BIFURCATION OF TRAVANCORE TEMPLES...

66

CHAPTER VII BIFURCATION OF TRAVANCORE TEMPLES AND TEMPLE ADMINSITRATION IN KANYAKUMARI DISTRICT On 1st November 1956, Indian states were reorganised on linguistic basis and obviously Kerala state was also re-organised. The four Tamil speaking taluks of Thovala, Agastheeswaram, Kalkulam and Vilavancode in the southern Travancore were merged with the then Madras state. These four taluks constituted the kanyakumari district which formed the southern most district of Madras state'. Consequently the Travancore temples were also bifurcated. Accordingly 490 Travancore temples were entrusted to the Kanyakumari Devaswom Board. They included 450 incorporated temples, 18 unincorporated temples, 12 sanketan temples and 2 sreepadam temples2. All these temples are widely appreciated for their exalted artistic excellence 3 . Subsequent to the bifurcation of Travancore temples, a separate fund called 1 B. Maria John, Linguistic reorganistion of Madras Presidency, Nagercoil, 1994, pp.78-88. 2 Vide in the Appendix VII, pp.44-58. Vide in the Appendix VIII, pp.59-61. 178

Transcript of BIFURCATION OF TRAVANCORE TEMPLES...

CHAPTER VII

BIFURCATION OF TRAVANCORE TEMPLESAND TEMPLE ADMINSITRATION IN KANYAKUMARI

DISTRICT

On 1st November 1956, Indian states were reorganised on

linguistic basis and obviously Kerala state was also re-organised.

The four Tamil speaking taluks of Thovala, Agastheeswaram,

Kalkulam and Vilavancode in the southern Travancore were merged

with the then Madras state. These four taluks constituted the

kanyakumari district which formed the southern most district of

Madras state'. Consequently the Travancore temples were also

bifurcated. Accordingly 490 Travancore temples were entrusted to

the Kanyakumari Devaswom Board. They included 450

incorporated temples, 18 unincorporated temples, 12 sanketan

temples and 2 sreepadam temples2. All these temples are widely

appreciated for their exalted artistic excellence 3 . Subsequent to the

bifurcation of Travancore temples, a separate fund called

1 B. Maria John, Linguistic reorganistion of Madras Presidency, Nagercoil, 1994,

pp.78-88.

2 Vide in the Appendix VII, pp.44-58.

Vide in the Appendix VIII, pp.59-61.

178

Kanyakumari Devaswom fund was also constituted on 1st

November 1956. The Commissioner, H.R. & C.E 4 (Administration)

was appointed as one man Board to administer the devaswom m

the transferred territory. The then Madras Government granted.

Rs. 13.5 lakhs to kanyakumari Devaswom Board which they got

from the consolidated annual grant of 51 lakhs. The amount

obtained as share to Travancore Devaswom Board was 37.5 lakhs.

The devaswom surplus fund available as on 31st October 1956 was

also divided in the above proportion and the kanyakumari

Devaswom Board got 24 lakhs as its share.

Kanyakumari Devaswom Board:

As per the Act 30 of 1959, passed by the Madras legislature,

the Kanyakumari Devaswom Board was established on 1st April

1960. The President and two members constituted the Board. The

president and a member were nominated by the then Madras

Government and the Ruler of Travancore nominated another

member. K.M. Boothalingam pillai (president), A.

BrahmanandaswamY Nadar and R.N. KrishnaswamY Iyer

H.R.&C.E:- Hindu Religious and Charitable Endowment.

179

(members) constituted the first Board 5 . Only the permanent

resident of the transferred territory was- eligible to be nominated to

the Board. He should profess the Hindu religion and must attain

the age of thirty-five years. The members could be removed on the

ground of misbehaviour or incapacity. The President and members

of the Devaswom Board were entitled to get travelling cum halting

allowances for every month and it was fixed as Rs.200. for their

tour at least for 10 days. Later the allowance was enhanced to

Rs.250/-6.

The Devaswom Board functioned from 1st April 1960 to 31st

December 1974 for about 15 Years. The working of the Board was

effective. The most important function of the Board was to control

the administration of devaswoms in the transferred territory. The

Board supervised the activities of the temple, made arrangements

for the proper conduct of pujas, ceremonies, ulsavams and other

festivals of the temples. The Board appointed temple servants for

the proper conduct of pujas and ulsavams. Board members visited

S. Nateson 'Devaswom in kanyakumari , Souvenir, Kanyakumari Devaswom

Board, Suchindrum, 1971, p.9.

Memorandum No. 64632 U/61, Suchindrum, dated 17 July 1961.

180

the important temples during the days of ulsavams. They were

entitled to get travelling allowances during their visit 7 . Apart from

temple administration, the Board has undertaken many social,

cultural and educational activities with a view to uplift the social,

economic and cultural betterment of the Hindu community. The

Board conducted meetings at regular intervals and urgent meetings

were conducted with circulation minutes. Assistant devaswom

commissioner acted as the secretary of the Board. The

kanyakumari Devaswom Board has prepared and passed byelaws

on various subject matters at the Board meetings. These byelaws

were published in one or more newspapers of local languages of the

locality, district gazettes, and exhibited them in the devaswom

notice board at Board's office at Suchindrum. People expressed

their objections and suggestion over the byelaws, which enabled

the Board to modify them. Such modified byelaws were sent to the

government through the commissioner8.

G.O. No.2229, Revenue Department, dated 24 may 1961.

8 G. O.No. 2229, Revenue Department, dated 13 u1y 1961.

181

The Board prepared the administration report every year. The

report covered all the activities of Board. In the administration

report. for the year 1960-'61, a detailed report regarding the social

activities of the Board had been given. The establishment of schools

and other educational institutions including the thevara patasala

at Suchindrum were the major educational activities of the Board-9

Temples:

The kanyakumari temples had a separate identity.

Kanyakumari was an important town of the Pandian Kingdom and

from the beginning of the Christian era it was a famous place of

pilgrimage 10 The temples here existed as centres of cultural

activity. During the bifurcation of Travancore temples, at the eve of

state re-organisation, the temples situated in this area were

entrusted to the Kanyakumari Devaswom Board. There were 490

temples of different categories".

Devaswom Minutes, Suchindrum ,June 1962, p.3.

10 Elamkulam p.n. .kunjan pillai, studies in kerala history, kottayam, 1970,

p.12

11 Kanyakumari Devasworn Board Administration Report, Suchindrum, dated

20 July 1992, p.2

182

1) Incorporated temples 458

2) Unincorporated temples 18

3) Sanketham temples 12

4) Sreepadam temples 2

Total 490

These temples were divided into five groups at taluk level, the

groups being12.

1) Nagercoil group (Agasteeswram taluk)

2) Bhoothpandy group (Thovala taluk)

3) Padmanabhapuram group (Kalkulam taluk)

12 Ibid.

183

4) Kuzhithurai group (Vilavancode taluk)

5) Shencotta-h group (Shencottai taluk ,Tirunelveli

district)

Group wise temples13

Nagerco Bootha Padma Kuzhi Shengott

il pany Nabapur thurai ah

Group Group am Group GroupGoru

94 66 116 94 83

3 6 2 2 5

2 1 8 1 -

- - 2 - -

99 1 73 1 128 1 97 1 93

Si

Name ofN

Temples0

i incorporatedTern les

2 UnincorporatedTemples

3 SankethaflTemples

4 SreepadaniTemples

Total

Grand ITotal I I 490

13 Administration Report, op.cit, p.2.

184

Incorporated Devaswoms were the temples mentioned in the

schedule of the devaswom proclamation of 1097 M.E., which had

been under the management of the ruler of Travancore. Then they

came under the revenue department and subsequently transferred

to Travancore Devaswom Board. During bifurcation these temples

were entrusted to Kariyakumari Devaswom Board. Total number of

temples under this category was 458 14 After the assumption of the

incorporated devaswoms, the Devaswom Board took over some of

the temples managed by trustees on account of their

mismanagement and these temples came to be known as

unincorporated devaswoms. The properties and funds of these

devaswoms were kept distinct and separate from the incorporated

devaswom. There were 18 unincorporated devaswoms under

Kanyakumari Devaswom Board'-5 . The administration of

SreePadmanabha Swamy temple and Sreepandaravaka properties

and funds of the said temple was vested in a trust with the ruler of

Travancore. There was a separate department known as

sanketham department. When sreepandaravaka lands were taken

over by the Government, the administration and management of

14 Ibid

IS Ibid.

