Benue State Government of Nigeria

19

The copyright of this document is reserved by Agusto & Co. Limited. No matter contained herein may be reproduced, duplicated or copied by any means whatsoever without the prior written consent of Agusto & Co. Limited. Action will be taken against companies or individuals who ignore this warning. The information contained in this document has been obtained from published financial statements and other sources which we consider to be reliable but do not guarantee as such. The opinions expressed in this document do not represent investment or other advice and should therefore not be construed as such. The circulation of this document is restricted to whom it has been addressed. Any unauthorized disclosure or use of the information contained herein is prohibited. Agusto & Co. RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT 2014 Municipal Bond Rating: Benue State Government Benue State Government of Nigeria ₦4.95 billion 16.5% Seven Year Fixed Rate Bond Issue Rating: Bbb+ Satisfactory quality debt issue with moderate credit risk; adequate capacity to pay returns and principal on local currency debt in a timely manner. Benue State: Bb- Outlook: Stable Issue Date: 9 February 2015 Expiry Date: The rating is valid throughout the life of the instrument but will be subject to annual monitoring and review. INSIDE THIS REPORT Rationale 1 Country Profile 3 Issuer Profile 6 The Issue 9 Financial Condition 10 Financial Forecast 13 Outlook 15 Financial Summary 16 Rating Definition 18 Analysts: Ikechukwu Iheagwam [email protected] Isaac Babatunde [email protected] Agusto & Co. Limited UBA House (5th Floor) 57, Marina Lagos Nigeria www.agusto.com RATING RATIONALE Agusto & Co. hereby affirms the „Bb-‟ rating of the Benue State Government (―the State‖, ―the Issuer‖ or ―Benue‖). The Issuer‘s rating is supported by its moderate leverage and high financial flexibility. The rating is however tempered by the State‘s low level of internally generated revenue (IGR), high personnel cost of the Ministries Departments and Agencies (MDAs) and over dependence on statutory allocation as evidenced by a five year average statutory allocation to revenue ratio of 74%. Benue State continues to rely overly on statutory allocation and this exposes the Issuer‘s revenue to adverse movements in crude oil production and prices – a recurrent problem of many states in the Country. Benue State intends to issue a ₦4.95 billion Seven-Year Fixed Rate Bond (―the Issue‖ or ―the Bond‖) to upgrade existing water works, complete rural electrification projects and construct & rehabilitate over 207 km roads in the State. The Bond will be backed by the approval of an Irrevocable Standing Payment Order (ISPO) authorizing monthly deductions of ₦103.8 million from the State‘s statutory allocation over the tenor of the Bond into a Sinking Fund Account (SFA) to cover the entire Bond obligations. In our opinion, the Issue has low credit risk given that the ISPO will ensure coupon and principal are paid as and when due. Following the decline in crude oil prices over the last four months, Agusto & Co. has stressed the Issuer‘s revenue and expenditure projections over the life of the Bond to reflect prevailing economic realities. When the ₦4.95 billion Bond is issued, total ISPO deductions will represent 13% of Benue‘s projected statutory allocation in 2015 which we consider to be satisfactory. The State‘s IGR, which we consider to be more reliable, will only account for just about 25% of revenue in 2015.

Transcript of Benue State Government of Nigeria

The copyright of this document is reserved by Agusto & Co. Limited. No matter contained herein may be reproduced, duplicated or copied by any means whatsoever without the prior written consent of Agusto & Co. Limited. Action will be taken against companies or individuals who ignore this warning. The information contained in this document has been obtained from published financial statements and other sources which we consider to be reliable but do not guarantee as such. The opinions expressed in this document do not represent investment or other advice and should therefore not be construed as such. The circulation of this document is restricted to whom it has been addressed. Any unauthorized disclosure or use of the information contained herein is prohibited.

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT 2014 Municipal Bond Rating: Benue State Government

Benue State Government of Nigeria ₦4.95 billion 16.5% Seven Year Fixed Rate Bond

Issue Rating:

Bbb+

Satisfactory quality debt issue with moderate credit risk; adequate

capacity to pay returns and principal on local currency debt in a timely

manner.

Benue State: Bb-

Outlook: Stable

Issue Date: 9 February 2015

Expiry Date:

The rating is valid throughout the life of the

instrument but will be subject to annual

monitoring and review.

INSIDE THIS REPORT

Rationale 1

Country Profile 3

Issuer Profile 6

The Issue 9

Financial Condition 10

Financial Forecast 13

Outlook 15

Financial Summary 16

Rating Definition 18

Analysts:

Ikechukwu Iheagwam

Isaac Babatunde

Agusto & Co. Limited

UBA House (5th Floor)

57, Marina

Lagos

Nigeria

www.agusto.com

RATING RATIONALE Agusto & Co. hereby affirms the „Bb-‟ rating of the Benue State

Government (―the State‖, ―the Issuer‖ or ―Benue‖). The Issuer‘s rating is

supported by its moderate leverage and high financial flexibility. The

rating is however tempered by the State‘s low level of internally

generated revenue (IGR), high personnel cost of the Ministries

Departments and Agencies (MDAs) and over dependence on statutory

allocation as evidenced by a five year average statutory allocation to

revenue ratio of 74%. Benue State continues to rely overly on statutory

allocation and this exposes the Issuer‘s revenue to adverse movements in

crude oil production and prices – a recurrent problem of many states in

the Country.

Benue State intends to issue a ₦4.95 billion Seven-Year Fixed Rate Bond

(―the Issue‖ or ―the Bond‖) to upgrade existing water works, complete

rural electrification projects and construct & rehabilitate over 207 km

roads in the State. The Bond will be backed by the approval of an

Irrevocable Standing Payment Order (ISPO) authorizing monthly

deductions of ₦103.8 million from the State‘s statutory allocation over the

tenor of the Bond into a Sinking Fund Account (SFA) to cover the entire

Bond obligations. In our opinion, the Issue has low credit risk given that

the ISPO will ensure coupon and principal are paid as and when due.

