Basic Financial Statements December 31,...

37

LASALLE PARISH SEWERAGE DISTRICT No. 1 Basic Financial Statements December 31, 2012

Transcript of Basic Financial Statements December 31,...

LASALLE PARISH SEWERAGE

DISTRICT No. 1

Basic Financial Statements

December 31, 2012

LASALLE SEWERAGE DISTRICT NO. 1 TROUT, LQUISL4NA

c ^ f : ^ ^

* LaSalle Sewei^ge District No, 1

LaSalie Sewerage District No. 1 was created by the LaSalle Parish Police Jury, as authorized by Louisiana Revised Statute 33:4562. The Sewerage District is administered by a board of commissioners who are appointed by the LaSalle Parish Police Jury, The district owns and operates sewerage facilities and engages in activities designed to provide sewerage disposal to the Trout, Goodpine and Midway Communities.

LASALLE PARISH SEWERAGE DISTRICT NO. 1 LASALLE PARISH POLICE JHURY

TROUT, LOUISIANA

C O N T E N T S

Independent Auditor's Report

Management's Discussion & Analysis

Basic Financial Statements

Statement of Net Position

Statement of Activities

Balance Sheet -- Governmental Funds

Reconciliation of the Govemment Fund Balance Sheet to the Government-Wide Financial Statement of Net Position

Statement of Revenues, Expenditures and Changes in Fund Balances - Govemmental Fund

Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances Of Governmental Funds to the Statement of Activities

Statement ofNet Position-Proprietary Funds

Statement of Revenues, Expenditures, and Changes in Net Position - Proprietary Fund

Statement of Cash Flows

Reconciliation of Cash Flows

Notes to the Basic Financial Statements , ,

Other Reports

Report On Internal Control Over Financial Reporting And On Compliance And Other Matters Based On An Audit Of Financial Statements Performed In Accordance With Govemment Auditing Standards

Schedule of Findings and Questioned Cost

Management's Corrective Action for Current Year Audit Findings

Management's Summary of Prior Year Findings

STATEMENT

D

E

PAGE#

1-2

3-6

A

B

C

8

9

10

n

12

F

G

H

I

13

14

15

16

17

18-27

29-30

31-32

33

34

JohnR VercherCPA THE VERCHER GROUP MEMBERS jrvtu>.centurylel.net t n j - • t ^ j - JT

A Professional Corporation of American institute of Jonathan M. Vercher M.S., C.P.A. Certified Public Accoiiutailts Certified Public Accountants [email protected] p Q ggx 1608

1737 N i " ' St - Suite A ^°'''^^^' ̂ '"̂ '̂ "'̂ '''"̂ David R. VercherM.B.A., C.P.A. -, i • •' n -̂xi-y Certified Public Accountants

Jena, Louisiana 71342 davidvercher@}'iiiail.coin Te!: (318) 992-6348

Fax:(318)992-4374

INDEPENDENT AUDITOR'S REPORT

LaSalle Parish Sewerage Dishict No. 1 Trout, Louisiana

Report on the Financial Statements

We have audited the accompanying financial statements of the govemmental and business-type activities of the LaSalle Parish Sewerage District No. 1, as of and for tlie year ended December 31, 2012, and the related notes to the financial statements, wliich collectively comprise the District's basic financial statements as listed in the table of contents.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to tlie preparation and fair presentation of financial statements that are free fi'om material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express opinions on tliese financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of tlie United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the fmancial statements. The procedures selected depend on tlie auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whetlier due to fraud or eiTor, In making those risk assessments, the auditor considers intemal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose ofexpresslng an opinion on the effectiveness of the entity's intemal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating die overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In otu- opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the govemmental and business-type activities of the LaSalle Parish Sewerage District No. 1, as of December 31, 2012, and the respective changes in financial position, and, where applicable, cash flows thereof for tlie year then ended in accordance with accounting principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America requne tliat the management's discussion and analysis be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to tlie required supplementary infonnation in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the infomiation and comparing the information for consistency with management's responses to our inquiries, the basic financial statements, and other Icnowledge we obtained during our audit of tlie basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us witli sufficient evidence to express an opinion or provide any assurance.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated May 24, 2013, on our consideration of the LaSalle Paiish Sewerage District No. I's intemal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and otiier matters. The purpose of that report is to describe the scope of our testing of intemal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on intemal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Goverivnent Auditing Standards in considering the LaSalle Parish Sewerage District No. I's internal control over financial reporting and compliance.

l̂ fie Vercfier (^roup Jena, Louisiana May 24, 2013

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISIANA

M A N A G E M E N T ' S D I S C U S S I O N AND A N A L Y S I S

As management of the District, we offer readers of the LaSalle Sewage District No. 1 financial statements this narrative overview and analysis of the financial activities of the District for the fiscal year ended December 31, 2012. We encourage readers to consider tiie information presented here in conjimction with the District's audited financial statements.

The Management's Discussion and Analysis (MD&A) is an element of the new reporting model adopted by the Governmental Accounting Standards Board (GASB) in their Statement No. 34 Basic Financial Statements - and Management's Discussion and Analysis - for State and Local Govemments issued June 1999. Certain comparative information between the current year and the prior year is required to be presented in the MD&A.

FINANCIAL HIGHLIGHTS

The assets of the District exceeded its liabilities at the close of the most recent fiscal year by $981,064 {netposition). This amotmt represents $935,516 net position for tiie business-type activities and $45,548 net position for the govemmental activities.

The District had total revenue of $14,740 in its govemmental fund and $284,623 in its enterprise fimd, including interest income of $464.

Expenses for the govemmental fi.ind totaled $8,775, while expenses for the enterprise fund totaled $254,554, including depreciation expense in tiie amount of $69,032, wliich is a non-cash transaction.

The change in net position of the governmental fund was $5,965, while tiie change in net position of the enterprise fimd was $30,069.

OVERVIEW OF THE FINANCIAL STATEMENTS

This discussion and analysis is intended to serve as an introduction to the District's basic financial statements. The District's basic financial statements consist of two components: 1) fiind financial statements, and 2) notes to the financial statements. This report also contains other supplementary information in addition to the basic financial statements themselves. The District is a special-purpose entity engaged in business-type and govemmental activities. Accordingly, only fimd financial statements are presented as the basic financial statements.

Effective, December 31, 2004, the District adopted Govemmental Accounting Standards (GASB) Statement No. 34, Basic Firiancial Statements ~ Management's Discussion and Analysis - for State and Local Govei-nments.

