BEPS and the EU - Keep Calm and Carry On!

41

Private Equity Forum 11 November 2014 www.pwc.lu

-

Upload

thorsten-lederer- -

Category

Presentations & Public Speaking

-

view

321 -

download

0

Transcript of BEPS and the EU - Keep Calm and Carry On!

Private Equity Forum

11 November 2014

www.pwc.lu

PwC

BEPS and the EU – Keep Calm and Carry On!

David Roach, Tax Expert, PwC Luxembourg

2

11 November 2014 PE Forum

PwC 3

11 November 2014 PE Forum

PwC 4

11 November 2014 PE Forum

PwC

The OECD September BEPS Package

Where we now are

• Many expected “watered down” versions of earlier drafts – but most was retained

• The 16 September reports were approved by G20 Finance Ministers on 20/21 September; BUT

• None of the reports are fully final (rushed drafting still shows in places) – some quite substantial chunks of text and conclusions may need to be rewritten / adapted to be consistent with the later Action Plan outputs due in September 2015; SO

• No formal amendments to be made to OECD Model Treaty / Commentary / TP Guidelines until early 2016?

5

11 November 2014 PE Forum

PwC

The OECD September BEPS Package

New reports

Action 5 Countering Harmful Tax Practices More Effectively, Taking into Account Transparency and Substance (“Harmful Tax Practices”) (65 pages)

Action 15 Developing a Multilateral Instrument to Modify Bilateral Tax Treaties (“Multilateral Instrument”) (63 pages)

6

11 November 2014 PE Forum

PwC

The OECD September BEPS Package

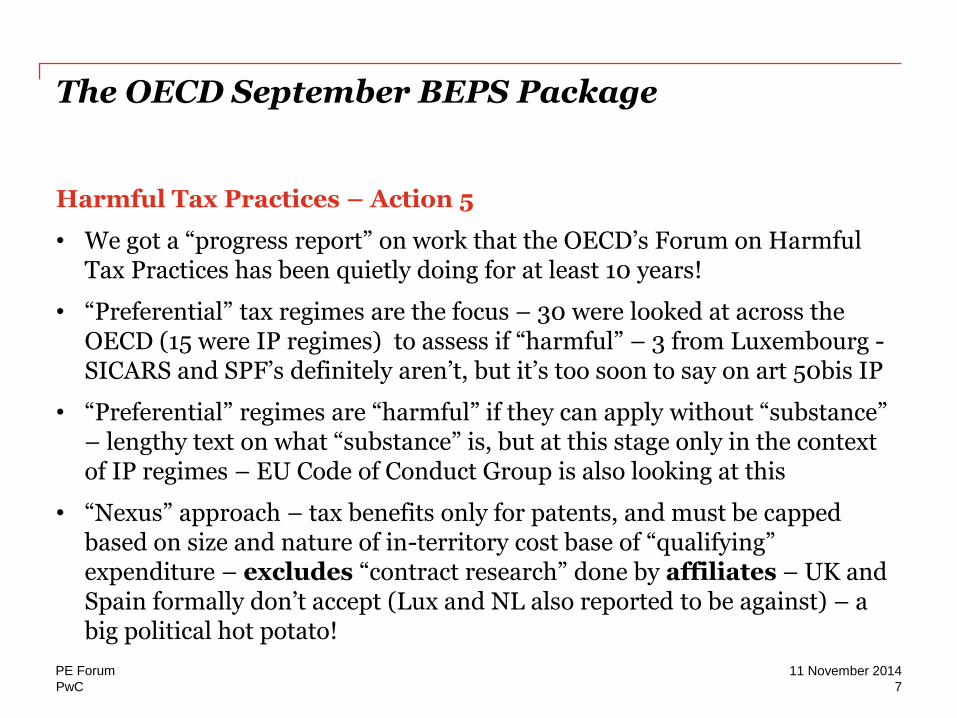

Harmful Tax Practices – Action 5

• We got a “progress report” on work that the OECD’s Forum on Harmful Tax Practices has been quietly doing for at least 10 years!

• “Preferential” tax regimes are the focus – 30 were looked at across the OECD (15 were IP regimes) to assess if “harmful” – 3 from Luxembourg -SICARS and SPF’s definitely aren’t, but it’s too soon to say on art 50bis IP

• “Preferential” regimes are “harmful” if they can apply without “substance” – lengthy text on what “substance” is, but at this stage only in the context of IP regimes – EU Code of Conduct Group is also looking at this

• “Nexus” approach – tax benefits only for patents, and must be capped based on size and nature of in-territory cost base of “qualifying” expenditure – excludes “contract research” done by affiliates – UK and Spain formally don’t accept (Lux and NL also reported to be against) – a big political hot potato!