Following the decline in crude oil prices over the last four months, Agusto

& Co. has stressed the Issuer‘s revenue and expenditure projections over

the life of the Bond to reflect prevailing economic realities. When the

₦4.95 billion Bond is issued, total ISPO deductions will represent 13% of

Benue‘s projected statutory allocation in 2015 which we consider to be

satisfactory. The State‘s IGR, which we consider to be more reliable, will

only account for just about 25% of revenue in 2015.

2 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

Agusto & Co will continue to monitor the decline in crude oil prices and

its effect on Benue State‘s revenue. Based on the adjusted revenue &

expenditure projections over the life of the Bond, the total interest cover

ratio and total debt coverage ratio at 7 times and 3 times respectively are

satisfactory. We believe these ratios reflect satisfactory financial capacity

to meet Bond obligations.

Based on the aforementioned, Agusto & Co. has reviewed the rating of

Benue State‘s ₦4.95 billion Seven-Year Fixed Rate Bond to “Bbb+” and

has also attached a stable outlook to the Issue.

Figure 1: Strengths and Weaknesses

•High financial flexibility

•Moderate leverage

•Political stability

Strengths

•Overdependence on statutory allocation

•High personnel cost

•Low internally generated revenue

Weaknesses

•Curtailing expenses on account of declining oil prices

Challenge

3 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

THE COUNTRY

The Federal Republic of Nigeria (‗Nigeria‘, ‗the Nation‘, or ‗the

Country‘) is located along the West African coastline. Nigeria is

bordered in the west by the Republic of Benin, in the east by

Chad and Cameroon, in the north by the Niger Republic, and

the Gulf of Guinea in the south. The Country is divided into 36

states and the Federal Capital Territory (FCT), and further sub-

divided into 774 Local Government Areas (LGAs). There are

over 250 native languages in Nigeria with the three major

languages being Hausa, Igbo and Yoruba. Nigeria has

population of over 160 million people, making it the most

populous country in Africa.

Prior to 2014, the Nigerian economy was considered to be driven by agriculture with strong oil & gas

presence. The Country is renowned globally for oil production and is currently ranked as the thirteenth

largest oil producer, while agriculture is the largest employer of labour. The Country‘s 2013 gross

domestic product (GDP) was rebased to US$ 510 billion in April 2014, signifying a growth of 89% from the

previous year (pre-rebased figures) and is now considered the largest in Africa. Nonetheless, Nigeria‘s

estimated GDP per capita of US$3,010 is lower than South Africa‘s US$6,618 but higher than Ghana‘s

US$1,850. Following the rebasing, services sector was revealed as the largest contributor to GDP,

accounting for 52%, while agriculture and oil & gas accounted for 22% and 14% respectively. According

to the National Bureau of Statistics (NBS), Nigeria‘s rebased GDP grew by 7.41% in 2013 compared with

5.09% and 6.66% recorded in 2011 and 2012 respectively. The Nigerian economy continues to record

moderate growth despite inadequate infrastructure, rising insecurity, corruption and poor governance.

Due to lax non-oil tax administration, oil receipt (crude oil sales, oil taxes and royalties) remains the

Country‘s major source of revenue. Other sources of revenue include company income tax (CIT); royalties

and rents; custom and excise duties and Value Added Tax (VAT).

Available data from the Central Bank of Nigeria (CBN) reveals total federally-collected revenue in 2013

amounted to ₦9,748 billion, representing a decline of 7% from the prior year. The decline was attributable

to a 16% drop in oil revenue, which masked some improvement in non-oil revenue. Gross oil receipts

constituted 70% of total federally-collected revenue, while non-oil income represented the balance (30%).

After deducting statutory transfers, the balance of federally-collected revenue is transferred to the

Federation Account for distribution among the three tiers of government and the 13% Derivation Fund.

About 27% of the funds in the federation account is distributed amongst the states as statutory allocation

on a monthly basis.

4 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

Statutory allocation refers to monthly remittances from the

Federation Account to the three tiers of government.

Sources of statutory allocation comprise Customs & Excise

duties, Companies Income Tax and Oil Revenue. Statutory

allocation also includes share of the Excess Crude Account,

which was established in 2004 to act as a budgetary buffer

against oil price volatility. In addition, states also receive

revenue allocations from the Federal Government‘s

Subsidy Re-investment and Empowerment Programme

(SURE-P), which was established in 2012 to terminate in

2015.

Source: Central Bank of Nigeria

Source: Institute of International Finance

On 21 May 2014, the President of Federal Republic of Nigeria signed the 2014 budget. The ₦4.96 trillion

expenditure budget, which was 1.52% lower than prior year (2013: ₦4.98 trillion), was predicated on the

assumptions of average exchange rate of N160/$, projected oil production level of 2.39 million barrels per

day, benchmark oil price of US$ 77.5/barrel and estimated GDP growth of 6.75%. The 2014 aggregate

expenditure comprises ₦1.10 trillion for capital expenditure, ₦2.43 trillion for recurrent expenditure,

₦399.7 billion for statutory transfers, ₦712 billion for debt service and ₦268.4 billion for SURE-P.

The Monetary Policy Committee (MPC) of the Central Bank of Nigeria (CBN) agreed to continue its

contractionary policy stance in its September 2014 meeting. Consequently, the benchmark interest rate

(Monetary Policy Rate) of 12% was maintained with a corridor of +/-2%. In addition, the MPC retained

public sector cash reserve requirement at 75% as well as private sector cash reserve requirement at 15%.

Figure 2: Gross Federation Account Revenue

(₦‟billion)

Figure 3: Revenue Sharing Arrangement for Federation Account and VAT Pool

5 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

As at close of 2013, the apex bank‘s focus on stability and tight monetary policy continued, leading to

relative stability of the Naira against the US dollar (USD) closing at ₦157.29/US$ in the official market.

