BICCU ANNUAL GENERAL MEEING 2020

108

BICCU ANNUAL GENERAL MEEING 2020 1

Transcript of BICCU ANNUAL GENERAL MEEING 2020

BICCU ANNUAL GENERAL MEEING 2020

1

BICCU ANNUAL GENERAL MEEING 2020

2

VISION STATEMENTTo offer economic empowerment to our members.

MISSION STATEMENTTo be the leading member owned financial services institution,

as we aim to be their primary source and support, offering friendly, quality, cutting edge services dedicated to helping

members achieve economic empowerment.

CORE VALUESCommitted to Service

Demonstrate care and concern for allCreate paths to financial freedom

Dedicated to the health and wealth of our members

BICCU ANNUAL GENERAL MEEING 2020

2

VISION MISSION VALUES

BICCU ANNUAL GENERAL MEEING 2020

3

TABLE OF CONTENTS

Vision & Core Values Inside Front Cover

Tables of Content 3

Standing Orders 4

Meeting Agenda 5

Prayer of St. Francis of Assisi 6

Message from The President of The League 7

Photos of Board of Directors 8

Photos of Supervisory, Credit & Education Committees 9

Photos of Staff 10

Directors’ & Committees’ Terms of Service 11

Minutes of the 30th AGM 12 – 24

Directors’ Report 25 – 29

Treasurer’s Report 30 – 32

Auditor’s Report & Financials 33 – 87

2021 Budget 88 – 89

Supervisory Committee’s Report 90 – 93

Credit Committee’s Report 94 – 97

Education Committee’s Report 98 – 99

Resolutions 100 – 102

2019 AGM Attendees 103 – 104

Highlights & Pictures 105 – 106

Notes 107

logo Back Cover

BICCU ANNUAL GENERAL MEEING 2020

4

• A member is to stand when addressing the Chair

• Speeches are to be clear and relevant to the subject before the meeting.

• A member shall only address the meeting when called upon by the Chairman to do so, after which he shall immediately take his seat.

• No member shall address the meeting except through the Chairman.

• When called upon by the Chairman, a member must first state his name before continuing with his comment and/or question.

• A member may not speak twice on the same subject except: a) The Mover of a Motion- who has the right to reply b) He rises to object or to explain (with permission of the Chair).

• The Mover of a Procedural Motion- such as an adjournment or postponement of the meeting, shall have no right to reply once the motion has been laid on the table.

• No speech is to be made after the “Question” has been put and carried negative.

• A member rising on a point of order is to state the point clearly and concisely. (A “point of order” must have relevance to the “Standing Order”).

• A member should not “call” another member “to order” but may draw the attention of the Chair to a ‘breach of order’.

• A question should not be put to vote if a member desires to speak on it or move an amendment to it- except, that a Procedural Motion “The Previous Question” “proceed to the next Business” or the “Closure”: “That the Question be NOW PUT”, may be moved at any time.

• Only one motion should be before the meeting at one and the same time.

• When a motion is withdrawn, it fails.

• The Chairman has the right to a “casting vote”.

• If there is equality of voting on an amendment, and the Chairman does not exercise his casting vote, the amendment is lost.

• Provision is to be made for protection by the Chairman from vilification (Personal Abuse) • Only members are allowed to speak or ask questions during the meeting.

STANDING ORDERS

BICCU ANNUAL GENERAL MEEING 2020

5

Call to OrderPrayer of St. Francis of AssisiWelcomeGreetings • The Bahamas Co-operative League Limited

Minutes from the 33rd Annual General MeetingMatters ArisingReports • Board of Directors’ Report • Treasurer’s Report • Auditor’s Report • 2021 Budget • Supervisory Committee’s Report • Credit Committee’s Report • Education Committee’s Report

New BusinessResolutionsElections • Board • Supervisory Committee • Credit Committee

Motion for Adjournment

MEETINGAGENDA 2020

BICCU ANNUAL GENERAL MEEING 2020

6

Prayer of St. Francis of Assisi

Lord, make me an instrument of Thy Peace. Where there is hatred, let me sow love

Where there is injury, pardonWhere there is doubt, faith

Where there is despair, hopeWhere there is darkness, light Where there is sadness, joy!

O divine Master, grant that I may not so much seek To be consoled as to console;

To be understood as to understand;To be loved as to love.

For it is in giving that we receive,It is in pardoning that we are pardoned,

And it is in dying that we are born to eternal life

OUR PRAYER

BICCU ANNUAL GENERAL MEEING 2020

7

Message fromMR. HILTON BOWLEGPresidentBahamas Co-operative League Limited (BCLL)

Fellow Cooperators it is indeed my privilege to extend greetings and congratulations to the Members, Volunteers and Staff of the Bahama

Islands Co-operative Credit Union on the hosting of your 34th Annual General Meeting.

2020 has been an extremely difficult year due to the Global Pandemic that has greatly affected the country and the Members of our great Movement in the most profound ways. The deadly virus, Covid-19, continues to wreak havoc on the lives and economies of the World and whilst it is believed that a vaccine will soon be available, it will take years for us to restore the economy of The Bahamas to where it was prior to the pandemic.

Your theme this year: “Weathering the storm while adapting to the new norm” is certainly what we must all do, as we work together to assist Members and continue to build a strong and vibrant Co-operative Credit Union sector. We must offer relevant products and services that meet the needs of members while adhering to the polices, laws and Co-operative Principles that govern our sector.

On behalf of The Bahamas Co-operative League Limited, I commend BICCU for its growth and advancement over the years. We know that the Credit Union will indeed weather this current storm through the dedication of its Members, Board and Staff. I also pledge the continued commitment of The Bahamas Co-operative League Limited as you pursue the advancement of the Credit Union.

Have a successful Annual General Meeting!

BICCU ANNUAL GENERAL MEEING 2020

8

BICCU ANNUAL GENERAL MEEING 2020

8

Barry RolleChairman

Hilton BowlegVice Chairman

Mark BullardAssistant Treasurer

Angela Culmer-Hinsey Treasurer

Estella Walkes-PrattSecretary

Janet GuerrieraAssistant Secretary

Gene AlburyDirector

Board Of Directors

BICCU ANNUAL GENERAL MEEING 2020

9

BICCU ANNUAL GENERAL MEEING 2020

9

EDUCATION COMMITTEE

CREDIT COMMITTEE

SUPERVISORY COMMITTEE

Rashard Ritchie Rhonda Richardson-Chase

Horatio McKenzie

Finesse Rahming

Marlon Bethel Kenneth Lightbourne

Shevaun Bain

Claudette FarringtonSecretary

David BarryChairman

A. Mary Davis Secretary

Tanishia BrennenChairman

Nashon RolleChairman

Jasmine CollieSecretary

Elston Bain A. Quentin Culmer

PhotoMissing

BICCU ANNUAL GENERAL MEEING 2020

10

BICCU ANNUAL GENERAL MEEING 2020

10

Mark BastianCEO

Jamison DavisCollections Manager

Catherine KnowlesLoan Officer I

Robertha MurraryTeller Supervisor

Bryan ButlerLoans Manager

Jayson LewisLoan Officer II

Neko MossAccounts Officer

Michelle KingMembership Services Rep. I

Maya MullingsTeller

Chandalear ForbesMarketing & Membership

Services Manager

Carolyn MossCompliance Officer

Patrice ColebrookMembership

Services Rep. II Alkeisha EdgecombeCollections Officer

Tamara StubbsMessenger/Filing Clerk

Demethera PoitierTeller

Alexandria MossMembership Services Rep. I

Michella BarryMembership Services Rep. I

Alexandria BoweFinancial Controller

Angelique McQueenInternal Auditor

Waydrissa McPhee Accounts Clerk

Delilah BarrHead Teller

Staff

BICCU ANNUAL GENERAL MEEING 2020

11

DIRECTOR ELECTED/APPOINTED 2020 2021 2022

Estella Walkes-Pratt 2017 √Hilton Bowleg 2018 √Barry Rolle 2019 √Mark Bullard 2018 √Janet Guerriea 2019 √Angela Culmer-Hinsey 2017 √Gene Albury 2018 √

MEMBER ELECTED 2020 2021 2022

Marlon Bethel 2019 √David Barry 2017 √Horatio McKenzie 2018 √Kenneth Lightbourne 2019 √Jasmine Jones 2017 √

MEMBER ELECTED/APPOINTED 2020 2021 2022Shevaun Stubbs 2018 √Archelaus Culmer 2019 √A. Mary Davis 2019 √Tanisha Brennen 2018 √Elston Bain 2019 √

BOARD OF DIRECTORS

SUPERVISORY COMMITTEE

CREDIT COMMITTEE

TERMS OF SERVICE

BICCU ANNUAL GENERAL MEEING 2020

12

1. CALL TO ORDERThe 33rd Annual General Meeting (AGM) of the Bahama Islands Co-operative Credit Union Limited (BICCU) was called to order at 6:10 pm on June 28th, 2019 in Crown Ballroom A, of the Atlantis Paradise Island Resort Hotel, by Chairman of the Board of Directors, Mr. Barry Rolle.

