Be Cool and Calculating

33

Be Cool and Calculating What some experienced Accounting teacher think you will need to concentrate on during your studies

-

Upload

germane-olson -

Category

Documents

-

view

16 -

download

0

description

Be Cool and Calculating. What some experienced Accounting teacher think you will need to concentrate on during your studies. Attempt past exams and practice exam. Under exam conditions to get use to completing them in the time limit. - PowerPoint PPT Presentation

Transcript of Be Cool and Calculating

Be Cool and Calculating

What some experienced Accounting teacher think you will need to

concentrate on during your studies

Attempt past exams and practice exam

• Under exam conditions to get use to completing them in the time limit.

• Every year the Examiners say student’s marks fall toward the end of the exam, because they have run out of time.

• I have some that you will not get off the website so just ask.

The Exam will be 2 hours long

• The Exam will cover Unit 3 & 4.• You can do the Exam questions in what ever

order you prefer but you must attempt every question.

Know your Accounting Principles and Qualitative Characteristics

• COM, REL, U Characteristics– Comparability– Relevance– Reliability– Understandability

• The others are Accounting Principles!– C @ HER MCG

Link the Accounting Principles and Qualitative Characteristics

• To the various topics and be prepared to explain why these items exist.

Understandability

• The setting out of the reports so that people who are not accountant can understand.– Balance Sheet fully classified with headings– Income Statement with headings– Cash Flow with appropriate headings

Entity

• The Balance Sheet – the business assets & liabilities are separate from the owner’s.

• Sales of a non-current asset – the residual value that we sell the NCA for now belongs to another business / entity.

Reporting Period

• Revenue & expense – earned or incurred in the current reporting period are matched to calculate profit.

• Balance Day Adjustments – revenue & expense items are made more accurate and matched to calculate profit.

Comparability

• Using the same Depreciation method each year consistently means reports can be compared.

• Using Control and Subsidiary accounts allows for comparing & checked

Think about the theory behind the practical

• Why do we use perpetual inventory? What is perpetual inventory?

• Why do some businesses use Control accounts? Why do we have subsidiary accounts if we already have the general ledger?

Journals

• General Journal entries are always popular.

GST

• Is not recorded on stock cards or in Stock Control.

• Check the GST at the start in the Balance Sheet from the previous year.

Depreciation

• If a Non Current Asset is bought part way through the year, then it will be depreciated for part of the year.

• If a Non Current Asset is sold in the middle of the year, then it will be depreciated for part of the year.

Disposal of a NCA

• If the NCA is sold, then an amount received is recorded in the Cash Receipts Journal.

• If the NCA is traded-in to the Sundry Creditor, then the value will be mentioned on the invoice for the purchase of the new NCA.

• If the NCA is written off, there will be no value.

Purchase of a new Non Current Asset

• You may be presented with an invoice that will include a deposit (record in Cash Receipts Journal).

• The remainder is owed to the Sundry Creditor.• There may be discount so watch for 2/7, n/30.• There will be GST on the purchase of a Non

Current Asset.

Accounting Reports

• Go to Template of Reports• Be familiar with the format of each• Be ready to reconstruct accounts• Don’t forget Variance reports and what they

show the owner.• How do BDA Adjustments affect Income

Statement and Balance Sheet?

Cash Versus Profit

• Can a business make a profit and have little or no cash?

• Can another business have plenty of cash but make a loss?

• What about Net Cash from Operation being positive but the business has a overdraft?

• How can these events happen?

Performance analysis

• The ratios will NOT be included in the exam.• Read the list of ratios from the photocopy I

gave you or the wiki then memorise them.• If you read the list every day, you will have a

good chance of remembering them.

Performance analysis

• Analyse the data• Interpret the results• Discuss them in relation to the needs of the

business (how improve?) and the owner.• Why has Return on Assets decreased?• How could the owner improve collections

from debtors?

Performance Analysis

• If you are asked to discuss a particular issue and you are making either positive or negative statements, make sure you provide supporting evidence to justify your statement.

• Refer to the data presented in the question to strengthen your point of view.

