Better Budgeting - CIMA · CIMA – ICAEW FFM BETTER BUDGETING CONTENTS July 2004 This publication...

16

FACULTY OF FINANCE AND MANAGEMENT, ICAEW www.icaew.co.uk/fmfac Tel: +44 (0)20 7920 8486 Fax: +44 (0)20 7920 8784 CHARTERED INSTITUTE OF MANAGEMENT ACCOUNTANTS www.cimaglobal.com Tel: +44 (0)20 7663 5441 Fax: +44 (0)20 7663 5442 Better Budgeting A report on the Better Budgeting forum from CIMA and ICAEW July 2004 Price: £15.00

Transcript of Better Budgeting - CIMA · CIMA – ICAEW FFM BETTER BUDGETING CONTENTS July 2004 This publication...

FACULTY OF FINANCE AND MANAGEMENT, ICAEW www.icaew.co.uk/fmfac Tel: +44 (0)20 7920 8486 Fax: +44 (0)20 7920 8784

CHARTERED INSTITUTE OF MANAGEMENT ACCOUNTANTS www.cimaglobal.com Tel: +44 (0)20 7663 5441 Fax: +44 (0)20 7663 5442

Better BudgetingA report on the Better Budgeting forum

from CIMA and ICAEW

July 2004 Price: £15.00

CIMA – ICAEW FFM

CONTENTSBETTER BUDGETING July 2004

This publication is based on the Better Budgetingforum held at Chartered Accountants’ Hall, London,on 24 March 2004. The event was jointly sponsoredby the Faculty of Finance and Management of theInstitute of Chartered Accountants in England andWales and the Chartered Institute of ManagementAccountants.

Any enquiries about this publication should beaddressed to:

Danka StarovicThe Chartered Institute of ManagementAccountants26 Chapter Street London SW1P 4NP Telephone: +44 (0)20 8849 2342 E-mail: [email protected]

or to:

Chris JacksonThe Faculty of Finance and Management, ICAEWChartered Accountants’ Hall, PO Box 433, Moorgate Place, London EC2P 2BJ Telephone: +44 (0)20 7920 8486 E-mail: [email protected]

For further details about CIMA and the Faculty,please see the inside back cover. The publication wasproduced by Silverdart Ltd (see back cover) on behalfof CIMA and the Faculty.

ISBN 1-84152-286-4

BetterBudgeting

FOREWORD 1

ROUND TABLE DISCUSSIONS

Debating the traditional roleof budgeting in organisations 2A report on the discussion by participants

COMPANIES REPRESENTED ATTHE FORUM 6

PRESENTATIONS

Driving value through strategic planning and budgeting 7Dr Mike Bourne, director of the Centre for Business Performance, Cranfield School of Management

The ‘beyond budgeting’ journey towards adaptive management 8Dr Peter Bunce, director of the Beyond Budgeting Round Table, Europe

Better budgeting orbeyond budgeting? 10Dr Stephen Lyne, senior lecturer in accountingand management, University of Bristol, andProfessor David Dugdale, professor of management accounting, University of Bristol

BIBLIOGRAPHY inside back cover

FOREWORD

1CIMA – ICAEW FFM

BETTER BUDGETINGJuly 2004

Foreword

Chris Jackson, head of theFaculty of Finance andManagement, ICAEW.

Danka Starovic, seniortechnical issues manager of the Chartered Institute ofManagement Accountants.

This dual-badged publication has beenproduced jointly by ICAEW and CIMA. It isbeing distributed as a Special Report byICAEW’s Faculty of Finance & Managementand as a Technical Report by CIMA.

The publication aims to present the latestthinking on budgeting from thought leaders,finance directors and financial controllersfrom large and respected companies. A list ofcompanies that participated is included onpage 6.

On 24 March 2004, ICAEW and CIMA helda joint round table event at CharteredAccountants Hall. The intention of thegathering was for senior members of bothinstitutes to discuss some of the practicalissues and challenges they face in planningand budgeting. The event was introducedby Paul Druckman, deputy president ofICAEW (now president) and chaired byCharles Tilley, the chief executive of CIMA.

The two institutes agreed to work togetherbecause budgeting is an important issue forprofessional accountants in business. Thecollaboration doubled the intellectual inputand halved the cost. It was experimental and– as the feedback showed the evening to be asuccess – we hope to repeat it.

The evening started with presentations fromDr Mike Bourne of Cranfield School ofManagement, Dr Peter Bunce of the BeyondBudgeting Round table and Dr Stephen Lyneand Professor David Dugdale from the

University of Bristol. They set the scene forthe day by presenting the results of theirresearch and highlighting the latest thinkingon the subject.

In the ensuing round table discussions,participants highlighted examples of bestpractice in their own organisations, as wellas suggesting areas deserving of furtherresearch or improvement. The debate waslively, and, if there was one overallconclusion of this session, it was thatbudgeting is alive and well, though practiceis evolving with new tools and techniques.

The event was held under ‘Chatham House’rules, ie participants could be open in theknowledge that their comments would notbe attributed to their companies, many ofwhom were large and well-known.

We are grateful to the speakers and inparticular to the finance directors andfinancial controllers who found time to takepart and thus provide the content for thispublication.

One of the most important objectives of theday for both CIMA and ICAEW was toengage with members and developrelationships and partnerships with them.In this way, members can help guide theinstitutes’ agendas as well as draw supportfor their businesses in the future. Theconclusions of the day’s discussions wererecorded for publication for the benefit ofwider membership. ■

The afternoon’s discussion aimed to explorethe budgeting theory and practice from theunique perspective of the finance function.In most organisations, the finance depart-ment ‘owns’ and administers the budgetingprocess. Accountants are therefore first inthe line of fire for its perceived shortcom-ings and are charged with making the nec-essary changes.

The debate, led by CIMA and ICAEW facili-tators, was an opportunity for a frank andconfidential exchange of views amongstsenior finance professionals about theseand other issues related to budgeting. Thissummary is not an attempt to be prescrip-tive about how budgeting ought to be doneand we are aware of the limitations of oursample size. It is simply an attempt to pro-vide a snapshot of the current best practicein some of the UK’s leading organisations.