7

11 November 2014 PE Forum

PwC

The OECD September BEPS Package

Harmful Tax Practices – Action 5 (continued)

• Big chapter on compulsory spontaneous exchange of rulings linked to any preferential regime – with ground rules designed to ensure all countries play the game consistently

• “Preferential” – any regime that deals with geographically mobile income, and results in a “no or low” effective rate of tax

• Details of the ruling given would have to be passed to the tax authorities of

- countries of counterparties affected by the arrangements; and

- countries of both direct and ultimate parents

within 3 months of ruling reaching “giving” country’s Comp. Authority

• In 2015 the OECD Forum on Harmful Tax Practices will review OECD members to see if their ruling practices are themselves “harmful” – but has the European Commission (and the media) got there first?!

8

11 November 2014 PE Forum

PwC

The OECD September BEPS Package

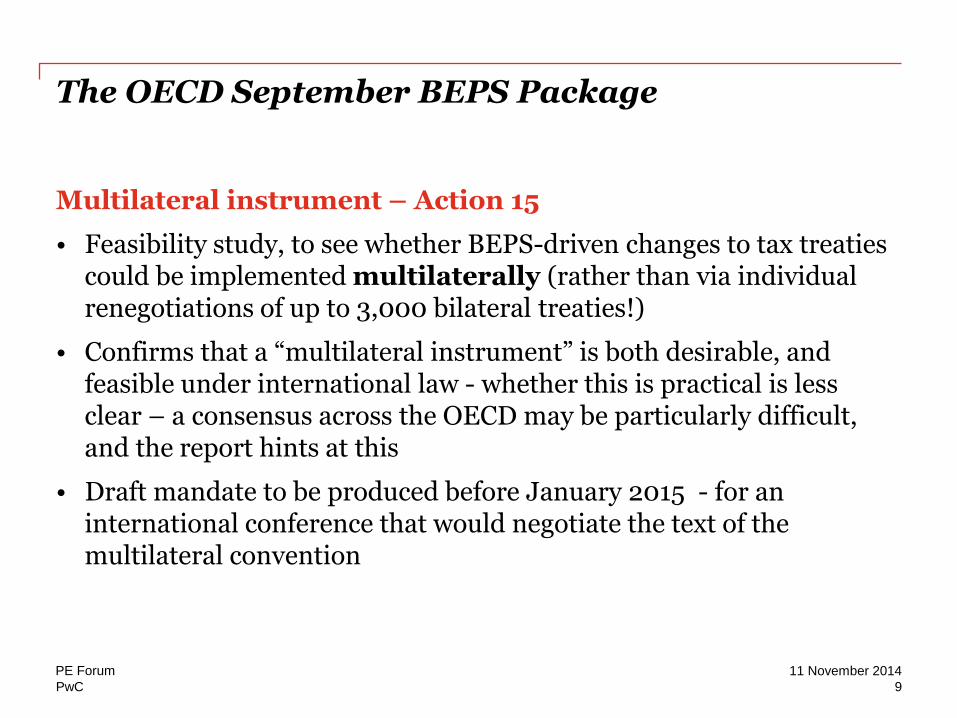

Multilateral instrument – Action 15

• Feasibility study, to see whether BEPS-driven changes to tax treaties could be implemented multilaterally (rather than via individual renegotiations of up to 3,000 bilateral treaties!)

• Confirms that a “multilateral instrument” is both desirable, and feasible under international law - whether this is practical is less clear – a consensus across the OECD may be particularly difficult, and the report hints at this

• Draft mandate to be produced before January 2015 - for an international conference that would negotiate the text of the multilateral convention

9

11 November 2014 PE Forum

PwC

The OECD September BEPS Package

“Final” versions of reports previously issued as Drafts

Action 1 Addressing the Tax Challenges of the Digital Economy (202 pages)

Action 2 Neutralise the Effects of Hybrid Mismatch Arrangements (99 pages)

Action 6 Preventing the Granting of Treaty Benefits in Inappropriate Circumstances (“Treaty Abuse”) (107 pages)

Action 8 Guidance on Transfer Pricing Aspects of Intangibles (130 pages)

Action 13 Guidance on Transfer Pricing Documentation and Country-by-Country Reporting (“CbCR”) (44 pages)