However, in the inter-bank market the Naira depreciated by 2.43% to close at ₦159.90/US$ and the

Bureau de Change segment recorded further depreciation in the Naira of 7.84% to close at ₦172.00/US$.

In August 2014, the CBN continued to maintain the exchange rate at the RDAS-SPT at ₦157.29/US$, but

the naira depreciated at the interbank and substantially at the BDC segment. As at the same date, the

interbank foreign exchange market closed at ₦162.40/US$, representing a 0.20% depreciation, while the

BDC segment depreciated by 1.2% to close at ₦169/US$.

Table 1: Budget Breakdown (2013 -2014)

2013 2014

Revenue (₦‘trn) 4.10 3.73

Aggregate Expenditure (₦‘trn) 4.99 4.96

Recurrent Expenditure (₦‘trn) 2.40 2.43

Capital Expenditure (₦‘trn) 1.588 1.119

Fiscal Deficit (% of GDP) 1.85 1.46

Oil Production (mbpd) 2.53 2.39

Oil Price ($‘pb) 79 77.5

Exchange Rate (₦/$) 160 160

In June 2014, the new Governor of the CBN, Mr. Godwin Emefiele, the erstwhile Managing Director of

Zenith Bank Plc, resumed at the apex Bank. The new Governor has over 26 years of experience in finance

and banking.

As at 17 September 2014, the County‘s gross external reserves stood at US$40.7 billion, which was

sufficient to provide cover for 7 months of imports. This is well above the internationally recommended

benchmark of 3 months.

According to the Nigerian Bureau of Statistics, inflation rate in the Country increased to 8.5% in August

2014 from 8.3% in July 2014, largely on account of higher food prices. We expect the run-up to elections

in 2015 to be accompanied by increased spending, which will exert some inflationary pressure on the

economy. Therefore, we believe the CBN‘s tight monetary policy stance will be maintained in the short

term to curb inflation.

In our opinion, improvement to security and infrastructure will help position Nigeria for foreign inflow of

investment. In addition, a level playing field for the upcoming general elections will provide veritable

support for credible elections in the future, which will translate to a better Nigeria.

6 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

THE ISSUER—BENUE STATE

Benue State (‗the State‘, ‗the Issuer‘, or ‗Benue‘) was created in 1976

and is located in the middle belt region of Nigeria with its capital in

Makurdi. The State shares boundaries with Nasarawa to the north,

Taraba to the east, Cross river to the south, Enugu to the southwest

and Kogi to the west. It also shares a boundary with the Republic of

Cameroun on the south east. Benue occupies a land mass of

approximately 33,955 square kilometers making it the eleventh

largest in the Country by landmass. Benue State also known as the

nation‘s food basket, lies within the lower river Benue and its

vegetation is conducive for farming, fishing and animal husbandry.

The major occupation of the indigenes of Benue is agriculture which is supported by its commercial

production of yams, rice, beans, cassava, potatoes, maize, soya beans, sorghum, millet and cocoyam. In

addition to its wide array of prominent crops grown commercially, the State has large deposits of

limestone and kaolinite which are commercially exploited too.

The State has an estimated population of 4.7 million people with Tiv, Idoma and Igede being the

dominant ethnic groups. Prominent cities in the State besides the capital include Gboko, Otukpo, Kastina-

Ala and Adikpo. Similar to other states in the Country, the official language is English, while the

predominant native languages are Tiv and Idoma. Benue has twenty three local government areas

administered by local government councils run by elected Chairmen. The State has an estimated

unemployment rate of 14.2%, which is lower than the National average unemployment rate of 25.7%.

Benue has a host of educational institutions including the Federal University of Agriculture, Makurdi;

Benue State University, Makurdi; University of Mkar, Mkar; Benue State Polytechnic, Ugbokolo; Fidei

Polytechnic, Gboko; Akperan Orshi College of Agriculture, Yandev; Federal College of Education, Agasha;

College of Education, Oju and College of Education, Kastina-Ala. The State‘s has a vibrant youthful

population with an English literacy rate of 84.7% (National: 76.3%).

The National Bureau of Statistics estimates that there are over 1,206 healthcare centers in the State which

reveals an average of 24 heath care facilities per 100,000 persons. Benue has a high HIV prevalence rate of

12.7% when compared to the national average of 4.1%.

Benue State has a rich and diverse culture with prominent masquerades and traditional dances, which it

showcases as part of its tourist attractions during festivals and celebrations.

7 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

POLITICAL STRUCTURE

Benue State has three arms of government namely; the Judiciary, the Legislature and the Executive which

are empowered by the constitution of the Federal Republic of Nigeria.

The Judiciary

The Chief Law Officer of the State is Barr. Adum Ter Alex, the Attorney General and Commissioner for

Justice. The State‘s judiciary is made up of the State High courts, the Magistrate Courts and Customary

Courts. Honorable Justice Iorhemen Hwande is the Chief Judge of Benue State.

The Legislature

The Benue State House of Assembly (―the House‖) is empowered by the Constitution to legislate on

matters relating to good governance of the State. The legislative powers of the State are vested in the

House of Assembly which comprises 28 legislators. The House of Assembly is headed by the Speaker,

Hon. Terseer Tsumba.

The Executive

The State Government is led by the Executive Governor, who is assisted by 19 members of the Executive

Council responsible for daily administration.

His Excellency, Hon. Dr. Gabriel Torwua Suswam is the Executive Governor of Benue State. Gabriel

Suswam obtained the LL.B (Hons) degree from the University of Lagos and proceeded to the Nigerian Law

School, Lagos, after which he was called to bar in 1991.

Dr. Suswam holds a Masters of Public Administration degree from the University of Abuja, a Master of Law

(LLM) degree and PhD in Law from the University of Jos. He has also attended various certificate courses

in management at Duke University, Harvard University, Kennedy School of Government, among others.