2. QUORUMChairman Barry Rolle read into the minutes, Section 22 (2), of the Bahamas Cooperative Credit Union Act, 2015: Quorum - “Where a quorum is not present one hour after the time fixed for the commencement of the meeting of members, the meeting shall proceed, and the members present shall constitute a quorum.”

3. PRAYER OF ST. FRANCIS OF ASSISIEstella Walkes-Pratt, Secretary of the Board of Directors led the AGM in the Prayer of St. Francis of Assisi.

4. STANDING ORDERChairman Rolle invited all to take a moment to review the Standing Orders printed on page four of the AGM Booklet.

5. ACCEPTANCE OF THE AGENDA Motion for the acceptance of the Meeting Agenda was moved by Mr. Jeremiah Hepburn, seconded by Mr. Calnan Weech and was carried unanimously.

6. WELCOMEChairman Rolle welcomed all on behalf of the Board of Directors, Committees, Management and Staff of BICCU to the 33rd AGM under the theme, “Striving to Make a Difference: Because Members Matter”. The Chairman requested a moment of silence for all of those who passed since the last AGM in particular Mrs. Deloris Cooper, wife of Founder Eugene Cooper. The Chairman extended a special welcome on behalf of the membership to Mr. Hilton Bowleg, President of the Bahamas Co-operative League Limited; Ms. Theresa Deleveaux and Ms. Jackie

Whymns of Teachers & Salaried Co-operative Credit Union Limited, Members and Guests.

Chairman Rolle invited Ms. Theresa Deleveaux to the podium to bring greetings on behalf of the Bahamas Co-operative League Limited.

7. GREETINGS

7.1. The Bahamas Co-operative League Ms. Deleveaux, extended congratulations to

the Board, Management, Staff and Members of Bahama Islands Co-operative Credit Union Limited on its 33rd Annual General Meeting, she stated that the theme “Striving to Make a Difference, Because Members Matter” is timely and very fitting because members are also owners of this great institution and the only way to ensure that credit unions remains a viable entity is by the membership doing business with themselves. Ms. Deleveaux stated that banks are trying to copy the co-operative way, they are attempting to lure members with lower interest rates, but unlike with credit unions, members do not share in the profits; she encouraged members to obtain their loans from their credit union as this drives income and helps to generate profit.

Ms. Deleveaux informed the members that they are also part owners of the insurance brokerage company, she encouraged all to utilize the company to insure their cars, homes etc. as a part of the profit will be returned to BICCU.

Additionally, Ms. Deleveaux notified the membership that the credit union through the insurance company offers protection over savings and loans. Further she explained that when a member dies before the age of 60, any savings in

MINUTES OF THE 33rd ANNUAL GENERAL MEETING

BAHAMA ISLANDS CO-OPERATIVE CREDIT UNION LIMITED

THEME: “STRIVING TO MAKE A DIFFERENCE: BECAUSE MEMBERS MATTER”

BICCU ANNUAL GENERAL MEEING 2020

13

the credit union up to $20,000.00 is doubled. Funds saved between 60 and 65 is paid at 75% providing it does not exceed $20,000.00. Additionally, loans once issued before the age of 60, are paid off upon death.

Ms. Deleveaux also highlighted other products offered by the insurance company such as the Burial Program whereby members can purchase a $10,000.00 plan for $7.00 per month; additionally, a very affordable medical coverage is offered.

Ms. Deleveaux informed that The Bahamas Co-operative League Limited, in addition to providing advocacy also provides training for the various credit unions which helps credit unions meet requirements established by The Central Bank of The Bahamas.

Ms. Deleveaux stated The League applauds BICCU on its growth and success to date; further she stated that she is happy to have played a role in the launch and setup of BICCU.

Ms. Deleveaux thanked BICCU for its continued support of the Bahamas Co-operative League Limited and on behalf of The League and the Insurance Company, she extended best wishes for a productive Annual General Meeting.

8. MINUTES OF THE 32nd AGM

A motion to dispense with the reading of the 32nd AGM Minutes was moved by Ms. Rosemary Campbell, seconded by Ms. Tamara Bullard and was carried unanimously.

Corrections:

8.1. Page 25 Item 16.4: Mr. Calnan Weech stated that the Education Committee received a stipend of $1,200.00 per person, per year. Mr. Weech’s comment was noted.

9. MATTERS ARISING

9.1. Page 13 Item 6.7: Mr. Calnan Weech stated that last year Vice Chairman Bowleg indicated that he would forward the report from the Bahamas Co-operative League Limited to all interested parties, he inquired as to whether this was done as he had

not received the report.

9.1.1 The member was presented with a copy of The League’s AGM Book, he responded that it was not what he was expecting but he would accept it.

9.1.2 Vice Chairman Bowleg advised that the League’s office was open daily, members can visit the office at any time and retrieve any information on the movement once it is related to the credit union.

9.1.3 Page 23 Item 14.13 Mr. Calnan Weech stated that the word should be report, the correction was noted.

The motion to accept the minutes with corrections and the matters arising was moved by Ms. Barbara Williamson and seconded by Ms. Rosemary Campbell, the Motion carried.

10. REPORTS

10.1. ANNUAL GENERAL MEETING BOARD OF DIRECTORS’ REPORT

10.2. The motion to dispense with the reading of the Board of Directors’ Report was moved by Ms. Rosemary Campbell and seconded by Mr. Dave Beckford, Motion carried.

10.3. Chairman Rolle thanked the members for their support over the year, he stated that it is because of the membership that the credit union has succeeded to the level that it has. The Chairman also thanked the Board and Committees but most importantly he thanked the staff and management team led by Mr. Mark Bastian, CEO who has worked diligently to improve the credit union’s performance compared to the year 2017 which he stated was a dismal year.

10.4 The Chairman advised that the credit union made good strides and ended 2018 with a profit of $236,000.00 compared to 2017 when there was a loss of $318,000.00, this was a $600,000.00 turn around. Further he stated that loans grew by $1.7 million in 2018.

10.5 Additionally the Chairman stated that the credit union’s delinquency rate decreased from 11.3% to 5.9% by the end of 2018 which is the second

BICCU ANNUAL GENERAL MEEING 2020

14

lowest of the credit unions. Chairman Rolle stated that the delinquency balance decreased from $2.6 million to $1.5 million while the delinquent accounts decreased from 355 account at the end of 2018 to 237 at the end of 2018. The amount of write-off also decreased from $939,000.00 to $636,000.00. Provisioning decreased from $967,000.00 to $472,000.00.

10.6 Chairman Rolle stated that the Board is pleased by the efforts made in the area of delinquency, he said that there is still a hurdle to cross relating to Baha Mar whose employees are still on the delinquency list due to the fact that the company does not allow salary deductions at this time; however, the Chairman advised that discussions are being had with Baha Mar in an effort to remedy this issue.

10.7 Chairman Rolle advised that the credit union’s membership increased by 835 members in 2018. The Chairman further advised that for the member’s convenience, the credit union installed an ATM and now offers cash eliminating the need to go to another bank to cash your BICCU cheques.

10.8 The Chairman stated that BICCU has made many strides and will continue to grow with the support of the membership. He stated that BICCU should be the members primary provider for financial services because once BICCU grows the members benefit. Once the credit union succeed, the members succeed. Further he advised that the only way the credit union could offer the low rates on loans and high rates on savings is if the credit union has the members’ ultimate support.

10.9 Mr. Calnan Weech congratulated the Board and management for a wonderful year. The member then referred to page 30 and inquired as why the Board had taken steps to curtail the growth of member deposits. Chairman Rolle advised that persons are coming to the credit union chasing the deposit rates, further he advised that the credit union is getting in more money than it is lending; consequently, a temporary moratorium has been placed on new member fixed deposits until loans can be increased.

10.10 Mr. Weech stated that in other words, the credit union wants its members to borrow more. The Chairman stated that the credit union is in the

business of loans.

10.11 Mr. Weech also highlighted the fact that the credit union cannot get deductions from members employed at Baha Mar which makes it difficult to keep these members off the delinquent list. Mr. Weech enquired as to whether National Credit Union was having the same issue. Chairman Rolle responded that they were.

10.12 Mr. Weech advised that persons such as the Pension Board and the Bahamas Hotel Association may be able to assist the credit union with securing deductions from Baha Mar. Mr. Weech stated that the President of the Bahamas Hotel Board is in attendance at the AGM as well as persons on BICCU’s Board who are also on the Pension Board, it is his hope that they can use their influence and get the contacts with Baha Mar to make this happen.

10.13 Chairman Rolle advised that a member of BICCU’s Board has tried to assist; however, it requires a change of the system currently used by Baha Mar.

10.14 Director Albury advised that it is not that Baha Mar would not give BICCU a deduction, the system currently employed by Baha Mar only allows for one deduction. The Director stated that he personally spoke to the person in charge and he will go back again to try to have the matter remedied.

