Barron’s Chapter 2. Discipline of Economics ► Absolute Advantage: The ability to produce...

21

Barron’s Chapter 2 Barron’s Chapter 2

-

Upload

eileen-hall -

Category

Documents

-

view

221 -

download

3

Transcript of Barron’s Chapter 2. Discipline of Economics ► Absolute Advantage: The ability to produce...

Barron’s Chapter 2Barron’s Chapter 2

Discipline of EconomicsDiscipline of Economics►Absolute Advantage: The ability to Absolute Advantage: The ability to

produce something more efficientlyproduce something more efficiently►Capital: Productive equipment or Capital: Productive equipment or

machinerymachinery►Comparative Advantage: The ability to Comparative Advantage: The ability to

produce something with a lower produce something with a lower opportunity costopportunity cost

►Economics: A social science that studies Economics: A social science that studies how resources are used and is often how resources are used and is often concerned with how resources can be concerned with how resources can be used to their fullest potentialused to their fullest potential

Discipline of EconomicsDiscipline of Economics►Efficiency: Using resources to their Efficiency: Using resources to their

maximum potentialmaximum potential►Labor: All human activity that is productiveLabor: All human activity that is productive►Land: All natural resourcesLand: All natural resources►Law of Increasing Costs: Law that states that Law of Increasing Costs: Law that states that

when more of a product is initially being when more of a product is initially being produced, the higher the opportunity cost produced, the higher the opportunity cost will be to produce still morewill be to produce still more

►Macroeconomics: Economic problems Macroeconomics: Economic problems encountered by the nation as a whole encountered by the nation as a whole

Discipline of EconomicsDiscipline of Economics► Microeconomics: Economic problems faced by Microeconomics: Economic problems faced by

individual units within the overall economyindividual units within the overall economy► Opportunity cost: The amount of one good that Opportunity cost: The amount of one good that

must be sacrificed to obtain an alternative goodmust be sacrificed to obtain an alternative good ΔΔY / Y / ΔΔXX

► Positive Economics: Economic analysis that Positive Economics: Economic analysis that draws conclusions based on logical deduction or draws conclusions based on logical deduction or induction. Value judgments are avoided.induction. Value judgments are avoided. Based on the scientific methodBased on the scientific method

► Production Possibilities Frontier: The Production Possibilities Frontier: The combinations of two goods that can be produced combinations of two goods that can be produced if the economy uses all of its resources fully and if the economy uses all of its resources fully and efficientlyefficiently

Discipline of EconomicsDiscipline of Economics►Normative Economics: Normative Economics:

Economics involving value Economics involving value judgmentsjudgmentsWhat What should should be done?be done?

►Resource: Anything that can Resource: Anything that can be used to produce a good or be used to produce a good or serviceservice