His professional working career started as a junior counsel in the corporate firm of Tokode & Company

between 1991 and 1994. He later formed his own legal firm, Tingir & Associates in 1994, which

metamorphosed into a corporate legal outfit based in Abuja. In 1999, Hon Suswam was elected into the

Federal House of Representatives to represent the K/Ala/Ukum/Logo federal constituency. He was

thereafter re-elected in 2003 and chaired several committees including members‘ welfare, appropriations

and power.

Hon. Suswam was elected as the executive Governor of Benue State in 2007 for a term of four years.

Subsequently, he was re-elected for another term of four years which would elapse by April 2015.

8 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

The members of the Executive Council include:

Name Responsibility

Chief Steven Obekpa Lawani Deputy Governor

Dr. David Salifu Secretary to Government

Mr. Terna Ahua Head of Service

HONOURABLE COMMISSIONERS

Mr. Omadachi Oklobia Finance & Budget

Hon. Egbiri Idaah Youth & Sport

Hon. John Tondu Land & Survey

Sir. John Ngbede Works & Transport

Pharm. Alexander Akpera Environment & Urban Development

Dr. Elizabeth Ugo Education

Mrs. Elizabeth Allagh Women Affairs & Social Development

Mrs. Comfort Ajene Culture & Tourism

Dr. Orduen Abunku Health & Human Services

Hon. Esther Dzungwe Water Resources

Mr. Terfa Atoza Ihindan Commerce & Industry

Hon. Anumeh Innocent Housing

Mr. Gbugho Amokaha Donald Agriculture & Natural Resources

Hon. Anthony Onuh Science & Technology

Hon. Justin Amase Information and Orientation

Hon. Aondowase Chia Rural Development & Co-operative

Source: Benue State Government of Nigeria

9 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

FEATURES OF THE BOND

Benue State intends to issue a ₦4.95 billion seven-year fixed rate Bond in Q1‘2015. The net proceeds of

the Bond will be used to fund the construction of over 207 km of roads in various local governments in

the State, upgrade of existing water works and complete rural electrification projects across the State. The

projects will not generate revenue to repay the Bond but are expected to improve the socio-economic

condition in the State.

Table 2: Utilization of Proceeds

Projects ₦'bn

Completion of rural electrification projects across the State 0.50 10%

Upgrading of existing water works at Makurdi, Otukpo & Kastina-Ala 1.00 20%

Construction of Taraku-Naka-Agada Road (61 km) 0.70 14%

Construction of Township Roads 0.45 9%

Upgrade & rehabilitation of Daudu-Gbajimgba Road (48.50 km) 0.60 12%

Construction of Oju-Obussa-Utonkon Road (51.48 km) 0.61 12%

Construction of Wannune-Ikpa-Igbor Road (36.73 km) 0.44 9%

Construction of Oshigbudu-Obagaji Road (10 km) 0.31 6%

Issue and underwriting cost 0.33 7%

Total Cost 4.95 100%

Source: Benue State Government of Nigeria

The Bond principal will be amortized semi-annually over seven years. The Issue will attract a fixed coupon

rate to be determined via a Book Building process and paid semi-annually.

In accordance with the Investment and Securities Act 2007 (ISA) and the Benue State Bonds, Notes and

other Securities (Issuance) Law of 2009, the Issuer will establish a Sinking Fund Account (SFA) to cover the

₦4.95 billion Bond obligations. The State will execute an Irrevocable Standing Payment Order (ISPO) for

monthly deductions of ₦103.8 million from the State‘s statutory allocation, which will be credited into the

SFA over the tenor of the Bond. In the event of any shortfall in the SFA, the Benue State Bond Issuance

Law of 2009 empowers the State House of Assembly to make supplementary appropriation to the Debt

Service Reserve Fund to meet the shortfall.

The SFA will be jointly managed by First Trustees Limited, Skye Trustees Limited and UBA Trustees

Limited. Pursuant to the Trust Deed, the Trustees will apply the funds in the SFA to pay bond obligations

as well as annual charges related to the management of the SFA. In our opinion, the Trustees are well

experienced in the management of Sinking Fund Accounts for state government bonds.

10 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

FINANCIAL CONDITION OF BENUE STATE

Obligations of the ₦4.95 billion seven-year fixed rate Bond will be paid out of the finances of the Benue

State Government. Therefore, we have analyzed the financial condition of the State.

Revenue Profile

Benue State‘s main sources of revenue are statutory allocation (SA), value added tax (VAT) and internally

generated revenue (IGR). During the year ended 31 December 2013, Benue‘s total revenue (excluding

grants) amounted to ₦81.8 billion showing a 6% increase from prior year, mainly driven by growth in

statutory allocation. In 2013, Statutory allocation accounted for 75% of total revenue, while IGR and VAT

contributed 14% and 11% respectively.

Akin to most states in the Country, the Issuer is highly

dependent on statutory allocation as evidenced by the

five-year average contribution of SA to total revenue

of 74%. According to the 2014—2016 Medium Term

Expenditure Framework (MTEF) and Fiscal Strategy

Paper (FSP) of the Government, contributions to

statutory allocation will remain upheld by oil revenue

from the Excess Crude Account, owing to the margin

between the average benchmark oil price of $75 per

barrel and the estimated average international oil price

of $104.6 per barrel over the period.

Also contributing to the State‘s revenue is VAT which is

collected centrally by the Federal Government, and 50% of the pool is distributed to all the states of the

Federation. In 2013 VAT grew by 11% to ₦8.9 billion from prior year, representing 11% of revenue. Over

the last five years, Benue State‘s share of the Value Added Tax has averaged 11% of total revenue.

The Issuer, like many other states in the Country, has a low capacity to generate internal revenue from tax

and non-tax sources. In the financial year ended 31 December 2013, the State‘s IGR increased by 18% to

₦11.3 billion largely due to an increase in non-tax sources. Consequently IGR represented 14% of revenue,

which is below our expectation.

