BEA2014 -Understanding the Global Book Market & How it will Change

65

Jonathan Nowell BookExpo America 28 May 2014 UNDERSTANDING THE GLOBAL BOOK MARKET AND HOW IT WILL CHANGE Booth 1113

-

Upload

bookexpoamerica -

Category

Data & Analytics

-

view

2.398 -

download

3

description

Today, all businesses in the publishing ecosystem need data. Big data and small data chunks provide publishers, booksellers, service providers and others with a deeper insight into the market and a grasp of key trends. Nielsen Book the leading market research company in the industry worldwide presents a global market overview for the book industry – highlighting key trends across the world with emphasis on the US market. This deep dive data presentation – both print and digital - from across the Nielsen business lines will include; consumer confidence, consumer research, and future trends in the book market. Information discussed will focus on book publishing, sales and marketing strategy and up-coming global trends. Quantified data from Nielsen in consumer purchasing, buying habits and devices used, will help BEA attendees gain a greater understanding of the industry and its highs and lows.

Transcript of BEA2014 -Understanding the Global Book Market & How it will Change

Jonathan Nowell BookExpo America

28 May 2014

UNDERSTANDING THE GLOBAL BOOK MARKET

AND HOW IT WILL CHANGE

Booth 1113

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

2

AGENDA

• DATA SOURCES

• INTERNATIONAL CONTEXT

• PRINT TRENDS (YEAR-TO-DATE DATA TO 19th APRIL 2014)

• E-BOOKS IN THE US

• E-BOOKS IN THE UK (DATA TO 19th JANUARY 2014)

• THOUGHTS ABOUT THE FUTURE

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

3

• Nielsen’s BookScan

• EPOS sales data supplied by retailers in 10 countries worldwide

• Nielsen’s Books & Consumers US survey

• Survey of 6,000 book buyers per month, selected from a nationally representative sample by age, gender, location

• Online questionnaire of ~75 questions

• Nielsen Insight into the UK E-book Consumer Market: May 2014

• Data from Kantar panel of 15,000 13-79 year olds, nationally representative of the UK population

• Online questionnaire collecting monthly book buying data

MAIN DATA SOURCES

INTERNATIONAL CONTEXT

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

5

CONSUMER CONFIDENCE TO Q1-2014

Asia-Pac lead the way

Russia

Brazil

US

Northern Europe

Southern Europe and France

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

6

0

20

40

60

80

100

120

140

160

121

106 100 100

89 87 82 82

61

45

Global average 96

Q1 2014 Nielsen Consumer Confidence Index

CONSUMER CONFIDENCE INDEX

Base : All respondents n=31972

Nielsen Global Survey of Consumer Confidence & Spending Intentions

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

7

BOOKSCAN’S TEN INTERNATIONAL TERRITORIES

A combined total of over 1 billion print book sales measured in 2013

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

8

?

-6.4% -1.1%

-4.4% -6.7%

-10.2%

1.1%

0.03%

9.5%

-9.6%

BOOKSCAN’S TEN INTERNATIONAL TERRITORIES As of April, three territories showing year to date growth in print book volume sales

