Becoming more specialist and most loved · Online sample includes PetPlanet, Amazon, Zooplus,...

28

0 Becoming more specialist and most loved

Transcript of Becoming more specialist and most loved · Online sample includes PetPlanet, Amazon, Zooplus,...

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

0

Becoming more specialist and most loved

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Customer vision: helping pets and their owners live long and happy lives together

1

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

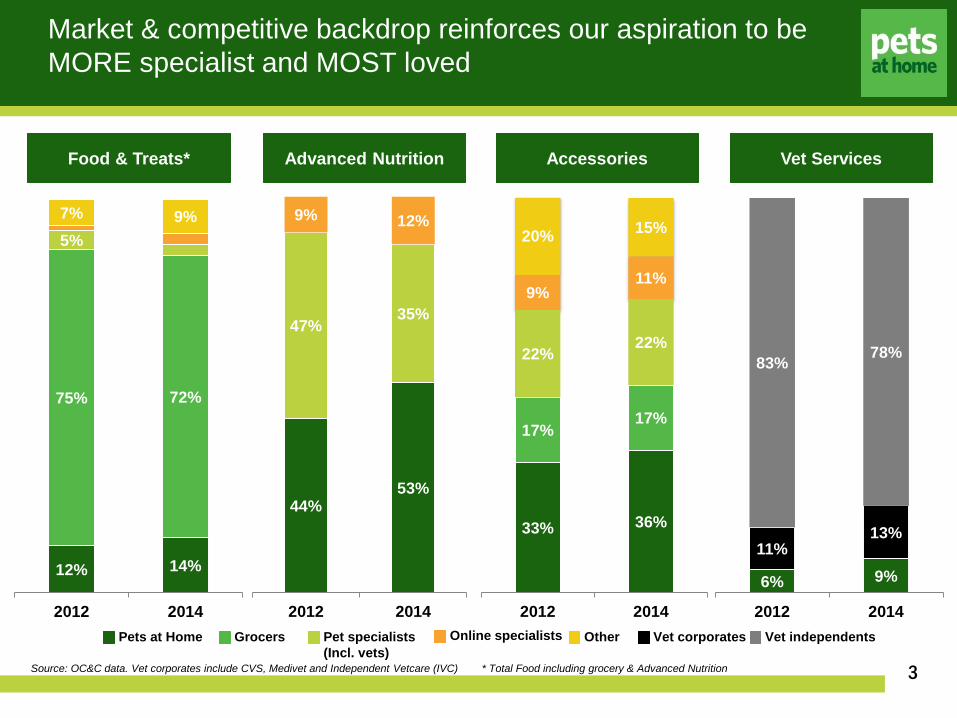

Market & competitive backdrop reinforces our aspiration to be MORE specialist and MOST loved

2

Pet market continues to show resilience & premium growth vs general retail

Online participation growth is <1% per year, store collection the fastest growing segment

Pet market

General retail

2.6%

2.2%

3.5%

1.5%

2008-12 2012-14

3.4%

5.9% 7.3%

8.6%

2008 2010 2012 2014

Online sales participation of total pet market

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Market & competitive backdrop reinforces our aspiration to be MORE specialist and MOST loved

3

12% 14%

75% 72%

5% 3%

1% 3% 7% 9%

2012 2014

44% 53%

47% 35%

9% 12%

2012 2014

Food & Treats* Advanced Nutrition Vet Services Accessories

33% 36%

17% 17%

22% 22%

9% 11%

20% 15%

2012 2014

Source: OC&C data. Vet corporates include CVS, Medivet and Independent Vetcare (IVC) * Total Food including grocery & Advanced Nutrition

Pets at Home Grocers Pet specialists (Incl. vets)