185

sanketham temples were placed with the devaswom Board 16 . There

were twelve sanketham temples in the transferred territory. The

sreepadam temples were managed by the palace directly. There

were separate lands known as sreepadam lands for these temples.

Sreepadam lands were taken over subsequently. The management

and control of these temples were transferred to the Devaswom

Board. There were two sreepadam temples under Kanyakumari

Devaswom Board 17 . The temples under category 3 and 4 were royal

family temples. They were entrusted with the Board because of

their properties being abolished by laws enacted by the

government. Among the incorporated temples, some of them were

considered as big temples. Such temples assumed that status on

the basis of the expenditure incurred by them for pujas,

ceremonies and other festivals. In other parts of Tamilnadu the

temples which have more income are considered as big temples.

This is a major difference between the temples of kanyakumari

district and other parts of Tamilnadu. Kanyakumari temple,

Suchindrum temple, Nagercoil Nagaraja temple, Mondaikadu

temple, Tiruvattar temple, Velimali kumarakoil temple are some of

16 SreepandaraVaka land abolition Act, 1964.

17 Administration Report, op.cit., p.3.

186

the ancient and famous temples in Kanykumari District 18 . These

temples are conducting many festivals and ulsavams apart from

nityanitanam. The expenditure in these temples are high and so

they are considered as major temples. The ritual in these temples

are similar to those of the temples of Travancore. Some of the

important ulsavams in Kanyakumari temples are Mondaikkadu

Koda Maholsavam, Kumarakoil Thirukalyanam, Kollamcode

Thookkam and Suchindrum car festival. A large number of people

participated in these festivals. Sivalaya Oottam in sivarathri day

and Saraswathy puja procession on navarathri eve are two notable

festivals in Kanyakumari District, which cover the entire district'9.

Many temple priests like santhikars, tantri, melsantlii,

kizhsanthi etc were appointed on the initiative of Board for the

proper conduct of pujas and u1savams20. The santhikars are

appointed for a particular period ordinarily for a term of three

years21 . The santhikars in Kanyakumari temples were directly paid

18 Administration Report op-cit., p.5.

19 Ibid.

20 The Travancore Devaswom hand Book, p.142.

21 G.O.No.D5067, public department, dated 4 October 1935.

187

with paddy but now they are paid in cash22.

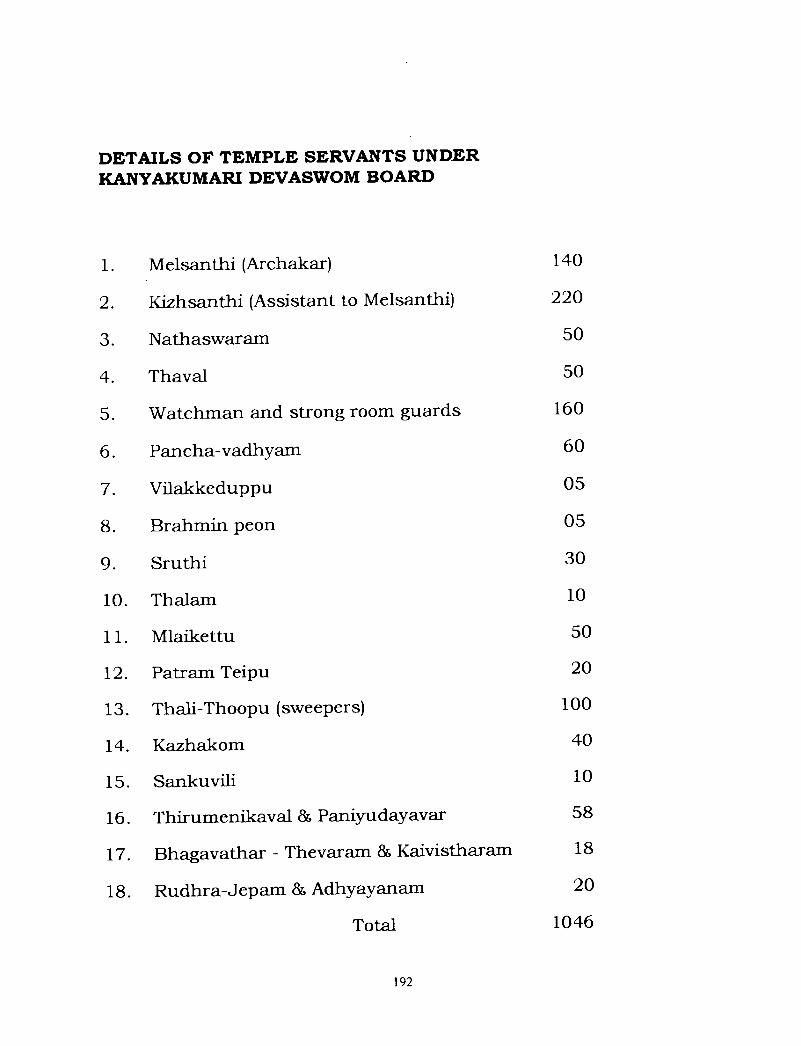

Temple Servants:

The temple servants under Kanyakumari Devaswom Board

are designated as contingency staff and they have not been given a

definite scale of pay similar to the government servants. They are

paid consolidated amount as their salary. In many temples the

santhikars have to deposit a security amount with the devaswomS

department and it is considered as a minimum qualification for the

post23 . Following is the amount of security deposit fixed by the

government.

1. Santhikars in the cape, Thiruppathisaralfl and Velimala

Devaswoms - Rs.500 each.

2. Perianambi in the Thiruvattar Devaswom - One year's

pay.

3. Santhikars in other DevaswomS - Rs.25 to 200.

22 K.K.Pillai, op.cit., p.174.

23 Government of Madras, G.O. M.S. No. 1986, Revenue Department, dated 29

July 1964.

188

Apart from santhikars, there are other temple servants

(contingency) such as nathaswaram, thaval, panchavathiam,

vilakiceduppU, suruthi, thalam, malaikettU, patramtheiPu,

thalithoopU, kazhakam, sankuvili, thirumefli kaval,

pariyudayavar, bhagavthar, thevaram , kai-vistharam, rudhra-

jepam and adthyayaflam. In addition to these temple servants,

brahmin peon, watchman and strong room guards are also

appointed24.

In addition to temple servants, there are 131 government

servants and 14 thirukoil servants25 . These two categories of

employees are drawing their salary as per the scale of pay

admissible to the government servants. They are governed by the

government service rules. There were 15 officers working under

kanyakumari Devaswom Board from 1960 onwards. The salary of

the temple servants has been revised subsequently. The practice of

giving kattichorU to some categories of temple servants have been

stopped and in lieu of that, paying cash was started. Contributory

24 Administration Report, op.cit., PP.5-6.

25 Ibid., pp.4-5.

189

provident fund was introduced "to temple servants and other

devaswom servants other than government servants 26 . As per this

scheme, the Board shall make contribution to the provident fund

based on the pay of the subscriber from time to time. Such

contribution shall be limited to six percent of the pay drawn by a

subscriber. The scale of pay for the officers of the Kanyakumari

Devaswom Board and other thirukoil servants were revised as per

the pay commission recommendations. The four categories of

contingency staff also received the enhanced dearness allowance.

However the temple servants are still treated as contingency

servants and their service conditions are yet to be improved. The

reason is that the temple staffs are paid their salaries out of the

collections from the 'hundis'. It is high time that this condition

ought to be changed and the service conditions, particularly the

salary of the temple servants should be paid, in accordance with

the basic requirements of their lives.