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

9

-15.0% -10.0% -5.0% 0.0% 5.0% 10.0% 15.0%

Adult Fiction

Non-Fiction

Children's

Total ES

IT

ROI

UK

EUROPEAN GENRE PERFORMANCE, 2014YTD VS 2013YTD

Nielsen BookScan

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

10

-30.0% -20.0% -10.0% 0.0% 10.0% 20.0% 30.0%

Adult Fiction

Non-Fiction

Children's

Total SA

IND

NZ

AUS

US

INTERNATIONAL GENRE PERFORMANCE, 2014YTD VS 2013YTD

Nielsen BookScan

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

11

Volume 2014YTD

41%

29%

26%

4%

F

T

S

Y

BRAZIL BY PRODUCT CLASS

28%

27%

41%

4%

F

T

S

Y

Value 2014YTD

Nielsen BookScan

23%

18%

8% T6 Religion

5%

F2

Y2

Y5

T6

T17

S5

S4

F1

T4

T1

S2

S1

T9

T2

T5

Volume 2014YTD by mid-level product class

Volume YTD: 12 million Value YTD: R$500 million

Avg. Weekly Sales 2014: 752k, R$31million

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

12

BRAZIL TOP 20 JULY 2013-APRIL 2014

Nielsen BookScan

Pos Title Author Publisher ASP

1 Kairos: O Tempo De Deus Rossi, Padre Marcelo Globo Livros R$16.54

2 Nada A Perder: Meus Desafios Diante Do Impossivel - Livro 2

Macedo, Edir Editora Planeta do Brasil R$27.48

3 A Culpa E Das Estrelas Green, John Intrinseca R$27.44

4 Inferno Brown, Dan Editora Sextante R$34.75

5 Destrua Este Diario Smith, Keri Intrinseca R$23.12

6 Cinquenta Tons De Cinza James, E.L. Intrinseca R$24.24

7 1889 Gomes, Laurentino Globo Livros R$38.49

8 Livro - Dona Benta: Comer Bem - Edicao Especial Completa

Nacional, Editora IBEP R$20.07

9 Cidades De Papel Green, John Intrinseca R$27.14

10 Silencio Das Montanhas, O Hosseini, Khaled Globo Livros R$34.00

11 Cinquenta Tons De Liberdade James, E.L. Intrinseca R$23.90

12 Teorema Katherine, O Green, John Intrinseca R$27.27

13 Cinquenta Tons Mais Escuros James, E.L. Intrinseca R$24.05

14 Pequeno Principe, O Saint-Exupery, Antoine Ediouro Livros R$19.61

15 Casa de Hades, A Riordan, Rick Intrinseca R$35.24

16 Lado Bom Da Vida, O Quick, Matthew Intrinseca R$22.46

17 Casamento Blindado Cardoso, Renato & Cristiane Ediouro Livros R$23.53

18 Eu Nao Consigo Emagrecer Dukan, Pierre Editorial Record R$27.49

19 Quem E Voce Alasca? Green, John WMF Martins Fontes R$28.36

20 Ladrao De Raios, O – Vol 1 Riordan, Rick Intrinseca R$23.51

PRINT TRENDS

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

14

Australia Volume Sales

0

2

4

6

8

10

12

14

16

Adult Fiction Trade Non-Fiction Specialist Non-Fiction Children's Total

Mill

ion

s

2012YTD

2013YTD

2014YTD

AUSTRALIA – RECENT TRENDS Fiction only broad genre in decline

Nielsen BookScan

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

15

India Volume Sales

0

1

2

3

4

5

6

Adult Fiction Trade Non-Fiction Specialist Non-Fiction Children's Total

Mill

ion

s

2012YTD

2013YTD

2014YTD

INDIA – RECENT TRENDS Specialist Non-Fiction leads growth

Nielsen BookScan

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

16

TCM Value Sales

£0

£50

£100

£150

£200

£250

£300

£350

£400

£450

£500

2005YTD 2006YTD 2007YTD 2008YTD 2009YTD 2010YTD 2011YTD 2012YTD 2013YTD 2014YTD

Mill

ion

s UK LONGER TERM TRENDS Year-on-year decline in TCM slowing so far in 2014

Nielsen BookScan

-1.4%

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

17

2014 UK BESTSELLERS

Nielsen BookScan

2014YTD

2013YTD

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

18

Adult Fiction TCM Sales

£0

£20

£40

£60

£80

£100

£120

£140

Mill

ion

s UK LONGER TERM SECTOR TRENDS

Adult Trade Non-Fiction TCM Sales

Nielsen BookScan

£0

£50

£100

£150

£200

£250

Mill

ion

s

-6.3% -4.1%

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

19

FOOD & DRINK LEADS YEAR-ON-YEAR DECLINE IN TRADE NON-FICTION AT -15.1% But Biographies with Atlas, Maps & Travel are leading the long term decline

