BIS Application Chapter two Forecasting. Forecasting Models 2 Forecasting is the process of...

38

BIS Application Chapter two Forecasting

-

Upload

dylan-jackson -

Category

Documents

-

view

225 -

download

3

Transcript of BIS Application Chapter two Forecasting. Forecasting Models 2 Forecasting is the process of...

BIS Application

Chapter two

Forecasting

Forecasting Models 2

Forecasting is the process of extrapolating the past into the future

Forecasting is something that organization have to do if they are to plan for future. Many forecasts attempt to use past date in order to identify short, medium or long term trends, and to use these patterns to project the current position into the future.

Backcasting: method of evaluating forecasting techniques by applying them to historical data and comparing the forecast to the actual data

Forecasting

Forecasting Models 3

Forecasting

Why Forecasting?

Characteristics of ForecastsForecasts are usually wrong or seldom correct

Aggregate forecasts are usually more accurate

Less accurate further into the future

Assumptions of Forecasting ModelsInformation (data) about the past is available

The pattern of the past will continue into the future.

Forecasting Models 4

The forecasting approach The forecasting approach to forecasting to forecasting •Starts with gathering and recording information about the situation

•Entering the data into the worksheet,

•Creating graphs

•The data and graphs are examined visually to get some understanding of the situation (judgmental phase)

•Developing hypotheses and models

•Trying alternative forecasting approaches and doing what if analysis to check if the resulting forecast fits the data

Forecasting Models 5

0

1

2

3

4

5

6

7

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

Devia

tio

ns

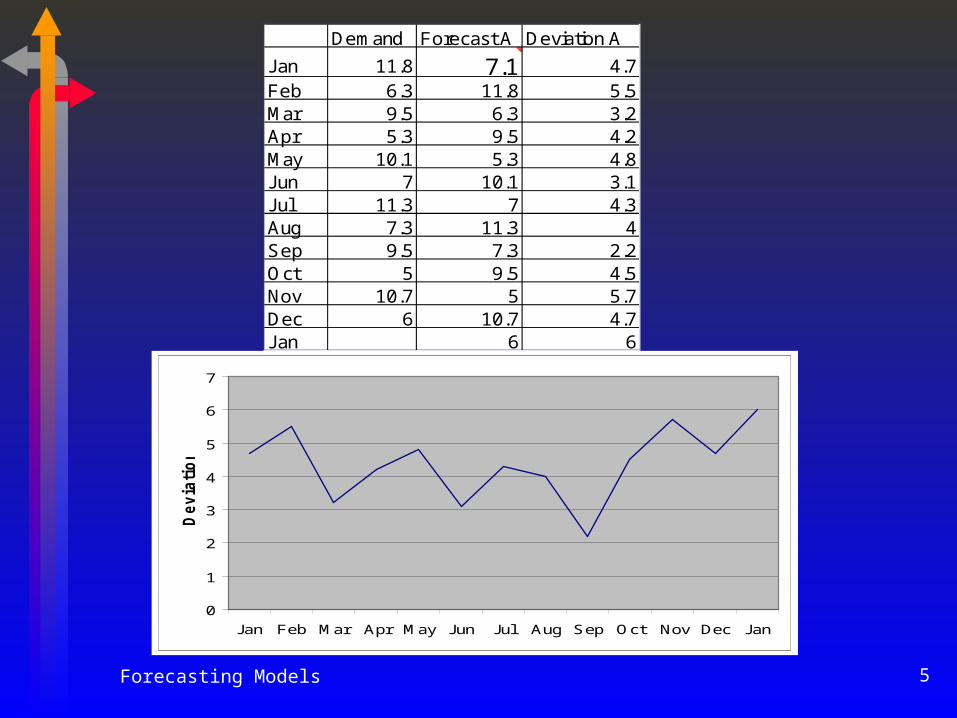

Demand Forecast A Deviation A

Jan 11.8 7.1 4.7Feb 6.3 11.8 5.5Mar 9.5 6.3 3.2Apr 5.3 9.5 4.2May 10.1 5.3 4.8Jun 7 10.1 3.1Jul 11.3 7 4.3Aug 7.3 11.3 4Sep 9.5 7.3 2.2Oct 5 9.5 4.5Nov 10.7 5 5.7Dec 6 10.7 4.7Jan 6 6