26 Government of Madras, G.O.No. 347, Revenue Department, dated 25

january 1962.

190

After the Board assuming office, it had taken some pragmatic

steps for the benefit of the temple servants. A survey was

conducted among the temple servants working in various temples

under the control of the Board. Vacant places in some temples were

filled up. There were 1046 temple servants working in different

temples under kanyakumari Devaswom Board. Similarly there were

14 thirukoil servants and 131 government servants who were also

working in the Board office, temple offices, libraries and maramath

department27 . Among them, scale of pay was granted only to the

government servants working in the administration wing. The

workers inside the temples including the santhikars were treated

as contingent staff and they were paid in the traditional way. The

split up figures of the temple servants, thirukoil servants and

government staff along with the pay scale are given separately28.

27 Administration report, op,cit, p.5.

28 Kanyakumari Devaswom Board Souvenir, op,cit., pA-.)

191

DETAILS OF TEMPLE SERVANTS UNDERKANYAKUMARI DEVASWOM BOARD

1. Melsanthi (Archakar)

140

2. Kizhsanthi (Assistant to Melsanthi)

220

3. Nathaswaram 50

4. Thaval

50

5. Watchman and strong room guards

160

6. Pancha-vadhyam

7. Vilakkeduppu

8. Brahmin peon

9. Sruthi

10. Thalam

11. Mlaikettu

12. PatramTeipu

13. Thali-Thoopu (sweepers)

14. Kazhakom

15. Sankuvili

16. Thirumenikaval & Paniyudayavar

17. Bhagavathar - Thevaram & Kaivistharam

18. Rudhra-Jepam & Adhyayanam

Total

60

05

05

%H

10

50

20

100

40

10

58

18

20

1046

192

DETAILS OF GOVERNMENT SERVANTS

1. Devaswom Superintendents 05

2. Managers 02

3. Maramath Section Officers 02

4. Assistants 14

5. Junior Assistants 22

6. Typists 03

7. Overseer 01

8. Suboverseers

9. Sreekariams 39

10. Chadrams 21

11. Office Assistants(peons)

16

12. Watchman 01

Total

131

193

DETAILS OF THIRUKOIL SERVANTS

1. Junior Assistants 02

2. Supervisors 02

3. Electricians 02

4. Maistry 03

5. Library Assistants 02

6. Office Assistants 03

Total 14

194

No01

0203

Eli

0506070809101112131415.16171819202122

Li

L26

HANYAKUMARI DEVASWOM BOARDSCALE OF PAY OF STAFF

DesignationAssistant DevaswomCommissionerDevaswom Accounts OfficerSuperintendents ofDevaswomThiruvabharaflam SpecialOfficerManager (office)Manager (Devaswom)Technical AssistantMaramath Section OfficerAssistantsAuditors (U.D)Junior AssistantsAuditors (L.D)Librariam

SrikariamTreasurerHead accountantChandramAccountantManager (P.D .DevaswomOverseerDraftsmanSuboverseerElectricianLast grade servantsWork Superintendent

Scale of Pay Rs300-600

300-600250-400

250-400

180-3QJ180-3QpJ150-37J150-375125-175125-17590-14090-14090-14090-14080-11080-11080-11070-10070-10070-100

125-175125-17590-14070-100

50-6030-60

195

Administration under legislation:

In the devaswoms of former Travancore and later

Kanyakumarj district, the major tool for the administrative change

was the statutes enacted from time to time. They are mainly the

Travancore - Cochin Hindu Religious Institutions Act, 1950

(T.C.Act XV of 1950), Tamilnadu Religious and Charitable

Endowments Act, 1959 (Tamilnadu Act 22 of 1959) and Tamilnadu

(Transferred Territory) Incorporated and unincorporated Devaswom

Act, 1959 (Tamilnadu Act 30 of 1959). The rules framed thereunder

streamlined the administration of devaswoms by giving a new

framework and functioning. The evolution of devaswom

administration shows two district stages29 . They are the devaswom

administration of the erstwhile Travancore state and devaswom

administration after the merger of transferred territories to Madras

state30 . These two stages clearly differ in nature and pattern of

devaswom administration. In spite of this system of administration

prevailed in Travancore continued to exist in Kanyakumari district

29 Adminstratjon Report, op.cit., p.1.

30 Transfer of the four Tamil speaking taluks (Thovala, agastheeswrarn,

Kalkulam and Vilavancode) to Madras State. (B.Maria John, op.cit, pp.78-88)

196

till formation of Kanyakumari Devaswom Board which was formed

in April 1960. During this period, the.. government brought the

above statues and subsequently a number of amendments. These

statues and amendments changed the administration of

devaswoms to a large extent.

The Hindu Religious Institutions Act of 1950 is a milestone in

the administration of devaswoms in Travancore after the abolition

of monarchy in the state. Similarly the Tamilnadu H.R.&C.E Act

1959 is an important landmark in the history of temple

administration in Tamilnadu. The administrative pattern of

devaswoms in the state changed drastically after the

implementation of the Act. The salient feature of this Act is that it

has given provision for the formation of charitable endowments

with the temples. In Hindu system there is no line of demarcation

between religion and charity. On the other hand charity is regarded

as part of religion. Hence charitable endowments were formed as

part of religious structure 31 . However the traditional aspects of

devaswoms have been protected by this Act. The legacies and in

roads of the previous temple administration and traditional

31 R.Sengottuvelafl, Tamilnadu H.R.&C.E. Act,1959, Madras, 1989, p.6.

197

aspects, materialised the H.R.&C.E., Act of 1959 into a moulding

frame work for the H.R.& C.E., administration32

According to the Act, a trust Board is constituted for each

temple and the trustees are nominated to the trust. The trust

Board is called aramkavalarkuzhu and the trustees are called

arumkavalarkal. The administration of the temples is handed over

to such trust Boards. Certain qualifications are prescribed for

becoming a trustee. He is not eligible to be a trustee if he does not

profess the Hindu religion 33 . The trustee of a religious institution

shall bound to obey all lawful orders issued under the provisions of

this Act by the government, the commissioner, the deputy

commissioner or the assistant commissioner. The trustees may be

hereditary trustees or the persons selected by the area committee.

They are appointed by the assistant commissioner as per the

provisions of the Act. Every Board of trustees constituted must

consist of not less than three and not more than five persons. One

shall be a member of the scheduled caste or scheduled tribe34 . They

32 S.V.MurUgafl., Tamilnadu H.R.&C.E Act 1959, Coimbatore,m 1983, p.4.

Tamilndu H.R.&C.E Act, 959, S.26(a)

TamilnadU H.R.&C.E. Act, op.cit., S.47, 1(2c).

198

can elect a chairman for the trust Board from among the members.

A trustee can be suspended, removed or dismissed on valid reasons

by the appropriate authority 35. One of the notable provision

included in the Act is the membership of a scheduled caste person

in the trust Board which can be termed as a progressive measure.

This is not guaranteed in the Board constituted under Travancore-

Cochin Hindu Religious Institutions Act 1950.

The Tamilnadu (Transferred territory) Incorporated and

unincorporated Devaswoms Act, 1959 (Act,30 of 1959) was brought

about for the administration and control of the incorporated and

unincorporated temples of the transferred territory. This Act gave

provision for the formation of Kanyakumari Devaswom Board36

The Board functioned under the control and authority of the

commissioner H.R.&C.E. Department, Madras. This was a major

difference between the Travancore Devaswom Board and the

Kanyakumari Devaswom Board. This Board only supervised the

administration of 490 devaswoms of the transferred territory which

had been bifurcated from Travancore Devaswom Board at the time

]bid, S.53(2)

36 Tamilnadu Act 30 of 1959, st.George Fort Gazette, Madras, March 1950.

199

of state re-organisation. The provison for the devaswom fund of

these temples has been incorporated inthe constitution of India on

the basis of the covenant entered into by the Raja of Travancore -

Cochin state with the Government of India 37 . Virtually the temples

covered under this Act are the royal controlled temples of erstwhile

Travancore. In recognition of this, one member of the Board was a

nominee of the maharaja of Travancore. A saving clause has also

been included in the Act38 . It says that nothing contained in this

Act shall affect or authorise any interference with the right and

privileges specified in schedule III to which the ruler of Travancore

is entitled by custom, established wage or otherwise. In the

schedule III many customs, established usages were prescribed.