In our opinion, the Issuer‘s revenue profile requires improvement.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 2012 2011 2010 2009

VAT IGR SA

Figure 4: Revenue Breakdown

11 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

Expenditure Profile

During the year ended 31 December 2013, Benue State‘s total expenditure decreased by 14% to ₦82.6

billion, driven by lower overheads and reduced personnel costs. Recurrent expenditure accounted for 60%

of total spending, while capital expenditure (capex) stood at 40%. This level of total spending is above

total revenue (including grants of ₦0.09 billion) in the period under review, leaving a budget deficit of

₦0.7 billion.

In 2013, the Issuer‘s capital expenditure of ₦33.1 billion represents a 34% improvement from prior year.

The capex was mainly expended on the economic sector (62%), social service sector (32%), general

administrative sector (4%) and environmental sector (2%). Over the last five years, Benue State has

maintained an average capex to total expenditure ratio of 35%, which is within our expectation.

Table 3: Breakdown of Capital Expenditure

Sector 2013 2012 2011 2010 2009

₦‘bn ₦‘bn ₦‘bn ₦‘bn ₦‘bn

Economic 20.5 62% 5.9 24% 4.2 15% 4.2 28% 9.4 53%

Social Service 10.7 32% 15.2 62% 18.4 66% 6.8 45% 5.0 28%

Gen. Administrative 1.4 4% 2.8 11% 1.7 6% 0.6 4% 0.6 3%

Environment 0.6 2% 0.7 3% 3.5 13% 3.5 23% 2.6 16%

Total 33.1 100% 24.7 100% 27.8 100% 15.1 100% 17.6 100%

Benue‘s recurrent expenditure of ₦49.4 billion comprised,

personnel costs (67%), overheads (15%), transfers (14%)

and interest payment (4%). Despite the decrease in the

State‘s personnel cost from the parastatals by 12% to ₦33

billion from prior year, the ratio of personnel cost to

revenue ratio at 40% is higher than our expectation.

The Issuer‘s overhead costs declined significantly by 69%

to ₦7.4 billion in the period under review (2012: ₦23.7

billion), owing to a reduction in general administrative

cost. Despite the substantial decline in 2013, overheads

cost to revenue ratio over the last three years (2010 –

2012) has averaged 23%, which we consider to be high.

In our opinion, Benue‘s expenditure profile is high and

requires improvement.

0%

10%

20%

30%

40%

50%

60%

2013 2012 2011 2010 2009

Personnel Cost Overhead Cost

Figure 5: Personnel/Overhead Cost to Revenue

12 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

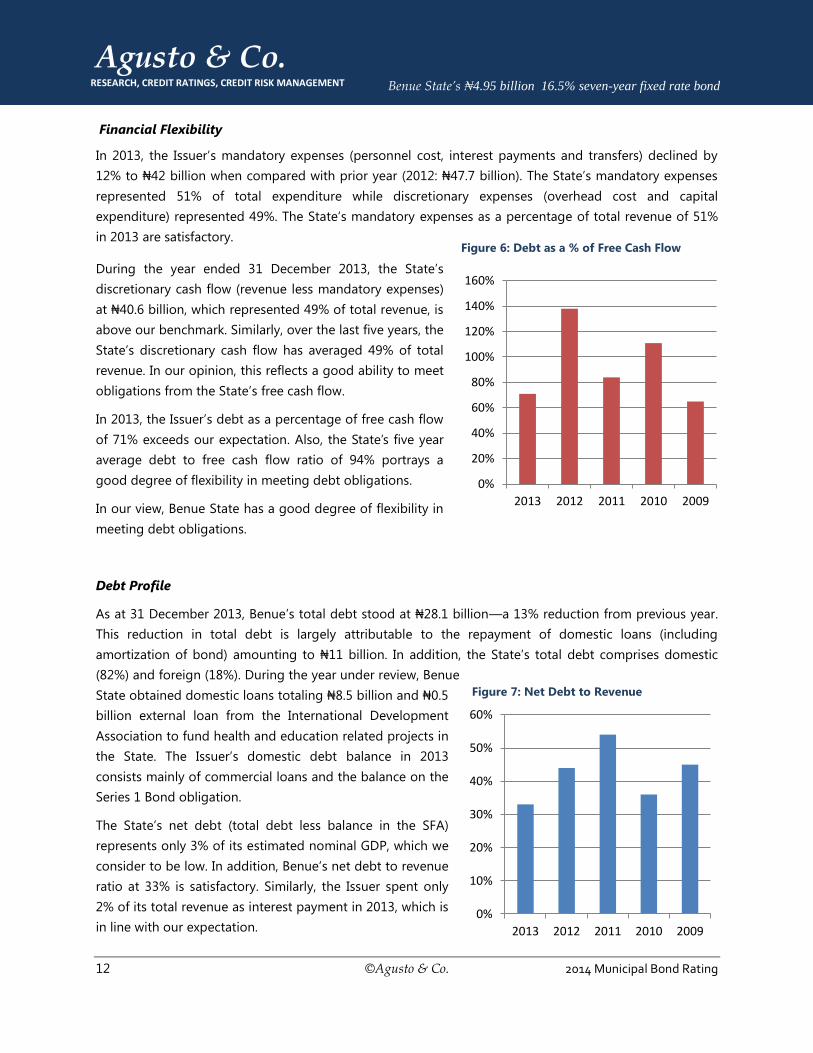

Financial Flexibility

In 2013, the Issuer‘s mandatory expenses (personnel cost, interest payments and transfers) declined by

12% to ₦42 billion when compared with prior year (2012: ₦47.7 billion). The State‘s mandatory expenses

represented 51% of total expenditure while discretionary expenses (overhead cost and capital

expenditure) represented 49%. The State‘s mandatory expenses as a percentage of total revenue of 51%

in 2013 are satisfactory.

