Authorized Economic Operator Program Compendium - AIMP - Asia

___________________________________________________________________________

2013/FMP/WKSP4/004 Session: II

Basel 3 and Trade Finance

Submitted by: International Finance Corporation

Workshop on Trade FinanceLombok, Indonesia

1 July 2013

Anurag Mishra

Regional Head, APR

Global Trade and Supply Chain

International Finance Corporation

July, 2013

Basel 3 and Trade Finance

• Basel 3 Aims at Improving Resilience of Banking Sector

• In the process it has come up with set of recommendations - as

far as Trade Finance is concerned it has made people nervous.

• Trade is also an important pillar of Economic Growth.

• Global Crises resulted in 23% decline in Trade volume in 2009.

• Present set of recommendations could have a similar impact on

Trade Finance.

• This could have a crippling impact on the Transformational shift

predicted in Trade Flows and in turn impact the role of Trade in

Global Economic growth and Global Economic Growth itself.

Background

Basel III – Strengthened pillars

Basel III focuses on bringing stability to financial markets by having

Stricter Capital, Leverage and Liquidity Requirements.

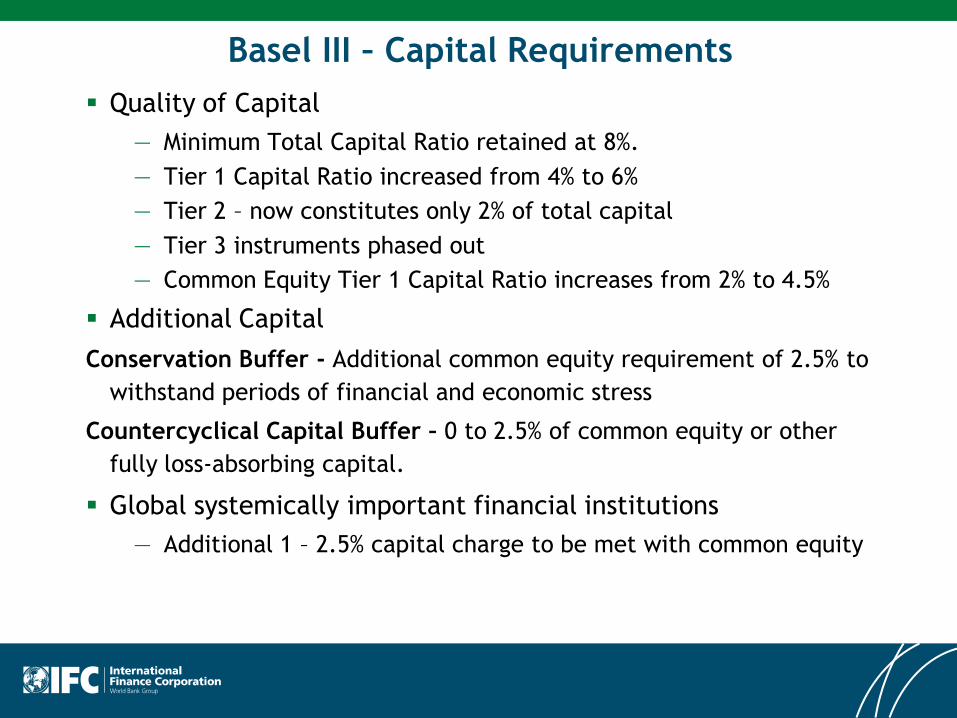

Basel III – Capital Requirements

Quality of Capital

— Minimum Total Capital Ratio retained at 8%.

— Tier 1 Capital Ratio increased from 4% to 6%

— Tier 2 – now constitutes only 2% of total capital

— Tier 3 instruments phased out

— Common Equity Tier 1 Capital Ratio increases from 2% to 4.5%

Additional Capital

Conservation Buffer - Additional common equity requirement of 2.5% to

withstand periods of financial and economic stress

Countercyclical Capital Buffer – 0 to 2.5% of common equity or other

fully loss-absorbing capital.

