Basel III & Beyond: A View from Asia - AUGUR Project III & Beyond: A View from Asia ... Student...

101

University of Cambridge Basel III & Beyond: A View from Asia Master of Finance Individual Project Student Project Supervisor: Professor Lord John Eatwell August 2011

Transcript of Basel III & Beyond: A View from Asia - AUGUR Project III & Beyond: A View from Asia ... Student...

University of Cambridge

Basel III & Beyond:

A View from Asia Master of Finance Individual Project

Student Project

Supervisor: Professor Lord John Eatwell

August 2011

CONTENTS

Executive Summary

1

Introduction

6

Research Methodology

7

CHAPTER ONE China

8

CHAPTER TWO Hong Kong

20

CHAPTER THREE Singapore

32

CHAPTER FOUR The Beginnings of an Asian Monetary Fund

46

Concluding Remarks

54

Appendix: Innovation & Liberalisation – Views of the 3 jurisdictions

55

References

1

EXECUTIVE SUMMARY

As the Basel III reform package endorsed by the G20 has largely been formulated to address problems of the Global Financial Crisis of 2007–2010 which originated from the West, a legitimate question would be: how relevant is the reform package to the Far East? This report attempts to answer the question of how Asia views Basel III by focusing on the reactions of regulators, bankers and local commentators in China (Chapter 1), Hong Kong (Chapter 2) and Singapore (Chapter 3). Local measures taken by each jurisdiction beyond Basel III are also presented in the report. A literature survey of information published by national regulators and local commentaries covered in media reports from 2007 to date found that the 3 jurisdictions generally endorse Basel III, albeit certain proposals have sparked more concerns than others. CHINA (Chapter 1) Officials’ views In China, the broad concept of Basel III is supported. Regulators welcome Basel III as the higher regulatory standards in Basel III indirectly endorses the conservative regulatory approach the Chinese has always adopted. Basel III also comes at an opportune time as credit growth in China has accelerated and tighter measures would thus be appropriate. China also sees participating in global regulatory reforms as ways to ensure national interests are safeguarded and to fulfil their responsibility as a member of G20, the Financial Stability Board and Basel Committee on Banking Supervision. Local commentaries Chinese bankers have generally taken Basel III positively, being well-positioned to meet the higher standards and support countercyclical and leverage measures as innovative policies appropriate for the industry. Commentators also think that Basel III would enhance growth opportunities in Asia because Chinese banks are better placed than European and American banks in meeting Basel III capital requirements and therefore are less constrained to make new loans. Given the availability of funding from banks, businesses could be attracted to the region, thus fuelling further growth in Asia. Specific Basel III proposals The Chinese version of Basel III is largely aligned to the G20’s reform package, with some differences, including: (a) an earlier adoption of capital requirements (b) a higher Common Equity Tier 1 ratio of 5%, compared to Basel III’s 4.5% and (c) a higher leverage ratio of 4% compared to Basel III’s 3%. Countercyclical measures were deemed particularly appropriate by both regulators and local commentators given the dramatic growth in credit in China. China has also decided to impose an additional 1% capital charge on domestic systemically important banks albeit regulators opined that this in itself is insufficient. It believes that at the same time, banks should not be allowed to become too complex or too interconnected with capital markets.

2

Beyond Basel III Chinese officials have introduced several measures relating to the extension of loans. The Chinese Banking Regulatory Commission (CBRC) requires banks to set aside loan loss provisions amounting to 2.5% of total loans or 150% of non-performing loans, whichever is higher. While bankers believed that meeting the 2.5% requirement would be a challenge, others argued that 2.5% would still be insufficient to cover losses from potentially bad loans given out to local government backed projects. Regulators have also imposed dynamic loan-to-value (LTV) and debt-to-income ratios as well as minimum down payment requirements and several other property purchase restrictions to cool the rising property market. In addition, monetary policies have been tightened. The CBRC also encourages banks to focus on credit quality and tries to direct credit growth by favouring flows to the real economy over those to the stock and property markets. Commentators opined that this is a smart way to control credit without affecting growth in the real economy. Apart from controls over credit growth, the CBRC sees the integration of banking and capital markets as a risk and thus controls activities that link the 2 markets. HONG KONG (Chapter 2) Officials’ views Hong Kong regulators support the aim of Basel III and intend to implement the Basel III reform package. As an international financial centre, officials see it necessary to adopt international standards and contribute to the resilience of the wider banking industry. Although Hong Kong banks have escaped relatively unscathed from the Global Financial Crisis, senior regulators see the need to be concerned about Basel III because Basel III affects Western banking systems and Asia is not decoupled from the West. In addition, Hong Kong hopes for greater Asian representation in international forums. Encouragingly though, it sees positive trends of greater Asian participation and willingness of others to listen to experiences of the region. Local commentaries The business community has generally taken the reform package positively but is concerned about the cumulative impact of various changes. Specific Basel III proposals Although Hong Kong is generally supportive, concerns have been raised over a few proposals. On liquidity rules, from the officials’ viewpoint, liquidity requirements are new and so should be closely monitored for unintended consequences. One unintended consequence that regulators foresee is the effects on corporate debt markets. Corporate debt markets in Asia are not developed and with liquidity rules focusing on government debt, it would be even more difficult to develop corporate debt markets. Another unintended consequence is the stability of deposits. As banks compete for stable retail deposits by raising deposit rates, customers become less loyal and would shift deposits, making retail deposits less ‘sticky’. Bankers are also concerned because Hong Kong does not have sufficient local government bonds to meet the definition of high quality assets. Some also disagree with the focus on government bonds as it forces banks to hold more low yielding