The budget is dead, long live the budget

If you were to believe all that has been writ-ten in recent years, you’d be forgiven forthinking that budgeting is on its way tobecoming extinct. Various research reportsallude to the widespread dissatisfactionwith the bureaucratic exercise in cost-cut-ting that budgeting is accused of havingbecome. Budgets are pilloried as being outof touch with the needs of the modernbusiness and accused of taking too long,costing too much and encouraging all sortsof perverse behaviour.

Yet if there was one conclusion to emergefrom the day’s discussions, it was thatbudgets are in fact alive and well. Not onlydid all the organisations present operate aformal budget but all bar two had nointerest in getting rid of it. Quite theopposite – although aware of the problemsit can cause, the participants by and large

regarded the budgeting system and theaccompanying processes as indispensable.

Research in organisations seems to suggestthat this is a commonly held view and thattraditional budgeting remains widespread.Some claim that as many as 99% ofEuropean companies have a budget in placeand no intention of abandoning it(Kennedy and Dugdale 1999:22 quoted inVuorinen).

A framework of control

CIMA’s Official Terminology of ManagementAccounting defines a budget as: ‘a quantita-tive statement for a defined period of time,which may include planned revenues, assets,liabilities and cash flows. A budget providesa focus for the organisation, aids the co-ordi-nation of activities and facilitates control.’

It is this last point that the participants sin-gled out as the main reason why budgetingcontinues to add value in their organisa-tions. Quite simply, it provides an overallframework of control without which itwould be impossible to manage.

Large companies in particular would strug-gle to plan, co-ordinate and control with-out such a framework. But, even in smallcompanies, a budget can provide a roadmap detailing where the business is, whereit wants to go and how it can get there.

Of course, this does not mean that a budgetcan prepare the company for every eventu-ality. Any budget is based on a set ofassumptions that may change as soon as it’spublished. Keeping an eye on the potentialrisks and changes in the environment isessential – as one delegate noted, budgetingmay provide you with a map but if youdrive with your eyes closed, you will crashanyway.

2 CIMA – ICAEW FFM

BETTER BUDGETING July 2004ROUND TABLE

Debating the traditional role ofbudgeting in organisations

Participants in the Better Budgeting forum discussed a range of issues relevant to thecentral theme, debating possible ways of improving the budgeting process andhighlighting areas for future research.

In mostorganisations,finance ‘owns’the budgeting

process

Variousresearchreports

allude towidespread

dissatisfaction– yet the

debateshowed thatbudgets are

alive and well

ROUND TABLE DISCUSSIONS

3

The delegates were keen to point out thatthere are also disadvantages to having for-mal controls in place. Some thought thatbudgets can stifle the entrepreneurial, risk-taking culture that, ultimately, can beresponsible for value creation. It can, forexample, force businesses to abandon newprojects because the resources for the yearhave already been allocated. In addition, try-ing to perfect control systems can lead to anexcessively inward focus at the expense ofcompetitive awareness and agility. The par-ticipants agreed that companies need tocounteract this with a culture that valuesopenness and flexibility.

From cost-cutting to value creation

There was an almost unanimous agreementamongst those present that budgets haveundergone some significant changes in thelast 20 or so years.

Then, the emphasis was on centralised andhighly bureaucratic cost control which leadsomeone to remark that while sociologistssee control as a problem, accountants see itas a solution. Now, it seems that budgets areused more often to contribute directly tovalue creation. They inform strategy imple-mentation, risk management and resourceallocation and are generally regarded as anintegral part of running a business.

The participants agreed that budgeting hasbeen evolving to meet the changing needsof modern business. Instead of abandoningit altogether, it seems that companies aresimply adapting it. This is not unusual –research shows that over 60% of companiesclaim they are continuously trying toimprove the budgeting process to meet thedemands set for management in creatingsustainable value (Ekholm and Wallin,2000, quoted in Vuorinen).

‘One man’s budget is another man’srolling forecast’

It quickly became obvious that, as one par-ticipant put it, “one man’s budget is anoth-er man’s rolling forecast”. What peoplerefer to when they talk about budgetingcould in reality be very different things.

But in general, for many of those presenton the day, the budget is prepared once ayear and supplemented by regular forecasts

as well as different ways of capturing non-financial performance data.

In fact, it could be said that the use of vari-ous tools to complement the traditionalbudget is precisely what allowed it tobecome more flexible and dynamic.

Forecasting

The increasing use of forecasting, in particu-lar, has meant that budgets have becomemore forward-looking and better linked tostrategic planning. In fact, the rolling fore-cast emerged as one tool in widespread usethat almost all the participants – but espe-cially those in companies that operate infast-changing environments – regarded asuseful.

Several participants thought that, in theircompanies, forecasting is in fact moreimportant than budgeting. Because theassumptions on which the budgeting num-bers are based change so quickly, theydepend on forecasts which are updatedmore frequently.

However, a detailed budget still provides abasis to work from, especially if somethinggoes wrong. It acts as an anchor – althoughthings change along the way, it is importantnot to lose sight of what was budgeted in thefirst place.

Forecasts are regarded as being high-levelplans, whereas budgets contain more detail.One participant referred to budgeting asbeing about “looking into boxes you rarelyopen”. Interestingly, it is precisely thisopportunity to discuss issues with otherparts of the organisation that for many rep-resents the real benefit of budgeting.Setting objectives and targets for the yearahead can only be done through a greatdeal of inter-functional co-ordination.

It is almost as if the process itself is morerelevant than the actual numbers – as thedelegates noted, the detail often becomesirrelevant after the first quarter anyway.There was a strong feeling that this bottom-up approach to budgeting was an opportu-nity for everyone to think and talk aboutthe factors influencing the performance of abusiness. As one participant put it: “it isimportant to get together and discuss issues.I know we should be doing this all the timebut the budget forces you to do it”.

CIMA – ICAEW FFM

BETTER BUDGETINGJuly 2004 ROUND TABLE

Budgets haveundergonesignificantchanges overthe last twodecades

Companiesincreasinglyuseforecasting –and some seeit as moreimportantthanbudgeting

4

In addition, better co-operation betweendifferent functions should result in betterquality budgets that take less time toprepare. Those ‘closer to the coalface’ willhave better assumptions on which to basethe numbers. This in turn should lead tofewer iterations in the preparation ofbudgets.

How often forecasts are done largelydepends on the nature of the business andthe environment in which it operates. Afast-changing industry such as telecommu-nications would need constant updatingwhereas, say, a not-for-profit organisationwith relatively predictable annual revenueswould only need to do a fixed budgetannually.