10.15 Mr. Weech recommended that the fact that the credit union now has an ATM and is on a cash basis, it should push not to be treated as a deduction but as another direct deposit into a bank. Further he stated that Atlantis should not be treating what is sent into the credit union as a deduction, it should be that the member is sending his/her money to different banks. Mr. Weech suggested that BICCU seek the backing of the Central Bank to get employers to treat credit unions the same way they treat the banks, deductions should simply be deposits into the credit union. Chairman Rolle stated that BICCU is working on this, working to be the primary financial institution for its members.

10.16 Mr. Weech enquired as to the ATM, he stated that there appears to be a link between BICCU and Fidelity. Chairman Rolle advised that the ATM is

BICCU ANNUAL GENERAL MEEING 2020

15

on Fidelity’s platform, they will be conducting the training and maintaining the system for BICCU. Mr. Weech further enquired as to whether withdrawals can be made from a Fidelity ATM, the Chairman answered in the affirmative.

10.17 Mr. Weech requested clarification on the treatment of qualifying shares. Chairman Rolle advised that the Credit Union attempted to split the shares into qualifying and equity shares. Further, he stated that in order to be a member of the Credit Union qualifying share must be purchased. He stated that in the past, upon leaving the Credit Union these funds were returned to the member; however, the Regulators advised that the qualifying share are nonrefundable. This he stated is with immediate effect.

10.18 Mr. Weech enquired as to whether dividends will still be paid on the shares. The Chairman answered in the affirmative.

10.19 Mr. Weech also enquired as to why the Credit Union does not take pattern after Teachers Credit Union and set up a company and go into the real estate business as the management of properties allows Teachers another revenue stream. Chairman Rolle responded that the Act prohibits the ownership of property unless it is utilized by the credit union. Further the Chairman advised that there are limitations on the type of investments.

10.20 Stephanie Miller enquired as to the ATM, is there a cost for Fidelity to run it? Chairman Rolle responded in the affirmative.

10.21 Barbara Williamson enquired as to whether the share price could be reduced since members shares are nonrefundable. Chairman Rolle stated that this is not permitted by the regulators.

10.22 A motion for the acceptance of the Annual General Meeting Board of Directors’ Report was moved by Mr. Calnan Weech, seconded by Ms. Ruth Neily and was carried unanimously.

11 TREASURER’S REPORT

11.1 The motion to dispense with the reading of the Treasurer’s Report was moved by Ms. Rosemary Campbell, seconded by Ms. Tamara Bullard and

was carried unanimously.

11.2 Mr. Calnan Weech enquired as to whether the auditor will be presenting his report. Assistant Treasurer Bullard answered in the affirmative.

11.3 Assistant Treasurer Bullard enquired as to whether there were any questions. There were none. The Assistant Treasurer stated that he wished to highlight three important points on the financial statement.

11.4 The Assistant Treasurer also stated that the success of 2018 should be celebrated. Last year, 2017, the credit union had a loss of $419,000.00, this year we had a profit of $236,000.00, a profit of 177%.

11.5 The Assistant Treasurer stated that it was important to highlight the number of deposits compared to the number of loans. Loans increased by 8.2% or $1,889,411. Deposits increased by 16.3% or $5,563,827.00. Further he stated that the two accounts are very related, the credit union had an increase of over $5 million in deposits but only $1.8 million in loans.

11.6 The Assistant Treasurer stated that deposits are growing more than loans, he added that the credit union grows via loans, so it is important to grow loans.

12 AUDITORS REPORT

12.1 Mr. James Gomez, Partner, Baker Tilly Gomez asked for permission to forgo the reading of the auditor’s report and to focus on the qualification in the financial statement and highlight the fact that it has been modified and to underscore to the membership why.

12.1.1 The motion to dispense with the reading of the Auditor’s Report was moved by Mr. Calnan Weech, seconded by Mr. Dave Beckford and was carried unanimously.

12.2 Mr. James Gomez advised that the audited report was dated May 6, 2019. Further, he advised that the report was modified for two reasons. The International Financial Reporting Standard 9 outlined on page 41 is the first base for the qualified opinion. It speaks to the accounting

BICCU ANNUAL GENERAL MEEING 2020

16

standards which require credit unions to reclassify its financial instruments into new categories and to provide for the impairment of certain financial instruments based upon expected losses instead of experienced losses.

12.3 Mr. Gomez stated that currently, and as it has been in the past, the credit union’s financial statements in terms of provisioning was based on what was experienced, the loss had already occurred and provisioning was based on the PEARLS standard and was on a percentage bases and what had already happened. The Auditor advised that the new standard, impairment on loan provisioning takes place on the date the loan is booked and is determined based on internal policies which must be consistent with standard to make provisioning on the loan at that time, this he stated should flow into the profit and loss.

12.4 Mr. Gomez stated that the fact that the credit union has been in existence for a long time means that once implemented, the credit union will take a significant hit to its bottom line. Further he stated that it will be necessary to assess each loan which will take some time; he advised that this is why the credit union got a qualified report.

12.5 The Auditor stated that the Central Bank has allowed for all credit unions to forgo the adoption of the standard; however, effective January 1, 2020 the credit union will have to be compliant.

12.6 Mr. Gomez advised that there would have to be an extensive exercise to assess every loan account to determine the likelihood of default.

12.7 The Auditor stated that there are other provisions in this standard, he advised that if the credit union held treasury bonds or government paper, every instrument must have an element of default as countries do default on their debt. Further, he stated that the Bahamas Institute of Chartered Accountants (BICA) has established a rate of default which will be used across the board for sovereign debt in respect of Government bonds. The Accountant further stated that provisioning will be straight across the board and will affect the bottom line.

12.8 Mr. Gomez stated that IFRS 9 is an aggressive policy, the benefit will not be seen until the policy

is fully implemented and the assessment is done as time passes.

12.9 Mr. Calnan Weech clarified that where the credit union has Bahamas Government registered Stock it will be necessary to implement an interest income loss provision. The Auditor answered in the affirmative. Further he stated that BICA firms got together and established a policy across the board for financial statements so that everyone who hold Government paper, credit unions, banks etc. will handle the provisioning the same.

12.10 Mr. Weech enquired as to whether this will be posted at some point because if a member pays his/her loan consistently for 5 to 10 years, the credit union will have to consider that the member may default on the loan so the credit union will have to put a percentage default on the loan that will have to be deducted from the net income. He asked if BICA will put a standard on this. Mr. Gomez answered in the negative stating that BICA only established the uniform policy for sovereign debt, Government paper. The Auditor explained that institutional paper varies from industry to industry so what is in a credit union may not be the same as what is in a bank. He stated that the individual will have to be examined on a person by person basis.

12.11 The Auditor advised that page 41 contains the statement referring to Central Bank’s deferment of the adoption of the standard until January 1, 2019, he stated that initially he said 2020; however, what he actually meant was that by January 1, 2020 IFRS9 must be in effect. Further Mr. Gomez clarified that the financial statements currently being reviewed is the 2018 statement, he stated that the financial statement for 2019 must show the full adoption of the standard.

12.12 Mr. Gomez stated that the full adoption of the standard will take a considerable amount of time, additionally, he stated that it is taxing, hence the credit unions were not ready. Further he stated that financial institutions have been working on the implementation of the standard for the last two years to be ready for full adoption in 2018.

12.13 The Auditor stated that the second reason for the qualification is that the credit union has classified members qualifying shares which are available for withdrawal, as equity and the statement of

BICCU ANNUAL GENERAL MEEING 2020

17

financial position and the dividends paid on these shares as an appropriation of retained earnings. This he said, should not happen as those shares are payable on demand as such they should be classified as liabilities and the dividends paid on these shares be classified as an expense. Further, he stated that if a member walks in the Credit Union and requests to close his/her account and withdraw his/her qualifying shares from the Credit Union there is nothing that prohibits the member from getting the funds.

12.14 Mr. Gomez stated that if member shares were classified in accordance with IFRS, liabilities will increase, and members equity will also increase by $1.4 million and profit would have decreased by $99,000.00 The Auditor stated that next year the numbers will be shown according to the standard in the first year and will have some impact on the Credit Union’s financial statement. He stated that members may be alarmed in the first year but in the subsequent years the impact will not be as significant as the Credit Union would be provisioning for the loan at the time the loan is booked.

12.15 The Auditor stated that the report on the Legal and Regulatory Requirements is found on page 43. Further, the Auditors confirmed that the Credit Union has kept its accounting and records in accordance with the Bahamas Co-operative Credit Union Act, 2015, its Regulations and Bye-Laws.

12.16 The auditor stated that too often the AGM forego the reading of the Treasurer’s Report, he stated that this is an important report as it is the lifeline of the organization so sometimes the AGM should take time to listen to the Treasurer’s Report.

12.17 Mr. Calnan Weech stated that it is accepted that if an audit is presented and there is an error, the entire audit should be dismissed. Mr. Weech advised that he found two errors, the first one was a small error on page 56, Cash in Hand which stated that the facility was secured by a hypothecation over $50,000.00 fixed asset in note 52 (b) (2), however, he stated that the reference should be 52 (b) (3), Scotia, Scotia, it should be consistent.