MD&A

Table 1 Balance Sheet (Enterprise Fund)

The following table represents a Comparative Balance Sheet as of December 31,2012:

2011 2012 % Change Assets Current Assets Restricted Assets Capital Assets, Net Total Assets

Liabilities & Net Position Current Liabilities Current Liabilities Payable From Restricted Assets Long-Term Liabilities Total Liabilities

Net Position Invested in Capital Assets, Net of Related Debt Restricted for Debt Service Unrestricted Total Net Position

Total Liabilities & Net Position

Table 2 Changes in Net Position (Enterprise Fund)

The following table reflects the Comparative Statement of Revenues, Expenses, and Changes in Net Position for the year ended December 31,2012:

81,553 $ 226,622

1,272,026 1,580,201

10,904 95,689

564,856 671,449

661,436 127,359 119,957 908,752

1,580,201 $

114,894 242,068

1,206,424 1,563,386

13,629 97,120 517,121 627,870

642,568 141,258 151,690 935,516

1,563,386

40.9 6.8 -5.2 -1.1

25.0 1.5 -8.5

-6.5

-2.9 10.9 26.5 2.9

-1.1

2011 2012 Revenues Operating Revenues Non-Operating Revenues Total Revenues

Expenses Operating Expenses Non-Operating Expenses Total Expenses

hicrease (Decrease) in Net Position

Prior Period Adjustment

Beginning Net Position Ending Net Position

% Change

$ 258,804 $

780 259,584

255,813

32,470

288,283

(28,699)

-0-

937,451

$ 908,752 S

284,159

464 284,623

225,728

28,826

254,554

30,069

(3,305)

908,752

935,516

9.8 -40.5

9.6

-11.8

-11.2

-11.7

204.8

-100.0

-3.1

2.9

MD&A

Table 3 Balance Sheet {Debt Service Fund)

The following table represents a Comparative Balance Sheet as of December 31, 2012;

Assets 2011 2012 % Change Casli & Casii Equivalents Receivables (Net of Allowances) Total Assets

Liabilities & Net Position Current Liabilities Total Liabilities

Fund Balances Restricted For Debt Service Total Liabilities & Fund Balances

$

$

57,628 $ 11,698 69,326

403 403

68,923 69,326 $

60,427 14,965 75,392

503 503

74,889 75,392

4.9 27.9

8.7

24.8 24.8

8.7 8.7

Table 4 Changes in Fund Balance (Debt Service Fund)

The following table reflects the Comparative Statement of Revenues, Expenditures, and Changes in Ftmd Balances forthe year ended December 31, 2012:

2011 2012 % Change Revenues Ad Valorem Taxes Total Revenues

Expenditures Bond Payment Principle Bond Payment Interest Total Expenditures

Net Change in Fund Balance

Fund Balances - Beginning Fund Balances - Ending

$

$

10,933 $ 10,933

-0-1,775 1,775

9,158

59,765 68,923 $

14,740 14,740

7,000 1,775 8,775

5,965

68,923 74,888

34.8 34.8

100.0 0.0

394.4

-34.9

15.3 8.7

MD&A

DEBT SERVICE FUND

The District maintains a debt service fund wliich collects ad valorem taxes in order to service the debt of tiie general obligation loans outstanding. As of December 31, 2012, the District had $28,496 in general obligation bonds payable.

USING THIS ANNUAL REPORT

The District's aimual report consists of financial statements tiiat show information about the District's flinds, an enterprise fund and a govemmental fund.

Our auditor has provided assurance in his independent auditor's report, located immediately following this Management's Discussion and Analysis, that the Basic Financial Statements are fairly stated. Varying degrees of assurance are being provided by the auditor regarding the other information included in tills report. A user of tills report should read the independent auditor's report carefully to ascertain the level of assurance being provided for each of tiie other parts of tiiis report.

CAPITAL ASSETS

Capital Assets

At December 31,2012, the District had $ 1,206,424 invested in a broad range of capital assets, including the sewer system, leasehold improvements, and equipment. This amount represents a net decrease (including additions, deductions and depreciation) of $65,602, or 5.2% from last year.

Capital Assets at Year-End 2011 2012

Sewer System, Machinery & Equipment $ 3,262,321 $ 3,265,751 Accumulated Depreciation (1,990,295) (2,059,327) Total Capital Assets, Net $ 1,272,026 $ 1,206,424

CONTACTING THE SEWER DISTRICT'S FINANCIAL MANAGEMENT

Our fmancial report is designed to provide our citizens, taxpayers, and creditors with a general overview of the LaSalle Sewerage District No. I's finances and to show the Districts accountability for the money it receives. If you have questions about this report or wish to request additional financial information, contact Sharon Keel, Clerk, at the Sewerage District, PC Box 1, Trout, Louisiana 71371, telephone number (318) 992-4777.

Statement A LASALLE PARISH SEWERAGE DISTRICT NO. 1

TROUT, LOUISIANA

Statement of Net Position December 31,2012

PRIMARY GOVERNMENT

ASSETS Cash & Cash Equivalents $ Receivables (Net of Allowances for UncoUectable) Restricted Receivables Restricted Cash Capital Assets (Net of Accumulated Depreciation) TOTAL ASSETS

LrABILITIES Accounts, Salaries, & Other Payables Accrued Interest Other Liabilities Customer Deposits Notes & Bonds Due Within One Year Notes & Bonds Due in More Than One Year T O T A L LrAB[LiTiEs

NET POSITION Invested in Capital Assets, Net of Related Debt Restricted Net Position Unrestricted Net Position TOTAL NET POSITION $

Governmental Activities

-0- $ -0-

14,965 60,427

-0-75,392

-0-845 503 -0-

7,000 21,496 29,844

-0-67,547

(21,999) 45,548 $

Business-Type Activities

41,512 $ 73,382

-0-242,068

1,206,424 1,563,386

11,611 21,389 2,018

28,996 46,735

517,121 627,870

642,568 141,258 151,690 935,516 $

Total

41,512 73,382 14,965

302,495 1,206,424 1,638,778

11,611 22,234 2,521

28,996 53,735

538,617 657,714

642,568 208,805 129,691 981,064

The accompanying notes are an integral part of this statement.

a Si

B a

( S

C f l

O

%-• u

t4H

o - M

a V

o M

1—(

(^ I^ U

X I

a (U

u Q T3 (U

-o e

S w u

1/3

u,

^ V

^ • * -

Ul

o ^

t t . o « o z

Si a 2:

I H

n o

/—̂ J . oo o o

' i n

'—• s '

,—̂ 0 0 o " O 1 — 4

*'—̂

v^ u

OJ t s

&•-t-..£: H tJ

<:

1 t

o o 1 1 o '

(U U

S .Si

U

c

K

6Q

9 g

/̂ ^ tn u S* 3 ^ e H E

1 f — >

O CO

' o i n

' '

,̂̂ ^ oo o i n

" '

(A c

^ 6 3 .S "•5 -iS 3 2 e 5 U R L. C. ^ "S O ^ g

u

1 1

o o 1

o I

w

o g

, — . , — 1

r : t > 0 a\ r-\ LO DO

so oo — r ' l ' . ' v '

'—̂ o O l " n »n • *

^ '

,-_, CO O l

o r~-2^

as o r-l

Os - t t >n • o r -

-o .-̂ m n

•̂ VO

-̂ a\ CN rn o" OS

^-v ^-> • ^ vjp o. r-l VO 00 VO 00 r - r-l

f—\

o Ol »n i n

^ > — -

/^ o r i "n »n S'

a\ o CO

^̂ VO

VO f - —

m r n

• ^

VO • ^

cn oo i n

i n r-

144

Q(o' a s O l VO CO

VD CO r— r^i

> — ' ' . - - '

s-O l i n

" n

3!-

-—̂ 0 0 O l

o r--^ > — '

• ^

rn o a\ o Ol

Tt-m o c^ O Ol

/ — s / — 1 0 0 s o O l O l t - 0 0

m 0 0 O l O l

Ci "^

i - - ^

r t i n i n

-*" i n O l

/—-O l VO o VO <n O l

LJ cn OJ >- ttJ u

O H 2

Ul

>

CD 0 0

c

1 cd

c OJ

l y i

a j

> s

cn u ;= z bJ

> g ^ 1 t J Z

^ < H o H

o r n r n

/—̂ i n o rn^ r n O

0 0 VO o

-—( • ^

OV

-^ VO

o 1 — •

CO as

as VO o" m

>n o rn

Ol r n Ol, r n

o

E O PM H

Z 5 b j

z

0

*!; H W

5

S < a o 5 bJ Q.

o

s a.

