Basel III/Prudential breakfast briefing series - PwC · 2015-09-10 · PwC – Basel III/...

10

www.pwc.co.uk/fsrr Stand out for the right reasons Basel III/Prudential breakfast briefing series Standardised Approach for CCR: A non-standard implementation? July 2015

Transcript of Basel III/Prudential breakfast briefing series - PwC · 2015-09-10 · PwC – Basel III/...

www.pwc.co.uk/fsrr

Stand out for the right reasons

Basel III/Prudential breakfast briefing series

Standardised Approach for CCR: A non-standard implementation?

July 2015

Basel III/Prudential breakfast briefing series PwC 1

The new Standardised Approach for calculating counterparty credit risk (SA-CCR) is more risk sensitive than the Current Exposure Method (CEM) that it replaces, but requires significantly more work. SA-CCR is also set to change the capital requirements for many types of derivative.

Many banks have been slow to prepare for SA-CCR as it fights for attention and resources against other seemingly more pressing changes. Yet, aligning SA-CCR with other developments including the Fundamental Review of the Trading Book (FRTB), Initial Margin for Non-Centrally Cleared Derivatives and BCBS 239 (Risk Data Aggregation and Reporting) would capitalise on the considerable synergies in data and evaluation, while giving business teams a much better indication of the overall impact on pricing and returns.

So what does SA-CCR mean for your business and how can you take advantage of the opportunities to simplify the implementation of regulatory change?

Basel III/Prudential breakfast briefing series PwC 2

Capitalising on the synergies between SA-CCR and other regulatory changes

SA-CCR is the new way to calculate the CCR exposures associated with over-the-counter (OTC) derivatives, exchange-traded derivatives and long settlement transactions. It supersedes the Standardised Method and Current Exposure Method (CEM). The basis for evaluation includes a Potential Future Exposure (PFE) approach that the Basel Committee has endeavoured to calibrate to Internal Model Method (IMM) approaches. If standardised capital floors are implemented, all firms, including those with IMM-approval, will be required to calculate capital requirements under the new SA-CCR approach.

SA-CCR is due to come into force from 1 January 2017, though some countries may adopt a different timeframe. SA-CCR is likely to have a significant impact on other developments. This includes feeding into the leverage ratio, the measurement and control of large exposures and the likely rules around capital floors.

The SA-CCR approach offers potential capital benefits, but it increases implementation costs as the Basel Committee strives to improve risk sensitivity. The new approach is considerably more risk sensitive than CEM and better reflects the offsetting of risks in the same asset class and netting sets. Collateral recognition improves by distinguishing margined and un-margined transactions. To achieve these aims, SA-CCR requires new and more granular data feeds, as well as a new and more complex calculator, supported by new business rules for mapping risk factors to hedging sets.

