Benchmark results 2017 3Q - digitalinnovationsummit.com · management. Dicitas Consulting ......

14

Digital dominance Benchmark Benchmark results 2017 3Q Martin Hermsen Dicitas Consulting January 2018

Transcript of Benchmark results 2017 3Q - digitalinnovationsummit.com · management. Dicitas Consulting ......

Digital dominance Benchmark

Benchmark results 2017 3Q

Martin Hermsen

Dicitas Consulting

January 2018

Dicitas Consulting

Being digital and strengthening

your brand in the digital space is

essential to become future proof

Digital dominance helps your

business to stay ahead of the

competition and be the winner

in your industry

For the second consecutive year Dicitas

Consulting conducted the Digital Dominance

Benchmark, evaluation the digital presence and

strengths of 90 brand in the Netherlands in 9

different sectors.

/2

Dicitas Consulting

Summary

Our research and experience in the digital world has taught us that companies need to invest smart to create digital differentiation and need:

• A strong web presence, inviting, quick to load, searchable with clear navigation and calls to action for the customer

• Mobile optimization beyond responsive design; also succinct, uncluttered and with a clearly visible value proposition

• Emotional engagement with the customer, utilizing and curating relevant stories and content delivered by a compelling customer experience

• A proactive social media strategy to engage with customers and communities on social where they turn to for information, counsel and decision making

• Paid media advertising to ensure brand visibility, awareness, consideration and customer activation

Many companies are struggling to get it ‘right’ with their digital efforts, and therefore, brands face the challenge to bridge the gap between customer expectations and the experience they deliver as a brand. Luckily, it is possible to determine who owns the digital space in each sector and what your company can do to get or stay ahead of your closest competitors.

The Digital Dominance Benchmark

/3

Dicitas Consulting conducted for the second consecutive year the Digital

Dominance Benchmark. The benchmarks measures the digital competitive

strengths of brands in 9 different industry sectors.

About Dicitas Consulting

Dicitas Consulting helps organizations to

transform and become digital leaders in

their market. Helping you get there is

what we do best. Together with our

business partners, we guide your

organization through sustainable

business performance improvement

and growth.

About Martin Hermsen

Martin Hermsen is partner

at Dicitas Consulting and is

responsible for the

Customer & Channel

practice. He has over 20

years of consulting

experience in growth &

competitive strategy,

product innovation,

marketing and customer

management.

Dicitas Consulting

The Digital Dominance Benchmark

tracks companies’ digital brand

performance and benchmarks it within

their industry, as well as cross-industry. It

shows how digital dominant brands are

in the digital spectrum. The Index is an

indicator that describes how strong

each company or brand performs in the

digital sphere.

Our benchmark will determine the digital

positioning in each sector. Different

aspects of the benchmark are more or

less relevant in different industries. Online

video might for example be of more

importance to certain, more consumer-

focused industries than others.

We measure digital dominance within 5

key digital areas: websites, SEO, social

media, online video and apps. With the

data we collect we are able to rank the

brands within each of the Digital pillars

The pillars consist of various KPIs that

allow for deeper investigation into what

exactly has affected a specific

company’s performance and what can

be done to improve performance. It can

also be used to match with your current

strategy and efforts to indicate what has

worked well and what has not.

Know your digital brand strength

/4

That most companies are increasing their digital budget is no secret, but the

question is, how far are digital initiatives taking companies in the strive for

digital excellence? In the age we live in, companies need to create a

competitive advantage by mastering their digital presence and customer

engagement.

