Beazley - Interim Results announcement

34

1 Cover Results for the six months ended 30 June 2013 Tuesday, 23 July 2013

-

Upload

company-spotlight -

Category

Economy & Finance

-

view

736 -

download

3

Transcript of Beazley - Interim Results announcement

1

Cover

Results for the six months ended 30 June 2013

Tuesday, 23 July 2013

Disclaimer notice

Certain statements in the presentation, are or may constitute “forward looking statements”. Such forward looking statements involve risks, uncertainties and other factors which may cause the actual results, performance or achievements of the company, or industry results, to be materially different from any future results, performance or achievements expressed by such forward looking statements. The information and opinions contained in this presentation are provided as at the date of this presentation and are subject to change without notice. There is no intention, nor is any duty or obligation assumed to supplement, amend, update or revise any of the information contained in this presentation.

2

Contents

Pages

Overview 5 Business update 6

FinancialsPerformance 8 Investments 9-10 Reserves 11-12 Capital position 13

In Focus Property 14-19

Underwriting review and outlook 20-22

Appendix 24-34

3

Generic title white

Overview

Overview – Strong underwriting performance in an increasingly competitive market

• Profit before income tax of $82.3m (2012 profit: $112.9m)

• Gross written premiums increased 5% to $1,066.7m (2012: $1,013.1m)

• Combined ratio 89% (2012: 91%)

• Rate change on renewal business 1% (2012: 3%)

• Prior year reserve releases of $60.8m (2012: $47.6m)

• Investment return of $0.3m (2012: $36.1m)

• Annualised return on equity of 12% (2012: 18%)

• Interim dividend up 7% to 2.9p

5

• Continue to achieve rate increases in specialty lines

• Changes made to property group to enhance performance

• Aviation business progressing well

• European floods are covered in our reserves (maximum loss would be $30m retention)

• Challenging investment markets in Q2

Business update

6

Generic title white

Financials

Six months financial performance

6 months ended 30 June 2013

6 months ended 30 June 2012

% increase

Gross written premiums ($m) 1,066.7 1,013.1 5%

Net written premiums ($m) 758.0 650.8 16%

Net earned premiums ($m) 758.8 703.3 8%

Profit before tax ($m) 82.3 112.9 (27%)

Earnings per share (pence) 9.3 12.5

Dividend per share (pence) 2.9 2.7

Net assets per share (pence) 152.0 142.2

Net tangible assets per share (pence) 138.0 126.0

8

Portfolio delivers a nil return during H1 2013

21.3

43.5

8.5

22.5

36.1

0.3

(62.8)

46.9

29.0

16.8

46.5

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

-80.0

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

100.0

2008 2009 2010 2011 2012 2013

2nd half 1st half Return

An

nu

alised

In

vestm

en

t R

etu

rn

($

m)

In

vestm

en

t R

etu

rn

9

Conservative portfolio maintained

Cash and Cash

Equivalents, 14

.7%

Sovereign and

Supranational,

47.7%

Investment

Grade

Credit, 23.9%

Other

Credit, 2.3%Capital Growth

Assets, 11.4%

Jun-13

Cash and Cash

Equivalents, 14.

7%

Sovereign and

Supranational, 4

8.8%

Other

Credit, 2.0% Capital Growth

Assets, 9.7%

Dec-12

10

Prior year reserve releases remain stable

11

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

-10

10

30

50

70

90

110

130

150

170

190

210

2008 2009 2010 2011 2012 2012 HY 2013 HY

Specialty lines Political risks and contingency Life accident and health Marine Property Reinsurance % of NEP

Whole account reserve strength within our target range

12

Preferred upper end

% a

bove a

ctu

ari

al estim

ate

6.1%

6.7%6.4%

6.7%

7.5% 7.4%

8.2%7.9%

7.4%

6.9%7.1%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 (HY)

Financial year

Strong capital position

Sources of funds 2013 HY 2012 FY

Shareholders funds ($m) 1,157.6 1,204.5

Subordinated debt ($m) 133.5 184.3

Retail bond ($m) 114.0 122.3

1,405.1 1,511.1

Uses of funds

Lloyd’s underwriting ($m) 876.0 876.0

US Insurance Company ($m) 107.7 107.7

983.7 983.7

Surplus ($m) 421.4 527.4

Unavailable surplus ($m) (236.1) (267.1)