3

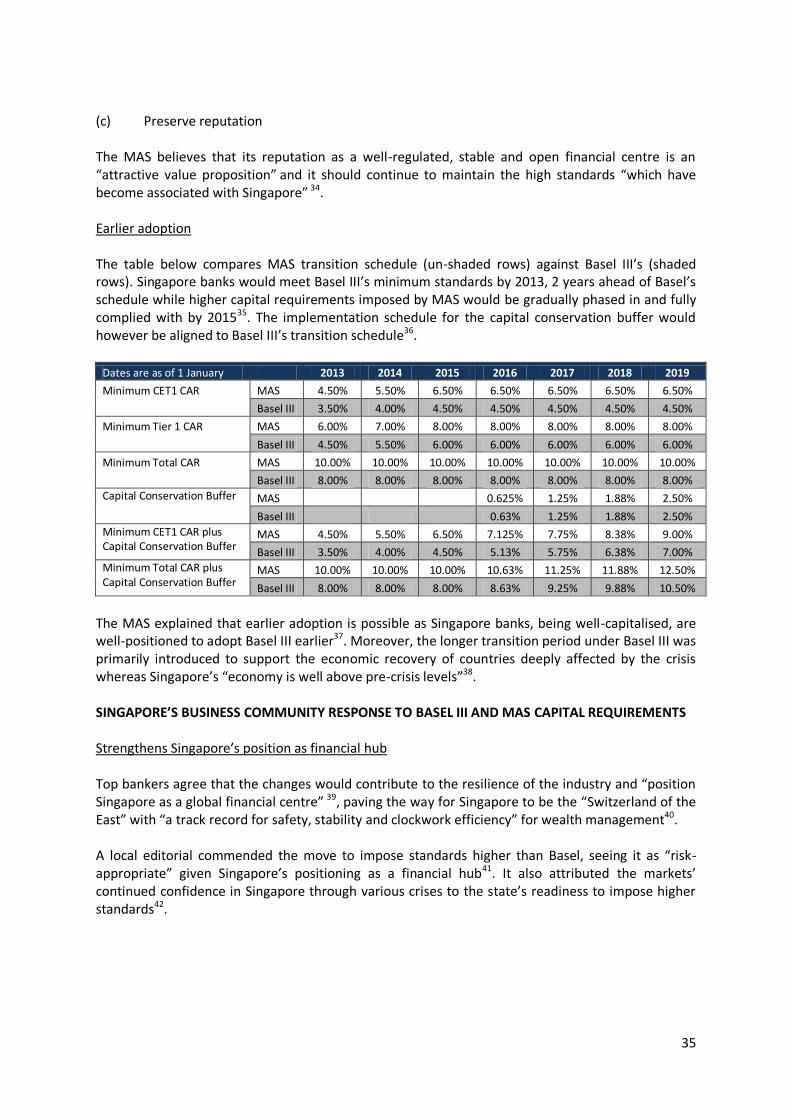

assets. Others make the observation that jurisdictions with low government debt are perversely penalised for managing their fiscal positions well. On the proposal to promote the use of central counterparties, there are concerns that the volume of Asian-Pacific derivatives is too low to ensure the viability of Asian clearing houses. Beyond Basel III Significant measures beyond Basel III are LTV and debt servicing ratio. The Hong Kong Monetary Authority sees LTV as a cornerstone of its regulatory policies that has withstood political pressures and market innovation such as securitisation. Regulators are also considering ring-fencing liquidity by requiring foreign banks to be set up as subsidiaries rather than as branches. Banks are also mandated to maintain a certain amount of assets in Hong Kong through the deposit insurance scheme. Most global banks, however, do not welcome this as they manage liquidity centrally. SINGAPORE (Chapter 3) Officials’ views Singapore officials support Basel III but make it clear that rules should be adapted to local circumstances to be effective, particularly given that Asia and Singapore are different from the West in stages of economic growth, banking business models and regulatory approaches. This, however, does not mean that higher standards will not be aspired to. In fact, because Singapore is a small and open economy that operates in a developing region, it believes higher standards are all the more important. Officials also see imposing high prudential standards as a source of competitive advantage as it reinforces Singapore’s reputation as a safe financial centre. Local commentaries Analysts believe that as Singapore banks are better positioned to meet Basel III standards, they enjoy an advantage over foreign banks which would have to incur higher costs to meet the new standards. On the other hand, a top banker pointed out the shortfall in Basel III in addressing what he saw was the root cause of the crisis which was lax lending practices. Specific Basel III proposals The Monetary Authority of Singapore (MAS) requires Singapore banks to meet Basel III capital standards earlier and to exceed Basel III’s Common Equity requirements by 2% primarily because all the four locally incorporated banks are systemically important domestically. The business community responded positively to the higher standards, believing that it would strengthen Singapore’s position as a financial hub. Bankers in Singapore expressed similar concerns as those in Hong Kong with regard to liquidity requirements. Given the lack of Singapore government bonds, bankers opined that they would be forced to hold low yielding foreign currency bonds and be exposed to foreign currency risks. On the proposal for central counterparties, the Singapore Exchange became the first in Asia to offer a clearing service for Over-the-Counter (OTC) financial derivatives. Although there has been

4

significant interest from both global and local institutions in the service, there are still doubts as to whether trading volumes would be sufficient to ensure the viability of an Asian clearing house. Beyond Basel III Land-scarce Singapore similarly imposed LTV limits which officials see as a more targeted tool that controls credit without affecting the availability of credit to other sectors. The government also introduced prohibitive seller’s stamp duty on properties sold within 4 years of purchase to deter speculation. Before the Global Financial Crisis, Singapore has already imposed rules which require foreign banks to maintain at least a minimum amount of assets in Singapore. Bankers largely disagree with this pointing out the inefficiencies of such requirements for global banks and the higher funding costs that need to be incurred. Beyond regulations, the MAS believes in the need for effective supervision and corporate governance as complementary forces to ensure banking stability and has proposed enhancements to banks’ corporate governance frameworks. Through researching the 3 jurisdictions’ responses to Basel III, it becomes clear that there are differences between Asia and the West. Hence, a longer-term question would be whether Asia could eventually seek out its own solutions, for example, in the form of an Asian Monetary Fund (AMF). Chapter 4 of this report explores if there are indeed signs of an early beginning of an AMF. THE BEGINNINGS OF AN ASIAN MONETARY FUND (Chapter 4) The idea for an AMF was first conceived during the Asian Financial Crisis of 1997–1998 but was quickly rejected by the International Monetary Fund (IMF) and the US Treasury. However, Asia continues to be interested in the proposal. Asia today, with healthier economic fundamentals, is better positioned to pursue the idea. Bitter memories of harsh policies imposed by the IMF on Asian economies during the Asian Financial Crisis as well as the current underrepresentation of Asia in the IMF provide the impetus to create an AMF. The first concrete step Asia has taken in its journey towards an AMF is to establish the Chiang Mai Initiative (CMI) which consisted of bilateral swap agreements that could be triggered to help member countries overcome liquidity problems in times of crisis. Participating countries include the 10 members of the Association of South East Asian Nations (ASEAN), China, Japan and Korea (collectively, ASEAN+3). In 2010, this arrangement was further enhanced by multilateralising the bilateral swap agreements, an initiative known as the Chiang Mai Initiative Multilateralisation (CMIM) so that reserves could be drawn on with just one agreement. However, in practice, members chose not to tap on the CMIM pool during the Global Financial Crisis but instead separately negotiated for other forms of back-up arrangements with different countries. This is largely due to the requirement for members to enter stand-by arrangements with the IMF before CMIM funds could be utilised. The link to the IMF was deemed necessary as the CMIM lacked a surveillance function which the IMF performs to guard against moral hazard. But such a requirement also meant that the CMIM would be an unpopular alternative of aid in times of stress.

5

In 2011, steps to address this gap in the CMIM were made by establishing the ASEAN+3 Macroeconomic Research Office (AMRO) which would perform surveillance and due diligence. Commentators viewed the establishment of AMRO very positively, likening it to the beginning of an AMF. Beyond CMI, CMIM and AMRO, there are other positive developments. Asia’s monetary policies are converging although not through deliberate coordination. Intra-regional trade is also high and is expected to increase even further. However, Asian savings are still largely invested outside the region. To facilitate intra-regional investments, there needs to be more progress on financial integration. Since the Asian Financial Crisis, progress has been made and the possibility of an AMF now seems more likely. However, time is needed for the new AMRO to build up competencies and for greater financial integration to take place before an AMF-like institution may truly be established.

6

INTRODUCTION

Background & Motivation of Study

The key regulatory response to the Global Financial Crisis of 2007–2010 has been the G20’s endorsement of the Basel III reform package developed by the Basel Committee on Banking Supervision. Since the reform package was to address problems of the crisis, which originated and significantly afflicted the West, how relevant is this to the Far East? There are good reasons to think that Asia may not regard Basel III as relevant. For one, Asia is different from the West. While problems in the West relates to leverage and regulatory flaws, Asia’s problems arise from “its dependence on exports and exposure to the volatility of international financial flows”1. Asia does not suffer from the same problems as the West as it began de-leveraging and tightening banking regulations after the Asian Financial Crisis of 1997- 19982. Asian banking products are also less complex and less risky3. For another, Asia, including both the more developed economies such as Australia, Korea, Hong Kong and Singapore and the emerging economies such as India and China, continues to be under-represented in international decision-making4. In part, the lack of influence is due to the fact that there is no unified Asian position in the G20, leading the US and Europe to become natural drivers in global efforts to reform financial regulations5. Further, to Asia, the very nations which have led the discussions might have lost moral high grounds to impose new measures. Howard Davies, former Chairman of UK’s Financial Services Authority, wrote in an article for Caijing Magazine, the most widely read finance journal in China, that: “…recent criticism of Asian regulators by US Treasury Secretary Timothy Geithner is viewed across the region with scorn, not to mention incredulity. A little more humility is in order, given US regulators’ performance in the run-up to the crisis. People who live in glass houses should not throw even rhetorical stones.”6 Overview of Report Given the possible different viewpoints of the West and the East, this report seeks to find how regulators and local commentators in Asia have responded to the G20 reform package by focusing on the responses of 3 jurisdictions - China, Hong Kong and Singapore (Chapters 1 to 3). Views of regulatory authorities and business communities as well as additional measures taken by each jurisdiction beyond Basel III are included in each chapter. From the analysis, it becomes evident that there are different circumstances in Asia which may render certain proposals less appropriate. Hence, the broader and more general question of whether Asia may eventually seek solutions of its own, for example in the form of an Asian Monetary Fund (AMF), emerges. Chapter 4 investigates if there are signs of early developments of an AMF. In the course of reviewing the responses of the 3 jurisdictions, it also becomes apparent that the 3 adopt slightly different approaches to innovation, regulation and liberalisation. The Appendix at the end of the report attempts to present the approaches adopted by the 3 jurisdictions.