Online specialists Other Vet corporates Vet independents

6% 9% 11%

13%

83% 78%

2012 2014

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

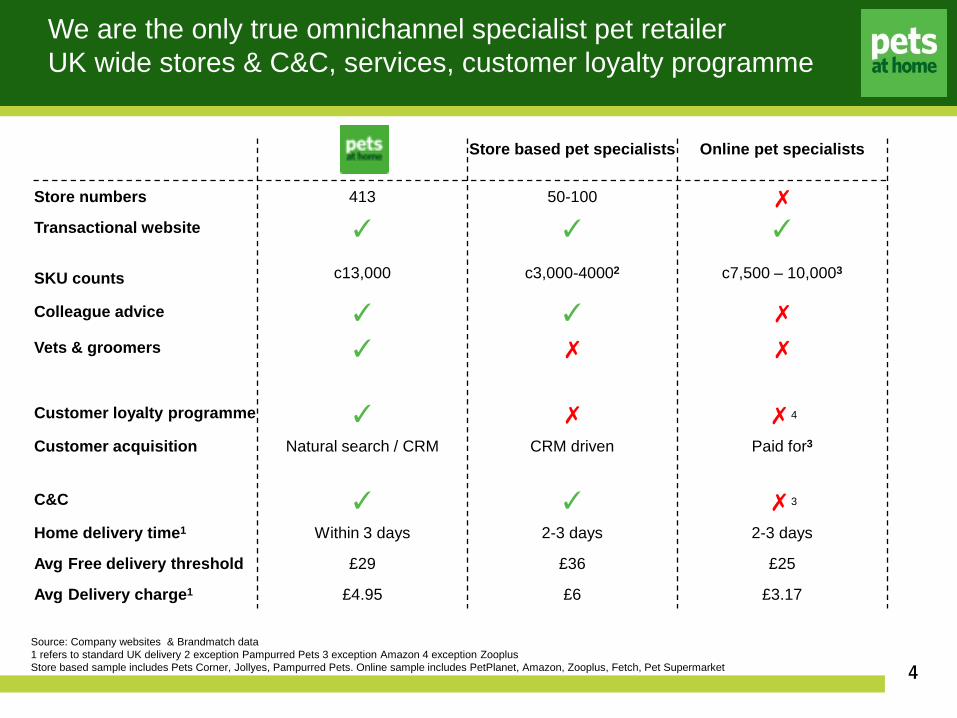

We are the only true omnichannel specialist pet retailer UK wide stores & C&C, services, customer loyalty programme

4

Store based pet specialists Online pet specialists

Store numbers 413 50-100 ✗ Transactional website ✓ ✓ ✓

SKU counts c13,000 c3,000-40002 c7,500 – 10,0003

Colleague advice ✓ ✓ ✗ Vets & groomers ✓ ✗ ✗

Customer loyalty programme ✓ ✗ ✗4

Customer acquisition Natural search / CRM CRM driven Paid for3

C&C ✓ ✓ ✗3

Home delivery time1 Within 3 days 2-3 days 2-3 days

Avg Free delivery threshold £29 £36 £25

Avg Delivery charge1 £4.95 £6 £3.17

Source: Company websites & Brandmatch data 1 refers to standard UK delivery 2 exception Pampurred Pets 3 exception Amazon 4 exception Zooplus Store based sample includes Pets Corner, Jollyes, Pampurred Pets. Online sample includes PetPlanet, Amazon, Zooplus, Fetch, Pet Supermarket

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

And we have unique attributes & capabilities to leverage

5

Market leading brands & customer relationships

Incomparable range, innovation, refreshment & sourcing advantages

Sector leading colleague expertise & qualified professionals

Best value private brands & own labels, plus exclusives

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Delivering on the PawPrint supports the core drivers of growth

Product and Innovation

Product Mix & Own Brand

Optimised Store & Pet Services

Roll Out

Key Growth Drivers

Driv

ers

of C

ore

Gro

wth

LFL

Space

Margin

VIP Club

Omnichannel

Services (Vets & Groomers)

Services Maturity

6

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Becoming more loved by pet owners

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Our customer is the engaged pet owner

8

What defines an engaged customer?

Source: Pets at Home survey of >5,000 pet owners July 2015 Note: 5 = “Strongly agree”, 1 = “Strongly disagree” * Scores reversed for this question

2.00

2.50

3.00

3.50

4.00

4.50

My pets are avery big part of

my life

I like topamper my

pets and makethem feelspecial

I always lookfor the

cheapestprices whenbuying pet

food

Nothing that Ibuy is too good

for my pets

My pets aremy children

I tell my pets Ilove them atleast twice a

day

I take my petsto the vet

regularly forcheck-ups

Non PaH customer

PaH customer

*

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

To become more loved by engaged owners, we focus on the criteria they value most: range, quality & advice

9

Customer rankings of key purchase criteria from 1-5 (where 5 is most important)

2.00

3.00

4.00

5.00

Highly engaged pet owners Low engagement pet owners

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

A wide range of Services & specialist advice from colleagues give customers more reasons to shop with us