Discipline of EconomicsDiscipline of Economics

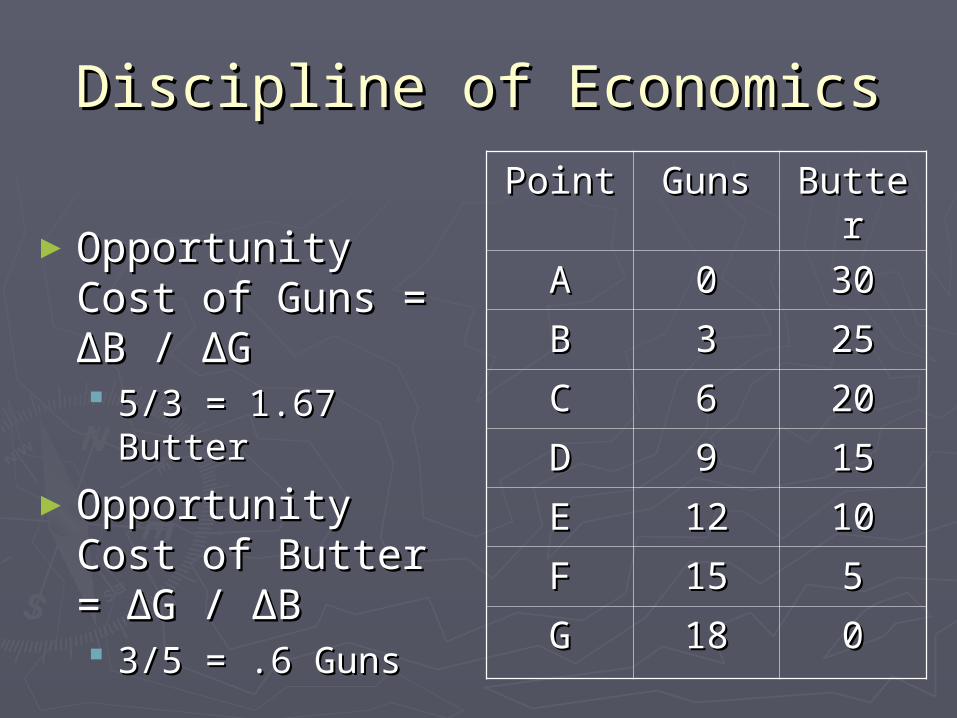

►Opportunity Cost Opportunity Cost of Guns = of Guns = ΔΔB / B / ΔΔGG 5/3 = 1.67 Butter5/3 = 1.67 Butter

►Opportunity Cost Opportunity Cost of Butter = of Butter = ΔΔG / G / ΔΔBB 3/5 = .6 Guns3/5 = .6 Guns

PointPoint GunsGuns ButterButter

AA 00 3030

BB 33 2525

CC 66 2020

DD 99 1515

EE 1212 1010

FF 1515 55

GG 1818 00

Discipline of EconomicsDiscipline of Economics

0

5

10

15

20

25

30

35

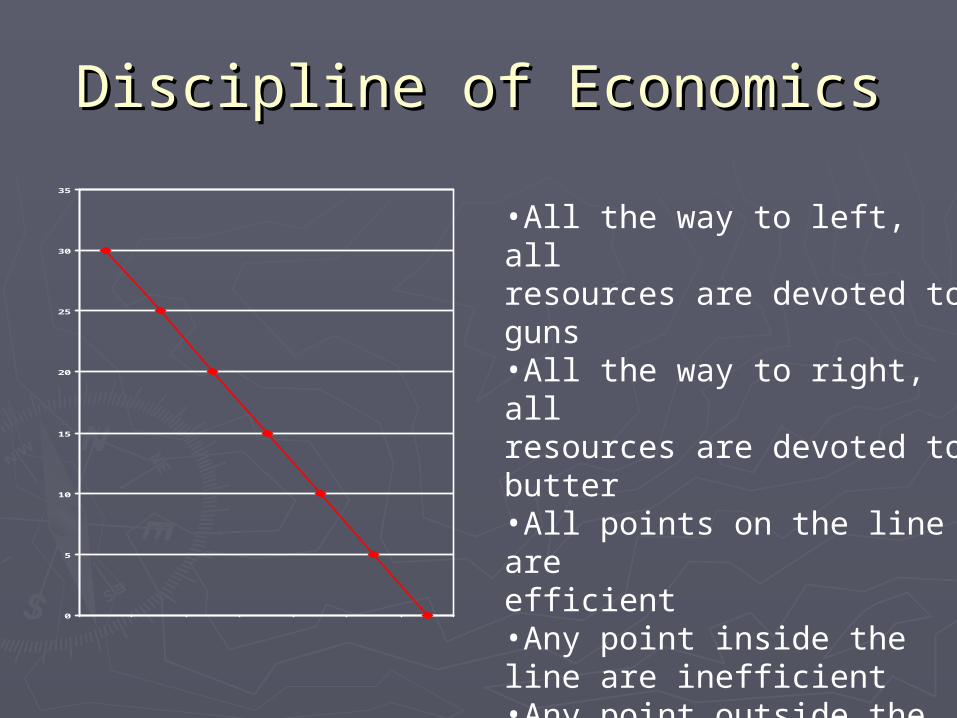

•All the way to left, all resources are devoted to guns•All the way to right, all resources are devoted to butter•All points on the line are efficient•Any point inside the line are inefficient•Any point outside the line are unattainable as of now

