Before the MAHARASHTRA ELECTRICITY REGULATORY COMMISSION ... · Before the MAHARASHTRA ELECTRICITY...

103

MERC, Mumbai Page 1 of 103 Before the MAHARASHTRA ELECTRICITY REGULATORY COMMISSION World Trade Centre, Centre No.1, 13th Floor, Cuffe Parade, Mumbai – 400 005 Tel. 22163964/ 65/ 69 Fax 22163976 Email: [email protected] Website: www.mercindia.org.in Case No. 71 of 2007 IN THE MATTER OF Maharashtra State Power Generation Company Ltd.’s (MSPGCL) Petition for approval of Annual Performance Review for FY 2007-08 and Tariff for FY 2008-09 Dr. Pramod Deo, Chairman Shri A. Velayutham, Member Shri S. B. Kulkarni, Member O R D E R Dated: May 31, 2008 In accordance with the MERC Tariff Regulations and upon directions from the Maharashtra Electricity Regulatory Commission (Commission), the Maharashtra State Power Generation Company Ltd. (MSPGCL), submitted its Petition for approval of Annual Performance Review for FY 2007-08 and Tariff for FY 2008-09, on affidavit. The Commission, in exercise of the powers vested in it under Section 61 and Section 62 of the Electricity Act, 2003 (EA 2003) and all other powers enabling it in this behalf, and after taking into consideration all the submissions made by MSPGCL, all the objections and comments of the public, responses of MSPGCL, issues raised during the Public Hearing, and all other relevant material, and after review of Annual Performance for FY 2007-08, determines the revenue requirement and as a result of it, determines the tariff for the generating stations of MSPGCL for FY 2008-09 as under:

Transcript of Before the MAHARASHTRA ELECTRICITY REGULATORY COMMISSION ... · Before the MAHARASHTRA ELECTRICITY...

MERC, Mumbai Page 1 of 103

Before theMAHARASHTRA ELECTRICITY REGULATORY COMMISSION

World Trade Centre, Centre No.1, 13th Floor, Cuffe Parade, Mumbai – 400 005Tel. 22163964/ 65/ 69 Fax 22163976Email: [email protected]

Website: www.mercindia.org.in

Case No. 71 of 2007

IN THE MATTER OFMaharashtra State Power Generation Company Ltd.’s (MSPGCL) Petition for

approval of Annual Performance Review for FY 2007-08 and Tariff forFY 2008-09

Dr. Pramod Deo, ChairmanShri A. Velayutham, MemberShri S. B. Kulkarni, Member

O R D E R Dated: May 31, 2008

In accordance with the MERC Tariff Regulations and upon directions from theMaharashtra Electricity Regulatory Commission (Commission), the Maharashtra StatePower Generation Company Ltd. (MSPGCL), submitted its Petition for approval ofAnnual Performance Review for FY 2007-08 and Tariff for FY 2008-09, on affidavit.The Commission, in exercise of the powers vested in it under Section 61 and Section62 of the Electricity Act, 2003 (EA 2003) and all other powers enabling it in thisbehalf, and after taking into consideration all the submissions made by MSPGCL, allthe objections and comments of the public, responses of MSPGCL, issues raisedduring the Public Hearing, and all other relevant material, and after review of AnnualPerformance for FY 2007-08, determines the revenue requirement and as a result of it,determines the tariff for the generating stations of MSPGCL for FY 2008-09 as under:

MERC, Mumbai Page 2 of 103

Table of Contents

1 BACKGROUND AND BRIEF HISTORY ___________________________ 6

1.1 Tariff Regulations _________________________________________________ 6

1.2 Commission’s Order on ARR And Tariff Petition for FY 2005-06 and FY2006-07 ________________________________________________________________ 6

1.3 Review Petition on Tariff Order for FY 2006-07 ________________________ 7

1.4 Commission’s Order on MYT Petition For MSPGCL for FY 2007-08 to FY2009-10 ________________________________________________________________ 7

1.5 MSPGCL APPEAL with ATE and ATE Judgment _____________________ 7

1.6 Petition For Annual Performance Review for FY 2007-08 and TariffDetermination for FY 2008-09 ____________________________________________ 14

1.7 Admission of Petitions and Public Process ____________________________ 15

1.8 Organisation of the Order _________________________________________ 16

2 OBJECTIONS RECEIVED, MSPGCL s RESPONSE ANDCOMMISSION S RULING _________________________________________ 17

2.1 PROCEDURAL issues ____________________________________________ 17

2.2 Power Generation ________________________________________________ 18

MSPGCL s response_____________________________________________________ 18

MSPGCL s response_____________________________________________________ 19

3 TRUING UP OF ANNUAL REVENUE REQUIREMENT FOR FY 2006-0720

3.1 Fuel Costs_______________________________________________________ 20

3.2 Depreciation_____________________________________________________ 26

3.3 Advance against depreciation ______________________________________ 27

3.4 Interest Expenses_________________________________________________ 29

3.5 Return on Equity (RoE) ___________________________________________ 30

4 PERFORMANCE PARAMETERS _______________________________ 38

4.1 Performance Parameters __________________________________________ 38

4.2 Generating Stations of MSPGCL ___________________________________ 38

4.3 station-Wise Performance Parameters and Tariff______________________ 41

5 ANALYSIS OF ENERGY AVAILABILITY, ENERGY CHARGE AND AFCFOR FY 2007-08 & FY 2008-09______________________________________ 63

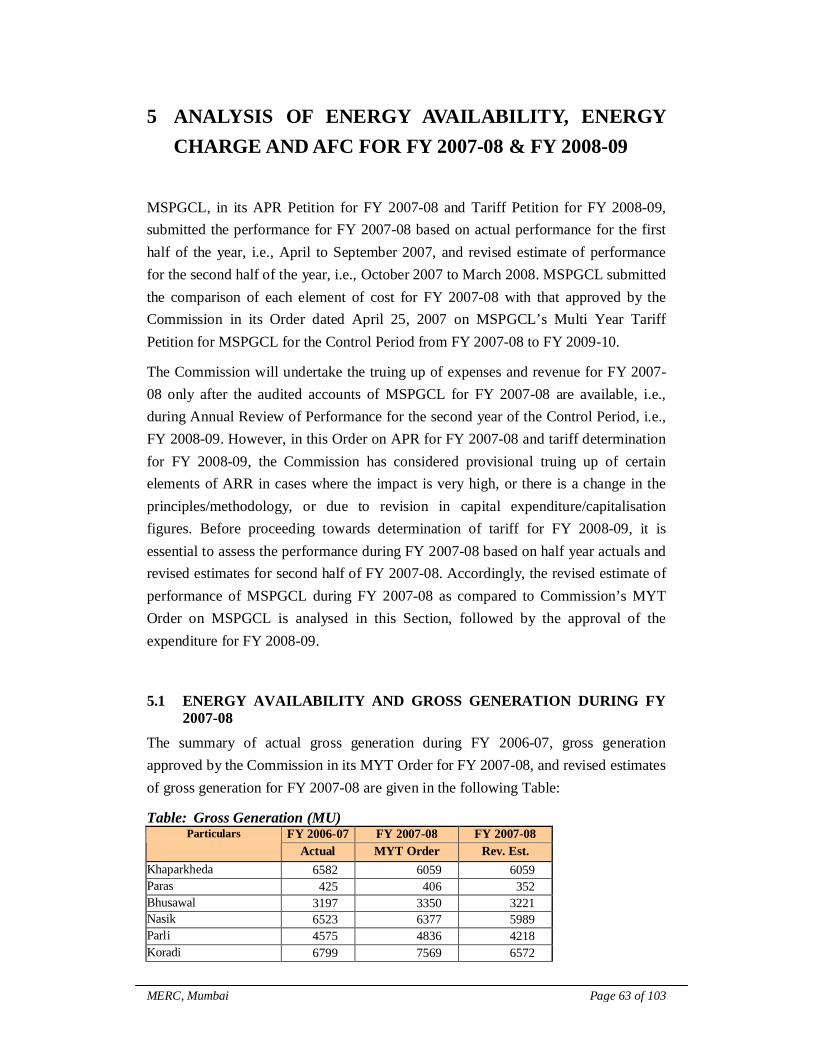

5.1 Energy Availability and Gross Generation during FY 2007-08 ___________ 63

MERC, Mumbai Page 3 of 103

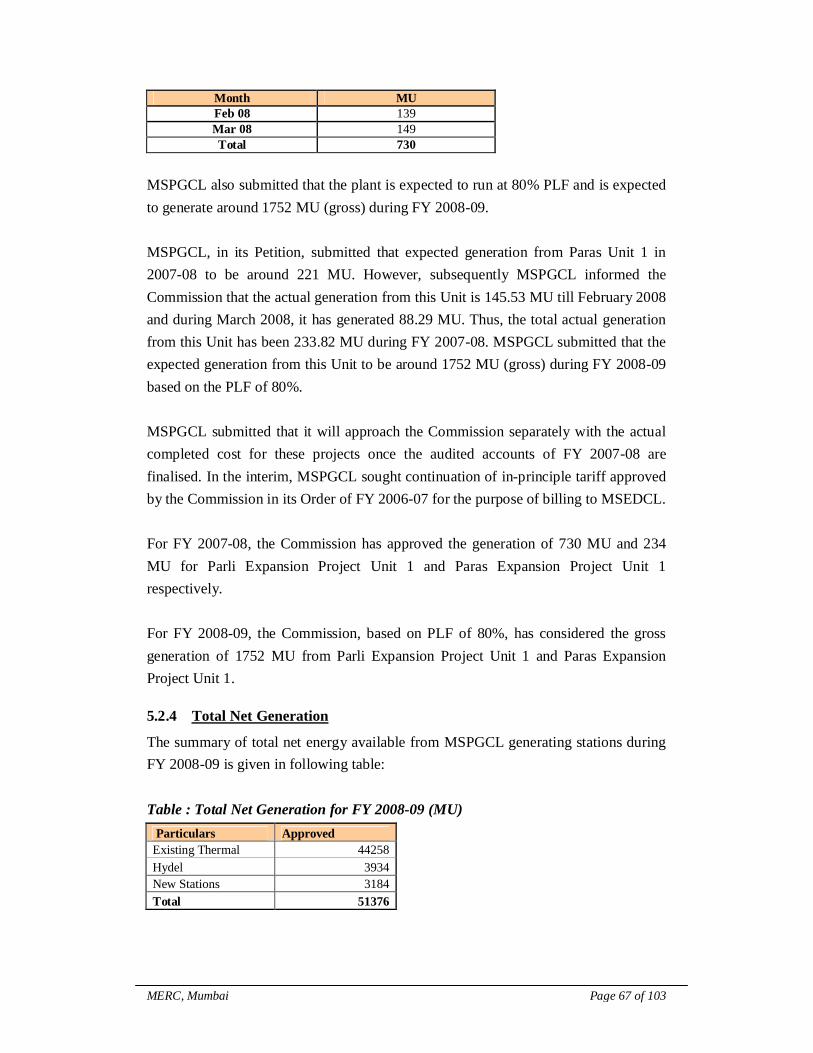

5.2 ENERGY AVAILABILITY FROM MSPGCL GENERATING STATIONSduring FY 2008-09 ______________________________________________________ 65