12.18 Additionally, Mr. Weech highlighted an error on page 57 Other Deposits, he stated that ordinarily the balance at the beginning of the year, deposits

and or withdrawals plus interest earned at the end of the year equals the balance at the end of the year. Mr. Weech stated that the balance at the end of 2017 was not carried over to the start of 2018, this he advised resulted in a difference of $1,300.00 and a balance of $976,363.00. Mr. Weech further stated that this number is also listed on the Balance Statement where the same number is brought across resulting in a total of $963.00 instead of $964.00.

12.19 Mr. James Gomez responded that in terms of financial statements the audit must be materially correct, he stated that Mr. Weech’s first point does not speak to materiality.

12.20 As for Mr. Weech’s second point the auditor stated that sometimes in printing, because the financial statement consists of a combination of excel and word documents, some things fall out of whack during the merge, so the number did not come over. Further Mr. Gomez confirmed that the number on the face of the financial statement, financial position #444 is correct.

12.21 Mr. Weech enquired as to whether the mistake will be corrected.

Motion to accept the Auditor’s Report with adjustments moved by Ms. Barbara Williamson; seconded by Mr. Ivan Miller and was passed unanimously.

13. 2020 Budget Report

Mr. Calnan Weech enquired as to the $2 million deposit with Fidelity. Chairman Rolle stated that Fidelity had the best rates.

A motion to accept the 2020 Budget was moved by Ms. Tamara Bullard seconded by Mr. Dave Beckford, and was unanimously carried.

14. SUPERVISORY, CREDIT & EDUCATION COMMITTEES REPORTS

14.1 SUPERVISORY COMMITTEE REPORT A motion to dispense with the reading of the

Supervisory Committee’s Report was moved by Ms. Rosemary Campbell, seconded by Ms. Tamara Bullard and was carried unanimously.

BICCU ANNUAL GENERAL MEEING 2020

18

14.1.1 Mr. Calnan Weech thanked the Supervisory Committee for a very good report. Mr. Weech referenced page 86, Bank Reconciliation, he enquired as to whether this is still a concern, he read the Committee’s comments, “The Committee continues to experience challenges with respect to the monthly reconciliation in a timely manner.”

14.1.2 Chairperson J. Almitra Jones stated that this was due to human resources challenges after the departure of the previously hired Accountant. In 2018 the Credit Union hired consultants who left early, two other persons who were hired left early. Ms. Jones stated that with the hire of an accountant and a junior accountant, they are still trying to come up to speed with the reconciliations.

14.1.3 Mr. Weech queried the Member Suspense Accounts Receivable Policy; he asked the Chairperson to highlight why was it is important for bank reconciliations to be done in a timely manner as it is the place where nefarious things could happen. Mr. Weech enquired as to the Suspense Accounts Receivable Policy, what is it and why is it an issue.

14.1.4 Chairperson J. Almitra Jones responded that the Suspense Accounts Receivable is an account that is used temporarily or permanently to carry a doubtful or if there is a discrepancy, the funds go into this account until the transaction has been identified. The Chairperson explained that the account should have a zero balance, at the very least it should be reconciled on a regular basis to ensure that nothing unethical or nefarious happens in the account. Ms. Jones further explained that the Board is equally as concerned as the Committee regarding this account and efforts are being made to reconcile this account. Additionally, the Chairman stated that an audit is scheduled for July when transactions will be reviewed, this she said will provide an independent assurance of the validity of the transactions in the Suspense Account.

14.1.5 Mr. Calnan Weech stated that the Board, Treasurer’s and Audit Report outlined the amount of work that has to be done. Further, he stated that the members should understand that this will result in higher regulatory cost for the credit unions, he suggested that credit unions should work together. Mr. Weech stated that World Council

of Credit Unions will be coming to The Bahamas, he stated that this is a wonderful opportunity to lobby government about how credit unions are treated. Further Mr. Weech suggested that the World Council President should meet with the Prime Minister or Deputy Prime Minister along with the League in an effort to bring down costs and to get a fair hearing with the Central Bank of The Bahamas.

14.1.6 Mr. Calnan Weech urged credit unions to do more things together so that expenses and prices are not so high otherwise with what the credit union is facing next year will be a huge loss for 2019, Chairperson Jones, agreed stating that there is strength in numbers.

Motion for the acceptance of the Supervisory Committee’s Report moved by Ms. Barbara Williamson, seconded by Ms. Ruth Neily, unanimously carried.

14.2 CREDIT COMMITTEE REPORT A motion to dispense with the reading of the Credit

Committee Report was moved by Ms. Barbara Williamson, seconded by Ms. Tamara Bullard and was carried unanimously.

14.2.1 As Mrs. Maxine Pratt Chairperson was not present in the room, the presentation of the report was delayed.

14.3 EDUCATION COMMITTEE REPORT A motion to dispense with the reading of the

Education Committee Report was moved by Ms. Barbara Williamson, second by Mr. Ivan Miller and was carried unanimously.

14.3.1 There were no questions or comments. Motion for the acceptance of the Education

Committee’s Report, moved by Mr. Rudy Dean, seconded by Mr. Ivan Miller, carried unanimously.

15. NEW BUSINESS

15.1 There was no New Business.

16. RESOLUTIONS

Secretary Walkes-Pratt presented the resolutions as follows:

BICCU ANNUAL GENERAL MEEING 2020

19

16.1 RESOLUTION #1

RESOLUTION FOR THE PAYMENT OF DIVIDENDS

WHEREAS the audited financial statements of the Bahama Islands Co-operative Credit Union Limited (BICCU) for the year ending December 31, 2018 were presented and accepted by this Annual General Meeting;

BE IT RESOLVED that this Annual General Meeting approved the payment of a Four percent (4 %) dividend to shareholders on their Qualifying Shares held for the year 2018;

BE IT FURTHER RESOLVED that calculation and

distribution of these dividends be credited to the individual member accounts not later than July 31, 2019

16.1.1 The Secretary invited all in favour of the Resolutions to sit, and all against the resolutions to stand. Resolution carried, unanimously.

16.2 RESOLUTION #2 RESOLUTION FOR THE APPOINTMENT OF

AUDITORS

WHEREAS The Bahamas Co-operative Union Act, 2015 requires that the Directors cause the accounts of the Credit Union to be audited at the end of each financial year by an auditor appointed by the Board.

BE IT RESOLVED that the Board of Directors of

the Bahama Islands Co-operative Credit Union Limited (BICCU) be allowed to choose an auditing firm to conduct the audit for the fiscal year 2019.

16.2.1 The Secretary invited all in favour of the Resolutions to sit, and all against the resolutions to stand. Resolution carried, unanimously.

16.3 RESOLUTION #3

RESOLUTION FOR REMUNERATION TO MEMBERS OF THE BOARD OF DIRECTORS

WHEREAS The Bahamas Co-operative Union Act of 2015 requires formal approval of all remuneration paid to Directors of the Bahama Islands Co-operative Credit Union Limited in accordance with –

Section 58 (1)

No director and or no member of a committee is entitled to be paid any remuneration in connection with his duties as a director or a committee member of a co-operative credit union or for his attendance at meetings unless the remuneration –

a) Is fixed in the bye-laws; and

b) Is ratified annually by the members, by resolution at the annual general meeting.

BE IT RESOLVED THAT Directors of the Bahama Islands Co-operative Credit Union Limited shall receive a stipend of Five Hundred Bahamian Dollars (B$500.00) per month.

16.3.1 The Secretary invited all in favour of the Resolutions to sit, and all against the resolutions to stand. Resolution carried, unanimously.

16.4 RESOLUTION #4 REMUNERATION TO SUPERVISORY

COMMITTEE MEMBERS OF THE BAHAMA ISLANDS CO-OPERATIVE CREDIT UNION LIMITED

WHEREAS The Bahamas Co-operative Union Act of 2015 requires formal approval of all remuneration paid to Members of the Supervisory Committee of the Bahama Islands Co-operative Credit Union Limited in accordance with –

Section 58 (1)

No director and or no member of a committee is entitled to be paid any remuneration in connection with his duties as a director or a committee member of a co-operative credit union or for his attendance at meetings unless the remuneration –

a) Is fixed in the bye-laws; and

BICCU ANNUAL GENERAL MEEING 2020

20

b) Is ratified annually by the members, by resolution at the annual general meeting.

BE IT RESOLVED THAT the members of the Supervisory Committee of the Bahama Islands Co-operative Credit Union Limited shall be paid a stipend of Two Hundred Bahamian Dollars (B$200.00) per month.

16.4.1 The Secretary invited all in favour of the Resolutions to sit, and all against the resolutions to stand. Resolution carried, unanimously.

16.5 RESOLUTION #5 REMUNERATION TO CREDIT COMMITTEE

MEMBERS OF THE BAHAMA ISLANDS CO-OPERATIVE CREDIT UNION LIMITED

WHEREAS The Bahamas Co-operative Union Act of 2015 requires formal approval of all remuneration paid to Members of the Credit Committee of the Bahama Islands Co-operative Credit Union Limited in accordance with –

Section 58 (1)

No director and or no member of a committee is entitled to be paid any remuneration in connection with his duties as a director or a committee member of a co-operative credit union or for his attendance at meetings unless the remuneration –

a) Is fixed in the bye-laws; and

b) Is ratified annually by the members, by resolution at the annual general meeting.

