Shareholder or prospective investor in connection with Biscuiteer Baking Company Ltd.

Any person who is not a resident of the United Kingdom wishing to agree to the Proposals must satisfy himself as to full observance of the laws of any relevant territory in connection therewith including any requisite governmental or other consents which may be required and compliance with any other requisite formalities. Recipients should consult their professional advisers to ascertain whether any governmental or other consents may be required or any other formalities need to be observed to enable them to accept the Proposals concerning Biscuiteer Baking Company Ltd.

Without limiting the generality of the preceding paragraph, this Circular does not constitute an offer of any securities in Biscuiteer Baking Company Ltd in the United States of America or any resident of the United States of America or any of its territories or to any US citizen resident outside thereof. Biscuiteer Baking Company Ltd shares have not been registered in the United States of America under the US Securities Act 1933.

© Biscuiteer Baking Company Ltd All rights reserved. This document comprises proprietary and confidential information and copyright material belonging to Biscuiteer Baking Company Ltd. Other than as permitted by law, no part of this document may be reproduced, adapted, or distributed, in any form or by any means, without the prior written consent of Biscuiteer Baking Company Ltd.

The information in this document is subject to change without notice. All trademarks acknowledged.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 4 of 32

Table of Contents 1 Introduction .................................................................................................................................... 5 2 Company Background..................................................................................................................... 6

2.1 Some important milestones ..........................................................................................................6

2.2 Awards and Recognition ...............................................................................................................6

2.3 Production and Premises ..............................................................................................................6

2.4 Products and Sales ........................................................................................................................7

3 Market............................................................................................................................................. 8 4 Opportunity .................................................................................................................................. 10 5 Products and Services ................................................................................................................... 11

5.1 Production .................................................................................................................................. 11

5.2 Online Sales ................................................................................................................................ 12

5.3 Retail Sales ................................................................................................................................. 13

5.4 Corporate Sales .......................................................................................................................... 13

5.5 Wholesale .................................................................................................................................. 14

5.6 Other Products and Sales ........................................................................................................... 14

6 Financial Summary ....................................................................................................................... 16 7 Management ................................................................................................................................ 18

7.1 Harriet Hastings – Founder and Managing Director .................................................................. 18

7.2 Stevie Congdon – Co-Founder ................................................................................................... 18

7.3 Non-Executive ............................................................................................................................ 18

7.4 New Hires ................................................................................................................................... 19

7.5 Organisation Chart ..................................................................................................................... 19

8 Competition .................................................................................................................................. 20 8.1 Food Gifting ................................................................................................................................ 20

8.2 Founder Driven Brands .............................................................................................................. 21

8.3 Larger Scale Gifting Businesses .................................................................................................. 22

9 Risk Factors ................................................................................................................................... 23 10 Expansion Plan and Funding ........................................................................................................ 24

10.1 Production .................................................................................................................................. 24

10.2 Website ...................................................................................................................................... 24

10.3 Operations ................................................................................................................................. 25

10.4 International .............................................................................................................................. 25

10.5 Staffing ....................................................................................................................................... 25

10.6 Retail .......................................................................................................................................... 26

10.7 Working Capital and Contingency .............................................................................................. 26

11 Summary ....................................................................................................................................... 27

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 5 of 32

1 Introduction The Biscuiteer Baking Company (“Biscuiteers”) is a small but market leading business. It specialises in making and selling hand baked hand iced biscuits in beautiful gift tins. It has grown each year since incorporation in 2007 and has been profitable throughout. The Company now wishes to build further on its foundations and with the introduction of external capital it plans to improve its operational infrastructure and extend its retail footprint.

This plan provides a comprehensive summary of the company’s history, its products and services, and the opportunities it is hoping to exploit over the medium to longer term. It outlines the scale and type of funding that the Directors are seeking and the Appendices provide extensive supporting material. It is principally addressed to Certified Sophisticated Investors and High Net Worth Individuals who may be interested in investing in the Company’s future.

For the most part the plan envisages ‘organic’ growth focusing on existing business activities which are already cash generative, and so the principal benefit of the additional funding will be to accelerate growth from a stronger capital base. It will also allow Biscuiteers to recruit some key managers to supervise this growth and open up the possibility of licensed sales outside the UK.

The Directors have already taken the first steps to implement the plan (by streamlining production processes and recruiting new digital expertise) and hope to finalise the funding arrangements in 2016 so that the full impact can be realised in 2017 and beyond.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 6 of 32

2 Company Background Biscuiteers is an award-winning online retailer of hand-made and hand-iced biscuits, cakes and chocolates. Launched in 2007 with the mission statement ‘why send flowers when you can send Biscuiteers instead?’ Biscuiteers was the first company in the UK to offer luxurious collections of hand-iced biscuits to send as gifts. With exceptional packaging and a range of constantly changing seasonal collections, it has established itself as a leading player in the premium gifting market.

2.1 Some important milestones Biscuiteers has achieved an extraordinary level of brand recognition among ABC1 opinion formers in a very short period. It has shown steady growth since launch and remained profitable throughout. The largest part of the business is composed of online sales direct to consumers, but the Company’s products are also stocked by leading retailers including Selfridges, Fortnum & Mason, Harrods and Conran.

Biscuiteers also has successful and growing corporate sales with regular customers including Chanel, Burberry, Mulberry and Net a Porter. It also produces special products under licence from Mr. Men, Royal Ascot, Warner Brothers Super Heroes, Scooby Doo, Beatrix Potter and The Snowman.

The Company’s first retail outlet was established in 2012 as a boutique biscuit icing café in Notting Hill, followed by a second café in 2014 in Battersea. The Biscuiteers Book of Iced Biscuits was published in 2010 with a second edition in 2012 and has sold 50k copies worldwide. A new publishing deal is currently being negotiated.

2.2 Awards and Recognition Biscuiteers were named as one of "Britain's most innovative, disruptive and creative young brands" in the Future 50 Awards and were a final nominee in the ‘Breakthrough Brand’ category at the Luxury Briefing Awards 2012. They were winners of ‘Best Food Gift Website’ in the Sheerluxe Online Shopping Awards in 2010, 2011 and 2013, and were winners of the Best of British category at the Good Web Guide Awards 2012.

Founders Harriet Hastings and Stevie Congdon were named in the 2013 Evening Standard’s Power 1000 list as two of London’s most influential foodies and tastemakers and Woman and Home identified Harriet as a trailblazing “W&H New Directions Hero” in the October 2013 edition of the magazine.

In 2014 Biscuiteers were winners of the Best Food and Drink category in the Licensing awards and Harriet was named as an Everywoman Ambassador in Retail, as well as Investec ‘Food and Drink Entrepreneur of the Year’ in 2014.

2.3 Production and Premises Biscuiteers hand make and hand ice all their products in their two London factories. The baking is carried out in the Camberwell facility and the icing and despatch are handled in Kennington. The offices are based above the icing hall in Kennington.

The Company also operates two retail outlets where they sell products over the counter to consumers, organise events including icing classes and parties, and where they can produce bespoke personalised

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 7 of 32

orders in their kitchens. Each retail outlet also houses a café although currently these represent only a small percentage of sales.

2.4 Products and Sales The overwhelming majority of Biscuiteers sales by product are hand iced biscuits, but the company also sells a small amount of cakes, gingerbread, cupcakes, chocolate and cheese. Other products and services include classes, parties, and various icing accessories including books.