Vazhivad on the birthday of His Highness and Kanikka offerings

by the Maharaja at his visit were common features in all the

temples39 . Navarathri puja is another custom followed in the south

Travancore. Every year as per the date and time fixed by palace,

Saraswathy Amman from Padmanabhapuram palace temple,

37 Eastern Book Company, (ed), Constitution of India, Article 290A, Lucknow,

1986, p.116.

38 Tamllnadu Act 30 of 1959, op.cit., S.32.

39 Ta,nilnadu Act 30 of 1959, op.cit., Schedule III, S.32.

TIIs]

Subramaniaswamy from Velimalai kumarakoil and Munnotti Nanga

Amman from Suchindrum temple are brought in procession to

Trivandrum and after puja etc in the palace they are taken back

after Vijayadasami. Necessary arrangements in this connection are

being done through the chief secretary to the Government. This

ceremony is still continuing as a semi-government function. Hence

the old systems are followed in the devaswoms of Kanyakumari

district, inspite of many years rolled after the state re-organisation.

This is due to the aforesaid provision included in the Act as well as

the customary belief followed by the people of this area.

Income and Expenditure:

The Kanyakumari Devaswom Board acted as a controlling

body with systematic supervision and control of the devaswom

finances here. The main source of income was the devaswom fund

constituted at the time of state reorganisation for the benefit of the

temples in the transferred territory. Accordingly, the annual

government contribution was fixed as Rs. 13.5 lakhs every year40.

This was guaranteed under Article 290A of the constitution of

° Adminsitration Report, op.cit., p.7.

201

India41 . This amount was given in lieu of the devaswom lands being

converted into pandarapattom or sircar lands42 . However this is

not the only source of income to the Kanyakumari Devaswom

Board. The Kanyakumari devaswom Board also received as its

share a sum of 24 lakhs from out of the devaswom surplus fund.

This amount has been invested in fixed deposit in scheduled

banks43 . Besides the above, the income derived by way of lease of

remaining lands, interest from investments made by the Devaswom

Board in banks and other financial establishments, rent from

buildings constructed at the temple premises and rented for shops,

kanikkas, nadavarvu etc from devotees are the other sources of

41 Annual payment to certain Devaswom Funds........A sum of Thirteen lakhs

and fifty thousand rupees shall be charged on and paid out of the consolidated

fund of state of Tamilnadu every year to Devaswom fund established in that

state for the maintenance of Hindu temples and shrines in the territories

transferred to that state on the 1st day of November 1956 from the state of

Travancore - Cochin(Indiai-i constitution Act 290 A, op-cit., p.1 16)

42 Chithiraputhra Pillai, 'Devaswom Finance -A study, kanyakumari

Devswom Board Sovenir, op.cit, p.52.

IbicL,p.52.

202

income for the devaswom 44 . However, the source of receipts have

shown steady increase since 1956.

Year

1957-58

1958-59

1959-60

1960-61

1961-62

II!iii%1

Receipts

1453561.47

WITISMS -13M

1491864.22

1503595.10

1511143.77

1949881.60

Expenditure

1532804.26

1446758.34

1446232.20

1568052.36

1568399.62

1612905.74

The increase in the income was mainly due to the increase in the

kanikkai and nadavaravu such as hundial receipt and archanai

kattanam, thulabharam, vadamalai (in Suchindrum temple) and

other vazhivadus of the devotees.

Kanyakumari Devaswom Board Administration Report, op.cit, p.71

Devaswom Minutes, Suchindrum, June 1963.

203

The landed properties belonging to the temples have also been

a source of steady income to devaswom. The temples under

Kanyakumari Devaswom Board owned the following landed

properties.

(1). Wet lands

137.57 Acres

(2). Dry lands

234.76 Acres

(3). Manavari

647.56 Acres

The annual income expected from the above properties are (i)

Rs.37500/- in cash and (ii) 60900 litres of paddy in kind. Yet this

is not properly received by Devaswom Board annually without any

lapse. At the close of the fasali Year 1400, the pending collection

amounts are as follows46:

f Kanyakumari Devaswom Board Administration Report, op.cit, p.6.

204

(i) Lease amount in cash

Rs. 1002713

(ii) Building rent

Rs. 14031 10

(iii) Lease amount in kind

53628 1.250(Litres of

Paddy)

Nadavaravu:

The income derived from the presentation and offerings by the

people is called nadavaravu. While much revenue was obtained

from land revenue, nadavaravu too formed a major source of

income of the temples. Presentation or kanikkas made to the

devaswoms in the form of coins, silver, gold, jewels, vessels, lamps,

silks, livestocks, grains, coconuts and other articles formed

nadavaravu47. Some articles like fruits, sugar, sandal etc were

received as thulabarams. In some temples strong Hundials were

47 Proceedings of the government regarding the Recorganisation of Devaswoms,

Trivandrum, p.16.

205

kept at the entrance of the temple for the people to deposit their

kanikkas. Nadaikkuvaipu kattanam for kavadi etc. are also

considered as nadavaravu. Sale proceeds of offerings like

sanchayachoru, parayeedu etc. will also make income to he

devaswoms48 . The live stocks received as offering in certain temples

were also auctioned49 . In some temples of rural area the people of

the locality, per house contribute a monthly amount called

masavari for the conduct of customary pujas of the temple.

Vazhivadus:

Vazhivadu is another source of income to the temples.

Nivedyam or food offering to the temples made by private

individuals are called vazhivadu. The vazhivadu articles are

entrusted to the santhikaran for preparation and performing-50 . A

fixed amount should be remitted to the devaswom as fee for each

vazhivadu. In some temples cracks are offered as vedivazhivadu

48 Travancore .Devaswom Manual, Vol. 1 'p.233.

' Government of Travancore, G.O.No.2013, Revenue Department,dated 23

Edavam 1086M.E(June 1900).

50 Proceedings of the Government regarding the organistion of Devaswom,

op.cit., p.16.

206

and a particular rate is fixed for each crack. In some temples

annual auction will be conducted to perform vedivazhivadu of a

year and income is received in advance as a lumpsum 51 . Archana

is another vazhivadu in which the offering is made in the name of

a particular individual. There is a fee for performing archana and it

is known as archana kattanam, which is a source of income to the

devaswom52.

Expenditure:

Each temple is a large consumer. Much of the income is spent

for the conduct of pujas and other related festivals. The ceremonies

for which expenditure is incurred may be broadly divided into

ordinary and extra-ordinary ceremonies-53 . Ordinary ceremonies are

nithyanidanam, masavisesham, attavisesham and ulsavam,

while extraordinary ceremonies are conducted for special occasions

on specific reasons. A considerable amount is spent for these

51 Auction of Vedivazhivadu at Vettuvanni Kandan Sastha Devaswom,

Martandam, Kanyakumari district.

52 Velimala Kumarakoil temple - Special Archana Rs.5/-, ordinary Archana

Rs. 3 / -The Travancore Devaswom Manual, vol.11, 1956, p.120.

207

ceremonies. In some temples the ceremonies on particular days

are conducted at the expense of certain private individuals 54 . For

minor and petty devaswoms all payments are made from the

deputy commissioner's office, Suchindrum by way of cheque on

production of bills and vouchers by the concerned temples-55 . A

register is maintained for each group in addition to the cash book

of expenditure-56 . The income derived and the expenditure made are

done as per the budget sanction for the particular financial year.

There are some temples in the district, which enjoyed grants

from Devaswom Board-57 . Apart from this the renovation and

reconstruction of temples were being systematically carried out

from year to year according to an approved scheme of the

maramath department functioning under the Devaswom Board.

