Big Box Outlook - · PDF fileJones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 4...

24

JLL introduces its Big Box Velocity Index TM Choice, cost and competition influence real estate decisions for both landlords and tenants. JLL‘s new Big Box Velocity Index (‘BBVI’) attempts to plot that on the supply-demand-curve. Find out how U.S. markets stack-up to one another and where tenants have options. Demand for warehouses is relatively strong – especially for buildings larger than 500,000 square feet – and continues to spread across all size thresholds. Will this momentum persist? Big Box Outlook United States . Fall 2013

Transcript of Big Box Outlook - · PDF fileJones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 4...

JLL introduces its Big Box Velocity Index TM

Choice, cost and competition influence real estate decisions for both landlords and tenants. JLL‘s new Big Box Velocity Index (‘BBVI’) attempts to plot that on the supply-demand-curve. Find out how U.S. markets stack-up to one another and where tenants have options. Demand for warehouses is relatively strong – especially for buildings larger than 500,000 square feet – and continues to spread across all size thresholds. Will this momentum persist?

Big Box Outlook United States . Fall 2013

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 3

Key takeaways 4

Two views on the U.S. landscape 5

Big Box Velocity Index TM methodology 6

Dispersion by geography 7

Demand dispersion by industry 8

Demand dispersion by size 8

Supply dispersion by size 9

United States: large block accommodation, by region 10

Construction by region 11

Speculative construction by region 11

Big box leases, YTD 2013 12

E-commerce 21

Contact information 22

Table of contents

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 4

• As a way for us to easily compare industrial markets, JLL introduces its new Big Box Velocity Index. We compare available inventory and requirements across size segments to rate supply and demand in major logistics corridors.

• Big box space requirements (on a square footage basis) and counts are up from Spring 2013.

• While overall demand is up, demand in the nation’s most active market, the Inland Empire, is flat. With the IE accounting for 18 percent of the nation’s speculative construction, we are watching this market closely.

• Speculative construction is occurring in nearly all markets. In most markets, tenants with requirements in excess of 750,000 square feet will not find much choice with existing inventory and will need to pursue either pre-build or build-to-suit opportunities.

• Will speculative building cool in certain markets?

• E-commerce is growing as a demand driver: more than 10 percent of total U.S. construction is for e-commerce users.

• In the Northeast, demand is concentrated in the larger, mid-size warehouse segment – anecdotal evidence that small- to mid-market firms are getting back into the leasing market. Demand is also very active in larger segments – space needs in excess of one million square feet are heavily concentrated in the region.

• The big box segment also remains strong.

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 5

Two views on the U.S. landscape

“Even though speculative construction is increasing, tenants with larger requirements are committing to more build-to-suits because demand exceeds supply.”

“Underwriting criteria for big box space is making true spec construction difficult. Many developers need pre-commitments prior to groundbreaking of ‘inventory’ buildings. This means today’s BTS are less about special purpose buildings, or design-build-projects, and are really about kicking off semi-spec buildings.”

“Because real estate demand is such a ‘long lead’, much of 2012 and 2013-year-to-date’s activity has stemmed from 2011’s more robust economy. Absorption is a lagging indicator.”

“Supply and demand are balanced in most markets as it relates to new construction deliveries.”

“Today, this is generally true. However a few markets may be getting ahead of themselves. This can be said for the Inland Empire, where requirements are flat in the 500-749 ksf segment.”

“We’ve had 14 consecutive quarters of positive net absorption and it looks like rents will further increase in 2014.”

206 184 175 174 173

97

53

150 116 115 114

97 93 91 87 82 79 78 74 72 70 68 65 64 59 58 50 46

050

100150200250

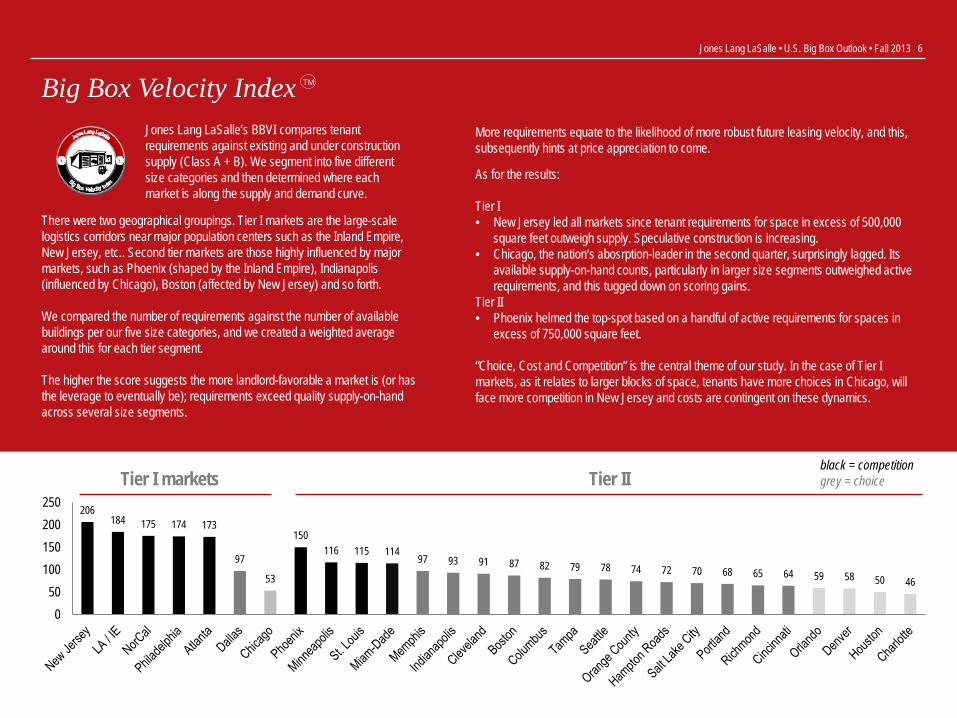

Big Box Velocity Index TM

There were two geographical groupings. Tier I markets are the large-scale logistics corridors near major population centers such as the Inland Empire, New Jersey, etc.. Second tier markets are those highly influenced by major markets, such as Phoenix (shaped by the Inland Empire), Indianapolis (influenced by Chicago), Boston (affected by New Jersey) and so forth. We compared the number of requirements against the number of available buildings per our five size categories, and we created a weighted average around this for each tier segment. The higher the score suggests the more landlord-favorable a market is (or has the leverage to eventually be); requirements exceed quality supply-on-hand across several size segments.