5.3 VARIABLE COSTS OF THERMAL GENERATING STATIONS _______ 68

5.4 Lease rent for hydel stations _______________________________________ 71

5.5 OPERATION AND MAINTENANCE EXPENSES ____________________ 72

5.6 Capital expenditure and capitalisation _______________________________ 76

5.7 Depreciation_____________________________________________________ 79

5.8 Advance against depreciation ______________________________________ 81

5.9 Interest Expenses_________________________________________________ 83

5.10 Return on Equity (RoE) ___________________________________________ 85

5.11 Interest on Working Capital for FY 2007-08 __________________________ 87

5.12 Interest on Working Capital for FY 2008-09 __________________________ 88

5.13 Non Tariff Income for FY 2007-08 __________________________________ 89

5.14 Non Tariff Income for FY 2008-09 __________________________________ 89

5.15 Income Tax for FY 2007-08 and FY 2008-09 __________________________ 89

5.16 Fixed Cost of Generation __________________________________________ 90

6 TARIFF OF MSPGCL S GENERATING STATIONS ________________ 92

6.1 Tariff for Thermal Power Generating Stations ________________________ 92

6.2 Tariff for Hydel Power Generating Stations __________________________ 95

6.3 AppliCAbility of Order and Tariff _________________________________ 101

MERC, Mumbai Page 4 of 103

List of AbbreviationsATE Appellate Tribunal for ElectricityA&G Administrative and GeneralAPR Annual Performance ReviewARR Aggregate Revenue RequirementAPH Air Pre HeaterAOH Annual OverhaulingBHEL Bharat Heavy Electriacals Ltd.Capex Capital ExpenditureCPI Consumer Price IndexCEA Central Electricity AuthorityCu.m Cubic meterCV Calorific ValueCOD Commercial Operation DateDPR Detailed Project ReportEA 2003 Electricity Act, 2003FAC Fuel Adjustment CostFOCA Fuel & Other Cost AdjustmentFY Financial YearGCV Gross Calorific ValueGFA Gross Fixed AssetsGOM Government of MaharashtraGOMWRD Government of Maharashtra-Water Resource DepartmentHPCL Hindustan Petroleum Corporation LimitedID Induced draftIWC Interest on Working CapitalKcal kilo calorieskW kilo WattkWh kilowatt hourLD Liquidity DamagesMCM Million Cubic MeterMMSCMD Million Standard Cubic Meters per DayMERC Maharashtra Electricity Regulatory CommissionMSEB Maharashtra State Electricity BoardMSPGCL Maharashtra State Power Generation Company LimitedMT Metric TonnesMU Million Units

MERC, Mumbai Page 5 of 103

MW MegaWattMYT Multi Year TariffOEM Original Equipment ManufacturerO&M Operations and MaintenancePLF Plant Load FactorPLR Prime Lending RateR&M Repair and MaintenanceRH Re-heaterSH Super HeaterSHPs Small Hydel PlantsTVS Technical Validation SessionWPI Wholesale Price Index

MERC, Mumbai Page 6 of 103

1 BACKGROUND AND BRIEF HISTORYThis Order relates to the Petition filed by the Maharashtra State Power GenerationCompany Limited (MSPGCL) for approval of Annual Performance Review for FY2007-08 and tariff determination for FY 2008-09.

The Maharashtra State Power Generation Company Limited (MSPGCL or MahaGENCO) is a Company formed under the Government of Maharashtra GeneralResolution No. ELA-1003/P.K.8588/Bhag-2/Urja-5 dated January 24, 2005 witheffect from June 6, 2005 according to the provisions envisaged in the Electricity Act,2003 (EA 2003). MSPGCL has been registered with the Registrar of Companies,Mumbai under the Companies Act, 1956.

The provisional Transfer Scheme was notified under Section 131(5)(g) of the EA2003 on June 6, 2005, which resulted in the creation of following four successorcompanies and MSEB Residual Company, to the erstwhile Maharashtra StateElectricity Board (MSEB), namely,

§ MSEB Holding Company Ltd.,

§ Maharashtra State Power Generation Company Ltd.,

§ Maharashtra State Electricity Transmission Company Ltd. and

§ Maharashtra State Electricity Distribution Company Ltd.

MSPGCL is in the business of generation of electricity.

1.1 TARIFF REGULATIONS

The Commission, in exercise of the powers conferred by the Electricity Act, 2003,notified the Maharashtra Electricity Regulatory Commission (Terms and Conditionsof Tariff) Regulations, 2005, on August 26, 2005. These Regulations superseded theMERC (Terms and Conditions of Tariff) Regulations, 2004.

1.2 COMMISSION’S ORDER ON ARR AND TARIFF PETITION FOR FY2005-06 AND FY 2006-07

MSPGCL submitted its ARR and Tariff Petition for FY 2006-07 on February 10,2006. The Commission, in exercise of the powers vested in it under Sections 61 and62 of the Electricity Act, 2003, and all other powers enabling it in this behalf, and

MERC, Mumbai Page 7 of 103

after taking into consideration all the submissions made by MSPGCL, all theobjections, responses of MSPGCL, issues raised during the Public Hearing, and allother relevant material, issued the Order on the ARR Petition of MSPGCL for FY2005-06 and ARR and Tariff Petition of MSPGCL for FY 2006-07 on September 7,2006.

1.3 REVIEW PETITION ON TARIFF ORDER FOR FY 2006-07

MSPGCL filed a review Petition on the above said Commission’s Order. TheCommission disposed off the Review Petition through its Order dated December 7,2006, in Case 34 of 2006.

1.4 COMMISSION’S ORDER ON MYT PETITION FOR MSPGCL FOR FY2007-08 TO FY 2009-10

MSPGCL submitted its ARR and Multi Year Tariff (MYT) Petition for the firstControl period from FY 2007-08 to FY 2009-10 on January 2, 2007. TheCommission, in exercise of the power vested in it under Sections 61 and 62 of theElectricity Act, 2003, and all other powers enabling it in this behalf, and after takinginto consideration all the submissions made by MSPGCL, all the objections,responses of MSPGCL, issues raised during the Public Hearing, and all other relevantmaterial, issued the MYT Order for MSPGCL for the first Control Period, i.e., FY2007-08 to FY 2009-10, on April 25, 2007, which came into effect from April 25,2007, and the tariffs were valid upto March 31, 2008. As the Annual PerformanceReview for FY 2007-08 and Tariff determination for FY 2008-09 were under process,the various Utilities filed Petition for continuation of tariff determined for FY 2007-08till the time of issuance of the respective Tariff Orders of each Utility. Accordingly,the Commission in its Order on April 1, 2008 extended the applicability of theaforesaid Tariff Orders for the Utilities till the revised tariffs are determined for FY2008-09 under the APR framework and orders issued thereunder.

1.5 MSPGCL APPEAL WITH ATE AND ATE JUDGMENT

MSPGCL, in its APR Petition, submitted that it has preferred Appeals with theAppellate Tribunal for Electricity (ATE) on the true up of expenses for FY 2005-06and for relaxation of the norms prescribed by the Commission during the ControlPeriod, and submitted that the ATE is likely to issue the Order on the Appeals beforethe issuance of the Order on this APR Petition by the Commission. MSPGCLrequested the Commission to consider such directives from the ATE on the norms ofperformance and true-up of expenses while issuing the Order on APR Petition.

MERC, Mumbai Page 8 of 103

MSGPCL further requested the Commission to allow it to provide additionalinformation, if required, to comply with such directives from the ATE.

MSPGCL filed two Appeals before the Honourable Appellate Tribunal for Electricity(ATE), viz., Appeal No.s 86 of 2007 and 87 of 2007, on the Commission’s Orderapproving ARR and tariff Order for FY 2005-06 and FY 2006-07, and the MYTOrder for the first Control Period from FY 2007-08 to FY 2009-10, respectively.

MSPGCL challenged the Commission’s Order for FY 2005-06 and FY 2006-07 onthe issues of:

• Administrative and General expenses• Transit loss of coal• Station Heat Rate• Tariff for small hydro projects

MSPGCL challenged the Commission’s MYT Order on the issues of:• Truing up of the fuel expenses for FY 2005-06• Disapproval of A&G expenses• Truing up of depreciation• Truing up of other debits• Truing up of interest expenses and financing charges• Truing up of revenue earned• Transit loss of coal• Station Heat Rate• Auxiliary consumption of various stations• Specific oil consumption• O&M expenses for base year for MYT Period• Hydel tariff• Tariff for small hydro power station• Reactive energy charges• Normative O&M expenses for hydel plants• Employee incentive schemes

The ATE dealt with the above issues vide its Judgment dated April 10, 2008 inAppeal No.s 86 & 87 of 2007. The ATE’s ruling on various aspects raised inMSPGCL’s Appeals have been summarised below:

• ATE upheld MSPGCL’s appeal regarding actual A&G expenses for FY 2005-06 for truing up purposes and directed the Commission to true up the said

MERC, Mumbai Page 9 of 103

expenses based on actuals, subject to prudence check. ATE also directed theCommission not to consider the A&G expenses towards projects underconstruction as recoverable through tariff, since such expenses should becapitalised.

• ATE directed the Commission to consider the transit loss levels in terms of thestation-wise loss reduction trajectory approved by the Commission in its TariffOrder for FY 2003-04,.

• ATE directed the Commission to engage an appropriate agency/ies either onits own or through MSPGCL, to carry out a study in a time bound manner(preferably within three months) to reasonably assess the achievable heat rateof the plants owned by MSPGCL. Such agency may also be asked to suggestmeasures to improve the heat rates over a period of time. ATE further directedthe Commission to determine the heat rate based on the outcome of the studyand directed that the pre-existing tariffs may be continued, subject to truing upbased on the revised heat rates, when available.

• ATE directed the Commission to take into consideration the independent studyand reset the operating parameters, viz., transit loss of coal, station heat rate,auxiliary consumption, and specific oil consumption, and align its Regulationsby prescribing achievable norms and not merely ideal norms. ATE alsoadvised the Commission to be cautious that deliberate inefficiencies on thepart of the Utility are not passed on to the consumers.

• Regarding the tariff for small hydro power stations, the ATE stipulated thatfixed charge as determined by the Commission is subject to change only onaccount of re-determination of the lease rents payable to Government ofMaharashtra and change in the working capital on account of the change in theexpenses towards lease rentals.

• ATE rejected MSPGCL’s appeal for entitlement of higher tariff for smallhydro projects as the Commission’s Order in this regard is applicable only inthe case of new projects. The ATE also did not agree with MSPGCL’scontention that the Commission has disregarded the provisions of Section 61(h) of the Electricity Act, 2003 while considering the tariff fixation of smallhydro project.

• ATE upheld MSPGCL’s appeal for monthly billing of the incentives and heldthat any under or over recovery on account of such claims may be adjusted onmonthly basis

• ATE upheld MSPGCL’s appeal as regards truing up of actual fuel expensestill such time the re-assessed improvement trajectory of parameters isavailable.

MERC, Mumbai Page 10 of 103

• ATE upheld MSPGCL’s appeal as regards truing-up of depreciation, whileruling that if the Commission has allowed any extra recovery in the past underthe head of depreciation, the same may be adjusted.

• ATE, while allowing the truing of other debits, held thato Both, MSPGCL and the consumers may bear the burden on this

account, and hence, the sum to be recovered from the consumers maybe spread over a period of three years, without any interest, to lessenthe burden on the consumers. However, the above cannot be taken as aprecedent for making similar claims in the future.

o Agreed with the Commission’s observation on the material costvariance of Rs 0.36 Crore

o Directed the Commission to examine the claim of MSPGCL for truingup on account of miscellaneous losses & write off, sundry expenses,intangible assets written off and intangible assets interest charges forHVDC, subject to prudence check.