7

RESEARCH METHODOLOGY

Research for this report was primarily performed using online secondary sources. The views of local regulators were collated from official government websites. Focus was given to press releases, speeches and circulars issued from 2007 onwards to coincide with the timing of the Global Financial Crisis. As Basel III relates to prudential measures, discussions relating to market conduct issues were excluded from the scope of this report. To obtain the views of the local banking community and other commentators, well-regarded and widely-read local and regional publications (see table below) were referred to, in addition to searches on Factiva, a commercial news database, and on the internet.

China Hong Kong Singapore Others

China-based

Caijing Magazine

21st Century Business Herald

Shanghai Securities News

China Securities Journal

China Daily Hong Kong-based (but covers China)

Hong Kong Economic Journal

South China Morning Post

The Wall Street Journal Asia

Caixin Online

Hong Kong Economic Journal

South China Morning Post

The Wall Street Journal Asia

Caixin Online

China Daily (Hong Kong Edition)

Straits Times

Business Times Singapore

AsiaRisk magazine Risk magazine

8

CHAPTER 1: CHINA

This chapter presents China’s response to Basel III. The first section of this chapter summarises China’s general reaction towards Basel III while the second section presents the Chinese’s responses to specific Basel III recommendations. The third section highlights additional measures taken by China beyond Basel III. Within each section, the official regulatory response and local business commentary are presented. SECTION 1: CHINA’S GENERAL RESPONSE TOWARDS BASEL III

THE OFFICIAL RESPONSE Supports Basel III Chinese officials recognise the merits of Basel III in addressing the flaws in the financial system and see Basel III as a means to improve the ability of the banking sector to handle external stress, ensure long-term robustness and reduce systematic risks1. Simon Topping, head of KPMG’s Financial Services Regulatory Centre of Excellence in Asia Pacific and former senior regulator at the Hong Kong Monetary Authority, believes that the Chinese regulators support Basel III because Basel III furthers the regulators’ aim for Chinese banks to strengthen “capital, liquidity, risk management and governance” 2 and provides indirect endorsement of the stricter regulatory stance the Chinese has always been adopting3. Elaine Wong, managing director and head of Professional Services Asia-Pacific at Moody’s Analytics further added that the China Banking Regulatory Commission (CBRC) uses Basel III (and Basel II) to remind banks of various risks4. In addition, Basel III comes at an opportune time as the imposition of tighter rules is especially appropriate given the dramatic credit growth in China in recent years5. Notwithstanding the officials’ acceptance of Basel III, the Chinese believe in the need to customise rules to suit local circumstances. To safeguard national interests and fulfil role as member of the international community The Chinese also sees participating in global regulatory reforms as ways to “actively safeguard the core interests of China’s banking industry”6. For instance, in the earlier drafts of Basel III proposals, CBRC Chairman Liu Mingkang had provided feedback that the draft proposals “mainly take into consideration the banking practices in the European and US economies” without adequately taking into account “the actual situation of emerging market economies”7. As a result, the oversight body of the Basel Committee was said to have made amendments to various proposals8. In general, however, as a new member of the Financial Stability Board (FSB) and Basel Committee on Banking Supervision (BCBS), China has kept a relatively low profile during the Basel III negotiations9. This could be because key subject matters which dominated discussions such as capital rules and

9

complex financial products were less of an issue for Chinese banks as they are well-capitalised and avoided complex financial products10. In addition, China also believes that it should adopt Basel III to fulfil its duties as a member of the G20, the FSB and BCBS11. THE BUSINESS COMMMUNITY RESPONSE The business community similarly saw merits in Basel III. A survey conducted between April and June 2010 which involved 44 Chinese banks found that Chinese bankers believe that innovative measures such as countercyclical capital buffers and leverage ratio are good models for the Chinese banking industry12. Other local commentators believe that “Basel III will provide China financial system with new [commercial] strength” 13. As Chinese banks are better capitalised than European and American banks, they face less constraints in growing their loan books, and thus would be better able to meet businesses’ financing needs. The combination of a strong banking sector and large liquid stock markets viz. Hong Kong, Shanghai and Shenzhen means there would be easier access to funding and this could incentivise multinational corporations to set up businesses in Asia, thereby fuelling further growth in the region14. Commentators also see practical value in Chinese banks adopting Basel III. Since Basel III is a global standard, adopting and meeting Basel III standards would help Chinese banks establish the credibility to expand internationally15. However, commentators agree with CRBC’s stand on the need to customise rules to cater to local circumstances. Dai Peng, an official with Export-import Bank of China, one of China’s policy banks pointed out that while Western markets were under-regulated and thus stricter regulations ought to be imposed, emerging markets are different as “economic development” should be the priority16. Fan Gang, former advisor to the People’s Bank of China (PBOC), China’s central bank, highlighted that another difference is that emerging markets are “more vulnerable to external risks” and “less capable of self-adjusting”, and hence policies need to be adapted to take care of such vulnerabilities17. SECTION 2: CHINA’S RESPONSES TO SPECIFIC BASEL III RECOMMENDATIONS

1. BASEL III CAPITAL REQUIREMENTS Basel III’s increased minimum capital requirements and transitional arrangements are as follows18:

Minimum Capital Requirements Common Equity Tier 1 Tier 1 Capital Total Capital

Minimum under Basel III

4.5% (2.0%)

6.0% (4.0%)

8.0% (8.0%)

Conservation buffer 2.5% (0.0%)

Minimum plus conservation buffer

7.0% (2.0%)

8.5% (4.0%)

10.5% (8.0%)

(Basel II requirements are shown in brackets for comparison)

10

Transitional Arrangements

Beginning 2013

Beginning 2014

Beginning 2015

Beginning 2016

Beginning 2017

Beginning 2018

Beginning 2019

Minimum Common Equity Capital Ratio

3.5% 4.0% 4.5% 4.5% 4.5% 4.5% 4.5%

Minimum Tier 1 Capital

4.5% 5.5% 6.0% 6.0% 6.0% 6.0% 6.0%

Conservation Buffer

0.625% 1.25% 1.875% 2.5%

CHINA’S OFFICIAL RESPONSE TO BASEL III CAPITAL REQUIREMENTS Stricter capital requirements than Basel III China has long held that capital requirements are important19. Thus, its support for Basel III capital requirements is not surprising. The Chinese version of Basel III capital rules is largely in line with the G20’s endorsement except for the minimum requirement on Common Equity Tier 1 Capital Adequacy Ratio (CAR) which the CBRC has set at 5% i.e. 0.5% higher than that prescribed in Basel III20. The stricter Common Equity Tier 1 CAR is justified on grounds that Chinese banks have already met Basel III’s minimum requirement of 4.5% and the downside of setting a higher minimum is limited as a ratio of 5% is not expected to generate significant negative impact on domestic banks21. Higher capital requirements is also seen by officials as part of the solution to the problem of rapid credit expansion, which the central government has set out to address in China’s 12th-Five-Year Plan22. Earlier adoption While Basel III requires the implementation of new capital regulatory standards to begin in 2013 and for standards to be met by the end of 2018, Chinese officials require banks to start implementation from the beginning of 2012 and to meet the standards by the end of 2016 i.e. 1 year ahead of the implementation schedule and 2 years ahead of the compliance schedule23. Systemically important banks are required to meet the standards even earlier by end 201324. Chinese regulators do not see the need for as long a transition timeframe because Chinese banks are in better positions (as of June 2011, the weighted average CAR and core CAR of Chinese banks stood at 12.2% and 9.92% respectively25) than the European and American banks which face significant capital shortage and more uncertain economic growth prospects26. Further, the Chinese believe that market forces will motivate international banks to reach the new standards before the end-2018 deadline and earlier adoption by Chinese banks will improve domestic banks’ credit ratings and reputation, paving the way for China’s “go global” banking strategy27.