10

11 November 2014 PE Forum

PwC

The OECD September BEPS Package

Digital Economy – Action 1

• USA 1 – France 0. An early goal here by the US. No special “Google taxes” are to be recommended by the OECD

• Confirms that the “digital economy” is so widespread that it represents not a special part of the economy, but the economy itself

• Big focus on indirect taxes – endorses the EU post 1 January 2015 approach of levying indirect taxes based on where the user is

• Task Force to make sure other BEPS Actions cover “digital-centric” issues such as “artificial non-PE” arrangements

11

11 November 2014 PE Forum

PwC

The OECD September BEPS Package

Hybrid mismatches – Action 2 (1)

• Re-ordered, restructured, refined version, combining two March 2014 Discussion Drafts – 80% is recommendations for domestic rules, rest recommends changes to Model Treaty to deal with transparent entities

• Report still feels “rushed” in places – e.g. “imported hybrids” drafting – OECD accepts further refinement needed

• OECD now wants to carry on refining the rules if it sees they aren’t effective (i.e. catch anything it finds it missed!) – it has also committed to write a Commentary, with practical examples, to be published by September 2015

• “A “hybrid mismatch” arrangement is an arrangement that exploits a difference in the tax treatment of an entity or instrument under the laws of two or more tax jurisdictions to produce a mismatch in tax outcomes, where that mismatch has the effect of lowering the aggregate tax burden of the parties to the arrangement “(para 41)

12

11 November 2014 PE Forum

PwC

The OECD September BEPS Package

Hybrid mismatches – Action 2 (2)

• Overall approach recommended is for “paying country” to deny deduction, if recipient country doesn’t tax as ordinary income. If this treatment is not applied a “defensive rule” usually comes into play, and the “recipient country” must either tax income (if D/NI) (c.f. July 2014 revision of the EU Parent/Subsidiary Directive), or deny the deduction (if DD)

• No “motive” test – just look at the outcome

• Must involve payments – mismatches in the value of a payment (e.g. forex) are not in scope

• Deemed payments are not in scope – nor are mismatches caused by deemed interest deductions for equity capital (e.g. NIDs)

• Cross-border mismatches caused by reasons such as payments of interest to a tax-exempt entity (e.g. FCP/SICAV, pension fund, or simply in a tax-neutral jurisdiction) are not in scope – only those that rely on a hybrid element to produce D/NI or DD outcomes are in scope

13

11 November 2014 PE Forum

PwC

The OECD September BEPS Package

LuxCo

A Co

Hybrid financing

Income flow

Country A

Luxembourg

Not included – because a “hybrid”

Deductible

Luxembourg

Country C

C Co

Normal loan

Deductible – but denied, because not included by A Co

Taxable

LuxCo offsets deduction against income

Interest

Hybrid mismatches – Action 2 (3)

• Complex “imported mismatch” rules may mean that PPL/CPEC/equivalent financing of Luxembourg platforms may have to be re-examined, IF Country Cs legislate

14

11 November 2014 PE Forum

PwC

The OECD September BEPS Package

Treaty abuse (1)

• Maintains the far-reaching and extreme approach of the March 2014 draft – still sees any inclusion of any intermediate country in an income flow as “treaty shopping” – OECD has “gone nuclear”

• New Model Treaty clause still to be introduced – containing either / both

- Very restrictive US-style “limitation-on-benefits” (“LoB”) rules, so only “qualified persons” (e.g. quoted companies, their “same state” subsidiaries, individuals) could access treaties; limited let-outs for “active trade or business” flows. (Sept 2014 – recognition that some types of CIV can be “qualified persons” (but drafting still outstanding); “derivative benefits” or “equivalent beneficiary” rules introduced) ; and / or

- A “principal purposes” test, for denial of benefits (i.e. no treaty benefits, if one of the principal purposes of an arrangement was trying to get treaty benefits) – i.e. a general anti-avoidance rule (“GAAR”)

• A “minimum level of protection” is now to be needed – so long as this is achieved (e.g. an LoB, plus a “principal purposes” test that deals specifically with “conduit” lending) then there is more scope to work within EU law?