In terms of sales channels online sales dominate at around 50% of total sales, with retail sales accounting for about 25% and fast growing corporate sales making up 15%. The balance is made up of ‘event’ and wholesale. Within the online business international orders are healthy and now account for around 5% of total sales.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 8 of 32

3 Market The perceived market for “gifting” in the UK runs to several £10 billions. This includes both the Gift Card (e.g. iTunes Voucher) and Greetings Card markets along with Gift Shops and some of the larger thematic segments like cut flowers (but does not include regular retail purchases which are actually gifts). It is more difficult to determine the size of more esoteric segments but research generally considers there are 2.5 million households in the UK capable of ‘premium’ spending and all of these would be potential targets for Biscuiteers. Looking specifically at gifting of hand baked hand iced biscuits there is no definitive research on the market size but it is safe to say that Biscuiteers is the clear market leader in the UK (and probably the world). What is more as the company continues to grow it appears to be penetrating other gifting markets such as flowers and chocolate. The flower market in a gifting sense is dominated by Interflora and the thousands of independent florists that sit under its banner. It is extremely fragmented and while a few larger retailers like Marks and Spencer, Debenhams and Waitrose are active flower sellers, it is by no means their main market. There are also a number of relatively new online retailers such as Bloom and Wild, Bunches.co.uk, FlowersDirect.co.uk and eFlowers.co.uk but nobody has come close to the brand recognition of Interflora. The Chocolate gifting market is smaller than the flower gifting market, but a few brands have been able to establish a credible presence: these include Hotel Chocolat (recently listed), Roccoco and Prestat. Smaller still is the market for other food related gifts such as cupcakes where Hummingbird and Lolas are the best known brands. Looking at the overall biscuit market the broadest measures suggest the UK produces more than 500 million kilos of biscuits each year with a market value of around £4bn. While this has little bearing on the ‘biscuit gifting’ it does show significant demand and is supported by a recent Mintel survey which confirmed that 92% of British consumers ate sweet biscuits each week. So although it is difficult to establish exact market sizes it is clear that the market is more than large enough to accommodate substantial growth at Biscuiteers, and in part it was the scale of the opportunity that enticed the Founders to establish Biscuiteers in 2007. More importantly it was perceived that gifting and food gifting in particular was an under exploited market particularly among more affluent middle aged consumers. The flower gifting market presented a very credible £40 price point and this has proven a useful benchmark for Biscuiteers. Although it is little changed over the last 8 years of recession and subsequent low inflation, it still provides a good balance between attractive gross margins for the seller and affordability for the buyer. If gardening became the ‘go to’ pastime of the 1990s and cycling of the 2000’s then baking is surely attracting the most new interest in recent years. On the one hand it could be argued that DIY biscuit making may undermine incumbent suppliers, but in the case of Biscuiteers and its bespoke hand made products the market attention has only served to stimulate demand. Indeed the success of TV programs like the Great British Bake Off have restored faith in quintessentially British pastimes and products and this plays directly to Biscuiteers brand strengths.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 9 of 32

As with any ‘gifting’ business there are countless opportunities to promote differentiated products and what is more the repetitive nature of many gifting opportunities (e.g. birthdays, Christmas) acts as a great catalyst for repeat business. Over the years Biscuiteers has developed specific products for all these recurring ‘special occasions’ and also for common but singular events (which include the ‘First Aid / Get Well Soon’ tin of biscuits). Another factor that has helped speed market penetration is the ability to personalise gifts – which is made very easy with the hand icing process. Although this flexibility may produce some scalability issues in the future for now it is broadening and deepening the interest in Biscuiteers products. In particular it has enabled the Company to produce a range of individually branded corporate gifts. It is also worth noting at this point that the ‘marketability’ of Biscuiteers products is as attractive as the size of its potential market. With an agile custom made product that looks extremely attractive in photographs it has been easy to seed attention across a wide spectrum of media interest. In particular social media has proven to be a very lucrative avenue for promoting the company’s products and extending brand awareness - Biscuiteers now has more than a million followers across various social media channels. Outside the UK there are a number of substantial markets, and in many of these sweet food products command a larger slice of disposable income. Americans and a number of Europeans are known for their sweet tooth, but culturally the Middle East and parts of Asia (Japan in particular), are likely to provide the biggest opportunities.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 10 of 32

4 Opportunity The opportunity for Biscuiteers is fairly straightforward. Having proven its ability to create a market leading brand for a highly desirable product at an attractive price point the Company is extremely well placed to scale significantly. Turnover of around £3,000,000 last year, represents a tiny fraction of the UK premium gifting market and a still smaller fraction of the international market.

The website has proven its ability to attract and retain customers for the online business and order values continue to increase. Online partnerships and new online outlets (such as the new specially curated shop within a shop due to launch at Amazon) will extend e-commerce activity. Retail sales also attract high net worth customers in local areas and turn them into ambassadors for the brand.

Corporate sales are growing both in terms of providing a gifting solution for individual executives but more importantly in terms of providing bespoke branded products to supplement customer service initiatives and events; these are especially popular at product launches.

While international sales represent only around 5% of total sales at present the increasing number of enquiries from potential international licensors demonstrates the latent demand for Biscuiteers products and brand. Overseas markets with a culturally sweet tooth should prove particularly lucrative.

Over the 7 years since inception sales have grown at around 20% per annum compounded. There is no reason to expect that unfunded organic growth cannot continue in the same vein which would see turnover increasing to more than £6.0 million in the year ending April 2020 with Operating Profits climbing to around £0.5 million.

However, with appropriate external funding invested to strengthen the corporate infrastructure and to accelerate growth the Directors believe that Turnover could reach £10.0 million with Operating Profits of more than £1.5 million by April 2020. The initial phase of investment as part of this plan is already yielding results in terms of production efficiencies and further improved customer acquisition.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 11 of 32

5 Products and Services Biscuiteers creates collections of themed hand iced biscuits, chocolates and cakes for every occasion. A premium gifting solution that offers same day dispatch for orders placed before 1pm and worldwide delivery 6 days a week.

Specifically focused on key gifting occasions like Valentine’s Day, Mother’s Day, Easter, Christmas, Halloween etc, Biscuiteers also offers a comprehensive range for personal occasions such as ‘Thank you’, ‘Happy Birthday’, ‘Get Well Soon’, etc to create a 365 day a year gifting model. With gifts ranging from a £8 Jolly Ginger up to a £40 tin of biscuits or £65 tin of chocolates, Biscuiteers aims to provide a witty, personalised and sophisticated approach to the gifting problem at a range of different price points.

5.1 Production Biscuiteers is a vertically integrated business manufacturing its own products and selling them through retail outlets and online. Over the years the manufacturing process has evolved to improve efficiency and scalability. The process is essentially split into two halves with “baking” in Camberwell and “icing” in Kennington from where the products are dispatched either to retailers or direct to customers. The value of the products is vested in the unique, handmade, artistic quality of the biscuits.

Looking forward the management team have identified a number of ways to further improve production efficiency and potentially significantly reduce production costs which would facilitate the launch of a diffusion range and a more aggressive entry into the wholesale marketplace.

5.1.1 Camberwell The site is composed of a 2,500 sq. ft. industrial bakery that focuses on baking. The rent for the site is £20,000 per annum with the lease ending in 2027 (and a review due in 2022). Aside from baking the site is also used for labelling and lining of tins and sorting chocolates in preparation for icing.

Over the next few months some initial icing stages will be moved to Camberwell focusing on iced outlining (initial lines of icing laid down on biscuits before flooding) which will leave Stannary responsible for the two more skilled aspects of hand icing and finishing of Biscuits.

Biscuiteers also rents two storage arches of 1,000 sq. ft. each for £10,000 each per annum with leases expiring in 2022 (and reviews in 2017).

5.1.2 Stannary The site amounts to 4,200 sq. ft. (including 800 sq. ft. of office space) for which the Company pays a gross £60,000 per annum (rent and rates). The lease runs until 2031 with the next review in 2018. [NB the office space is shared with Lettice Limited which makes a £16,000 contribution leaving Biscuiteers with a net bill of £44,000 per annum].