11

CHINA’S BUSINESS COMMUNITY RESPONSE TO BASEL III AND CBRC CAPITAL REQUIREMENTS The supporters Supporters such as China Merchants Bank’s President believe that higher capital requirements would motivate domestic banks to transform, improve economic capital management and constrain the build-up of risky assets28. The sceptics Sceptics however point out that while higher capital requirements seem appropriate given the current macro-economic situation in China, it is uncertain whether in the longer term, higher capital requirements would indeed increase stability for the whole banking sector29. Business impact analysis Business consultants are confident that big Chinese banks can meet Basel III CAR requirements and point out that there are business opportunities for banks which do not need to raise additional capital to meet the higher standards30. As Chinese banks do not face the same constraints in loan growth as European and American banks which lack capital and stable funding sources, they could win a greater share of the global funding market for capital intensive projects31. But the less optimistic consultants opined that Chinese banks lack international experience, are still focused on the domestic market and are therefore not prepared to take advantage of global opportunities32. Instead, they foresee that Chinese banks would “develop more diversified businesses, adjust their business model and reduce reliance on extending loans” which attract heavy capital charges33. The picture for smaller Chinese banks though is likely to be different. They are more likely to have to raise capital as they tend to be more aggressive in extending loans which require more capital backing34. Indeed, a number of banks which wish to continue with their business expansion plans in the face of higher capital requirements and tightened monetary conditions (Section 3, subsection 3 below provides details of the tightened monetary policies) have announced intentions to raise additional capital35. 2. BASEL III COUNTER-CYCLICAL CAPITAL BUFFER Under Basel III, an additional counter-cyclical buffer of up to 2.5% of Common Equity Tier 1 could be imposed in periods of rapid credit growth and released in downturns36. CHINA’S OFFICIAL RESPONSE TO COUNTERCYCLICAL CAPITAL BUFFER In line with G20’s endorsement, the CBRC requires commercial banks to set aside up to 2.5% as countercyclical capital buffer37. Chinese officials view the impositions of counter-cyclical measures during periods of market irrationality as more important than the stop-gap regulatory reforms which typically follow each crisis38. They believe that without countercyclical regulatory intervention, market failures will be more frequent39. CHINA’S BUSINESS COMMUNITY RESPONSE TO COUNTERCYCLICAL CAPITAL BUFFER Bankers surveyed in the Chinese Bankers Survey Report for 2010 welcomed the countercyclical capital buffer as an innovative and good regulatory policy for the industry40.

12

Citing China’s credit-to-GDP ratio, analysts gave their support for high countercyclical capital buffers. Credit Suisse analysts Jain and Wu pointed out that China’s credit-to-GDP ratio increased from 120% to 166% between end 2008 and March 201141. In comparison, guidance published by the Basel Committee in December 2010 suggested imposing the maximum buffer when credit-to-GDP ratio exceeds long-term trend by 10%42. 3. BASEL III ADDITIONAL CAPITAL CHARGES FOR SYSTEMICALLY IMPORTANT FINANCIAL

INSTITUTIONS (SIFIs) Recent proposals recommend imposing capital surcharges ranging from 1% to 2.5% on global SIFIs43. CHINA’S OFFICIAL RESPONSE TO CAPITAL CHARGES FOR SIFI Prior to Basel and FSB’s recent recommendation on the size of capital charges for global SIFIs, the CBRC has temporarily set the additional capital requirement for domestic SIFIs at 1%44. In total, this means that systemically important banks (SIB) need to maintain minimum CAR of 11.5% by end of 2013. Although Chinese regulators have endorsed Basel III, the Chinese believes that existing regulatory responses such as capital charges, proprietary trading restrictions and “living will” for interconnected SIFIs are insufficient. In CBRC Chairman Liu’s words, “prevention is, as a rule, better than cure”45. For the Chinese, prevention takes the form of a firewall between banking and capital market activities to minimise interactions and contagion risks46 (Section 3, subsection 6 below provides details of the “firewall” policy). The CBRC believes that banks should not become too complex to manage or supervise47. CBRC Chairman Liu opined that some US institutions have failed because they had offered too many products which made it difficult to monitor and control risks effectively48. His preference is thus for Chinese banks to focus on niche areas and deliver targeted products to customers49. Hence, CBRC manages banks’ expansions to new activities carefully. For instance, while commercial banks could pilot the integration of traditional banking and non-banking activities, the banks have to ensure that their non-bank subsidiaries make and implement specific exit plans if they fail to meet targets within specified timeframes50. CHINA’S BUSINESS COMMUNITY RESPONSE TO ADDITIONAL CAPITAL CHARGES FOR SIB Moody’s regards China’s capital requirements on SIB to be “credit positive” for the banking system as higher capital provides better protection for debt-holders and depositors51. However, Wu Xiaoling, former deputy governor of People’s Bank of China and current director of China Europe International Business School Lujiazui International Finance Research Centre 52 , cautioned that although SIB currently do not face capital shortages, in five years’ time there could be a shortfall in capital of between 400 billion yuan and 500 billion yuan if banks’ lending continue to increase 53. Indeed, some banks, including those that are expected to be classified as SIB54, have announced plans to raise additional capital55.

13

4. BASEL III LEVERAGE RATIO Under Basel III, a non-risk-weighted minimum leverage ratio (defined as the ratio of Tier 1 capital to total exposures, including on- and off-balance sheet items) of 3% is being tested for planned migration to Pillar 1 in 201856. CHINA’S OFFICIAL RESPONSE TO LEVERAGE RATIO Stricter leverage ratio requirement CBRC stipulates that tier-one capital must be at least 4% of total on- and off-balance sheet assets57. This is higher than the minimum 3% requirement in Basel III. Chinese banks are also required to meet the leverage ratio requirement earlier58. The Chinese observed that although the capital adequacy ratio of major western banks was relatively high prior to the crisis, their levels of leverage continued to increase, indicating that risk-weighted capital adequacy ratio alone was not able to effectively control the level of leverage59. The CBRC further noted that some Western banks had used complicated models to “disguise” the true level of capital adequacy60. Lehman Brothers, for instance, was about 30 times leveraged61. The CBRC also noted that increased levels of leverage made the financial system more vulnerable62. The Chinese officials thus believe that a leverage ratio should be imposed to prevent financial institutions from excessively expanding their balance sheets to curb irrational growth and build-up of systematic risks and to offset potential weaknesses in banks’ internal risk management63. Regulators believe that a higher minimum leverage ratio ought to be imposed because the majority of the banking institutions in China have already reached 4% leverage ratio and a ratio that is set too low will not effectively constrain banks’ rapid expansions64. CHINA’S BUSINESS COMMUNITY RESPONSE TO BASEL III LEVERAGE RATIO The Chinese Bankers Survey Report for 2010 which gathered 752 valid questionnaires responses and 70 face-to-face interviews with senior banking executives from a variety of banking sectors (large-size commercial banks, joint-stock commercial banks, city commercial banks, rural credit cooperatives and policy banks) found that bankers support the leverage ratio as a good regulatory standard for the Chinese banking industry65. Guo Tianyong, an economist and director of the Research Centre of the Chinese Banking Industry at the University of Finance and Economics, however, pointed out that leverage restrictions would be less effective in China as Chinese banks do not use financial derivatives as extensively as their Western counterparts66. Nonetheless, this restriction should prove useful in the longer term67. 5. BASEL III LIQUIDTY RATIOS Under Basel III, two liquidity standards would be introduced68: (a) Banks would need to maintain a Liquidity Coverage Ratio (LCR) of at least 100% to ensure

that they hold sufficient high quality assets to cover net cash outflows for 30 days in a severe stress scenario.

14

Eligible assets are categorised into ‘level 1’, comprising mainly domestic sovereign bonds and ‘level 2’ which can include non-financial corporate bonds and covered bonds not issued by banks69. Haircuts are applied to level 2 assets and such assets cannot make up more than 40% of the overall stock after haircuts have been applied70.

(b) Banks would also need to maintain a Net Stable Funding Ratio (NSFR) of at least 100% to

ensure that stable funding is available to cover funding requirements over a one year period of extended stress.