• IDL answers:– Identify– Define – Link

Stock Cards will include:

• Sales returns• Purchase returns• Period costs• Product costs• FIFO• Reversing FIFO

• Make sure you are very familiar how these are recorded on the Stock cards.

Product Costs

• Those costs that– can be logically applied to the stock– assist in getting the stock into position and

condition for sale

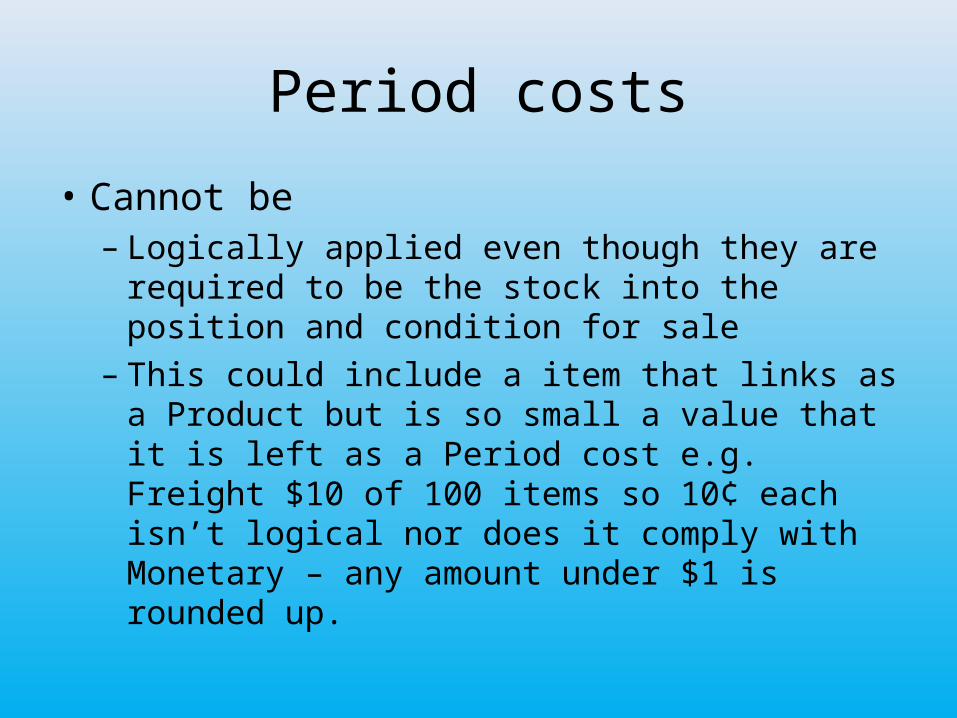

Period costs

• Cannot be– Logically applied even though they are required to

be the stock into the position and condition for sale

– This could include a item that links as a Product but is so small a value that it is left as a Period cost e.g. Freight $10 of 100 items so 10¢ each isn’t logical nor does it comply with Monetary – any amount under $1 is rounded up.