BE IT RESOLVED THAT the members of the Credit Committee of the Bahama Islands Co-operative Credit Union Limited shall be paid a stipend of Two Hundred Bahamian Dollars (B$150.00) per month.

16.5.1 Mr. Calnan Weech highlighted the fact that the words in the resolution stated a stipend of Two Hundred Dollars, however the dollar amount stated B$150.00 per month.

16.5.2 Secretary Walkes-Pratt thanked the member and advised that the amount should be One Hundred

Fifty Dollars.

16.5.3 The Secretary invited all in favour of the Resolutions with corrections to sit, and all against the resolutions to stand. Resolution carried, unanimously.

16.6 RESOLUTION #6

REMUNERATION TO EDUCATION COMMITTEE MEMBERS OF THE BAHAMA ISLANDS CO-OPERATIVE CREDIT UNION LIMITED

WHEREAS The Bahamas Co-operative Union Act of 2015 requires formal approval of all remuneration paid to Members of the Education Committee of the Bahama Islands Co-operative Credit Union Limited in accordance with –

Section 58 (1)

No director and or no member of a committee is entitled to be paid any remuneration in connection with his duties as a director or a committee member of a co-operative credit union or for his attendance at meetings unless the remuneration –

a) Is fixed in the bye-laws; and

b) Is ratified annually by the members, by resolution at the annual general meeting.

BE IT RESOLVED THAT the members of the Education Committee of the Bahama Islands Co-operative Credit Union Limited shall be paid a stipend of One Hundred Bahamian Dollars (B$100.00) per month.

16.6.1 The Secretary invited all in favour of the Resolutions to sit, and all against the resolutions to stand. Resolution carried, unanimously.

16.7 RESOLUTION #7

QUALIFYING SHARES WHEREAS the Bahamas Co-operative Credit

Union Act, 2015 defines qualifying shares as non-withdrawable

BICCU ANNUAL GENERAL MEEING 2020

21

BE IT RESOLVED that per the directive from the Central Bank of The Bahamas, BICCU wishes to reverse the share split (Qualifying shares $50.00 and Equity Shares $150.00) approved by the Membership at the 32nd Annual General Meeting held June 29, 2018, and with immediate effect cease the practice of allowing the withdrawal of Qualifying Shares.

16.7.1 The Secretary invited all in favour of the Resolutions to sit, and all against the resolutions to stand. Resolution carried, unanimously.

16.8 RESOLUTION #8

CONSTITUTION OF ELECTED COMMITTEES

BE IT RESOLVED that the Elected Committees cannot have more than one serving Committee Member employed in the same department at the same employer.

16.8.1 The Secretary invited all in favour of the Resolutions to sit, and all against the resolutions to stand. Resolution carried, unanimously.

16.9 RESOLUTION #9

NOMINATIONS FROM THE FLOOR

WHEREAS the Draft Uniform Bye-Laws for Co-operative Credit Unions operating in The Bahamas under The Bahamas Co-operative Credit Unions Act, 2015 states that no member may be elected to the Board, the Credit committee and the Supervisory committee unless he or she has satisfied the fit and proper requirements.

BE IT RESOLVED that for the effective management and proper administration of the Credit Union, effective immediately, no member will be nominated to hold an elected office unless an application was duly submitted and approved by the Nomination Committee.

16.9.1 The Secretary invited all in favour of the Resolutions to sit, and all against the resolutions to stand. Resolution carried, unanimously.

16.10 RESOLUTION #10

MAXIMUM LIABILITY

WHEREAS the Bahamas Co-operative Credit Union Act, 2015 states that a co-operative credit union shall not borrow funds in excess of ten percent of its total assets.

BE IT RESOLVED that the Maximum Liability that

the Directors can bind the Credit Union for is ten percent of the Credit Union’s total assets.

16.10.1 The Secretary invited all in favour of the Resolutions to sit, and all against the resolutions to stand. Resolution carried, unanimously.

16.11 RESOLUTION #11

TRAINING BUDGET

WHEREAS the Draft Uniform Bye-Laws for Co-operative Credit Unions operating in The Bahamas under The Bahamas Co-operative Credit Unions Act, 2015 states that the Annual training and conference budget of board members shall not exceed one third (1/3) of the credit union’s total staff training budget.

BE IT RESOLVED that the Annual training and conference budget of BICCU’s Board of Directors shall not exceed one third (1/3) of the credit union’s total staff training budget

16.11.1 The Secretary invited all in favour of the Resolutions to sit, and all against the resolutions to stand. Resolution carried, unanimously.

RESOLUTIONS SUBMITTED BY THE NOMINATION COMMITTEE

16.12 RESOLUTION #12

BOARD TERM LIMITS

WHEREAS societal and economic changes require Boards to continually assess their skill sets to ensure the Board remains competent.

AND WHEREAS the Bahama Islands Co-operative Credit Union wishes to encourage fresh viewpoints in the boardroom and the broadest

BICCU ANNUAL GENERAL MEEING 2020

22

with responsibility for the prudent management of millions of dollars in assets;

AND WHEREAS this responsibility requires that

Board members have a minimum level of financial literacy;

BE IT RESOLVED that new Board members be required to attend and complete an approved assigned course in financial management;

BE IT FURTHER RESOLVED that a copy of the

certificate of completion be placed on the board member’s files.

16.14.1 The Motion to accept the Resolution was moved by Ms. Rose Campbell, seconded by Ms. Barbara Williamson. Resolution carried, unanimously.

17. ELECTIONS

Chairman Rolle invited Mr. Carlton Russell, Chairman of the Nomination Committee to the podium. Mr. Russell congratulated the Board, led by Chairman Rolle and the CEO, Mark Bastian for a fine job, year over year, 2017 over 2018, a 177% turnaround which equates to over $600,000.00.

Nomination Committee Chairman Carlton Russell invited Directors Barry Rolle and Janet Guerriea to demit their seats. Further he explained that the election process will require that the room be counted three (3) times, once before each vote. There will be one line to place the ballot in the box and members are asked to place the ballot in the box with the hand that has the wrist band. Additionally, he advised that members were only allowed to place one (1) ballot in the ballot box, no member would be allowed to place another member’s ballot in the box.

17.1 BOARD OF DIRECTORS: Mr. Russell advised that there were two vacancies

introduced the nominees for the Board of Directors as follows:

1. Janet Guerriea 2. Barry Rolle 3. Rosemary Campbell

17.1.1 There were no nominations from the floor. The nominees were given two minutes to address the members.

possible participation of members.

BE IT RESOLVED that directors be limited to three consecutive terms in office, and eligible for re-election to the Board after a minimum one-year absence from the board of directors.

16.12.1 The Motion to accept the Resolution was moved by Ms. Hope Curry, seconded by Ms. Claudette Farrington. Resolution carried unanimously.

16.13 RESOLUTION #13

AMENDMENT TO THE NOMINATION REQUIREMENTS

WHEREAS the Bahama Islands Co-operative Credit Union wishes to ensure that candidates for elected offices have demonstrated an interest in the credit union’s governance practices.

AND WHEREAS the current requirement of attendance at a minimum of two consecutive Annual General Meetings to qualify for nomination may be too restrictive.

BE IT RESOLVED that Bye-Law section 45, sub-

section (1) be amended as follows: Any member seeking a nomination to any elected

Committee must attend no less than two of the past three Annual General Meetings to qualify for nomination.

16.13.1 Member Rose Campbell requested

clarification of the resolution. Secretary Walkes-Pratt explained that the member was required to attend at least two of the last three AGM meetings.

16.13.2 The Motion to accept the Resolution was moved by Ms. Barbara Williamson, seconded by Ms. Rose Campbell. Resolution carried, unanimously.

16.14 RESOLUTION #14

FINANCIAL LITERACY

WHEREAS the Bahama Islands Co-operative Credit Union is a financial services organization

BICCU ANNUAL GENERAL MEEING 2020

23

Votes:

Nominees Votes Received Elected

Janet Guerriea 80 √

Barry Rolle 133 √

Rosemary Campbell 60

Congratulations were extended to Ms. Janet Guerriea and Mr. Barry Rolle.

17.2 SUPERVISORY COMMITTEE Members were advised there were (2) vacancies

for the Supervisory Committee, nominees are as follows:

1. Elston Bain 2. Marlon Bethel 3. Astranique Bowe 4. Rosemary Campbell 5. Fidentia Dorsett 6. Kenneth Lightbourne

17.2.1 There were no nominations from the floor. The nominees were given two minutes to address the members.

Votes:

Nominees Votes Received Elected

Elston Bain 49

Marlon Bethel 51 √

Astranique Bowe 3

Rosemary Campbell 45

Fidentia Dorsett 46

Kenneth Lightbourne 85 √

17.2.2 Congratulations were extended to Marlon Bethel and Kenneth Lightbourne on their election to the Supervisory Committee.