Discipline of EconomicsDiscipline of Economics►PPF CAN shift:PPF CAN shift:

Changes in the amount of Changes in the amount of resources in the economyresources in the economy

Changes in technology and Changes in technology and productivityproductivity►Increases in these shift the PPF Increases in these shift the PPF outout►Decreases in these shift the PPF inDecreases in these shift the PPF in

Discipline of EconomicsDiscipline of Economics►As more of a product is produced, the As more of a product is produced, the

opportunity cost increasesopportunity cost increases►The more guns we produce, the more The more guns we produce, the more

expensive it will be to produce one more expensive it will be to produce one more gun (in terms of butter)gun (in terms of butter)

►The opportunity cost of producing a good The opportunity cost of producing a good becomes greater as more resources are becomes greater as more resources are forced into industries where they are not forced into industries where they are not as productive. Causes the PPF to be as productive. Causes the PPF to be CONCAVE to the origin (bowed out).CONCAVE to the origin (bowed out).

Discipline of EconomicsDiscipline of Economics

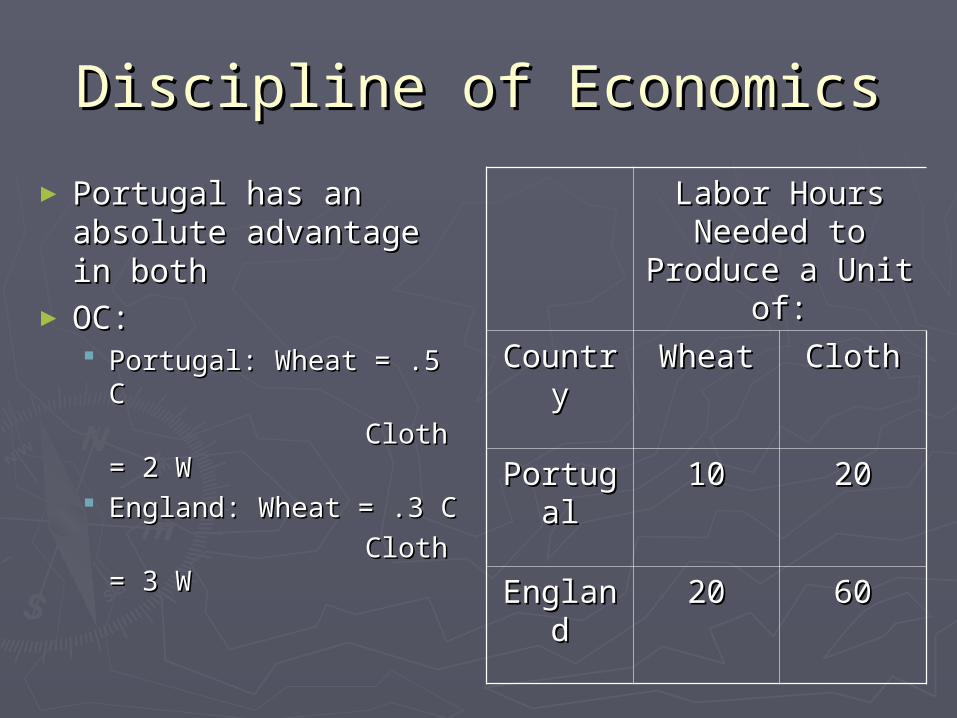

► Portugal has an Portugal has an absolute advantage absolute advantage in bothin both

►OC:OC: Portugal: Wheat = .5 Portugal: Wheat = .5

CC

Cloth = 2 WCloth = 2 W England: Wheat = .3 England: Wheat = .3

CC

Cloth = 3 WCloth = 3 W

Labor Hours Labor Hours Needed to Needed to

Produce a Unit Produce a Unit of:of:

CountryCountry WheatWheat ClothCloth

PortugaPortugall

1010 2020

EnglanEnglandd

2020 6060

Economic SystemsEconomic Systems►Allocative Efficiency: Term for resources Allocative Efficiency: Term for resources

being deployed to produce just the right being deployed to produce just the right amount of each product to satisfy society’s amount of each product to satisfy society’s wantswants

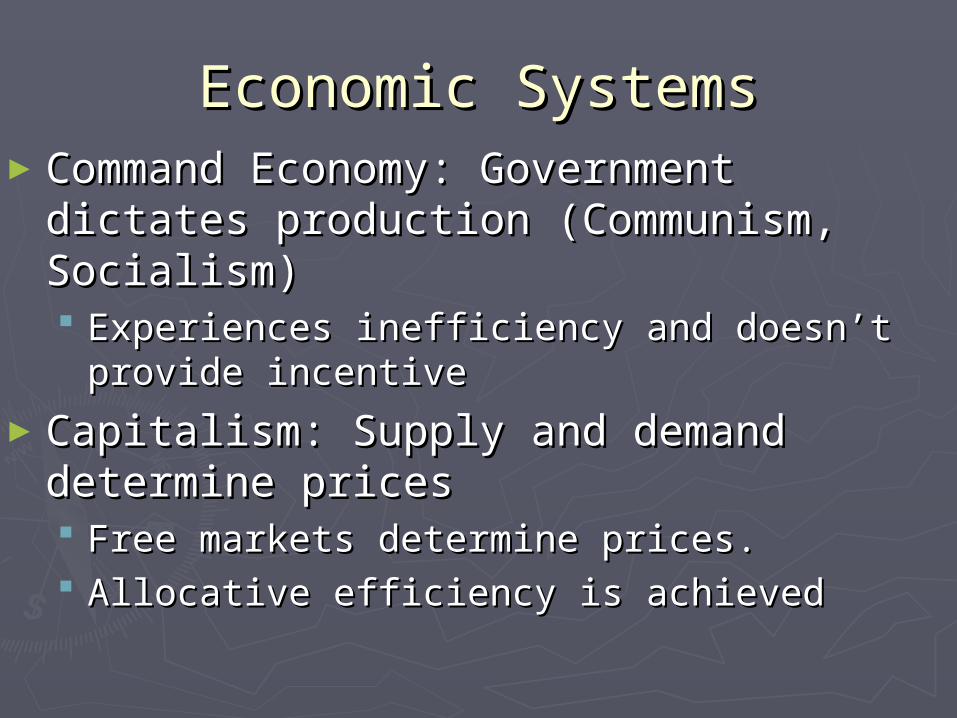

►Capitalism: An economic system where Capitalism: An economic system where supply and demand determine pricessupply and demand determine prices

►Circular Flow Diagram: Diagram that shows Circular Flow Diagram: Diagram that shows how households and firms are related y the how households and firms are related y the exchange of resources and productsexchange of resources and products

►Command Economy: Economy in which the Command Economy: Economy in which the central government dictates what will or central government dictates what will or will not be produced and who gets whatwill not be produced and who gets what

Economic SystemsEconomic Systems►The Law of Demand: Law that states that The Law of Demand: Law that states that

when the price of a product increases, when the price of a product increases, the quantity demanded decreasesthe quantity demanded decreases

►The Law of Supply: Law that states that The Law of Supply: Law that states that when the price of a product increases, when the price of a product increases, the quantity supplied increasesthe quantity supplied increases

►Mixed Economy: A blend of government Mixed Economy: A blend of government commands and capitalismcommands and capitalism

Economic SystemsEconomic Systems►Command Economy: Government Command Economy: Government

dictates production (Communism, dictates production (Communism, Socialism)Socialism) Experiences inefficiency and doesn’t provide Experiences inefficiency and doesn’t provide

incentiveincentive

►Capitalism: Supply and demand Capitalism: Supply and demand determine pricesdetermine prices Free markets determine prices. Free markets determine prices. Allocative efficiency is achievedAllocative efficiency is achieved