Ol i n r-CO o 0^

VO 1—4

i n i n m 0^

w

u z z u z s O f=l W Z ca td

1 1 z z g o P E in cn O O O. P. H H t d U

z z

c OJ

£ (D

ra u^ i r t

< 4 - l

o t : n CL

1 00

-t-J

c

C3 (O

L'l u o c Ofl

s ' ? 1 c Ed a. E o o u ra QJ

H

E-g E o

-J

z

E E > o

H 2

O E

< a

> H

I cn cn

cn 5

cn b l

>

< c->

1 w

^ ^ a

cn

ca

O H

> O

<

-I

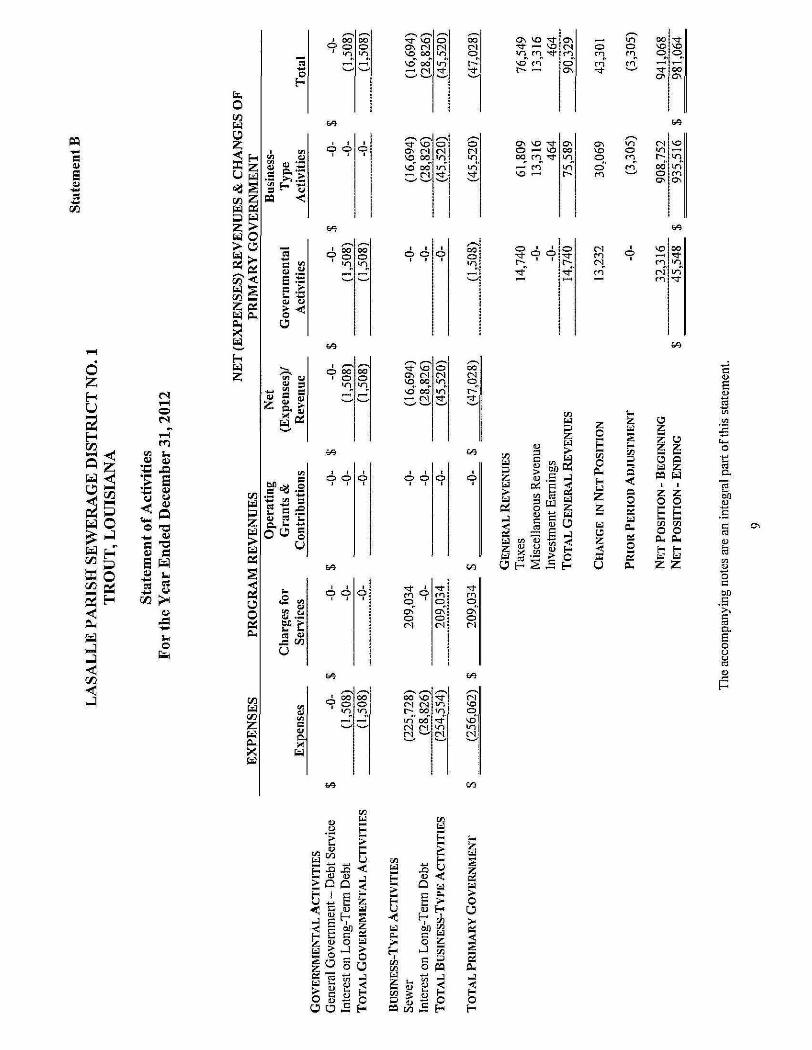

statement C LASALLE PARISH SEWERAGE DISTRICT NO. 1

TROUT, LOUISIANA

Balance Sheet-Governmental Fund December 31,2012

DEBT SERVICE

FUND ASSETS Restricted Cash Restricted Receivables (Net of Allowances for Uncollectables) TOTAL ASSETS

LIABILITIES & FUND BALANCES Deduction from Ad Valorem Tax TOTAL LIABILITIES

Fund Balances: Restricted for Debt Service TOTAL LIABILITIES & FUND BALANCES

$ 60,427

14,965

75,392

503 503

74,889

$ 75,392

The accompanying notes are an integral part of this statement.

10

statement D LASALLE PARISH SEWERAGE DISTRICT NO. 1

TROUT, LOUISIANA

Reconciliation of the Government Fund Balance Sheet To the Government-Wide Financial Statement of Net Position

December 31 , 2012

Amounts reported for governmental activities in the Statement of Net Position are different because:

Fund Balance, Total Govemmental Funds (Statement C) $ 74,889

Capital assets used in govemmental activities are not financial resources and, therefore, are not reported in the govemmental funds.

-0-Long-term liabilities including bonds payable are not due and payable in the current period and, therefore, are not reported in the governmental fiinds.

GO Bonds (28,496) Accrued Interest (845)

(29,341) Net Position of Govemmental Activities (Statement A) $ 45,548

The accompanying notes are an integral part of this statement.

11

statement E LASALLE PARISH SEWERAGE DISTRICT NO. 1

TROUT, LOUISIANA

Statement of Revenues, Expenditures & Changes in Fund Balances Governmental Fund December 31, 2012

REVENUES Ad Valorem Taxes TOTAL REVENUES

EXPENDITURES

Bond Payment Principle Bond Payment Interest TOTAL EXPENDITURES

NET CHANGE IN FUND BALANCE

FUND BALANCES - BEGINNING

FUND BALANCES - ENDING

DEBT

SERVICE

FUND

14,740 14,740

7,000 1,775 8,775

5,965

68,923 74,888

The accompanying notes are an integral part of this statement.

12

statement F LASALLE PARISH SEWERAGE DISTRICT NO. 1

TROUT, LOUISIANA

Reconciliation of the Statement of Revenues, Expenditures, & Changes In Fund Balances of Governmental Fund to the Statement of Activities

December 31,2012

Amounts reported for governmental activities in the Statement of Activities are different because:

Net Change in Fund Balances, Total governmental Funds, Statement E $ 5,965

Governmental funds report capital outlays as expenditure. However, in the statement of activities the cost of those assets is allocated over their estimated usefiil lives and reported as depreciation expense. This is the amount by which capital outlays exceeded depreciation In the current period.

-0-The issuance of long-term debt (bonds, leases, etc.) provides current financial resources to govemmental funds, while the repayment of the principal of long-tenn debt consumes the current financial resources of govemmental funds. Neither transaction, however, has any effect on net position. Also, governmental funds report the effect of issuance costs premiums, discounts, and similar items when debt is issued, whereas these amounts are deferred and amortized in the statement of activities. This amount is tlie net effect of tliese differences in tlie treatment of long-term debt and related items.