The Company is increasingly moving to separate skilled elements from unskilled to maximize the value of skilled icers, who often come from a creative arts background. As the business has grown it has been able to take on more icers on a full time basis increasing stability in the team. This core team is supplemented with a large part-time team on shift work.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 12 of 32

In the summer new icers are recruited and trained to prepare for the Christmas season. The long shelf life on the biscuits (6 months or more) enables Biscuiteers to build large Christmas stock over August/September/October and creates production space for bespoke Christmas orders in November. The addition of a vacuum packing machine has provided better shelf life and stock levels, again improving flexibility and increasing capacity.

5.2 Online Sales Biscuiteers started life as an online retailer selling bespoke iced biscuits to a discerning but fragmented market. By the time the brand launched in 2008 ‘the last mile’ block that had blighted so many early dotcom businesses had been resolved and the Company was able to easily and efficiently deliver finished products to consumers at short notice.

The strap line of “Why send flowers when you can send biscuits’ quickly attracted new customers, but the quality and consistency of the product kept people coming back for more. On top of this the shelf life of biscuits is good (especially compared to flowers) and unique packaging provided a brand legacy for every recipient.

Over the years the functionality of the website has continually evolved to help improve the user experience and to drive margins higher. It incorporates a number of features including basic gift messages, multiple address options (perfect for corporate sales), international delivery, date selection and range of delivery options.

The table below shows how the online business has prospered over the last few years in terms of customers and revenues. Although growth was slightly slower over 2016 the refurbished website is now generating much stronger returns and higher order values are being maintained.

E-Commerce 2011 2012 2013 2014 2015 2016 Year to end January Actual Actual Actual Actual Actual Actual

Active Customers 13,873 17,028 20,189 22,624 27,111 30,100 YoY growth % 23% 19% 12% 20% 11%

New Customers 11,247 12,520 13,841 14,412 16,490 17,911 YoY growth % 11% 11% 4% 14% 9%

Total Orders 26,183 31,677 34,804 39,949 48,457 52,425 YoY growth % 21% 10% 15% 21% 8%

Returning Customer Sales £ 138,659 257,716 370,033 454,803 580,785 674,214 YoY growth % 86% 44% 23% 28% 16%

New Customer Sales £ 434,594 540,887 591,245 591,594 654,444 781,068 YoY growth % 24% 9% 0% 11% 19%

Average Order Frequency 1.89 1.86 1.72 1.77 1.79 1.74 Average Order Value £ 21.89 25.21 27.62 26.96 25.98 27.49

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 13 of 32

5.3 Retail Sales Having established a successful model online the Directors decided that they could achieve higher levels of penetration in specific geographic sub-markets by opening retail outlets. Each shop unit has its own kitchen enabling some bespoke production to be done on site with the regular stock of biscuits and other products coming from the central kitchens.

‘High Street’ stores are an effective way of building brand, acquiring new customers and creating successful extensions of the business. This model has been successfully adopted by other businesses like Hotel Chocolat. They also allow for much deeper penetration of the customer base by offering a venue for events and parties. Biscuiteers two shops regularly host icing classes and icing parties for both children and adults.

5.3.1 Notting Hill Shop Covering approximately 850 sq. ft. in premises located at 194 Kensington Park Road the Notting Hill shop has 8 years of lease left with a review in 2016, current rent is £45,000 per annum.

This shop is the home of the original Biscuiteers Icing School offering 2 hour icing classes both during the day and in the evenings. The classes range from ‘Beginners’ to ‘Masterclasses’ and include a number of themed events (e.g. biscuits featuring characters from the Nutcracker ballet).

5.3.2 Battersea Shop Covering approximately 900 sq. ft. in premises located at 12 Northcote Road the Battersea shop has 9 years left on its lease. It is currently going through a rent review which is anticipated to lead to a rent of £70,000 per annum.

This shop is also home to a Biscuiteers Icing School offering the full range of icing classes and events. The main difference from Notting Hill is that a much larger floor area is given over to the café with café sales accounting for nearly 20% of turnover against less than 10% in Notting Hill.

5.4 Corporate Sales Biscuiteers has a very successful corporate bespoke business (which is anticipated to grow by 30% this year). The company supplies bespoke designs, logos designs and icing experiences, for a range of corporate marketing activities including product launches and media events. In addition to enhancing their marketing activities corporate clients also use Biscuiteers’ products for staff rewards and client gifting.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 14 of 32

The company operates a special loyalty scheme for PA’s to encourage them to use Biscuiteers as their preferred gifting service. The “Biscuits for Business” guide shows all the different bespoke options that can be created plus details of the unique packaging. Not only does corporate business create value in itself but also it is an excellent way to improve brand value and attract High Net Worth individuals as all Biscuiteers products carry the company branding.

The full range of corporate services has attracted a wealth of blue chip clients over the years including: Cartier, Mulberry, Mac Cosmetics, benefit, Heathrow T2, Lush, Talk PR, K-Swiss, Laura Ashley, Jo Malone, Harrods, Goldman Sachs, Claridges, Warner Bros, BBC, Investec, Liberty, Nestle, L’Oreal, Prada, Marmite, BAFTA, Virgin Media, Burberry, Rolls Royce, Net-a-porter, Swatch Watch, and Gameloft.

5.5 Wholesale The Wholesale business is relatively small but nonetheless an important component of the sales mix. Biscuiteers supplies most of the high end food outlets in London and beyond and this is a very useful tool to keep the brand front of mind. These retailers include Selfridges, Fortnum & Mason, Harrods, Conran and Fenwick.

Given the bespoke nature of the Company’s products it has not yet been possible to produce a lower priced product in sufficient scale or with sufficient margin to justify expanding this wholesale business to a broader mid market. However, the Directors see this as feasible over the longer term, especially if more of the manufacturing process could be automated.

5.6 Other Products and Sales

5.6.1 Licenced Products Biscuiteers has some very high profile licensed partnerships. These help to drive new customers to the website, provide opportunities for additional corporate sales (with licensors themselves) and drive PR and marketing

Although Biscuiteers gets many approaches to take on new licenses, it focuses on the ones that are clearly linked to a gifting occasion as these are the best sales drivers. These licences add unique additions to the product mix with marketing activity based around seasonal opportunities , key anniversary events (Beatrix Potter 150th anniversary is next year) and promotional opportunities around the licenses (e.g. Film launches).

The key partnerships are with: x Mr Men (the first license and winner of a food and drink licensing award) x Ascot Racecourse – seasonal licensed tin sold at the racecourse and online x Warner Brothers superheroes (Batman, Superman etc) and Scooby Doo x Beatrix Potter x The Snowman and The Snowdog x Great Ormond Street Hospital – children's biscuit collection which enables Biscuiteers to

support its charity of choice. There is also an option to donate online at the checkout.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 15 of 32

5.6.2 Gluten Free Launched in the Autumn of 2015 the 'Gluten Free' range has had a strong start. Currently available for just 6 bestselling tins, there are already plans to make it more widely available in the New Year to capitalise on strong demand.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 16 of 32