During the year ended 31 December 2013, the State‘s

discretionary cash flow (revenue less mandatory expenses)

at ₦40.6 billion, which represented 49% of total revenue, is

above our benchmark. Similarly, over the last five years, the

State‘s discretionary cash flow has averaged 49% of total

revenue. In our opinion, this reflects a good ability to meet

obligations from the State‘s free cash flow.

In 2013, the Issuer‘s debt as a percentage of free cash flow

of 71% exceeds our expectation. Also, the State‘s five year

average debt to free cash flow ratio of 94% portrays a

good degree of flexibility in meeting debt obligations.

In our view, Benue State has a good degree of flexibility in

meeting debt obligations.

Debt Profile

As at 31 December 2013, Benue‘s total debt stood at ₦28.1 billion—a 13% reduction from previous year.

This reduction in total debt is largely attributable to the repayment of domestic loans (including

amortization of bond) amounting to ₦11 billion. In addition, the State‘s total debt comprises domestic

(82%) and foreign (18%). During the year under review, Benue

State obtained domestic loans totaling ₦8.5 billion and ₦0.5

billion external loan from the International Development

Association to fund health and education related projects in

the State. The Issuer‘s domestic debt balance in 2013

consists mainly of commercial loans and the balance on the

Series 1 Bond obligation.

The State‘s net debt (total debt less balance in the SFA)

represents only 3% of its estimated nominal GDP, which we

consider to be low. In addition, Benue‘s net debt to revenue

ratio at 33% is satisfactory. Similarly, the Issuer spent only

2% of its total revenue as interest payment in 2013, which is

in line with our expectation.

0%

20%

40%

60%

80%

100%

120%

140%

160%

2013 2012 2011 2010 2009

Figure 6: Debt as a % of Free Cash Flow

0%

10%

20%

30%

40%

50%

60%

2013 2012 2011 2010 2009

Figure 7: Net Debt to Revenue

13 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

Benue State intends to raise a ₦4.95 billion fixed rate bond in Q1‘2015 to finance key road projects,

upgrade existing water works and complete rural electrification projects across the State. Subsequent to

bond issuance, the Issuer‘s outstanding net debt (less balance in SFA) will represent 39% of 2013 revenue.

This is below the 50% maximum limit set by the Investment and Securities Act 223 (2007) for state

governments.

The State also intends to set aside monies in a sinking fund account by way of a monthly ISPO of ₦103.8

million over the life of the Issue. In our view, the total amounts to be set aside in the SFA will be adequate

to repay total bond obligations.

FINANCIAL FORECAST

Benue State has prepared revenue and expenditure forecasts covering the life of the Bond. The projection

is based on the general assumption that there will be no significant changes in the Federal Government‘s

monetary and fiscal policies during the forecast period that will adversely affect the State. In addition, the

Federal Government will continue to play an active role in stimulating the economy and pursue the goal

of a single-digit inflation rate, as well as assume a relative stable sharing formula of the Federation

Account, Excess Crude Oil Account, Value Added Tax pool and Others (NNPC refund, Sure-P) over the

tenor of the Bond.

The Issuer anticipates cumulative revenue of ₦589 billion over the seven year period ending 2021 on the

back of moderate increases to statutory allocation, VAT and IGR. Over the tenor of the Bond, Statutory

allocation will account for 63% of cumulative revenue, while IGR, VAT and others will represent 19%, 16%

and 2% respectively.

The 2014—2016 Medium Term Expenditure Framework (MTEF) and Fiscal Strategy Paper (FSP) projects

10% reduction in statutory allocation in 2014 and an increase of 5% and 3.5% in 2015 and 2016

respectively. Benue State has adopted the MTEF forecast and projects a 2% annual increase in statutory

allocation from 2017 to the end of the Bond. In our opinion, the projections are realistic; hence we have

adopted the State‘s forecast.

In addition, the State‘s value added tax (VAT) forecast was hinged upon the Federal Governments‘

projection as contained in the MTEF. The MTEF projects a 10.4% reduction in VAT in 2014 and subsequent

increase of 3.6% in 2015, 10% in 2016 and further growth of 10% annually from 2017—2021. This

projection is at variance with Benue State‘s Compound Annual Growth Rate (CAGR) of 11%, which opines

a positive growth for VAT in the foreseeable future. Therefore, we have adjusted the Issuer‘s VAT

expectations to align with the rebased GDP growth rate forecast from the National Bureau of Statistics.

VAT is a tax on consumer spending driven by level of economic activity in a country.

14 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

The State‘s internally generated revenue over the last five years has been skewed with positive and

negative movements, with increases as much as over 100% and reductions below 30%. Barring these

variations, Benue State intends to improve its internal revenue (tax & non-tax sources) through various

enhancement collection strategies across the Ministries Departments and Agencies (MDAs). The State

forecasts that the strategies will result in IGR growth of 10% in 2014, 15% in 2015, 20% in 2016 and 5%

thereafter over the projected period. Agusto & Co, believes that despite the State‘s inconsistency in IGR

generation over the last five years and its proposed revenue enhancement strategies, the State may

experience a tepid growth of 5% annually over the life of the Bond. In our opinion, the projected tepid

growth of IGR will depend largely on improved tax awareness, better tax administration, implementation

of revenue collection strategies and improvements to the security situation in the State.

The State projects cumulative spending of ₦558 billion, leaving a surplus of ₦31 billion over the seven

year period. The total spending forecast has a recurrent component of 72% and capital expenditure of

28%.

The Issuer‘s proposed cumulative recurrent expenditure comprising personnel cost, overhead cost and

consolidated revenue fund charges, was based on the assumptions of a 5.1% increase in 2014 and

subsequent 1% annual increase over the life of the Bond, across all the components of recurrent

expenditure. The CAGR for personnel cost over the last five years stood at 24%, while CAGR for overhead

cost (barring the 69% decline in 2013) over a four year period (2009—2012) was 20%. In our view,

personnel cost will grow higher than forecasted, while overheads will continue to be underpinned by

inflation rate. Therefore, we have made relevant adjustments to personnel and overhead cost. Agusto &

Co. believes that the State‘s assumption on capital expenditure and consolidated revenue fund charges

over the tenor of the bond are realistic, hence we have adopted same.