Accrued Interest 267 Principal Payment 7,000

Some expenses reported in the statement of activities do not require the use of current financial resources and, therefore, are not reported as expenditures in govemmental fiinds.

7,267

-0-Changes in Net Position of Governmental Activities, statement B $ 13,232

The accompanying notes are an integral part of this statement.

13

Statement G LASALLE PARISH SEWERAGE DISTRICT NO. 1

TROUT, LOUISIANA

Statement of Net Position Proprietary Fund

December 31, 2012

ASSETS

CURRENT ASSETS

Cash & Cash Equivalents Receivables (Net of Allowances for Uncollectables) TOTAL CURRENT ASSETS

NON-CURRENT ASSETS

Restricted Cash Capita! Assets (Net of Accumulated Depreciation) TOTAL NON-CURRENT ASSETS

TOTAL ASSETS

LLVBILITIES

CURRENT LIABILITIES

Accounts Payable Accrued Wage/Payroll Taxes Payable Accrued Compensated Absences Deduction from Ad Valorem Tax TOTAL CURRENT LIABILITIES

LIABILITIES PAYABLE FROM RESTRICTED ASSETS

Customer Deposits Accrued Interest Notes & Bonds Due Within One Year TOTAL LIABILITIES PAYABLE FROM RESTRICTED ASSETS

NON-CURRENT LIABILITIES Notes & Bonds Due in More Than One Year

TOTAL NON-CURRENT LIABILITIES

TOTAL LUBILITIES

NET POSITION

Invested in Capital Assets Net of Related Debt Restricted for Debt Service Unrestricted TOTAL NET POSITION

BUSINESS-TYPE ACTIVITIES

ENTERPRISE FUND

41,512 73,382

114,894

242,068 1,206,424 1,448,492

1,563,386

5,980 1,853 3,778 2,018

13,629

28,996 21,389 46,735

97,120

517,121 517,121

627,870

642,568 141,258 151,690

935,516

The accompanying notes are an integral part of this statement.

14

statement H LASALLE PARISH SEWERAGE DISTRICT NO. 1

TROUT, LOUISIANA

Statement of Revenues, Expenses, & Changes in Net Position Proprietary Fund

December 31,2012

OPERATING REVENUES

Service Charge Ad Valorem Tax Miscellaneous Revenue TOTAL OPERATING REVENUES

OPERATING EXPENSES Cost of Sales & Services Administration Depreciation TOTAL OPERATING EXPENSES

OPERATING INCOME (Loss)

NON-OPERATING REVENUES (EXPENSES) Interest Earnings Interest Expense TOTAL NON-OPERATING REVENUES (EXPENSES)

CHANGE IN N E T POSITION

PRIOR PERIOD ADJUSTMENT

TOTAL NET POSITION - BEGINNING

TOTAL N E T POSITION - ENDING

BUSINESS-TYPE

ACTIVITIES

ENTERPRISE FUND

; 209,034 61,809

, 13,316 284,159

109,304 47,392 69,032

225,728

58,431

464 (28,826) (28,362)

30,069

(3,305)

908,752 935,516

The accompanying notes are an integral part of this statement.

15

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISIANA

Statement of Cash Flows Year Ended December 31 , 2012

statement I

CASH FLOWS FROM OPERATING ACTIVITIES Receipts From Customers & Users Receipts from Other Operating Payments to Suppliers Payments to Employees NET CASH PROVIDED (USED) BY OPERATING ACTIVITIES

CASH FLOWS FROM CAPITAL & RELATED FINANCING ACTIVITIES Acquisition and Construction of Capital Assets Interest Expense Principal Payment on Long-Term Debt NET CASH PROVIDED (USED) BY CAPITAL & RELATED FINANCING ACTIVITIES

CASH FLOWS F R O M INVESTING ACTIVITIES

Investments Interest Earnings NET CASH PROVIDED (USED) BY INVESTING ACTIVITIES

NET INCREASE (DECREASE) IN CASH & CASH EQUIVALENTS

CASH - BEGINNING OF YEAR

C A S H - E N D OF YEAR

ENTERPRISE

FUND

261,804 13,316

(122,383) (37,040)

115,697

(3,430) (28,826) (46,733)

(78,989)

(15,446) 464

(14,982)

21,726

19,786 41,512

The accompanying notes are an integral part of this statement.

16

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISIANA

Statement of Cash Flows Year Ended December 31,2013

Reconciliation

RECONCILIATION OF OPERATING INCOME TO NET CASH

PROVIDED (USED) BY OPERATING ACTIVITIES

Operating Income (Loss) $ 58,431

Depreciation Expense 69,032 (Increase) Decrease in Accounts Receivable (11,615) Increase (Decrease) in Accounts Payable (324) Increase(Decrease)in Accrued Wage/Payroll Taxes Payable (660) Increase (Decrease) in Accrued Compensated Absences -0-Increase (Decrease) in Deduction From Ad Valorem Tax 403 Increase (Decrease) in Customer Deposits 2,173 Increase (Decrease) in Accrued Interest (1,743) TOTAL ADJUSTMENTS 57,266

NET CASH PROVIDED (USED) BY OPERATING ACTIVITIES 115,697

LISTING OF NONCASH IIWESTING, CAPITAL, & FINANCIAL ACTIVITIES

Contributions of Capital Assets From Government $ ^0-

The accompanying notes are an integral part of this statement.

17

^ig^;^^:!T:a-'-wps?^p;gs?^ii!!ii!JA'Mi'%r.i5as?^;i^^?^

Notes to the Basic Financial Statements

LASALLE PARISH SEWERAGE DISTRICT NO, 1 TROUT, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

LaSalle Sewerage District No. 1 was created by the LaSalle Parish Police Jtiry, as authorized by Louisiana Revised Statute 33:4562. The Sewerage District is administered by a board of five commissioners who are appointed by the LaSalle Parish Police Jury. The district ovras and operates sewerage facilities and engages in acfivities designed to provide sewerage disposal to the Trout, Goodpine, and Midway Communities.

For financial reporting purposes the District is a component unit of the LaSalle Parish Police Jury, die goveming body of fiie parish. The accompanying financial statements present fmancial information only on the flinds and account groups maintained by LaSalle Sewerage District No. 1 and do not present information on the Police Jury and the general government services provided by that govemmental unit or any ofits other component tmits.

A. GOVERNMENT-WIDE & FUND FINANCIAL STATEMENTS

The government-wide financial statements (i.e., the Statement of Net Position and the Statement of Changes in Net Position) report information on all of the nonfiduciary activities of the primary goverimient and its component units. For the most part, tlie effect of interfund activity has been removed from these statements. Governmental acfivities, which normally are supported by taxes and intergovemmental revenues, are reported separately from business-type activities, which rely to a significant extent on fees £ind charges for support. Likewise, the primary government is reported separately from certain legally separate component units for which the primary govermnent is financially accountable.