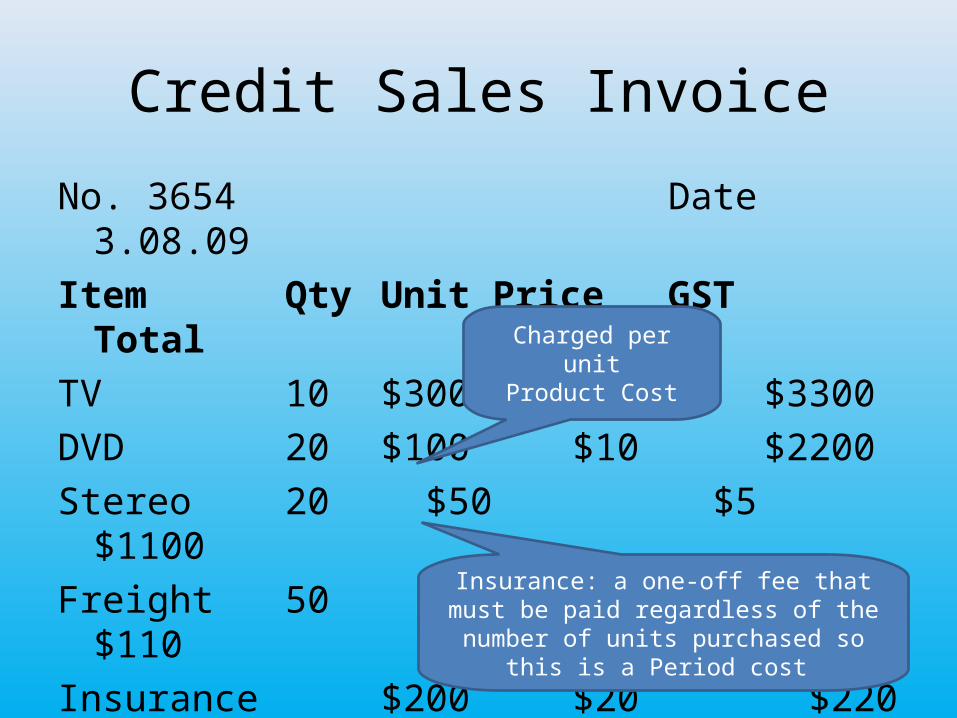

Credit Sales Invoice

No. 3654 Date 3.08.09Item Qty Unit Price GST TotalTV 10 $300 $30 $3300DVD 20 $100 $10 $2200Stereo 20 $50 $5 $1100Freight 50 $2 .20¢ $110Insurance $200 $20 $220Total $6930

Charged per unitProduct Cost

Insurance: a one-off fee that must be paid regardless of the number of units purchased

so this is a Period cost

Also, in the Answer Booklet

• If students are asked to record this transaction in the Journals, the Answer Booklet will provide a Purchases Journal and a General Journal.

• Both Journals must be used – the examiners wouldn’t provide both if they didn’t expect both to be used.

Purchase of a Non-current assets on credit

• Usually in combination with – the disposal / trade-in of a Non-current asset– and calculation of depreciation.

When a purchase is made, check

• If stock is being purchased for resale:– Credit Purchase of stock > Purchases Journal >

Creditors Control account

• If a non-current asset is being purchase to be used to earn revenue:– Credit Purchase of non-current asset > General

Journal > Sundry Creditors account

BDA

• Prepaid expenses• Accrued expenses• Prepaid revenue• Accrued revenue• Stock Write Down• Bad Debts• Stock Losses• Stock Gains

Prepaid Revenue

• Students do badly in this area.• For 2007 & 2008 exams this was examined by

looking at stock sold on credit.

Prepaid Sales - where

– Stock was ordered for delivery and payment at a later date,

– Paid a deposit when the stock was ordered,– Received some of the stock ordered (and an

Invoice has accompanied the stock),– Paid the balance owing on the Invoice.

All of these transactions occur over two reporting periods.