Global systemically important financial institutions

— Additional 1 – 2.5% capital charge to be met with common equity

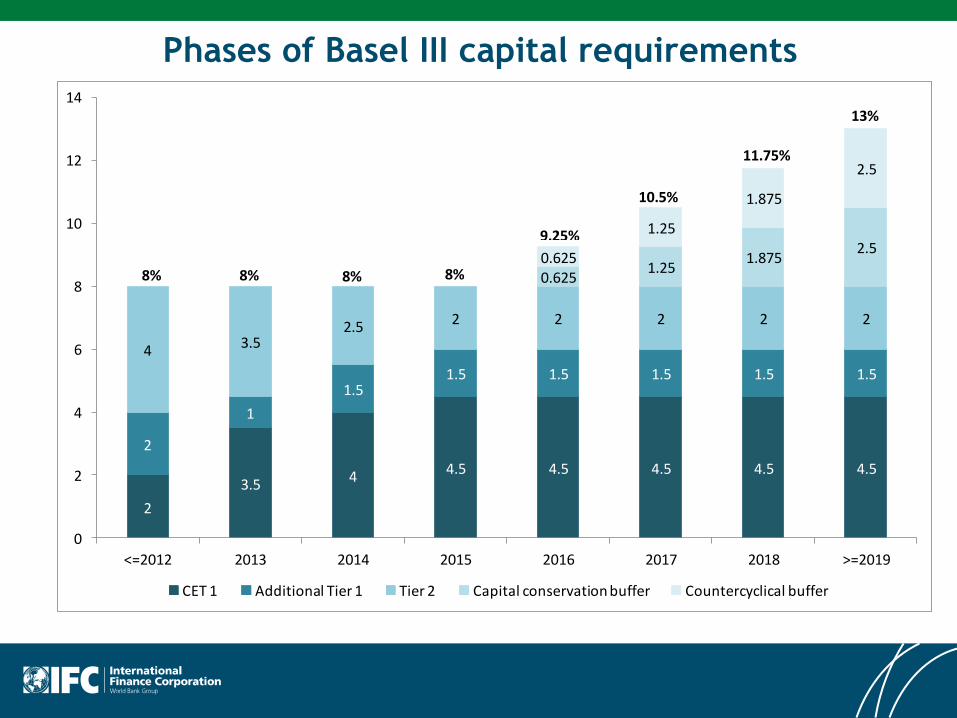

Phases of Basel III capital requirements

2

3.5 4 4.5 4.5 4.5 4.5 4.5

2

1

1.51.5 1.5 1.5 1.5 1.5

4 3.52.5 2 2 2 2 2

0.6251.25

1.8752.5

0.625

1.25

1.875

2.5

0

2

4

6

8

10

12

14

<=2012 2013 2014 2015 2016 2017 2018 >=2019

CET 1 Additional Tier 1 Tier 2 Capital conservation buffer Countercyclical buffer