10

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Showcase our knowledge & passion, to help customers make the most of their lives together

11

Widen the range of care plans in our vet practices

Be the first place people think of when they buy a new pet

Ensure colleagues have more, not less, customer facing time

Help every customer to feed a better diet – bridge the gap to AN

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Strengthening our specialist credentials

12

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

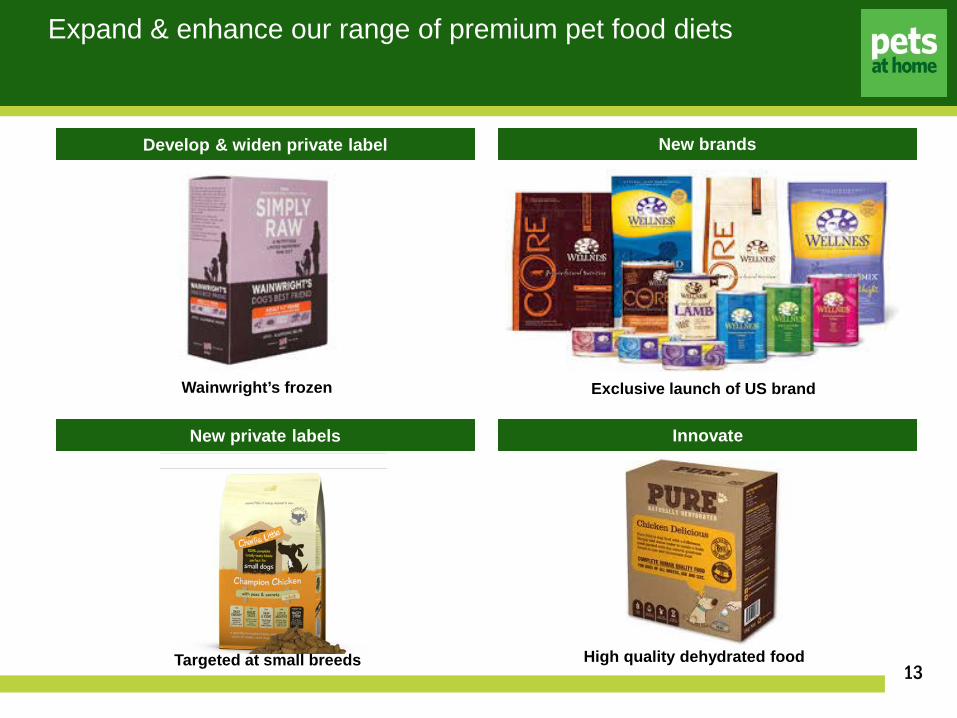

Expand & enhance our range of premium pet food diets

13

New brands

Exclusive launch of US brand

High quality dehydrated food

Innovate

Develop & widen private label

New private labels

Wainwright’s frozen

Targeted at small breeds

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

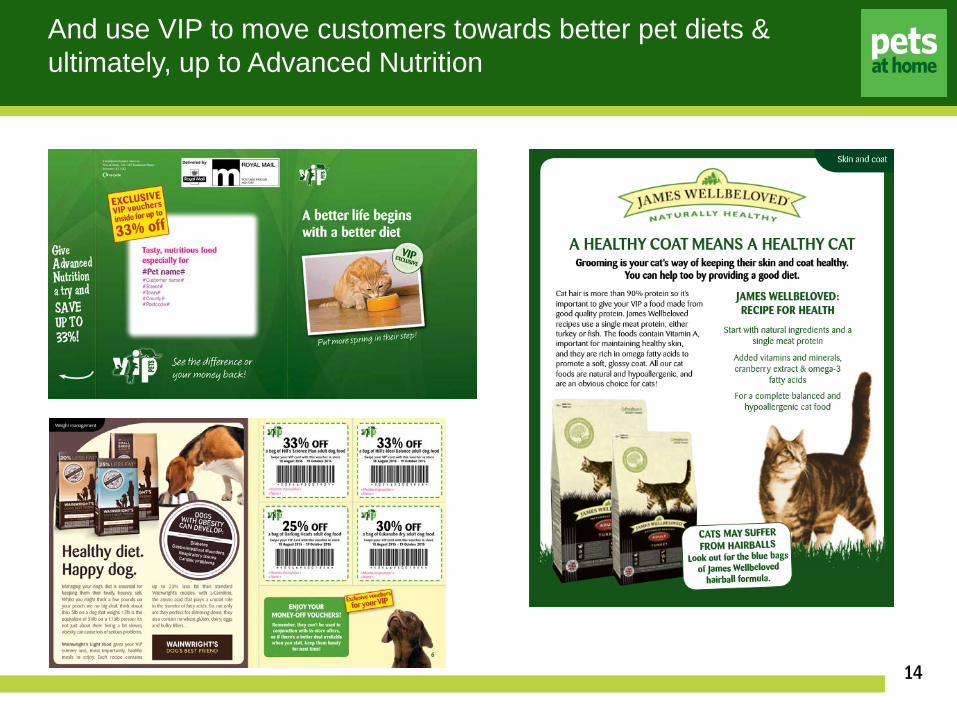

And use VIP to move customers towards better pet diets & ultimately, up to Advanced Nutrition

14

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

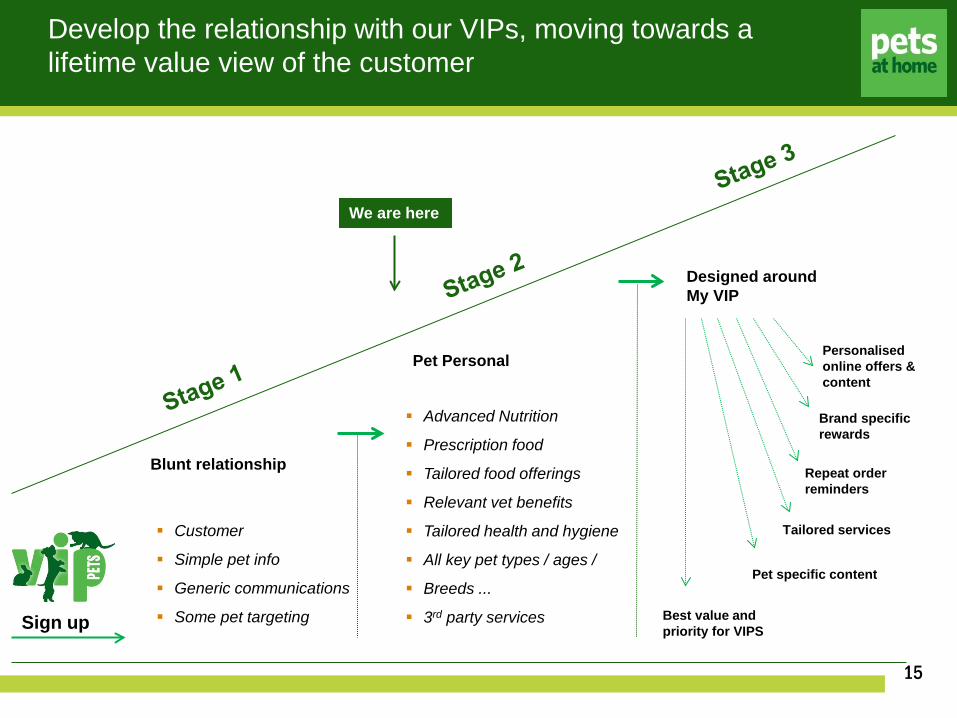

Sign up

Blunt relationship

Customer

Simple pet info

Generic communications

Some pet targeting

Pet Personal

Advanced Nutrition

Prescription food

Tailored food offerings

Relevant vet benefits

Tailored health and hygiene

All key pet types / ages /

Breeds ...

3rd party services

Designed around My VIP

We are here

Develop the relationship with our VIPs, moving towards a lifetime value view of the customer

Personalised online offers & content

Repeat order reminders

Brand specific rewards

Tailored services

Pet specific content

Best value and priority for VIPS

15

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

c50% of our online orders are picked up in-store

Store convenience for frequent food purchase

Stores will always be a fundamental part of our proposition

16

Vet & grooming services will never be delivered online

Live pet & grooming provides entertainment & education

Customers want to bring their pet, & talk pet with other

owners Average basket <£20, not a

natural online market

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Whilst adapting to our customers shopping habits by working towards a seamless offline & online experience

17

Order in-store kiosks

Increase extended

online product range

Order in-store via colleague

PetPads

Richer online content & imagery

Digital screens to showcase

extended range

Greater potential for

online bookings

VIP App

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Trialling new formats offers further routes to growth & retains our specialist edge over the competition