As for the results: Tier I • New Jersey led all markets since tenant requirements for space in excess of 500,000

square feet outweigh supply. Speculative construction is increasing. • Chicago, the nation‘s abosrption-leader in the second quarter, surprisingly lagged. Its

available supply-on-hand counts, particularly in larger size segments outweighed active requirements, and this tugged down on scoring gains.

Tier II • Phoenix helmed the top-spot based on a handful of active requirements for spaces in

excess of 750,000 square feet. “Choice, Cost and Competition” is the central theme of our study. In the case of Tier I markets, as it relates to larger blocks of space, tenants have more choices in Chicago, will face more competition in New Jersey and costs are contingent on these dynamics.

Tier I markets Tier II black = competition grey = choice

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 6

Jones Lang LaSalle‘s BBVI compares tenant requirements against existing and under construction supply (Class A + B). We segment into five different size categories and then determined where each market is along the supply and demand curve.

More requirements equate to the likelihood of more robust future leasing velocity, and this, subsequently hints at price appreciation to come.

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 7

Where is demand?

30,000,000+ s.f.

10,000,000 s.f. to 29,999,999 s.f.

500,000 s.f. to 9,999,999 s.f.

Activity continues to shift to the east because deals in the Mid-West have taken place

• The Northeast is leading the country in terms of active tenant requirements, outpacing the Mid-West (which now ranks second, by square footage). The top three industries shopping the market include: e-commerce retailers, traditional retailers and consumer non-durables. On a square footage basis, the volume of requirements increased 43 percent from our last report to serve the region’s 55-million-strong population. In New Jersey, Amazon, Williams-Sonoma and Tory Birch already signed notable deals in excess of 500,000 square feet this year.

• Requirements in the Mid-West are down by 26 percent; a function of robust leasing activity in quarters past. E-commerce retailers presently lead all other industries. In Chicago, three size segments are especially active: 50,000 to 150,000 square feet, 250,000 to 399,999 square feet and 800,000 square feet; e-tailers are especially active in the latter segment.

• Demand in the Southeast is relatively unchanged. Consumer non-durables and food & beverage tenants presently lead all requirements. Logistics & distribution companies have been active in recent quarters.

• Southern California is also generally flat with regards to tenant requirements. Notable big-box leases were signed in recent quarters and there has been a progressive tapering off of needs in the 500,000 to 749,000-square-foot segment. Year-to-date, 13 leases for space in excess of 500,000 square feet were inked.

‘Mega-box’ still reigns, but….

Substantial leasing volume of larger facilities across the U.S. has pushed demand to smaller size segments as the supply of quality spaces has dwindled, user competition has escalated and rents have increased. It has also encouraged small and mid-cap distributors to re-enter the market and take space before values appreciate.

All of this speaks to why construction is on the rise.

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 8

Who will lease space?

Five of the top 6 industries prefer the Northeast

• Food & beverage is active.

• Retailer (e-commerce) users are congregating to the Northeast and Mid-West.

• Logistics & distribution requirements are generally spread across regions, with a West Coast emphasis. This is not surprising given the number of cargo seaports from Southern California to Seattle.

• Consumer non-durables retain a pronounced presence.

• Manufacturing has enjoyed gains in recent months, and on-shoring moves will help future momentum.

Retail is the true king

• Total retail requirements account for a third of total demand—most of which is concentrated in the Northeast. Vacancies are expected to decline in markets such as New Jersey as absorption gains occur.

Demand dispersion by industry

Widespread, except…(by square footage)

• Demand for 250,000 to 499,999 square feet is nearly on par with requirements for spaces in excess of 1.0 million square feet. This speaks to a resurgence in activity from mid to larger distributors, and they want modern space: 31 percent of the nation’s speculative development is in this size segment.

• Generally, tenant requirements are spread out across size segments, with the exception of the 750,000 to 999,000-square-foot grouping. Corporate occupiers seem to prefer this segment for consolidation moves, but the economy is on the mend and the majority of such moves have already occurred. The handful of tenants with requirements in this segment are likely to pursue build-to-suit options; the same can be said for those with needs in excess of one million square feet.

Counts favor smaller size segments

• Food & beverage, logistics & distribution, consumer non-durables, 3PLs and manufacturing companies favor space under 500,000 square feet; more than 70 percent of their respective requirements fit into this size segment.

• Retailer (e-commerce) users are the most diverse as it relates to space needs. Smaller private companies are shopping product under 250,000 square feet, while major retailers are opening mega fulfillment centers larger than one million square feet near key population centers, with mid-size locations in secondary markets.

Demand is spreading into smaller buildings Demand dispersion by size

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 9

100-249 ksf 1,261

250-499 ksf 414

500-749 ksf 124

750-999 ksf 28

1 msf+ 9

By count

By counts (includes existing and under construction Class A and B space)

Mid-West and Northeast to feel the appreciation

Percent of supply on hand, by region Size Northwest Southern California Southwest Mountain Mid-West Northeast Southeast Total Count

100-249 ksf 7% 12% 13% 4% 25% 20% 19% 1,261250-499 ksf 7% 13% 16% 3% 23% 19% 21% 414500-749 ksf 4% 11% 19% 3% 29% 15% 19% 124750-999 ksf 0% 11% 14% 0% 36% 14% 25% 281 msf+ 22% 0% 11% 0% 33% 22% 11% 9

Putting two and two together* • The 100,000 to 249,999-square-foot segment clearly has the most availabilities and is chiefly

based in the Mid-West and Northeast.

• Based on demand needs, manufacturing, 3PLs, logistics & distribution and consumer non-durables are actively shopping spaces in this segment.

• Consumer non-durables, 3PLs and manufacturing companies have the most requirements in the Northeast, meaning this size segment is set to appreciate in the region.