But due to the scarcity of funds, this could not be carried out

promptly and regularly. Purchase and repair of temple cars, vessels

and other articles form a major expenditure. The cleaning of temple

ponds, white washing and painting etc. are the obligatory items of

The Travancore Devaswom Manual, vol.1, 1954, p.125.

Budget File No.F3, R.C.No.2193/62 of kanyakumari devaswom Board.

The Travancore Devaswom Hand Book, op.cit., p.208.

Vide in the Appendix VII, pp.57-58.

208

expenditure. Similarly some unexpected items of expenditure such

as the repair of temple car of Suchindrum etc. by fixing two new

wheels for the car, have to be carried out 58 . The feeding cost of

elephants and other live stocks belonging to the temple also incur

expenditure.

Besides, the Act has provided for a certain non-devaswom

expenditure such as for the social, educational and cultural

advancement of the Hindu community59 according to the

availability of funds after meeting thc obligatory items of

expenditure. Under this category of expenditure, the expenses for

starting schools, colleges, libraries and grant for other cultural

institutions are coming. The Kanyakumari Devaswom Board has

started schools at Mondaikkadu, Tripparappu, Kuzhithurai and

Suchindrum and a college at Kuzhithurai. A library at Nagercoil

was also started60.

Another major item of expenditure is the salary and wages

given to temple servants other than the departmental officers and

58 Kanyakumari Devaswom Board Minutes, Suchindrurn, June 1964.

The Ta,nilnadu Act3O of 1959, s.18.

60 Kanyakumari Devaswom BoardMinuteS, Suchindrum, 1961-67.

209

employees who are paid directly from the devaswom fund. The

enhancement of dearness allowance, contributory provident fund,

pensionary benefits, travelling allowances, mahout wages etc are

met from the devaswom revenue. Hence almost all the thirty items

of expenditure6 ' existed during the period of Travancore Devaswom

Board existed under the Kanyakumari Devaswom Board also.

A budget is prepared for each financial year and the

expenditure is made in accordance with the budget provisions.

Unlike in government, the expenditure has to be limited to the

receipts of fund. There is no provision for a deficit budget since the

deficit could not be adjusted through the mobilistion of more

income from other means. Hence the receipts and expenditure

would always be tallied and in some cases the expenditure would

be less than the receipts62 . The Board must submit the budget to

the commissioner, H.R.&C.E department, Madras63 . The

commissioner has full power to make alternations, omissions, or

additions in the budget as he may deem fit and proper. His decision

61 Travancore Devaswom Manual, op.cit., p.243.

62 Kanyakumari Devswom Board Financial Report, 1961-71.

63 The Tamilnadu Act 30 of 1970, pp.3-4.

ME

is final in this respect. This principle is certainly a retrograde

step64 . The Travancore Devaswom Boar ,I has more powers

regarding the budget. There, the Board is more or less an

autonomous body accountable only to the high court concerning

budget and auditing. But the H.R.&C.E department, Madras was

more powerful than the Kanyakumari Devaswom Board.

The following details regarding receipts and expenditure give

the real picture about the budget of Kanyakumari Devaswom Board

R.Ramaswamy pillai, op.cit., p.16.

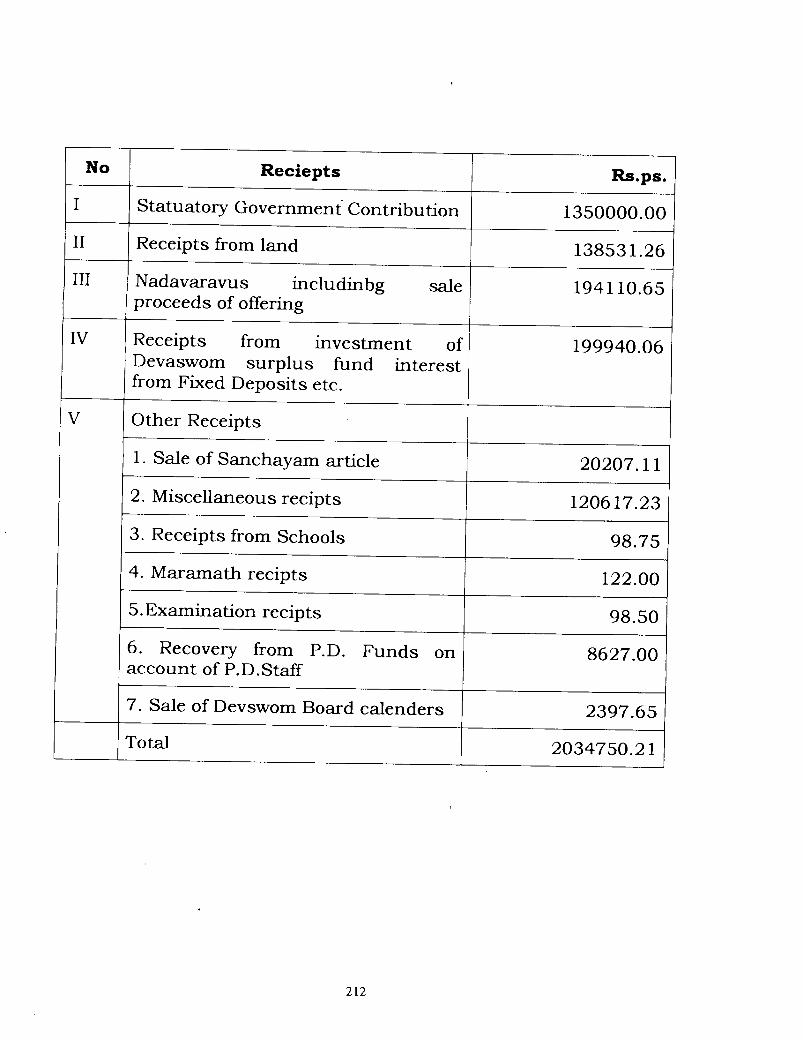

211

No Reciepts Rs.ps.I Statuatory Government Contribution 1350000.00II Receipts from land 138531.26III Nadavaravus includinbg sale 194110.65

proceeds of offering

IV Receipts from investment of 199940.06Devaswom surplus fund interestfrom Fixed Deposits etc.

V Other Receipts

1 Sale of Sanchayam article 20207.11

2. Miscellaneous recipts 120617.23

3. Receipts from Schools 98.754. Maramath recipts 122.005.Examination recipts 98.506. Recovery from P.D. Funds on 8627.00account of P.D.Staff