8% 8% 8% 8%

9.25%

10.5%

11.75%

13%

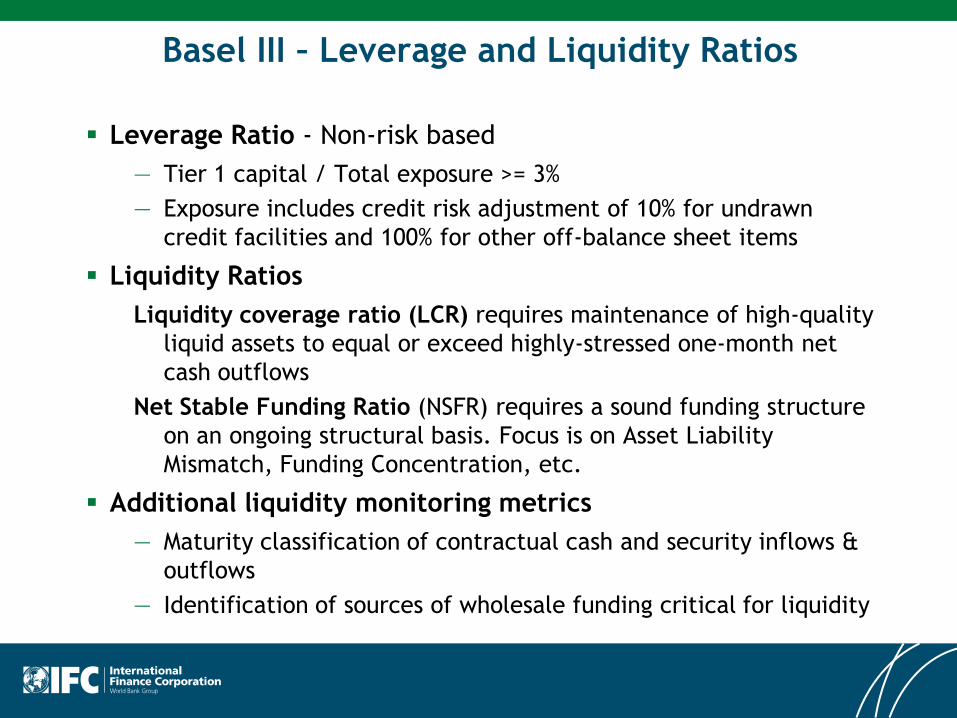

Basel III – Leverage and Liquidity Ratios

Leverage Ratio - Non-risk based

— Tier 1 capital / Total exposure >= 3%

— Exposure includes credit risk adjustment of 10% for undrawn

credit facilities and 100% for other off-balance sheet items

Liquidity Ratios

Liquidity coverage ratio (LCR) requires maintenance of high-quality

liquid assets to equal or exceed highly-stressed one-month net

cash outflows

Net Stable Funding Ratio (NSFR) requires a sound funding structure

on an ongoing structural basis. Focus is on Asset Liability

Mismatch, Funding Concentration, etc.

Additional liquidity monitoring metrics

— Maturity classification of contractual cash and security inflows &

outflows

— Identification of sources of wholesale funding critical for liquidity

Basel III regulations will have significant effect on trade finance

Quality of Capital – Most of the Capital Requirement needs to

be met through Common Equity – it will increase cost of

doing business including Trade Finance.

Amount of Capital - In addition to Tier1 and Tier 2 Capital –

the Capital Conservation Buffer plus Counter Cyclic Buffer

and Additional Capital requirement for G-SIBs can add up to

15.5% - which again adds to cost.

However non G-SIBs will also suffer on account of higher cost

of funds as they typically borrow from G-SIBs who will have

no choice but to lend at higher rates to recover their cost.

It will also impact trade business denominated in non G3

currencies as local banks will be more liquid and therefore

competitive than the G-SIBs in this space.

Impact of Basel III on Trade Finance

Impact of Basel III on Trade Finance (cont.)