• ATE directed the Commission to consider the interest on working capitalcomputed on normative basis for FY 2005-06 truing up and if any interest onshort-terms loans has been allowed which are in the nature of working capital,the same should be disallowed

• As regards truing of other income, the ATE ruled that if the other incomecannot be reasonably linked to any cost item allowed by the Commission as apart of the ARR, the same should not be adjusted against the ARR ofMSPGCL.

• ATE held that the Commission has considered MSPGCL’s estimates of O&Mexpenses for FY 2006-07 and also allowed escalation at the rate of 5.38%,which results into deviation from norms in favour of MSPGCL. ATE directedMSPGCL to take up the claim for base O&M expense for FY 2006-07.

• ATE directed the Commission to devise a mechanism which addresses theconcern of peak and off peak generation, by determining the ratio of peak andoff-peak generation after taking into consideration the operational capacity ofMSPGCL and system pattern, and also meets the objective of the Commissionto send economic signal about pricing of hydel generation.

• ATE held that since MSPGCL is incurring additional expenditure withoutbeing compensated, for extending support for reactive energygeneration/absorption for grid stability, the Commission should either workout a scheme specifically for State power generators for compensation forincurring the additional expenditure or extend the incentive/penalty

MERC, Mumbai Page 11 of 103

mechanism available for transmission licensees, distribution licensees andopen access users, to the State generators.

• ATE rejected MSPGCL’s request to set aside the norm for O&M expenses setby the Commission for old hydel plants and ruled that since the existing hydroelectric plants are not covered by the Policy of the Government it will beinappropriate to compare the O&M expenses of the existing plants with that ofthe new hydel stations covered under Regulations.

• ATE directed the Commission to consider the issue of employee incentiveschemes in accordance with law.

The ATE, in view of the above findings/observations, set aside the impugnedTariff Orders and allowed the appeals partially, and remitted the matter back tothe Commission for re-determination of the tariff for MSPGCL.

As ATE has set aside the Commission’s Order dated September 7, 2006 onMSPGCL’s ARR and Tariff Petition for FY 2005-06 and FY 2006-07 andCommission’s Order dated April 25, 2007 on MSPGCL’s MYT Petition for thefirst Control Period from FY 2007-08 to FY 2009-10, the Commission askedMSPGCL to submit the impact of the ATE Judgement for each year separatelyalongwith appropriate reasons and justification as follows:

• Impact on Truing up of Revenue and Expenses for FY 2005-06• Impact on Truing up of Revenue and Expenses for FY 2006-07• Impact on Revised estimates of expenses for FY 2007-08• Impact on Projected Expenses for FY 2008-09

Further, in order to implement the directions given by ATE in its Order onproposed treatment towards certain heads of expenses and revenue and asrequested by MSPGCL in its Petition, the Commission asked MSPGCL to submitthe additional information/clarifications related to following heads of expensesand revenue:

i. Actual A&G Expenses for FY 2005-06 and A&G expenses incurred in FY2005-06, FY 2006-07 and FY 2007-08 incurred in respect of projectsunder construction

ii. Interest on Working Capital for FY 2005-06iii. Expenses on Intangible Assets, Sundry Expenses, etc., during FY 2005-06iv. Non Tariff Income for FY 2005-06v. Reactive Power Injection into the system during FY 2006-07vi. GFA and Depreciation details for FY 2005-06

MERC, Mumbai Page 12 of 103

MSPGCL vide its letter Ref. SE/RC/BD/07450 dated May 29, 2008 has submittedthe impact of the ATE Judgement for each year separately and the reply to someof the queries sought by the Commission under certain heads of expenses andrevenue.

The Commission is of the view that as the Orders of the Commission have beenset aside and the ATE in its Order has directed the Commission to re-determinethe tariff, and as the original Orders in both the cases, i.e., ARR and TariffDetermination for FY 2006-07 and MYT Order for the first Control Period, i.e.,FY 2007-08 to FY 2009-10 were issued after following the due public processincluding public hearing, the re-determination of ARR and tariff for MSPGCLneeds to be undertaken after following the due public process including publichearing. The Commission will initiate a separate process for re-determination oftariff for MSPGCL for FY 2005-06, 2006-07 and FY 2007-08. However, thisOrder has to be issued, since the tariff payable to MSPGCL is a major input costto MSEDCL, and the Order of MSEDCL cannot be delayed till such time thecomplete data is submitted by MSPGCL and the due regulatory process isfollowed to revise the tariff of MSPGCL.

As regards norms for performance parameters, viz., transit loss of coal, stationheat rate, auxiliary consumption, and specific oil consumption of MSPGCL’sgenerating stations, ATE directed the Commission to undertake an independentstudy, either through MSPGCL or on its own, and reset the operating parametersand align its Regulations by prescribing achievable norms and not merely idealnorms after taking into consideration the results of such independent study. ATE,in its Order, has also mentioned that till such time the Commission re-determinesthe Station Heat Rate, MSPGCL may continue with the pre-existing tariff, subjectto truing up when revised Station Heat Rates when available. The Commission,abiding by the directions of ATE, will engage an appropriate independent agencyto carry out independent study to reasonably assess the achievable performance ofMSPGCL stations and to suggest the measures to improve the performance over aperiod of time. Based on the outcome of the study, the Commission will re-determine the performance parameters of MSGPCL’s generating stations, whetherhigher or lower than the norms stipulated in the Tariff Regulations and normsapproved in the Tariff Orders, and will carry out the truing up of MSPGCL’sexpense and revenue based on re-determined performance parameters.

MERC, Mumbai Page 13 of 103

Further, the impact of directions of ATE in respect of following heads of expensesand revenue needs to be assessed based on additional information/clarifications:

• A&G Expenses• Truing up of Depreciation for FY 2005-06• Truing up of Other Debits for FY 2005-06• Truing up of Interest and Finance Charges for FY 2005-06• Truing up of Revenue earned in FY 2005-06• Truing up of non-tariff income earned in FY 2005-06 and FY 2006-07• Compensation for Reactive Energy generation.

The Commission, in its Order dated April 25, 2007 on MYT Petition for the firstControl Period, has already undertaken the final truing up of expenses andrevenue for FY 2005-06. However, consequent to ATE Order, the truing up ofexpenses and revenue for FY 2005-06 will have to be undertaken againconsidering the ATE’s directions and based on impact and additionalinformation/clarifications submitted by MSPGCL. The Commission is of the viewthat it will be preferable to carry out the truing up of all elements of expenses andrevenue for FY 2005-06 once again based on impact of truing up and additionalinformation/clarifications from MSPGCL and after following due public process.The Commission has therefore not undertaken the truing up of expenses andrevenue for FY 2005-06 again in this Order. The Commission, after following thedue public process, will issue an Order which will deal with the truing up of allthe elements of expenses and revenue for FY 2005-06.

The truing up of expenses and revenue for FY 2005-06 will have certainimplications on ARR for FY 2006-07 and for subsequent years. The O&Mexpenses for FY 2005-06 approved after truing up, will have a bearing onallowable O&M expenses in subsequent years’. Similarly, the truing up ofdepreciation for FY 2005-06 may have effect on depreciation expenses to beallowed for FY 2006-07 and subsequent years. As regards truing up of fuelexpenses for FY 2006-07, the Commission is of the view that MSPGCL hasalready recovered variation in fuel prices through the FAC mechanism and truingup of fuel expenses on account of variation in performance parameters has to beexamined based on approved performance parameters upon completion of studyby independent agency. The Commission, in this Order, has therefore undertakenthe truing up of certain expenses and revenue for FY 2006-07. The Commissionwill undertake the final truing up of expenses and revenue for FY 2006-07 along

MERC, Mumbai Page 14 of 103

with truing up of expenses and revenue for FY 2005-06 and re-determination ofperformance parameters.

In addition, the Commission in this Order has carried out the Annual PerformanceReview for FY 2007-08 and determined the tariff for FY 2008-09.

1.6 PETITION FOR ANNUAL PERFORMANCE REVIEW FOR FY 2007-08AND TARIFF DETERMINATION FOR FY 2008-09

As per the MERC Tariff Regulations, application for the determination of tariff isrequired to be made to the Commission not less than 120 days before the date fromwhen the tariff is intended to be made effective. The Commission had directedMSPGCL to submit the Petition for Annual Performance Review latest by November30 of each year in line with the Regulation 9.1 of the Tariff Regulations.

MSPGCL submitted its Petition for Annual Performance Review for FY 2007-08 andtariff determination for FY 2008-09 on November 30, 2007, based on actual auditedexpenditure for FY 2006-07, actual expenditure for first half of FY 2007-08, i.e.,from April to September 2007 and revised estimated expenses for October 2007 toMarch 2008, and projections for FY 2008-09. MSPGCL, in its Petition, requested theCommission to

• Undertake truing up for FY 2006-07 based on actual audited data;• Undertake Annual Performance Review for FY 2007-08;• Consider the revised projections for FY 2007-08 and approve the ARR for FY

2008-09 in accordance with the submissions and rationale given in thePetition;

• Approve the revised ARR and tariff for FY 2008-09;• Recover the revenue gap, if any, in FY 2006-07 on account of applicability of

the MYT Order from April 25, 2007 instead of April 1, 2007.

The Commission, vide its letter dated December 12, 2007, forwarded the preliminarydata gaps and information required from MSPGCL. MSPGCL submitted its replies topreliminary data gaps and information requirement on December 24, 2007.

The Commission held a Technical Validation Session (TVS) on MSPGCL’s APR forFY 2007-08 and Tariff Petition for FY 2008-09, on December 26, 2007, in thepresence of authorised Consumer Representatives. The list of individuals, whoparticipated in the TVS, is provided at Appendix-1. During the TVS, the Commission

MERC, Mumbai Page 15 of 103

directed MSPGCL to provide additional information and clarifications on the issuesraised during the TVS. The Commission also directed MSPGCL to submit the draftPublic Notice in English and Marathi in the format prescribed by the Commission.

1.7 ADMISSION OF PETITIONS AND PUBLIC PROCESS

MSPGCL submitted its responses to the queries raised during the TVS, on January 9,2008, and the Commission admitted the APR Petition of MSPGCL on January 10,2008.

In accordance with Section 64 of the EA 2003, the Commission directed MSPGCL topublish its application in the prescribed abridged form and manner, to ensure publicparticipation. The Commission also directed MSPGCL to reply expeditiously to allthe suggestions and comments received from stakeholders on its Petition. MSPGCLissued the Public Notice in newspapers inviting comments/suggestions fromstakeholders on its APR Petition. The Public Notice was published in The Times ofIndia, Indian Express, Loksatta and Samana newspapers on January 12, 2008 andrevised Public notice was published on January 27 2008. The copies of MSPGCL'sPetitions and its summary were made available for inspection/purchase to members ofthe public at MSPGCL's offices and on MSPGCL's website (www.mahagenco.in) andalso on the web site of the Commission (www.mercindia.org.in) in downloadableformat. The Public Notice specified that the suggestions/objections, either in Englishor Marathi, may be filed in the form of affidavit along with proof of service onMSPGCL.

The Commission received written objections expressing concerns on proceduralissues, quantum of generation, etc. The Public Hearing originally scheduled onFebruary 4, 2008 was held on February 13, 2008 at 11:00 hours at Vista Hall, 30th

Floor, Centre 1, World Trade Centre, Cuffe Parade, Mumbai-400 005. The list ofobjectors, who participated in the Public Hearing, is provided in Appendix- 2.