£0

£20

£40

£60

£80

£100

£120

£140

£160

£180

£200

2009YTD 2010YTD 2011YTD 2012YTD 2013YTD 2014YTD

£18 £19 £24 £19 £21 £18

£25 £22 £21

£19 £17 £17

£18 £17 £17

£17 £16 £16

£24 £19

£20

£18 £16 £16

£15 £14

£14

£14 £13 £13

Mill

ion

s

T18 Fiction Related Items

T2 Dictionaries & Reference

T7 Politics & Government

T10 Mind, Body & Spirit

T12 Transport

T15 Sport

T13 Humour, Trivia & Puzzles

T6 Religion

T3 Literature, Poetry & Criticism

T17 Personal Development

T8 The World / Ideas / Culture: General Interest

T9 Family, Health & Relationships

T11 Leisure & Lifestyle

T5 History & Military

T4 Biographies & Autobiographies

T1 The Arts

T14 Atlases, Maps & Travel

T16 Food & Drink

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

20

Adult Specialist Non-Fiction TCM Sales

£0

£10

£20

£30

£40

£50

£60

£70

Mill

ion

s UK LONGER TERM SECTOR TRENDS

Children’s (Ex. Y5) TCM Sales

Nielsen BookScan

£0

£10

£20

£30

£40

£50

£60

£70

£80

Mill

ion

s

-1.3%

+8.7%

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

21

US Volume Sales

0

50

100

150

200

250

2005YTD 2006YTD 2007YTD 2008YTD 2009YTD 2010YTD 2011YTD 2012YTD 2013YTD 2014YTD

Mill

ion

s US LONGER TERM TRENDS Includes Walmart sales as of 2013

Nielsen BookScan

+0.03%

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

22

US Volume Sales by Product Class 2013YTD

42%

25%

26%

7% Adult Non-Fiction

Juvenile Fiction

Adult Fiction

Juvenile Non-Fiction

US MARKET BY GENRE Juvenile Fiction sales have overtaken Adult Fiction in 2014 so far