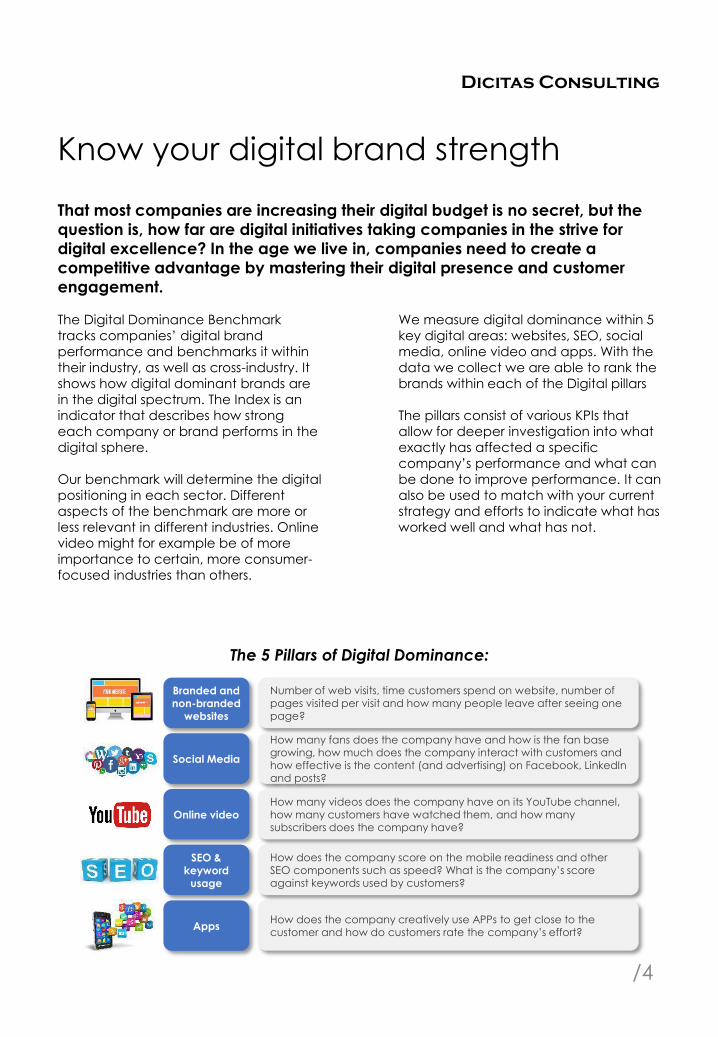

The 5 Pillars of Digital Dominance:

Branded andnon-branded

websites

SEO & keyword

usage

Social Media

Online video

Apps

Number of web visits, time customers spend on website, number of pages visited per visit and how many people leave after seeing one page?

How many fans does the company have and how is the fan base growing, how much does the company interact with customers and how effective is the content (and advertising) on Facebook, LinkedIn and posts?

How many videos does the company have on its YouTube channel, how many customers have watched them, and how many subscribers does the company have?

How does the company score on the mobile readiness and other SEO components such as speed? What is the company’s score against keywords used by customers?

How does the company creatively use APPs to get close to the customer and how do customers rate the company’s effort?

Dicitas Consulting

Why is it important to measure your

digital brand strength?

• To gain insights into how direct and

non-direct competitors are

performing on all digital channels

• To compare to and learn from

companies in other industries how to

improve your own digital brand

performance

• To learn which digital capabilities you

need to improve and how

• Being able to see whether your

previous efforts have paid off and

which have been less effective

• It helps you to define a digital

strategy to ensure that you become

the dominant player in the digital

world

The Digital Dominance Benchmark

allows you to compare the digital

strengths of your brands with

competitors in- and outside your

industry.

Our current diagnostic peer group

contains 9 industry sectors, 11 countries

and over 150 brands. We perform the

digital benchmark research in

Netherlands, Belgium, UK, Germany,

Italy, Spain, France, Japan, Australia,

Canada and USA.

Besides our yearly digital dominance

benchmark we can benchmark specific

brands in specific countries on special

request of our customers.

Why it is important

/5

Companies that invest strongly in their digital capabilities not only get ahead

of competition in the digital sphere, but also improve their overall business

performance. The Digital Dominance Benchmark helps you to define the right

direction for your investments.

Benchmark pool Netherlands:

Dicitas Consulting

Key take aways:

Most brands in the Netherlands just

slightly improved relative to the previous

benchmark in 2016 in terms of digital

visibility and digital strength and

dominance. This in contrary to the digital

development of brands in other

countries in Europe like the UK, Germany

and France.

The average score in each sector

increased.

For most sectors, the benchmark

dispersion being the spread between

best and worst brand per category

decreased. Brands get closer in their

digital dominance. Suggesting that it

seems to get harder to differentiate.

Netherlands is ahead of Belgium.

