Bill Gross Investment Outlook Jan_03

of 5

-

Upload

brian-mcmorris -

Category

Documents

-

view

212 -

download

0

Transcript of Bill Gross Investment Outlook Jan_03

-

8/14/2019 Bill Gross Investment Outlook Jan_03

1/5

InvestmentOutlook BillGross

January 20

The Grand Scheme of Things

Im not a paranoid type of guy despitewhat you might be thinking: you andall of those other people that is. I believethe world is energized by self-interestand that when objectives coincide, then

families, companies, and countriesare conceived with a common bond.But self-interest dominates, stirs thepot, makes it next to impossible forconspiracies la John Le Carr to existother than on the pages of spy novels.Not that there arent spies out thereand that some of them arent watchingme right now. Theyre just not part of an organized plot. Its the coordinationthats the hard part, you see. Too manypieces to juggle behind closed doors.Still I believe in uncoordinated schemesand even uncoordinated grand schemes because self-interests, like the planets,sometimes fall into alignment. Now isone of those times. Now is the time fora global grand scheme.

The economic worlds disparateinterests are currently aligned becauseit has a common enemy: de ation.Born and bred out of the bowels of (1)globalization, (2) excessive buildup of good times debt, and (3) a demand-sti ing demographic imbalance, theworld is now threatened by de ationand its 21st century poster boy China.

And so the times are changing not viaa back room, cigar smoke laden plot, butstep-by-step, month-by-month, policy- by-policy. The pieces are beginning toform a coherent whole but there is no

giant, behind the scenes, puzzle maker only individual countries trying tosurvive and, if possible, thrive duringthese darker de ationary days.

As proof I submit a chronology of disparate, certainly unsyncopatedpolicy changes that began severalyears ago when the original cauldronof de ation Japan cut its interestrates to near absolute zero. Japan wasfollowed in January of 2001 by AlanGreenspan and the U.S. Fed, reducingshort-term yields from 6 to 1 % in just short of two years time. The ECBreluctantly joined the anti-de ationparty at about the same time, but attheir own pace, bringing their yieldsdown to a still high 2 %. On the scal

front Euroland, the U.S., and Japanall proceeded individually but withcommon alignment in the directionof large budget de cits all the betterto ght de ation. In addition, in theaftermath of 9/11, the U.S. selected a listof evil doer nations and targeted (notsurprisingly) the one with the large oilreserves, not the most imminent

-

8/14/2019 Bill Gross Investment Outlook Jan_03

2/5

Investment Outlook

January 2003

Source: PIMCO

70.0

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

115.0

120.0

M a r -

9 5

J u n - 9

5

S e p - 9

5

D e c - 9

5

M a r -

9 6

J u n - 9

6

S e p - 9

6

D e c - 9

6

M a r -

9 7

J u n - 9

7

S e p - 9

7

D e c - 9

7

M a r -

9 8

J u n - 9

8

S e p - 9

8

D e c - 9

8

M a r -

9 9

J u n - 9

9

S e p - 9

9

D e c - 9

9

M a r -

0 0

J u n - 0

0

S e p - 0

0

D e c - 0

0

M a r -

0 1

J u n - 0

1

S e p - 0

1

D e c - 0

1

M a r -

0 2

J u n - 0

2

S e p - 0

2

D e c - 0

2

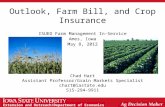

What Goes Up Must...

I n d e

x

Trade-Weighted Dollar Index

nuclear capability, as enemy numberone. A future attack would/will notonly stimulate the domestic economyvia military spending, but presumablyassure us of cheaper oil to ght thede ationary menace and stimulateeconomic growth. These disparateevents form no giant global conspiracy they arise from individual countriesdeciding that its interests are bestserved by policy reversals. The policieshowever have a common element eliminating the de ationary menacefrom their own economic homeground.

It is, to be sure, a grand scheme.

In recent months we have beeninformed of additional measures whichwould hopefully eliminate the D wordfrom our current economic lexicon:Bushs Republicans are convinced thatthe election gave them free rein to cuta myriad of taxes when in fact it was ahomeland security referendum. We will,however, have lower taxes in additionto internal security. Japan is about toappoint a new central bank governorwho may more aggressively re ate via

in ation targeting. Europe is gettingserious on structural reforms, as wellas considering further interest rate cuts.And of course Fed Governor Bernankehas delivered the coup de grce of anti-de ationary policies by threatening theuse of seldom if ever used maneuverssuch as buying Treasury and corporate bonds to keep the good times rolling.While in last monthsInvestmentOutlookI shouted that I believe them,its still not clear if ultimately they orany other government will succeed. Japan is proof that de ation once it take

hold is a behemoth to be reckoned with.