41%

28%

23%

8% Adult Non-Fiction

Juvenile Fiction

Adult Fiction

Juvenile Non-Fiction

US Volume Sales by Product Class 2014YTD

Nielsen BookScan

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

23

2014 US BESTSELLERS DOMINATED BY JUVENILE FICTION

Nielsen BookScan

2014YTD

2013YTD

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

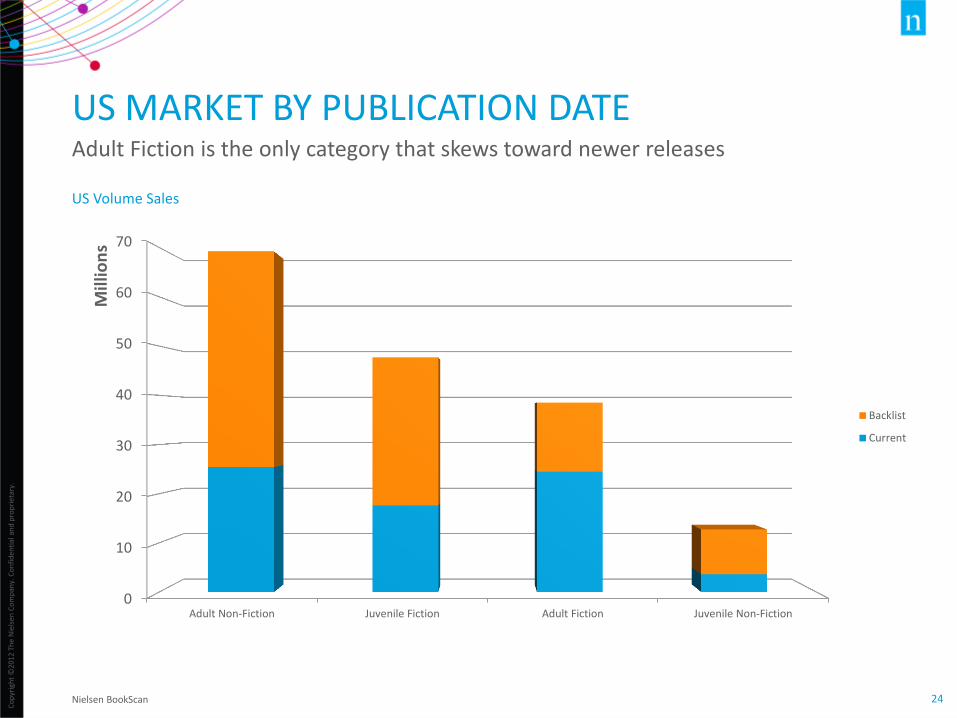

24

US Volume Sales

0

10

20

30

40

50

60

70

Adult Non-Fiction Juvenile Fiction Adult Fiction Juvenile Non-Fiction

Mill

ion

s

Backlist

Current

US MARKET BY PUBLICATION DATE Adult Fiction is the only category that skews toward newer releases

Nielsen BookScan

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

25

US Volume Sales by Publisher

0

10

20

30

40

50

60

Mill

ion

s

2013YTD

2014YTD

TOP 10 US PUBLISHERS IN 2014 SO FAR Four of the top publishers in growth on 2013

Nielsen BookScan

+3.1%

+12.2%

+8.8% +8.4%

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

26

US Volume Sales – Adult Fiction

0

10

20

30

40

50

60

70

2005YTD 2006YTD 2007YTD 2008YTD 2009YTD 2010YTD 2011YTD 2012YTD 2013YTD 2014YTD

Mill

ion

s US LONGER TERM SECTOR TRENDS Includes Walmart sales as of 2013

Nielsen BookScan

-13.1%

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

27

2014 US FICTION BESTSELLERS

Nielsen BookScan

2014YTD

2013YTD

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

28

US Volume Sales – Adult Fiction

0

2

4

6

8

10

12

Mill

ion

s

2013YTD

2014YTD

US ADULT FICTION BY CATEGORY Graphic Novels and Westerns are the only categories in growth

Nielsen BookScan

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

29

Percent Growth in Volume Sales

GRAPHIC NOVELS SEE INTERNATIONAL GROWTH Eight out of ten territories have increased sales so far in 2014

Nielsen BookScan

0% 10% 20% 30% 40%

ES

IN

US

ROI

UK

AUS

IT

NZ

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

30

US Volume Sales – General Fiction

-35.1%

+11.1% -13.7%

+42.8%

+14.1%

Literary Historical General Contemporary Women Short Stories (single author) Sagas Humorous Family Life Coming of Age Erotica African American / Urban Media Tie-In Anthologies (multiple authors) Urban African American / Contemporary Women Biographical Political Gay Alternative History Dystopian Native American & Aboriginal African American / General African American / Historical Mashups Amish & Mennonite Cultural Heritage Lesbian Sports Holidays African American / Erotica Satire Sea Stories

US GENERAL FICTION BY BISAC DESCRIPTION Literary and Historical account for almost half of General Fiction sales 2014YTD

Nielsen BookScan

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

31

US Volume Sales – Adult Non-Fiction

0

10

20

30

40

50

60

70

80

90

100

2005YTD 2006YTD 2007YTD 2008YTD 2009YTD 2010YTD 2011YTD 2012YTD 2013YTD 2014YTD

Mill

ion

s US LONGER TERM SECTOR TRENDS Includes Walmart sales as of 2013

Nielsen BookScan

-1.3%

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

32

2014 US NON-FICTION BESTSELLERS

Nielsen BookScan

2014YTD

2013YTD

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

33

US Volume Sales – Adult Non-Fiction

0

2

4

6

8

10

12

Mill

ion

s

2013YTD

2014YTD

US ADULT NON-FICTION BY CATEGORY Already a top category, Religion/Bibles grew 8.3% on 2013YTD

Nielsen BookScan

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

34

US Volume Sales – Religion/Bibles

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Mill

ion

s

2013YTD

2014YTD

TOP IMPRINTS IN RELIGION/BIBLES Thomas Nelson up 34% year-on-year; only two imprints of top ten in decline