• The same will occur, likely at a slower pace, for 500,000 to 749,999-square-foot product in the Mid-West where e-commerce retailers are pursuing space.

• Available supply counts in the 750,000 to 999,999-square-foot range are high in the Mid-West and Southeast and user demand has slowed after notables leases from Williams-Sonoma, Pactiv and Navarre Corporation. Rental rates will likely remain flat, given the diminutive pool of existing requirements.

• E-commerce users also want spaces in excess of one million square feet in the Northeast and Mid-West; available blocks (particularly cold shell, A-space) should fare well.

* see the next page for all data tables

Supply dispersion by size

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 10

All markets have space to burn as it relates to the 100,000 to 249,999-square-foot segment. In larger size segments, active requirements will help lower vacancies in the Mid-West, Northeast and Southeast – regions whose vacancies presently exceed West Coast markets.

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

350

100-

249k

sf

250-

499k

sf

500-

749k

sf

750-

999k

sf

>1ms

f

100-

249k

sf

250-

499k

sf

500-

749k

sf

750-

999k

sf

>1ms

f

100-

249k

sf

250-

499k

sf

500-

749k

sf

750-

999k

sf

>1ms

f

100-

249k

sf

250-

499k

sf

500-

749k

sf

750-

999k

sf

>1ms

f

100-

249k

sf

250-

499k

sf

500-

749k

sf

750-

999k

sf

>1ms

f

100-

249k

sf

250-

499k

sf

500-

749k

sf

750-

999k

sf

>1ms

f

100-

249k

sf

250-

499k

sf

500-

749k

sf

750-

999k

sf

>1ms

f

Northwest Southern California Mountain Southwest Mid-West Northeast Southeast

Available blocks of Class A and B space (existing and under construction) Active requirements

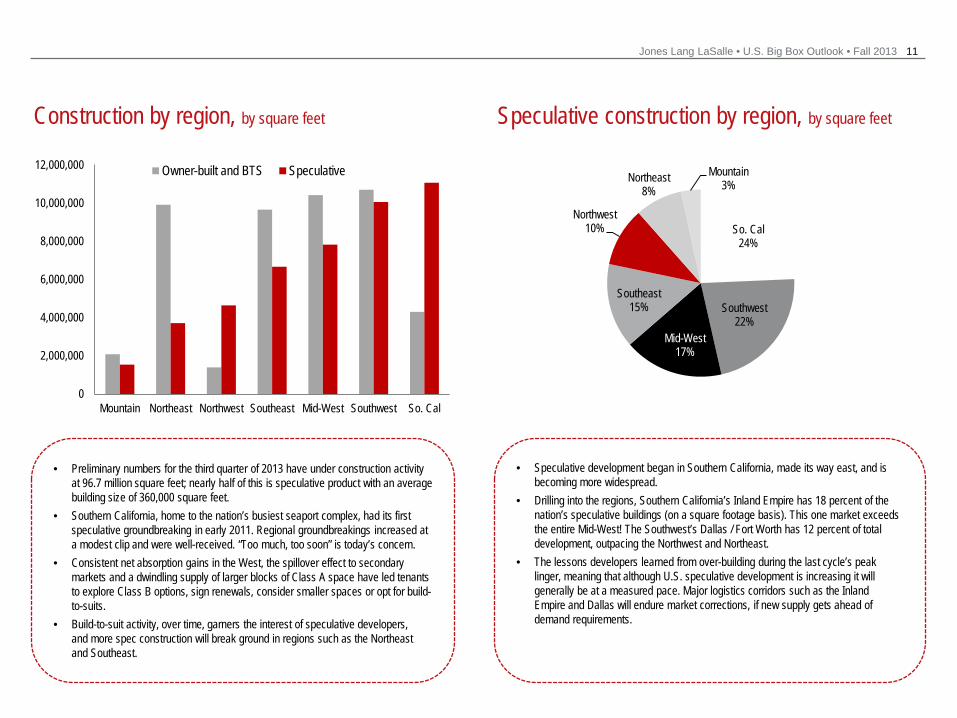

Focus on… United States: large block accommodation, by region

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 11

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

Mountain Northeast Northwest Southeast Mid-West Southwest So. Cal

Owner-built and BTS Speculative

So. Cal 24%

Southwest 22%

Mid-West 17%

Southeast 15%

Northwest 10%

Northeast 8%

Mountain 3%

Construction by region, by square feet Speculative construction by region, by square feet

• Preliminary numbers for the third quarter of 2013 have under construction activity at 96.7 million square feet; nearly half of this is speculative product with an average building size of 360,000 square feet.

• Southern California, home to the nation’s busiest seaport complex, had its first speculative groundbreaking in early 2011. Regional groundbreakings increased at a modest clip and were well-received. “Too much, too soon” is today’s concern.

• Consistent net absorption gains in the West, the spillover effect to secondary markets and a dwindling supply of larger blocks of Class A space have led tenants to explore Class B options, sign renewals, consider smaller spaces or opt for build-to-suits.

• Build-to-suit activity, over time, garners the interest of speculative developers, and more spec construction will break ground in regions such as the Northeast and Southeast.

• Speculative development began in Southern California, made its way east, and is becoming more widespread.

• Drilling into the regions, Southern California’s Inland Empire has 18 percent of the nation’s speculative buildings (on a square footage basis). This one market exceeds the entire Mid-West! The Southwest’s Dallas / Fort Worth has 12 percent of total development, outpacing the Northwest and Northeast.

• The lessons developers learned from over-building during the last cycle’s peak linger, meaning that although U.S. speculative development is increasing it will generally be at a measured pace. Major logistics corridors such as the Inland Empire and Dallas will endure market corrections, if new supply gets ahead of demand requirements.