Forecasting Models 6

Forecasting Approaches1- Qualitative

Forecasting Forecasting based on experience,

judgment, and knowledge

2- Quantitative Forecasting

Forecasting based on data and models

Forecasting Models 7

Judgmental/Qualitative Quantitative models

Time Series Causal

Moving average

Exponential smoothing

Trend projection

Seasonal indexes

RegressionCurve fitting

Econometric

Market survey

Expert opinion

Decision conferencing

Data cleaning

Data adjustment

Environmental factors

Forecasting Approaches

Forecasting Models 8

Quantitative Forecasting

Time Series Models:

Time Series Model

Year 2000 Sales

Sales1999 Sales1998

Sales1997……

Casual Models:

Causal Model

Year 2000 Sales

Price PopulationAdvertising

……

Forecasting Models 9

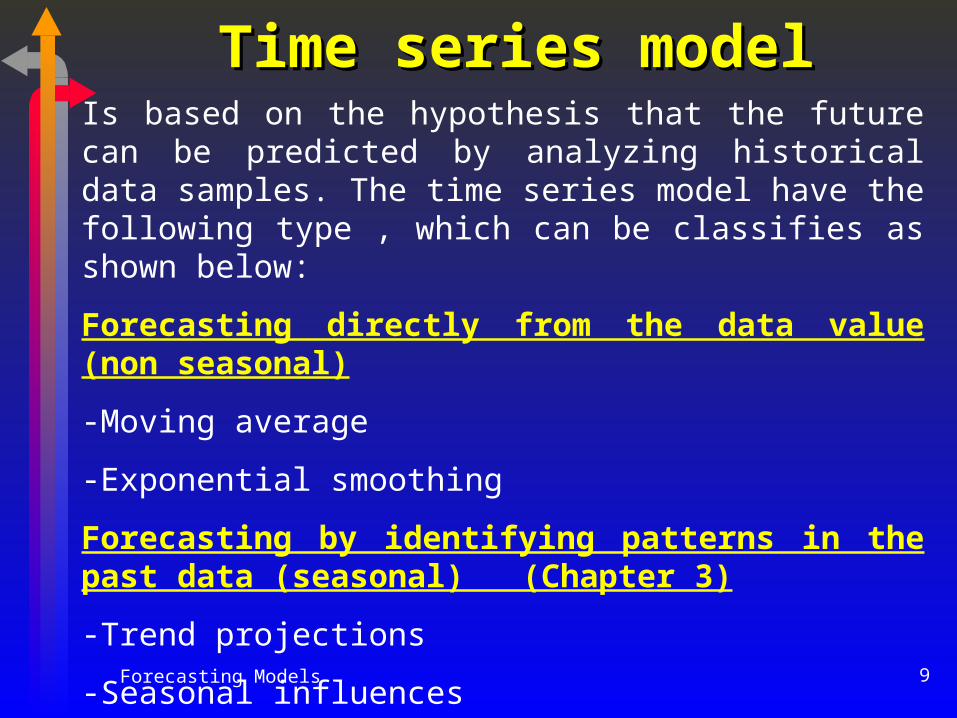

Is based on the hypothesis that the future can be predicted by analyzing historical data samples. The time series model have the following type , which can be classifies as shown below:

Forecasting directly from the data value (non seasonal)

-Moving average

-Exponential smoothing

Forecasting by identifying patterns in the past data (seasonal) (Chapter 3)

-Trend projections

-Seasonal influences

-Cyclical influences

Time series modelTime series model

Forecasting Models 10

The Time series model can be also classified as

Non-seasonal Model

Trend

Moving average

Exponential smoothing

Seasonal Model

Seasonal Decomposition

Cyclical influence

Time series modelTime series model

Forecasting Models 11

Causal Models (Chapter 3)

Causal forecasting seeks to identify specific cause-effect relationships that will influence the pattern of future data. Causes appear as independent variables, and effects as dependent , response variables in forecasting models.