Nielsen BookScan

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

35

Percent Growth in US Volume Sales – Self-Help

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Personal Growth / General

Personal Growth / Success

Motivational & Inspirational

Creativity

Personal Growth / Happiness

General

Personal Growth / Self-Esteem

Spiritual

Sexual Instruction

Mood Disorders / General

GROWTH IN SELF-HELP BOOKS More than half of top categories up on 2013

Nielsen BookScan

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

36

US Volume Sales – All Juvenile

0

10

20

30

40

50

60

70

2005YTD 2006YTD 2007YTD 2008YTD 2009YTD 2010YTD 2011YTD 2012YTD 2013YTD 2014YTD

Mill

ion

s US LONGER TERM SECTOR TRENDS Includes Walmart sales as of 2013

Nielsen BookScan

+11.9%

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

37

YTD Volume Sales in Y Children’s, Young Adult & Educational/All Juvenile (US)

0 10,000,000 20,000,000 30,000,000 40,000,000 50,000,000 60,000,000

US

UK

AUS

IN

ROI

2014YTD

2013YTD

GROWTH IN INTERNATIONAL CHILDREN’S MARKET Five territories up year-on-year in Children’s sector

Nielsen BookScan

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

38

US Volume Sales – Juvenile Fiction

0

5

10

15

20

25

30

35

40

45

50

2011YTD 2012YTD 2013YTD 2014YTD

Mill

ion

s

Holidays/Festivals/Religion

Concepts

Animals

Classics

History/Sports/People/Places

Social Situations/Family/Health

Science Fiction/Fantasy/Magic

General

US JUVENILE FICTION BY CATEGORY Science Fiction/Fantasy/Magic up 47% on 2013

Nielsen BookScan

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

40

US Volume Sales – All Juvenile

0

0.5

1

1.5

2

2.5

3

Mill

ion

s

2013YTD

2014YTD

DIVERGENT CARRIES VERONICA ROTH TO TOP AUTHOR IN JUVENILE FICTION New entries in top ten for 2014: Roth, Green, Riggs, Zusak

Nielsen BookScan

E-BOOKS IN THE US

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

42

0

5

10

15

20

25

30

35

40

45

50

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Jan-14

%

Volume

Value

E-BOOK SHARE OF US BOOK PURCHASES

Source: US Books & Consumers © Nielsen 2014 2014 data provisional and require caution

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

43

0

10

20

30

40

50

60

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Jan-14

%

Adult fiction

Adult NF

Children's

E-BOOK SHARE OF US BOOK PURCHASES, WITHIN CATEGORY: VOLUME

Source: US Books & Consumers © Nielsen 2014 2014 data provisional and require caution