Non-financial performance measures

The participants acknowledged the impor-tance of non-financial data but were some-what apprehensive about its lack of integrityand the resulting loss of control. Theyagreed that coming up with non-financialperformance measures and targets isn’t initself difficult, but linking those clearly tofinancial strategy and results was much moreproblematic.

This is particularly obvious in the context ofthe now ubiquitous balanced scorecard.Many companies found the cause-and-effectlinkages between the four quadrants of thescorecard – financial, operational, customerand learning – difficult to prove. They oftendo not have any degree of empiricalunderpinning, so strategy is based onintuition rather than fact. The participantsadmitted that there is still a long way to gobefore non-financial data can be completelytrusted.

Technology

Part of the reason why budgeting practicewas able to evolve is because it has beensupported by new technology which haschanged the way data is collected andstored in organisations. In some cases,enterprise-wide systems have increasedboth the speed and the accuracy of budgetsand forecasts.

Both are crucial – frequent reforecasting, forexample, is simply not possible if it takesthe finance department months to collect

and reconcile the relevant data. In addition,working from a single data set can helpalign budgets to operational plans andstrategic objectives – it ensures a visibilityof assumptions that have gone into deci-sion-making.

New technology has also helped companiesmove away from organisational culturecharacterised by functional divisions and‘silo’ mentality. Managers using off-linespreadsheets, for example, can end up dis-connected from other parts of the businessthat would impact on their planning.

Last but not least, speed and accuracy meanthat budget holders have more time tofocus on activities which really add value tothe business rather than on collecting dataand ensuring its integrity.

There have been negative effects of techno-logical changes too. For example, somemaintained that enterprise resource plan-ning (ERP) systems have led to a higherdegree of centralisation which is at oddswith the more bottom-up, participativenature of the more recent budgeting prac-tice. This seems to contradict the promise ofnew technology to make data more widelyavailable and more transparent. Otherspointed out that the pace of technologicalchange outstrips the more gradual andorganic culture change so there will often bea disconnect between the two.

Plus, the sheer amount of data such systemsare capable of generating is daunting. Onedelegate said that his company’s state-of-the-art new platform was abandoned after onlytwo years because the unnecessary data itwas producing was resulting in micro-man-agement. More data means it is tempting tokeep adding to the budget – and prudentaccountants may be particularly guilty ofthis. “You need to be very brave to takethings away”, noted one participant.

Culture and incentives

Organisational culture is by far the biggestinfluence on how formal systems andprocesses operate in practice. Fostering theright culture, whatever that may be in thecontext of individual companies, was recog-nised as one of the most important factors inthe success or otherwise of budget practice. Unsurprisingly, the discussions offered no‘silver bullet’ solution to creating the kind

CIMA – ICAEW FFM

BETTER BUDGETING July 2004ROUND TABLE

Better co-operation

should resultin betterbudgets

Participantswere

apprehensiveabout non-

financialmeasures

New technologyhas movedcompaniesaway from

‘silo’ mentality– but has also

generateddaunting data

volumes

5

of environment where the budget is free ofsub-optimal behaviour and skewed incen-tives. According to delegates, if the less cen-tralised budgeting is to survive, it needs tobe supported by a culture of trust andempowerment. But the difficulties of creat-ing a system of accountability that isn’tplagued by blame and mistrust – as is fre-quently the case with budgeting – wereopenly acknowledged.

Commitment at the highest level is crucialto making changes to the process. However,the ever-shortening tenure of an averagechief executive officer (CEO) was seen asmore of a threat than an opportunity – anew CEO may be in the best position tomake radical changes but he/she may beunwilling to try a new and perhaps moreradical approach to performance manage-ment and put their reputation on the line.In any case, culture and attitudes takelonger to change than the average time aCEO spends in a job.

Pay and reward structures were seen as byfar the biggest influence on people’s moti-vation. Few of the companies had remuner-ation tied to achievement of budgetary tar-gets – although this is recognised as com-mon practice – acknowledging that it canresult in dysfunctional behaviour. It canalso lead to budgeting becoming a way ofnegotiating pay. Instead, in some compa-nies, pay is deliberately linked to other tar-gets. For senior executives, this can be totalshareholder returns relative to peers.

The weight of City expectations

As part of the wider debate about the pur-pose of budgeting, one of the main issuesdiscussed was the relationship between thenumbers contained in budgets and forecastsand those disclosed formally – and sig-nalled informally – to capital markets andto City analysts in particular. Does the pres-sure of City expectations and the desire tomeet them mean that there is a risk of agap between the two?

Internal forecasts – which are often ‘stretch’targets used to motivate and sometimesincentivise employees – could become thebasis of what is communicated to analystsand therefore of analysts’ own predictions.It is not difficult to imagine a situation inwhich a company feels under pressure ifthose targets are then not reached.

Alternatively, the opposite could happenwith companies deliberately communicat-ing a lower figure to the City to ensureforecasts are met. Either way, there ispotential mismatch.

Few companies would admit to artificiallysmoothing their earnings to meet analysts’forecasts yet research has shown that thishappens on a regular basis. Short-termactions can often produce the results tomeet profit expectations. If that fails, any-thing from mild cosmetic enhancements toaggressive earnings management can beused to get the ‘right’ number.

The participants were unanimous in sayingthat there needs to be a clear line of sightbetween the numbers used to run the busi-ness and those communicated externally.They argued that if the analysts’ forecastsdiffer wildly from their own, companiesneed to understand why and act immedi-ately to correct any discrepancies.Management credibility is rooted in goodcommunication with the City and the keyis to be honest and realistic.

Despite this, there was an admission thatthe way companies control their relation-ship with the City has become an impor-tant part of their overall strategy. Thedynamics of relationships has changed,with investors – and other stakeholders –becoming more demanding.

The participants conceded that externalexpectations, chiefly from analysts andfund managers, always play a part in howcompanies are managed. This is, to a cer-tain extent, inevitable as long as thoseexpectations do not end up being translat-ed into unrealistic internal targets. Theonus is on companies to communicatewith honesty and integrity. The resultingtrust in management will mean their mes-sages stand less chance of being misunder-stood.