Independent variable Dependent, response variable

Price demand

Decrease in population decrease in demand

Number of teenager demand for jeans

The issue is to determine the approximate functional relationships, the model, and the parameter of the model that relate the input(independent) and output(dependent) variables.

Forecasting Models 12

Causal Models (Chapter 3)

Regression analysis Curve Fitting: Simple Linear Regression One Independent Variable (X) is used to predict one

Dependent Variable (Y): Y = a + b X

Find the regression line with Excel Use Function:

a = INTERCEPT(Y range; X range)

b = SLOPE(Y range; X range) Use Solver Use Excel’s Tools | Data Analysis | Regression

Forecasting Models 13

Curve Fitting: Multiple RegressionCurve Fitting: Multiple RegressionTwo or more independent variables are used to

predict the dependent variable:

Y = b0 + b1X1 + b2X2 + … + bpXp

Use Excel’s Tools | Data Analysis | Regression

Causal Models (Chapter 3)

Forecasting Models 14

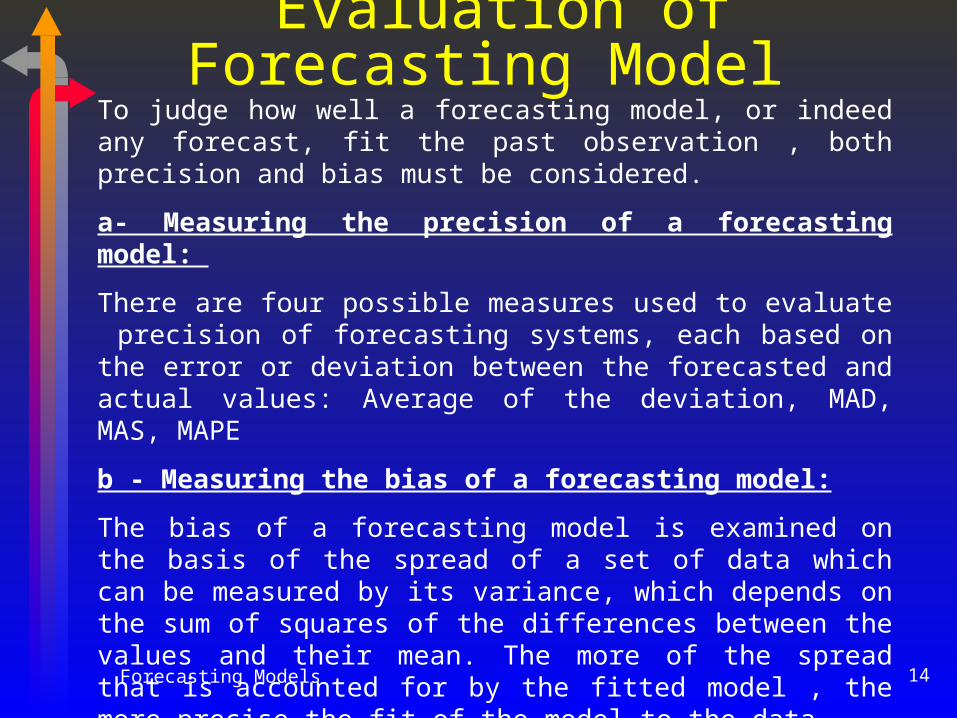

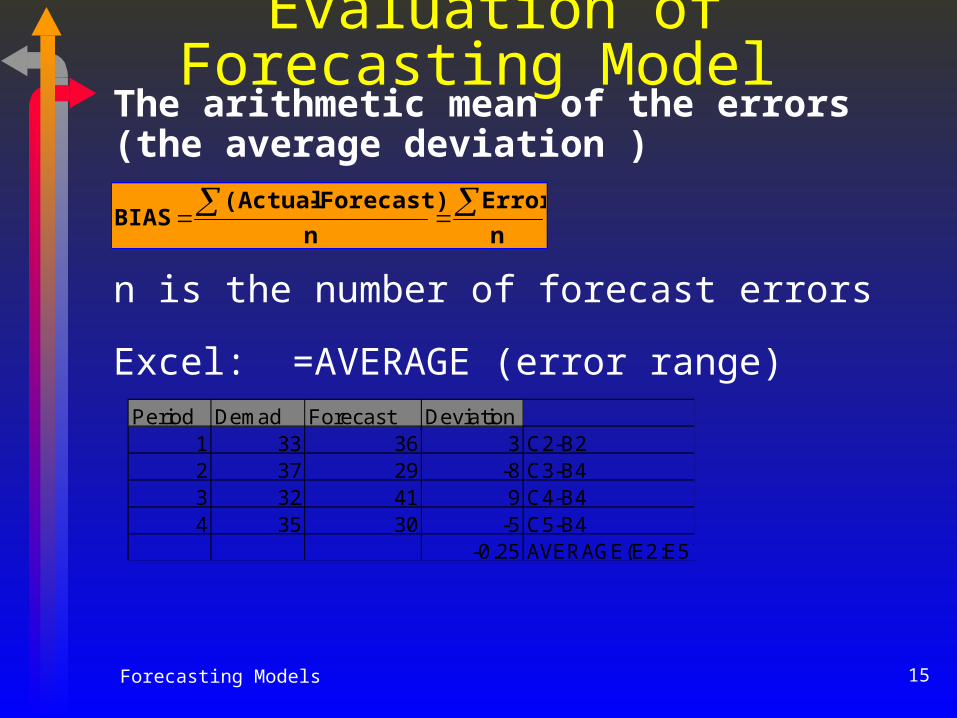

Evaluation of Forecasting Model To judge how well a forecasting model, or indeed any forecast, fit the past observation , both precision and bias must be considered.

a- Measuring the precision of a forecasting model:

There are four possible measures used to evaluate precision of forecasting systems, each based on the error or deviation between the forecasted and actual values: Average of the deviation, MAD, MAS, MAPE

b - Measuring the bias of a forecasting model:

The bias of a forecasting model is examined on the basis of the spread of a set of data which can be measured by its variance, which depends on the sum of squares of the differences between the values and their mean. The more of the spread that is accounted for by the fitted model , the more precise the fit of the model to the data.

R2 – used only for curve fitting model such as regression

Forecasting Models 15

Period Demad Forecast Deviation1 33 36 3 C2-B22 37 29 -8 C3-B43 32 41 9 C4-B44 35 30 -5 C5-B4

-0.25 AVERAGE(E2:E5)

The arithmetic mean of the errors (the average deviation )

n is the number of forecast errors

Excel: =AVERAGE (error range)