7. Sale of Devswom Board calenders 2397.65Total 2034750.21

'IPI

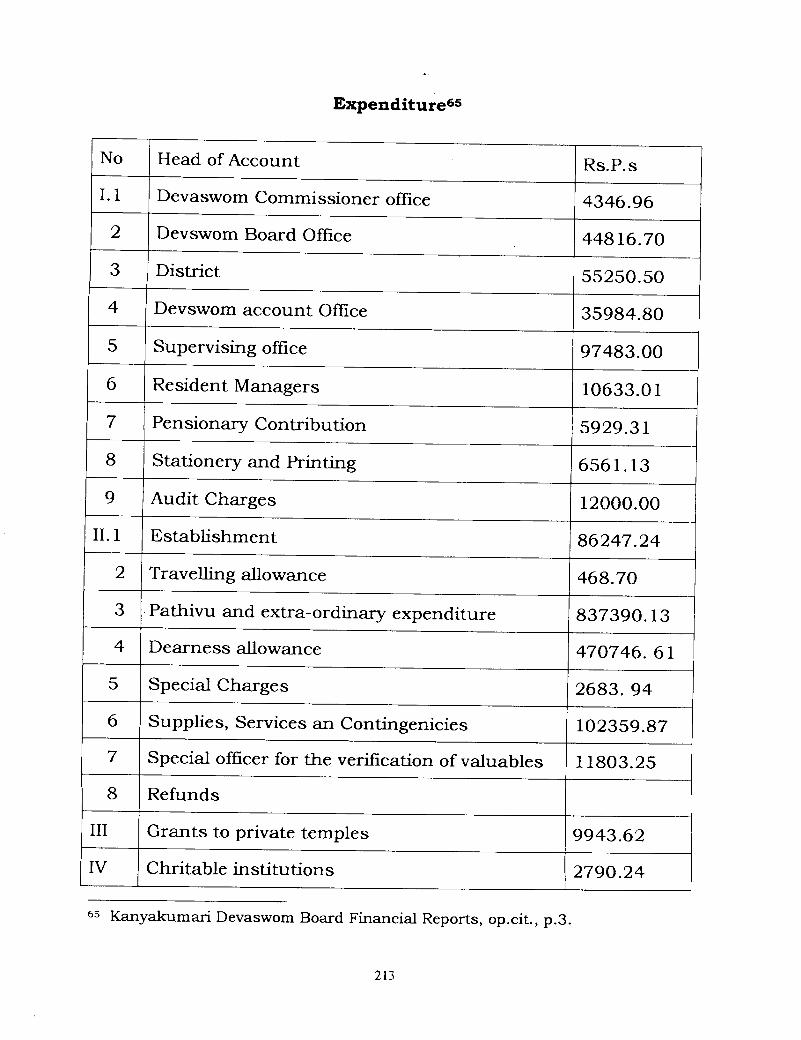

Expenditure65

No Head of Account Rs.P.s1.1 Devaswom Commissioner office 4346.96

2 Devswom Board Office 44816.703 District 55250.50

4 (Devswom account Office 35984.80

5 Supervising office 97483.00

6 Resident Managers 10633.01

7 Pensionary Contribution 5929.31

8 Stationery and Printing 6561.13

9 Audit Charges 12000.00

11.1 Establishment 86247.24

2 Travelling allowance 468.70

3 Pathivu and extra-ordinary expenditure 837390.13

4 Dearness allowance 470746. 61

5 Special Charges 2683.94

6 Supplies, Services an Contingenicies 102359.87

7 Special officer for the verification of valuables 11803.25

8 Refunds

III Grants to private temples 9943.62

IV Chritable institutions 2790.24

Kanyakumari Devaswom Board Financial Reports, op.cit., p.3.

213

V

VI

VII

VIII

Ix.

X

XI

XII

XIII

XIV

Payments to surplus fund

Law Department

Maramath Department

Capital Expenditure

Educational Department

Social uplift

Cultural Advancement

Inrterest on Provident Fund Deposits

Conrtribution on Account of D.C.P.F

Arrear claims

Total

10000.00

4058.96

80135.53

14658.58

975.00

2925.00

17418.00

1927610.08

214

Financial position:

When years passed by expenditure exceeded the income. For

example for fasli year 1400, the expenditure exceeded the income

by a margin of Rs 152083/-. There are many reasons for this. First

of all the price of things have gone up considerably. An article

worth of Rupees one in the year 1960 has multiplied in cost

subsequently. Like wise the cost of materials required for the

maramath work has also increased considerably. But, whereas the

annual government contribution of Rs. 13.5 lakhs fixed during 1956

and being paid every year for the maintenance and up keep of the

458 incorporated devaswoms remain unaltered66 . Therefore the

annual maintenance works in some archaeological and historically

important temples67 were not carried out for the past several years

due to lack of funds. Further mere remuneration paid to be temple

servants also could not be increased even to the extent necessary to

suit their living68 . This clearly shows that the financial position of

the Kanyakumari Devaswom Board was not at all satisfactory. In

66 kanyakumari devaswoms Board Adminsitration Repoert, op.cit, p.7.

67 Vide in the Appendix VIII, pp.59-61.

68 Ibid. p.7.

215

order to improve the financial condition of the Devasworn Board

many novel schemes have been planned and implemented. It has to

be done systematically and effectively with a long run programme.

The kanyakumari Devaswom Board has taken effective

measures to improve the income of the temples. Many experts and

experienced persons were consulted for this purpose. In many

important temples, new vazhivadu schemes such as laksharchana

and kodiarchana have been conducted. Many worshippers came

forward to contribute for the new vazhlvadu schemes69 . The Board

has also taken the following decisions to improve the income

sources of the temples

(1) To allow the devotees to enter the temples wearing

pants, shirts etc so that there will be, an increase in the

number of devotees. So the kanikal offerings to the

temple will also increase.

(2) To lease the temple tanks to the Department of

Fisheries for fish culture.

69 AdminstratiOn Repoert, op.cit, p.12.

216

(3) To hire the vacant mandaparns for daily rent to conduct

marriages.

(4) To construct buildings for shops and Thirumana

Mandapams in the available vacant sites with bank loan

and public contribution.

(5) To keep open the main door of the temple more time so

that the pilgrims and tourists arriving at any time may

have a darsan of the deity and present their offerings.

Some of the decisions of the Board seem to be against the

established usage and custom of the temples, yet it can be allowed

to the extent they do not affect the sanctity of the temples. The

kanyakumari devaswom Board functioned fairly well till its

abolition in December 1974.

217

CONCLUSION

The state of Travancore had thc complexion of a Hindu

state by virtue of the domination of Hindu population and reign of

Hindu sovereigns. The Hindu character of the state was re-enforced

when the rulers assumed the bile 'sreepadmanabhadasa', which

symbolised that the ruler being the dasa or servant of

Sreepadmanabha, the prime deity of the royal family.In Travancore

most of the temples were founded and endowed by Hindus and

managed by trustees called uralars.In course of time enormous

wealth accumulated in the temples by way of donations from the

people and the ruler. The state had direct control over a few

temples but it exercised melkoyma right over the management of

other temples. The uralars not only enjoyed unrestricted power in

the administration of temples but also exercised judicial and

executive powers among the people within the temple sanketams.

Later they became corrupt and began to misappropriate the funds

of the temples. As a result the pujas and other ceremonies were not

held properly in some temples.

218

On seeing the ugly state of affairs of the temple

administration Col Munro,the resident dewan of Travancore took

over the management of 348 major and 1123 minor temples with

all their properties. This was a turning point in the history of

temple administration of Travancore. The orders of the government

emphasised that the assumption was in the interest of better

management of temples. However, much criticism was levelled

against the assumption by several Hindus who considered the act

amounting to that of confiscation of temples and their properties.

This contention was rejected by the Travancore high court holding

that the position of the government was only that of a trustee and

the government was not entitled to transform the properties

belonging to temples into sircar properties. Thereafter the revenue

department was entrusted to administer the temples of Travancore

and the pandaravalca properties. Yet the administration of temples

by the revenue department was also not an unmixed blessing. The

inconvenience felt by the revenue authorities leading to their

inability to look after the affairs of the temples was the first reason

to demand for a separate devaswom department. Secondly the non-

219

Hindus and non-caste Hindus demanded for the separation of

devaswoms from revenue department since they were kept off from

the appointment of revenue department which included

devaswoms, owing to the rigidity of caste rules. The sovereign also

convinced that the assumption of administration by the

government did not make any change in the quality of

administration. Therefore the government appointed a committee

to enquire and report on the feasibility of separation of devaswoms

from land revenue department. The committee favoured for the

separation which culminated into the formation of devaswom

department in April 1922. Though the devaswom commissioner

was the head of the newly formed clivaswom department, he

functioned under the dewan of Travancore. When examining the

devaswom administration from 1811 to 1922, it is evident that the

governmental interference in the administration of temples did not

fetch any improvement to the devaswoms, lest it harmed the

existence of such devaswoms. But the trent began to change

gradually after 1922, when the newly formed devaswom

department began to function in the right direction by introducing

many reforms in the devaswoms of Travancore. But one can not

expect that the earlier evils melted in the administrative machinery

220

of the temples could be removed all on a sudden. However these

reforms opened the door for the genesis of popular movements for

temple entry to all sections of Hindu community irrespective of

caste, creed and social status. These movements gained

momentum inviting more charges in the temple administration of

Travancore. The historic temple entry proclamation made by the

maharaja of Travancore on 12th November 1936 had a positive

impact on the society that accelerated the process of social change

through spiritual freedom and equality of worship. It paved the way

for popularisation of temple worship in Travancore, which had its

repercussions in many ways. Due to the increase in the flow of

Hindu population to the temples, there was an improvement in the

general economy of temples. This necessitated for proper regulation

in the financial administration of temples which included

accounting and auditing of funds collected through various

sources. Moreover with the abolition of monarchy, the dawn of

democracy appeared and the religious institutions were

democratized in the light of new legislations. Thus the Travancore -

Cochin Hindu Religious Institutions Act, 1950 was enacted by the

Travancore legislative assembly which provided for the

establishment of Travancore Devaswom Board.