The Statement of Activities demonstrates the degree to wliich the direct expenses of a given function or segment are ofiset by program revenues. Direct expenses are those that are clearly identifiable witli a specific function or segment. Program revenues include 1) charges to customers or applicants who purchase, use or directly benefit from goods, services, or privileges provided by a given function or segment and 2) grants and contributions that are restricted to meetings the operational or capital requirements of a particular function or segment. Taxes and other items not properly included among program revenues are reported instead as general revenues.

Separate financial statements are provided for govemmental funds, proprietary funds, and fiduciary funds, even tlirough the latter are excluded fi'om the govemment-wide financial statements. Major individual govemmental funds and major individual enterprise funds are reported as separate columns in the fund financial statements.

19

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS

(CONTINUED)

B. MEASUREMENT FOCUS, BASIS OF ACCOUNTING, & FINANCIAL STATEMENT PRESENTATION

The govemment-wide financial statements are reported using the economic resources meastirement focus and the accrual basis of accotmting, as are the proprietary fund and fiduciary fiind financial siatements. Revenues are recorded when earned and expenses are recorded when a liabifity is inctirred, regardless of the timing of related cash flows. Property taxes are recognized as revenues in tiie year for which tiiey are levied. Grants and similar items are recognized as revenue as soon as all eligibility requirements imposed by tiie provider have been met.

Govemmental fund fmancial statements are reported using the current financial resotirces measurement focus and the modified accrual basis of accounting. Revenues are recognized as soon as they are both measurable and available. Revenues are considered to be available when they are collectible within tiie cun-ent period or soon enough thereafter to pay liabilities of the current period. For tliis purpose, the government considers revenues to be available if they are collected within 60 days of the end of the current fiscal period. Expenditures generally are recorded when a liability is incurred, as under accrual accounting. However, debt service expenditiu-es, as well as expenditures related to compensated absences and claims and judgments, are recorded only when payment is due.

Property taxes, fi-anchise taxes, licenses, and interest associated with the current fiscal period are all considered to be susceptible to accmal and so have been recognized as revenues of the current fiscal period. All otiier revenue items are considered to be measurable and available only when cash is received by the government.

The municipality reports tiie following major govemmental fimds:

• Debt Service - To account for ad valorem taxes dedicated to debt service.

The municipality reports tiie following major proprietary funds:

® Sewer Fund - The Enterprise Fimd is the municipality's primary operating fund. It accounts for all financial resources of the general govemment, except tliose required to be accounted for in another fiind.

As a general rule the effect of interfund activity has been eliminated fi:om the govemment-wide financial statements. Exceptions to this general rule are payments-in-iieu of taxes and otiier charges between the govemment's enterprise operations. Elimination of tiiese charges would distort the direct costs and program revenues reported for the various fimctions concerned.

Amounts reported as program revenues include 1) charges to customers or applicants for goods, services, or privtieges provided, 2) operating grants and contributions, and 3) capital grants and contributions, including special assessments. Intemally dedicated resources are reported as general revenues rather than as program revenues. Likewise, general revenues include all taxes.

20

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS

(CONTINUED)

Proprietary hinds distinguish operating revenues and expenses fi'om nonoperating items. Operating revenues and expenses generally result from providing services and producing and delivering goods in connection with a proprietary fund's principal ongoing operations. Principal operating revenues are utility billings. Operating expenses for enterprise fiinds include the cost of sales and services, administrative expenses, and depreciation on capital assets. All revenues and expenses not meeting this definition are reported as nonoperating revenues and expenses.

Wlien both restricted and mirestricted resources are available for use, it is the District's policy to use restricted resources first, and then unrestricted resources as they are needed.

Impact of Recently Issued Accounting Principles

In December 2010, die GASB issued Statement No. 62, Codification of Accoimting and Financial Reporting Guidance Contained in Pre-November 30, 1989 FASB and AICPA Pronouncements. GASBS No. 62 incorporates into the GASB's authoritative literature certain accounting and financial reporting guidance tiiat is included in the following pronouncements issued on or before November 30, 1989, wliich does not conflict with or contradict GASB pronouncements: Financial Accounting Standards Board (FASB) Statements and Interpretations, Accounting Principles Board Opinions and Accounting Research Bulletins of the American Institute of Certified Public Accountants' (AICPA) Committee on Accoimting Procedure. This Statement is effective for periods beginning after December 15, 2011, and has been implemented in fiscal year 2012. The adoption of GASBS No. 62 does not have any impact on the District's financial statements.

Ll Jtme 2011, tiie GASB issued Statement No. 63, Financial Reporting of Deferred OidfloM>s of Resources, Deferred Inflows of Resources, and Net Position. GASBS No. 63 provides guidance for reporting deferred outflows of resources, deferred inflows of resources, and net position in a statement of fmancial position and related disclosures. The Statement of Net Assets is renamed the Statement of Net Position and includes tiie following elements: assets, deferred outflows of resources, liabilities, deferred inflows of resources, and net position. This Statement is effective for periods beginning after December 15, 2011, and has been implemented m fiscal year 2012. The adoption of GASBS No. 63 does not have any impact on tiie District's financial statements.

C. CASH & INVESTMENTS - (C.D.'s IN EXCESS OF 90 DAYS)

Deposits

It is the District's policy for deposits to be 100% secured by collateral at market or par, whichever is lower, less the amount of the Federal Deposit Insurance Corporation insurance. The District's deposits are categorized to give an indication of the level of risk assumed by the District at year end. Tlie categories are describes as follows:

21

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS

(CONTINUED)

• Category 1 - Insured or collateralized with securities held by the District or by its agent in the District's name.

B Category 2 - Collateralized witii securities held by the pledging financial institution's tmst department or agent in the District's name.

• Category 3 - Uncollateralized.

Bank Balance Bank At 12/31/2012 Southern Heritage Bank S 344,785

Amounts on deposit are secured by the following pledges: Southern Heritage

Description Market Value FDIC (Categoiy 1) $ 344,785 Securities (Category 2) 90,518 Total $ 435,303

All deposits were fully secured as of December 31,2012.

D. INVENTORIES

Inventories of materials and supplies are considered to be expenditures at the time purchased. Amoimts on hand at the financial statement date are considered knmaterial and therefore not included on the statements of assets and liabilities.

E. ACCOUNTS RECEIVABLE & ALLOWANCES FOR BAD DEBTS

UncoUectable amounts due for customers' utility receivables are recognized as bad debts tlirough the establisliment of an allowance accoimt at the time infomiation becomes available which would indicate the uncollectables of the receivable. Below is a summary of accounts receivable and allowance for bad debts by funds;

Proprietary-Accounts Receivable $ 15,143 Allowance for Bad Debt (757) Ad Valorem Tax Receivable 58,996 Total Receivables $ 73,382

Allowance for bad debts is established at 5% of customer accounts receivable.

Debt Service-Ad Valorem Tax Receivable (Restricted) $ 14,965

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS

(CONTINUED)

2. AD VALOREM TAXES

For the year ended December 31, 2012, laxes of 12.52 mills were levied on property with assessed valuations totafing $7,882,534 and were dedicated as follows:

General Sewer Maintenance Debt Service (G.O. Bonds) Total

TOTAL VALUATION

$ - $

$ 7,882,534 $

TAX ASSESSED

62,090 15,491 77,581

MILLS

10.02 2.50 12,52

Total taxes levied were $77,581. Taxes are due October 15 of each year and become delinquent January 1.