n

Error

n

Forecast) - (Actual BIAS

Evaluation of Forecasting Model

Forecasting Models 16

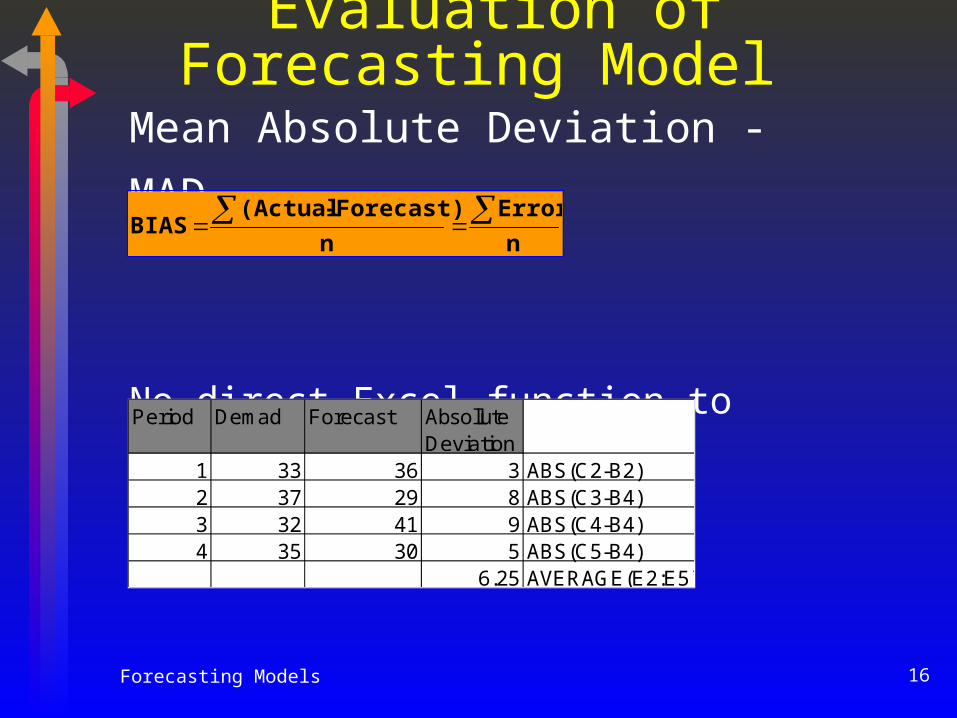

Mean Absolute Deviation - MAD

No direct Excel function to calculate MAD

n

Error

n

Forecast) - (Actual BIAS

Period Demad Forecast Absollute Deviation

1 33 36 3 ABS(C2-B2)2 37 29 8 ABS(C3-B4)3 32 41 9 ABS(C4-B4)4 35 30 5 ABS(C5-B4)

6.25 AVERAGE(E2:E5)

Evaluation of Forecasting Model

Forecasting Models 17

Mean Square Error - MSE

Excel: =SUMSQ(error range)/COUNT(error range)

n

(Error)

n

Forecast) - (Actual MSE

22

Evaluation of Forecasting Model

Period Demad Forecast Squared Deviation

1 33 36 9 (C2-B2) 2̂2 37 29 64 (C3-B3) 3̂3 32 41 81 (C4-B4) 4̂4 35 30 25 (C5-B5) 5̂

6.68954 SQRT(AVERAGE(E2:E5))

Forecasting Models 18

Mean Absolute Percentage Error - MAPE

nActual

|Forecast - Actual|

MAPE

%100*

Evaluation of Forecasting Model

Period Demad Forecast Squared Deviation

1 33 36 9.09% ABS((C2-B2)/B2)2 37 29 21.62% ABS((C3-B3)/B3)3 32 41 28.13% ABS((C4-B4)/B4)4 35 30 14.29% ABS((C5-B5)/B5)

18.28% AVERAGE(E2:E5)

Forecasting Models 19

Which of the measure of forecast accuracy should be used?

Straight average is not used because positive and negative deviations cancel out.

The most popular measures are MAD and MSE.

The problem with the MAD is that it varies according to how big the number are.

MSE is preferred because it is supported by theory, and because of its computational efficiency.

Forecasting Models 20

The ratio of MAD or MSE to the average demand which describes the relative percentage of error, may be used

MAPE is not often used.

In general, the lower the error measure (BIAS, MAD, MSE) or the higher the R2, the better the forecasting model

Which of the measure of forecast accuracy should be used?

Forecasting Models 21

As its discussed that neither MAD nor MSE gives an accurate indication of validity of forecast. Thus, judgment must be used. Raw data sample should always be subjected to managerial judgment, and analyzed and adjusted before formal quantitative techniques can be applied.

Good Fit – Bad Forecast

Forecasting Models 22

Outlier: may result from simple data entry errors, or they may be correct but atypical observed values (ex can occur in time periods when the product was just introduced or about to be phased out).

So experienced analyst are well aware that raw data sample may not be clear.

a- Dirty Data

0

10

20

30

4050

60

70

80

90

100

J an Feb Mar Apr May J un J ul Aug Sep Oct Nov Dec J an Feb

P

Demand data with an outlier

Forecasting Models 23

Before quantitative analysis is performed, the historical data sample needs to be examined from the point of view of cause-and-effect relationships.