Banking and retail have the highest

averages in both countries. For both

Netherlands and Belgium, products

scores the lowest average. Dispersion in

some industries is larger than others. The

best in the Netherlands have higher

scores than the best in Belgium, for all

sectors.

Digital Dominance Benchmark results in 2017

/6

Dicitas Consulting conducted for the second consecutive year the Digital

Dominance Benchmark. The benchmarks measures the digital competitive

strengths of brands in 9 different industry sectors.

The 2017 Results

Average DDI scores per industry with 2017 compared with 2016:

Dicitas Consulting

Most brands in most sectors are working

hard and seriously to build the needed

digital capabilities and invest in digital

transformation and new digital platforms

and tools. However the customer

journeys and experience delivered are

still often broken in silos and does not

deliver the customer experience that is

useful, relevant, easy, omnichannel and

correctly managed over a longer period

of time.

Due to digital, marketers are being

challenged by a deluge of data that is

well beyond the capacity of their

organizations to comprehend and use.

Their strategies are not keeping up with

the disruptive effects of technology-

empowered customers; the proliferation

of media, channel, and customer

contact points; or the possibilities for

micro segmentation.

Closing the widening gap between the

accelerating complexity of their markets

and the limited ability of their

organizations to respond demands new

thinking about digital marketing

capabilities.

The drivers for the widening digital

performance gap are increasing

complexity, interacting with an

accelerating rate of change in markets

and serious organizational impediments

to responding. The growing gap is

unquestionably costing firms profitability

now and competitiveness in the future.

If the gap has become too wide to

tolerate, what are companies doing to

narrow their capability gap and possibly

gain an advantage over slower-moving

competitors?

The Digital Performance Gap still exist

/7

The digital performance gap still exist. The difference between what customers

expect and what they experience is still too large and for most companies

bridging this gap remains a challenge.

The 2017 Results

How to bridge the gap between customer expectations and the experience

your brand is delivering?

Dicitas Consulting

All industries improved their average DDI scores. Some sectors improved more

significantly then others.

Average DDI results per industry sector compared with last year:

With Individual brands however, there are winners and losers. Brands that lagged behind in

2016, improved on average more the last year’s winners:

For all industries, the average brand score per channel increased in 2017

/8

The 2017 Results

Dicitas Consulting

The benchmark results and 3 best performing brands by Sector (1/3)

/9

The 2017 Results

Banks

Avg. score: 57%

Best score: 68%

Most banks score above the cross sector average and the sector

is the most dominant in the web and app categories. The overall

DDI score is 2nd after retail and has improved since 2016. Mobile

banking drives app usage and it’s popularity. The leading banks

regularly release updates of their apps and innovate their web

user experience on a continuous basis. The dispersion between

the best and worst became smaller. For banks it became more

difficult to differentiate themselves.

Insurance

Avg. score: 49%

Best score: 60%

Insurance companies score at the cross sector average of 49%

and their average score has improved since 2016. The dispersion

between the best and worst is still large giving significant

opportunity to improve. Specifically apps, video and social are

lagging behind.

Health Insurance

Avg. score: 40%

Best score: 51%

Health insurance are behind the insurance family and have a

long way to go to reach an acceptable level op digital

performance. All channels can be improved to communicate

better with their customers and to deliver a better customer

experience. The dispersion between the best and worst is

relatively large.

Energy

Avg. score: 48%

Best score: 56%

The energy sector is a true ”average joe”. They all perform just

below average in all categories. The energy sector seems to

have difficulties to develop relevant digital services. Smart

meters, local energy production and storage, solar panels, smart

grid, in house services are all market opportunities that will force

the energy sector to bridge this digital performance gap.

Telecom

Avg. score: 58%

Best score: 63%

The telecom sector scores third just behind the retail and banking

sectors. The dispersion between the best and worst is smallest

from all sectors suggesting little differentiation between the

brands. Market leaders like KPN and Vodafone did not make it in

the top 3. Digital dominance seems a strategy that is most used

by the market challengers to reach and convert customers to

gain market share.

Dicitas Consulting

The benchmark results and 3 best performing brands by Sector (2/3)

/10

The 2017 Results

Retail (Non-Food)

Avg. score: 60%

Best score: 67%

Retail is the most digital dominant sector in the benchmark. All

retailers score above the cross sector average. Retail also scores

best in the social category with a considerable head start to the

laggards. Retailers set the benchmark starters consistent with the

growth of ecommerce in the last years. The consumer searches,

finds buys, experience and returns more and more online.