Available for underwriting surplus ($m) 185.3 260.3

Un-utilised banking facility ($m) 225.0 225.0

13

Generic title white

In Focus – Property

15

• Team Structure

• Product Mix

• Performance

•

Covering:

• Continuity in leadership

• Increased margins

• Growth where appropriate

• Favourable trading conditions

Key themes

Property Group

Large Risks

Middle market

Small business

Construction

& Engineering

RiskSize

Team/Location Products Access

London and Singapore

US

London

Lloyd’s broker

Lloyd’s broker

US wholesalebroker

Team/LocationLondon, Singapore, US

ProductsLarge risks in London and Singapore

Smaller risks in US

AccessLloyd’s brokers (London & Singapore)

US wholesale and retail brokers (US)

“To become and be recognised as the highest performing specialist property insurer”

• Commercial Property

• Commercial Property• Homeowners

• Homeowners• Commercial Property• Jewellers’ Block

16

Where we underwrite

17

Where our business

comes from

Europe

Worldwide

USA

Split by team

Large Property

Medium Market Property

Small Business

Construction and Engineering

Property Group – 5 year summary

18

GW

P $

m

Favourable market conditions

19

50.0%

100.0%

150.0%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 HY

Rate changes of Beazley Property Group

Underwriting review and outlook

20

Cumulative rate change since 2001

21

50%

100%

150%

200%

250%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Rate

Ch

an

ge

Underwriting Year

Life, accident & health Marine Political risks & contingency Property Reinsurance Specialty lines All divisions

HY

• Increasing competitive headwinds

• New capital entering the reinsurance market

• Entrants to US surplus lines markets

• Broker led initiatives increasing capacity in London

• Beazley’s balanced portfolio is well positioned for these headwinds and thanks to specialty lines, we are planning to achieve flat rates in 2014

• We have growth areas that will continue into 2014

• We expect to earn a 2% yield on the investment portfolio going forward

Outlook

22

Questions?

Any questions?

Generic title white

Appendix

US interest rates

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

30/06/2011 30/09/2011 30/12/2011 30/03/2012 30/06/2012 30/09/2012 30/12/2012 30/03/2013 30/06/2013