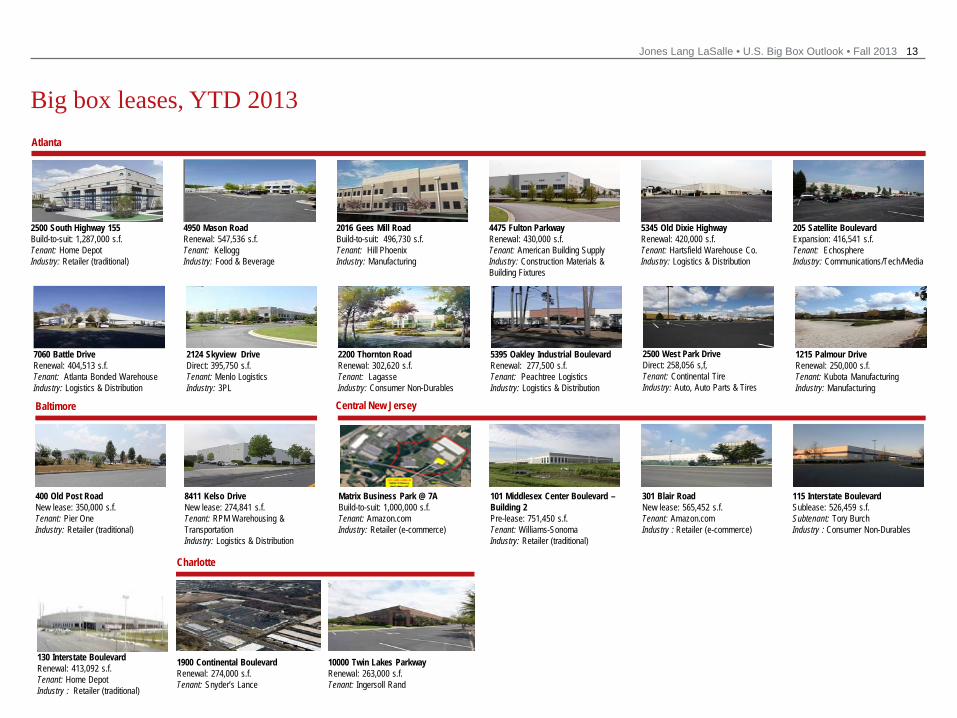

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 12

Big box leases, YTD 2013

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 13

7060 Battle Drive Renewal: 404,513 s.f. Tenant: Atlanta Bonded Warehouse Industry: Logistics & Distribution

2124 Skyview Drive Direct: 395,750 s.f. Tenant: Menlo Logistics Industry: 3PL

2200 Thornton Road Renewal: 302,620 s.f. Tenant: Lagasse Industry: Consumer Non-Durables

5395 Oakley Industrial Boulevard Renewal: 277,500 s.f. Tenant: Peachtree Logistics Industry: Logistics & Distribution

2500 West Park Drive Direct: 258,056 s,f, Tenant: Continental Tire Industry: Auto, Auto Parts & Tires

1215 Palmour Drive Renewal: 250,000 s.f. Tenant: Kubota Manufacturing Industry: Manufacturing

Big box leases, YTD 2013 Atlanta

4950 Mason Road Renewal: 547,536 s.f. Tenant: Kellogg Industry: Food & Beverage

2500 South Highway 155 Build-to-suit: 1,287,000 s.f. Tenant: Home Depot Industry: Retailer (traditional)

2016 Gees Mill Road Build-to-suit: 496,730 s.f. Tenant: Hill Phoenix Industry: Manufacturing

205 Satellite Boulevard Expansion: 416,541 s.f. Tenant: Echosphere Industry: Communications/Tech/Media

4475 Fulton Parkway Renewal: 430,000 s.f. Tenant: American Building Supply Industry: Construction Materials & Building Fixtures

5345 Old Dixie Highway Renewal: 420,000 s.f. Tenant: Hartsfield Warehouse Co. Industry: Logistics & Distribution

Baltimore

8411 Kelso Drive New lease: 274,841 s.f. Tenant: RPM Warehousing & Transportation Industry: Logistics & Distribution

400 Old Post Road New lease: 350,000 s.f. Tenant: Pier One Industry: Retailer (traditional)

Matrix Business Park @ 7A Build-to-suit: 1,000,000 s.f. Tenant: Amazon.com Industry: Retailer (e-commerce)

101 Middlesex Center Boulevard – Building 2 Pre-lease: 751,450 s.f. Tenant: Williams-Sonoma Industry: Retailer (traditional)