Retailers need to develop digital and mobile first strategies to

remain competitive in the future.

Food Retail

Avg. score: 50%

Best score: 66%

Compared to (non food) retail, food retail has a large gap to

bridge. Although Albert Heijn home delivers for years did other

just started and still have modest sales as percentage of their

total revenue. The average sector score of food retail has

improved but remain below the cross sector average. Due to the

faster digital developments in other sectors, food retail falls

behind. Only the larger food retailers score above the cross

sector average, all other score below. Most retailers work hard

with various digital initiatives to bridge this gap.

Consumer Products

Avg. score: 45%

Best score: 56%

The scores in the CP sectors has the highest dispersion. The

average score of the sector scores below the cross sector

average and has only improved slightly. Specifically the

categories web and apps can be improved. The score for video

is above average. It seems the the strategic priority for most

consumer product brands is on brand development and less on

consumer activation.

Kitchen Appliances

Avg. score: 34%

Best score: 42%

New in the benchmark this year is the kitchen appliance sector.

Digital and for instance the internet of things and connectivity did

not became mainstream. The digital presence of the sector is

limited and falls far behind the cross sector average. Most brand

seems to lack a clear digital strategy. However, this digital kitchen

is getting closer faster then the sector might expect. We believe

that the brands that innovate digitally are going to make the

difference and win the consumers.

Human Resource

Avg. score: 44%

Best score: 53%

The HRM sector is on the rise. The sectors recognizes the need to

engage digitally with customer and candidates over a longer

period of time and cross channel. Digital engagement is only the

first step in the full digital matching process that automatically will

balance supply and demand. The requires new digital

capabilities like artificial intelligence, big data, customer journey

management and more.

Dicitas Consulting

For organizations and brands detailed reporting is available. It can help to

understand how they perform in the digital world and how to get and stay

ahead of the competition.

Benchmark insights

/11

A detailed look into the top and bottom performers in each of the industry sectors on all five pillars measured in the Digital Dominance Benchmark.

Gain insights on how your brand performs on each of the pillars cross industry. Compare your brand to best in class performers, companies you want to learn from or your closest competitors.

Be able to see the dispersion of the industries (weakest to strongest brands) including the industry averages and the

average of all brands measured in the Digital Dominance Benchmark.

Have a detailed look into the performance of your brand within each of the pillars and individually view your performance on every digital KPI.

The 2017 Results

Dicitas Consulting

The 2017 winners!

/12

The 2017 Results

The top 3 most digital dominant brands in 2017 are:

The winners per sector will be announced at the fourth edition of the “Digital

Innovation Summit” on the 22nd of March 2018 at the MindCenter, Vianen.

Dicitas Consulting

Digital Dominance press coverage 2016

/13Press icon to read article.

Dicitas Consulting

Being digitally dominant is important for your brand since more and more

consumers use digital in their daily lives. Being relevant, present and dominant

on digital channels is what determines your success for the future.

1. Companies need to be very aware of their customers, who they are and

what their digital behaviour is.

2. When you understand your customers it is possible to allocate the right

resources in the right way to optimize business performance attained

through the digital channels of their choice.

3. The digital performance gap still exist. The difference between what

customers expect and what they experience is still too large and for most

companies bridging this gap remains a challenge.

4. Companies that invest strongly in their digital capabilities not only get

ahead of competition in the digital sphere, but also improve their overall

business performance. The Digital Dominance Benchmark helps you to

define the right direction for your investments.

5. The digital dominance benchmark will help you in gaining these insights

and knowing whether you are doing the right things. In case you are not,

we can help you to gain grip on your digital channels and outperform

your competitors.

6. This year we award those brands that stand out in digital dominance in

the eyes of the consumer through digital channels. We benchmarked the

key brands in the Netherlands we will reward the winners during the Digital

Innovation Summit 2018.

/14

Martin Hermsen

+31 6 46 82 87 85

www.dicitas.com

www.digitalinnovationsummit.com

Key take aways of the 2017 Digital Dominance Benchmark

Dicitas Consulting