Best Practices In Investor Presentations · 3 PRESENTATION BACKGROUND •Survey conducted to gain...

53

Best Practices In Investor Presentations

Transcript of Best Practices In Investor Presentations · 3 PRESENTATION BACKGROUND •Survey conducted to gain...

Best Practices

In Investor

Presentations

PRESENTERS

2

Yvette LokkerPresident and Chief Executive Officer

CIRI

Rebecca CorbinFounder and Managing Partner

Corbin Perception

3

PRESENTATION BACKGROUND

• Survey conducted to gain better understanding of IR and

investor alignment and disconnects

‒ “IR Survey” conducted by CIRI | n = 57, IR professionals

‒ “Investor Survey” conducted by Corbin | n = 271,

investment professionals globally (ongoing research)

• Research serves to affirm best practices and uncover high-

impact areas for further capturing investor/analyst

mindshare

• Selected examples of best-in-class slides on leading topics

of interest to the investment community provided

CIRI:

IR Membership

Survey

Findings

What are the most important communication channels for getting your story

heard?

IR SURVEY FINDINGS

6

Which of the following components do you include in your presentation?

IR SURVEY FINDINGS

Top 5

Bottom 5

7

*not financial guidance

For what timeframe do you provide

quantitative targets?*

IR SURVEY FINDINGS

What quantitative targets do you

provide?

8

What do you post to the IR section of your website?

IR SURVEY FINDINGS

9

How do you notify holders when a new presentation is posted to website?

IR SURVEY FINDINGS

10

IR SURVEY FINDINGS

80% feel the deck is

understandable

as a stand-

alone

document

without the

benefit of

commentary

6% incorporate

videos into

the deck

89% develop the

deck internally

with the

remainder

collaborating

with external

consultants

Corbin:

Research-

based Insights

Not for distribution 12

The Investor Deck Is One Of The Most Important Sources Of Information

LEADING SOURCES OF INFORMATION

Investors rank deck

as important as

meeting with

management

91% indicate it is

THE leading driver to

the IR website

Not for distribution 13

Communicate The What, The How, The Why & Most Importantly….The “So What”