To this mix of potential re ationarypalliatives must be added one additional(and perhaps the one most dangerous)hole card for U.S. policymakers to play.I speak of the dollar and its potentialdepreciation, which if done graduallyand without causing investor ight would correct a number of globalimbalances that are holding downgrowth and in ation at the same time.Thats a big IF, however, and astuteobservers know it. Foreigners now hold

-

8/14/2019 Bill Gross Investment Outlook Jan_03

3/5

over $7 trillion of U.S. assets and theywill not take kindly to a devaluingof their investments. 13% of the U.S.stock market, 35% of the U.S. Treasurymarket, 23% of the U.S. corporate bondmarket, and 14% direct ownership inU.S. companies are now in the hands of foreign investors. Its a theater crowdedwith foreigners and if someone yellsFire, Feuer, or Kaji there could be arather crushing stampede for the exits.

Still, theres little doubt in my mind thata lower dollar might help to break up

several current policy logjams. Despitehope for future progress, both Japanand Euroland are dragging their heelson labor and bank related structuralreforms, which if implemented couldfree up underutilized capacity andpromote stronger growth. With botheconomies resting near the 0% growthline, a weaker dollar would make theirexports even less competitive, applyinga reform hammerlock that forces themto cry Uncle (Sam) much sooner. Inaddition, the ECB would be given thatmuch more leeway to bring yields closerto U.S. levels since a depreciating dollarand an appreciating Euro reduce futurein ationary pressures on the Continent.And a depreciating dollar of courseraises prices for U.S. imports, adding a

tint of in ation to the current mix andstemming de ationary momentum herein America.

A strong dollar policy, however, has been part of the U.S. economic mantra

ever since Robert Rubin rst utteredthe words in 1995 after succeedingLloyd Bentsen as Treasury Secretary.His presumed (although never directlystated) belief was that a strong dollarwould attract foreign investment and liftall market boats. Mr. Rubin succeeded beyond anyones most bubblish dreams, but now with the trade de cit at 6% of GDP, and our need to attract nearly 80%of all the worlds ongoing savings just tokeep the dollar at current levels, an endto the party is clearly in sight. Futureinvestment by foreigners in anything

with a $ sign attached is at risk. Inaddition, Rubins policy succeededso famously that our bonds and ourstocks now have lower yields and muchhigher P/Es than most other alternativemarkets. Rubin and his successors havepainted us into a corner from whicheither a falling dollar, depreciating

nancial markets, or both are nearlyinevitable.

Despite these negative rami cationsfor the U.S. currency and its nancialmarkets there is no doubt that this nal,last-gasp hole card in Uncle Sams handwould be played if deemed necessary.Incoming Treasury Secretary John Snowmay continue to mouth the mantra of a U.S. strong dollar policy but at some

point his lack of enthusiastic supportor perceived silence on the topic may be enough to cause a run on the bank.Besides, astute investors and holdersof dollar-denominated securities mustknow by now that public proclamation

-

8/14/2019 Bill Gross Investment Outlook Jan_03

4/5

840 Newport Center D

Suite

Newport Beach, CA 9

949.720

of the strong dollar policy was alwaysa ruse, that there was no necessity fora Wizard to hide within the palace of Oz whispering strong dollar, strongdollar. Our appreciating currency upuntil mid-2001 was a result of our roleas the worlds lone superpower andour perceived superiority in generatingproductivity and ultimately capitalgains. Now that Iraq, North Korea, andan anemic recovery are threatening thatimage on all fronts, the dollar is sinkingwith or without Rubin, Summers,ONeill, and Snow as Wizard of Oz

sound-alikes. If the dollar is to decline itwill sink of its own weight, not from thepronouncements or lack thereof fromWizards on high. Still it would be a kick in the pants for others to speed thingsup, to re ate at an accelerated pace inorder to avoid the Japanese malaiseof the past decade. Europe and Japanwould have to listen.

This nal playing card, however, must be viewed as just one of a multitude inan anti-de ationary deck that can andhas been dealt in recent months andyears by rather independently mindedglobal poker players. Japan, Europe,and the U.S. may be employing rathersimilar strategies at different times butthey do so independently in order to

defend their own economic interests.

Together, these disparate stepsrepresent a grand scheme to defeat thede ationary Dragon now represented by China but created by globalization,high debt, and ongoing demographicstilted against consumption. Investmentrami cations remain uncertain if only because the ultimate winnerremains in doubt. What I think I doknow however is that every weaponin the global arsenal will be red atsome future point to prevent decliningprices and a concomitant economiccollapse. With such resolve, and with

U.S. Treasury yields already near rock bottom, the odds favor bear marketTreasury trends if only because aslast months Genie observed whenyields cant go down they musteventually go up. The Grand Schemeof Things points towards re ationover the next several years and higherTreasury rates but the Dragon will notgo down easily.

William H. GrossManaging Director

-

8/14/2019 Bill Gross Investment Outlook Jan_03

5/5