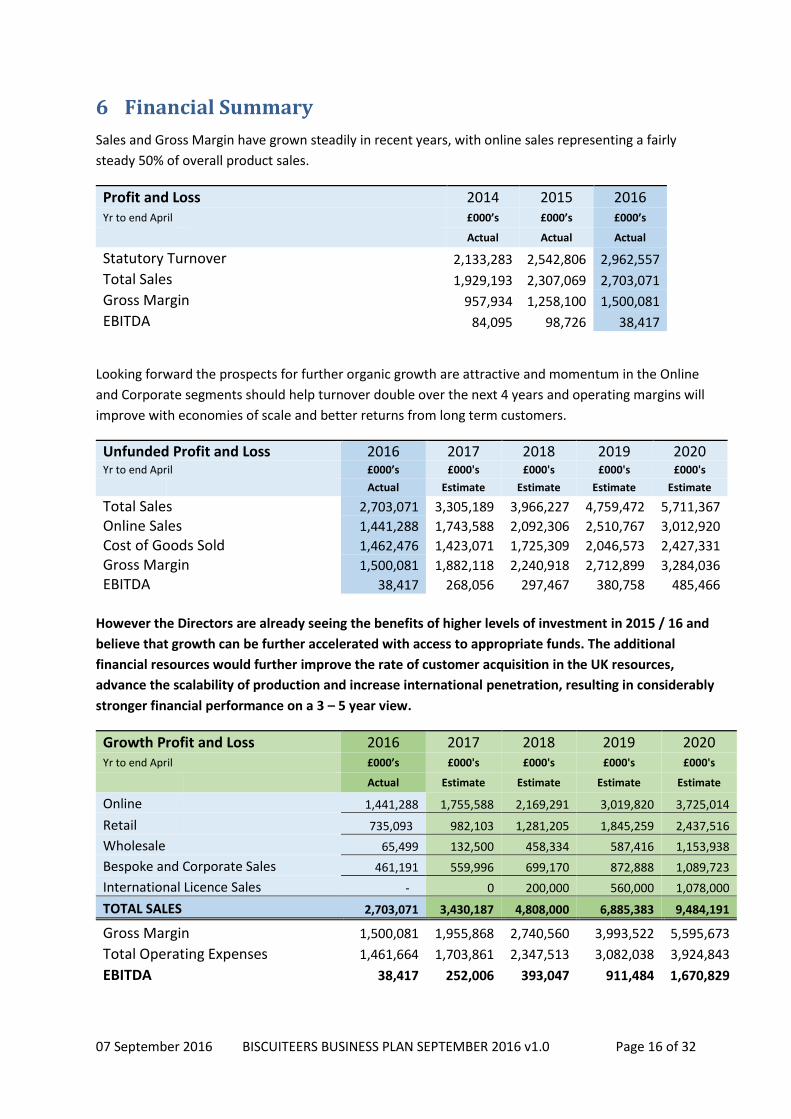

6 Financial Summary Sales and Gross Margin have grown steadily in recent years, with online sales representing a fairly steady 50% of overall product sales.

Profit and Loss 2014 2015 2016 Yr to end April £000’s £000’s £000’s

Actual Actual Actual

Statutory Turnover 2,133,283 2,542,806 2,962,557 Total Sales 1,929,193 2,307,069 2,703,071 Gross Margin 957,934 1,258,100 1,500,081 EBITDA 84,095 98,726 38,417

Looking forward the prospects for further organic growth are attractive and momentum in the Online and Corporate segments should help turnover double over the next 4 years and operating margins will improve with economies of scale and better returns from long term customers.

Unfunded Profit and Loss 2016 2017 2018 2019 2020 Yr to end April £000’s £000's £000's £000's £000's Actual Estimate Estimate Estimate Estimate

Total Sales 2,703,071 3,305,189 3,966,227 4,759,472 5,711,367 Online Sales 1,441,288 1,743,588 2,092,306 2,510,767 3,012,920 Cost of Goods Sold 1,462,476 1,423,071 1,725,309 2,046,573 2,427,331 Gross Margin 1,500,081 1,882,118 2,240,918 2,712,899 3,284,036 EBITDA 38,417 268,056 297,467 380,758 485,466

However the Directors are already seeing the benefits of higher levels of investment in 2015 / 16 and believe that growth can be further accelerated with access to appropriate funds. The additional financial resources would further improve the rate of customer acquisition in the UK resources, advance the scalability of production and increase international penetration, resulting in considerably stronger financial performance on a 3 – 5 year view.

Growth Profit and Loss 2016 2017 2018 2019 2020 Yr to end April £000’s £000's £000's £000's £000's

Actual Estimate Estimate Estimate Estimate

Online 1,441,288 1,755,588 2,169,291 3,019,820 3,725,014

Retail 735,093 982,103 1,281,205 1,845,259 2,437,516 Wholesale 65,499 132,500 458,334 587,416 1,153,938 Bespoke and Corporate Sales 461,191 559,996 699,170 872,888 1,089,723 International Licence Sales - 0 200,000 560,000 1,078,000

TOTAL SALES 2,703,071 3,430,187 4,808,000 6,885,383 9,484,191

Gross Margin 1,500,081 1,955,868 2,740,560 3,993,522 5,595,673 Total Operating Expenses 1,461,664 1,703,861 2,347,513 3,082,038 3,924,843 EBITDA 38,417 252,006 393,047 911,484 1,670,829

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 17 of 32

The ‘Growth’ model is predicated on a number of factors including opening new retail space during the second half of FY2016 and launching a new online shopping experience through Amazon; collectively new initiatives should help to add £500,000 of incremental sales this year and more than a £1,000,000 in 2017/18. This year would also see a 65% increase in marketing spending taking it to 8% of sales and additions to the senior management team. Additional retail and technology costs would largely be capitalised. A more detailed financial model is available in the Appendices, but the core assumption is that scale will not only generate production and distribution efficiencies but also spread fixed costs across a wider base thereby improving operating margins and cash generation.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 18 of 32

7 Management Currently Biscuiteers is run by two Executive Directors, supported by a part time Finance Director and one Non-Exec. The next tier of management includes operational staff in marketing, finance and production roles. This team has built the business from scratch but it is recognised that additions will need to be made to facilitate the next phase of growth (see 10.6)

7.1 Harriet Hastings – Founder and Managing Director Harriet founded Biscuiteers in 2007 after a successful career in marketing services and serving as a director of Lettice the party design and catering business established by her husband 30 years ago. She is currently responsible for overseeing Strategy, Sales, Marketing, Retail, Brand, Partnerships and HR.

Aside from Biscuiteers Harriet is also Managing Director of the Baileys Women's Prize for Fiction. She has worked on the prize since it was launched in 1996 initially running all marketing and PR under the original sponsor Orange. She took over as Managing Director of the prize in 2006, and negotiated a new sponsorship deal with Baileys who subsequently took over as headline sponsor in 2014.

Prior to establishing Biscuiteers Harriet was a Director of Powerhouse PR from 1993 which subsequently became MacLaurin Communications where she became Director of Consumer Technology. Following acquisition by Hatch Group she took over as Director of the Consumer Division until 2004 when Hatch became Trimedia.

Before her time in marketing services Harriet worked in publishing as Publicity and Marketing Director for Michael Joseph within Penguin Books and as Publicity Director for Pavilion Books.

7.2 Stevie Congdon – Co-Founder Stevie’s been in the catering and events industry for thirty years, beginning his journey serving satay off the back of a bicycle at cocktail parties around London. Eventually, he graduated to Cambridge May Balls, Mick Jagger’s birthday party and Claudia Schiffer’s wedding. Stevie was voted top Tastemaker and one of London’s most influential people in the Evening Standard Power 1000 in 2013.

Stevie Congdon is Co-Founder and Production Director at Biscuiteers, supervising all biscuit and cake production; and he is also responsible for finance and logistics. When he is not focusing on Biscuiteers he devotes his time to Lettice which is one of London’s leading catering and party organising businesses, where he is Founder and Managing Director.

7.3 James Kilpatrick – Finance Director James has worked within UK SME’s for nearly 20 years after beginning his career in finance and investment. He has worked as a consultant advising Biscuiteers for the last year and has recently been asked to take on the role of Finance Director. James’ works predominantly in the service sector with particular experience in retail, digital and media.