15

11 November 2014 PE Forum

PwC

The OECD September BEPS Package

Treaty abuse (2)

• EU Commission efforts to put a GAAR into the P/S Directive are continuing actively under the Italian Presidency – compromise text nearly agreed (ECOFIN Council Press Release 7 Nov)

• Will be a common EU minimum requirement – Member States can still be stricter

• Amendment will require Member States “to refrain from granting the benefits of the Directive to an arrangement, or series of arrangements, that are not ‘genuine’ and have been put in place to obtain a tax advantage, rather than for valid commercial reasons reflecting economic reality”

• The BEPS pressure for substance is, albeit indirectly, becoming reality

16

11 November 2014 PE Forum

PwC

The OECD September BEPS Package

Country-by-Country Reporting / TP documentation

• OECD TP Guidelines are to require all MNE groups to prepare and maintain contemporaneous TP documentation, in the form of a group “master file” and “local files”, each with OECD-specified detailed content. There must also be country-by-country reports (“CbCRs”) of outcomes

• CbCRs are to follow an OECD template, and show – on a per country basis – revenues (related party and unrelated party), profits before tax, taxes accrued and cash tax paid, as well as “economic indicators” including total tangible non-cash assets, and employee numbers (but much less info than called for in January 2014 draft)

• How this CbCR data is to be shared between tax authorities (automatic exchange, or exchange on request?) has yet to be decided – OECD wants this and confidentiality issues sorted out by January 2015

• Many countries keen to implement – UK says it has already done so! Will certainly allow tax authorities much more visibility of “profits but little substance”

17

11 November 2014 PE Forum

PwC

The OECD – since September and to come?

More Discussion Draft Reports

30 October Action 7 – PE Status (25 pages)

3 November Action 10 – Low value adding services (intra-group service charges) (31 pages)

mid-November

Action 6 – Preventing the Granting of Treaty Benefits in Inappropriate Circumstances (“Treaty Abuse”) (further draft on CIVs)

mid-December

Action 4 – Interest Deductions

18

11 November 2014 PE Forum

PwC 19

11 November 2014 PE Forum

PwC 20

11 November 2014 PE Forum

PwC

The EU strikes – FIAT

What did Fiat do?

• FIAT Finance and Trade (“FFT”) was a finance company – but, less usually, much of its borrowing was from third parties, and it also had a much more significant equity base than usual

• FFT operated fully in line with the January 2011 Circular LIR 164/2 on transfer pricing, and in March 2012 submitted an APA, supported by a detailed TP report prepared by KPMG – the APA was granted in September 2012

• The TP report uses CAPM and the TNMM methodology to set a benchmark level of reward for the functions FFT carried out and the risk FFT bore on the equity attributed to the financing activity. This reward was defined in the form of a set figure for pre-tax profit, being the mid-point of a range – rather than the more normal “bps on principal being financed” approach

21

11 November 2014 PE Forum

PwC

The EU strikes – FIAT

What has the EU done? (1)

• March 2014 – European Commission had asked Luxembourg Government for information – to see if tax practices (rulings, and IP regime) breached State aid rules – Luxembourg refused to respond fully, so the Commission sought an injunction forcing delivery

• April 2014 – Luxembourg confirms its view that the Commission was undertaking an illegal “fishing expedition”, and takes its case to CJEU

• 11 June 2014 – Commission announces that it has opened in-depth State Aid investigations into transfer pricing rulings granted by the tax authorities to Apple (in Ireland), Starbucks (in Netherlands), and FFT (in Luxembourg) – and confirms that it is continuing an inquiry into tax rulings in more Member States. It emerges that the Commission was able to identify FFT, despite efforts by Luxembourg to ensure that all material provided to the Commission was anonymised

22

11 November 2014 PE Forum

PwC

The EU strikes – FIAT

What has the EU done? (2)

• 12 June 2014 – Luxembourg MoF issues press release confirming that it has serious doubts about the legality of the requests, and that it is confident that it has not granted any illegal State aid

• 30 September 2014 – Commission publishes on its website the 33 page letter (reproducing significant parts of the KPMG TP report prepared for FFT) it had sent to the Luxembourg Government in June 2014 setting out why it decided to initiate State aid procedures, giving its preliminary view that State aid had been given, because flaws in the CAPM-based benchmarking that the Luxembourg Tax Authorities had accepted resulted in too little profit, and too fixed an amount, being taxed

23

11 November 2014 PE Forum

PwC 24

11 November 2014 PE Forum

PwC 25

11 November 2014 PE Forum

PwC

The EU strikes again – Amazon

What has the EU done?