CHINA’S OFFICIAL RESPONSE TO LIQUIDITY RATIOS Prior to the G20 endorsement, the CBRC provided feedback that the original draft liquidity proposals were not sufficiently prudent: for instance, it believed that highly rated corporate bonds and covered bonds should not qualify as high quality liquid assets71. In the revised version of the Basel III liquidity proposals, such assets were then classified under ‘level 2’72. CBRC endorses the revised proposals and requires banks to meet Basel III liquidity ratios73. It believes that the liquidity requirements would encourage China’s commercial banks to increase holdings of high quality liquid assets, reduce maturity mismatch and increase long-term stable funding sources74. Based on CBRC’s quantitative impact studies, the majority of domestic banks have already reached or would soon reach the regulatory requirements on liquidity75. Additional requirements for liquidity In addition to the two Basel III liquidity ratios, Chinese banks are required to meet other regulatory liquidity indicators such as deposit-to-loan ratio, liquidity gap ratio and financing concentration76 and to monitor the liquidity of deposits daily and loans monthly77. CBRC believes that this will motivate banks to establish a system of liquidity risk controls that incorporates multiple scenarios, currencies and time-frames78. The CBRC has also issued guidelines on liquidity risk management. Amongst many others, CBRC’s recommendations encourage banks to79 Appoint dedicated personnel for liquidity risk management; Incorporate liquidity risk management into banks’ internal audit processes; Perform stress tests covering scenarios such as erosion in the value of liquid assets and

significant loss in retail deposits; Formulate emergency plans and Develop a list of early warning indicators of liquidity risks e.g. rapid assets growth, increase in

counterparties’ requests for additional collateral for credit exposure, refusals by counterparties to carry out new transactions, etc.

15

SECTION 3: ADDITIONAL MEASURES IMPOSED/ PROPOSED BY CHINA BEYOND BASEL III

1. LOAN LOSS PROVISIONING CBRC requires banks to set aside provisions of at least (a) 2.5% of total outstanding loans (“loan loss provision ratio”) and (b) 150% of total non-performing loans (“provisioning coverage ratio”), whichever is higher80. As the loan loss provision ratio is linked to loan size rather than asset quality, it is more sensitive to credit expansion and thus acts as a countercyclical balance which accumulates reserves during credit expansion and which could be used to cover losses during economic downturns, hence compensating for the underestimation and overestimation of loan losses over the credit cycle81. RESPONSE TO LOAN LOSS PROVISIONING Evaluation of effectiveness The media notes that 2.5% is a high requirement going by international standards and should bolster investors’ confidence in mainland banks82. Market analysts by and large gave support to the new rules and CBRC’s model of “prudent banking supervision” 83. Bankers could also understand why regulators would want to build up precautionary reserves to cover non-performing loans given the high rate of loan growth in recent years84. However, citing statistics from a study done by CBRC, a South China Morning Post journalist opined that the new standards would still be insufficient against future loan losses. In a CBRC investigation on bank lending to local government-backed investment projects, the CBRC estimates that only 27% of loans could be serviced by cash flows from the projects and that as much as 23% of loans (1.7 trillion yuan) were highly likely to turn bad while a further 50% would likely require additional support from the local governments85. As the local government guarantees are implicit (and not explicit) and local governments could choose not to extend support, there is a risk that as much as 5.62 trillion yuan in bank loans could default86. Using typical recovery rates of 20%, this means that losses could amount to 9% of banks’ entire loan books87. In comparison, the 2.5% loan loss provision would thus be inadequate88. If the estimated losses truly materialised, profits for the entire banking industry would not only be completely erased, CAR would also be forced down to single digits89. To compound the problem, up to 40% of local government debts are due to mature in 2011 and 2012 and bank loans take up 79% of total local government debts90, which means that repayment risks, if any, are imminent. To further address default risks arising from local government backed loans, the CBRC has instructed banks not to extend loans to local governments for “unapproved projects” and is working with local governments to keep their debt at manageable levels91. In a move supported by local economists, the Ministry of Finance has also advised local governments to sell realisable assets to help pay off debts92.

16

Impact on banks While bankers generally do not think meeting the 150% minimum provision coverage ratio is a problem (industry’s provisioning coverage ratio stood at 155% as of end 200993), they see the 2.5% loan loss provision ratio as a challenge94. Bankers also expect the new provision policies to negatively affect profitability95. Economists further predict that such pressures would continue in the longer-term96. Faced with more intense regulatory constraints, a senior bank executive opined that banks would have to accelerate their transformation to maintain profitability growth97. 2. MORTGAGE LOAN & PROPERTY MARKET RESTRICTIONS China imposes dynamic loan-to-value (LTV) and debt-to-income (DTI) ratios on home mortgage lending98 and requires minimum down payments of 40% for second home mortgage loans to discourage speculation in the property market99. In addition, further restrictive measures could be imposed in selected cities. Examples include: (a) the imposition of property taxes100; (b) disallowing ownership of more than 2 houses per family in one’s hometown101; and (c) disallowing ownership of more than 1 house if the city is not one’s hometown102. Most recently in August 2011, the government introduced a pilot scheme for land auctions whereby the cost of the land is fixed and the developer who promises the lowest selling price for homes developed on the site would be awarded the auction103. RESPONSE TO MORTGAGE LOAN & PROPERTY MARKET RESTRICTIONS A senior government researcher sees China's attempts to cool soaring property prices as measures to control inflation and “ease social discontent over widening wealth disparity”104. There are signs that the policies are beginning to work. Property developers have reported an increase in inventory in the first half of 2011105. Property prices in cities such as Beijing, Shanghai, Guangzhou and Shenzhen where additional restrictions are imposed have increased at a slower rate than those where restrictions are not imposed106. In June 2011, 26 cities out of 70 major cities even reported declining or stagnating prices which is an improvement over May 2011’s 20 cities107. There are, however, implementation challenges on the ground. Individuals who still wish to buy additional properties are advised by property agents not to take mortgage loans and to pay “extra fees” to local officials to circumvent the rules. Analysts also expect some couples to file for divorces so that up to 4 houses (instead of 2) could be purchased108. The government is aware that local implementation may be lacking and sends investigation teams to provinces and cities to assess the real situation109. Others point out that property purchase restrictions are but short-term measures; to address the longer term issues, the government should commission more affordable housing projects to meet growing demand110.

17

3. TIGHTENED MONETARY POLICIES To discourage excessive bank lending, the central bank frequently raises the reserve requirement ratio (e.g. the ratio has been raised at least 6 times in 2011 and the 12th time since January 2010111) and the benchmark interest rate112. The PBOC is also considering implementing differentiated reserve requirement ratios for different banks113. RESPONSE TO TIGHTENED MONETARY POLICIES Commentators observe that loose monetary policy in the past has led to over-enthusiastic lending114 and agree that the reserve ratio is one of the most effective ways to discourage excessive lending115. Indeed, tightened monetary policies have led some banks to increase minimum down payment for property purchases and raise mortgage interest rates, suggesting that tightened monetary policies have been effective, at least in some sectors, in discouraging excessive lending116. However, the reduction in the availability of loans and increase in borrowing costs have caused difficulties for Small-and-Medium- size Enterprises (SME)117. Some businesses in Xijiang, for instance, have put expansion plans on hold or closed down production lines 118 . The Wenzhou SME Development Association even warned that as much as 40% of SMEs in China would have to cease operations if access to bank loans continues to be limited119. On the other hand, effectiveness of the policy is marred by implementation loopholes. Banks have tried to circumvent the tighter monetary conditions by engaging companies to source and channel large deposits to the banks on the last day of each month to temporarily boost their deposits base and meet the required reserve requirements for reporting to the central bank120. 4. ADDITIONAL MEASURES TO CONTROL AND DIRECT CREDIT GROWTH In addition to the above, China has introduced other measures to discourage unnecessary credit growth and to direct credit growth to the real economy. Examples include: (a) Forbidding blanket loan agreements for unspecified projects121 (b) Encouraging banks to focus on loan quality over quantity. Directives specify that attention

ought to be paid to documentation122, due diligence, large exposure limit and accurate loan classification123. Directives cover a wide spectrum of loan types. For instance, the frequently-dubbed "Three Measures and One Guideline" cover loans for fixed assets, project financing, liquidity loans and personal loans124. The directives also provide very detailed guidance. For example, in the Provisional Rules on the Management of Fixed Asset Loans, lending procedures including preliminary reviews of loan applications, risk evaluation, loan approvals and loan disbursements are extensively described125.

18

(c) Encouraging banks to extend loans to the real economy rather than to the property and stock markets, which are susceptible to asset bubbles126. For instance, to ensure that loans are used for the declared purpose, lenders are asked to disburse funds directly to the end supplier declared by the borrower, instead of to the borrower127. This addresses the phenomenon described by a banking insider whereby Chinese enterprises previously borrow more than is needed for business operations and channel the excesses to speculation128.