The Commission ensured that the due process, contemplated under the law to ensuretransparency and public participation was followed at every stage meticulously andadequate opportunity was given to all the persons concerned to file their say in thematter.

This Order deals with the Annual Performance Review of FY 2007-08 and tariffdetermination of generating stations of MSPGCL for FY 2008-09. Various objectionsthat were raised on MSPGCL’s Petition after issuing the public notice both in writing

MERC, Mumbai Page 16 of 103

as well as during the public hearing, along with MSPGCL’s response andCommission’s rulings have been detailed in Section 2 of this Order.

1.8 ORGANISATION OF THE ORDER

This Order is organised in the following six Sections:

• Section 1 of the Order provides a brief history of the quasi-judicial regulatoryprocess undertaken by the Commission. For the sake of convenience, a list ofabbreviations with their expanded forms has been included.

• Section 2 of the Order lists out the various objections raised by the objectors inwriting as well as during the Public Hearing before the Commission. The variousobjections have been summarized, followed by the response of MSPGCL and therulings of the Commission on each of the points.

• Section 3 of the Order details the MSPGCL’s proposal on truing up of expensesand revenue for FY 2006-07

• Section 4 of the Order details the performance parameters as approved by theCommission in MYT Order for first Control Period and MSPGCL’s proposal forperformance parameters during FY 2007-08 and FY 2008-09.

• Section 5 of the Order comprises the review of performance for FY 2007-08(including provisional truing up) and the Commission's analysis on variouscomponents of Energy Charges and Annual Fixed Charges of MSPGCL’s Stationsfor FY 2008-09.

• Section 6 of the Order details the tariff design for MSPGCL’s Stations and theapproved Annual Fixed Charges and Energy Charges for FY 2008-09.

MERC, Mumbai Page 17 of 103

2 OBJECTIONS RECEIVED, MSPGCL’s RESPONSEAND COMMISSION’S RULING

2.1 PROCEDURAL ISSUES

Shri Rakshpal Abrol and others quoted the provisions of Regulation 90 (a) of MERC(Conduct of Business) Regulations, 2004, and submitted that adequate time of threeweeks as stipulated in the Regulations were not provided to the public to study thedocuments and submit the responses. They added that the Commission has notfollowed Regulations 8.4, 9.1 and 11.1 of the MERC (Terms and Conditions ofTariff) Regulations, 2005.

The Sidhpura Co-Operative Industrial Estate Ltd. submitted that no tariff or part oftariff may ordinarily be amended more frequently than once in any financial year,except in respect of any changes expressly permitted under the terms of any fuelsurcharge formula as specified in Regulation 82 of MERC (Terms and Conditions ofTariff) Regulations, 2005.

MSPGCL ResponseMSPGCL submitted that the format of Public Notice was provided and approved bythe Commission and it has followed the directives issued by the Commission fromtime to time.

Commission s RulingAs mentioned in Section 1 of the Order, MSPGCL submitted its Petition for AnnualPerformance Review for FY 2007-08 and tariff determination for FY 2008-09 for itsGeneration business on November 30, 2007. The Commission communicated the datagaps in the Petition and held a Technical Validation Session on MSPGCL’s Petition,in the presence of authorised Consumer Representatives. Upon submission of revisedPetition by MSPGCL incorporating the additional information and replies to queriesraised by the Commission, the Petition was admitted for further public process onJanuary 10, 2008. The Commission directed MSPTCL to host the detailed RevisedAPR Petition and formats in MS Excel on its website for easy download by interestedstakeholders.

The Public Notice was published on January 12, 2008 in leading newspapers and thepublic hearing was originally scheduled to be held on February 4. Considering therequests made by the stakeholders for additional time, the Commission postponed the

MERC, Mumbai Page 18 of 103

Public Hearing, which was finally held on February 13, 2008. Thus, adequate time, asenvisaged under the Regulations has been provided to stakeholders to submit theirviews/suggestions before the Public Hearing, and additional time of 7 days was alsoprovided to file rejoinders.

As regards determination of tariff on annual basis, the Commission in its MYT Orderfor MSPGCL dated April 25, 2007 has approved the Annual Fixed Charges andtrajectory of performance parameters for MSGPCL stations for the Control Periodfrom FY 2007-08 to FY 2009-10, while the tariff was determined for FY 2007-08only, in accordance with Regulation 20.1 of the MERC (Terms and Conditions ofTariff) Regulations, 2005, which stipulates that the tariff will be determined on anannual basis. Hence, in this Order, the Commission is approving the tariff ofMSPGCL stations for FY 2008-09. The Commission would like to clarify that thetariff of MSPGCL stations for FY 2007-08 was approved in MYT Order and tariff ofMSPGCL stations for FY 2007-08 is being approved in this Order. Thus, the tariff isnot amended more frequently than once a year.

2.2 POWER GENERATION

Shri George John submitted that the net generation indicated in the APR Petition filedby MahaGenco does not give the details for gas power station, power purchased, totalpower sold and T&D losses. Shri George John pointed out that the figures for FY2004-05 and FY 2005-06 should also be provided in the Petition.

MSPGCL’s response

MSPGCL responded that the net generation from Thermal Plant (Coal based) andThermal (Gas Based) for three years is given as under:

ThermalGeneration( MU)

FY 2006-07Actual

FY 2007-08Estimated

FY 2008-09Projected

Coal Based 37494 38939 38807Gas Based 4028 3737 3939Total Thermal 41522 42676 42746

MSPGCL further clarified that as a Generation Company, MSPGCL does notpurchase any power and Transmission & Distribution (T&D) losses do not pertain tothe Generation Company.

MERC, Mumbai Page 19 of 103

Commission s RulingThe Commission would like to clarify this Petition relates to determination ofGeneration Tariff for MSPGCL’s stations for sale of power to MSEDCL. The issuesrelated to total power purchase, net energy sold and distribution losses are included inMaharashtra State Electricity Distribution Company Limited’s (MSEDCL) APRPetition. As regards providing generation data for FY 2004-05 and FY 2005-06, asper APR formats issued for submitting the information, the Generating Company hasto submit information for previous year (based on actual performance), current year(based on actual performance for first six months and estimated performance for nextsix months) and projected performance for ensuing year.

2.3 FUELShri G.P. Misra submitted that the revenue losses due to “Unburnt Fuel EnergyLosses through exhaust” in power generation should be addressed in separate table.

MSPGCL’s response

MSPGCL has not responded to this objection.

Commission s RulingMSPGCL has submitted the information with respect to performance parameters andvarious elements of cost and revenue in accordance with the provisions of MERC(Terms and Conditions of Tariff) Regulations, 2005 and formats prescribed forsubmitting the information. Further, the Commission does not find any merit in thesuggestion made by the objector, as the above aspect gets addressed in the StationHeat Rate.

MERC, Mumbai Page 20 of 103

3 TRUING UP OF ANNUAL REVENUE REQUIREMENTFOR FY 2006-07

MSPGCL, in its Petition for Annual Performance Review for FY 2007-08 anddetermination of revenue requirement and tariff for FY 2008-09, has included asection on the final truing up of expenditure for FY 2006-07 based on actualexpenditure as per Audited accounts. MSPGCL provided the comparison of actualexpenditure against each head with the expenditure approved by the Commissionalong with the reasons for deviations.

Further, the Commission has stipulated in its Order dated September 7, 2006, that thegains and losses on account of controllable and uncontrollable factors will be sharedbetween the Generating Company and the Licensee at the time of truing up of ARRbased on actuals, in accordance with Regulation 19 of the MERC (Terms andConditions of Tariff) Regulations, 2005. As discussed in Section 1, the Commissionwill carry out the final truing up of expenses and revenue for FY 2006-07 throughseparate proceedings in the context of the ATE Judgment. Hence, the Commissionwill carry out the sharing of gains and losses on account of controllable anduncontrollable factors alongwith final truing up of expenses and revenue for FY 2006-07.

3.1 FUEL COSTS

MSPGCL, in its Petition, has submitted that the total actual fuel cost for FY 2006-07as per audited accounts was Rs. 5565.22 Crore as against the Commission approvedamount of Rs 5054.95 Crore. MSPGCL submitted that the increased fuel costs arelargely on account of expenditure on other variable charges (including water,chemical, lubricants etc.), variation in performance parameters, poor quality of coaland higher transit losses.

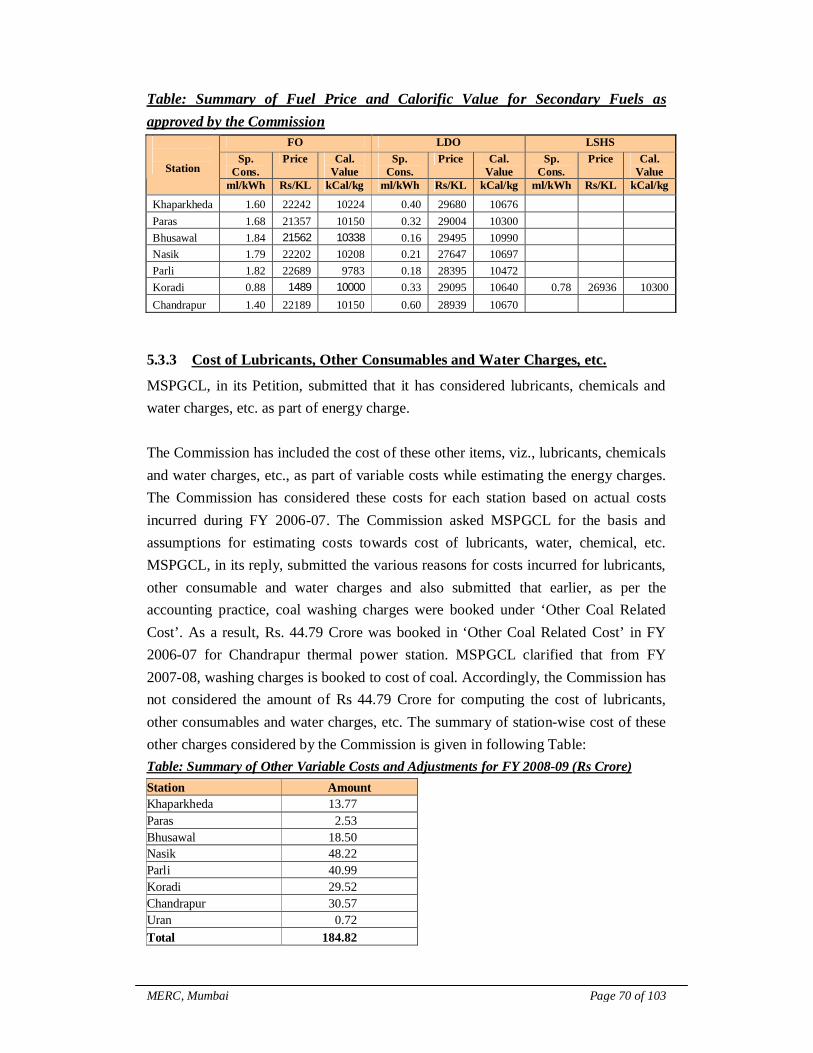

3.1.1 Other Variable Charges

MSPGCL submitted that the main variation in fuel expenses is due to non-consideration of other charges such as lubricants, chemicals, water charges, etc.,pursuant to change of Fuel and Other Costs Adjustment (FOCA) mechanism to FuelAdjustment Cost (FAC) mechanism. MSPGCL further submitted that the Commissionhas considered such charges while truing up of fuel costs for FY 2005-06 and hasincluded such expenses in the variable cost of generation in the MYT Order.