Conclusion

Budgeting is evolving, rather than becom-ing obsolete. Although it has changed, thechange has been neither dramatic nor radi-cal. Instead, we have witnessed incremen-tal improvements, with traditional budgetsbeing supplemented by new tools andtechniques. Forecasting has become animportant tool to manage the continuously

CIMA – ICAEW FFM

BETTER BUDGETINGJuly 2004 ROUND TABLE

Lesscentralisedbudgetingneeds aculture oftrust andempowerment

Managementcredibility isrooted in goodcommunicationwith the City

Investors aremoredemanding –andcompaniesmust havehonesty andintegrity

6

changing environment. We have also seen ashift from the top-down, centralised processto a more participative, bottom-up exercisein many companies.

It is a pragmatic message that won’t appealto everyone. But those who call for a morefundamental change, including abandoningbudgets altogether, should take comfortfrom the fact that it is precisely their critiquethat exposed many of the inherent problemsof traditional budgeting. It is likely that thisinspired at least some of the changes men-tioned. As always, instead of following theconsultants’ or academics’ advice by thebook, companies pick and choose accordingto their individual circumstances.

There is a real opportunity for finance toraise its game in this area and become

more of a business partner by encouragingunderstanding of budgets across the organ-isation. There was no consensus aboutwhether the finance function should ownor simply facilitate the budgeting process.But the participants thought that its roleshould be to educate other parts of theorganisation about what value-creatingdecisions are – and how they are not neces-sarily the same as profit-making ones. Italso needs to supply the information andanalysis required to support these deci-sions.

In the end, good budgeting comes down totrust, integrity and transparency. It maynot add value directly but, as someoneremarked on the night, “there are certainthings that can’t be achieved any otherway”. ■

CIMA – ICAEW FFM

BETTER BUDGETING July 2004ROUND TABLE

The following companies were represented at the Better Budgeting forum

Allen & Overy LLP

Armstrong Laing Group

Atos KPMG Consulting

BAA plc

BAT

BBC

Bellis-Jones, Hill Group

Beyond Budgeting Round Table

BUPA

Cranfield School of Management

Celltech Pharmaceuticals Limited

DHL Worldwide Express

DIAM International

ESAB

Ford Premier Automotive Group

GlaxoSmithKline

Jaguar

Jarvis

Land Rover

Partners for Change

Pelican Shipping Limited

PGA European Tour

Procter & Gamble

Rank Hovis Ltd

Research International

J Sainsbury plc

Samsung

Three Valleys Water

TNT Express Services

Unilever

University of Bristol

WSP Group plc

Budgeting isevolving,

rather thanbecoming

obsolete – itdepends on

trust andtransparency

Driving value through strategicplanning and budgeting

7

In 2001, Cranfield University teamed upwith Accenture’s Finance and PerformanceManagement Service line to undertake alarge worldwide review of planning and bud-geting. They focused on 15 companies in theUS and Europe which had already madeadjustments to their budgeting practice. Inaddition, the researchers reviewed over 100academic and practitioner books on the sub-ject.

The results showed a widespread dissatisfac-tion with the budgeting process (see box,right). The catalogue of complaints was theusual one: the process was too time consum-ing, too costly, too distorted by gaming, toofocused on cost control and so on. Most sig-nificantly, budgeting seemed almost totallydivorced from the company’s overall strategicdirection.

The aim of the research was to try and estab-lish what constitutes best practice in plan-ning and budgeting in those companies thathave already made adjustments to theirprocesses. Unsurprisingly, the researchersfound that there was no uniform view –instead, companies reported a variety ofapproaches and reform priorities. Some aremanaging without budgets, some are separat-ing budgeting from re-forecasting, some areaiming for fast closing, and so on.

The research team did, however, identify someunderlying principles common to all the com-panies investigated. These are not tools ortechniques as such – rather, they seem to rep-resent a more general philosophy and a newapproach to budgeting by leading companies,which:

● have an external focus – what matters at theend of the day is their performance againstcompetitors, not their results against analready out-of-date budget. The targets are

linked to external benchmarks, not past per-formance, and the incentives are deliberate-ly separated from budgets. This serves toeliminate some of the gaming that blightsthe traditional budgeting process;

● are explicitly focused on strategy – theyknow that better financial performanceultimately comes from having and main-taining competitive advantage in the mar-ket place, not from better financial man-agement in itself. This strategic orienta-tion means that leading companies fre-quently use strategy-related scorecardsdesigned to measure more than just thefinancial targets;

● invest in IT systems which generate a com-mon set of numbers throughout the company– very often this is not the case and timeis wasted trying to reconcile numbers or

CIMA – ICAEW FFM

BETTER BUDGETINGJuly 2004 THE PRESENTATIONS

Criticisms of the budgeting process

● Budgets are time-consuming and costly to put together.● Budgets constrain responsiveness and flexibility and are

often a barrier to change.● Budgets are rarely strategically focused and are often con-

tradictory.● Budgets add little value, especially given the time required

to prepare them.● Budgets concentrate on cost reduction and not on value

creation.● Budgets strengthen vertical command and control.● Budgets do not reflect the emerging network structures

that organisations are adopting.● Budgets encourage ‘gaming’ and perverse behaviours.● Budgets are developed and updated too infrequently, usual-

ly annually.● Budgets are based on unsupported assumptions and guess-

work.● Budgets reinforce departmental barriers rather than encour-

age knowledge sharing.● Budgets make people feel undervalued.

PRESENTATION 1

The first presentation was given by Dr Mike Bourne, director of the Centre for Businessperformance at Cranfield School of Management. He described recent studies byCranfield into the budgeting processes of major European organisations.

Companieshave a rangeof approachesto budgetreforms – butthere aresomecommonunderlyingprinciples

8

get data from different, often incompatible,applications. Creating a single view eradi-cates the unnecessary duplication ofeffort;

● use explicit forecasting models, separate fromtheir financial management systems – theassumptions underlying those models aremade clear at every step of the way. Thismeans they can be changed in response toenvironmental triggers to produce a new,equally accurate forecast. A company isafforded a higher level of speed and flexi-bility; and

● put their efforts into managing future results,not explaining past performance – theyrealise that endless scrutiny of past resultsadds little value. Instead, they try to fore-cast variances before they occur and focuson taking actions that really do drivevalue. Many of those actions will be non-financial, which highlights the limitationsof traditional budgeting.

Even when all the above elements are present,the researchers point out that real change willbe unachievable without a high degree oftrust. Under the old budgeting system, controlwas exercised by business units and divisionsreporting their actual performance and vari-ances and the head office used this informa-tion to predict year-end results. By contrast,leading companies now trust their managersto tell them what they will achieve.