301 Blair Road New lease: 565,452 s.f. Tenant: Amazon.com Industry : Retailer (e-commerce)

115 Interstate Boulevard Sublease: 526,459 s.f. Subtenant: Tory Burch Industry : Consumer Non-Durables

130 Interstate Boulevard Renewal: 413,092 s.f. Tenant: Home Depot Industry : Retailer (traditional)

Central New Jersey

Charlotte

1900 Continental Boulevard Renewal: 274,000 s.f. Tenant: Snyder’s Lance

10000 Twin Lakes Parkway Renewal: 263,000 s.f. Tenant: Ingersoll Rand

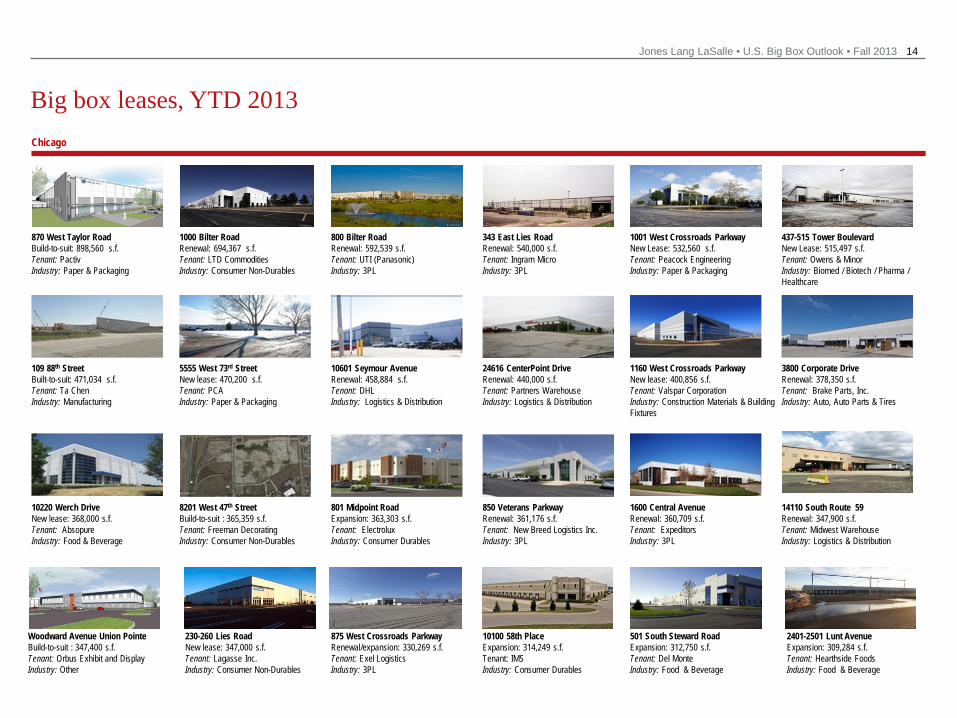

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 14

Big box leases, YTD 2013 Chicago

800 Bilter Road Renewal: 592,539 s.f. Tenant: UTI (Panasonic) Industry: 3PL

1001 West Crossroads Parkway New Lease: 532,560 s.f. Tenant: Peacock Engineering Industry: Paper & Packaging

343 East Lies Road Renewal: 540,000 s.f. Tenant: Ingram Micro Industry: 3PL

1160 West Crossroads Parkway New lease: 400,856 s.f. Tenant: Valspar Corporation Industry: Construction Materials & Building Fixtures

870 West Taylor Road Build-to-suit: 898,560 s.f. Tenant: Pactiv Industry: Paper & Packaging

437-515 Tower Boulevard New Lease: 515,497 s.f. Tenant: Owens & Minor Industry: Biomed / Biotech / Pharma / Healthcare

1000 Bilter Road Renewal: 694,367 s.f. Tenant: LTD Commodities Industry: Consumer Non-Durables

109 88th Street Built-to-suit: 471,034 s.f. Tenant: Ta Chen Industry: Manufacturing

14110 South Route 59 Renewal: 347,900 s.f. Tenant: Midwest Warehouse Industry: Logistics & Distribution

1600 Central Avenue Renewal: 360,709 s.f. Tenant: Expeditors Industry: 3PL

5555 West 73rd Street New lease: 470,200 s.f. Tenant: PCA Industry: Paper & Packaging

850 Veterans Parkway Renewal: 361,176 s.f. Tenant: New Breed Logistics Inc. Industry: 3PL

10601 Seymour Avenue Renewal: 458,884 s.f. Tenant: DHL Industry: Logistics & Distribution

24616 CenterPoint Drive Renewal: 440,000 s.f. Tenant: Partners Warehouse Industry: Logistics & Distribution

3800 Corporate Drive Renewal: 378,350 s.f. Tenant: Brake Parts, Inc. Industry: Auto, Auto Parts & Tires

10220 Werch Drive New lease: 368,000 s.f. Tenant: Absopure Industry: Food & Beverage

801 Midpoint Road Expansion: 363,303 s.f. Tenant: Electrolux Industry: Consumer Durables

8201 West 47th Street Build-to-suit : 365,359 s.f. Tenant: Freeman Decorating Industry: Consumer Non-Durables

10100 58th Place Expansion: 314,249 s.f. Tenant: IMS Industry: Consumer Durables

230-260 Lies Road New lease: 347,000 s.f. Tenant: Lagasse Inc. Industry: Consumer Non-Durables

875 West Crossroads Parkway Renewal/expansion: 330,269 s.f. Tenant: Exel Logistics Industry: 3PL

501 South Steward Road Expansion: 312,750 s.f. Tenant: Del Monte Industry: Food & Beverage

Woodward Avenue Union Pointe Build-to-suit : 347,400 s.f. Tenant: Orbus Exhibit and Display Industry: Other

2401-2501 Lunt Avenue Expansion: 309,284 s.f. Tenant: Hearthside Foods Industry: Food & Beverage

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 15

Big box leases, YTD 2013 Chicago (continued)

901 West Crossroads Parkway New lease: 301,474 s.f. Tenant: Bunzl Industry: Paper & Packaging

99 North Pinnacle Drive New lease: 281,963 s.f. Tenant: Sleepy’s Industry: Consumer Durables

430 Gibraltar Drive New lease: 281,464 s.f. Tenant: Sony Industry: Consumer Durables

7701-7711 95th Street Renewal: 252,825 s.f. Tenant: Honeywell Industry: Consumer Durables

Columbus

Centerpoint Business Park Direct: 580,000 s.f. Tenant: Avnet, Inc. Industry: Consumer Durables

175 Heritage Drive Build-to-suit: 766,633 s.f. Tenant: Navarre Corporation Industry: Logistics & Distribution

10 Enterprise Parkway Build-to-suit: 530,000 s.f. Tenant: Ace Hardware Industry: Retailer (traditional)

5765 Green Pointe Drive North Renewal: 358,760 s.f. Tenant: Sears Industry: Retailer (traditional)

6200 Commerce Center Direct: 437,000 s.f. Tenant: HD Supply Industry: Construction Materials & Building Fixtures

4900 Creekside Parkway Direct: 337,859 s.f. Tenant: Exel, Inc. Industry: 3PL

2859 Rohr Road New Lease: 314,000 s.f. Tenant: Excel Global Logistics Industry: 3PL

4900 Creekside Parkway Direct: 337,859 s.f. Tenant: Exel, Inc. Industry: 3PL

Dallas / Fort Worth

2425 Esters Boulevard New Lease: 297,500 s.f. Tenant: Jacobson Companies Industry: 3PL

5101 Frye Road New lease: 728,520 s.f. Tenant: Trader Joe’s Industry: Food & Beverage

5500 South Freeway New lease : 552,600 s.f. Tenant: Sygma Network Industry: Food & Beverage

13300 Park Vista Boulevard New Lease : 399,000 s.f. Tenant: Carolina Beverage Industry: Food & Beverage

4800 Langdon Road New lease: 321,123 s.f. Tenant: Conn Appliances Industry: Retailer (traditional)

3737 Duncanville Road New lease: 510,400 s.f. Tenant: Owens Corning Insulating Industry: Construction Materials & Building Fixtures