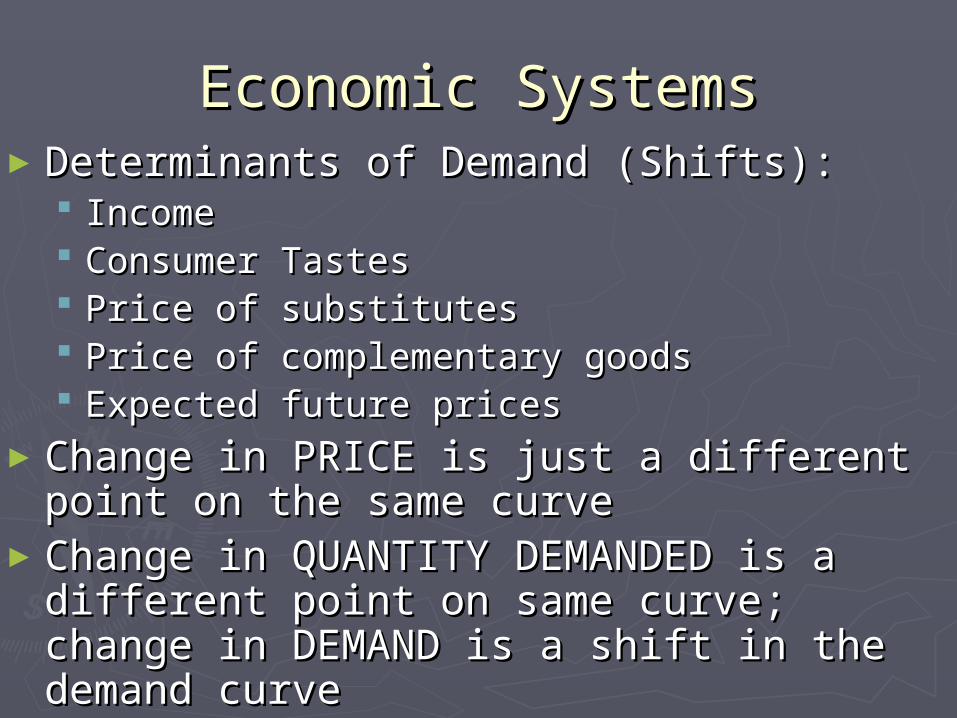

Economic SystemsEconomic Systems►Determinants of Demand (Shifts):Determinants of Demand (Shifts):

IncomeIncome Consumer TastesConsumer Tastes Price of substitutesPrice of substitutes Price of complementary goodsPrice of complementary goods Expected future pricesExpected future prices

►Change in PRICE is just a different point Change in PRICE is just a different point on the same curveon the same curve

►Change in QUANTITY DEMANDED is a Change in QUANTITY DEMANDED is a different point on same curve; change in different point on same curve; change in DEMAND is a shift in the demand curveDEMAND is a shift in the demand curve

Economic SystemsEconomic Systems►Determinants of Supply (Shifts):Determinants of Supply (Shifts):

Price of inputsPrice of inputs Technology and productivityTechnology and productivity Expected future priceExpected future price

►Change in price is a different point on the Change in price is a different point on the same curve (QUANTITY SUPPLIED)same curve (QUANTITY SUPPLIED)

►Shift refers to a change in SUPPLYShift refers to a change in SUPPLY

Demand and SupplyDemand and Supply►Market: Place where buyers and sellers Market: Place where buyers and sellers

meet to exchange goods and servicesmeet to exchange goods and services►Quantity Demanded: Has an inverse Quantity Demanded: Has an inverse

relationship with changes in the price of a relationship with changes in the price of a particular goodparticular good

►Quantity Supplied: Has a direct Quantity Supplied: Has a direct relationship with changes in the price of a relationship with changes in the price of a particular goodparticular good

►Change in Demand (Supply): Shift in Change in Demand (Supply): Shift in demand (supply) due to non-price factors demand (supply) due to non-price factors or determinantsor determinants