James has been a director of several growth companies notably ILG Digital, Opta Sports Data and KFS Group, all of which achieved successful exits for shareholders. He is currently a director of Kett Country Cottages, AFP Services, Craigie Mains, Starblu Holdings, Housing Hand and Luna Mae London.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 19 of 32

7.4 Non-Executive There is one Non-Executive Director, Bill Barlow, who represent 25% shareholder Deepwater Partnership and helps to co-ordinate the finance, budgeting and reporting functions. Bill is a director of Big Fish, the eminent London design agency to whom Biscuiteers outsource their design work including their iconic packaging.

7.5 New Hires It is anticipated that the management team will be supplemented with several new hires which would create a team with broader experience and allow for increased specialisation by senior managers, which will be important as the company accelerates its growth. The Board has already identified a Finance Director and a potential Operations Director and it is hoped that appointments can be confirmed once funding has been cleared.

The growth plan also anticipates the recruitment of key managers in the Retail and International areas although consultants will be used on an interim basis. Initially the focus of these roles would be to establish the most productive roll out strategy for Retail and International operations and then to implement the first stages of the agreed plan. As these areas of the business grow junior managers will be required to manage the ongoing operations.

It is also likely that more strength in depth will be added to the Marketing and Production areas, again this will be particularly relevant as scale demands increasingly specialised knowledge.

Finally the Board will be supplemented with the addition of another Non-Executive to help broaden the pool of experience and ensure appropriate governance for the wider shareholder base.

7.6 Organisation Chart In due course the Company will work towards a deeper organisation structure as shown below:

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 20 of 32

8 Competition As noted Biscuiteers has few if any direct competitors (i.e. handmade biscuit gifting businesses) but there are numerous businesses that share common aspects with Biscuiteers. So, rather than provide an in depth analysis of major competitors that do not exist this section of the plan will highlight a number of business that have some common characteristics. These should provide a useful indication of the opportunities that are available to Biscuiteers.

8.1 Food Gifting Although flower gifting has dominated certain sections of the gifting market, especially the delivered gift at the £40 price point, a number of food companies have entered the space in recent years. They are dominated by Chocolate businesses that in some case enjoy the ability to significantly personalise the gift. Of these Hotel Chocolat, founded in 1987, probably provides the best comparison in terms of growth potential, although it took well over 15 years before it was strong enough to accelerate its retail roll out.

Other more niche businesses like Rococo Chocolates, while arguably catering better for the bespoke market have failed to achieve any scale. Betty’s of Harrogate offer an attractive online gifting service but have not achieved the retail presence to match the likes of Hotel Chocolat.

Hotel Chocolat Rococo Chocolates

Prestat Hummingbird Bakery

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 21 of 32

Betty’s of Harrogate Regency Hampers

8.2 Founder Driven Brands Over the last couple of decades a number of niche businesses have been able to establish themselves as strong national brands despite starting out as limited product offerings from relatively few sales points. Amongst these Emma Bridgewater (Designer China), Brora (Cashmere Clothing), Rapha (Cycling Clothing) and Monica Vinader (Designer Jewellery) are some of the most celebrated.

Although none of these businesses are principally ‘gifting’ or ‘food’ businesses, like Biscuiteers they have developed from the focused idea of a founder who has recognised an opportunity to both exploit a gap in an existing market but also create a market of their own. Some have deployed catalogues, others have focused on retail outlets or digital marketing (usually a combination) but in each case proof of concept and early growth was funded by internal cash generation and the support of family and friends.

Also each of these businesses remains focused on its original product type and has benefitted from smart marketing helping to develop a very strong brand presence. It may be an exaggeration to still call them ‘market leaders in a market of one’ but their names and products remain very distinctive. They have also all ridden the ecommerce wave using the internet to close highly fragmented markets.

Emma Bridgewater Rapha

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 22 of 32

Brora Monica Vinader

8.3 Larger Scale Gifting Businesses Interflora was founded in the UK in 1923 and remains the predominant flower gifting business in the UK and indeed the world. Now listed on the US NASDAQ exchange with a market capitalisation exceeding $800 million (a P/E ratio of more than 25x), it trades in over 150 countries while retaining UK sales of more than £100 million.

Moonpig.com, which specialises in the online sale of personalised greeting cards was founded much more recently as the dotcom world crashed in 2000. It was acquired by PhotoBox in 2011 for £120 million, a little over 3x its turnover. Sales have continued to grow to more than £50 million in 2014.

Both these businesses demonstrate the ability to achieve significant financial returns based on people’s predisposition to buy premium gifts for others.

Interflora Moonpig

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 23 of 32

9 Risk Factors Biscuiteers is a manufacturer and multi-channel retailer and as such is vulnerable to a wide range of risk factors. At a macro level these risks include: x General Economic Conditions, especially in respect of consumer confidence and spending x Competition in all sales channels x Regulatory changes x Changing consumer preferences x Tightening labour markets x Legal challenges by disgruntled customers x Terrorism, Natural Disasters & Geo-political events x Internet connectivity More specifically Biscuiteers needs to be aware of the following risks: x Regulatory change in food retail x Availability and cost of finance x Availability and cost of skilled labour x Health backlash against high sugar content products x Failure to raise sufficient capital to fund growth x Failure to properly execute growth strategy x Failure to implement robust and connected IT infrastructure x Loss of key management / failure to recruit new management x Volatility in international markets (e.g. Middle East) x Data management and security x Procurement costs x Failure to find appropriate production locations x Failure to find appropriate retail locations

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 24 of 32

10 Expansion Plan and Funding Having established firm foundations for growth Biscuiteers now wishes to embark on a sustained expansion plan. This will require significant investment in a number of areas including production, marketing, website, operations, retail and international. Therefore the Directors are seeking to raise up to £1.2 million of additional capital to fund this investment program. The company would like to secure at least £500,000 in 2016 and would look to supplement this in 2017 or 2018.

The focus of this fund raising activity is to raise both equity finance through a share issue to individual investors. The Board is hoping to attract a range of investors including people that have experience in scaling e-commerce and or retail businesses that have a strong brand focus. The initial offer is for 9.5% of the equity for £550,000 which equates to a pre-money valuation of £5,250,000 with the hope that any further equity funding would be undertaken at a higher valuation.

During the course of the equity funding round the Board will enter discussions with banks to provide a revolving working capital facility of up to £500,000 to ensure that it is in a position to accelerate growth more quickly if demand exceeds expectations and to help cushion some of the seasonal cash flow fluctuations.

In respect of both the equity and debt funding options the Board will consider using Crowd Funding facilities to augment the process as they believe that this provides a cost effective route to investors and would also help to enhance brand penetration amongst affluent consumer households.

10.1 Production and Distribution As noted above mainstream production is undertaken across two principal locations in Camberwell and Kennington. Smart utilisation of this space will allow the company to increase production levels to provide for between £5 million and £6 million of sales, but some existing equipment will need to be replaced / modernised and some new equipment will need to be bought.

Most of the equipment investment will be focused on ovens, dryers, and packing tables and should amount to £80,000 over 18 months beginning in the second half of 2016. The company is also considering investing in vehicles / transport to improve efficiency between the production centres and distribution to the retail outlets with £70,000 earmarked over the same period, (although vehicle leasing remains an alternative to capex).

Thirdly the Board are looking at way to introduce some level of automation to the production process. Initially this may be through the introduction of some automated icing using robotic arms. This would enable the company to produce larger numbers of simple iced biscuits and in turn open the possibility of a diffusion range and even white labelling for supermarkets and corporate orders at a much lower price point but with comparable gross margins.