RESPONSE TO ADDITIONAL MEASURES TO CONTROL AND DIRECT CREDIT GROWTH As the directives focus on loan quality rather than impose explicit quantity restrictions, analysts opined that this is a clever way to manage credit growth while still enabling credit to flow to the real economy129. Different commentators have viewed the new directives positively: Yu Xiaoyi, analyst with Guangfa Securities, sees the directives as enabling banks to engage in

sustainable expansion130. Guo Tianyong, a professor with the Central University of Finance and Economics, opined that

the new directives will prevent systemic risk associated with rapid credit expansion131. Jing Ulrich, Chairman of China Equities and Commodities at JP Morgan Chase, expects banks

to continue to lend to support real economic activity, but be more vigilant especially in short-term lending and heed the regulators’ advice on guarding against asset bubbles132.

5. CONCENTRATION LIMITS Chinese officials view concentrated loan portfolios as a possible source of systemic risk as they believe banks with concentrated loan portfolios are more sensitive to fluctuations in macro-economic variables133. To manage concentration risks, CBRC requires banks to extend loans through syndication if the exposure to any single company or project exceeds 10% of capital or if the exposure to a conglomerate exceeds 15% of capital134. Banks are also reminded to aggregate bonds, loans, guarantees and credit commitments when measuring credit concentration risk exposure to corporate borrowers135. 6. SEPARATE BANKING AND CAPITAL MARKETS The CBRC believes that when banking and capital market operations are allowed to interact, financial institutions become more complex and regulatory limits lose some of their effectiveness136. As the boundary between banking and capital markets becomes blurred, contagion risk across markets is also exacerbated137. The recent crisis in which securitization created the linkage between banking and capital markets and distorted the incentives of loan originators, further convinced CBRC of the need to segregate banking and capital markets, a policy it terms as the “firewall” between credit and capital markets. It believes that a firewall is particularly well-suited given the early stages of financial market development in China138. To erect the firewall, the CBRC restricts banks from offering guarantees for bond issuance and checks for illegal flows of credit funds into the stock market139. There is also a clear prohibition of

19

complicated securitisation and re-securitisation140. Securitisation of non-performing assets and assets with less predictable cash flows are also strictly controlled141. 7. INTERNATIONAL BANK RESOLUTION PROCESS Beyond domestic regulation, CBRC Chairman Liu has a suggestion for cross-border bank resolutions142. As it is difficult to harmonize legal frameworks across countries, he suggests that an international treaty establishing rules on depositor protection and information sharing across countries should be established to ensure that stakeholders across jurisdictions are fairly and equally treated. 143 This would provide clarity on the resolution process and limit opportunities for national authorities to take unilateral actions144, which may be to the disadvantage of foreign counterparties145. The CBRC has already begun work on its suggestion. In July 2011, the CBRC signed an agreement with the Monetary Authority of Singapore (MAS) where the 2 countries agree to “strengthen cooperation and information-sharing on cross-border crisis management and resolution issues”146. RESPONSE TO SUGGESTION ON INTERNATIONAL BANK RESOLUTION The Wall Street Journal Asia notes that such public suggestions from China on the global financial framework are rare147. While the impact of such a proposed treaty on Chinese banks is expected to be minimal in the near future as Chinese banks are as yet not major global players, this is likely to change in the longer term when Chinese banks ‘go global’ and as the Chinese yuan becomes more widely used148. SECTION 4: CHINA’S RESPONSE: SUMMARY & CONCLUSION

In summary, China supports the broad concept of Basel III. Officials welcome the tighter regulation in Basel III as it indirectly endorses the Chinese’s traditionally conservative regulatory approach and furthers their plans to strengthen the domestic banking system. Basel III also comes at an appropriate time as tougher regulations would counter the current high credit growth rates in China. Notwithstanding the Chinese’s endorsement of Basel III, officials are open to customise domestic rules where they deem appropriate. In areas where they have done so, rules tended to be more stringent, because Chinese banks have already largely met Basel III requirements and are in the position to withstand stricter rules. The local business community has generally taken Basel III positively, being well-positioned to meet the higher standards, and support countercyclical and leverage measures as good and innovative measures for the industry. Beyond Basel III, officials have introduced several measures relating to the extension of loans to manage credit risk and credit growth. The CBRC also believes that banking and capital markets should be separated by a “firewall” to limit contagion risks.

20

CHAPTER 2: HONG KONG

This chapter focuses on Hong Kong’s responses. The first section summarises Hong Kong’s general reaction towards Basel III while the second section focuses on its responses to specific Basel III recommendations. The third section highlights additional measures taken by Hong Kong beyond Basel III. Within each section, views of regulators and business commentators are presented. SECTION 1: HONG KONG’S RESPONSE TOWARDS BASEL III AS A WHOLE

THE OFFICIAL RESPONSE Support for Basel III The Hong Kong Monetary Authority (HKMA) states publicly that it is supportive of the underlying objective of Basel III to strengthen the resilience of the banking sector against cyclical economic shocks and intends to fully implement Basel III in Hong Kong1. Officials from HKMA dispelled the misconception that Basel III is not relevant for Hong Kong simply because Hong Kong banks have escaped relatively unscathed from the Global Financial Crisis. While Basel III has indeed been designed to address faults in failed banking systems in the West, it would be a mistake to ignore Basel III because Hong Kong as an international financial centre must adopt international standards2 and contribute to the resilience of the global financial system3. Hong Kong also needs to be concerned because Asia is not “decoupled from the developed world”

and if Basel III significantly affects Western banks, Asia would also be impacted 4. Furthermore, Asia’s speedy recovery should not be construed to mean that its banking system is sufficiently robust. The region’s quick recovery is also very much due to the underlying growth momentum of the economies5 and the fact that the region’s debt products are not as complicated as those of the developed world6. Notwithstanding Hong Kong’s official support for Basel III, the HKMA makes it clear that endorsing Basel III does not mean that measures would be adopted wholesale and inflexibly7. Desire for Increase in Asian Representation Speeches by HKMA officials acknowledge that Asia currently does not have a strong presence in international forums8, which are currently dominated by countries “in the deepest trouble” 9. Nevertheless, Asia still has a “responsibility to speak up” to ensure that decisions made take into account Asia’s circumstances10. Asia needs to continue to participate not only because of its growing economic influence but also because developing economies tend to suffer the most in economic crises11. On a positive note, HKMA observes that Asia has gained greater participation in international forums which signals that “the world is paying attention to, and ready to learn from, the experiences of this region”12.

21

THE BUSINESS COMMMUNITY RESPONSE Positive … The general consensus amongst bankers in Hong Kong is that Basel III “will make banks more stable in the face of financial turbulence”13. …. but with notes of caution However, Asian bankers including those from Hong Kong also state that they would like regulators to be conscious of “the cumulative impact of different measures”14. SECTION 2: HONG KONG’S RESPONSES TOWARDS SPECIFIC BASEL III RECOMMENDATIONS

1. BASEL III CAPITAL REQUIREMENTS Basel III has increased minimum Common Equity Tier 1 from 2% to 4.5% and minimum Tier 1 Capital from 4% to 6% but held minimum Total Capital constant at 8%15. An additional conservation buffer of 2.5% which banks could draw on in stress times would also be imposed16. The definition of what qualifies as capital has also been tightened17. With transitional arrangements, the new rules would

be fully implemented by beginning 201918. HONG KONG’S OFFICIAL RESPONSE TO BASEL III CAPITAL REQUIREMENTS Karen Kemp, HKMA’s executive director for banking policy, believes that the crisis has clearly highlighted that pre-crisis capital levels were too low19. Hence, higher capital requirements would be a step in the right direction. The HKMA thus intends to implement the higher minimum capital requirements in accordance with the Basel Committee on Banking Supervision (BCBS) transitional timetable20. Officials foresee no problems in local banks meeting the new regulatory standards as many Hong Kong banks have already exceeded Basel III minimum capital requirements21 (as of March 2011, average Tier 1 ratio was 12.5% while average Total Capital Adequacy Ratio stood at 16%22). Hong Kong’s existing capital rules are also already largely aligned with the tightened definition of capital23. The HKMA’s own quantitative impact study on the new capital and liquidity rules suggest that “regulatory reform would bring a net positive long-term effect for the Hong Kong economy” albeit the net benefit was estimated to be lower than that found in a separate study performed by BCBS for selected economies (HKMA: 2.11% - 2.76% of real GDP vs. BCBS: 4.3% - 5.85%, under the assumption of permanent GDP loss in banking crises)24. The milder impact reflects the already high capitalisation of Hong Kong banks, the significant use of common equity in banks’ capital base and the reliance on stable customer deposits as key funding sources (77% of total funding) 25.