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

44

E-BOOK SHARE OF US BOOK PURCHASES WITHIN GENRE: VOLUME, Y/E JAN 2014

Source: US Books & Consumers © Nielsen 2014

35%+

Crime

SF

Romance

25-34%

Thriller

General fiction

Historical fiction

Fantasy

Horror

Action/adventure

Christian fiction

Children’s fiction

True crime

10-24%

Biography

Fitness/health

Religion/MBS

Sport

Humour

IT/business

YA fiction

Literary fiction

History

Travel

Cookery

Self help

Art

Children’s NF

<10%

Graphic novel

Bibles

Science/nature

Home/garden

Picture books

Early learning

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

45

44%

70%

5%

26%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Jan-14

Smartphone

Tablet

eReader

HOUSEHOLD OWNERSHIP AMONG US BOOK BUYERS

Source: US Books & Consumers © Nielsen 2014

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

46

68

35

42

4 7

0

10

20

30

40

50

60

70

80

90

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Jan-14

% eReader

Tablet

SmartPhone

DEVICE SHARE OF US E-BOOK PURCHASES

Source: US Books & Consumers © Nielsen 2014

E-BOOKS IN THE UK

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

48

Cumulative Volume sales of e-books among the UK population aged 13-79

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

23

-Jan

-11

20

-Fe

b-1

1

20

-Mar

-11

17

-Ap

r-1

1

15

-May

-11

12

-Ju

n-1

1

10

-Ju

l-1

1

07

-Au

g-1

1

04

-Se

p-1

1

02

-Oct

-11

30

-Oct

-11

27

-No

v-1

1

25

-De

c-1

1

22

-Jan

-12

19

-Fe

b-1

2

18

-Mar

-12

15

-Ap

r-1

2

13

-May

-12

10

-Ju

n-1

2

08

-Ju

l-1

2

05

-Au

g-1

2

02

-Se

p-1

2

30

-Se

p-1

2

28

-Oct

-12

25

-No

v-1

2

23

-De

c-1

2

20

-Jan

-13

17

-Fe

b-1

3

17

-Mar

-13

14

-Ap

r-1

3

13

-May

-13

09

-Ju

n-1

3

07

-Ju

l-1

3

04

-Au

g-1

3

01

-Se

p-1

3

29

-Se

p-1

3

27

-Oct

-13

24

-No

v-1

3

22

-De

c-1

3

19

-Jan

-14

125.1m

Fiction Non-fiction Children's

GROWTH AND COMPOSITION OF UK E-BOOK MARKET, JAN 2011- JAN 2014

Nielsen Insight into the E-book Consumer Market

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

50

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

23

-Jan

-11

20

-Fe

b-1

1

20

-Mar

-11

17

-Ap

r-1

1

15

-May

-11

12

-Ju

n-1

1

10

-Ju

l-1

1

07

-Au

g-1

1

04

-Se

p-1

1

02

-Oct

-11

30

-Oct

-11

27

-No

v-1

1

25

-De

c-1

1

22

-Jan

-12

19

-Fe

b-1

2

18

-Mar

-12

15

-Ap

r-1

2

13

-May

-12

10

-Ju

n-1

2

08

-Ju

l-1

2

05

-Au

g-1

2

02

-Se

p-1

2

30

-Se

p-1

2

28

-Oct

-12

25

-No

v-1

2

23

-De

c-1

2

20

-Jan

-13

17

-Fe

b-1

3

17

-Mar

-13

14

-Ap

r-1

3

13

-May

-13

09

-Ju

n-1

3

07

-Ju

l-1

3

04

-Au

g-1

3

01

-Se

p-1

3

29

-Se

p-1

3

27

-Oct

-13

24

-No

v-1

3

22

-De

c-1

3

19

-Jan

-14

UK MARKET PENETRATION OF E-BOOKS Percentage of the UK population aged 13-79 that have bought an e-book: Jan 2011-2014

22%

Nielsen Insight into the E-book Consumer Market: May 2014

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

51

Numbers of individuals aged 13-79 entering the e-book market: period-on-period growth in population number terms

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Jan

11

Feb

11

Mar

11

Ap

r 1

1

May

11

Jun

11

Jul 1

1

Au

g 1

1

Sep

11

Oct

11

(1)

Oct

11

(2)

No

v 1

1

Dec

11

Jan

12

Feb

12

Mar

12

Ap

r 1

2

May

12

Jun

12

Jul 1

2

Au

g 1

2

Sep

12

(1

)

Sep

12

(2

)

Oct

12

No

v 1

2

Dec

12

Jan

13

Feb

13

Mar

13

Ap

r 1

3

May

13

Jun

13

Jul 1

3

Au

g 1

3

Sep

13

(1

)

Sep

13

(2

)

Oct

13

No

v 1

3

Dec

13

Jan

14

Feb

-14

Mar

-14

Ap

r-1

4

May

-14

Jun

-14

Jul-

14

Au

g-1

4

Sep

14

(1

)

Sep

14

(2

)

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

New buyers projected to fall below 100k throughout 2014

Nielsen Insight into the E-book Consumer Market: May 2014

Forecasted E-book Adoption

GROWTH IN E-BOOK BUYERS SLOWING

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

52

0

5

10

15

20

25

30

35

40

45

50

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Jan-14

%

Volume

Value

E-BOOK SHARE OF UK BOOK PURCHASES

Source: UK Books & Consumers © Nielsen 2014 2014 data provisional and require caution