US Government Bond Yields

US 10 Year Index US 5 Year Index US 2 Year Index

25

Specialty lines incurred claims remain in line with expectations

Net ultimate premium $m

26

74%

113%

84%

56%

41% 42% 41%45%

62% 62%

46% 47%

26%

5%

79 109 53 94 268 322 340 354 430 465 427 441 420 429

0%

20%

40%

60%

80%

100%

120%

140%

1993-

1996

1997-

2000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Net

incu

rred

lo

ss r

ati

o

Underwriting Year

Net incurred loss ratio at each development year

6

5

4

3

2

ULR

Development YearDevelopment Year

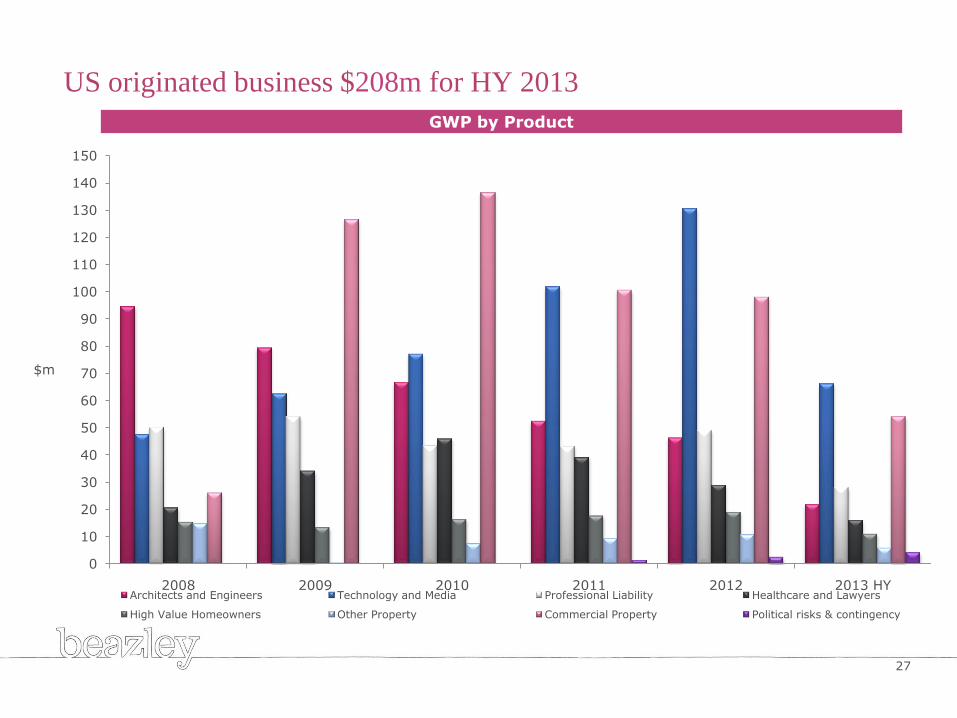

US originated business $208m for HY 2013

$m

27

GWP by Product

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

2008 2009 2010 2011 2012 2013 HYArchitects and Engineers Technology and Media Professional Liability Healthcare and Lawyers

High Value Homeowners Other Property Commercial Property Political risks & contingency

Diversified portfolio achieves consistent combined ratio through market cycles

28

40

60

80

100

120

140

160

2008 2009 2010 2011 2012 2013

Year

%

%

%

%

%

%

%

HY

Life, accident & health

6 months ended 30 June

2013 2012

Gross premiums written ($m) 56.4 49.7

Net premiums written ($m) 39.0 45.3

Net earned premiums ($m) 45.4 43.7

Claims ratio 76% 60%

Rate change on renewals (1%) (1%)

Percentage of business led 78% 79%

29

• Reserves strengthened on our

Australian business

• US admitted open for business

Marine

6 months ended 30 June

2013 2012

Gross premiums written ($m) 197.1 184.6

Net premiums written ($m) 165.2 156.8

Net earned premiums ($m) 131.5 135.9

Claims ratio 43% 47%

Rate change on renewals (2%) -

Percentage of business led 44% 46%

30

• 7% growth in gross premiums

with aviation team delivering

against plan

• Developing marine liability

account

• Prior year reserve releases of

$17.0m (2012: $8.9m)

Political risks and contingency

• Reduction in gross premiums due to

increased competition in political

risks

• Prior year reserve releases of

$10.2m (2012: $13.8m)

6 months ended 30 June

2013 2012

Gross premiums written ($m) 63.3 71.9

Net premiums written ($m) 46.0 58.2

Net earned premiums ($m) 46.3 49.8

Claims ratio 33% 22%

Rate change on renewals (1%) (1%)

Percentage of business led 74% 70%

31

Property

• 33% growth in net premiums

written as a result of consolidation

in reinsurance purchased

• Expense ratio improved to 39%

(2012: 51%)

6 months ended 30 June

2013 2012

Gross premiums written ($m) 199.0 201.5

Net premiums written ($m) 130.1 98.7

Net earned premiums ($m) 150.2 130.2

Claims ratio 52% 50%

Rate change on renewals 3% 7%

Percentage of business led 71% 68%

32

Reinsurance

• 22% increase in gross premiums

with growth across the account

• Prior year reserve releases of

$14.9m (2012: $1.6m)

• Increased competition in this

market due to new capital

entering

6 months ended 30 June

2013 2012

Gross premiums written ($m) 170.3 139.8

Net premiums written ($m) 121.1 96.7

Net earned premiums ($m) 70.8 59.6

Claims ratio 24% 51%

Rate change on renewals (1%) 5%

Percentage of business led 41% 39%

33

Specialty lines

• Continue to grow premiums in

the technology and media

product range

• Prior year reserve releases of

$17.9m (2012: $19.6m)

6 months ended 30 June

2013 2012

Gross premiums written ($m) 380.6 365.6

Net premiums written ($m) 256.6 195.1

Net earned premiums ($m) 314.6 284.1

Claims ratio 62% 63%

Rate change on renewals 4% 3%

Percentage of business led 95% 94%

34