10.2 Website The existing website has developed organically over time and it works effectively both in terms of visibility through search and usability. However the legacy code makes it less agile and more difficult to edit. Also extracting data can be a little cumbersome which in turn makes it difficult to achieve clarity on customer analytics.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 25 of 32

Work has already begun on renovating the website and this is already bearing fruit in terms of SEO and conversion optimisation. There are further plans to address all areas of functionality and performance while retaining the current look and feel that has proven so successful. It will also help to improve integration with new logistics and other operations systems. The budget for the website component of the IT spending is at least £50,000 over two years.

10.3 Operations The Company currently operates several different IT infrastructures including the website, the Lightspeed till system in the retail shops, QuickBooks for the finance department, Magenta for the Website, Salesforce for Corporate sales and Exact Targeting for Email campaigns.

Looking forward the Company would like to improve operational integration and reduce the number of platforms it utilises to run the business, probably by utilising compatible systems from the Salesforce software suite. This will include investment in a new customer service system and an upgrade to the ECRM system. Incremental IT spending will amount to £100,000 in the first year of which up to £50,000 will be recurring.

10.4 International Over the years the Company has received a number of approaches from overseas businesses looking to licence the Biscuiteers model outside the UK. Given the bespoke production techniques, the intricate designs, and the ruthless protection of brand identity it has been too much of a stretch for the management team to exploit these opportunities to date.

However, given everything that has been learned from establishing its market leading position in the UK the Directors are keen to explore overseas expansion during the next few years. The Middle East and Asia appear to represent the best opportunities both in terms of the cultural fit (a taste for sweet foods and a propensity to gift) and also the level of interest being shown in the brand.

While these opportunities look attractive and could be extremely lucrative the Company does not currently have sufficient financial resources to attack these overseas markets in earnest, and more importantly it does not have senior people that can devote enough time to scoping and implementing the expansion.

Bearing these factors in mind it is the company’s intention to let any international partner fund the overseas venture supported by a senior Biscuiteers executive / consultant.

10.5 Staffing In each of the key investment areas outlined above there is a need for experienced management to support the current executive team. Although some of the main roles have been scoped, and indeed some hires have been made to strengthen the website team the most significant personnel have yet to be recruited.

While each of these will strengthen Biscuiteers infrastructure and promote growth, they will mostly add to central overheads rather than having a direct influence on sales. Consequently the company is

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 26 of 32

looking to initially finance these appointments from the proposed funding in advance of generating the revenue that they will support.

The Directors have identified the following roles as being important to the growth strategy:

10.5.1 Operations Director Establish a robust operational infrastructure (including Systems, IT and Data), manage Supplier and Partner relations, and oversee Premises and HR.

10.5.2 Senior Production Manager (already appointed) Focus on maintaining production efficiency as the business scales, organise purchasing, organise packaging, and prepare for longer term facility requirements and or additional shifts.

10.5.3 Retail Manager / Director Oversee and optimise the activity in the existing retail outlets; scope, plan and manage new outlets.

10.5.4 International Director Evaluate proposals from potential international partners, negotiate licences and oversee the implementation of licences and joint ventures.

10.5.5 Finance Director (already appointed) To work with the existing finance and non-executive team to plan for expansion and to assist with corporate and banking activity.

In aggregate the five posts listed above are likely to add more than £100,000 to the payroll in their first full year but £300,000 by year 3.

10.6 Retail The Company currently operates two well located retail outlets which not only make a positive return in their own right but also improve brand awareness and attract customers to the website for online purchases. From an operating point of view the holistic approach employed in the existing retail outlets providing a combination of retail product sales, café, classes, parties and bespoke order preparation has made good sense, but going forward the emphasis will initially be on smaller units (or pop-ups) which are more focussed on customer acquisition.

Initially the plan is to continue to focus retail space in London, targeting affluent areas like Covent Garden, Marylebone High Street, Primrose Hill, Canary Wharf or the City. Operating and staffing costs are fairly uniform across London but rent and rates will vary based on location and also length of tenure.

It is envisaged that one new site will be opened in 2016/17 and a further site later in 2017. The budget for establishing these locations is £250,000 per unit which will cover the cost of Rent Deposits, Equipment, Fixtures and Fittings, Refurbishment, Working Capital and Start-Up Losses.

10.7 Working Capital and Contingency Although Biscuiteers is a largely cash positive business, able to obtain supplies on credit and sell many of its products and services for cash up front, the Directors recognise that any growing business will consume cash and as such they are seeking a working capital facility of £300,000 to cover this and other contingencies.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 27 of 32

This means that Biscuiteers would like to raise up to £1,250,000 to fund its growth plans with a preferred split of £750,000 of equity and a debt facility of up to £500,000 (which should always be repayable within 4 years). Please see Appendix 9 for more information.

11 Summary History

Biscuiteers was founded by Harriet Hastings in 2007 to provide a witty and attractive alternative to gifting with flowers. The business draws from Harriet’s experience in both marketing services and food production, and focuses on outstanding design and exceptional brand development. Initially all sales were made online from www.biscuiteers.com but two Biscuiteer Boutiques have subsequently opened in 2012 and 2014.

The Company’s principal product remains its biscuits, all of which are hand baked and then individually hand iced to provide unique eye-catching gifts that taste great. Biscuiteers also sells Chocolates, Cakes and other personalised products, while offering icing classes and events such as children’s parties, and a wide range of services for its corporate clients.

Although it is easy to see Biscuiteers as an ‘online biscuit business’ its real focus is on the ‘gifting’ market, and its growth is driven by its strap line “Why send flowers when you can send Biscuiteers?” The brand has seen turnover grow at a compound rate of more than 20% per annum to more than £2.9million in the year to April 2016.

Market

It is somewhat difficult to establish the size of the Gifting Market in the UK, but it is certainly measured in 10s of billions of pounds. Gift Cards (e.g stores, iTunes etc) account for more than £5bn, Giftware (e.g. collectibles) account for more than £5bn, Greeting Cards about £2bn, Cut Flowers for gifts about £1bn and none of these categories include general retail sales of goods and services where the items are purchased for someone else.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 28 of 32

Opportunity

Across Biscuiteers different business lines there is an array of opportunities but most are concentrated on organic growth of its share in the gifting sector. ‘Middle England’ remains aspirational and incrementally more affluent which is empowering the premium gifting market. This encouraging environment is supported by a more stable economic and political environment which in turn is fuelling corporate buying.

On top of this the Biscuiteers brand and the idea of gifting biscuits and other foodstuffs is gathering pace. The internet remains the primary sales channel and the most effective route to a fragmented market, but retail / café sales are an increasingly important component (both in terms of revenue and customer acquisition). More selective corporate gifting (in the wake of recent bribery legislation) and an enthusiasm for distinctive brand partnerships are also fuelling growth.

Beyond these core opportunities the brand is seeing increasing interest from international licensors as quintessentially British produce is extremely popular in overseas markets and medium size privately owned food brands are among the UK’s most successful ‘exporters’.

Biscuiteers is also beginning to explore the possibility of broadening its product range to provide a greater variety of price points. Although the average price point is showing a rising trend it is also clear that lower priced biscuit cards are selling well. It may even be possible to improve production efficiency with a less bespoke diffusion range that would be much more scalable.

Products and Services

The principal driver for growth at Biscuiteers is the strength of its brand, which is aspirational, witty and widely appealing. Supported by outstanding creative talent, thematic design and a raft of popular licenced products the Company is the undisputed leader in the biscuit gifting market.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 29 of 32

Its sales are derived from six principal channels: Online, Retail, Corporate, Licence, Wholesale and International. They are made up of a range of products and services including Biscuits, Chocolates, Cakes, Icing Classes, Parties, Events, Café sales, Licenced Products and Publications.

Online sales of biscuits for gifts remains the Company’s principal source of revenue and continues to grow steadily year on year. However the increasing success of the retail outlets and corporate sales suggests that online sales will fall to less than half of total turnover in this financial year.