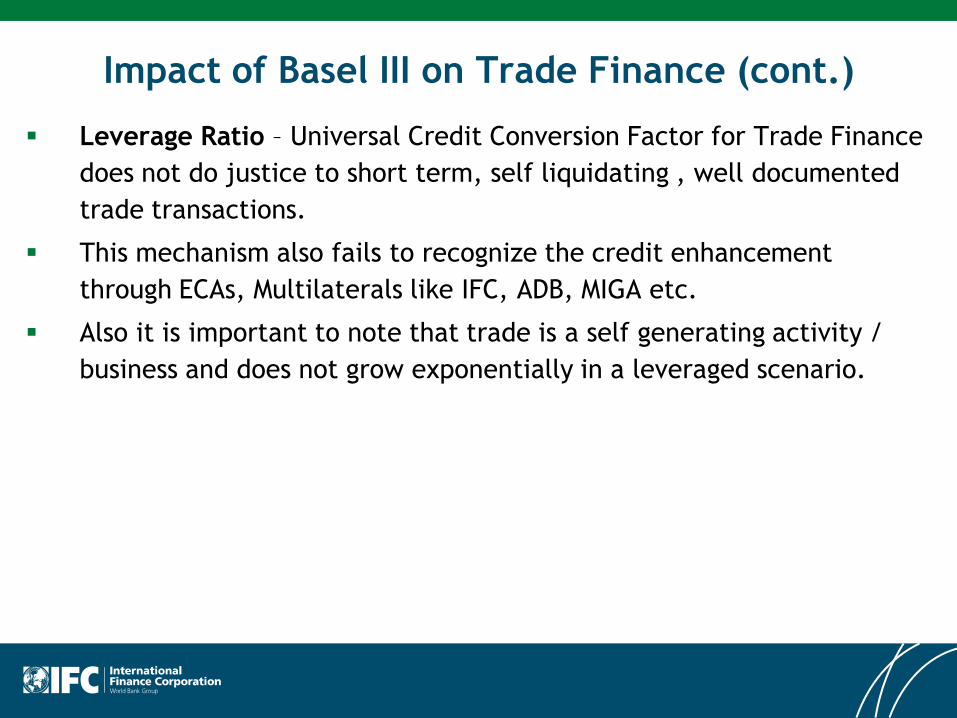

Leverage Ratio – Universal Credit Conversion Factor for Trade Finance

does not do justice to short term, self liquidating , well documented

trade transactions.

This mechanism also fails to recognize the credit enhancement

through ECAs, Multilaterals like IFC, ADB, MIGA etc.

Also it is important to note that trade is a self generating activity /

business and does not grow exponentially in a leveraged scenario.

Impact of Basel III on Trade Finance (cont.)

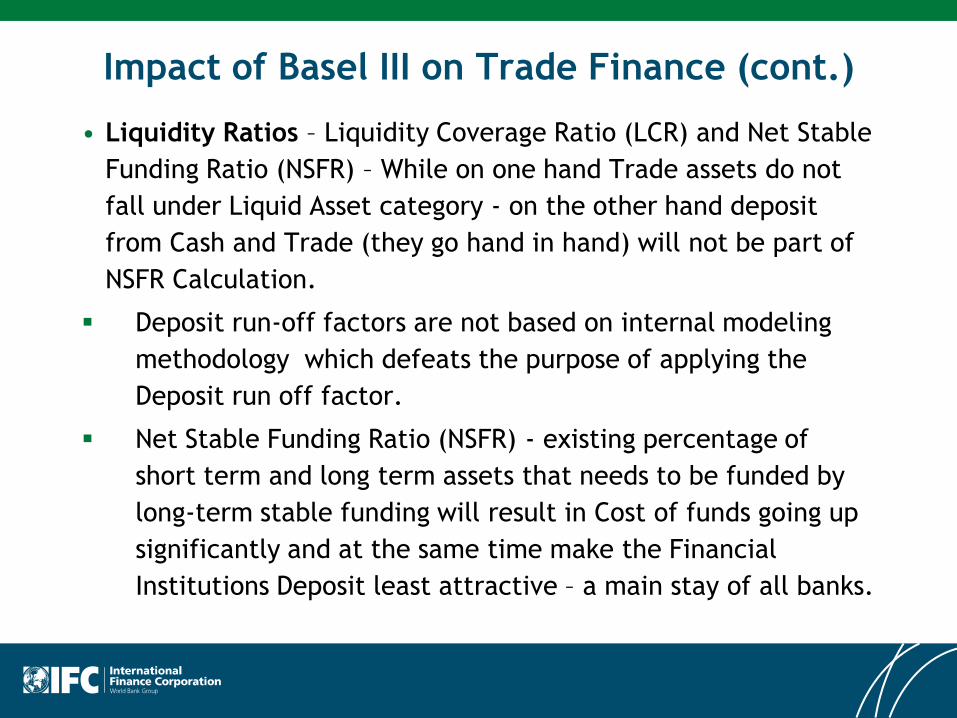

• Liquidity Ratios – Liquidity Coverage Ratio (LCR) and Net Stable

Funding Ratio (NSFR) – While on one hand Trade assets do not

fall under Liquid Asset category - on the other hand deposit

from Cash and Trade (they go hand in hand) will not be part of

NSFR Calculation.

Deposit run-off factors are not based on internal modeling

methodology which defeats the purpose of applying the

Deposit run off factor.