3. RESTRICTED ASSETS- GOVERNMENTAL FUND

At December 31, 2012, restricted assets for tiie government fund were applicable to tiie following:

Ad Valorem Casli Ad Valorem Receivables Total

$ 60,427 14,965 75,392

4. RESTRICTED ASSETS - PROPRIETARY FUND TYPES

At December 31, 2012, restricted assets for the proprietary fund were applicable to the following:

Bond Reserve Account Bond Contingency Account Customers' Deposit Sinking Fund Reserve CD Customer Deposit Savings Total

$ 57,173 45,186 20,536 58,023 49,000 12,150

S 242,068

5. CHANGES IN FIXED ASSETS - PROPRIETARY FUNDS

A summary of proprietary fund type property, plant and equipment at December 31, 2012:

System (Cost) Less Allowance for Depreciation Net Plant

Beginning Balance Additions

3,262,321 $ 3,430 $ (1,990,295) (69,032) 1,272,026 S (65,602) $

Deletions -0- S -0--0- $

Ending Balance

3,265,751 (2,059,327) 1,206,424

23

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS

(CONTINUED)

6. ACCOUNTS PAYABLE

The payables of $13,629 at December 31, 2012, were as follows:

Accounts Payable Accrued Payroll Payroll Taxes Payable Accrued Absences Deduction from Ad Valorem Tax Total

$

$

5,980 927 926

3,778 2,018

13,629

7. CHANGES IN LONG-TERM DEBT

The following is a summary of payable transactions of the LaSalle Sewerage District No. 1 for the year ended December 31, 2012.

General Revenue Truck Obligation Bonds Lease Total

Beginning-Bonds & Notes Payable $ 35,496 $ 608,858 $ 1,732 $ 646,086 Additions -0- -0- -0- -0-Reductions (6,500) (45,898) (836) (53,234) Ending-Bonds & Notes Payable $ 28,996 $ 562,960 $ 896 S 592,852

Bonds and lease payables at December 31, 2012 are comprised of the following individual issues:

General Obligation Bonds $170,000 Sewer F.O. Bonds dated 3/30/78; due in annual installments through 3/30/2017, interest at 5%. $ 28,496

Revenue Bonds (Enterprise Fund) $427,000 Sewer Revenue Bonds dated 3/30/1978; due in annual installments of$25,600 through 3/30/2019, interest at 5%. 129,000

$58,000 Sewer Revenue Bonds dated 6/8/1979; due in annual installments of $3,500 through 3/30/2019, interest at 5%. 14,000

$820,000 Sewer Revenue Bonds dated 8/30/1990; due in annual installments of $48,191 through 3/30/2030, interest at 5%. 419,960

Truck Lease (Enterprise Fund) $3,473 Truck Lease dated 06/11/10; due in annual installments of $961.35 (Sewer's Portion) through 06/11/13; interest at 7.25%. 896

Total $ 592,352

24

Sewer G.O.

Bonds 10,550 $ 10,200 10,800 10,400 10,950

-0--0--0-

52,900 $

Sewer Revenue Bonds

75,341 $ 76,291 76,191 76,041 75,841

270,455 240,955 144,574

1,035,689 $

Truck Lease

961 $ -0--0--0--0--0--0--0-

961 $

Total 86,852 86,491 86,991 86,441 86,791

270,455 240,955 144,574

1,089,550

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISLANA

NOTES TO THE BASIC FINANCIAL STATEMENTS

(CONTINUED)

The aimual requirement to amortize all debt outstanding as of December 31, 2012, including interest payments are as follows:

Year Ending December 31 2013 2014 2015 2016 2017 2018-2022 2023-2027 2028-2032 Total

8. FLOW OF FUNDS; RESTRICTIONS ON USE - ENTERPRISE FUND REVENUE

Under tiie tcmis of the bond indenture relating to Sewer Bonds, all income and revenues (hereinafter referred to as revenue) of every nature, eamed or derived from operations of the Sewer System are pledged and dedicated to the retirement of said bonds, and are to be set aside into the following special fiinds:

(A) Out of revenue to the "Operations and Maintenance Fund", and amount sufficient to provide for expenses of the system.

(B) Each month, there will be set aside into a fimd called the "Bond and Interest Redemption Fund", an amount constituting 1/12 of the next maturing yearly installment of principal and interest payments. Tliese funds may be used only for payment of bond principal and interest.

(C) There shall also be set aside into a "Bond Reserve Fund" an amotmt equal to 5% of the monthly payment being made in to the sinking fiind until it equals the highest combined annual debt service in any future year on the outstanding bonds or $77,913. Such amount may be used only for the payment of maturing bonds and interest for which sufficient funds are not on deposit in the "Bond and Interest Redemption Fund".

(D) Funds will also be set aside into a Contingency Fund at the rate of $375 per month. Money in this fund may be used for the maldng of extraordinary repairs to the system which are necessary to keep the system in operating condition. Money in tliis fund may be used to pay principal or interest on the bonds falling due at any time there is not sufficient money for payment in the other bond funds.

(E) All of the revenue received in any fiscal year and not required to be paid in such fiscal year into any of the above noted funds shall be regai'ded as smplus and may be used for any lawful purpose of the District.

Reservations of net position have been made for funds in restricted accounts that exceed current interest and principal requirements.

25

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS

(CONTINUED)

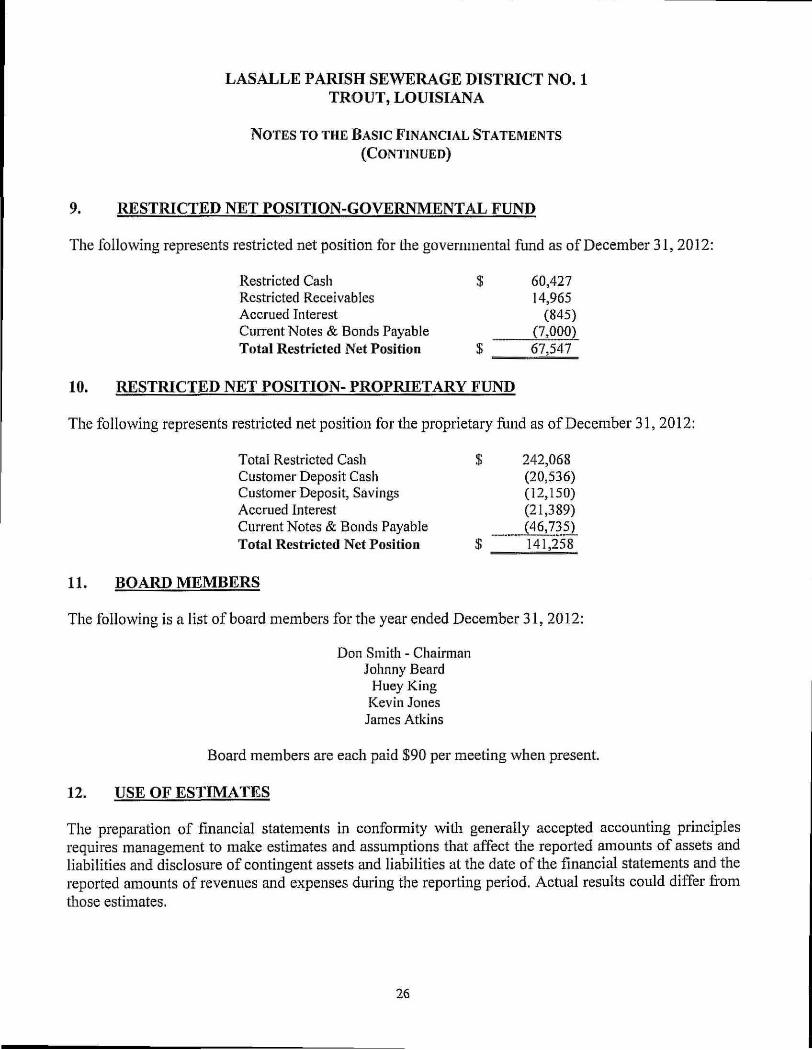

9. RESTRICTED ISET POSITION-GOVERNMENTAL FUND

The following represents restricted net position for tlie govermnental fund as of December 31,2012:

Restricted Cash Restricted Receivables Accrued Interest Current Notes & Bonds Payable Totai Restricted Net Position

$

$

60,427 14,965

(845) (7,000) 67,547

10. RESTRICTED NET POSITION- PROPRIETARY FUND

The following represents restricted net position for tiie proprietary fund as of December 31, 2012:

Total Restricted Cash $ 242,068 Customer Deposit Cash Customer Deposit, Savings Accrued Interest Current Notes & Bonds Payable Total Restricted Net Position $ _

(20,536) (12,150) (21,389) (46,735) 141,258

11. BOARD MEMBERS

The following is a list of board members for the year ended December 31, 2012:

Don Smith - Chainnan Johnny Beard

Huey King Kevin Jones James Atkins

Board members are each paid $90 per meeting when present.

12. USE OF ESTIMATES

The preparation of financial statements in confonnity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ firom tiiose estimates.

26

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISIANA

N O T E S TO THE BASIC FINANCIAL STATEMENTS

(CONTINUED)

13. ACCRUED SICK LEAVE AND VACATION

The following is a summary of changes in compensated absences payable at December 31, 2012: Current Noncurrent Total

Beginning of year $ 3,778 -0- 3,778 Additions/(Retirements) -0- -0- -0-End ofyear $ 3,778 -0- 3,778

The accrued sick leave and vacation is as follows: Employee Amount Charies Smith $ 1,406 Aubrey Brown 716 Sharon Keel 782 Marie Carter 0 Mike Gibson 874 Total Accrued Sick Leave & Vacation S 3,778

14. LITIGATION

The District had no outstanding judgments or pending litigations as of December 31, 2012.

15. RETIREMENT PLANS

The system does not offer its employees a retirement plan. All employees are in tiie social security

system.

16. SEWER RATES

TTie Districfs current sewer rates are as follows:

Residential $ 13.44 per month flat rate plus $1.79 for each 1,000 gallons of

water

Residential (Non-Metered Water) % 19.84 per month flat rate

Industrial $ 32.00 per month flat rate plus $2.30 for each 1,000 gallons of water

17. JOINT VENTURE W I T H T O V m OF JENA The Town of Jena ov^is and maintains tiie sewer treatment plant that processes the District's sewerage. The Town of Jena charges the District 1/3 of the operation and maintenance costs of the sewer plant.

18. PRIOR PERIOD ADJUSTMENT The District has a prior period adjustment in the amount of $3,305 to correct accmed sick leave and vacation from the previous year.

27

i^amK^i^j^!^qrag^;^^^BPv!^^^g^sai^m^^f^^^^s^

Other Reports

28

John R. Vercher C.P.A. T H E V E R C H E R G R O U P MEMBERS

A Professional Corporation of American institute of Jonathan M. Vercher M.S., C.P.A. Cer t i f ied P u b U c A c c o u n t a n t s Certified Public Accountants [email protected] p^Q_ gp^ 1608

1737 N l""* St —Siiitp A Society of Louisiana DavidR. VercherM.B.A., C.P.A. j , . .* - i - ,^^ Certified Public Accountants

Jena, Louisiana 71342 [email protected] Tel: (318) 992-6348 Fax: (318) 992-4374

INDEPENDENT AUDITOR'S REPORT O N I N T E I U ^ A L CONTROL OVER

FINANCIAL REPORTING AND O N COMPLIANCE AND OTHER MATTERS BASED

ON AN AUDIT O F FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE

W I T H GOVERNMENT AUDITING STANDARDS

LaSalle Parish Sewerage District No. 1 Trout, Louisiana

We have audited, in accordance with tiie auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the financial statements of the business-type activities of the LaSalle Pm"ish Sewerage District No. 1, as of and for the year ended December 31, 2012, and the related notes to the financial statements, which collectively comprise the LaSalle Parish Sewerage District No. I's basic financial statements, and have issued our report thereon dated May 24, 2013.

Internal Control Over Financial Reporting

In plaiming and performing our audit of the financial statements, we considered the LaSalle Parish Sewerage District No. I's intemal control over financial reporting (intemal control) to determine the audit procedures that are appropriate in the circumstances for tiie purpose of expressing our opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the LaSalle Parish Sewerage District No. I's intemal control. Accordingly, we do not express an opinion on the effectiveness of tiie LaSalle Parish Sewerage District No. I's intemal control.

A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a trniely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity's financial statements will not be prevented, or detected and corrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in intemal control that is less severe tiian a materieil wealcness, yet important enough to merit attention by those charged with governance.

29

Our consideration of intemal control was for the limited purpose described in the first paragraph of tiiis section and was not designed to identify all deficiencies in intemal control that might be material wealoiesses or significant deficiencies and therefore, material weaknesses or significant deficiencies may exist that were not identified. Given these limitations, during our audit we did not identify any deficiencies in intemal control that we consider to be material weaknesses. However, material wealoiesses may exist that have not been identified. We did identify certain deficiencies in internal control, described in the accompanying schedule of findings and questioned costs that we consider to be significant deficiencies. (2012-1-1 Small Size of Entity)

Compliance and Other Matters

As part of obtaining reasonable assurance about whetiier tiie LaSalle Parish Sewerage District No. I's financial statements are free fi-om material misstatement, we performed tests of its compliance witii certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with tiiose provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Covernmeiit Auditing Standards.

LaSalle Parish Sewerage District No. I 's Response to Findings

The LaSalle Parish Sewerage District No. I's response to the finding identified in our audit is described in the accompanying Schedule of Findings and Questioned Costs. The LaSalle Parish Sewerage District No. I's response was not subjected to the auditing procedures applied in the audit of the financial statements and, accordingly, we express no opitiion on it.

Purpose of this Report

The purpose of tins report is solely to describe the scope of our testing of intemal control and compliance and the results of tiiat testing, and not to provide an opinion on the effectiveness of the entity's intemal control or on compliance. This report is an integral part of an audh performed in accordance with Government Auditing Standai-ds in considering the entity's internal control and compliance. Accordingly, tiiis communication is not suitable for any other purpose.