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

53

0

10

20

30

40

50

60

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Jan-14

%

Adult fiction

Adult NF

Children's

E-BOOK SHARE OF UK BOOK PURCHASES, WITHIN CATEGORY: VOLUME

Source: UK Books & Consumers © Nielsen 2014 2014 data provisional and require caution

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

54

E-BOOK SHARE OF UK BOOK PURCHASES WITHIN GENRE: VOLUME, Y/E JAN 2014

Source: UK Books & Consumers © Nielsen 2014

45%+

Crime

Fantasy

Romance

25-44%

Thriller

General fiction

Historical fiction

Erotic fiction

Horror

Classic fiction

Sci fi

True crime

Self help

10-24%

Biography

Fitness/diet

Religion/MBS

Sport

Humour

IT

YA fiction

<10%

Graphic novel

Food & drink

Science/nature

Travel

Art

Business

Home/garden

Picture books

Children’s NF

Early learning

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

55

46

61

14

51

21 24

0

10

20

30

40

50

60

70

80

90

100

%

Smartphone

Tablet

eReader

HOUSEHOLD OWNERSHIP AMONG UK BOOK BUYERS

Source: UK Books & Consumers © Nielsen 2014

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

56

84

47

40

5 8

0

10

20

30

40

50

60

70

80

90

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Jan-14

% eReader

Tablet

SmartPhone

DEVICE SHARE OF UK E-BOOK PURCHASES

Source: UK Books & Consumers © Nielsen 2014

THOUGHTS ABOUT THE FUTURE

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

58

CHANGING FACE OF THE AMERICAN CONSUMER

With important implications on the future …

URBANIZATION & INDUSTRIALIZATION

DECLINING BIRTH RATES

AGING POPULATION

Uneven Population Growth

Older Consumers With New Needs

Changes in Per Household Spending

Immigration & Growth in

Ethnic Families

Declining % of HHs with Children

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

59

KEY ATTRIBUTES OF TWO SPENDING POWERHOUSES

Hardwired Untethered

By Appointment Always On

Listeners Sharers

Physical Virtual

BOOMERS MILLENNIALS

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

61

DO YOU KNOW YOUR CATEGORY’S ENTHUSIAST?

Source: FreshFacts® Shopper Insights powered by Spire, 52 weeks ending 8/10/13

1% of muffin buyers

23% of muffin sales

account for

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

62

DO YOU KNOW YOUR BOOK ENTHUSIAST?

Source: FreshFacts® Shopper Insights powered by Spire, 52 weeks ending 8/10/13

1% of book buyers

15% of book sales

account for

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

63

THE WORLD IS YOUR OYSTER

Source: BBC

• 2.0bn people learning English

• 600m as first language

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

64

Our brains process 11,000,000 bits of sensory information every second.

But our conscious minds can only handle about 40 bits per second.

That’s a selection ratio of 0.000004%.

What happens to the other 10,999,960 bits of information?

Consumer brains process them subconsciously.

The majority of processing is subconscious

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

65

TWO THINGS WE HAVE LEARNED FROM NEUROSCIENCE

Milliseconds matter

We make decisions differently than we thought

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

66

If this is true, our goal is to

persuade.

TRADITIONAL VIEW

THINK

ACT

FEEL

If this is true, our goal is to

engage emotion.

EMERGING VIEW (FROM COGNITIVE SCIENCE)

FEEL

ACT

THINK Rationalize Our

Decisions

EMOTIONS LEAD, REASON FOLLOWS

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

68

SUMMARY – OPTIMISTIC!!

• Global consumer confidence is patchy but improving

• English language markets are huge and digital makes them reachable

• Traditional book markets are flat – some in decline

• Emerging markets are growing fast

• ebooks will continue to grow – but pace will be wildly different in each market

• Consumer $ is moving from boomer to millennial – maximise boomer spend now!

• We will need to publish and sell books differently … as we compete for consumer time and $ …

Jonathan Nowell BookExpo America

28 May 2014

Booth1113