Net Stable Funding Ratio (NSFR) - existing percentage of

short term and long term assets that needs to be funded by

long-term stable funding will result in Cost of funds going up

significantly and at the same time make the Financial

Institutions Deposit least attractive – a main stay of all banks.

Impact of Basel III on Trade Finance (cont.)

Counterparty Credit Risk - Basel 3 has come up with a higher Asset

Value Correlation (AVC) for large financial institutions (FI) (US$100

billion worth of assets) and unregulated FI through an AVC multiplier of

1.25. Standardized AVC places all Bank to Bank Exposures at par.

Therefore trade finance will attract came capital as other riskier and

more correlated products such as syndicated loans and bonds.

1.25 AVC multiplier for Trade Finance should not be applied.

Impact of Basel III on Trade Finance (cont.)

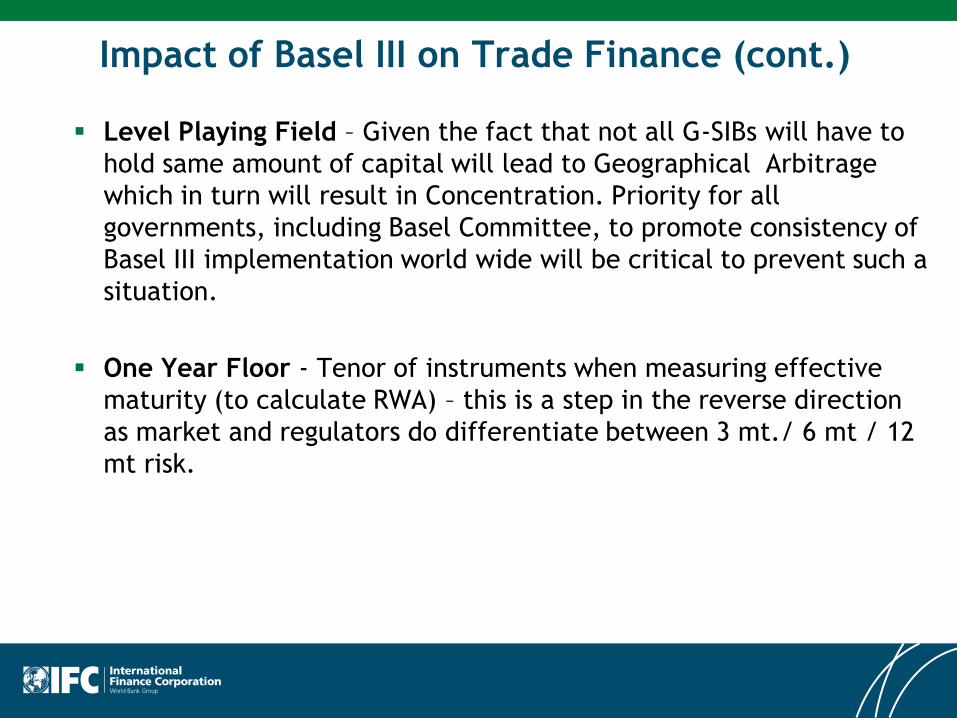

Level Playing Field – Given the fact that not all G-SIBs will have to

hold same amount of capital will lead to Geographical Arbitrage

which in turn will result in Concentration. Priority for all

governments, including Basel Committee, to promote consistency of

Basel III implementation world wide will be critical to prevent such a

situation.

One Year Floor - Tenor of instruments when measuring effective

maturity (to calculate RWA) – this is a step in the reverse direction

as market and regulators do differentiate between 3 mt./ 6 mt / 12

mt risk.

Conclusion

Bottom Line is that Trade Finance is a relatively low risk business.

The Short Term, Self Liquidating and Well Documented nature of

Trade Finance makes it inherently safer.

There is sufficient empirical data to establish the same.

Therefore Regulators need to look at Trade Finance with a

perspective that is fair and takes into account the inherent

nature of the business.

Also regulators need to try and keep the rules of the game

uniform or else it will lead to arbitrage.

Thank You