22

HONG KONG’S BUSINESS COMMUNITY RESPONSE TO BASEL III CAPITAL REQUIREMENTS Confidence in meeting standards Local bankers expressed confidence in meeting the higher capital requirements. Andrew Fung, general manager and head of treasury and investment at Hang Seng Bank, believes that local banks would have no problems meeting the new standards especially given the long transitional period26. Other Hong Kong-based commentators agree, noting that unlike European and American banks, Hong Kong capital ratios are much higher27. Moreover, given that hybrids and other non-common equity capital are not common components of the capital base of Hong Kong banks, domestic banks would have no problems meeting the Common Equity Tier 1 ratio which is viewed by many as the most challenging capital requirement28. The local stock market also reacted positively on news of Basel III capital requirements, reflecting a similar confidence that Hong Kong banks would not be forced to raise fresh capital29. Fung believes that the only adjustment banks might have to make is to revise their loan portfolios in the future to attract lower capital charges30. Some fund managers, however, highlighted that banks which are intensifying expansions may face cash shortages and would have to cut dividend payout ratios given the higher capital requirements31. This could cause their stocks to fall out of favour with investors as investors generally invest in Hong Kong-listed bank stocks for their high and stable dividends32. Well-capitalised banks, however, are unlikely to be affected33. Transition period is too long Commentators in the local media opined that the 2019 implementation timeframe is too long and by 2019, another 2 financial crises could have occurred 34 . There are concerns that the long implementation timeframe could result in a scaling back of reforms as memories of the crisis fade and lobbying from the industry grows stronger35. However, the HKMA clarifies that Basel III’s long transitional period is meant “to allow unintended consequences [of the reforms] to be observed and addressed” and to recognise the current challenging economic realities36. The long implementation period thus should not be interpreted as a lack of resolve37. Divestment of non-core assets creating opportunities for new start-ups Simon Yoo, Asia-Pacific co-head of financial institutions at Citigroup, forecasts that in the new regime where capital is harder to come by, owning diversified businesses would be a challenge38. Hence, banks would be under pressure to divest riskier, non-core businesses39. Indeed, the industry has observed a number of new Asian-focused hedge funds spun out from banks’ proprietary desks and set up by managers from established funds starting out on their own40. One manager who jointly bought out the private equity arm of his bank with other managers to set up their own fund explained that an additional benefit of leaving the bank is that they would be less subjected to continually changing banking regulations41.

23

2. BASEL III COUNTER-CYCLICAL CAPITAL BUFFER Under Basel III, an additional counter-cyclical buffer of up to 2.5% of Common Equity Tier 1 could be imposed in periods of rapid credit growth and released in downturns42. HONG KONG’S OFFICIAL RESPONSE TO COUNTERCYCLICAL CAPITAL MEASURES The HKMA supports the adoption of countercyclical capital buffer but expects the transition and implementation phase to bring out new questions such as the amount of lead time to give banks to build up the buffer, the type of communication strategy to employ43, etc. Issues such as difference in opinions between home and host regulators would also have to be worked out. For example, in the event that a home regulator thinks there is credit expansion in the host country but the host regulator does not trigger the buffer, a question would be whether the home regulator should take any action44. Apart from Basel III’s countercyclical capital buffer, Hong Kong has implemented other countercyclical measures45. For instance, it actively monitors credit growth in the economy and intensifies supervisory efforts as well as issues additional guidance to banks when credit growth is deemed too rapid. In December 2010, the HKMA expressed concerns that drawing from “international experience”, the strong credit growth in the jurisdiction might partly be due to lax underwriting standards and if this is indeed the case, it would increase systemic risks to the whole banking system46. To address this concern, the HKMA would thus step up on-site examinations to monitor loan approvals47. In April 2011, the HKMA issued a public letter to Chief Executives of banking institutions, warning that loans granted by them have grown very rapidly and cautioned that the “rapid pace of credit growth is unsustainable” and could lead to “pressure on funding, liquidity and concentration”48. It then instructed banks to submit new business plans and targets for loan and deposit growth, L/D ratio and other risk indicators for the remaining 2011 to the HKMA 49. 3. BASEL III LEVERAGE RATIO Under Basel III, a non-risk-weighted minimum leverage ratio (defined as the ratio of Tier 1 capital to total exposures, including on- and off-balance sheet items) of 3% is being tested for planned migration to Pillar 1 in 201850. HONG KONG’S OFFICIAL RESPONSE TO LEVERAGE RATIO The HKMA announced that it intends to adopt BCBS implementation timetable, including transitional arrangements for the leverage ratio51 and would closely monitor effects of the new leverage ratio to ensure that it does not adversely affect banks which are fundamentally sound and conservative52.

24

4. BASEL III LIQUIDTY RATIOS Under Basel III, two liquidity standards would be introduced: (a) A minimum Liquidity Coverage Ratio (LCR) of 100% would be imposed to ensure that the

bank holds sufficient high quality assets to cover net cash outflows for 30 days in a severe stress scenario53.

Eligible assets are categorised into ‘level 1’, comprising mainly domestic sovereign bonds and ‘level 2’ which can include non-financial corporate bonds and covered bonds not issued by banks54. Haircuts are applied to level 2 assets and such assets cannot make up more than 40% of the overall stock after haircuts have been applied55.

(b) A minimum Net Stable Funding Ratio (NSFR) of 100% would be imposed to ensure that

stable funding is available to cover funding requirements over a one year period of extended stress56.

HONG KONG’S OFFICIAL RESPONSE TO LIQUIDITY RATIOS Confident in meeting standards although lack of supply of eligible assets is a challenge The HKMA does not expect banks in Hong Kong to have significant problems complying with the new liquidity standards but would take into account the issue of insufficient supply of HKD-denominated government debt and high quality non-financial corporate debt in its implementation of the LCR57. The HKMA would also provide feedback to the Basel Committee on this issue58. Banks need to begin preparation now Arthur Yuen, deputy chief executive of HKMA, urged bankers to begin preparation soon as the implementation timelines are only "deceptively long" because as part of the observation period for the LCR, banks need to complete detailed studies very soon so that regulators could report findings to the Basel Committee by 2013 for implementation in 201559. Unintended effects on corporate debt markets and stability of retail deposits On the downside, HKMA officials have highlighted that there are possible unintended adverse consequences. For one, the LCR requires banking institutions to own high quality government and public sector debt. In Asia, where debt markets are not as developed, trying to develop the corporate debt market would be even more difficult in the future as the LCR does not count corporate debt as highly liquid assets (i.e. level 1) 60. In addition, the competition amongst banks for ‘sticky’ retail deposits may actually result in retail deposits becoming less ‘sticky’ because as banks raise interest rates to attract ‘sticky’ deposits, customers become less loyal and are more ready to shift deposits to banks offering higher rates, making retail deposits a less stable funding source61. The HKMA, however, puts to rest concerns that higher costs brought about by higher deposit rates could be passed on to bank customers62. It believes that there would be minimal impact on consumers’ cost as competition in Hong Kong’s banking sector is intense63.