PwC – Basel III/ prudential breakfast briefing series

Basel III/Prudential breakfast briefing series PwC 3

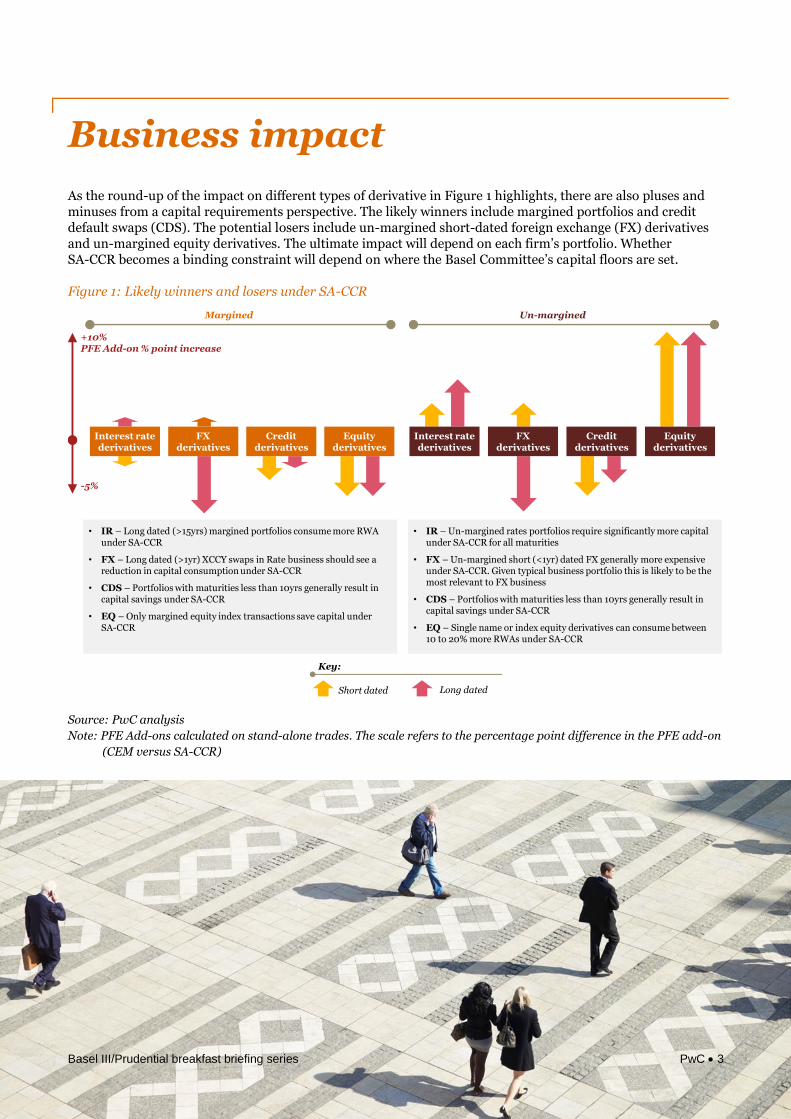

As the round-up of the impact on different types of derivative in Figure 1 highlights, there are also pluses and minuses from a capital requirements perspective. The likely winners include margined portfolios and credit default swaps (CDS). The potential losers include un-margined short-dated foreign exchange (FX) derivatives and un-margined equity derivatives. The ultimate impact will depend on each firm’s portfolio. Whether SA-CCR becomes a binding constraint will depend on where the Basel Committee’s capital floors are set.

Figure 1: Likely winners and losers under SA-CCR

• IR – Long dated (>15yrs) margined portfolios consume more RWA under SA-CCR

• FX – Long dated (>1yr) XCCY swaps in Rate business should see a reduction in capital consumption under SA-CCR

• CDS – Portfolios with maturities less than 10yrs generally result in capital savings under SA-CCR

• EQ – Only margined equity index transactions save capital under SA-CCR

• IR – Un-margined rates portfolios require significantly more capital under SA-CCR for all maturities

• FX – Un-margined short (<1yr) dated FX generally more expensive under SA-CCR. Given typical business portfolio this is likely to be the most relevant to FX business

• CDS – Portfolios with maturities less than 10yrs generally result in capital savings under SA-CCR

• EQ – Single name or index equity derivatives can consume between 10 to 20% more RWAs under SA-CCR

Long dated

Key:

Margined Un-margined

+10%PFE Add-on % point increase

-5%

Short dated

FXderivatives

Interest rate derivatives

Credit derivatives

Equity derivatives

FXderivatives

Interest rate derivatives

Credit derivatives

Equity derivatives

Source: PwC analysis

Note: PFE Add-ons calculated on stand-alone trades. The scale refers to the percentage point difference in the PFE add-on

(CEM versus SA-CCR)

Business impact

Basel III/Prudential breakfast briefing series PwC 4

The complexities and business impact of SA-CCR raise a number of dilemmas for banks. One of the key points of discussion at a seminar for bankers hosted by PwC in June 2015 was whether the risk or finance function should take the lead in managing SA-CCR. A number of participants felt that the risk function is ideally equipped to analyse, understand

and explain the risk sensitivities, though finance is best placed to manage the reporting process. All stressed the importance of close collaboration between risk and finance teams, with some looking to set up dedicated joint ventures responsible for exposure data or integrated operating models akin to the ones now being developed for stress testing. Several

participants emphasised the importance of working closely with the business units, not only to supply but also verify the data. The significance of the capital impacts of SA-CCR and the implementation costs mean that business units should be closely involved from the outset.

Who takes the lead?