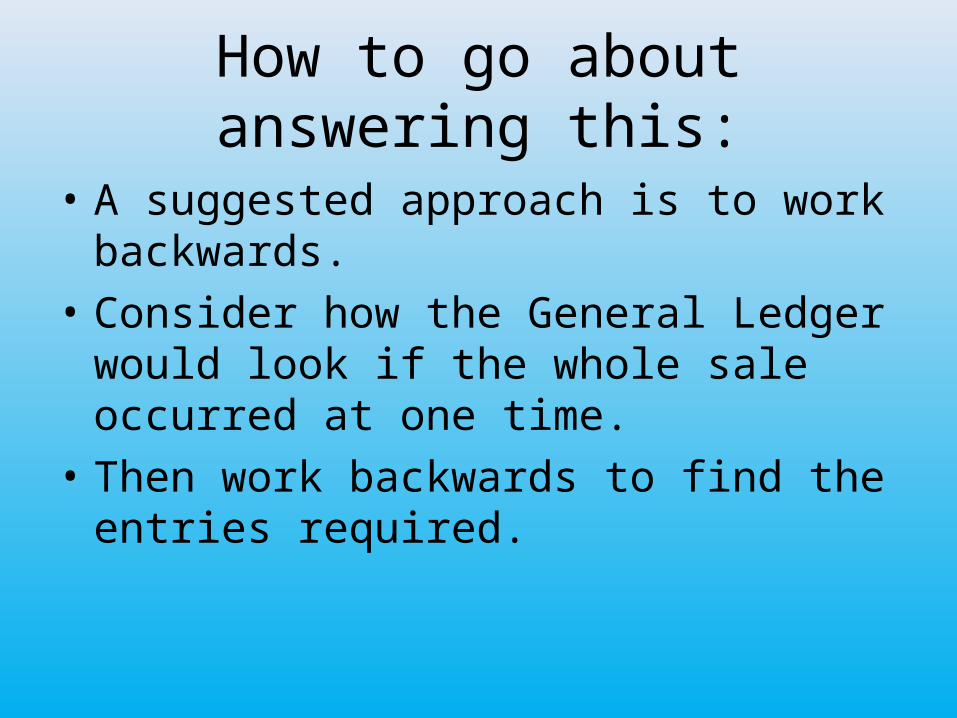

How to go about answering this:

• A suggested approach is to work backwards.• Consider how the General Ledger would look

if the whole sale occurred at one time.• Then work backwards to find the entries

required.

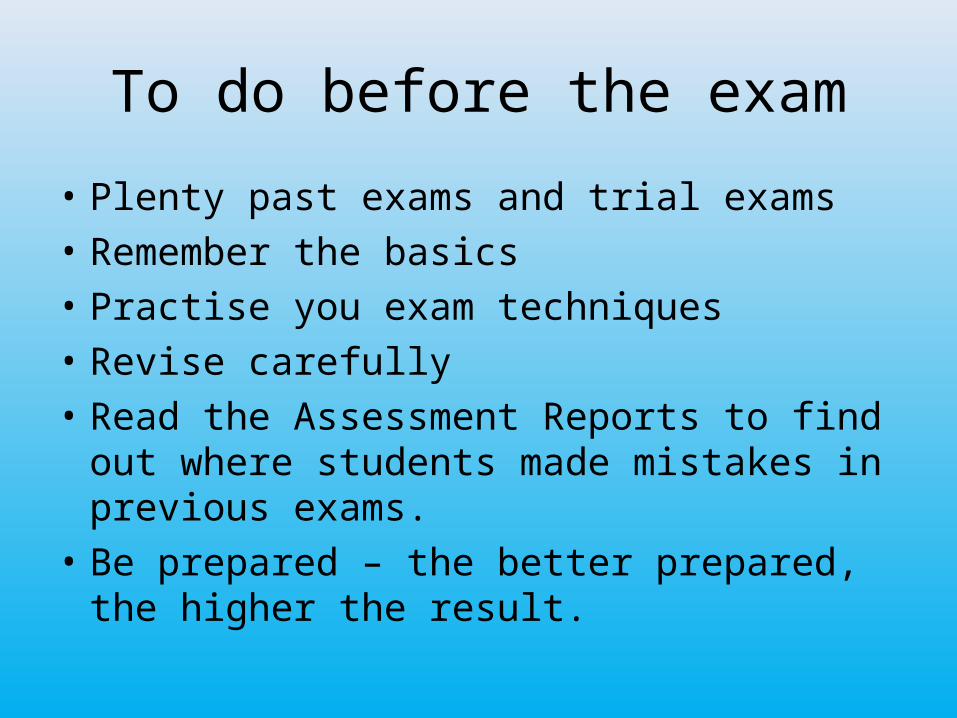

To do before the exam

• Plenty past exams and trial exams• Remember the basics• Practise you exam techniques• Revise carefully• Read the Assessment Reports to find out where

students made mistakes in previous exams.• Be prepared – the better prepared, the higher

the result.

The Exam Date

•Monday, November 11th 11.45am to 2.00pm

• Difficult time of day – you will be hungry• Eat something healthy before the exam– Avoid the sugary snacks that make you jittery