Within the e-commerce business existing customers now account for more than half of revenue but new customer order value also continues to increase and now adds more than £700,000 per annum. Biscuits are the dominant product accounting for 85% of online sales.

Financials

The Company has grown steadily since inception and sales this financial year will approach £3 million at a Gross Margin of nearly 60%. Historically cash has been reinvested in the business to accelerate growth and as fixed costs are more widely spread operating profit margins are beginning to improve.

From a Balance Sheet perspective Net Assets exceed £350,000 after accounting for loans and leases of just £120,000. The current Business Plan calls for the raising of additional Equity and Loan capital to fund further investment and growth.

Management

Harriet Hastings is the Founder and Managing Director of Biscuiteer Baking Company. She is responsible for overseeing Strategy, Sales, Marketing, Retail, Brand, Partnerships and HR. Harriet’s husband Stevie Congdon is her Co-Founder and Production Director. Day to day he runs one of London’s leading commercial catering business (Lettice) but he also supervises all biscuit and cake production at Biscuiteers, and is also responsible for finance and logistics. James Kilpatrick has recently been engaged as Finance Director.

There is one Non-Executive Director, Bill Barlow, who represents 25% shareholder Deepwater Partnership and helps to co-ordinate the finance, budgeting and reporting functions. The next tier of management includes operational staff in marketing, finance and production roles. Recently the team

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 30 of 32

has been boosted by the addition of a specialist digital marketer and a senior production manager with plans afoot to recruit an Operations Director and a more experienced Finance Director pending funding.

Competition

Although the UK gift market remains very competitive there are no direct competitors to Biscuiteers in handmade bespoke biscuit gifting. In terms of other edible gifts with a personalised touch Hotel Chocolat and Rococo Chocolates are the chocolate market leaders followed by Prestat; and Betty’s of Harrogate and Hummingbird Bakery lead the cake and cupcake markets.

Bigger gifting businesses such as Interflora and Moonpig also include some edible gifts, but they are a very small proportion of sales and targeted at lower price points.

Risks

As with any business that derives a huge proportion of sales online Biscuiteers is at the mercy of ‘connectivity’. It relies on the fact that its website is fully functional and accessible, and it also means its customers need to have good broadband access as well. Operating in a ‘premium market’ the Company relies on a reasonably healthy economy and adequate levels of disposable income at both the personal and corporate level.

In order to grow further Biscuiteers will need to access more skilled but affordable labour in both production and marketing, as well as having access to reliable and affordable distribution and logistics. One cannot ignore the threat from the ‘sugar police’ or an increase in similar health concerns (although biscuit sales have generally remained resilient over time).

Funding

Having prepared extensive Operational, Financial and Marketing plans as part of a strategic growth review the Company is now preparing to raise some external finance to help fund the implementation of the plans. In total this will amount to £1,250,000 and is likely to be made up of both equity and debt. Projections currently assume an initial equity funding tranche of £550,000, supplemented with a manageable drawdown facility of £500,000 to be available as needed and £200,000 of further equity in due course.

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 31 of 32

The additional funds will be applied in a number of areas including, marketing, the hiring of key staff including an Operations Director, a small increase in production capacity, more focused corporate and wholesale sales, establishment of further retail outlets, and improved data analytics to support customer acquisition and retention.

Once implemented the Directors intend to grow the business to a point in 4 to 5 years where a further (larger) funding round can be initiated to facilitate a move to more scalable production facilities, launch a lower priced wholesale range, and build a more substantial infrastructure for international operations.

Conclusion

The Biscuiteer Baking Company Limited is a dynamic growth business. It is a profitable and well established leader in its market and is well placed to develop into a much more substantial corporate entity. The Management Team has a clear plan to fund and facilitate growth both over the short and medium term.

The base goal is to generate £10 million of turnover and £1.5 million of profit in 4 years’ time, but the stretch target with a broader product range and international growth could be much higher.

***

For more information on Biscuiteers and the current funding opportunity please contact James Kilpatrick on 07768-076-876 or at [email protected]

07 September 2016 BISCUITEERS BUSINESS PLAN SEPTEMBER 2016 v1.0 Page 32 of 32

Appendices (under separate cover).

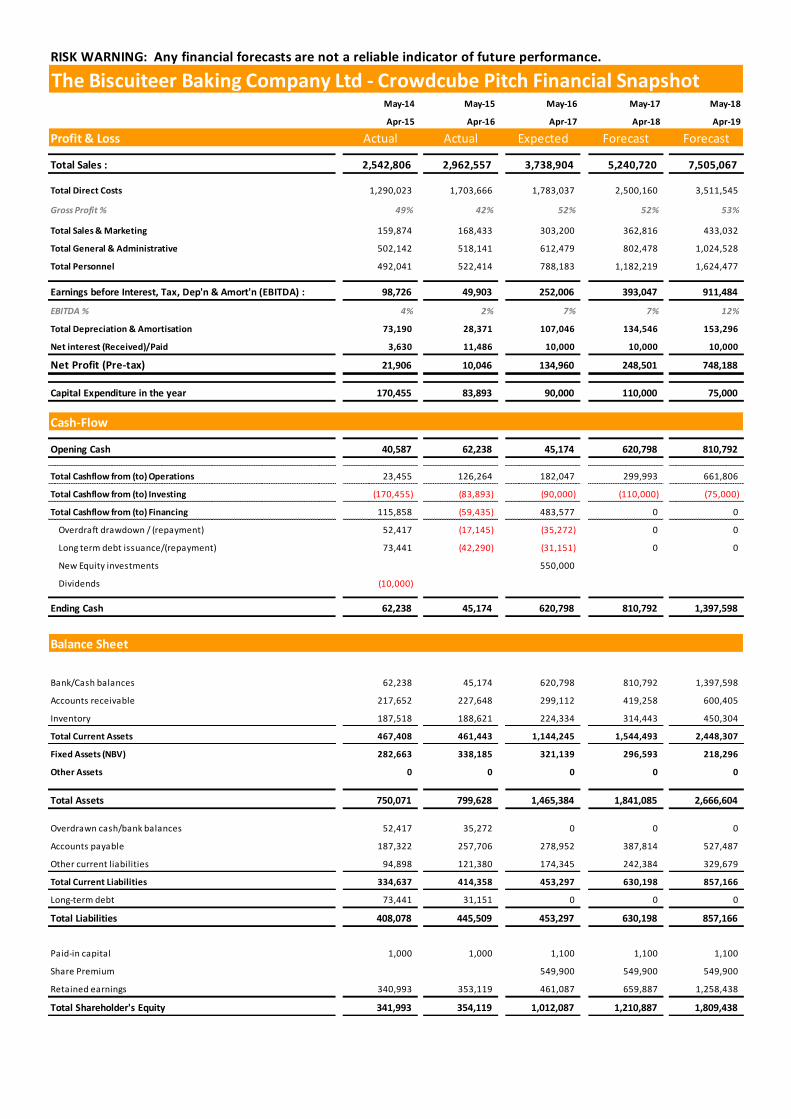

RISK WARNING: Any financial forecasts are not a reliable indicator of future performance.