4798 Henrietta Creek Road New lease: 472,542 s.f. Tenant: National Distribution Centers Industry: Logistics & Distribution

1011 Isuzu Parkway Direct: 470,000 s.f. Tenant: General Electric Company Industry: Consumer Durables

5300 Westport Parkway New leases: 788,142 s.f. Tenant: Walmart.com Industry: Retailer (e-commerce)

3700 Pinnacle Point Drive Direct: 419,438 s.f. Tenant: Ozburn-Hessey Logistics Industry: 3PL

4700 Arnon Carter Boulevard Renewal: 352,054 s.f. Tenant: United America Corp. Industry: Communications / Tech / Media

1800 Columbia Club Drive TBD: 288,041 s.f. Tenant: Iron Mountain Industry: Other

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 16

Big box leases, YTD 2013 Denver

Indianapolis

17901 East 40th Avenue BTS: 541,662 s.f. Tenant: United Natural Foods Industry: Food & Beverage

Houston

10650 Okanella Ln. Direct: 267,273 s.f. Tenant: DB Schenker Logistics Industry: Logistics & Distribution

359 Pike Court Renewal: 341,190 s.f. Tenant: Katoen Natie Industry: Logistics & Distribution

Citypark East Industrial Park Renewal: 767,362 s.f. Tenant: Exel; 3 separate renewals Industry: Logistics & Distribution

Eastport Industrial Park Renewal: 370,000 s.f. Tenant: United DC Industry: Logistics & Distribution

Rampart Corporate Center Direct: 299,840 s.f. Tenant: Goodman Manufacturing Industry: Manufacturing

945 Monument Drive Build-to-suit: 715,000 s.f. Tenant: Subaru of America, Inc. Industry: Auto, Auto Parts & Tires

2209-2233 Stafford Road Renewal: 600,576 s.f. Tenant: Cross Road Centers Industry: 3PL

281 Airtech Parkway Expansion: 405,942 s.f. Tenant: Ozburn-Hessey Logistics Industry: 3PL

300 Purity Drive Expansion: 355,000 s.f. Tenant: Gander Mountain Industry: Retailer (traditional)

8175 North Allison Avenue New lease: 300,000 s.f. Tenant: Pinnacle Oil Industry: Auto, Auto Parts & Tires

861-881 Perry Road Expanded lease: 296,000 s.f. Tenant: Eby-Brown Company Industry: Food & Beverage

3052 North Distribution Way New lease: 250,058 s.f. Tenant: Spectra Premium Industry: Auto, Auto Parts & Tires

4925-4945 West 86th Street New lease: 309,600 s.f. Tenant: Heartland Sweetener Industry: Food & Beverage

1801 Innovation Boulevard Build-to-suit: 545,000 s.f. Tenant: Gordman’s Industry: Retailer (traditional)

7520 Georgetown Road Renewal 528,000 s.f. Tenant: Hewlett Packard Industry: Consumer Durables

2525 N Shadeland Avenue New lease: 545,000 s.f. Tenant: Kid Glove Industry: 3PL

1101 Whitaker Road Renewal: 379,322 s.f. Tenant: Ozburn-Hessey Logistics Industry: 3PL Inland Empire

4100 Mission Boulevard Renewal: 763,228 s.f. Tenant: Georgia Pacific Industry: Paper & Packaging

5400 Shea Center Drive Renewal: 623,630 s.f. Tenant: Dorel Industry: Manufacturing

City of Perris, California Build-to-suit: 1,100,000 s.f. Tenant: Home Depot Industry: Retailer (e-commerce)

13052 Jurupa Avenue Renewal: 827,560 s.f. Tenant: Jarden Consumer Solutions Industry: Consumer Durables

3000 E Philadelphia Street Renewal: 750,000 s.f. Tenant: Pier 1 Imports Industry: Retailer (traditional)

22775 Oleander Avenue New lease: 677,909 s.f. Tenant: DSC Logistics Industry : 3PL

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 17

Big box leases, YTD 2013 Inland Empire (continued)

12249 Holly Street Renewal: 457,120 s.f. Tenant: Exel Logistics Industry: 3PL

1900 South Rochester Avenue New lease: 506,436 s.f. Tenant: Mobis Parts America (Hyundai) Industry: Auto, Auto Parts & Tires

9333 Hermosa Avenue New lease: 573,000 s.f. Tenant: Campbell’s Industry: Food & Beverage

18012 Slover Avenue Build-to-suit: 610,120 s.f. Tenant: Distribution Alternatives Industry: 3PL

4041 East Francis Street New lease: 500,000 s.f. Tenant: Cal Cartage Industry: Logistics & Distribution

6725 Kimball Avenue Renewal: 423,080 s.f. Tenant: NFI Industries Industry: Logistics & Distribution

3950 East Airport Drive Renewal: 414,435 s.f. Tenant: Timberland Industry: Retailer (traditional)

1801 South Carlos Avenue New lease: 414,453 s.f. Tenant: Imax Worldwide Industry: Consumer Non-Durables

2825 Jurupa Avenue New lease: 612,104 s.f. Tenant: Samsung Industry: Consumer Durables

12471 Riverside Drive New lease: 376,007 s.f. Tenant: Genco Industry : 3PL

11001 Etiwanda Avenue New lease: 404,730 s.f. Tenant: ACT Fulfillment Industry: 3PL

9425 Nevada Street New lease: 390,780 s.f. Tenant: Kuehne & Nagel Industry: Logistics & Distribution

2111 Eastridge Avenue Renewal: 360,000 s.f. Tenant: ModusLink Industry: 3PL

Moreno Valley Commerce Park Build-to-suit: 354,810 s.f. Tenant: Minka Lighting, Inc. Industry: Construction Materials & Building Fixtures

11296 Harrell Street New lease: 353,361 s.f. Tenant: Oakley, Inc. Industry: Consumer Non-Durables

13083 Slover Avenue New lease: 323,660 s.f. Tenant: Subaru Industry: Auto, Auto Parts & Tires

1000 Etiwanda Avenue New lease: 302,080 s.f. Tenant: ODW Logistics Industry: 3PL

24950 Grove View Road Renewal: 301,100 s.f. Tenant: Harman Consumer Group Industry: Consumer Non-Durables

13725 – 13835 Pipeline Avenue Renewal: 300,000 s.f. Tenant: ODW Logistics Industry: 3PL