Adjusted Revenue and Expenditure Forecast

Based on our adjusted forecast, the Issuer‘s cumulative revenue will amount to ₦566 billion, while the

State‘s cumulative expenditure is estimated at ₦589 billion. This leaves an estimated deficit of ₦23 billion,

which can be financed through borrowing or can be reduced if discretionary spending from overhead and

capex estimated at ₦252 billion is curtailed in line with available revenue.

Revenue Breakdown

2015 2016 2017 2018 2019 2020 2021 TOTAL %

₦'mns ₦'mns ₦'mns ₦'mns ₦'mns ₦'mns ₦'mns ₦'mns

IGR 10.969 11,518 12,094 12,698 13,333 14,000 14,700 89,313 15

VAT 10,711 11,504 12,355 13,269 14,251 15,306 16,438 93,834 17

Federal Allocation 50,287 51,467 52,201 53,052 53,972 54,911 55,919 371,809 66

Grants & Others 1,600 1,600 1,600 1,600 1,600 1,600 1,600 11,200 2

Total Revenue 73,567 76,088 78,250 80,620 83,156 85,817 88,657 566,155 100

15 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

Expenditure Breakdown

2015 2016 2017 2018 2019 2020 2021 TOTAL %

₦'mns ₦'mns ₦'mns ₦'mns ₦'mns ₦'mns ₦'mns ₦'mns

Recurrent 63,373 61,248 59,938 61,862 63,520 60,274 61,182 431,397 73

Capital 10,800 15,120 21,168 23,285 25,613 28,175 33,810 157,971 27

Total Expenditure 74,173 76,368 81,106 85,147 89,133 88,449 94,992 589,368 100

Free Cash Flow Forecast

Benue State‘s discretionary cash flow over the life of the Bond at ₦108 billion is adequate to cover total

interest payments 7 times. The free cash flow (before debt servicing) is also sufficient to meet total debt

obligations 3 times, which in our opinion is good.

2015 2016 2017 2018 2019 2020 2021 TOTAL

₦'mns ₦'mns ₦'mns ₦'mns ₦'mns ₦'mns ₦'mns ₦'mns

Discr. Cash flow 16,570 16,454 16,292 14,782 13,211 16,608 14,938 108,864

Coupon (16.5%*) (800) (728) (644) (545) (430) (294) (135) (3,576)

Discr. Cash flow after coupon 15,770 15,726 15,648 14,237 12,781 16,314 14,803 105,288

Principal (418) (490) (574) (673) (788) (924) (1,083) (4,950)

Interest Cover (Times) 4 5 5 9 8 11 56 7

Total Debt Coverage (Times) 3

OUTLOOK Benue State also known as the nation‘s food basket, lies within the lower River Benue and its vegetation is

conducive for farming, fishing and animal husbandry. In addition, the State is endowed with large

deposits of limestone and kaolinite which are not fully exploited. These reflect good potentials for vibrant

economic activities, which could translate to higher IGR from tax collection. The State intends to improve

its internal revenue (tax & non-tax sources) through improved tax awareness, better tax administration

and implementation of revenue collection strategies across the (Ministries Departments and Agencies

(MDAs). This is expected to translate to increased internal revenue in the foreseeable future against the

backdrop of its low 14% contribution to revenue.

The State plans to Issue a ₦4.95 billion seven year fixed rate Bond in Q1‘2015 to fund some key projects

including road construction, water works and rural electrification in the State. The Issuer has requested for

an ISPO for monthly deductions of appropriate amounts from its statutory allocation into a designated

SFA over the tenor of the Bond. After the ₦4.95 billion Bond issuance, the State‘s total debt to revenue

ratio at 39% is below the Investment and Securities Act limit of 50% for state governments‘ borrowing. In

our view, the Issuer has the capacity to meet its interest payment and total debt obligations over the life

of the Issue as evidenced by Agusto & Co.‘s sensitized forecast of 7 times and 3 times respectively.

Therefore, we have attached a stable outlook to Benue State‘s ₦4.95 billion Bond.

* Indicative

16 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

FINANCIAL SUMMARY REVENUE & SPENDING

2013 2012 2011 2010 2009

REVENUE ₦'mns % ₦'mns % ₦'mns % ₦'mns % ₦'mns %

Tax revenue

Personal Income Tax 5,247.3 6% 7,903.3 10% 3,125.3 4% 1,778.7 3% 1,138.6 2%

Share of VAT collected centrally 8,982.2 11% 8,091.0 11% 7,420.8 11% 6,361.4 12% 5,451.6 12%

Share of other revenues collected

centrally (Stat. Allocation)

61,564.6 75% 53,369.0 69% 54,060.6 78% 36,468.2 71% 34,037.1 74%

Property tax

Other taxes

75,794.1 93% 69,363.4 90% 64,606.7 93% 44,608.4 87% 40,627.3 88%

Non-tax revenue

Asset sales

Investment income 724.6 1% 364.2 0% 864.2 1% 730.6 1% 3,051.9 7%

Other 5,362.8 7% 1,330.2 2% 1,465.6 2% 5,895.9 11% 1,986.6 4%

6,087.4 7% 1,694.5 2% 2,329.8 3% 6,626.5 13% 5,038.5 11%

TOTAL REVENUE 81,881.4 100% 71,057.8 92% 66,936.5 96% 51,234.9 99% 45,665.8 99%

Of which internally generated revenue

(IGR) is

11,334.7 9,597.8 5,455.1 8,405.3 6,177.0

Grants 9.0 0% 5,896.5 8% 2,591.0 4% 289.0 1% 348.7 1%

TOTAL REVENUE & GRANTS 81,890.4 100% 76,954.3 100% 69,527.5 100% 51,523.8 100% 46,014.5 100%

SPENDING

Transfers (including pension costs) 7,016.5 8% 7,879.7 8% 3,577.4 5% 17,038.6 28% 1,524.7 4%