Basel III/Prudential breakfast briefing series PwC 5

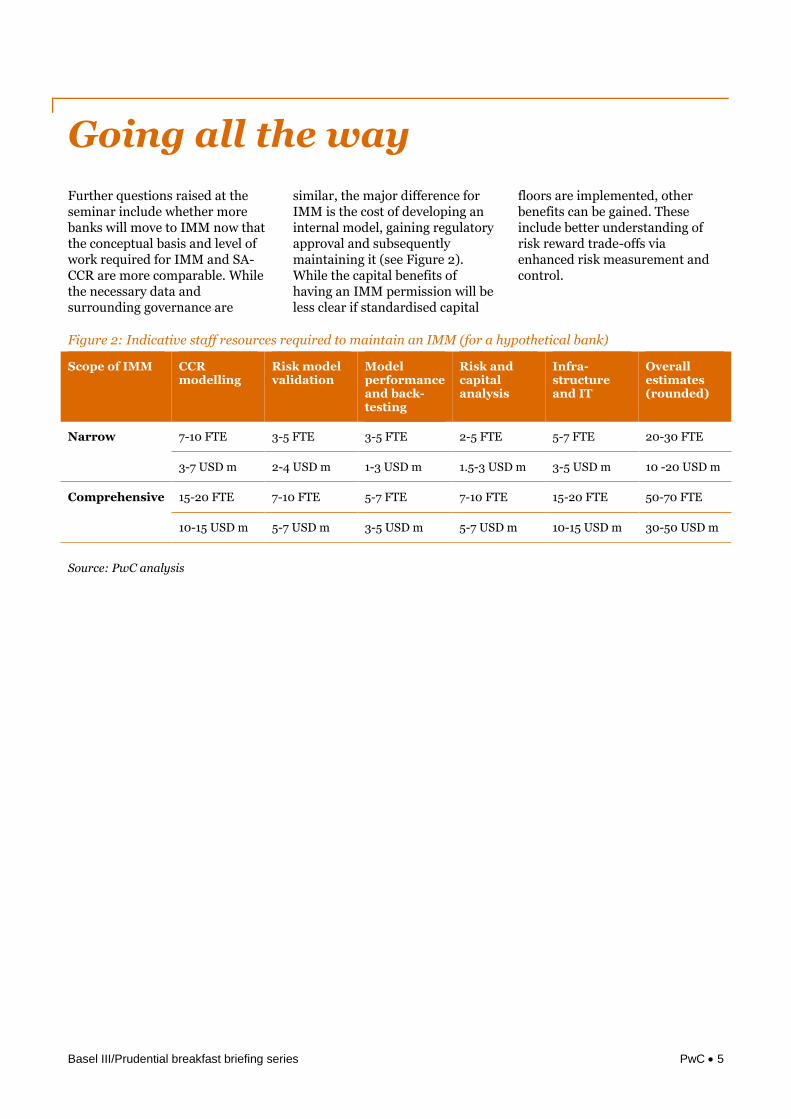

Further questions raised at the seminar include whether more banks will move to IMM now that the conceptual basis and level of work required for IMM and SA-CCR are more comparable. While the necessary data and surrounding governance are

similar, the major difference for IMM is the cost of developing an internal model, gaining regulatory approval and subsequently maintaining it (see Figure 2). While the capital benefits of having an IMM permission will be less clear if standardised capital

floors are implemented, other benefits can be gained. These include better understanding of risk reward trade-offs via enhanced risk measurement and control.

Figure 2: Indicative staff resources required to maintain an IMM (for a hypothetical bank)

Scope of IMM CCR modelling

Risk model validation

Model performance and back-testing

Risk and capital analysis

Infra-structure and IT

Overall estimates (rounded)

Narrow 7-10 FTE 3-5 FTE 3-5 FTE 2-5 FTE 5-7 FTE 20-30 FTE

3-7 USD m 2-4 USD m 1-3 USD m 1.5-3 USD m 3-5 USD m 10 -20 USD m

Comprehensive

15-20 FTE 7-10 FTE 5-7 FTE 7-10 FTE 15-20 FTE 50-70 FTE

10-15 USD m 5-7 USD m 3-5 USD m 5-7 USD m 10-15 USD m 30-50 USD m

Source: PwC analysis

Going all the way

Basel III/Prudential breakfast briefing series PwC 6

Despite the business impact and tough operational demands imposed by SA-CCR, the seminar revealed that preparations vary quite considerably from bank to bank. The most advanced banks tend to come from markets that are likely to be in the first wave of adoption. In other banks, SA-CCR is queuing up behind seemingly more pressing regulatory demands. Examples include operational risk deep dives, forex remediation plans, FRTB and risk data enhancement. SA-CCR implementation has in many cases made little progress beyond initial gap and quantitative impact analysis.