Demand and SupplyDemand and Supply►Equilibrium Price: Price at which quantity Equilibrium Price: Price at which quantity

supplied equals quantity demandedsupplied equals quantity demanded►Price Ceiling: Established below the Price Ceiling: Established below the

equilibrium priceequilibrium price►Price Floor: Established above the Price Floor: Established above the

equilibrium priceequilibrium price

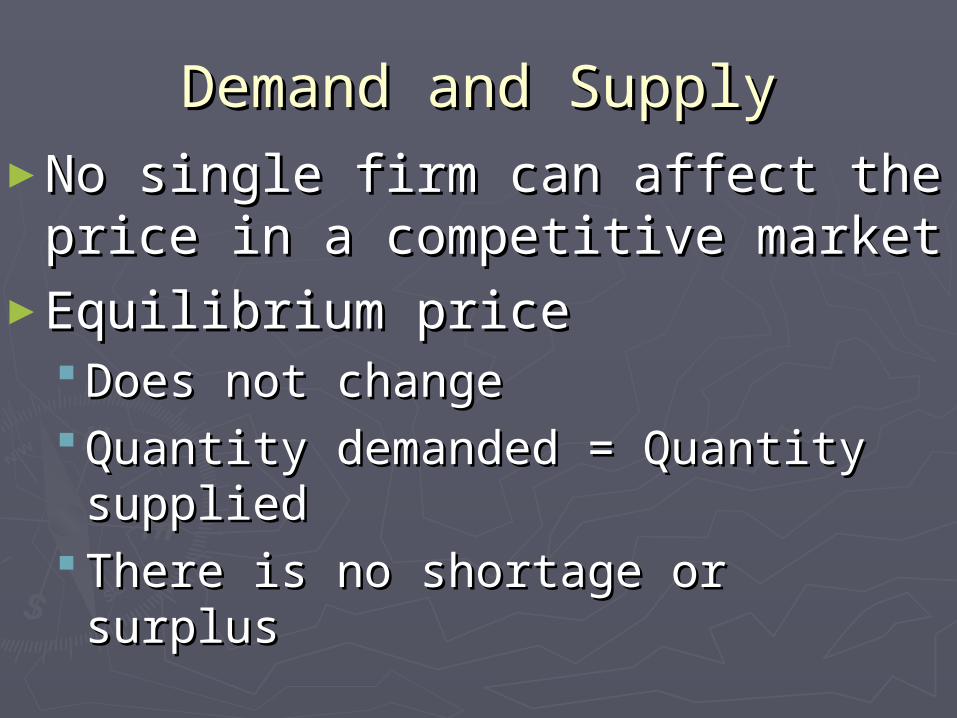

Demand and SupplyDemand and Supply►No single firm can affect the No single firm can affect the

price in a competitive marketprice in a competitive market►Equilibrium priceEquilibrium price

Does not changeDoes not change Quantity demanded = Quantity Quantity demanded = Quantity

suppliedsupplied There is no shortage or surplusThere is no shortage or surplus

Demand and SupplyDemand and Supply►Determinants of DemandDeterminants of Demand

Number of consumersNumber of consumers Tastes and preferences of Tastes and preferences of

consumersconsumers Prices of substitutes and Prices of substitutes and

complementscomplements Consumers’ incomeConsumers’ income Price expectationsPrice expectations

Demand and SupplyDemand and Supply►Determinants of SupplyDeterminants of Supply

Number of sellersNumber of sellers Costs of resources or productionCosts of resources or production Price of substitute goodsPrice of substitute goods Price expectationsPrice expectations TechnologyTechnology Taxes/subsidiesTaxes/subsidies

Demand and SupplyDemand and Supply►Price floor is always Price floor is always

established above the established above the equilibrium price. Always equilibrium price. Always causes a surplus.causes a surplus.

►Price ceiling is always Price ceiling is always established below the established below the equilibrium price. Always equilibrium price. Always causes a shortage.causes a shortage.