A multitude of causes may affect the patterns in data sample :

- The data sample before a particular year may not be applicable because:

- Economic conditions have changed

- The product line was changed

- Data for a particular year may not be applicable because:

- There was an extraordinary marketing effort

- A natural disaster prevented demand from occurring

b- Causal data adjustment

Forecasting Models 24

The meaning of a :good fit” is subject to interpretation, so before a forecast is accepted for action, quantitative techniques must be augmented by such judgmental approaches as decision conferencing and expert consultations.

c- Illusory (misleading) patterns

Forecasting Models 25

To prepare a valid forecast, the following factors To prepare a valid forecast, the following factors that influence the forecasting model must be that influence the forecasting model must be examine:examine:

- Company actions

- Competitors actions

- Industry demand

- Market share

- Company sales

- Company costs

- Environmental factors

Time series forecasting model

Forecasting Models 27

Time Series Model Building

Historical data collection

Data plotting (time series plot)

Forecasting model building

Evaluation and selection of model

Forecasting with the final selected model

Forecasting Models 28

Components of A Time Series

Trend: long term overall up or down

movement

Seasonality: periodic pattern repeating

every year

Cycles: up & down movement repeating over

long time frame

Random Variations: random movements follow no

pattern

Forecasting Models 29

Components of A Time Series

Time

Trend

Randommovement

Time

Cycle

Time

Seasonalpattern

Dem

and

Time

Trend with seasonal pattern

Forecasting Models 30

-the forecast is the mean of the last n observation. The choice of n is up to the manager making the forecast

-If n is too large then the forecast is slow to respond to change

-If n is too small then the forecast will be over-influenced by chance variations

First : Forecasting directly from First : Forecasting directly from the data value : the data value : Moving averageMoving average

Forecasting Models 31

-This approach is considered as a “quick and dirty” approach for forecasting

-This approach can be used where a large number of forecasting needed to be made quickly, for example in a stock control system where next week’s demand for every item needs to be forecast

First : Forecasting directly First : Forecasting directly from the data value : from the data value : Moving Moving average average

Forecasting Models 32

Mounth Demand Moving Avarage Forecast

Oct 6Nov 5Dec 5Jan 1.63 5.33 AVARAGE(B3:B5)

Feb 1.95 3.88 AVARAGE(B4:B6)

Mar 7.5 2.86 AVARAGE(B5:B7)

Apr 2.49 3.69 AVARAGE(B6:B8)

May 6.18 3.98 AVARAGE(B7:B9)