MERC, Mumbai Page 21 of 103

MSPGCL sought true-up of the expenses on such other variable charges for FY 2006-07 to the tune of Rs 229.42 Crore.

The summary of such expenses are provided in the Table below:

Table : Break-up of other fuel related expenses (Rs Crore)S. No. Particulars Amount

1. Other Fuel Related Costs 110.22. Verification of Coal Stock 8.33. Stock Shortages on Physical Verification of Oil Stock 0.04. Excess found on physical verification of fuel stock – oil -0.05. Cost of Water 82.66. Lubricants & Consumable Stores 23.67. Station Supplies 4.9

Total 229.6

The Commission asked MSPGCL to submit the details of the other fuel related costs.MSPGCL submitted the details under various sub heads like charges for coal handlingcontract charges, demurrage on coal wagons, siding charges, penalties foroverloading, commission to agents, payments to railway staff posted at powerstations, coal stock maintenance cost, other coal related cost, oil handling contractcharges and demurrage on oil tankers. MSPGCL submitted that in case ofChandrapur station, an amount of Rs 44.79 Crore pertaining to other coal related costshas been booked, which corresponds to coal washing charges, which the station hasinadvertently booked under a wrong head in FY 2006-07 and the washing chargeswere not included in the fuel expenses for the station.

3.1.2 Performance Parameters

MSPGCL submitted that increase in the fuel cost is on account of increased stationheat rate as compared to norms approved by the Commission in its Tariff Order forFY 2006-07. MSPGCL submitted that the actual heat rate achieved by the generatingstations of the MSPGCL have not deviated much from the estimated heat rate valuesas submitted in its Petition for FY 2006-07.

3.1.3 Heat Rate

The actual heat rate achieved during FY 2006-07 for all the sations exceptKhaperkheda was higher as compared to the heat rate approved by the Commission inthe Tariff Order for FY 2006-07. MSPGCL further submitted that as regard to thedeviation between heat rate especially for Bhusawal, Nasik, Parli and Chandrapur, theCommission in its MYT Order had approved revised levels of heat rate for FY 2007-

MERC, Mumbai Page 22 of 103

08 based on a comparative exercise with plants of similar vintage operating elsewherein the country.

The summary of Station-wise heat rate approved in the Order and actual heat rate forFY 2006-07 is given in the following Table:

Table: Heat Rate kcal / kWh)Particulars FY 2006-07Gross Generation (MU) Tariff Order ActualsKhaparkheda 2644 2612Paras 3105 3261Bhusawal 2561 2666Nasik 2584 2672Parli 2573 2678Koradi 2907 2997Chandrapur 2480 2600Uran Gas 1950 1969

3.1.4 Secondary Fuel Oil Consumption

The Commission, in its Order on ARR and Tariff Petition for FY 2006-07, approvedthe station-wise secondary oil consumption of 2 ml/kWh based on the normativesecondary fuel oil consumption of 2 ml/kWh specified in the Tariff Regulations.,MSPGCL submitted that the actual secondary fuel consumption utilised during FY2006-07 is different from the norm of 2 ml/kWh. The summary of actual secondaryfuel oil consumption for FY 2006-07 and that approved by the Commission in theTariff Order for FY 2006-07 is given in the following Table:

Table: Secondary Fuel Oil Consumption ( ml/ kWh)Particulars FY 2006-07

Specific Oil Consumption(ml/kWh) Tariff Order Actuals

Khaparkheda 2.00 0.70Paras 2.00 1.41Bhusawal 2.00 4.04Nasik 2.00 2.41Parli 2.00 3.05Koradi 2.00 2.74Chandrapur 2.00 0.97

MSPGCL submitted that the quality of coal received by the stations primarily belongsto Grade D, E and F with calorific value ranging from 4900 to 2400 kcal/kg, which issignificantly lower than the design Gross Calorific Value (GCV) of coal, which isroughly in the range of around 5000 kcal/kg. MSPGCL also submitted that the ashcontent in such coal ranges from 35% to 45 % or even greater at times leading to

MERC, Mumbai Page 23 of 103

either burning of excess coal or excess use of secondary oil for flame stabilisation,thus increasing the heat rate of the stations. Further, it was submitted that the situationworsens during the rainy season, as the coal received by the stations is from open castmines and the coal becomes muddy and wet in such seasons resulting in drop in boilerefficiency considerably resulting in deterioration of heat rate. Also, excess coal needsto be burnt in such a case, which requires increased air flow resulting in high dry fluegas losses.

MSPGCL submitted that the Commission had approved a transit loss of 0.8% for allits power stations. MSPGCL contended that it has no control over the loss duringtransit of coal and therefore, has a limited role to control the same and the actualtransit loss during FY 2006-07 have been more than 0.8% for majority of its stations,and requested the Commission to consider the actual transit loss for truing uppurposes of fuel cost.

MSPGCL submitted that it is inappropriate to calculate fuel cost consideringnormative levels of plant performance, because these are theoretically calculatedlevels, which do not consider the practical problems faced by the generating stations.

The summary of station wise total fuel cost as approved in the Order and actual fuelcost is given in the following Table:Table Fuel Costs (Rs Crore)Particulars FY 2006-07Fuel Cost (Rs Crore) Tariff Order ActualsKhaparkheda 620.36 661.49Paras 52.12 57.08Bhusawal 406.52 480.81Nasik 970.30 997.65Parli 654.43 657.76Koradi 746.44 794.65Chandrapur 1318.37 1379.46Uran Gas 286.42 306.00Sub-Total 5054.96 5334.91Other Fuel Cost 0.00 229.61Total Fuel Cost 5054.96 5564.52

As discussed in Section 1, the Commission is of the view that MSPGCL has alreadyrecovered variation in fuel prices through FAC mechanism. Moreover, truing up offuel expenses on account of variation in performance parameters has to be examinedbased on re-determined performance parameters after completion of study by theindependent agency. Regarding other variable charges of Rs 229.6 Crore, as the same

MERC, Mumbai Page 24 of 103

was not included as part of fuel costs in the original Order due to change ofmechanism from Fuel and Other Cost Adjustment (FOCA) to Fuel Adjustment Cost(FAC), the Commission approves the actual amount of other variable charges of Rs229.6 Crore for FY 2006-07.

3.1.5 Operation & Maintenance Expenses

MSPGCL submitted that the Commission had approved the O & M expenses of Rs817.58 Crore in its Order for FY 2006-07, for the existing stations of MSPGCL. TheCommission had not provided the break-up of O & M expenses as Employeeexpenses, Administration & General expenses and Repairs and MaintenanceExpenses. MSPGCL submitted that as per the Audited accounts for FY 2006-07, theactual expenditure on O & M is Rs 854.45 Crore and submitted the following break-up:

Table: Details of O & M expenses (in Rs Crore) in 2006-07Particular Gross

ExpensesCapitalization Net Expenses

Employee Expenses 434.28 86.14 348.15A & G Expenses 54.58 7.05 47.53Repairs & Maintenance Expenses 459.25 0.47 458.78Total O & M Expenses 948.12 93.66 854.45

MSPGCL requested the Commission to kindly consider the O & M expenses as perAudited accounts for truing up purposes. MSPGCL submitted that it has relied on thejudgment of ATE (Appeal No. 251 of 2006/ Order dated April 4, 2007), wherein theATE has upheld the Appeal filed by Reliance Energy Limited regarding the allowanceof the Employee expense and A&G expense based on actual audited figures for FY2004-05 and FY 2005-06. MSPGCL also submitted that the ATE in its judgement inAppeal No 76 of 2007 had directed the Commission to allow the A&G expenses asper accounts subject to prudence check.

As regards the Repairs and Maintenance expenses, the Commission in its MYT orderhad made the following comments on such expenditure for 2006-07:

“ …..Actual Repair and Maintenance expenditure as given by MSPGCL aregiven in the Table below:

Spent uptoNov 06

Expenditure inDec 06

Total Expenditure inQ1,Q2,Q3

Projected expenditure inFY 2006-07

311.89 36.35 348.23 464.31

MERC, Mumbai Page 25 of 103

Based on the actual expenditure incurred by MSPGCL as per details given byMSPGCL, it is projected that MSPGCL may spend Rs. 464 crore, i.e., 90 % ofthe proposed expenditure up to March 31, 2007. Further, considering that onan average, at least around 20 % of the expenditure is meant for upgradation,modernization, high cost insurance spares, etc., which are of capital nature,the actual expenditure on Repairs and Maintenance in FY 2006-07 isestimated at Rs. 370 crore, which works out to approximately 73 % ofMSPGCL’s proposal of Rs 508.64 Crore. This also amounts to a 12% increaseover the actual R&M expenditure booked by MSPGCL in FY 2005-06, whichcould also include expenditure of capital nature. Considering the aboveaspects, the Commission has not considered the truing up of R&M expensesfor FY 2006-07 at this stage. In order to have a clear picture regardingRepairs and maintenance expenditure, MSPGCL should maintain a cleardemarcation of capital expenditure and revenue expenditure heads, andsubmit Capital expenditure proposals for Renovation and Modernisationschemes, for the Commission’s approval. The Commission considering theaspects discussed above will consider the actual R&M Expenses based onaudited accounts for FY 2006-07 subject to prudence check at the time ofAnnual Performance Review for FY 2007-08, and based on clear segregationof capital related expenditure and revenue expenditure.”

MSPGCL submitted that the Commission in its MYT Order had opined that the true-up on Repairs and Maintenance expenses for FY 2006-07 shall be done on the basisof audited accounts subject to prudency check. As regards the separation ofexpenditure of capital nature from the repairs and maintenance expenditure, MSPGCLsubmitted that since the Order for MYT was issued on April 25, 2007, much after theyear under consideration i.e. FY 2006-07, it was therefore not possible to streamlinethe internal accounting principles on a retrospective basis. However, going forwardfrom FY 2007-08 onwards the MSPGCL submitted that it has implemented separatebooking of capital related expenditure in the manner directed by the Commission.

Accordingly, MSPGCL requested the Commission, to consider the O&M expenses asper the audited accounts and allow a true up of 36.87 Crore in O&M expenses for FY2006-07.

As discussed in Section 1, as the Commission will undertake the truing up of O&Mexpenses for FY 2005-06 and FY 2006-07 including A&G expenses through a

MERC, Mumbai Page 26 of 103

separate process, the Commission in this Order has not carried out the truing up ofO&M expense for FY 2006-07, since the final truing-up cannot be undertaken twice.

3.2 DEPRECIATION

The Commission, in its earlier Order dated September 7, 2006 (Case 48 of 2005), hadpermitted depreciation to the extent of Rs 187.06 Crore for FY 2006-07, whichamounts to 1.98% of Opening level of Gross Fixed Assets (GFA) of MSPGCL for FY2006-07, which was stated at Rs 9444 Crore. The depreciation rates were consideredas prescribed under MERC (Terms and Conditions of Tariff) Regulations, 2005. Inthe absence of station-wise depreciation computation from MSPGCL, theCommission had determined the station-wise depreciation amount by spreading theunaccounted depreciation of each station (limited to 90% of GFA) over its remaininglife. For determining the life of the station, weighted average life (on the basis ofcapacity) of the units had been considered.