25

Observation period is essential Kemp believes that since the liquidity standards are un-tested and the impact of the new standards on banks’ liquidity risk management and on the corporate debt market is uncertain, the observation period is critical64. Existing liquidity measures With the introduction of Basel III liquidity ratios, the HKMA is also reviewing the relevance of its existing liquidity measures. It is conducting a quantitative impact study65 to decide whether Hong Kong banks should continue to be required to maintain 25% of liquid assets on top of deposits66. In other areas, the HKMA has decided to retain additional liquidity measures. The HKMA expects banks to continue to ensure that they have sufficient funds to continue operations for a minimum stress period of five business days under a bank-specific crisis scenario, which includes a retail deposit run, in addition to the LCR requirement 67. HONG KONG’S BUSINESS COMMUNITY RESPONSE TO LIQUIDITY RATIOS Confidence in meeting NSFR Given that the majority of Hong Kong banks have extensive retail networks and substantial deposit bases, industry commentators do not expect Hong Kong banks to have problems meeting the NSFR68. LCR may not reflect Asia’s liquidity problems However, some believe that the liquidity reform fails to reflect issues specific to Asia. Simon Topping opined that the LCR was modelled based on “liquidity problems experienced by banks in the West during the global financial crisis” such as the drying up of wholesale funding markets, whereas in Asia, liquidity problems are often caused by bank runs69. For instance, Asia’s deposit run-off rate is 20 or 30 times higher than that assumed by Basel70. Asia’s bank run problems are more acute due to lower public confidence in banks71. This is because for a long time, there is no established deposit insurance and Asia’s history is marked by massive bank runs of not just small but also large banks72. He further highlights that while Basel III’s 30-day timeframe is based on “slow-burn liquidity problems”, things in Asia move much more quickly73. Hence, he suggests, local regulators should introduce 7-day periods to reflect local circumstances74. Too much reliance on government debt Gary Wang, finance director at Dah Sing Bank in Hong Kong, opined that the list of eligible assets placed too much emphasis on government debt75. The focus on government debt forces commercial banks to hold low-yielding assets which are not part of commercial banks’ core businesses76. Another commentator close to the Asian banking sector, also highlights that “the requirement to hold large quantities of government debt perversely penalises well-managed economies” with sound fiscal policies77.

26

Insufficient supply of eligible assets The initial Basel III proposal in December 2009 was met with criticisms from countries with limited supply of government bonds including Hong Kong78. As a result, for such jurisdictions, the revised proposal allows additional options including (a) contractual committed liquidity facilities from the relevant central bank, with a fee (b) foreign currency liquid assets and (c) additional use of Level 2 assets with a higher haircut79. However, the additional options are also met with criticisms (elaborated below). Additional options are not without problems Banking experts suggest that the committed liquidity facility with the central bank increases the risk of moral hazard, as it blurs the role of the central bank as a lender of last resort 80. Topping also believes that Basel has not fully considered the extent to which foreign currency assets could be applied to a bank’s balance sheet81. Although Hong Kong is in a slightly more enviable position compared to other jurisdictions with limited supply of government bonds as banks in Hong Kong could overcome the lack of HKD denominated government bonds by buying US treasuries and not face significant currency risk given the HKD’s peg to the USD, there could still be interest rate mismatches82. In addition, Dah Sing’s Wang points out that if the bank’s liability base is HKD, there would still be a need to enter currency swaps arrangements, thereby incurring costs83. Other assets should also be eligible Wang also believes that banks in Hong Kong and Asia should be allowed to count high-quality prime residential mortgages with low loan-to-valuation ratios as eligible assets since such assets have proven for many decades to be of high quality and especially if they are accepted by central banks as collateral of sufficiently good quality84. Doubts over whether rules would be adapted for local circumstances However, there are doubts that local regulators would have much room to deviate from international norms given the practice of peer reviews by fellow regulators from other jurisdictions and the value Basel III places on consistency85. 5. ENHANCING RISK COVERAGE Under Basel III, capital requirements for counterparty credit risk exposures in derivatives, repo and securities financing activities will be strengthened86. Incentives are also introduced to move Over-the-Counter (OTC) derivative contracts to central counterparties (CCP)87. HONG KONG’S OFFICIAL RESPONSE TO ENHANCING RISK COVERAGE HKMA intends to implement Basel III reform package and is currently studying the feasibility of adopting advanced methods for counterparty credit risk calculations 88. Hong Kong has also committed to establishing a clearing house89.

27

HONG KONG’S BUSINESS COMMUNITY RESPONSE TO ENHANCING RISK COVERAGE Keith Noyes, Regional Director (Asia Pacific) at the International Swaps and Derivatives Association (ISDA) based in Hong Kong, observed that the G20 did not specify whether CCPs have to be home country CCPs or global CCPs90. An Asian regulator opined that it would be difficult to rely on foreign CCPs if they are not regulated by the host countries as there is no certainty that local banks would be treated fairly and equally by the foreign CCPs91. Given so, it is not surprising that a number of countries in Asia including Hong Kong, China, India, Japan, South Korea and Singapore are creating or have created home country CCPs92. However, Noyes pointed out that Asian markets are not big or liquid enough to ensure the viability of home country clearing entities93. According to a Bank for International Settlements Triennial Survey, Asia Pacific interest rate derivatives markets account for only about 8% of total global volume as of 30 June 201094. HKD swaps, for example, are substantially cleared through the London Clearing House95. The unfortunate implications of this are that clearing houses may have to either accept less liquid and less standardised products to boost volume which introduces greater risk or impose higher clearing fees which may discourage end users from hedging96. An additional complication could arise when trades are entered with foreign counterparties. If regulators mandate that banks must clear trades through a local clearing house, which appears to be the case for Hong Kong, it is unclear which country’s clearing house should be used97. In complying with the new clearing rules, banks may also incur additional costs as some Asian clearing houses are/would be using customised platforms which do not interface easily with banks systems resulting in the need for banks to purchase additional technology solutions98. SECTION 3: ADDITIONAL MEASURES ADOPTED/BEING CONSIDERED BY HONG KONG BEYOND BASEL III

1. LOAN-TO-VALUE (LTV) & DEBT SERVICING RATIO (DSR) The HKMA has introduced several prudential measures, including: (a) Imposing maximum LTV ratios based on the value of the properties99:

Residential Property Value (HK$)

Maximum Loan-To-Value (LTV)

10 – 12 million 50%

7 – 10 million 60% (with maximum loan amount capped at HK$5 million)

Below 7 million 70% (with maximum loan amount capped at HK$4.2 million)

(b) Lowering the above maximum LTV ratios by 10% if the principal income of the loan applicant

is not derived from Hong Kong100;

28

(c) Imposing maximum LTV ratio of 40% for net worth-based mortgage loans as it is difficult to regularly verify borrowers’ net worth101;

(d) Imposing maximum LTV ratio of 50% for non-owner-occupied properties, properties held by

companies and commercial/industrial properties102; (e) Imposing 50% cap on DSR103; and (f) Limiting stressed DSR to 60%. Stressed DSR is computed assuming a 2% increase in mortgage

rates104. Used as countercyclical prudential measures, the HKMA proactively lowers LTV ratios when it observes warning signs such as:

high transaction prices in government land sale auctions

high property prices above 1997 peaks and

unusually low mortgage rates e.g. 1% vs. more typical rates of 10%105. Prudential measures are also introduced in response to supervisors’ findings during onsite examinations. For example, supervisors noted that banks faced difficulties assessing the debt servicing ability of borrowers who derive income principally from overseas106 and thus direct that maximum LTV ratios for such applicants be lowered by a further 10%. In addition to the above prudential measures, the HKMA disallows the practice of principal repayment holidays whereby borrowers service only interest payments during the holidays and repay principal only after the holidays end107. Banks are also expected to meet industry best practices published by the HKMA such as those relating to the computation of DSR and proof of income108. The government also manages the supply of land to address supply-side imbalances109. Official evaluation of effectiveness The HKMA sees LTV as a cornerstone of its policies that has survived market innovation viz. securitisation and contributed to the stability of the banking system110. So convinced it is of its effectiveness that Joseph Yam, then Chief Executive of HKMA, wondered publicly why developed economies did not adopt LTV ratios as one of their prudential measures111. An econometric analysis performed by the HKMA on 13 economies confirmed that the LTV ratio is an effective tool in reducing systemic risk arising from property market cycles112. Systemic risk is contained by reducing the sensitivity of mortgage default risk to property price shocks113. For instance, if the maximum LTV ratio had been 90% instead of 70% before 1997, the delinquency ratio of a 40% decline in property prices in 1997–1998 would have been 1.7% instead of the actual level of 0.84% as of end-1998114. Using data from three economies that have adopted LTV, the study also found that the effect of LTV policy is transmitted through lowering household leverage rather than directly dampening property market activities115. The tool is not without adverse impact though. LTV limits could impose higher liquidity constraintsa on home buyers but mortgage insurance programmes (see Annex at end of Chapter) could and were

a Home buyers may not qualify for a mortgage even if they could service the loan repayments because they

cannot afford the substantial down payments.

29