17.3 CREDIT COMMITTEE Members were advised that there were three (3)

vacancies on the Credit Committee. The Chairman explained that the two individuals with the highest number of votes will serve for the three (3) year rotation and the individual with the lowest number of votes will serve for one (1) year to complete the

vacancy left by the resignation of Omar Rolle. The nominees were as follows:

1. Elston Bain 2. A. Mary Davis 3. Rudolph Dean 4. Charles Lightbourne 5. Edison Morley

17.3.1 Nominations from the floor:

1. Archelaus Culmer

Nominated by Ms. Shantell Morris-Lockhart, 2nd Kenneth Lightbourne

17.3.2 The nominees were given two minutes to address the members.

Votes:

Nominees Votes Received Elected

Elston Bain 77 √

A. Mary Davis 82 √

Rudolph Dean 24

Charles Lightbourne 12

Edwin Morley 46

Archealus Culmer 74 √

17.4 Congratulations were extended to Elston Bain, Archealus Culmer and A. Mary Davis on their election to the Supervisory Committee.

17.4.1 Motion for the ballots to be destroyed was moved by Mr. Nashon Rolle and second by Mr. Dave Beckford. Motion carried unanimously.

18. NOMINATION COMMITTEE

Chairman Rolle stated that in accordance with Section 13 45 (1) (A) of BICCU’s Bye-Laws, at each annual general meeting the membership shall appoint a nomination committee for the following year.

The motion that the Nomination Committee remain the same was moved by Mr. Nashon Rolle, seconded by Mr. Dave Beckford. The AGM unanimously accepted the Nominees.

BICCU ANNUAL GENERAL MEEING 2020

24

19. MOTION FOR ADJOURNMENT

The Motion for the adjournment of the 33rd Annual General Meeting of BICCU was moved by Mr. Nashon Rolle, second by Mr. Dave Beckford

The meeting ended at 9:30 pm.

We hereby certify that the foregoing is a true copy of the minutes and deliberations of the Board of Directors of the Bahama Islands Co-operative Credit Union Limited, held Friday June 28th, 2019.

______________________ _________________________Barry Rolle Estella Walkes-PrattChairman Secretary

BICCU ANNUAL GENERAL MEEING 2020

25

BOARD OF DIRECTORS REPORTTHE BAHAMIAN ECONOMY

In 2019 the Bahamas expected a strengthening of its economy as growth in real gross domestic product (GDP) was projected at 2.1 percent. The growth rate decelerated to .9 percent when compared to the 1.6 percent GDP growth of 2018. The modest growth rate was due to the increased activity in the tourism industry but adversely affected by the passage of Hurricane Dorian in September 2019. The Bahamas recorded 7.2 million visitors to the country during 2019, which was the highest ever recorded visitor arrivals for a year. The destruction caused by Hurricane Dorian slowed the country’s economic growth, especially in Grand Bahama and Abaco, the nation’s second and third largest island economies.

At the beginning of 2020, the country saw a gradual recovery as tourism to the other islands not affected by Hurricane Dorian saw an uptick relative to the fourth quarter 2019. For the most part, a mild economic contraction was still being projected for 2020, but some growth was expected once the infrastructure and tourism capacity was rebuilt. This gradual recovery from the severe damage caused by Hurricane Dorian was being felt when the global outbreak of COVID-19 happened. The outbreak has devastated our tourism-dependent economy.

It is always important to present the status of the Bahamian economy, as it is heavily influenced by the performance of the tourism sector. BICCU’s membership is still mostly hospitality industry centric and its success is also heavily influenced by that sector. As we deliver our report to you, we will try to let you know what we have done in 2019 and 2020 as it relates to our operation and the services provided as well as the impact of the pandemic on the credit union. We continue to work with management to ensure that BICCU delivers quality products and services and remain viable during these tough times.

OPERATIONS

OverviewBICCU continues experiencing a challenge with increasing its loan portfolio and with eliminating non-performing loans from its operation. Competition in the lending business is fierce, with the continued growth in different types of lending agencies. The pandemic has now brought on a different challenge in that many of our members are either furloughed or have become unemployed because of the COVID-19 outbreak. We the members of the Board, along with the management of BICCU have reviewed and taken steps to address all the concerns relating to our operation.

The Board recognizes that our operation has come under increased scrutiny due to the fact that our membership is heavily concentrated in the hospitality sector, which has been hit hard due to pandemic. We received guidance from the Central Bank of the Bahamas as our Regulator, and we have accepted those guidance points to ensure that we are protecting the assets of the credit union.

We have also made decisions that are in line with the worldwide credit union motto of “people helping people”. Accordingly, we have initiated ways to help people during difficult situations.

LoansFor the year ended December 31st, 2019, the Credit Union granted two thousand two hundred and ninety-nine (2,299) loans totaling twelve million four hundred and sixty-nine thousand nine hundred dollars ($12,469,900). The loans payoff/payments for the year totaled ten million seven hundred and twenty-one thousand seven hundred and eighty-five dollars ($10,721,785). For the year ending December 31st, 2019, the loan portfolio had a net increase of

BICCU ANNUAL GENERAL MEEING 2020

26

one million seven hundred and forty-eight thousand one hundred and fifteen dollars ($1,748,115). Our total loans portfolio as of December 31st, 2018, totaled $24,802,381 compared to December 31st, 2019 total of $26,550,496 which is an increase of 7.05 percent. The 7.05 percent growth in the loan portfolio in 2019 was excellent and it meant that gross loans kept pace with the growth in member deposits of 6 percent over the same period.

The Board took several steps to aid members who needed loans. After the passing of Hurricane Dorian, the Board allowed lower rates on loans for members who wanted to assist their families in Grand Bahama and or Abaco. The same privilege was also extended to members in Nassau that experienced flooding damage. As it was done in the latter part of 2018, the Board also reduced the interest rate on several consumer related loans by one (1) percent and by two (2) percent for new mortgage and car loans at the end of 2019. Although the original loan rates were reinstated in 2020, we continued monitoring to aid in the strengthening of the portfolio. During the 2019 Christmas season, the Board and management created a $1,000 loan promotion. This $1,000 loan was available to all members with current loans that were in good standing and there was a relaxation of terms such as exposure and debt service ratio for all members participating. Additionally, at the beginning of the COVID-19 pandemic, BICCU made available to all loan members that were in good standing with the credit union prior to being furloughed from work, a cash give- away equivalent to one month’s loan payment. With the approval of the Central Bank, loan payments have also been deferred through the end of year for furloughed workers. Non-Performing LoansThe Board continues to ensure that management gives special attention to the reduction of delinquent or non-performing loan accounts. We have also placed an emphasis on the recovery of charged off loans. We did not see the results that we would have liked to see regarding a reduction in provisioning and in accounts written off but there was a slight increase in recoveries. Provisioning for loan impairment increase from $471,657 at December 2018 to $1,057,625 at the end of December 2019. Delinquent accounts written off also increased from $635,653 at December 2018 to $882,680 at the end of December 2019, while recoveries of written off accounts increased to $200,427 for 2019 compared to $138,674 during 2018.

BICCU ANNUAL GENERAL MEEING 2020

27

As mentioned last AGM, the credit union needed to adapt to IFRS 9, which we said, would increase the level of loan impairment provisioning. An additional $557,290 was the effect of applying IFRS 9 to our allowance for doubtful loans. The impact for 2020 is expected to be even more significant, as we have crossed into uncharted territory with the deferrals of loan payments for furloughed workers. The Central Bank has provided some guidance on how to treat these loans at the end of the year.