However, subsequently under its MYT petition, MSPGCL furnished station-wisecomputation of the depreciation. MSPGCL, under its APR Petition, submitted actualdepreciation expenses incurred for FY 2006-07 as Rs 337.55 Crore, at an overalldepreciation rate of 3.50% corresponding to opening GFA of Rs 9641.99 Crore.

The Commission has examined the depreciation and actual capitalisation claimed byMSPGCL in detail as against the various capex schemes approved by theCommission. The Commission has noted that the actual Opening level of GFA for FY2006-07 amounts to Rs 9641.99 Crore as against Rs 9444 Crore considered by theCommission in its earlier Tariff Order. The Commission has verified the same withaudited financial statements of MSPGCL. Accordingly, for the purposes of true-upexercise for FY2006-07, the Commission has considered opening GFA for MSPGCLat Rs 9641.99 Crore as claimed by MSPGCL, as per its audited accounts. Further,MSPGCL in its additional submissions confirmed that depreciation has not beenclaimed beyond 90% of the asset value in line with the Tariff Regulations. Thedepreciation expenses approved by the Commission for FY 2006-07 has beensummarised in the following Table:

Table: Depreciation (Rs Crore)Particulars Tariff Order Actuals Allowed after truing up

Depreciation 187.06 337.55 337.55Opening GFA 9444.00 9641.99 9641.99Depreciation Rate 1.98% 3.50% 3.50%

MERC, Mumbai Page 27 of 103

Though, the Commission has carried out truing up of depreciation for FY 2006-07 inthis Order based on details submitted by MSPGCL, it may be noted that as discussedin Section 1, the truing up of depreciation for FY 2005-06 is to be undertaken througha separate process based on the data to be submitted by MSPGCL, and may have animpact on depreciation for FY 2006-07. Therefore, the Commission will carry out thefinal truing up of depreciation for FY 2006-07 alongwith the final truing up ofexpenses and revenue for FY 2005-06 and FY 2006-07 through a separate process.

3.3 ADVANCE AGAINST DEPRECIATION

MSPGCL sought approval for advance against depreciation in line with the conditionsstipulated under the Commission’s Tariff Regulations. Further, MSPGCL submittedthat since the Commission is determining the tariff separately for individual powerstations, hence, it may be allowed the advance against depreciation based on loanrepayment vis-à-vis the depreciation for individual stations. MSPGCL furthersubmitted that the loan repayment exceeds the depreciation as per the Commission’snorms by Rs 116.54 Crore (Rs 96.52 crore in case of Khaperkheda and Rs 20.01Crore in case of Koradi Thermal power Station). Accordingly, it has claimed totalAdvance against depreciation for FY 2006-07 at Rs 120.53 Crore.

As per Regulation 32.3 of MERC (Terms and Conditions of Tariff) Regulations,2005, where the actual amount of loan repayment in any financial year exceeds theamount of depreciation allowable under Regulation 34.4.1, the generating companyshall be allowed an advance against depreciation for the difference between the actualamount of such repayment and the allowable depreciation for such financial year.

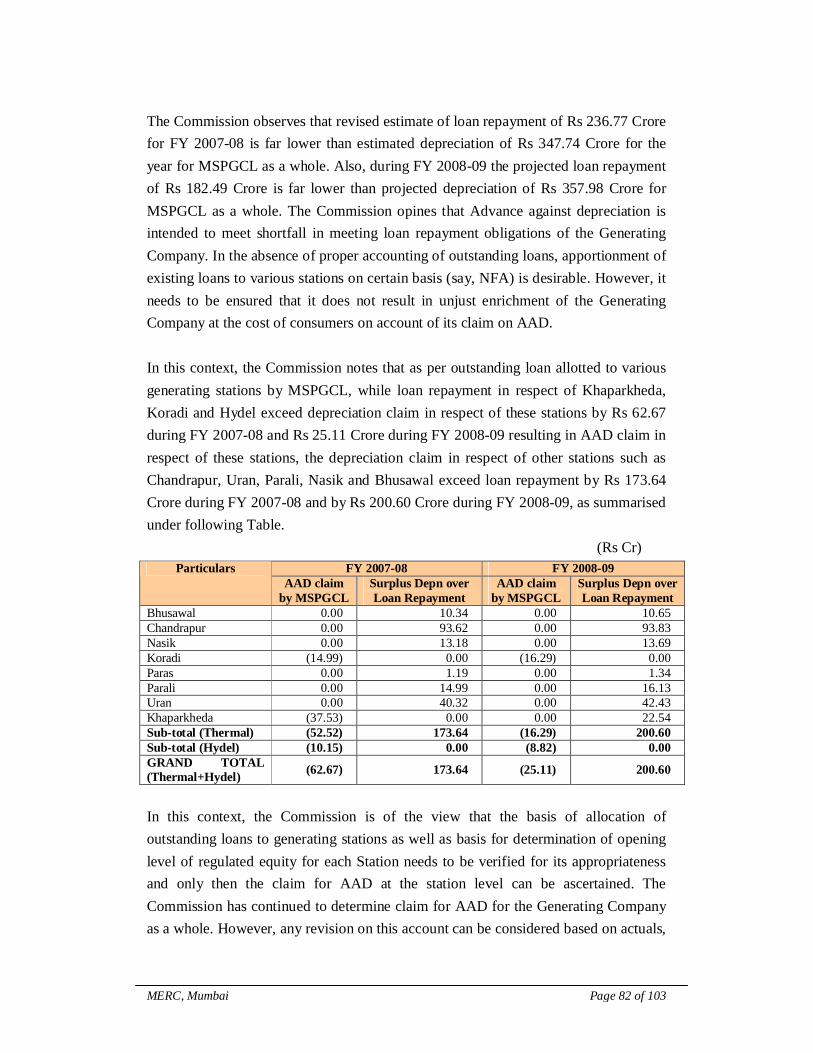

The Commission observes that actual loan repayment of Rs 269.62 Crore for FY2006-07 does not exceed actual depreciation of Rs 337.55 Crore for the year forMSPGCL as a whole. The Commission opines that Advance against depreciation isintended to meet shortfall in meeting loan repayment obligations of the GeneratingCompany. In the absence of proper accounting of outstanding loans, apportionment ofexisting loans to various stations on certain basis (say, NFA) is desirable. At the sametime, it needs to be ensured that allowing advance against depreciation does not resultin unjust enrichment of the Generating Company at the cost of consumers on accountof its claim on AAD.

In this context, the Commission notes that as per outstanding loan allocated to variousgenerating stations by MSPGCL, while loan repayment in respect of Khaprkheda,Koradi and hydel stations exceeds depreciation claim in respect of these stations by

MERC, Mumbai Page 28 of 103

Rs 120.53 during FY 2006-07 resulting in AAD claim in respect of these stations, thedepreciation claim in respect of other stations such as Chandrapur, Uran, Parali, Nasikand Bhusawal exceeds loan repayment by Rs 188.47 Crore during FY 2006-07, assummarised under following Table.

(Rs Cr)FY 2006-07Particulars

AAD claim byMSPGCL

Surplus Depn overLoan Repayment

Bhusawal 0.00 10.24Chandrapur 0.00 101.40Nasik 0.00 13.04Koradi (20.01) 0.00Paras 0.00 1.16Parali 0.00 15.57Uran 0.00 47.06Khaparkheda (96.52) 0.00Sub-total (Thermal) (116.54) 188.47Sub-total (Hydel) (4.00) 0.00GRAND TOTAL(Thermal+Hydel) (120.53) 188.47

It is worthwhile to note here that in case of Khaparkheda Generating station for whichAAD of Rs 96.52 Crore is claimed, Opening Balance of Net Fixed Assets (NFA) ofthe station has been reported as Rs 1140.90 Crore during FY 2006-07 whereasOpening regulated equity is reported as Rs 900.81 Crore for FY 2006-07 andoutstanding loan balance against this station for FY 2006-07 is reported as Rs 431.47Crore. Thus, basis of allocation of outstanding loans to generating station as well asbasis for determination of opening level of regulated equity for each Station needs tobe verified for its appropriateness and only then claim for AAD at the station levelcan be ascertained. Given these issues, the Commission has continued to determineclaim for AAD for the Generating Company as a whole. However, any revision onthis account can be considered based on actuals, subject to prudence check, whiletruing up, during subsequent Annual Performance Review exercise.

Accordingly, Advance against Depreciation (AAD) projected by MSPGCL andapproved by Commission for true-up of FY 2006-07 is summarised in the followingTable:

Rs CroreParticulars Tariff Order Actuals Allowed after truing upLoan Repayment 303.15 269.62 269.62

Depreciation 187.06 337.55 337.55Advance Against depreciation (AAD) 116.09 120.53 0.00

MERC, Mumbai Page 29 of 103

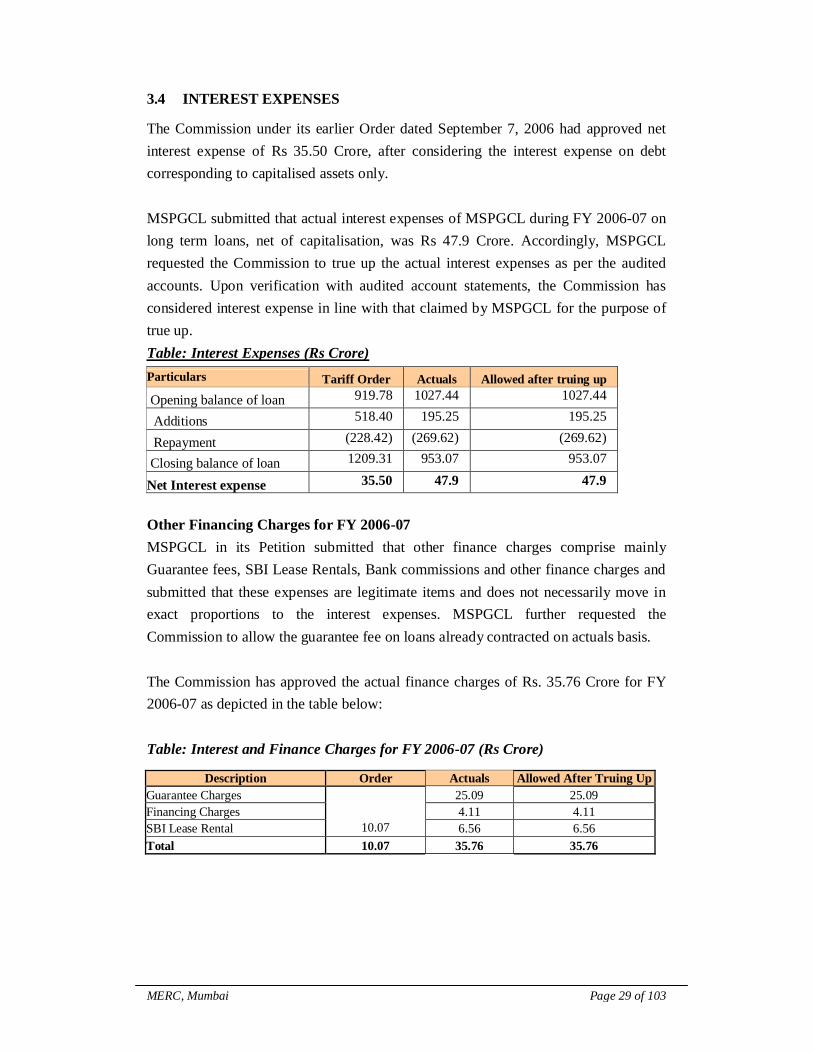

3.4 INTEREST EXPENSES

The Commission under its earlier Order dated September 7, 2006 had approved netinterest expense of Rs 35.50 Crore, after considering the interest expense on debtcorresponding to capitalised assets only.