Finally, although the research as a whole iscritical of the budgeting process, the projectdoes not amount to a call to abandon budgetsaltogether. Instead, it highlights the level ofimprovement that can be achieved even withrelatively simple modifications and a greatdeal of trust. ■

For further information, see: www.som.cranfield.ac.uk/som/cbp/Research_Report.pdf

CIMA – ICAEW FFM

BETTER BUDGETING July 2004THE PRESENTATIONS

The ‘beyond budgeting’ journeytowards adaptive management

Dr Peter Bunce, director of the Beyond Budgeting Round Table, Europe, outlined thereasons for looking further than traditional methods of performance measurement andmanagement.

PRESENTATION 2

The Beyond Budgeting Round Table (BBRT)is at the centre of a movement to helporganisations continuously improve theirperformance in a business environment thatis market led, highly competitive and unpre-dictable, and in which intellectual capital isthe key strategic resource. It has been in exis-tence since 1998 with its origins in the UK,but it now has many members from the restof Europe, the US and Australia.

The BBRT is the combination of a new con-cept (‘beyond budgeting’) and a community(‘round table’). The BBRT community is anindependent research collaborative thatshares its knowledge across its global networkthrough conferences and workshops.

The BBRT starts off with the same catalogueof complaints about the failures of budget-

ing as some of the other studies – it is tootime-consuming, too expensive and com-pletely out of tune with the needs oftoday’s managers. Because it contains a mixof fixed targets and financial incentives, itdrives people to behave in ways that maybe at odds with the needs of the organisa-tion.

The BBRT also warns that budgets are a‘relic from an earlier era’. The problemsthey cause will be particularly acute incompanies that are trying to move awayfrom the command and control cultureand become more flexible. In a way, thebudgeting process acts as a protectiveshield blocking any attempt to change.

The BBRT maintains that ‘better budgeting’is not an answer – it merely speeds up the

The research iscritical, but

does not callfor

abandonmentof budgets

BBRT suggeststhat budgets

are a ‘relicfrom an earlier

era’

9CIMA – ICAEW FFM

BETTER BUDGETINGJuly 2004 THE PRESENTATIONS

current flawed process and perpetuates the‘fixed performance contract’ and centralisedcontrol.

The BBRT solution is radical – the only waythe inherent contradictions of the budgetingprocess can be resolved is by scrapping italtogether. It goes on to cite a number ofcompanies that have ‘broken free from theshackles of budgeting and its culture of gam-ing and misinformation’. They no longerproduce an annual detailed plan determin-ing the allocation of resources or what thebusiness units need to make or sell. Neitherdo they use such a plan for performanceevaluation and rewards. They have aban-doned the fixed performance contract,where individual incentives are based on theachievement of fixed targets.

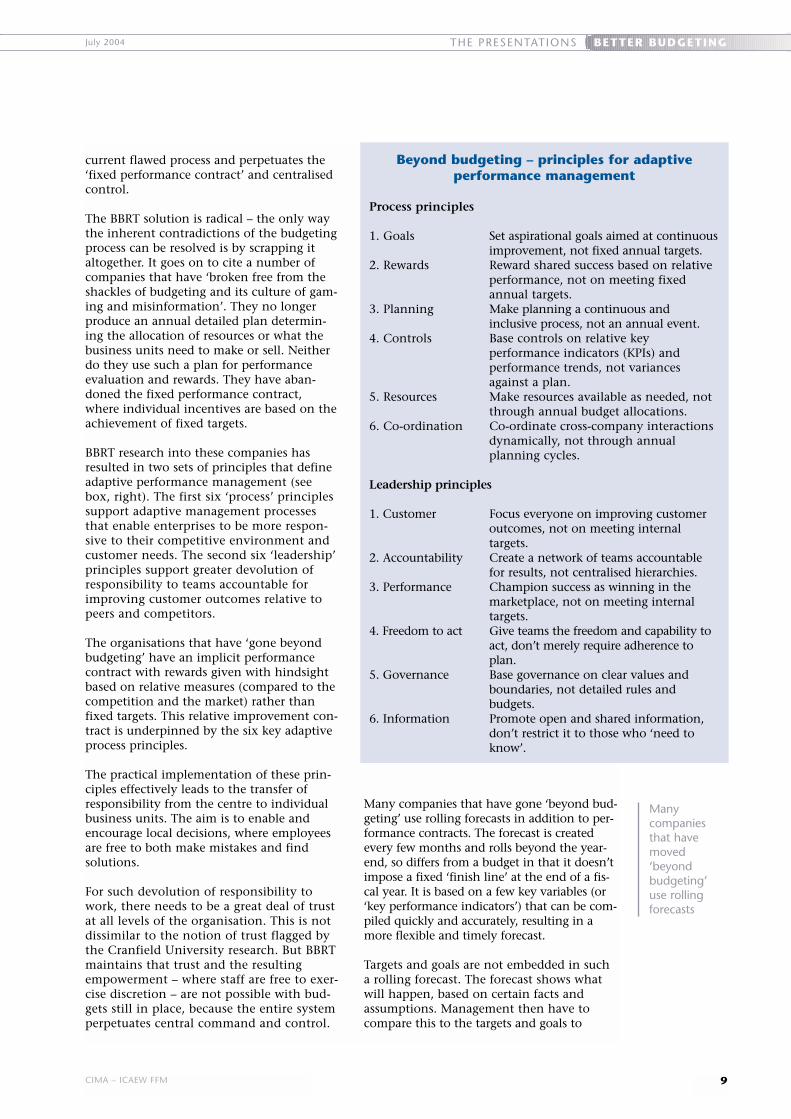

BBRT research into these companies hasresulted in two sets of principles that defineadaptive performance management (seebox, right). The first six ‘process’ principlessupport adaptive management processesthat enable enterprises to be more respon-sive to their competitive environment andcustomer needs. The second six ‘leadership’principles support greater devolution ofresponsibility to teams accountable forimproving customer outcomes relative topeers and competitors.

The organisations that have ‘gone beyondbudgeting’ have an implicit performancecontract with rewards given with hindsightbased on relative measures (compared to thecompetition and the market) rather thanfixed targets. This relative improvement con-tract is underpinned by the six key adaptiveprocess principles.