221

The Act envisaged a well-defined devaswom

establishment with the creation of a Devaswom Board along with

the hierarchy of officers and employees for the control and

management of devaswoms. The evaluation of the working of

Travancore Devaswom Board upto 1960 reveals that the Board can

provide effective administration to all categories of temples existing

in the state.

In 1956,due to state re-organisation the Travancore

temples were bifurcated and 490 temples of the transferred

territory were handed over to the newly formed Kanyakumari

Devaswom Board. The special study on the administration of

temples in Kanyakumari district from 1956 to 1960 shows many

unique features. The temples here got the legacy from Travancore

and the pujas, rituals and ceremonies conducted here are very

much similar to that of Travancore temples as per the established

custom and usages. Therefore these 490 temples still preserve a

kind of separate identity from other temples of Tamilnadu.

However, as time went on, some changes have taken place in the

222

administrative set up of these temples due to the application of H.R

& C.E. Act of Tamilnadu. Subsequently, the Kanyakumari

Devaswom Board which was established in 1960 was abolished.

Yet these 490 incorporated and unincorporated temples are still

under the control of a separate deputy commissioner and executive

officer working at Suchindrum where once the Kanyakumari

Devaswom Board functioned.

223

GLOSSARY

A

Abhishekam Pouring water,milk,ghee etc over thehead of the idol.

Achimar Nair woman sweepers in temples.

ikdayara A fee paid by temple priests whenthey get transfer from one templetoanother.

Adhikari Village officer.

Adukkuvat A renewal fee on lands.

Agamas Tantra text or treatise on templeworship.

Agrasala Feeding house attached to sreePadmanabhaswamy templeTrivandrum.

Akattepad ithram

Chief executive officer.

A temple servant to look after theinternal affairs of temple.

Expentiture for the ritual itemsinside the temple.

Akakkoima

Akatternan usyam

224

Akapotural temple servant in charge of internalmanagement.

Alakku-virutti

Alan karamandapam

Lands leased for cloth washingservices in temples.

The pillard structure where thedecorated idol is seated for publicView.

The sharing system of revenue.

A part of the ceremony of theTalikket' of Devadasis

Amani

Am argam

Aminadars Officers of the Revenue Departmentdeputed for technical supervisionin temples.

Am palapati A person who supervises templeproperty.

Ampalavasi Hereditary servants of templesperforming various duties outsidethe inner shrine.

Anaval Manager of a temple.

Anjali A land tax imposed on private paddylands.

An A Tamil month corresponding to theMalayalam month Mithunam(June-July)

Anubhogam A right of enjoying allowance inlands.

225

Arayalam

A temple ceremony.

The ceremonial bath of the idol of adeity at the end of the

festival.

a tax collected from the gaden lands.

Apamargam

Aratt

Archana Offering flower before the deity byreciting verses for the welfare ofthe devotee.

Arilonnu

Ashtabandakalasam

Fee for archana

A Pillard structure just in front ofsanctum sanctorum.

One sixth (a measurement of renton leases land)

A ritual followe in temples whilefixing the idol in the pedestal.

Archanakattanam

Ardhamandapam

Athazhapuja Night ritual.of the temple.

Attavisesham Ceremonies in the temples onspecial days in each years.

Asudhj Pollution

Adima Slave.

Audi A Tamil month corresponding toKarkidakam of the Malayalam era.(July- August)

Avani A Tamil month corresponding tochingam of th Malayalamera.(August-. September)

226

Avarnas Non-caste Hindus.

Ayacut Land revenue account or permanentsettlement record.

Bali

Balikkalpura

Bhad radeepam

Brahmaswarn

Sacrifice, Offering.

Hall with pillars where the balikkal(sacrificial stone) is set.

Festival of Lamps- A half yearlyfestival in the sreePadmanabhaswamy temple atTrivandrum.

Wealth of land belonging toBrahmanas.

Idol.

C

Cora otti

A copper coin of Travancore.

A low caste in Hindus.

A service tenure for preparingsandal paste in temples.

lands purchased by Governmentfrom Devaswoms.

Chakram

Chandala

Chantu-Viruthu

227

Chuttu-Viruttj

Chingam

A service tenure to carry the torchesin front of the deity duringprocession.

Malayalam month cirresponing toAugust- September.

IC

Dakshina

Danam

Dasan

Dasi

Deva(Devan)

Devadanam

Devadasj

Devad ayam

DevanadyUranma

Devaswom

Devaswom Pilla

Devaswomvaka

Customary gift of money,Cloth etc.to Brahmins, priests, preceptors etc.

Gift or aim.

Male servant

Female servant

Heavenly Immortal

Gift to god both movable andimmovable received from devotees.

Maid of God; a woman dancer,singerattached to a temple.

Wealth belonging to God.

Village temples dedicated to thedeity.

Assets of God: a templeestablishment.

Accountant of a temple.

Property of a temple.

228

A title given to the chief minister ofTravancore after A.D. 1784.Head of the Revenue Department ofthe state of Travancore.

Malayalam month corresponding toDecember- January.

Canons of rules and customs of thestate.

Flag staff

A ritual connected with theinstallation of temple flag staff.

Dewan

Dewan Peishkar

Dhanu

Dharmasastras

Dhawajastam bha

Dhawajaprathishta

E

Edavam(ltavam)

Elavanipattam

Ezhuthitheeruvayulla

Ezhuthitheeruvayillatha

Ettarayogam

Malayalam month corresponding toMay-June

A tenure for supplying beta] andplantain leaves to temples.

Incorporated devaswom

Unincorporated devaswom.

Royal Council of eight members.

F

Fasli year Revenue year

229

G

Garbhagraha Sanctum -Sanctorurñ

Gopuram A pyramidal or multistoreyed towerover the gate way of a temple.

H

Boundary

Dewan 's office

Proclamation.

I

A measure containing eighty cubicinches.

An upper class community amongthe Avarnas.

Voluntary gift (rent free land)

Tax free

H a ra

Huzur

Hukkumnama

ltangazhi

Izhavas(Ezhavas)

Inarn

I rayili

230

3

J alaj apam Chanting of vedic hymns at hetemple tank

Jamabandhi The term used for the threedepartment of Treasury, Revenueand Finance under old system.

Janmam land

Japam

Janmi

Janrnibhogarn

Land owned by the nobles or landlords.

Chanting of vedic hymns or namesof Gods.