MSPGCL submitted that actual interest expenses of MSPGCL during FY 2006-07 onlong term loans, net of capitalisation, was Rs 47.9 Crore. Accordingly, MSPGCLrequested the Commission to true up the actual interest expenses as per the auditedaccounts. Upon verification with audited account statements, the Commission hasconsidered interest expense in line with that claimed by MSPGCL for the purpose oftrue up.Table: Interest Expenses (Rs Crore)Particulars Tariff Order Actuals Allowed after truing up

Opening balance of loan 919.78 1027.44 1027.44

Additions 518.40 195.25 195.25

Repayment (228.42) (269.62) (269.62)

Closing balance of loan 1209.31 953.07 953.07

Net Interest expense 35.50 47.9 47.9

Other Financing Charges for FY 2006-07MSPGCL in its Petition submitted that other finance charges comprise mainlyGuarantee fees, SBI Lease Rentals, Bank commissions and other finance charges andsubmitted that these expenses are legitimate items and does not necessarily move inexact proportions to the interest expenses. MSPGCL further requested theCommission to allow the guarantee fee on loans already contracted on actuals basis.

The Commission has approved the actual finance charges of Rs. 35.76 Crore for FY2006-07 as depicted in the table below:

Table: Interest and Finance Charges for FY 2006-07 (Rs Crore)

Description Order Actuals Allowed After Truing UpGuarantee Charges 25.09 25.09Financing Charges 4.11 4.11SBI Lease Rental 10.07 6.56 6.56Total 10.07 35.76 35.76

MERC, Mumbai Page 30 of 103

3.5 RETURN ON EQUITY (ROE)

MSPGCL submitted that it has computed return on equity in accordance with theprinciples outlined under MERC (Terms and Conditions of Tariff) Regulations, 2005.It has claimed return on equity of Rs 358.88 Crore for FY 2006-07 as compared tothat approved by Commission in its earlier Tariff Order dated September 7, 2006 atRs 376.74 Crore. The reduced claim for ROE is mainly on account of the lower valueof actual opening regulated equity as per its audited accounts for FY 2006-07.

The Commission has verified MSPGCL’s claim for lower opening regulated equityfor FY 2006-07 as per its audited financial statements. Accordingly, the Commissionhas considered opening balance of regulated equity for FY 2006-07 as claimed byMSPGCL. The Commission has computed the RoE for FY2006-07 in accordancewith Regulation 34.1 of the Tariff Regulations as applicable for the generationbusiness. The summary of RoE as projected by MSPGCL and approved by theCommission for FY 2006-07 is summarised in the following Table:

Table: Return on Equity (Rs Crore)

FY 2006-07ParticularsTariffOrder

Revised Estimateby MSPGCL

Allowed aftertruing up

Regulatory Equity at the beginning of theyear 2691.00 2563.41 2563.41

Return on Regulatory Equity 376.74 358.88 358.88

3.5.1 Income Tax

MSPGCL submitted that a total provision of Rs 120.53 Crore has been made towardsincome tax as per the Audited accounts of FY 2006-07 as against the Commission’sapproval of Rs. 48 Crore of income tax for the year.

Hence, MSPGCL requested the Commission for truing up of Income tax for Rs 72.53Crore and allow the same, as per Audited accounts.

The Commission asked MSPGCL to submit the details of the income tax challanscopies for FY 2006-07 as part of the part of additional information requirement.MSPGCL submitted the details of income tax challans for FY 2006-07 and theCommission observes that the actual payment towards tax as per challans works outto Rs 43.15 Crore as against the income tax provisioning of Rs 120.53 Crore inMSPGCL’s Audited accounts. The Commission in its Tariff Order for FY 2006-07approved income tax by considering Minimum Alternate Tax (MAT) as MSPGCL

MERC, Mumbai Page 31 of 103

had no income tax liability because of the erstwhile MSEB’s accumulated losses.Accordingly, the Commission has considered actual income tax paid of Rs 43.15Crore as per the income tax challans for FY 2006-07 for truing up purposes.

Further, in the context of income tax, the Commission specifically asked MSPGCL tosubmit the details of the income tax refund received by MSPGCL for FY 2005-06, ifany. MSPGCL, in its reply, submitted the details of the income tax refund for FY2005-06. The Commission has analysed the details provided by MSPGCL andobserved that MSPGCL has received a refund of Rs 30.694 Crore towards income taxrefund for FY 2005-06 and also received a refund of Rs 18.18 Lakh towards fringebenefit tax.

Though the Commission could have undertaken the truing up of the tax refundreceived by MSPGCL for FY 2005-06 in this Order, however, as discussed in Section1, the Commission will issue a separate Order, which will deal with the revised finaltruing up of all the elements of expenses and revenue for FY 2005-06 in accordancewith the ATE Judgment in this regard, after following the due regulatory process.Accordingly, the Commission would consider the amount received by MSPGCL asrefund for income tax and fringe benefit tax while undertaking the revised final truingup of FY 2005-06.

3.5.2 Prior period True-up computation on revenue earned by MSPGCL in2005-06

MSPGCL submitted that the Commission in its Order dated April 25, 2007considered true-up of revenue earned in FY 2005-06. MSPGCL submitted that it hasfiled an appeal before the ATE for the revenue considered for truing up. However,pending such decision of the Tribunal, MSPGCL submitted the following facts to theCommission for consideration in true-up for FY 2006-07.

The Commission while considering the true-up of FY 2005-06 has stated that “TheCommission has received the jointly reconciled accounts of the Utilities and hasconsidered the same while truing up the ARR and Revenue for FY 2005-06 instead oflimited review accounts submitted by MSPGCL”

MSPGCL submitted that the Commission has accordingly considered all expenditureincurred by it as per the jointly reconciled accounts. MSPGCL submitted that theCommission has inadvertently considered the notional revenue earned by it as per thelimited review accounts. MSPGCL submitted that it is erroneous to consider the

MERC, Mumbai Page 32 of 103

notional revenue as far as truing up is concerned since an under recovery of revenuecan have serious repercussions on the cost recovery by the Utility and that thenotional income could be an overstated figure without having any practical basis.

The jointly reconciled accounts do not mention the revenue earned by sale of power toMSEDCL. MSPGCL accordingly has reworked the revenue side true-up for FY 2005-06 by prorating the revenue considered by the Commission into two periods i.e., 66days for April 1, 2005 to June 5, 2005 and 299 days from June 6, 2005 to Mar 31,2006 as provided below:

Table: Revised computation of Revenue side true-up for FY 2005-06MERC Order

for 2005-06(A)

True-up for 2005-06(MYT order)

(B)

Revisedcomputation

(C)Revenue from sale of power (Jun6,05 to Mar 31,06)

5370.531 5361.70 5361.702

Revenue from sale of power (Apr 1,2005 to June 5, 2005)

1185.473 1218.28 1185.47

Revenue from Generation 6556.00 6579.98 6547.17

Surplus/(Gap) (B-C) or (C-A) 23.98 (8.83)

MSPGCL claimed that it should have been allowed to recover the deficit of Rs 8.83Crore along with the gap in Net revenue requirement as computed by the Commissioni.e., Rs 15.03 Crore for FY 2005-06 in the MYT order.

However, by computing a revenue surplus of Rs 23.98 Crore after considering thenotional revenue as per the limited accounts, the Commission had adjusted the netrevenue requirement of Rs 15.03 Crore and has accordingly calculated an overallsurplus of Rs 8.95 Crore. The Commission has further reduced the revenuerequirement of FY 2007-08 by the same amount.

On the basis of true-up methodology adopted by the Commission, MSPGCLsubmitted that it should have been allowed to recover an overall gap of Rs 23.86Crore for FY 2005-06 (Rs 8.83 Crore + Rs 15.03 Crore) and also increase the amount

1 the total revenue considered by Commission has been proportionally split into two accounting periodsof 299 days ( June-6, 2005 to Mar 31, 2006) and 66 (Apr 1, 2005 to June 5, 2005 days2 As per Audited accounts for June 6, 2005 to Mar 31, 2006.3 MERC total revenue for 2005-06 considered on pro-rata basis for 99 days period.

MERC, Mumbai Page 33 of 103

of ARR for FY 2006-07 by Rs 8.95 Crore thus, allowing a net recovery of Rs 32.81Crore (Rs 23.86 Crore for FY 2005-06 + Rs 8.95 Crore for FY 2006-07).

However, MSPGCL only sought an increase in true-up amount for FY 2006-07 by Rs8.95 crore since it tends to differ from the Commission’s viewpoint of revenue sidetrue-up. With regard to the Net Revenue Gap of Rs 15.03 Crore computed by theCommission in the MYT Order for FY 2005-06, MSPGCL requested the Commissionto reconsider the gap in light of the forthcoming judgment of Appellate Tribunal on itsappeal (Case No: 86 and 87 of 2007) and then issue suitable orders regarding thesame.

As discussed in Section 1, the Commission will separately carry out the truing up ofrevenue and expenses for FY 2005-06, hence, the Commission in this Order has notcarried out any truing up for prior period.

3.5.3 Non Tariff Income

The Commission, in its Tariff Order dated September 07, 2006 for determining ARRfor FY 2006-07, has not projected Non Tariff Income, on the grounds of absence ofhistorical actuals of Non Tariff Income and opined that any Non Tariff Income atactuals would be adjusted during the truing up.

Accordingly, MSPGCL submitted the Non Tariff Income (NTI) as Rs. 95.68 Crore,however, it has shown Rs. 37.96 Crore of non-tariff income, in formats for respectivegenerating stations. The Commission asked MSPGCL about the details of the sourceof remaining NTI. MSPGCL replied that some of the NTI is booked against the headoffice and has not been included in the formats for individual stations.

Further, the Commission observed that MSPGCL has not considered NTI for truingup purposes for FY 2006-07, for determining the revenue gap/surplus. TheCommission asked MSPGCL to compute the revenue gap/surplus for FY 2006-07,considering the actual revenue earned by MSPGCL in FY 2006-07, including tariffrevenue, FAC revenue and Non Tariff Income. MSPGCL in its reply submitted it hasappealed before the ATE for not considering the NTI as part of the revenue.

The ATE dealt with the above issues vide its Judgment dated April 10, 2008 inAppeal No.s 86 & 87 of 2007 and ruled that if the other income cannot be reasonablylinked to any cost item allowed by the Commission as a part of the ARR, the sameshould not be adjusted against the ARR of MSPGCL. Accordingly, the Commissionhas asked specific queries regarding this issue for each item of non-tariff income.

MERC, Mumbai Page 34 of 103

Based on the replies received from MSPGCL and after the due regulatory process, theCommission will carry out the truing up of non tariff income for FY 2006-07alongwith truing up of non tariff income for FY 2005-06.

3.5.4 Interest on Working Capital

MSPGCL, in its Petition, submitted that it has computed interest on working capitalas per the Regulations and accordingly computed the interest on working capital forFY 2006-07 as Rs 205.92 Crore as against the approved interest on working capital ofRs 171 Crore in the Tariff Order for FY 2006-07.