18

Niche, additional market segment Highly engaged dog owners Affluent high street locations

For the core Pets at Home customer Convenience format Infill locations or towns without retail parks

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Primary Practices

In-store or standalone

Extended hours

Super Surgery

24/7

CT scanner

Particular pet

specialists

Grow our veterinary business through through convenience & specialisms

19

Our primary practices can inter-refer & leverage the benefits of other Vet Partners

CT scanner

Particular pet specialists

Super Surgery

In-store or standalone

Extended hours

24/7

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Acquiring specialist referral hospitals to access an additional and complementary segment of the market

20

Solidifies our specialist credentials & reputation Captures additional market spend Vertical integration Minimises revenue leak from primary practices

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

The long term potential of our retail and services model

21

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

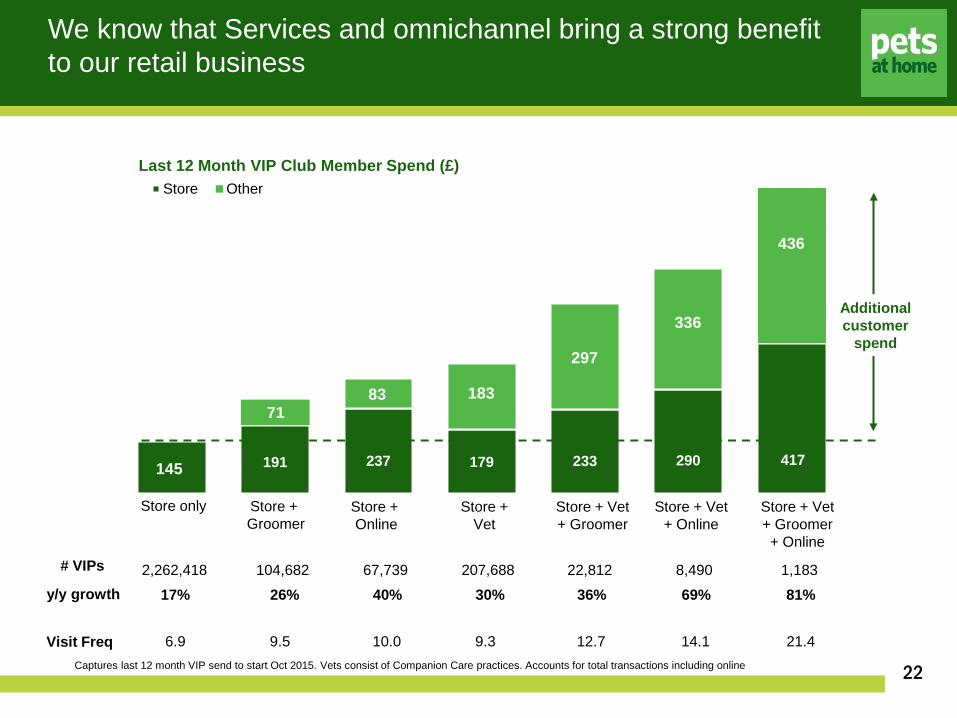

We know that Services and omnichannel bring a strong benefit to our retail business

22

191 237 179 233 290 417

Store Other Vet, Groom, Web

Additional customer

spend

Last 12 Month VIP Club Member Spend (£)

145

Captures last 12 month VIP send to start Oct 2015. Vets consist of Companion Care practices. Accounts for total transactions including online