The practical implementation of these prin-ciples effectively leads to the transfer ofresponsibility from the centre to individualbusiness units. The aim is to enable andencourage local decisions, where employeesare free to both make mistakes and findsolutions.

For such devolution of responsibility towork, there needs to be a great deal of trustat all levels of the organisation. This is notdissimilar to the notion of trust flagged bythe Cranfield University research. But BBRTmaintains that trust and the resultingempowerment – where staff are free to exer-cise discretion – are not possible with bud-gets still in place, because the entire systemperpetuates central command and control.

Many companies that have gone ‘beyond bud-geting’ use rolling forecasts in addition to per-formance contracts. The forecast is createdevery few months and rolls beyond the year-end, so differs from a budget in that it doesn’timpose a fixed ‘finish line’ at the end of a fis-cal year. It is based on a few key variables (or‘key performance indicators’) that can be com-piled quickly and accurately, resulting in amore flexible and timely forecast.

Targets and goals are not embedded in sucha rolling forecast. The forecast shows whatwill happen, based on certain facts andassumptions. Management then have tocompare this to the targets and goals to

Beyond budgeting – principles for adaptiveperformance management

Process principles

1. Goals Set aspirational goals aimed at continuousimprovement, not fixed annual targets.

2. Rewards Reward shared success based on relativeperformance, not on meeting fixedannual targets.

3. Planning Make planning a continuous andinclusive process, not an annual event.

4. Controls Base controls on relative keyperformance indicators (KPIs) andperformance trends, not variancesagainst a plan.

5. Resources Make resources available as needed, notthrough annual budget allocations.

6. Co-ordination Co-ordinate cross-company interactionsdynamically, not through annualplanning cycles.

Leadership principles

1. Customer Focus everyone on improving customeroutcomes, not on meeting internaltargets.

2. Accountability Create a network of teams accountablefor results, not centralised hierarchies.

3. Performance Champion success as winning in themarketplace, not on meeting internaltargets.

4. Freedom to act Give teams the freedom and capability toact, don’t merely require adherence toplan.

5. Governance Base governance on clear values andboundaries, not detailed rules andbudgets.

6. Information Promote open and shared information,don’t restrict it to those who ‘need toknow’.

Manycompaniesthat havemoved‘beyondbudgeting’use rollingforecasts

10 CIMA – ICAEW FFM

BETTER BUDGETING July 2004THE PRESENTATIONS

The survey investigated the current use ofbudgets in medium and large companies. Itattempted to identify the changes that havetaken place over the last five or so years,against the background of the debate aboutthe merits of budgeting.

Some experts have mounted wide-rangingcritiques of the manner in which budgetingsystems are typically implemented. Theprocess can often be bureaucratic and expen-sive, budgeting can fail to meet the needs ofmanagers in competitive environments andbudget systems can lead to managerial ‘gam-ing’ of the numbers. In practice, recommen-dations to go ‘beyond budgeting’ ofteninvolve virtually abandoning budgeting.These criticisms are primarily made by non-financial managers who have to ‘suffer’ atthe hands of management accountants

persisting in implementing outdated budget-ing procedures.

This project found little evidence to supportthese views. There seems to be no widespreaddissatisfaction with traditional budgeting.Instead, managers generally see budgets asimportant, especially for planning, controland evaluation. There is also a high degree ofagreement between financial managers (FMs)and non-financial managers NFMs) on therole and importance of budgeting.

The research project was based on a surveymailed to companies in the South-West ofEngland. By concentrating on companieswhere the financial manager was a member ofBristol Centre for Management AccountingResearch (BRICMAR), an overall response rateof 40.1% was obtained.

ascertain the gaps and determine how theseare to be managed.

BBRT is keen to stress that going ‘beyond bud-geting’ is not about new ‘tools’ or ‘tech-niques’. It is a management philosophy basedon a set of principles developed from realcases leading to adaptive performance man-agement.

The tools already exist – eg, balanced score-cards, rolling forecasts, customer relationshipmanagement, benchmarking, shareholdervalue models, enterprise wide information sys-tems and activity based management amongstothers. But by and large, they have failed todeliver on their promises because the underly-ing processes haven’t been changed to accom-modate them.

The potential of those models has, in effect,been ‘neutralised by the powerful antibodiesof the budgeting immune system. Budgeting,perhaps more than any other process,defines the cultural norms inside an organi-sation.’

There is no simple recipe to implement‘beyond budgeting’. The steps chosen willdepend on each company’s culture, struc-ture, history, IT infrastructure and so on.But there are lessons to be learnt from thepioneers. In many cases, it is simply aboutmanaging change – building and selling acase and creating a shared vision for thefuture. ■

For further information, see:www.bbrt.org

Beyond budgeting or better budgeting?

The final presentation was given by Dr Stephen Lyne, senior lecturer in accounting andmanagement at University of Bristol, and Professor David Dugdale, professor ofmanagement accounting at University of Bristol. They presented the results of theirrecent survey into attitudes towards budgeting.

PRESENTATION 3

Going beyondbudgeting is amanagement

philosophy

Criticism ofbudgeting is

primarilymade by non-

financialmanagers

THE PRESENTATIONS

11CIMA – ICAEW FFM

BETTER BUDGETINGJuly 2004

A completed questionnaire was requestedfrom both a financial and a non-financialmanager in each company. In 40 companies afinance manager responded and in 21 of thesea completed questionnaire was also receivedfrom a non-financial manager.

The first research question sought to deter-mine whether FMs and NFMs had differentattitudes to budgeting in their companies.The overwhelming yet surprising findingwas that these two sets of managers gavevery similar answers throughout the ques-tionnaire.

The only significantly different responsesrelated to the time consuming nature of bud-gets and their realism and importance:

● FMs agreed more strongly with the state-ment that ‘budgets are too time-consumingfor the results achieved’; and

● NFMs agreed more strongly that ‘budgetsare unrealistic’ and ‘budgets are too inaccu-rate: more resources and technology needsto be devoted to them’.

Perhaps these results reflect the fact that FMsactually do most of the work in preparing,disseminating and updating budgets. NFMsdo not necessarily see budgets as overlytime-consuming and counterproductive.