MOST IMPORTANT ELEMENTS IN THE INVESTOR DECK

Not for distribution 14

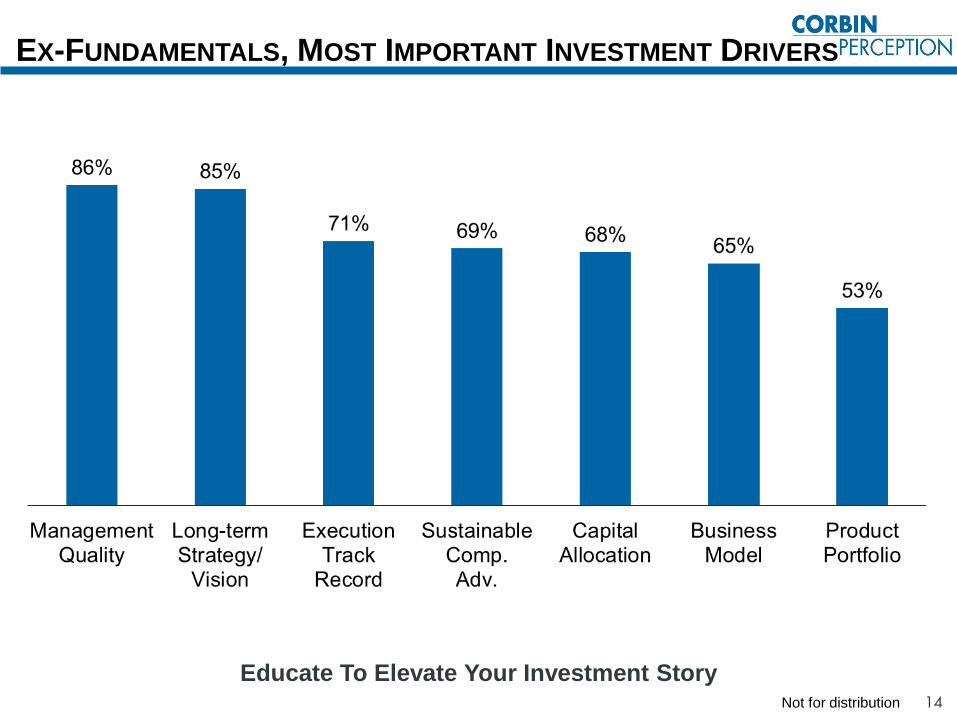

Educate To Elevate Your Investment Story

EX-FUNDAMENTALS, MOST IMPORTANT INVESTMENT DRIVERS

Strategy &

Growth

Initiatives

Not for distribution 16

DECK SHOULD HAVE A CLEARLY LABELED STRATEGY SLIDE

Not for distribution 17

CAN’T GET MUCH CLEARER THAN THIS

Not for distribution 18

PROVIDE HIGH LEVEL GOALS AND CLEAR INITIATIVES

Not for distribution 19

GREAT EXAMPLE: TRANSFORMATION & OUTCOME

Sustainable

Competitive

Differentiators

Not for distribution 21

Operational Excellence/Leading Innovation Growing Focus For Investors

MOST IMPORTANT SUSTAINABLE COMPETITIVE ADVANTAGES

Not for distribution 22

VERY CLEAR ABOUT HOW THEY ARE DIFFERENTIATED

Specific

about

what they

do not do

Not for distribution 23

CLEARLY COMMUNICATES UNIQUE APPROACH

Not for distribution 24

HIGHLIGHTS COMPETITIVE ADVANTAGES AND FOCUS

Not for distribution 25

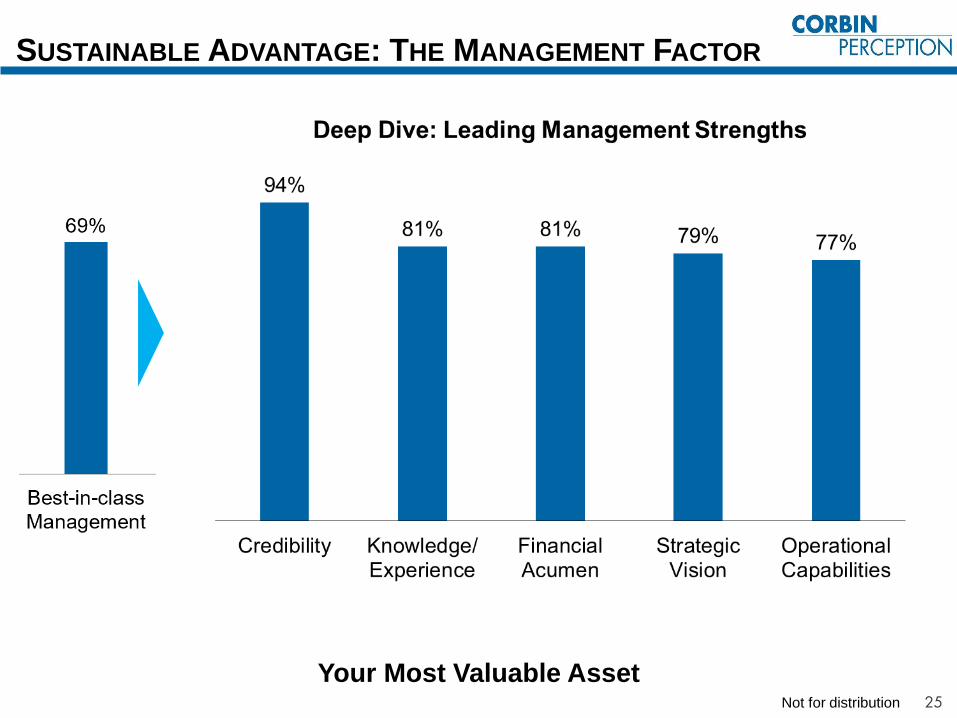

Your Most Valuable Asset

SUSTAINABLE ADVANTAGE: THE MANAGEMENT FACTOR

Not for distribution 26

CREDIBILITY-BUILDING COMMUNICATION

Don’t

See

This

Every

Day!