Visit Freq 6.9 9.5 10.0 9.3 14.1

# VIPs 2,262,418 104,682 67,739 207,688 8,490

12.7

22,812

21.4

1,183

17% 26% 40% 30% 69% 36% 81% y/y growth

Store only Store + Groomer

Store + Online

Store + Vet

Store + Vet + Groomer

Store + Vet + Online

Store + Vet + Groomer + Online

71 83 183

297

336

436

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

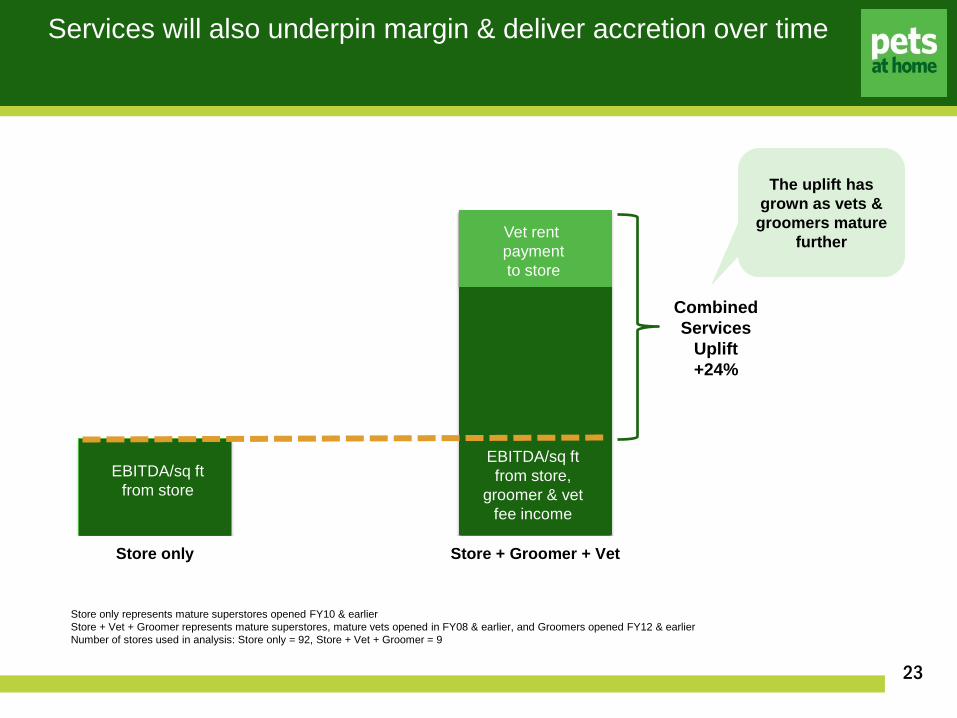

Services will also underpin margin & deliver accretion over time

23

Store only Store + Groomer + Vet

EBITDA/sq ft from store

EBITDA/sq ft from store,

groomer & vet fee income

Combined Services

Uplift +24%

Vet rent payment to store

Store only represents mature superstores opened FY10 & earlier Store + Vet + Groomer represents mature superstores, mature vets opened in FY08 & earlier, and Groomers opened FY12 & earlier Number of stores used in analysis: Store only = 92, Store + Vet + Groomer = 9

The uplift has grown as vets &

groomers mature further

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

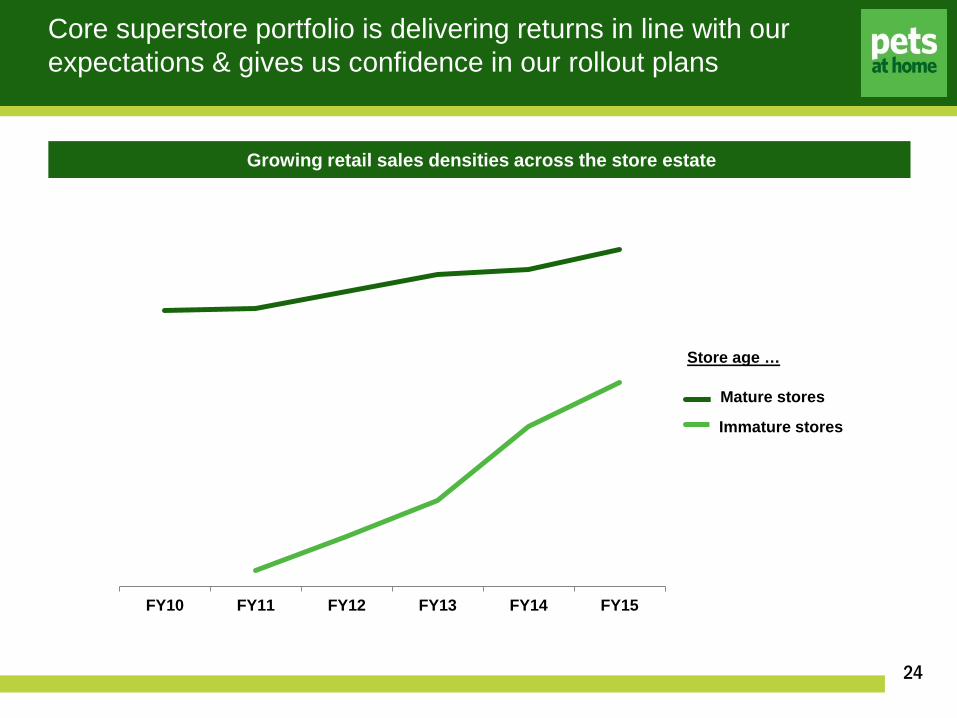

FY10 FY11 FY12 FY13 FY14 FY15

> 5 yrs old≥ 1 yr & ≤ 5 yrs old

Core superstore portfolio is delivering returns in line with our expectations & gives us confidence in our rollout plans