May-14 May-15 May-16 May-17 May-18

Apr-15 Apr-16 Apr-17 Apr-18 Apr-19

Profit & Loss Actual Actual Expected Forecast Forecast

Total Sales : 2,542,806 2,962,557 3,738,904 5,240,720 7,505,067

Total Direct Costs 1,290,023 1,703,666 1,783,037 2,500,160 3,511,545

Gross Profit % 49% 42% 52% 52% 53%

Total Sales & Marketing 159,874 168,433 303,200 362,816 433,032

Total General & Administrative 502,142 518,141 612,479 802,478 1,024,528

Total Personnel 492,041 522,414 788,183 1,182,219 1,624,477

Earnings before Interest, Tax, Dep'n & Amort'n (EBITDA) : 98,726 49,903 252,006 393,047 911,484

EBITDA % 4% 2% 7% 7% 12%

Total Depreciation & Amortisation 73,190 28,371 107,046 134,546 153,296

Net interest (Received)/Paid 3,630 11,486 10,000 10,000 10,000

Net Profit (Pre-tax) 21,906 10,046 134,960 248,501 748,188

Capital Expenditure in the year 170,455 83,893 90,000 110,000 75,000

Cash-Flow

Opening Cash 40,587 62,238 45,174 620,798 810,792

Total Cashflow from (to) Operations 23,455 126,264 182,047 299,993 661,806

Total Cashflow from (to) Investing (170,455) (83,893) (90,000) (110,000) (75,000)

Total Cashflow from (to) Financing 115,858 (59,435) 483,577 0 0

Overdraft drawdown / (repayment) 52,417 (17,145) (35,272) 0 0

Long term debt issuance/(repayment) 73,441 (42,290) (31,151) 0 0

New Equity investments 550,000

Dividends (10,000)

Ending Cash 62,238 45,174 620,798 810,792 1,397,598

Balance Sheet

Bank/Cash balances 62,238 45,174 620,798 810,792 1,397,598

Accounts receivable 217,652 227,648 299,112 419,258 600,405

Inventory 187,518 188,621 224,334 314,443 450,304

Total Current Assets 467,408 461,443 1,144,245 1,544,493 2,448,307

Fixed Assets (NBV) 282,663 338,185 321,139 296,593 218,296

Other Assets 0 0 0 0 0

Total Assets 750,071 799,628 1,465,384 1,841,085 2,666,604

Overdrawn cash/bank balances 52,417 35,272 0 0 0

Accounts payable 187,322 257,706 278,952 387,814 527,487

Other current liabilities 94,898 121,380 174,345 242,384 329,679

Total Current Liabilities 334,637 414,358 453,297 630,198 857,166

Long-term debt 73,441 31,151 0 0 0

Total Liabilities 408,078 445,509 453,297 630,198 857,166

Paid-in capital 1,000 1,000 1,100 1,100 1,100

Share Premium 549,900 549,900 549,900

Retained earnings 340,993 353,119 461,087 659,887 1,258,438

Total Shareholder's Equity 341,993 354,119 1,012,087 1,210,887 1,809,438

The Biscuiteer Baking Company Ltd - Crowdcube Pitch Financial Snapshot

Management explanatory notes

1) SALES: Key sales driversa) The sale of hand baked biscuits through various distribution channels (53% online, 2% wholesale, 17% events/corporate and 27% retail)b) Existing customers - repeat business accounts for around half of sales and loyalty marketing push should improve order frequencyc) New customers - both individual and corporate driven by increased sales and marketing activity and the availability of new products

2) USE OF FUNDS: Outline how you plan to use the funds you raise on Crowdcube?a) Increase marketing activity to peak at around 9% of sales from around 6% as we still get positive marginal returns on our current spendingb) Increase investment in production efficiency to improve scalability and cut unit costs which will improve gross margins and open new price points.

3) EXPENSES AND PROFITABILITY: Please comment on your expense levels, gross and EBITDA marginsa) We have begun our investment program already which led to higher expenses (mostly staff) in 2015, but this is leading to better growth in 2016b) Gross margin dipped in 2015 but new production management has improved efficiency and we have started the new FY well ahead of budget

4) EXISTING DEBT OR EQUITY INVESTMENTS: Please outline the background to any existing debt or equity finance on the company balance sheeta) We have never raised equity capital before so all growth to date has been funded from historic profits and internal cash generationb) As of April 2016 there was £52K of outstanding bank loans and overdraft facilities. The term loan is expected to be repaid fully by year end through

operating cash flow. There was also £14K of outstanding hire purchase obligations. Management intends to secure a £500K line of credit post raise

5) CASH: Cash burn rate, Operational cashflow, when will you need to raise the next round?a) The company has been profitable every year since inception and has been cash generative.b) There are no immediate plans to raise any more invetsment as accelerated growth should further improve ability to generate cash

6) CREDITORS: Are you in any form of insolvency proceedings? Have you established any form of payment plans with creditors?a) No we are not in any form of insovency proceedingsb)

Biscuiteer Baking Company Ltd - Crowdcube Pitch : Important Information

The content of this financial information document (the "Financial Snapshot") by Biscuiteer Baking Company Ltd (the "Company") and the documents, comments and information contained within it (together the "Pitch") have been prepared by the Company and reviewed by Crowdcube for compliance with FCA regulations.

As part of the Pitch, the Financial Snapshot is approved as a financial promotion, and communicated, by Crowdcube Ventures Limited ("Crowdcube") in accordance with section 21 of the Financial Services and Markets Act 2000 ("the Act"). Crowdcube , is authorised and regulated by the Financial Conduct Authority under registered number 650205.

The Financial Snapshot and Pitch may contain forward looking statements and financial projections. Forecasts are not a relia ble indicator of future performance.

The Financial Snapshot and Pitch is not investment advice and Crowdcube makes no judgement or opinion regarding the Financial Snapshot or the likelihood of targets being achieved.

Potential investors are encouraged to "cross examine" the Company by interactive due diligence and use of the available online forums to bring the "wisdom of the crowd" to bear.

IMPORTANT - PLEASE READ CAREFULLY

The information contained in this Financial Snapshot is subject to the full risk warning and disclaimers contained on the Crowdcube website from time to time. It is only intended for Crowdcube members and should not be relied on for investment outside of Crowdcube.

The Pitch does not purport to be all-inclusive or necessarily to contain all the information that a prospective investor may desire in investigating the Company, and may be subject to updating, withdrawal, revision or amendment. No representation or warranty, express or implied, is or will be given by Crowdcube, the Company, their advisers or any of their respective directors, shareholders, partners or employees as to the accuracy or completeness of the Pitch or the information or opinions contained therein.

Any financial projections given are illustrative only and none of the projections or assumptions should be taken as promises on the part of the Company nor should they be taken as implying any indication, assurance or guarantee that those assumptions are correct or exhaustive. The Pitch contains forward-looking statements. These statements relate to, amongst other things, the Company’s future prospects, developments and business strategies. Forward-looking statements are identified by their use of terms and phrases such as “believe”, “could”, “envisage”, “estimate”, “intend”, “may”, “plan”, “will” or the neg ative of those, variations or comparable expressions, including references to assumptions.The forward-looking statements in this Pitch are based on current expectations and are subject to risks and uncertainties that could cause actual results to differ materially from those expressed or implied by those statements. If one or more of these risks or uncertainties materialises, or if underlying assumptions prove incorrect, the Company’s actual results may vary materially from those expected, estimated or projected. Given these risks and uncertainties, potential investors should not place any reliance on forward looking statements. These forward-looking statements are made only as at the date of the Pitch.

Each recipient of the Pitch must make their own independent assessment of the information provided by the Company and is recommended to seek independent advice on the contents hereof from an authorised person specialising in advising on investments of the kind in question. Neither the Company, Crowdcube nor any of their advisers, nor their respective directors, partners, representatives, agents, consultants or employees shall be liable for any direct, indirect or consequential loss or damage suffered by any person relying on statements or omissions from the Pitch and to the maximum extent permitted by law, all conditions, warranties and other terms which might be implied by statute, common law or the law of equity and any such liability are expressly excluded. The Pitch should not be construed as a recommendation to prospective investors by the Company or Crowdcube or any of their respective officers to invest in the Company, and does not form any commitment by the Company to proceed with an investment. The Company and Crowdcube reserve the right to terminate the procedure at any time and to terminate any discussions and negotiations with any prospective investors at any time and without giving any reason.