All 40 FMs confirmed that their companies setbudgets, typically starting the process four to

six months before the start of the financialyear. Some 80% agreed that there were fre-quent revisions to the budget during the bud-geting process. More than 90% reported bothmonth and year-to-date figures showing bud-gets, actual results and variances. Fewer report-ed results for the previous year although 80%showed some past year data for comparison(either actual figures, variances or both).About 75% of the respondents also reportedthat their companies provide some estimate ofthe out-turn for the current financial year.

The chosen sample of FMs revealed a nearuniversal view that budgets are important (seebox, above). However, budgets can still haveunfortunate consequences and, in view of thebad press that budgeting has received inrecent years, it might be expected that man-agers would be unhappy with their budgetingsystems on a number of counts. But theresults do not support such expectations.Around 55% of respondents reported someform of change in the past five years and anumber of themes emerged from their writtencomments, eg:

● greater involvement of junior managementin budgeting processes;

● more detailed analysis; and ● intensification of the use of budgets.

In only one company did there seem to be aless intensive approach to budgeting withmonthly sales targets abandoned in favour of

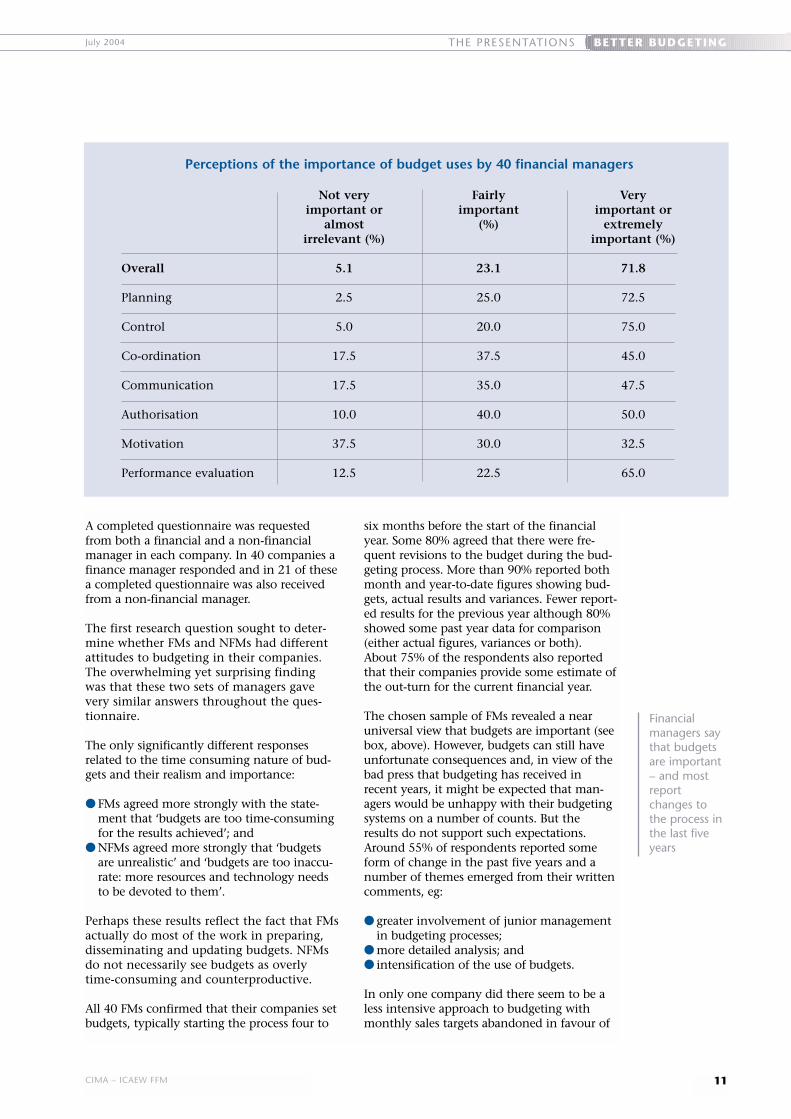

Perceptions of the importance of budget uses by 40 financial managers

Overall

Planning

Control

Co-ordination

Communication

Authorisation

Motivation

Performance evaluation

Not veryimportant or

almostirrelevant (%)

5.1

2.5

5.0

17.5

17.5

10.0

37.5

12.5

Fairlyimportant

(%)

23.1

25.0

20.0

37.5

35.0

40.0

30.0

22.5

Veryimportant or

extremelyimportant (%)

71.8

72.5

75.0

45.0

47.5

50.0

32.5

65.0

Financialmanagers saythat budgetsare important– and mostreportchanges tothe process inthe last fiveyears

12 CIMA – ICAEW FFM

BETTER BUDGETING July 2004THE PRESENTATIONS

a six monthly target. This was intended toencourage managers to maximise monthlysales (rather than simply meet the budget).These results seem to be in direct contrast tothe BBRT critique.

Budgeting has become more important inrecent years, as have a number of ‘modern’ideas, such as the balanced scorecard. Thesurvey also suggests that the importance ofstandard costing and variance analysisseems to be diminishing. However, whiletraditional budgeting is now more likely tobe combined with increased use of non-financial indicators, its demise seemsunlikely.

The researchers suggest that budgets can beanalysed on two dimensions: implementa-tion, control and evaluation; and planning. Also, negative attitudes to the consequencesof budgeting can be analysed on six dimen-sions: bureaucracy; poor culture; gaming;rigidity; causing conflict between realisticand challenging targets; and having a histor-ical, constraining orientation.

This analysis also identified four dimensionsin respondents’ attitudes to certainty/uncer-tainty: certainty of actions; certainty of out-comes; uncertainty of outcomes; and uncer-tainty in the environment.

The authors point out a number of associa-tions:

● in competitive, uncertain situations juniormanagers were more likely to be involvedin budgeting processes. In relatively stableenvironments junior managers were lesslikely to be involved;

● the dangers of excessive centralisationwere flagged by a strong correlationbetween top management driving thebudget process and perceived bureaucracyand the inhibition of junior managers;

● there was a significant correlation betweensophisticated IT and top management dri-ving the budget. However, there was also apositive correlation between sophisticated

IT and both the involvement of juniormanagers and multiple budget iterations.The researchers conclude that IT can facili-tate greater managerial involvement and amore complex process;

● in relatively predictable environmentsbudgets are likely to be more importantfor control (not planning) and managerstend to disagree with pejorative state-ments about budgeting; and

● when there is more uncertainty, budgetsbecome less important for control andmore important for planning. A realisticbudget is sufficiently challenging to man-agers. There are likely to be more itera-tions during preparation of the budgetand, perhaps because of this, greater scopefor managerial gaming.