24

Growing retail sales densities across the store estate

Store age …

Mature stores

Immature stores

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

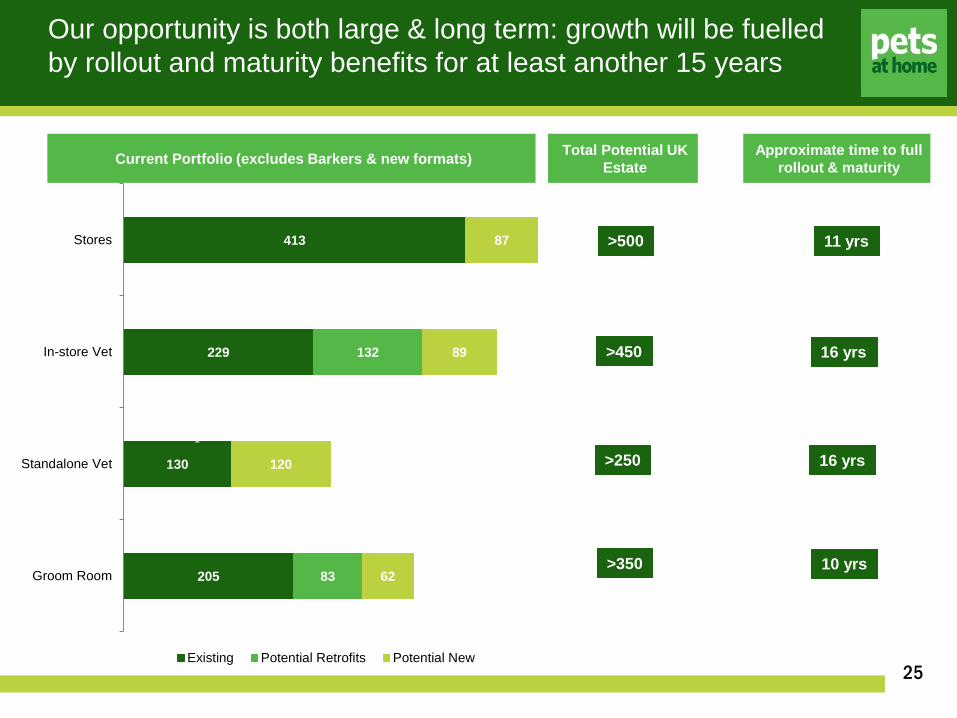

205

130

229

413

83

132

62

120

89

87

Groom Room

Standalone Vet

In-store Vet

Stores

Existing Potential Retrofits Potential New

Current Portfolio (excludes Barkers & new formats)

Our opportunity is both large & long term: growth will be fuelled by rollout and maturity benefits for at least another 15 years

Total Potential UK Estate

Approximate time to full rollout & maturity

1

1

25

>500

>450

>250

>350

11 yrs

16 yrs

16 yrs

10 yrs

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

$33.8m

$38.7m

H1 FY15 H1 FY16

6.3p

7.2p

H1 FY15 H1 FY16

£381.5m

£404.5m

H1 FY15 H1 FY16

Strong growth & highly cash generative business

EPS Revenue & Like-For-Like Growth

4.2% 1.8%

FCF & Conversion

38.0% 47.3%

26

£22.3m

£29.5m

Net debt / EBITDA

2.0x

H1 FY15

1.5x

H1 FY16

nemo2014\Presentations\Analyst Presentation Jan14\201401 Nemo Analyst Presentation Master-22nd Jan FINAL.pptx

Becoming MORE specialist and MOST loved

27

Operating as the significant leader in a resilient market

Continue to accentuate our strengths with core focus on the engaged pet owner

Delivered through our stores, colleagues, services and VIP club

Long term maturing store and services opportunity underpinning space and profit growth

Consistent cash returns on invested capital & strong cash generation