This report is intended solely for the information and use of tiie audit committee, management, federal awarding agencies and Legislative Audhor's Office and is not intended to be and should not be used by anyone other tiian these specified parties. However, this report is a public document and its distribution is not limited.

The T^erclier (^rowp

Jena, Louisiana May 24, 2013

30

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISLANA

SCHEDULE OF FINDINGS AND QUESTIONED COST For the Year Ended December 31, 2012

We have audited the basic financial statements which collectively comprise tiie LaSalle Parish Sewerage District No. 1 as of and for the year ended December 31, 2012, and have issued our report thereon dated May 24, 2013. We conducted om" audit in accordance with generally accepted auditing standards and the standards applicable to financial audits contained in Govemment Auditing Standards, issued by the Comptroller General of the United States. Our audit of tiie financial statements as of December 31, 2012, resulted in an unqualified opinion.

Section I Summary of Auditor's Results

a. Report on Internal Control and Compliance Material to the Financial Statements

Internal Control Material Weaknesses CU Yes Kl No Other Condhions ^ Yes • No

Compliance Compliance Material to Financial Statements O Yes ^ No

b. Federal Awards - (Not Applicable)

Intemal Control Material Wealmesses \Z] Yes Q No Otiier Conditions Q Yes HH No

Type of Opinion On Compliance Q Unqualified O Qualified For Major Programs CU Disclaimer CU Adverse

Are the findings required to be reported in accordance with Circular A-133, Section .510(a)?

n Yes D No

c. Identification Of Major Programs:

CFDA Number (s) Name Of Federal Program (or Cluster)

Dollar tlireshold used to distinguish between Type A and Type B Programs: $

Is tiie auditee a How-risk' auditee, as defined by OMB Circular A-133? Q Yes G No

31

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOXnSIANA

SCHEDULE OF FINDINGS AND QUESTIONED COST - (CONT.) For the Year Ended December 31, 2012

Section II Financial Statement Findings

2012-1-1 Small Size of Entitv

Condition: Because of the small size of the Sewerage District and the lack of separation of duties of employees, many of the important elements of good intemal controls cannot always be achieved to ensure adequate protection of the Sewerage District's cash.

Criteria: Important elements of good intemal controls often require that the same employee does not handle tiie functions of accounting, collections, biUing, receiving and check writing.

Cause of Condition: Small size of entity and lack of employees.

Effect of Condition: Significant deficiency in intemal controls.

Recommendation: We recommend that management continue to provide the necessai-y oversight in its current intemal control procedures, specifically in the areas of cash receipts, collection receipt activities, recordation of those receipts, deposhing of funds collected, and review of checks written.

Client Response: Management continues to provide tiie necessary oversight in its current intemal control procedures, specifically in the areas of cash receipts, collection receipt activities, recordation of those receipts, depositing of funds collected, and review of checks written.

Section HI Federal Awards Findings and Questioned Costs.

Not applicable.

32

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISIANA

MANAGEMENT'S CORRECTIVE A C T I O N

F O R CURRENT Y E A R AUDIT FINDINGS

FINDINGS:

2012-1-1 Small Size of Entitv

Condition: Because of the small size of the Sewer System and the lack of separation of duties, many of the important elements of good intemal controls cannot always be achieved to ensure adequate protection of the Sewer System's cash.

Corrective Action: Management wiU continue to provide the necessary oversight in its current intemal control procedures, specifically in the areas of cash receipts, collection receipt activities, recordation of those receipts, depositing of fimds collected, and review of checks written.

Contact Person: Sharon Keel

Anticipated Completion Date: December 31, 2013

33

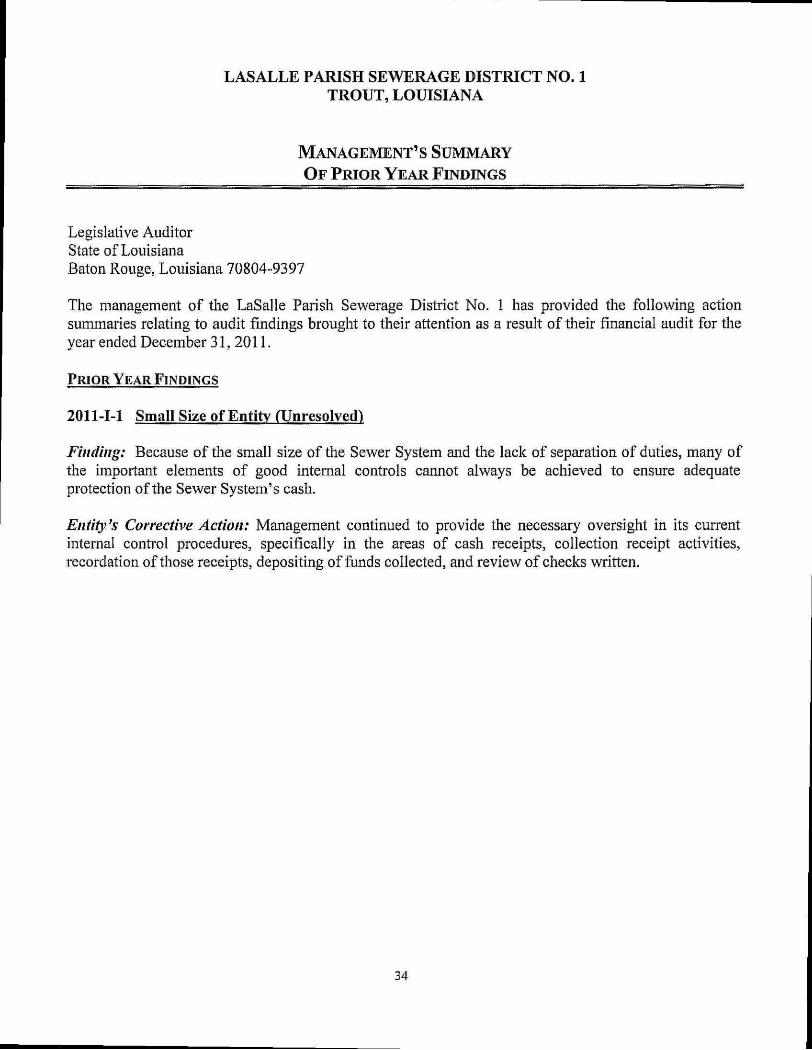

LASALLE PARISH SEWERAGE DISTRICT NO. 1 TROUT, LOUISIANA

MANAGEMENT'S SUMMARY O F P R I O R Y E A R F I N D I N G S

Legislative Audhor State of Louisiana Baton Rouge, Louisiana 70804-9397

The management of the LaSalle Parish Sewerage District No. 1 has provided the following action summaries relating to audit findings brought to their attention as a result of their financial audit for tiie year ended December 31, 2011.

PRIOR YEAR FINDINGS

2011-1-1 Small Size of Entitv (Unresolved)

Finding: Because of tiie small size of the Sewer System and the lack of separation of duties, many of the important elements of good intemal controls caimot always be acliieved to ensure adequate protection of the Sewer System's cash.

Entity's Corrective Action: Management continued to provide the necessary oversight in its current internal control procedures, specifically in the areas of cash receipts, collection receipt activities, recordation of those receipts, depositing of funds collected, and review of checks written.

34