• 4 July 2014 – FT publishes a report that the Commission had made a State aid-related information request to Luxembourg regarding Amazon

• August 2014 – Luxembourg provides Commission with information

• 7 October 2014 – Commission issues press release confirming that it has opened an in-depth investigation into an ATA that Amazon EU Sàrl made in 2003, concerning royalties payable to a Luxembourg SCS. The ATA set out the way in which the royalties were to be calculated. The Commission says that it considers that this has resulted in royalties in excess of arm’s length amounts being paid and tax-deducted, and hence tax is being underpaid, with the “missing” amount of tax being State aid

26

11 November 2014 PE Forum

PwC 27

11 November 2014 PE Forum

PwC

Keep Calm and Carry On

State aid challenges

• Use of State aid investigations to challenge perceived tax avoidance is a new and drastic development – and “scary” because (at least in theory) companies could be made to “repay” as extra tax all the State aid they are found to have received over the last 10 years

• Wider implications?

- FIAT situation is broadly (but not really) similar to very many other “financing activity” structures that have sought or got APAs following the TP Circular – understandable if fund managers might be concerned

- The Commission position in both the FIAT and Amazon cases relies entirely on the argument that the TP used was wrong – but TP is an “inexact science” (per OECD TP Guidelines). The risk of State aid penalties in such a subjective area is worrying

- APAs and ATAs become of much less value – and harder to get

- A lengthy period of uncertainty, especially if it goes to CJEU

28

11 November 2014 PE Forum

PwC

Keep Calm and Carry On

State aid challenges – BUT (1)

• Despite the way the press has presented things, nobody has yet decided that there has been State aid – it has just been decided that there should be an investigation

• Big picture – this is probably all deeply politically motivated

• Some Member States have clear concerns over the implications the Commission’s action brings for erosion of their country’s fiscal sovereignty – or how the Commission has acted in a high-handed way in dealing with Luxembourg’s concerns over taxpayer confidentiality

• US “diplomacy” and US political forces will rally round the big US MNEs – this may well become an issue in wider US / EU relations

• What message does this send about inward investment into EU – compared with places like Singapore?

• Luxembourg will not concede readily. Nor IRL or NL?? (But IRL has acted to end the “Double Irish” – what will others now have to do? Luxembourg last month acted to update its TP regime, and make ATA/APA’s more transparent)

29

11 November 2014 PE Forum

PwC

Keep Calm and Carry On

State aid challenges – BUT (2)

• The Commission so far seem not to have shown great expertise in grasping difficult TP issues – and already in places reasoning looks to be driven by the need for the politically-desired answer. Particularly in cases like Amazon, the Commission will now face highly-skilled resistance from the MNE with support from the tax advisers that did the original TP work – how would the Commission get on at CJEU?

• How wrong can the FFT APA actually have been? The correct arm’s length spread cannot be many EUR mi different from the agreed one – when will the Commission see that here, they are fighting over something where the outcome is very likely to be “you were near enough, so we can’t be sure there was any State aid”?

• FFT followed the TP Circular, which Luxembourg had only recently adopted under EU Code of Conduct Group pressure – this prior involvement by the EU (albeit a different unit) may both cosmetically and legally weaken the Commission’s position

30

11 November 2014 PE Forum

PwC

Keep Calm and Carry On

State aid challenges – BUT (3)

• Luxembourg MoF position - “Luxembourg is confident that the allegations of State aid in this case are unsubstantiated and that the Commission investigation will conclude that no special tax treatment or advantage has been awarded…”

• Even if the matter does end up at the CJEU and the Commission’s position is upheld (unlikely), it is even more unlikely that the harshest sanctions would be imposed – meaning that the risk of taxpayers facing any retrospective tax liabilities is at worst remote

• The Luxembourg APA and ATA processes are not themselves State aid - the Commission has confirmed this

• Despite FFT, there is no fundamental challenge to the validity of the TP Circular, or how advisers benchmark the arm’s length spread

• No APAs or ATAs have become invalid, and no ATA or APA should automatically cause anyone to have had illegal State aid

31

11 November 2014 PE Forum

PwC 32

11 November 2014 PE Forum

PwC 33

11 November 2014 PE Forum

PwC

Keep Calm and Carry On

BEPS

• Media focus on tax planning by major corporates (Apple, Google, etc.), and the role of Luxembourg, Ireland etc., isn’t going to go away – we just have to deal with it, and recognise that “LuxLeaks” and similar stigmatisation may put some businesses off (but Luxembourg is doing, and will continue to do, all it can – e.g. on transparency – to protect its “brand”)

• Political momentum for change and more transparency, and public perception that there is now a “moral obligation” for businesses to pay their “fair share”, will also endure