Jun 9.18 5.39 =

Jul 5.24 5.95 =

Aug 8.3 6.87 =

Sep 2.72 7.57 =

Oct 7.43 5.42 =

Nov 7.49 6.15 =

Dec 9.58 5.88 =

Jan 8.02 8.17 =

Feb 4.13 8.36 =

0

2

4

6

8

10

12

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

Demand

Forecast

Forecasting Models 33

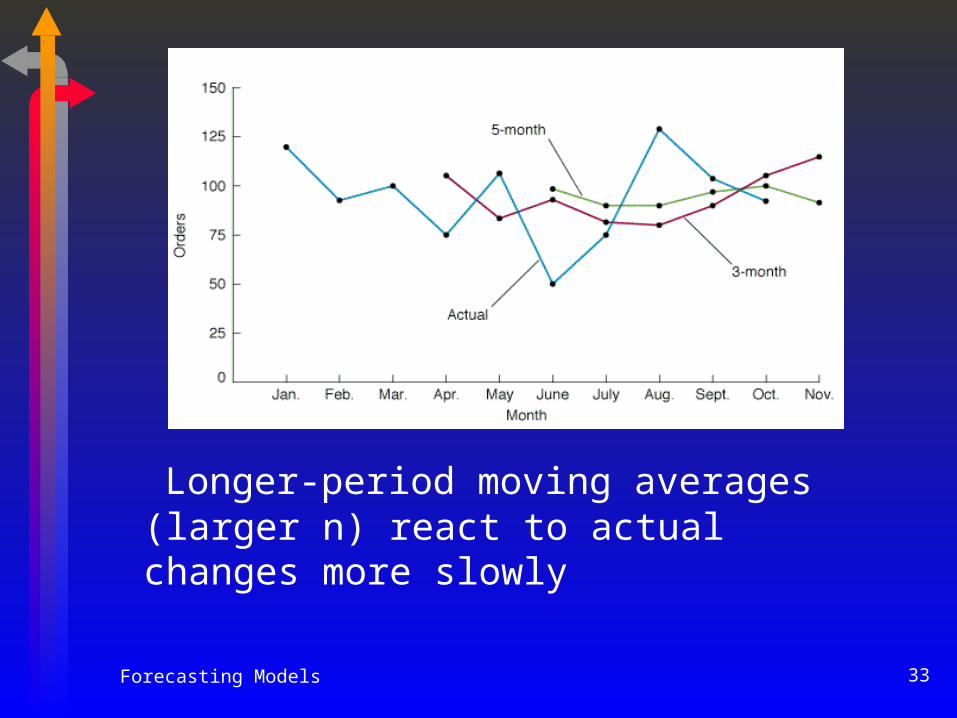

Longer-period moving averages (larger n) react to actual changes more slowly

Forecasting Models 34

-it gives weight to all past observations, in such a way that the most resent observation has the most influence on the forecast, and older observation always has less influence than the more recent one.

-It is only necessary to store two values (the last actual observation and the last forecast, plus the value of the smoothing constant) in order to make the next period’s forecast.

-Smoothing constant () the proportion of the different between the actual value and the forecast.

-F2 = F2 = *D1 +(1- *D1 +(1- )*F1)*F1

First : Forecasting directly First : Forecasting directly from the data value : from the data value : Exponentional smoothing Exponentional smoothing

Forecasting Models 35

•Alpha (smoothing constant) must set between 0 and 1. Normally the value of the smoothing constant is chosen to lie in the range 0.1 to 0.3.

•Typically, a value closer to 0 is used for demand that is changing slowly, and a value closer to 1 for demand that is changing more rapidly.

•There is no way to calculate F1 because each forecast is based on the previous forecasts.

First : Forecasting directly First : Forecasting directly from the data value : from the data value : Exponentional smoothing Exponentional smoothing

Forecasting Models 36

First : Forecasting directly First : Forecasting directly from the data value : from the data value : Exponential Exponential smoothing smoothing How to select smoothing constant

•Sensitivity analysis is an analysis used to test how sensitive the forecast is to the change in alpha or smoothing constant.

•A general rule for selecting alpha is to perform scenario analysis and pick the value that produces a reasonable value for the MAD and a forecast that is reasonably close to the actual demand.

Forecasting Models 37

Trend-Adjusted Exponential Trend-Adjusted Exponential SmoothingSmoothing

With trend-adjusted exponential smoothing, the trend is calculated and included in the forecast. This allows the forecast to be smoothed without losing the trend.

Trend-adjusted exponential smoothing requires two parameters: the alpha value used by exponential smoothing and beta value used to control how the trend component enters the model. Both values must be between 0 and 1.

The formula to calculate the forecast component is :

F2 = FiT1+ F2 = FiT1+ *(D1-FiT1)*(D1-FiT1)

The formula to calculate the trend component is

T2 = T1 + T2 = T1 + * * *(D1-FiT1) *(D1-FiT1)

Forecasting Models 38

Optimizing Trend-Adjust Exponential Optimizing Trend-Adjust Exponential SmoothingSmoothing

Optimizing alpha and beta with trend-adjusted exponential smoothing has a marginal impact.

To find the optimum value for alpha and beta:

First the original value of alpha and beta will be used in the forecasting model. Once the spreadsheet is ready, Solver is used to vary alpha and beta in order to minimize the MAD.