As per the Regulations, interest on working capital has to be computed based on thenorms which depends on various elements of ARR like O&M expenses, maintenancespares, receivables, fuel expenses. As discussed in Section 1, the Commission willcarry out the truing up of various elements of expenses for FY 2006-07 such as O&Mexpenses, fuel expenses based on re-determined performance parameters through aseparate process. As the truing up of all these elements have impact on interest onworking capital, the Commission will carry out the truing up of interest on workingcapital as part of final truing up for FY 2006-07.

3.5.5 Revenue

MSPGCL, in its Petition, has not considered the actual revenue earned from sale ofpower generated at various generating stations for FY 2006-07, for determining therevenue gap/surplus. The Commission asked MSPGCL to compute the revenuegap/surplus in FY 2006-07 after considering the actual revenue earned by it in FY2006-07, including tariff revenue, FAC revenue and Non-tariff income.

MSPGCL replied that it has preferred an appeal in the ATE and has submitted thatnon-tariff income should not be considered as part of the revenue. Considering thatthe matter is subjudice, MSPGCL requested the Commission to consider the issue inaccordance with the outcome of the proceedings before the ATE. However, MSPGCLprovided the revenue earned under various heads as shown in the Table below:

Particulars Rs CroreRevenue from Tariff 6385.90FAC Revenue 612.03Other Income 95.68Total Revenue 7093.61

MERC, Mumbai Page 35 of 103

Also, MSPGCL submitted that while the actual billed amount in FY 2006-07 was Rs6385.90 Crore, however in the Audited accounts there is an additional provision forFuel Adjustment Charges (FAC) charges of Rs 340 Crore and adjustments foradvance billing on the first and last day of the year (units generated from midnight ofApril 1, 2006 and units generated till midnight of Mar 31, 2007) on account of whichthe total revenue earned works out to Rs 7440.63 Crore.

The Commission observed a difference of Rs 50.40 Crore between the amount shownas revenue from sale of power to MSEDCL in the Audited Accounts of MSPGCL andthe amount shown as cost of power purchase from MSPGCL in the Audited Accountsof MSEDCL, for the period from April 1, 2006 to March 31, 2007 as shown in thefollowing Table: Rs Crore

Particulars 1-04-2006 to 31-03-2007MSPGCL Revenue 7338.87 (Audited A/c of MSPGCL)Power Purchase charge paid to MSPGCL 7287.974 (Audited A/c of MSEDCL)Difference 50.40

MSPGCL, in its reply, explained the difference as shown below:Amount billed by MSPGCL toMSEDCL

7338.37 Amount as per audited accounts of MSPGCL

Less: Amount disputed ( Excess Bill,hence not considered by MSEDCL)

26.36 This is a Disputed Amount not included inaccounts of MSEDCL

Less : Provision of differential billingrate in the books of accounts ofMSPGCL 142.10

This amount is not considered in accounts ofMSEDCL

Add : Differential of FAC consideredby MSEDCL in accounts than thatactually billed by MSPGCL ( 316.40-197.94) 118.46

MSEDCL has considered an FAC of Rs 316.40 cr.On the other hand MSPGCL has considered anamount of Rs 197.94 cr. Therefore in MSEDCL’saccounts Rs 118.46 is additional amount for FAC.

Less: Adjustments for advance billing (in Apr-07 and Apr-06) 0.40

The same pertains to correction in advance billing.

Final cost of power purchaseconsidered by MSEDCL 7287.97

This is the final amount as per books of accounts ofMSEDCL

Difference 50.40

Upon analysing the replies given by MSPGCL, the Commission observed that in itsreply to query 16 of its additional submission dated December 20, 2007, it hassubmitted total actual revenue billed by MSPGCL to MSEDCL for FY 2006-07, as Rs7441.11 Crore, which includes FAC revenue and excludes other income (non-tariffincome). In its reply to query 17, MSPGCL submitted the revenue earned fromMSEDCL as Rs 6997.93 Crore (Revenue from tariff Rs 6385.90 Crore plus FACrevenue of Rs. 612.03 crore). Also, there is a mention of additional provision of Rs340 Crore towards FAC under the Audited Accounts. Thus, the Commission observed

MERC, Mumbai Page 36 of 103

that there is a difference of around Rs 103.2 Crore between the revenue indicated inreply to Query 16 (Rs 7441 Crore) and the total revenue from tariff indicated in replyto Query 17 (Rs 7338 Crore). The Commission asked MSPGCL to reconcile thedifference as discussed above and confirm the actual revenue to be considered fortruing up for FY 2006-07.

MSPGCL in its reply submitted that the revenue booked as per accounts comprise ofthe following:

S.No. Particulars Rs Crore1 Revenue From Tariff 6385.902 FAC Revenue 612.033 Provision for unbilled revenue in the books of accounts 340.654 Total Revenue 7338.58*

* may not tally due to rounding off

MSPGCL submitted that as per the actual billings done for FY 2006-07, the amountactually billed for S.No. 3 in the above table is Rs 450.60 Crore. Also there is areduction in the amount actually billed corresponding to billing period starting from00:00 hrs (in place of 12:00 pm ) since December 2006 to March 2007 of (Rs 7.41Crore). The amount actually billed as shown in the Table below:

S.No. Particulars Rs Crore1 Revenue From Tariff (As per accounts) 6385.902 FAC Revenue (As per accounts) 612.033 Actual billing against the provision of Rs 340.65 crore in

the books of accounts)450.60

4 Correction in Bill amount for 00:00 hrs -7.414 Total Revenue Billed for 2006-07 7441.12

MSPGCL submitted that therefore, there is a difference of around Rs 103 Crore andclarified that the actual billing of Rs 450.60 is correct and would be considered inaccounts in the subsequent year.

However, as discussed in Section 1, the Commission for truing up of non tariffincome has asked MSPGCL to submit certain additional information in accordancewith the ATE Order, and the Commission has not undertaken the truing up of revenuefor FY 2006-07 in this Order. The Commission will undertake the truing up ofrevenue of MSPGCL for FY 2006-07 as part of final truing up for FY 2006-07through due Regulatory process.

MERC, Mumbai Page 37 of 103

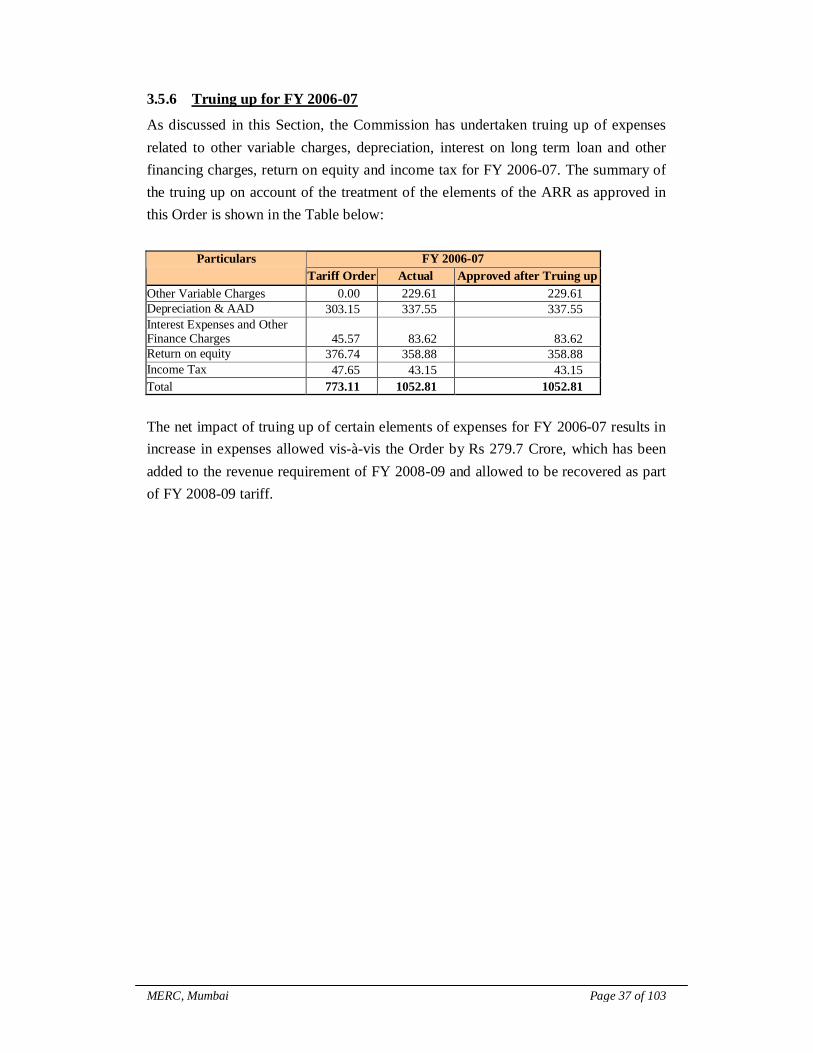

3.5.6 Truing up for FY 2006-07

As discussed in this Section, the Commission has undertaken truing up of expensesrelated to other variable charges, depreciation, interest on long term loan and otherfinancing charges, return on equity and income tax for FY 2006-07. The summary ofthe truing up on account of the treatment of the elements of the ARR as approved inthis Order is shown in the Table below:

FY 2006-07ParticularsTariff Order Actual Approved after Truing up

Other Variable Charges 0.00 229.61 229.61Depreciation & AAD 303.15 337.55 337.55Interest Expenses and OtherFinance Charges 45.57 83.62 83.62Return on equity 376.74 358.88 358.88Income Tax 47.65 43.15 43.15Total 773.11 1052.81 1052.81

The net impact of truing up of certain elements of expenses for FY 2006-07 results inincrease in expenses allowed vis-à-vis the Order by Rs 279.7 Crore, which has beenadded to the revenue requirement of FY 2008-09 and allowed to be recovered as partof FY 2008-09 tariff.

MERC, Mumbai Page 38 of 103

4 PERFORMANCE PARAMETERS

4.1 PERFORMANCE PARAMETERS

Regulation 16.1 of the MERC (Terms and Conditions of Tariff) Regulations, 2005,stipulates,

“The Commission may stipulate a trajectory, which may cover one or morecontrol periods, for certain variables having regard to the reorganization,restructuring and development of the electricity industry in the State.

Provided that the variables for which a trajectory may be stipulated include,but are not limited to, generating station availability, station heat rate,transmission losses, distribution losses and collection efficiency.” (emphasisadded)

The Commission, in its MYT Order for MSPGCL, had approved the trajectory offollowing performance parameters:

• Availability• Heat Rate• Auxiliary Consumption• Transit Loss• Secondary Fuel Oil Consumption

4.2 GENERATING STATIONS OF MSPGCL

The Commission, in its MYT Order, considered the total installed capacity ofMSPGCL as 9510 MW. The Commission had not considered the derated capacity asprojected by MSPGCL in its MYT Petition for some of its stations, as the applicationfor deration of the installed capacity was pending with Central Electricity Authority(CEA) for approval.

The Commission asked MSPGCL to submit the approval obtained from CEA forderated capacity of its generating stations and MSPGCL has submitted the same alongwith the APR Petition. MSPGCL, in its APR Petition, submitted that CEA hasapproved the de-rating of capacities on April 20, 2007 for Nasik, Koradi, Bhusawal,Paras and Parli TPS. The Commission has accepted the de-rated capacity as submittedby MSPGCL for its generating station in accordance with the approval granted byCEA.

MERC, Mumbai Page 39 of 103