The researchers identified significant correla-tion between managers’ satisfaction and cer-tain contingent variables:

● satisfaction was greatest in stable envi-ronments where budgets were taken seri-ously, especially for control and evalua-tion; and

● conversely, satisfaction was lower in moreuncertain situations and when the budgetprocess was perceived to be bureaucraticor the cause of de-motivation and a cul-ture of blame.

In the light of the findings, one can imaginetwo ‘ideal types’ of budget process:

● in stable circumstances, the budget mightbe prepared efficiently with few iterationsand little junior management involve-ment. There may be dangers in excessivecentralisation; and

● in competitive, uncertain situations, thebudgeting process might involve severaliterations with greater involvement ofjunior managers. There may be dangers ofcomplexity and gaming. ■

A full working paper on which this briefing paperwas based can be accessed at the BRICMAR website: www.ecn.bris.ac.uk/www/ecsrl/bricmar.htm

Theimportance of

standardcosting and

varianceanalysis seems

to bediminishing

Satisfaction isgreatest where

budgets aretaken seriously

CIMA – ICAEW FFM

BETTER BUDGETINGJuly 2004 B IBLIOGRAPHY / ABOUT US

About CIMA

The Chartered Institute of ManagementAccountants (CIMA) represents financial man-agers and accountants working in industry,commerce, not-for-profit and public-sectororganisations. Its key activities relate to busi-ness strategy, information strategy and financialstrategy. CIMA is the voice of over 80,000 stu-dents and 62,000 members in 155 countries. Itsfocus is to qualify students, to support bothmembers and employers and to protect thepublic interest.

For further information visit:www.cimaglobal.com

About the Faculty

The Faculty of Finance and Management is oneof five specialist faculties established by theInstitute of Chartered Accountants in Englandand Wales (ICAEW) and caters for the profes-sional needs of members working in industryand commerce and practising as consultants inthis field. We offer members up-to-date businessideas, the latest management tools, techniquesand information from an independent view-point, to help them be effective and to continuetheir professional development.

For further information visit:www.icaew.co.uk/fmfac

Accenture and Cranfield School of Management (2001)Driving value through strategic planning and budgeting,www.som.cranfield.ac.uk/som/cbp/P&B%20Report.pdf

Ahmad, N N M, Sulaiman, M, and Alwi, N M (2003) Arebudgets useful? A survey of Malaysian companies. ManagerialAuditing Journal, vol 18 no 9.

Barrett, R (2003) The search for prophet ability. FinancialManagement, June.

Barrett, R (2004) Traditional budgeting tools may not beenough. Faculty of Finance and Management of theICAEW, January.

Bourne, M, Neely, A and Heyns, H (2002) Lore reform.Financial Management, January.

Carlson, B and Palaveev, P (2004) Budget brawn. Journal ofFinancial Planning, March, vol 17 no 3.

Cassell, M (2003) Can we budge it? (beyond budgeting).Financial Management, November.

Fanning, J (2000) 21st century budgeting. Faculty of Financeand Management of the ICAEW.

Gahagan J (2003) Reaching for financial success (integratingbudgeting, planning and other systems). Strategic Finance,November, vol 85 no 5.

Gould, S (2003): Beyond budgeting: blowing up the budget.Insight, April.www.cimaglobal.com/newsletters/archives/bb.htm

Hope, J and Fraser, R (2003) Beyond budgeting: how man-agers can break free from the annual performance trap.Harvard Business School Press.

Hope, J and Fraser, R (2003) Who needs budgets. HarvardBusiness Review, February.

Howard, M (2004) Go figure. Financial Management, March.

Hunt, S W (2003) Tactical issues & best practice solutions inbudgeting. Financial Executive, December, vol 19 no 9.

ICAEW (2003) Prospective financial information – guidancefor UK directors, available as PDF at www.icaew.co.uk/bettermarkets, or printed copies from 020 7920 8634.

Jensen, M C (2003) Paying people to lie: the truth about thebudgeting process. European Financial Management,September, vol 9 no 3.

Meall L, (2003) Bye, bye budget (budgeting software).Accountancy, September, vol 132 no 1321.

Neely, A (2002) Business performance measurement.Cambridge University Press.

Neely A, Bourne M, and Adams C, (2003) Better budgetingor beyond budgeting? Measuring Business Excellence, vol 7 no 3.

Prendergast, P (2000) Budgets hit back. ManagementAccounting, January.

Prendergast, P (1997) Budget padding: is it a job for thefinance police? Management Accounting, November.

Prickett, R (2003) Beyond budgeting case study 1: the privatecompany. Financial Management, November, p24.

Smith PT, Goranson C A, and Astley M F (2003) Intranetbudgeting does the trick. Strategic Finance, May, vol 84 no 11.

Steele, R and Albright, C (2004) Games managers play atbudget time. MIT Sloan Management Review, Spring, vol 45 no 3.

Vuorinen, I (2004) The evolvement of organisational controlsystems, paper presented at the 27th Annual Congress,European Accounting Association, Prague, 1-3 April 2004.

Bibliography

© ICAEW/CIMA 2004. All rights reserved. No partof this work covered by copyright may bereproduced or copied in any form or by any means(including graphic, electronic or mechanical,photocopying recording, recorded taping or retrievalinformation systems) without written permission ofthe copyright holder. The views expressed herein arenot necessarily shared by the Council of theInstitute or by the Faculty. Articles are publishedwithout responsibility on the part of the publishersor authors for loss occasioned by any person actingor refraining from acting as a result of any viewexpressed therein.

... is produced on behalf ofCIMA and the ICAEW Faculty ofFinance and Management bySilverdart Ltd, Unit 211, LintonHouse, 164-180 Union Street,London SE1 0LH. Tel: 020 79287770; fax: 020 7928 7780;contact: Alex Murray orGabrielle Liggett

Better Budgeting

TECPLM3227

www.cimaglobal.com

The Chartered Institute of Management Accountants

26 Chapter Street London SW1P 4NP

Telephone: +44 (0)20 7663 5441

The Faculty of Finance and Management, ICAEWChartered Accountants’ Hall, PO Box 433, Moorgate Place, London EC2P 2BJ

Telephone: +44 (0)20 7920 8486

www.icaew.co.uk/fmfac