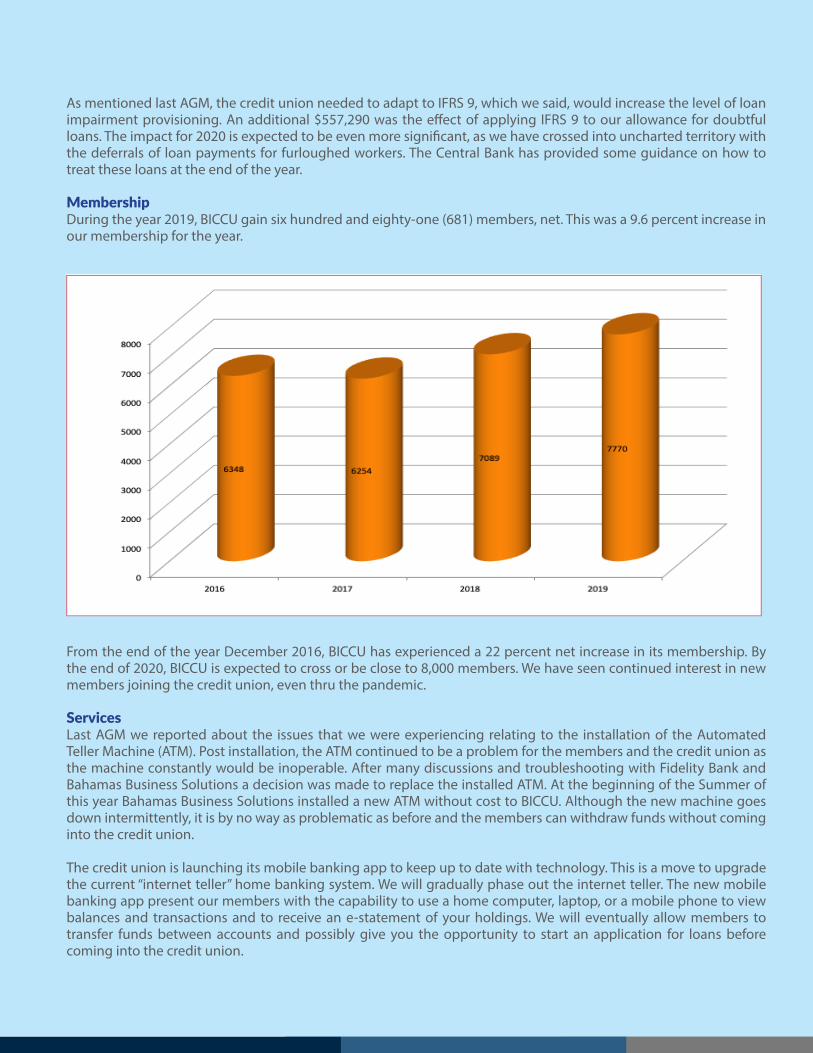

Membership During the year 2019, BICCU gain six hundred and eighty-one (681) members, net. This was a 9.6 percent increase in our membership for the year.

From the end of the year December 2016, BICCU has experienced a 22 percent net increase in its membership. By the end of 2020, BICCU is expected to cross or be close to 8,000 members. We have seen continued interest in new members joining the credit union, even thru the pandemic.

ServicesLast AGM we reported about the issues that we were experiencing relating to the installation of the Automated Teller Machine (ATM). Post installation, the ATM continued to be a problem for the members and the credit union as the machine constantly would be inoperable. After many discussions and troubleshooting with Fidelity Bank and Bahamas Business Solutions a decision was made to replace the installed ATM. At the beginning of the Summer of this year Bahamas Business Solutions installed a new ATM without cost to BICCU. Although the new machine goes down intermittently, it is by no way as problematic as before and the members can withdraw funds without coming into the credit union.

The credit union is launching its mobile banking app to keep up to date with technology. This is a move to upgrade the current “internet teller” home banking system. We will gradually phase out the internet teller. The new mobile banking app present our members with the capability to use a home computer, laptop, or a mobile phone to view balances and transactions and to receive an e-statement of your holdings. We will eventually allow members to transfer funds between accounts and possibly give you the opportunity to start an application for loans before coming into the credit union.

BICCU ANNUAL GENERAL MEEING 2020

28

The credit union is actively intent on upgrading the way we process loans and has partnered with an entity to bring on stream a new loan origination system. The introduction of this system should allow for faster approval of loans. The system will consider a person’s credit score, which is made up of many different factors to determine whether a person qualifies for a loan. Once the application is entered in the system, the individual with approval rights will be to determine that the applicant has met the requirements and an approval decision can be rendered. This system will work hand in hand with the core system as approved loans will also automatically be updated to the members’ account. This system will also be able to give updated information to the newly formed Bahamas Credit Bureau. StaffFor the most part, BICCU staff remained stable during 2019 through 2020. The senior leadership in the credit union remained unchanged. There were some changes that took place at a few junior positions, but nothing that interrupted the flow of work.

The credit union hired a contractual worker to assist with recovery of written off delinquent accounts. That individual was successful in bringing in more than twenty-five (25) thousand dollars a month during his tenure with the credit union. Unfortunately, the COVID-19 pandemic resulted in BICCU having to let that individual go, as not many persons were unable to pay on their delinquent accounts. Additionally, the credit union hired a contractual person to render assistance on the outstanding reconciling items on the bank account. The reconciliation of the main bank account has been problematic since the 2017 and 2018 upheaval of Accounts Department staff. We are of the opinion that the contractual individual has aided in bringing some resolution to this issue.

CENTRAL BANK SUPERVISION & REGULATORY MATTERS

The Central Bank of The Bahamas in their role as Regulator has maintained an active oversight of the credit union’s activities. At the end of June 2020, they commenced an On-site examination of BICCU. The Examination’s objectives were to review and assess the credit union’s: 1) Board structure and its oversight of the diversified functions reporting to them, 2) oversight and internal control processes, 3) money laundering, terrorist, and proliferation financing risk management program and 4) credit risk program. The examination was later extended to include COVID-19 contingency planning and the 2020 Auditor’s report. The examination pointed out that there is a need to have a comprehensive review of BICCU’s policies and procedures in order to approach things from a risk-based perspective and to align the operations with the bye-laws and credit union 2015 Regulations. The Board fully understands this approach, as several senior managers embarked on risk-based training earlier in the year. We expect to see some implementation of the risk-based approach and an alignment of our policies and procedures with the bye-laws and Regulations in 2021.

The credit union has been placed in a vulnerable position because of COVID-19. The fact that our membership base is highly concentrated on the hospitality sector and the majority of hotels and related business have been closed during the pandemic means that BICCU’s operation has been affected negatively. The Central Bank is aware of our situation and have expressed concern about the long-term impact should hotels not re-open. As a result, BICCU has reported monthly to them on the status of the deferred loans. As it stands, more than sixty percent of the loan portfolio has been allowed to defer monthly loan payments through the end of year. The deferred payments only relate to furloughed employees. If it is known that an individual member has been terminated their loan reverts to the active delinquent status if no payments are being received.

The Central Bank also paid attention to the 2019 Audit where BICCU received a Qualified Opinion based on unidentified items on the main bank account reconciliation. The Board has placed an emphasis on rectifying this issue that dates to 2017 and 2018 when there were staffing issues in the Accounts department. The Central Bank has mandated that the matter be resolved before December 2020. As noted earlier, a contractual consultant with familiarity of the system has assisted in trying to resolve this issue. We are confident that management will satisfactorily address this situation so that it will not be a recurring issue on the 2020 Audit of BICCU’s records.

BICCU ANNUAL GENERAL MEEING 2020

29

The Central Bank of the Bahamas has sanctioned CRIF Information Services Bahamas Limited to operate the credit bureau. The process of getting ready for them has already began. We are working with a service provider to automatically make the data available for transfer as required. It is believed that this system will become operational in 2021.

The credit union as with all Supervised Financial Institutions (SFIs) are constantly providing information on its operation to the Central Bank of the Bahamas. The Annual Risk Assessment and Hurricane Preparedness documents are time consuming to prepare, but aid in helping management address weaknesses in the operation.

BICCU’s PROPERTIES

The Saunders Beach property continues to receive many enquiries and several offers, but no offers have been received that has met the satisfaction of the Board. The Village Road property is still being leased to a government agency and remains available for sale should a legitimate offer be made.

BICCU is not in the real estate business, but the Board will make decisions for the betterment of the credit union and our members.

TRAINING

Board of DirectorsJuly 2019 World Credit Union Conference (Nassau)February 2020 Anti-Money Laundering & Counter Financing Terrorism (Nassau)July 2020 Virtual Credit Union Leadership Convention

Supervisory, Education & Credit CommitteesFebruary 2020 Anti-Money Laundering & Counter Financing Terrorism (Nassau) StaffJune 2019 C.U. Jamboree & Staff Empowerment (Nassau) July 2019 World Credit Union Conference (Nassau)November 2019 Enterprise Risk & Information Security Workshop (Nassau)January 2020 Enterprise Risk Management Strategy & Certification (Nassau)February 2020 Anti-Money Laundering & Counter Financing Terrorism (Nassau)March 2020 Police Safety Training (Nassau) June 2020 Payment Card Industry Training (Nassau)July 2020 Credit & Collections Course (Nassau)September 2020 HomeCU Mobile App Virtual TrainingNovember 2020 BICA Accountants Week (Nassau)

Thank You

The Board takes this opportunity to thank the membership for the opportunity to serve and for their continued confidence and support.

__________________________ ______________________________Barry Rolle Estella Walkes-PrattChairman Secretary

BICCU ANNUAL GENERAL MEEING 2020

30

Bahama Islands Co-operative Credit Union Limited

TREASURER’S REPORT2019

BALANCE SHEET

The Treasurer of the Bahama Islands Co-operative Credit Union (BICCU) reports that 2019 has been another year where our credit union has experienced a growth in assets. Our total assets have passed the $50 million milestone and stood at $50,299,708 at the end of December 2019. That represented a 4% growth over December 2018 total assets figure of $48,183,826. From December 2015 to the end of December 2019, BICCU has seen a growth of 56% in its total assets.

There was marginal growth in both the member deposits and the loan portfolio over the year. The Board recognized that member loans were not growing as fast as member deposits were growing and therefore reduced rates on member deposits and placed a moratorium on deposits from new members.

At the end of December 2019, the total member deposits in the Credit Union were $42,081,204. When compared to the balance as of December 2018 of $39,690,731, it represented a growth of 6%.