Not for distribution 27

A Best-in-Class Trait That Is Generally Not Well Articulated By Companies

An analysis of companies thateffectively position operational

excellence reveals:

• Business system is defined

and tangible objectives

provided

• Positioned as a sustainable

competitive differentiator

and core competency; it often

defines the culture

• Financial impact is tied to

business system

SUSTAINABLE ADVANTAGE: OPERATIONAL EXCELLENCE

PROOF POINTS

Improved working capital

turns

FCF generation, conversion

Margin outperformance

Ability to pass on cost

Top-line, organic growth

Superior M&A integration

Market share gains

Customer experience

Leadership/employee

engagement

Shareholder value delivery,

leading TSR

Not for distribution 28

FROM EXECUTING ON OPERATIONAL INITIATIVES…

Not for distribution 29

…TO CULTIVATING A CULTURE OF OUTPERFORMANCE

Not for distribution 30

CONTINUOUS IMPROVEMENT IS THE CULTURE…

Not for distribution 31

…ALWAYS EVOLVING TO DRIVE INDUSTRY-LEADING RESULTS

The next

BIG ENABLER

Not for distribution 32

ILLUSTRATING THE BUSINESS SYSTEM IMPACT

Not for distribution 33

Must Link Innovation To Financial Impact

SUSTAINABLE ADVANTAGES: LEADING INNOVATION

Not for distribution 34

INITIATIVES DRIVING ORGANIC GROWTH? CHECK!

Not for distribution 35

AND EVEN MORE POWERFUL EVIDENCE OF REINVESTMENT!

Capital

Deployment

And M&A As

Differentiators

Not for distribution 37

CAPITAL DEPLOYMENT: BEST IN CLASS ANALYSIS1

The Benefit of Transparency

• Investors appreciate details

• Increases management

credibility by enhancing

information flow with metrics

largely under management’s

control

• Demonstrates execution

track record

• Proactively addresses issues

that would otherwise create

an opening for “financial

investors” or activists

Disclosure In Action

• 72% | “Disciplined” acquisitions

• 68% | “Opportunistic” share repurchase

• 56% | “High ROI” capital expenditures

• 56% | Dividend growth

• 28% | Internal R&D

• 28% | Investment grade balance sheet

1Based on internal research on 50 of companies and selection of 25 that detailed capital allocation