• Countries such as France and Italy will remain ardent BEPS supporters – and Germany will want to keep parity between local businesses/mittelstand and MNEs operating in Germany. BEPS will “happen” most, and mostly, in mainland Europe

• Some BEPS projects – e.g. CbCR, and spontaneous exchange of rulings between fiscs – will “happen” over the next 2 to 3 years, and will definitely help tax authorities in deciding which structures are best to challenge

34

11 November 2014 PE Forum

PwC

Keep Calm and Carry On

BEPS – BUT… (1)

• Significant changes to the US tax system, like removing the incentive to keep earnings offshore, or deterring hybrids (e.g. by abolishing the “check the box” rules) will simply not happen, meaning that US MNEs will push hard to keep the wider international tax system “as is”

• The US believes it is already pretty BEPS-compliant – and will increasingly see BEPS as simply an excuse for “foreign countries [to] raid the American Treasury”. “Failure is an option, for the US”

• Despite much effort, and the strongest support for BEPS being within the EU, the European Commission will struggle to achieve the Member State unanimity needed to make any major BEPS-driven changes to Tax Directives – e.g. the latest attempt at the GAAR in the P/S Directive is a compromise – the State aid issue may have “poisoned the well” for a while?

35

11 November 2014 PE Forum

PwC

Keep Calm and Carry On

BEPS – BUT… (2)

• Most BEPS change will come “bottom up” – i.e. unilateral, but BEPS-encouraged, action by individual countries – more anti-abuse rules, domestic implementation of the OECD “hybrids” recommendations, new “interest capping” rules following the 2015 OECD Action Plan 4 deliverable, etc. So while life will get harder, there will still be “mismatches”, and so opportunities will remain

• The OECD’s worst fears may even come true – unilateral actions resulting in double or multiple taxation of cross-border investment, or part-adoption creating a highly distorted tax system. It would then be the tax advisers’ task to secure as little as single taxation!

• As some countries adopt BEPS measures, those that don’t will become more attractive for MNEs – delay will bid up competitive advantage

36

11 November 2014 PE Forum

PwC

Keep Calm and Carry On

BEPS – BUT… (3)

• Countries face an enormous “incentive incompatibility” between adopting BEPS and staying in the tax competition for mobile income. Result - tax competition will trump BEPS – the UK’s position on “patent boxes” is a good early example?

• The OECD has done well to secure as much consensus as it has done to date – but can this continue? Already there are suggestions that the “multilateral instrument” may be feasible in theory but impossible to implement in practice

• A full implementation of the whole BEPS menu – the renegotiation of all treaties to adopt the revised Model Convention (with new LoB and PPT rules), internationally consistent CFC rules, and changes to domestic laws on a consistent and simultaneous basis – feels far from likely

37

11 November 2014 PE Forum

PwC 38

11 November 2014 PE Forum

PwC

Keep Calm and Carry On

BEPS – BUT… (4)

• At some point the G20 politicians (other than some on the Left) will realise that the BEPS battle cannot truly be won, and do an “Iraq 2003” by declaring victory and moving on

• Businesses will always need to continue to mitigate tax costs and protect “earnings per share” or “rate of return to fund owners” – thinking about how much tax is being paid cannot and will not stop!

• But the “fallout ” from BEPS – notably the EU moves to add a GAAR to the P/S Directive (“a tax advantage, rather than for valid commercial reasons reflecting economic reality”) will push many businesses much further towards a model where their management structure matches their holding/financing structure – the “substance” war of attrition will slowly be won by the tax authorities

39

11 November 2014 PE Forum

PwC 40

11 November 2014 PE Forum

Questions?

This publication has been prepared for general guidance on matters of interest only, and does not

constitute professional advice. You should not act upon the information contained in this

publication without obtaining specific professional advice. No representation or warranty (express

or implied) is given as to the accuracy or completeness of the information contained in this

publication, and, to the extent permitted by law, PricewaterhouseCoopers Société Coopérative, its

members, employees and agents do not accept or assume any liability, responsibility or duty of

care for any consequences of you or anyone else acting, or refraining to act, in reliance on the

information contained in this publication or for any decision based on it.

© 2014 PricewaterhouseCoopers Société Coopérative. All rights reserved. In this document,

“PwC” refers to PricewaterhouseCoopers Société Coopérative, which is a member firm of

PricewaterhouseCoopers International Limited, each member firm of which is a separate legal

entity.