Interest payment 1,958.5 2% 2,085.3 2% 1,481.1 2% 1,356.1 2% 1,692.6 4%

MDA spending 73,631.7 89% 86,133.1 90% 62,194.4 92% 43,003.6 70% 40,122.2 93%

TOTAL SPENDING 82,606.7 100% 96,098.1 100% 67,252.9 100% 61,398.2 100% 43,339.5 100%

MDA spending is made up of

Personnel costs 33,035.2 40% 37,713.6 39% 18,694.8 28% 16,008.0 26% 11,157.6 26%

Purchase of goods & services 7,432.7 9% 23,694.4 25% 15,682.8 23% 11,830.7 19% 11,275.3 26%

Capital expenditure 33,163.8 40% 24,725.1 26% 27,816.8 41% 15,164.8 25% 17,689.3 41%

TOTAL MDA SPENDING 73,631.7 89% 86,133.1 90% 62,194.4 92% 43,003.6 70% 40,122.2 93%

Budget Balance (716.3) (19,143.8) 2,274.6 (9,874.4) 2,675.0

BUDGET BALANCE AS % OF GDP -0.1% -2.4% 0.3% -1.5% 0.4%

-

Surplus/(deficit) of prior years 8,562.3 6,728.2 10,665.3 8,562.3 6,728.2

Domestic borrowing (net) (2,659.9) 1,807.9 14,759.6 (2,141.5) (2,678.2)

External borrowing (net) 417.6 (9,139.3) (5,196.6) (67.2) 158.7

Others 20.0 20.0

TOTAL FINANCING 6,340.1 (603.2) 20,228.3 6,373.6 4,208.7

Foreign Loans- New Borrowings 490.1 3,541.8 - 141.7 286.0

Repayment during the year 72.5 12,681.1 5,196.6 208.9 127.3

Foreign loan balance 5,034.7 4,617.0 8,843.4 13,968.5 14,035.8

Domestic- New Loans 8,463.8 7,355.2 16,804.9 2,344.2 5,500.0

Loan due (repaid) within the year 11,123.7 5,547.2 2,045.3 4,485.7 8,178.2

Domestic loan balance 23,115.3 27,595.87 27,442.9 4,641.8 6,300.00

17 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

KEY RATIOS 2013 2012 2011 2010 2009

Revenue

IGR as % of GDP 1% 1% 1% 1% 1%

Tax revenue as % of GDP 9% 9% 9% 7% 7%

Total revenue as % of GDP 10% 9% 9% 8% 8%

IGR as % of total revenue & grants 14% 12% 8% 16% 13%

Tax revenue as % of IGR 46% 82% 57% 21% 18%

Growth in tax revenue 9% 7% 45% 10% -7%

Spending

Spending as % of GDP 10% 12% 9% 9% 7%

Non-discretionary spending* as % of tax

revenue

55% 69% 37% 77% 35%

Capital expenditure as % of total spending 40% 26% 41% 25% 41%

Payroll as % of revenue 40% 53% 28% 31% 24%

Other overheads as a % of revenue 9% 33% 23% 23% 25%

Leverage

Budget balance (₦'mns) (716.28) (19,143.77) 2,274.61 (9,874.36) 2,674.96

Net Debt as % of nominal GDP 3% 4% 5% 3% 3%

Interest payments as % of total revenue 2% 3% 2% 3% 4%

Net Debt as % of Revenue 33% 44% 54% 36% 45%

Financial flexiblity

Discretionary revenue** as % of total revenue 49% 33% 65% 33% 69%

Debt as % of Free cash flow*** 71% 138% 84% 111% 65%

Share of savings in "excess crude account"

(₦'mns)

Non-discretionary Spending as % of total

spending

51% 50% 35% 56% 33%

Outstanding Debt/Revenue 34% 45% 54% 36% 45%

Loan Repayment/Revenue 14% 26% 11% 9% 18%

* Non-discrectionary spending is made up of statutory transfers, interest payments and

personnel costs

** Discretionary revenue is total revenue minus non-discretionary

spending

*** Free cash flow is defined as revenue minus non-discretionary

spending

18 ©Agusto & Co. 2014 Municipal Bond Rating

Agusto & Co.

RESEARCH, CREDIT RATINGS, CREDIT RISK MANAGEMENT Benue State’s ₦4.95 billion 16.5% seven-year fixed rate bond

RATING DEFINITIONS

Aaa Highest quality debt issue with minimal credit risk; strongest capacity to pay returns

and principal on local currency debt in a timely manner.

Aa

High quality debt issue with very low credit risk; very strong capacity to pay returns

and principal on local currency debt in a timely manner.

A

Good quality debt issue with low credit risk; strong capacity to pay returns and

principal on local currency debt in a timely manner.

Bbb

Satisfactory quality with low credit risk; adequate capacity to pay returns and principal

on local currency debt in a timely manner.

Bb

Below average quality with moderate to high credit risk; speculative capacity to pay

returns and principal on local currency debt in a timely manner.

B

Weak quality with high credit risk; speculative capacity to pay returns and principal on

local currency debt in a timely manner.

C

Very weak capacity to pay returns and principal. Debt instrument with very high credit

risk.

D In default.

Rating Category Modifiers

A "+" (plus) or "-" (minus) sign may be assigned to ratings from ‘Aa’ to ‘C’ to reflect comparative position within the rating category.

Therefore, a rating with + (plus) attached to it is a notch higher than a rating without the + (plus) sign and two notches higher than a

rating with the - (minus) sign.

19 ©Agusto & Co.

THIS PAGE HAS BEEN LEFT BLANK INTENTIONALLY