13366 Philadelphia Street New lease: 266,950 s.f. Tenant: Harman International Industries Industry: Consumer Non-Durables

1670 Champagne Avenue New lease: 263,500 s.f. Tenant: Genco Industry: 3PL

5700 East Airport Drive New lease: 250,248 s.f. Tenant: DCG Industry: 3PL

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 18

Big box leases, YTD 2013 Kansas City

1400 Warren Street New lease: 289,000 s.f. Tenant: Piston Automotive Group

Las Vegas

2280 North Lamb Boulevard New lease: 303,000 s.f. Tenant: Hand Air Express Industry : 3PL

Los Angeles

4501 East Conant Street New lease: 1,091,754 s.f. Tenant: Mercedes Benz Industry: Auto, Auto Parts & Tires

2501 West Rosecrans Avenue New lease: 298,474 s.f. Tenant: American Logistics Intl. Industry: Retailer (e-commerce)

108-288 Mayo Avenue Expansion: 775,000 s.f. Tenant: Port Logistics Group Industry: 3PL

2849 Ficus Street Renewal: 322,817 s.f. Tenant: G.P.R. Logistics, LLC Industry: 3PL

9306 Sorensen Avenue Direct lease: 305,422 s.f. Tenant: Phoenix Industry: 3PL

6281-6285 East Slauson Avenue Renewal: 268,391 s.f. Tenant: Performance Paper Industry: Paper & Packaging

771 East Watson Center Road Direct lease: 258,678 s.f. Tenant: Damco Distribution Industry: Logistics & Distribution

1560 East Stateline Road Renewal: 374,000 s.f. Tenant: Trane Industry: Construction Materials & Building Fixtures

699 Research Drive New Lease: 514,980s.f. Tenant: Home Décor Cos. Industry: Consumer Durables

Memphis

3399 East Raines Road Renewal: 600,000 s.f. Tenant: Philips Electronics Industry: Consumer Durables

5461 Davidson Road New Lease: 500,000 s.f. Tenant: Technicolor Industry: Consumer Durables

8734 South Crossroads Drive New Lease: 533,226 s.f. Tenant: Genco Industry: 3PL

6100 Holmes Road New Lease: 414,076 s.f. Tenant: Market TJ Maxx Industry: Retailer (traditional)

Minneapolis

1301 Industrial Boulevard NE Renewal: 350,347 s.f. Tenant: Superior Third Party Logistics Industry: 3PL

1187 Park Place Sale-leaseback: 370,000 s.f. (9-month term) Tenant: TE Connectivity Industry: Communications / Tech / Media

1909 Zephyr Street Direct: 394,000 s.f. Tenant: Menlo Logistics Industry: 3PL

Northern California

Sperry Avenue & Baldwin Road Build-to-suit: 1,030,000 s.f. Tenant: Amazon.com Industry: Retailer (e-commerce)

North Chrisman Road @ Grant Line Road Build-to-suit: 1,017,353 s.f. Tenant: Amazon.com Industry: Retailer (e-commerce)

1550 North Chrisman Road Renewal: 749,840 s.f. Tenant: Kellogg’s Industry : Food & Beverage

4400 Florin Perkins Road Renewal: 412,808 s.f. Tenant: Grocery Outlet Industry: Food & Beverage

6700 Automall Parkway Renewal: 476,177 s.f. Tenant: Office Depot Industry: Retailer (traditional)

7331-7337 Las Positas Road Direct: 286,100 s.f. Tenant: International Paper Co. Industry: Paper & Packaging

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 19

Big box leases, YTD 2013 Philadelphia / Harrisburg

9300 Old Scotland Road Pre-Lease: 1,700,000 s.f. Tenant: Proctor & Gamble Industry: Consumer Non Durables

2785 Commerce Center Boulevard Direct: 1,200,000 s.f. Tenant: Wal-Mart Industry: Retailer (e-commerce)

600 Oak Ridge Road Pre-Lease: 1,054,011s.f. Tenant: American Eagle Outfitters Industry: Retailer (e-commerce)

3215 Commerce Center Boulevard Pre-Lease: 1,000,000 s.f. Tenant: Wal-Mart Industry: Retailer (e-commerce)

2040 North Union Street Renewal: 507,000 s.f. Tenant: Sears Tires Industry: Auto, Auto Parts & Tires

5 True Temper Drive Renewal: 511,000 s.f. Tenant: SC Johnson Industry: Consumer Non Durables

Address is TBD Pre-Lease: 980,000 s.f. Tenant: NFI Industry: 3PL

601 Memory Lane New lease: 458,000 s.f. Tenant: Harley Davidson Industry: Auto, Auto Parts & Tires

2869 Route 22 New lease: 550,000 s.f. Tenant: Bridgestone Tires Industry: Auto, Auto Parts & Tires

5800 Coliseum Way Renewal: 336,600 s.f. Tenant: Kaiser Permanente Industry : Biomed / Biotech / Pharma / Healthcare

Northern California (continued)

9750 Commerce Circle New Lease: 503,000 s.f. Tenant: One Kings Lane Industry: Retailer (e-commerce)

40 Logistics Drive New lease: 550,000 s.f. Tenant: Menlo Logistics Industry: 3PL

597 Alexander Spring Road New lease: 1,059,650 s.f. Tenant: Mondelez International Industry: Food & Beverage

221 South 10th Street Renewal: 489,213 s.f. Tenant: Genco Industry: 3PL

100 Quality Circle Renewal: 440,000 s.f. Tenant: Ingram Micro Industry: Communications / Tech / Media

2834 Schoeneck Road Renewal: 270,000 s.f. Tenant: The Lehigh Group Industry: Consumer Durables

771 East Watson Center Road Direct lease: 258,678 s.f. Tenant: Damco Distribution Industry: Logistics & Distribution

201 Fulling Mill Road Renewal: 650,761 s.f. Tenant: Schneider Electric Industry: Communications / Tech / Media

Phoenix

1110 North 127th Avenue New lease: 278,000 s.f. Tenant: Conn’s Furniture Industry: Consumer Durables

Portland

Rivergate Corporate Center Renewal: 402,450 s.f. Tenant: Georgia Pacific Industry : Paper & Packaging