However, as the seminar discussions highlighted, there are considerable overlaps in the source data, calculation and reporting between SA-CCR and other incoming demands include the FRTB, Initial Margin for un-cleared OTC derivatives and BCBS 239. Aligning implementation could avoid the cost and disruption of digging up the road more than once. In our view, it would also be valuable to build SA-CCR into an updated target operating model that embraces the leverage ratio, stress testing and other overlapping regulatory evaluation and reporting demands.

Aligning implementation

Basel III/Prudential breakfast briefing series PwC 7

Therefore, moving SA-CCR up the priority list and building it into an integrated implementation and delivery model could not only save costs, but also enable your business to develop a timelier and more comprehensive response.

We believe there are four key considerations that will need to be addressed to ensure your business is ready to move over to SA-CCR and make the most of the synergies with other developments:

1. Identify parallel demands and take advantage of the opportunities to develop a common, integrated implementation programme and save cost.

2. Design the target operating model and front-to-back process with clear roles, responsibilities and accountabilities.

3. Identify who needs to supply, analyse, verify and aggregate the data across risk, finance and business teams and how they can collaborate most effectively.

4. Assess the impacts of SA-CCR on capital requirements, and identify options for mitigating its impacts through considering new trade structures, portfolio effects and commercial strategy.

The way forward

Basel III/Prudential breakfast briefing series PwC 8

We are helping a range of banks to prepare for SA-CCR and to take advantage of synergies with other regulatory developments. If you would like to know more about the impact of SA-CCR on your business and how to manage it, please call your usual PwC contact or one of the regulatory team leaders listed here:

Richard Barfield Oliver Rosenberg Sylvain Cheroutre

T: +44 (0)20 7804 6658

T: +44 (0)7889 643591

T: +44 (0)7725 632509

Giving you the edge

www.pwc.co.uk/fsrr

This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

© 2015 PricewaterhouseCoopers LLP. All rights reserved. In this document, "PwC" refers to the UK member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

150713-123210-RR-OS

Financial services risk and regulation is an opportunity.

At PwC we work with you to embrace change in a way that delivers value to your customers, and long-term growth and profits for your business. With our help, you won’t just avoid potential problems, you’ll also get ahead.

We support you in four key areas.

• By alerting you to financial and regulatory risks we help you to understand the position you’re in and how to comply with regulations. You can then turn risk and regulation to your advantage.

• We help you to prepare for issues such as technical difficulties, operational failure or cyber attacks. By working with you to develop the systems and processes that protect your business you can become more resilient, reliable and effective.

• Adapting your business to achieve cultural change is right for your customers and your people. By equipping you with the insights and tools you need, we will help transform your business and turn uncertainty into opportunity.

• Even the best processes or products sometimes fail. We help repair any damage swiftly to build even greater levels of trust and confidence.

Working with PwC brings a clearer understanding of where you are and where you want to be. Together, we can develop transparent and compelling business strategies for customers, regulators, employees and stakeholders. By adding our skills, experience and expertise to yours, your business can stand out for the right reasons.

Stand out for the right reasons

Alert

Protect

Adapt

Repair

5 | March 2015 | Basel III/Prudential breakfast briefing series

Financial services risk and regulation is an opportunity.

At PwC we work with you to embrace change in a way that delivers value to your customers, and long-term growth and profits for your business. With our help, you won’t just avoid potential problems, you’ll also get ahead.

We support you in four key areas.

By alerting you to financial and regulatory risks we help you to understand the position you’re in and how to comply with regulations. You can then turn risk and regulation to your advantage.

We help you to prepare for issues such as technical difficulties, operational failure or cyber attacks. By working with you to develop the systems and processes that protect your business you can become more resilient, reliable and effective.

Adapting your business to achieve cultural change is right for your customers and your people. By equipping you with the insights and tools you need, we will help transform your business and turn uncertainty into opportunity.

Even the best processes or products sometimes fail. We help repair any damage swiftly to build even greater levels of trust and confidence.

Working with PwC brings a clearer understanding of where you are and where you want to be. Together, we can develop transparent and compelling business strategies for customers, regulators, employees and stakeholders. By adding our skills, experience and expertise to yours, your business can stand out for the right reasons.

Stand out for the right reasons