Not for distribution 38

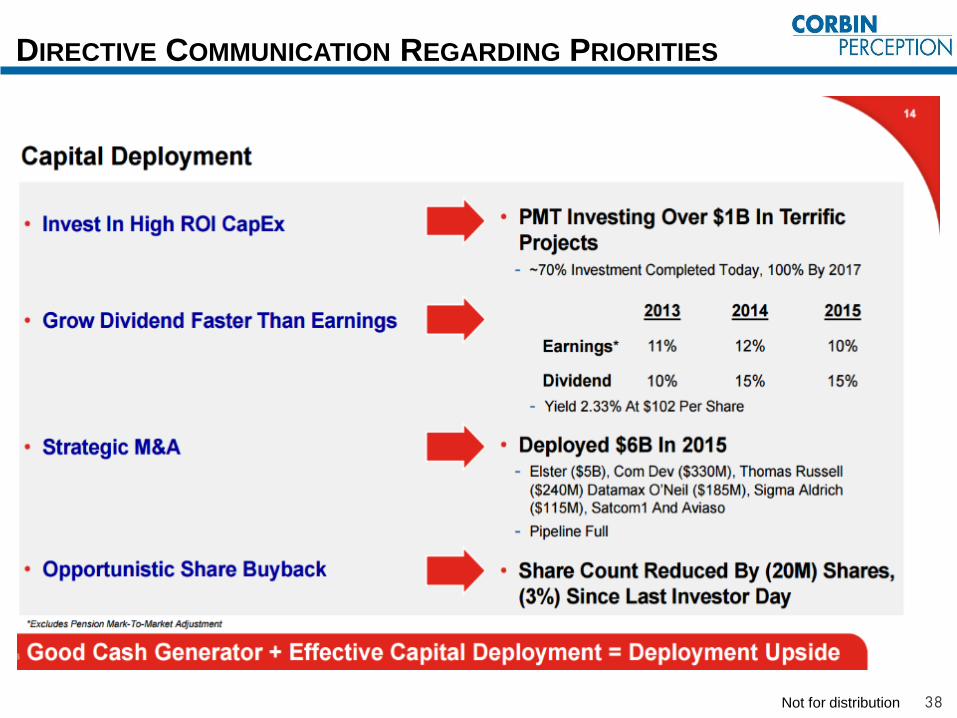

DIRECTIVE COMMUNICATION REGARDING PRIORITIES

Not for distribution 39

SPECIFIC GOALS DRIVING AT GROWTH

Not for distribution 40

SHOWCASES ALLOCATION OVER THE YEARS

Not for distribution 41

M&A: BEST IN CLASS ANALYSIS1

• Deployment of best

practices

• Cost synergies

• Sales synergies

• Leverage distribution

channel

• Leverage supply base

50% address benefits

Communicated Rationale

• 68% | Strategic fit: “Within the realm

of what we do”

• 55% | Technologies, products and

services

• 36% | Adjacent Markets

• 18% | “Good” industries

• 18% | Hold leading market share

• 14% | Where scale would add value

• 9% | Geographic expansion

1Based on internal research on 50 of companies and selection of 22 detailed M&A expectations

Not for distribution 42

M&A: BEST IN CLASS ANALYSIS1

1Based on internal research on 50 of companies and selection of 22 detailed M&A expectations

Communicated Metrics

• 41% |Accretive in Year One on:

‒ EPS

‒ EBITDA

‒ ROIC

• 18% | IRR > WACC

• 18% |Double-digit ROI

• 9% |At corporate OM or better

• Number of acquisitions over a

period(s)

• Amount allocated toward

acquisitions over a period(s)

and tied to sales growth

41% highlight track record

Not for distribution 43

REINFORCING M&A AS A STRENGTH

Not for distribution 44

COVERS ALL BASES AND THEN SOME

Not for distribution 45

TELLS THE M&A HISTORY AND A STORY

Not for distribution 46

M&A PROOF POINTS + ANOTHER EXAMPLE OF CREDIBILITY

Not for distribution

A RECOGNIZED COMPETITIVE ADVANTAGE FOR THIS COMPANY

47

Long-term Targets & Guidance

Not for distribution 49

Encourages Investors To Focus On Where You Are Going

LONG-TERM METRICS MOST IMPORTANT TO INVESTORS

58% prefer

3-year targets

Not for distribution 50

3-YEAR TARGETS, BOTH QUANTITATIVE AND QUALITATIVE

Not for distribution 51

4-YEAR TARGETS

Not for distribution 52

2020 TARGETS AND THE PATH TO ACHIEVE

Not for distribution 53

FINAL THOUGHTS: INVESTOR DECK BEST PRACTICES

Ensure one-click

access on IR

website

Some Pictures Are

Worth 1,000 Words

BUT Content Is

King

Content should be

robust enough so that

investor can follow

without the benefit of

speaker’s commentary

Send a proactive email

when important

updates are made;

point out whether they

are material or not

53% of investors report

update email prompts review

(almost immediately) – send

updates!