Land lord

A share of a land lord

Its-Kaccam(Kacham) A fine imposed on uralar for

fraudulent dealings

Lands given for military service

Hand written receipt

A hereditary duty or privilege of atemple servant

Store keeper

A temple sevant in charge of theadministration of properties

Kacha Virutti

Kaichartt

Kalakam

Kalavarakkaran

Kampittan

231

Kanakkan

Kanam

Kanappattam

Kanikka

Kanni

Kantukrisi

Kara

Karakkar

Karamozhivu

Karanma

Kariakkar

Accountant

A type of land tenure possession ofland

The land mortgaged for money

Offering to God

Malayalam month correspondingSeptember-October

A kind of tenure

Village

Villagers

Exemption from tax

Hereditary right of tenants for doingcertain duties in the temples

Administrative head of a taluk

Karthikai Tamil month corresponds toVirchikam of theMalayalam Era(November- December)

Kavu

Karkitakam

Kizhsanthi

Koda Maholsavam

Kovil Adhikarai

Serpant grove located near temples

Malayalam month corresponding toJuly-August

Subordinate priest in a temple

Annual celebration in theBhagavathy temples ofsouth ,Travancore

Administrative authority of a temple

232

Koy im a

Kudirnana

Kudiyan

Kum bham

Kunibanyasa

A government officer to supervisethe temple

Free house site

A tenant or serf

Malayalam month corresponding toFebruary-March

A temple ceremony

Kuttakapattam Lease of government lands for adefinite period or on permanentbasis

Kuruthi Sacrifice(A ritual in certain minordeity temples)

L

Lakshadeepam A sexennial festival of one lakhlights. (The Siveli mandapam of SreePadmanatha swamy temple atTrivandram is decorated with onelakh lights)

M

Makaram

Man u syam

Maryada

Masappadi

Malayalam month corresponding toJanuary- February

Temple servant or member of atemple council

Custom

Tax collector

233

Masavan Monthly contribution to temples

Masavisesharn Monthly festival day of the temple

Matilai<am-Grancjhavarj Old cadjan records relating totemples kept in the repository ofSree Pad manabha swamy templeatTrivandram

Medam Malayalam month corresponding toApril-May

Melanma

Mithunam

A right of permanent pattam givento tenants by the janmi

Chief or senior Accountant

Supervisory power

Senior member of a temple council

Principal priest of a temple

A portion of produce given to theking or land lord on pattam account

The land lord's share of all crops

Malayalam month corresponding toMarch -April

Malayalam month corresponding toJune- July

One of low (Polluted) Class.

Administrative division of a taluk.

Melelutt Pillai

Melkoyma

Melmanusyam

Melsanihj

M elvararri

Michavaram

Minam

Mleccha

Mukharn

Murajapam A religious ceremony in the SreePad manabhaswamy temple heldonce in six years and it concludeswith lakshadeepam ceremony.

2.4

Muri Sub division of a village or 'Kara'

N

N ad avarav u

Naduvazhj

Na lam balarri

Na ma ska ram

Nazhi(nali)

Natakava] Virutti

Nitt

Income of temples in the form ofgifts of money.

A Local Chief ruler (Itaprabha)

Cloister around the main shrine.

Prostration before a deity king etc.

A liquid or grain measure ¼ of anitangazhi or 20 cubic inches incapacity.

Land given for watchman duty intemples.

Rule or doctrine

Causes

Early morning ritual in the templebefore holy bath.

Royal writ

Nibandha

Nim ittas

Nirmalyam

Nityanidanam Daily expense or procedure of puja.Nivedydyam Offering to God.

Nrittaam(Nrttarn) Dance

Ola Palm-leaf document

235

Olugu

Ottaikkal maridapa

Record of property entered in thesettlement register.

The single stone stage in front of thesanctum sanctorum of theSreepad manabhaswamytemple,Trivandram

IN

Pad itharam Scale of expenditure

Painkuni Tamil month corresponding toMalayalam month Minam (March-April)

Pakuti s division of land equivalent to avillage, the smallest unit of revenueadministration.

Pntheeradi puja

Pathivus

Para

Paru taiyar

Pandaravaka

Pandarapattom

Patta

Ritual conducted in between athemorning puja and noon puja.

Regulations, customary accountsand payments.

A grain measure equivalent to tenIntangalis or a 800 cubic inches

A village officer.

Government property

Governtment pattom

Land registration document.

236

Pattu parivattom Cloth for idol.

Pattu virutti Land given for supply of silk clothfor the idol.

Pavitrata Purity.

Payasam Pudding prepared with rice or othergrains, milks and sugar orjuggery.

Pei shkar District head of the revenuedepartment.

Pra kara The outer wall of the templeprecinct.

Prasadam Sandal, flowers and scared foodoffered to the deity and issued tothe devotees.

Puiateman u sysam

Pu rathepaditharam

Image of the deity.

Offerings to the deity or rituals

Vedic treastises based on Hindumythology.

Temple servant to look after theexternal affairs of a temple.

Expenditure outside the temple forvarious functions.

Pratishata

Pujas

Pu ranas

Puruttasi Tamil month corresponding toMalayalammonthKanni(Septemher - October)

237

it

Rajabhoga m Light rate rent levied in thecase of favourable tenures.

S

Sanku Virutti

Sannad

An official communication.

Vedic School

Temple Manager.

Revenue department land.

Temple domain whereimmunity for Brahminsprevailed from stateinterference.

Lease of land granted forblowing knoch-shell intemples.

A government order ofauthorisation or licence.

Priest or priest hood.

Temple priest.

Lease of land for priestlyservices.

Sad hanarn

Salai

Sam udayarn

Sa nchayam

San ketain

San ti

Santikars

Sand virutti.

Sarvad h ikariakkar

Sastras

Sattar

Sattavariyola

Satvagraha

Savarn as

Sircar

Sh roff

Sreepadarn land

Sreepandaravaka Land

Sriveli orsriI)elI

Srikaryakkaran

Tai

Adminsitrative head (officer) ofa district.

Canons of law and conduct.

Student who studies vedas andupanishads.

A set of rules framed for theguidance ofgovernmentofficials.

Non-violent residence

Caste Hindus

Government.

Cash keeper

Property, temple belonging toMaharaja or Maharani ofTravancoreLands belonged to SreePad man abhaswamytemple,Trivandrum

Sribeii (offering)held atprescribed times in thetemples.Temple manager.

IN

Tamil month corresponding

to Malayalam month

239

Makaram(January- Fubrury)

Tantri

Tindal

Tindal palakas

Tiratt

Tulabharam

Tularn

Ritual ,Ceremonies

Book of vedic prescription forrituals

An ecclesiastical dignitary whohas learned the art ofexhibiting proper signs andsymbols accompanied by -

'mantras'

V i llage Assemly

Members of Tarakkuttam

Ornaments for the idol.

Holy marriage(A festive! inVellimalaj Kumara Koil

Temple)

Untouchability, pollutioncaused aby low castes.

Wooden boards marking thelimits of approachability

(Prohibitive sign board)

A general abstrct of alltransaction including reciptsand expenditure for the year.

Ceremony of weighing the bodyagainst precious articles, asan offering at temples.

Malayalam monthCorresponding to October -November

Tantram

Tantrasamuchayam

Tarakkuttam

'i'iravazh is('Faravalj s)

Thiruvabharanams

Thiru kalyanam

240

U

Uchapuja

Uliyam

Ulpadan

Ulsavam

Unnis

Ur.

Uralar

Uranma

Uranamakkar

Ushapuja

Uttu pura

Noon ritual in temples.

Service rendered in return forthe enjoyment of landsgrantedfor the purpose.

A temple servant in charge ofthe internal matters.

Festival in temples.

A temple servant belonging tothe Ambalavasi group.

Village

Trustees

Ownership of Temples.

Village headman who managedthe lands.

Morning ritual in temples.

Free feeding centres for theBrahmins

V

Vatavilakku Perpetual Lamp

Vaid ikan Learned men in the vedas

Vazhivad

Offering to a deity

241

Vanchi

Variyam

Variyola

Virutti lands

Viruttika r

Vittu Virutti

Vrisch ikani

Strong box kept in the templesfor keeping money

An elected council of a temple

A government order (or) Memoof instructions

Caste

A major land tenure system

Idol

Land leased for the service oflighting lamps in temples

A decorative arch

A Kind of free service to thestate and temples

(Service tenure)

Tax free lands granted totenants for their free service tothe state and temples

Virutti service holders

Free service to a house

Malayalam Monthcorresponding to November-December)

Varna.

Venpattam

Vigraham

Vilakku Virutti

Vimana

Virutti

k An

Warner A Temple servant of theAmbalavasi group.

242

Y

Yaga

Yoga

A sacrifice- a ritual(ceremony)in which offerings are given tothe sacred fire in the name ofGod.

Meditation

Yogakkar Member of a temple governingbody.

Yogam Management Council.

24