2375 East Newlands New Lease: 337,500 s.f. Tenant: TREX Industries Industry: Consumer Durables

Reno Seattle

Pacific Gateway Renewal: 265,000 s.f. Tenant: HD Supply Industry : Logistics & Distribution

Pacific Gateway Business Park Renewal: 265,000 s.f. Tenant: Pacific Distribution Services Industry: 3PL

Valley South Renewal: 370,000 s.f. Tenant: Pacific Distribution Services Industry: 3PL

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 20

Big box leases, YTD 2013 Seattle (continued)

4702 Park 370 Boulevard New/Expansion: 494,000 s.f. Tenant: Jacobson Industry: Food & Beverage

9 Gateway Commerce Center Drive New lease: 297,000 s.f. Tenant: Unilever Industry : Consumer Non-Durables

5620 Inner Park Drive Renewal: 1,200,000 s.f. Tenant: Unilever Industry: Consumer Non-Durables

3971 Lakeview Corporate Drive Renewal: 540,000 s.f. Tenant: World Wide Technology Industry: Communications / Tech / Media

St. Louis

Park 277 Renewal: 262,000 s.f. Tenant: PlyGem Industry : Construction Materials & Building Fixtures

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 21

By count

Retailer (e-commerce) Percent of industry demand, by size

100-249 ksf 12% 250-499 ksf

12%

500-749 ksf 33%

750-999 ksf 6%

1 msf+ 36%

Online sales are only increasing • Total U.S. retail sales were $4.4 trillion in 2012; e-commerce comprised 5.5

percent of this. E-commerce sales are expected to nearly double over the next four years.

• The rate of internet penetration in the U.S. is high at 81.0 percent and there were 253.4 million internet users in 2012 – 183.8 million of which are estimated to be online shoppers. This means that 59 percent of the country’s population shops online.

Evolving in order to stay relevant • Retailers are deploying substantial capital to stay relevant in today’s environment,

and this directly benefits industrial real estate. • The numbers do not lie: Wal-Mart experienced comparable-store sales growth of

3.3. percent from 2011 to 2012; their web sales were up 20.3 percent over the same time period. Other major retailers have similar success stories. Macy’s posted a one-tenth of a percentage point increase in comparable store sales, yet 41.0 percent growth via their website; the Home Depot was one-tenth versus 16.7 percent, Sears Holdings was negative 7.5 percent versus 16.5 percent growth, and Lowe’s was one-fifth of a percentage point compared to a resounding 51.5 percent jump in their web sales.

Market potential benefits industrial demand • Twelve percent of total U.S. requirements, on a square footage basis, are e-

commerce-related. • U.S. industrial construction activity was 96.7 million square feet near the end of

third quarter. Of this, 10.4 percent was comprised of e-commerce users, and all committed to build-to-suit or owner-built facilities. This speaks to the building requirements today’s occupiers demand in this highly specialized industry.

Retailers are adapting to avoid deletion E-commerce demand concentration, by market

100-249 ksf = Smaller e-tailers / operations

250-749 ksf = Regional fulfillment centers

750-1 msf+ = Mega fulfillment centers

NorCal

Phoenix Dallas/Fort Worth

Memphis

Baltimore

New Jersey

Boston

Philadelphia Columbus

Chicago

Indianapolis

St. Louis

Tampa

Seattle/Puget Sound

Cincinnati

Salt Lake City Sacramento

San Joaquin

Inland Empire

Atlanta

Jones Lang LaSalle • U.S. Big Box Outlook • Fall 2013 22

Craig S. Meyer, SIOR President Industrial Brokerage Services – Americas T +1 424.294.3460 [email protected]

Aaron L. Ahlburn Senior Vice President Americas Director of Research – Industrial T +1 424.294.3437 [email protected]

Richard H. Thompson Managing Director T +1 773.458.1385 [email protected]

Kristian D. Bjorson, SIOR International Director T +1 773.458.1397 [email protected]

Dain Fedora Research Manager Americas Industrial T +1 213.239.6262 [email protected]

Head of Supply Chain & Logistics Solutions Head of Retail/e-commerce Distribution

www.us.jll.com/industrial

For more information please contact:

©2013 Jones Lang LaSalle IP, Inc. All rights reserved. No part of this publication may be reproduced by any means, whether graphically, electronically, mechanically or otherwise howsoever, including without limitation photocopying and recording on magnetic tape, or included in any information store and/or retrieval system without prior written permission of Jones Lang LaSalle. The information contained in this document has been compiled from sources believed to be reliable. Jones Lang LaSalle or any of their affiliates accept no liability or responsibility for the accuracy or completeness of the information contained herein and no reliance should be placed on the information contained in this document.

About Jones Lang LaSalle Jones Lang LaSalle (NYSE:JLL) is a professional services and investment management firm offering specialized real estate services to clients seeking increased value by owning, occupying and investing in real estate. With annual revenue of $3.9 billion, Jones Lang LaSalle operates in 70 countries from more than 1,000 locations worldwide. On behalf of its clients, the firm provides management and real estate outsourcing services to a property portfolio of 2.6 billion square feet and completed $63 billion in sales, acquisitions and finance transactions in 2012. Its investment management business, LaSalle Investment Management, has $46.3 billion of real estate assets under management. For further information, visit www.jll.com. Jones Lang LaSalle Research Jones Lang LaSalle’s research team delivers intelligence, analysis, and insight through market-leading reports and services that illuminate today’s commercial real estate dynamics and identify tomorrow’s challenges and opportunities. Our 350 professional researchers track and analyze economic and property trends and forecast future conditions in over 70 countries, producing unrivalled local and global perspectives. Our research and expertise, fueled by real-time information and innovative thinking around the world, creates a competitive advantage for our clients and drives successful strategies and optimal real estate decisions. We are committed to developing new metrics and methodological tools to capture and understand the factors driving office, retail and warehousing/logistics real estate markets across the world and bring insight to the future for our clients.