2019

BICCU ANNUAL GENERAL MEEING 2020

31

Our net loans portfolio grew at a rate of 4% when comparing December 2019 to December 2018. The Board and management continued with the efforts to increase the loan portfolio, through loan & mortgage promotions where rates were lowered with the intent of writing more loans. Although there were some positive results, the loan growth rate is still being outpaced by the member deposit growth rate.

BICCU ANNUAL GENERAL MEEING 2020

32

INCOME STATEMENT

BICCU recorded a profit of $418,197 for the year ending December 31st, 2019. This was an increase of $181,461 or approximately 77% when comparing it to the previous year. The Board and management continue placing an emphasis on profitability to ensure sustainability.

The increased profit was recorded even though the credit union had net loan losses reported in the profit and loss of $857,198 in 2019 as compared to $332,983 in 2018. The 2019 loan impairment provisioning expense of $1,057,625 which included the effect of the application of IFRS 9 amount of $557,290 was more than the 2018 figure of $471,657. On the other hand, recoveries on written off loans increased by $61,753 when comparing the $200,427 recorded in 2019 against $136,674 recorded in 2018.

Interest Income increased over the prior year by $256,171 partly because of placing the emphasis on adding more loans on the books. Interest Expense decreased by an amount of $106,573. This is mostly attributable to placing the moratorium on new member fixed deposits and reducing the interest rates on member deposits.

We will continue to monitor our non-interest income and operating expense lines to ensure that they are kept in line with our expectations.

The way forward….

The Board understands the need for BICCU to remain a viable entity, so we will continue to push for adding quality loans to the books, making sound investment decisions, controlling delinquencies and maintaining control of our operating expenses.

We continue “striving to make a difference because members matter”.

__________________________ ______________________Angela Culmer-Hinsey Mark BullardTreasurer Assistant Treasurer

BICCU ANNUAL GENERAL MEEING 2020

33

BICCU ANNUAL GENERAL MEEING2020

33

BAHAMA ISLANDS CO-OPERATIVE CREDIT UNION LIMITED

FINANCIAL STATEMENTS

31 DECEMBER 2019

BICCU ANNUAL GENERAL MEEING 2020

34

BAHAMA ISLANDS CO-OPERATIVE CREDIT UNION LIMITED

Contents Page

Report of the Auditors 1-3

Appendix to the Auditors’ Report 4

Statement of Financial Position 5

Statement of Profit or Loss and Other Comprehensive Income 6

Statement of Changes in Equity 7

Statement of Cash Flows 8

Notes to the Financial Statements 9 – 53

35

38

39

40

41

42

43

BICCU ANNUAL GENERAL MEEING 2020

35

BICCU ANNUAL GENERAL MEEING 2020

36

BICCU ANNUAL GENERAL MEEING 2020

37

BICCU ANNUAL GENERAL MEEING 2020

38

4

APPENDIX TO THE AUDITORS’ REPORT

Detailed Description of Our ResponsibilitiesAs part of an audit in accordance with ISAs, we exercise professional judgment andmaintain professional skepticism throughout the audit. We also:

· Identify and assess the risk of material misstatement of the financial statements,whether due to fraud or error, design and perform audit procedures responsiveto those risks, and obtain audit evidence that is sufficient and appropriate toprovide a basis for our opinion. The risk of not detecting a material misstatementresulting from fraud is higher than for one resulting from error, as fraud mayinvolve collusion, forgery, intentional omissions, misrepresentations, or theoverride of internal control.

· Obtain an understanding of internal control relevant to the audit in order todesign audit procedures that are appropriate in the circumstances, but not forthe purpose of expressing an opinion on the effectiveness of the Credit Union’sinternal control.

· Evaluate the appropriateness of accounting policies used and the reasonablenessof accounting estimates and related disclosures made by management.

· Conclude on the appropriateness of management’s use of the going concern basisof accounting and, based on the audit evidence obtained, whether a materialuncertainty exists related to events or conditions that may cast significant doubton the Credit Union’s ability to continue as a going concern. If we conclude thata material uncertainty exists, we are required to draw attention in our auditor’sreport to the related disclosures in the financial statements or, if suchdisclosures are inadequate, to modify our opinion. Our conclusions are based onthe audit evidence obtained up to the date of our auditor’s report. However,future events or conditions may cause the Credit Union to cease to continue as agoing concern.

· Evaluate the overall presentation, structure and content of the financialstatements, including the disclosures, and whether the financial statementsrepresent the underlying transactions and events in a manner that achieves fairpresentation.

We communicate with those charged with governance regarding, among other matters,the planned scope and timing of the audit and significant audit findings, including anysignificant deficiencies in internal control that we identify during our audit.

We also provide those charged with governance with a statement that we have compliedwith relevant ethical requirements regarding independence, and to communicate withthem all relationships and other matters that may reasonably be thought to bear on ourindependence, and where applicable, related safeguards.

From the matters communicated with those charged with governance, we determinethose matters that were of most significance in the audit of the financial statements ofthe current period and are therefore the key audit matters. We describe these mattersin our auditor’s report unless law or regulation precludes public disclosure about thematter or when, in extremely rare circumstances, we determine that a matter shouldnot be communicated in our report because the adverse consequences of doing so wouldreasonably be expected to outweigh the public interest benefits of such communication.

BICCU ANNUAL GENERAL MEEING 2020

39

The notes on pages 43 to 87 form an integral part of these financial statements.

BICCU ANNUAL GENERAL MEEING 2020

40

6

BAHAMA ISLANDS CO-OPERATIVE CREDIT UNION LIMITED

STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

FOR THE YEAR ENDED 31 DECEMBER 2019

Note 2019 2018$ $

FINANCE INCOMELoan interest income 16 2,864,486 2,668,554

Investment interest income 16 308,769 248,530

3,173,255 2,917,084FINANCE COST Deposit interest expense 16 1,078,160 1,172,961

Borrowings 16 101,157 112,929

1,179,317 1,285,890NET FINANCE INCOME BEFORE PROVISION FOR LOAN LOSSES 1,993,938 1,631,194 Provision for loan losses 9 (857,198) (332,983)

NET FINANCE INCOME 1,136,740 1,298,211Non-interest income 17 1,448,079 1,089,968

2,584,819 2,388,179OPERATING EXPENSES Personnel 18 924,682 759,495

Organisational 19 231,367 231,213 General business 20 219,261 329,654

Occupancy 21 331,082 361,322 Members’ security 22 330,209 339,336

Computer expense 23 91,374 80,805 Marketing 24 38,647 49,618

2,166,622 2,151,443

NET INCOME FOR THE YEAR 418,197 236,736

OTHER COMPREHENSIVE INCOME/(LOSS)Fair value gain/(loss) on investments 2,180 (16,830)

TOTAL COMPREHENSIVE INCOME $420,377 $219,906====== ======

The notes on pages 9 to 53 form an integral part of these financial statements.

7BAHAMA ISLANDS CO-OPERATIVE CREDIT UNION LIMITED

STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 31 DECEMBER 2019

Qualifying Statutory Fair value Donated Retained shares reserve fund reserve capital earnings Total $ $ $ $ $ $

1 January 2018 1,250,800 3,020,218 110,480 -- 832,159 5,213,657

Comprehensive income Net income for the year -- -- -- -- 236,736 236,736 Other comprehensive loss -- -- (16,830) -- -- (16,830) -- -- (16,830) -- 236,736 219,906Transactions with owners Net shares issued during the year 167,000 -- -- -- -- 167,000 Dividends on qualifying shares -- -- -- -- (99,056) (99,056) 167,000 -- -- -- (99,056) 67,944Transfer between reserves Statutory reserve -- 240,929 -- -- (240,929) --31 December 2018 1,417,800 3,261,147 93,650 -- 728,910 5,501,507Effect of IFRS 9 adoption (Note 9) -- -- -- -- (557,290) (557,290)31 December 2018, as restated 1,417,800 3,261,147 93,650 -- 171,620 4,944,217

Comprehensive income Net income for the year -- -- -- -- 418,197 418,197 Other comprehensive income -- -- 2,180 -- -- 2,180 -- -- 2,180 -- 418,197 420,377Transactions with owners Net shares issued during the year 136,000 -- -- 7,400 -- 143,400 Dividends on qualifying shares -- -- -- -- (56,128) (56,128) 136,000 -- -- 7,400 (56,128) 87,272Transfer between reservesStatutory reserve -- 104,528 -- -- (104,528) --

31 December 2019 $1,553,800 $3,365,675 $95,830 $7,400 $429,161 $5,451,866 ======= ======= ===== ==== ====== =======

The notes on pages 9 to 53 form an integral part of these financial statements.

The notes on pages 43 to 87 form an integral part of these financial statements.

BICCU ANNUAL GENERAL MEEING 2020

41

7BAHAMA ISLANDS CO-OPERATIVE CREDIT UNION LIMITED

STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 31 DECEMBER 2019

Qualifying Statutory Fair value Donated Retained shares reserve fund reserve capital earnings Total $ $ $ $ $ $

1 January 2018 1,250,800 3,020,218 110,480 -- 832,159 5,213,657