Emmanuel Stamatakis 1 , Moushumi Chaudhury 1 1 Department of Epidemiology and Public Health, UCL

2013

KCE REPORT 199CS

BARRIERS AND OPPORTUBIOSIMILAR MEDICINESSYNTHESIS

BARRIERS AND OPPORTUNITIES FOR THE UPTAKBIOSIMILAR MEDICINES IN BELGIUM - SYNTHESIS

www.kce.fgov.be

NITIES FOR THE UPTAKE OFSYNTHESIS

Belgian Health Care Knowledge Centre

The Belgian Health Care Knowledge Centre (KCE) is an organization of public interest, created on the 242002 under the supervision of the Minister of Public Health and Social Affairs. KCE is in charge ofthat support the political decision making on health care and health insurance.

Executive BoardPresident

CEO - National Institute for Health and Disability Insurance (vicepresident)President of the Federal Public Service Health, Food Chain Safety andEnvironment (vice president)President of the Federal Public Service Social Security (vice president)

General Administrator of the Federal Agency for Medicines and HealthProductsRepresentatives of the Minister of Public Health

Representatives of the Minister of Social Affairs

Representatives of the Council of Ministers

Intermutualistic Agency

Professional Organisations

Professional Organisations

Hospital Federations

Social Partners

House of Representatives

Belgian Health Care Knowledge Centre

The Belgian Health Care Knowledge Centre (KCE) is an organization of public interest, created on the 242002 under the supervision of the Minister of Public Health and Social Affairs. KCE is in charge ofthat support the political decision making on health care and health insurance.

Actual Members

Pierre GilletNational Institute for Health and Disability Insurance (vice Jo De Cock

President of the Federal Public Service Health, Food Chain Safety andEnvironment (vice president)

Dirk Cuypers

President of the Federal Public Service Social Security (vice president) Frank Van Massenhove

General Administrator of the Federal Agency for Medicines and Health Xavier De Cuyper

Representatives of the Minister of Public Health Bernard Lange

Bernard Vercruysse

Representatives of the Minister of Social Affairs Lambert Stamatakis

Ri De Ridder

Representatives of the Council of Ministers Jean-Noël Godin

Daniël Devos

Intermutualistic Agency Michiel Callens

Patrick Verertbruggen

Xavier Brenez

Professional Organisations - representatives of physicians Marc MoensJean-Pierre Baeyens

Professional Organisations - representatives of nurses Michel FoulonMyriam Hubinon

Hospital Federations Johan Pauwels

Jean-Claude Praet

Rita Thys

Paul Palsterman

House of Representatives Lieve Wierinck

The Belgian Health Care Knowledge Centre (KCE) is an organization of public interest, created on the 24th

of December2002 under the supervision of the Minister of Public Health and Social Affairs. KCE is in charge of conducting studies

Members Substitute Members

Pierre GilletJo De Cock Benoît Collin

Dirk Cuypers Christiaan Decoster

Van Massenhove Jan Bertels

Xavier De Cuyper Greet Musch

Bernard Lange Brieuc Van Damme

Bernard Vercruysse Annick Poncé

Lambert Stamatakis Vinciane Quoidbach

Ri De Ridder Koen Vandewoude

Noël Godin Philippe Henry deGeneret

l Devos Wilfried Den Tandt

Michiel Callens Frank De Smet

Patrick Verertbruggen Yolande Husden

Xavier Brenez Geert Messiaen

Marc Moens Roland LemyePierre Baeyens Rita Cuypers

Michel Foulon Ludo MeyersMyriam Hubinon Olivier ThononJohan Pauwels Katrien Kesteloot

Claude Praet Pierre Smiets

Leo Neels

Paul Palsterman Celien Van Moerkerke

Lieve Wierinck

Control Government commissioner

Management Chief Executive OfficerAssistant Chief Executive Officer

Manager Program Management

Contact Belgian Health Care Knowledge Centre

Doorbuilding (10Boulevard du Jardin Botanique, 55B-1000 BrusselsBelgium

T +32 [0]2 287 33 88

F +32 [0]2 287 33 85

http://www.kce.fgov.be

Government commissioner Yves Roger

Chief Executive OfficerAssistant Chief Executive Officer

Raf MertensChristian Léonard

Manager Program Management Kristel De Gauquier

Belgian Health Care Knowledge Centre (KCE)

Doorbuilding (10th

Floor)Boulevard du Jardin Botanique, 55

1000 BrusselsBelgium

T +32 [0]2 287 33 88

F +32 [0]2 287 33 85

http://www.kce.fgov.be

Kristel De Gauquier

2013

KCE REPORT 199CSHEALTH SERVICES RESEARCH

BARRIERS AND OPPORTUBIOSIMILAR MEDICINESSYNTHESIS

ISABELLE LEPAGE-NEFKENS, SOPHIE GERKENS, IMGARD VINC

BARRIERS AND OPPORTUNITIES FOR THE UPTAKBIOSIMILAR MEDICINES IN BELGIUM - SYNTHESIS

GERKENS, IMGARD VINCK, JULIEN PIÉRART, FRANK HULSTAERT, MARIA

www.kce.fgov.be

NITIES FOR THE UPTAKE OFSYNTHESIS

STAERT, MARIA-ISABEL FARFAN-PORTET

COLOPHON

Title: Barriers and opportunities for the uptake of biosimilar medIcines in Belgium

Authors: Isabelle LepagePortet

Reviewers: Carine Van de Voorde

External experts: Bruno Flamion (Université d

Acknowledgements: Claudia Barth (Kuratorium für Dialyse und Nierentransplantation)läkemedelsförmånsverket (TLV))(Erasmus Medical Centre, Rotterdam)sent the link to the web survey:BelgiqueGrève (Belgian Society of Medical Oncology (BSMO)), Sylvie Tenoutasse (Belgian Study Group for PediatricEndocrinology (BSGPE)),GNFB), Yves Beguin (Hematological SocietyNefrologie (NBVN)), Thomas De Rijdt (Vlaamse vereniging van ziekenhuisapotwho participated in the face

External validators: Francis Colardyn (UZ Gent), Jaime Espin (EASP

Stakeholders: JeanGheuens (NBVN), Julie GusmanHoebus (Amgen), Michel Jadoul (GNFB), Philipe Jorens (RUZB), Myriam Nechelput (Roche(Pharma.be), Dominique Petit (Sandoz),Assche (Febelgen), Robert Vander Stichele (BCFI), Chris Van Hul (OZ), Luc Van Oevelen (Janssen), DirkVerschueren (Hospira),

Other reported interests: Membership of a stakeholder group on which the results of t(Febelgen vzw,

Owner of subscribed capital, options, shares or other financial instruments:actionby Pfizer)

Fees or other compensation for wri(employee by

A grant, fees or funds for a member of staff or another form of compensation for the execution of research:Van Assche

Barriers and opportunities for the uptake of biosimilar medIcines in Belgium

Isabelle Lepage-Nefkens, Sophie Gerkens, Imgard Vinck, Julien Piérart, Frank Hulstaert, MaríaPortet

Carine Van de Voorde, Germaine Hanquet, Christian Léonard, Raf Mertens

Bruno Flamion (Université de Namur), Serge Van Praet (CHU Saint-Pierre),

Claudia Barth (Kuratorium für Dialyse und Nierentransplantation)läkemedelsförmånsverket (TLV)), Irene Kraemer (Johannes Gutenberg(Erasmus Medical Centre, Rotterdam), Roland Windt (Universität Bremen)sent the link to the web survey: Dominique Wouters (Association Francophone desBelgique (AFPHB)), Luc De Clercq (Belgian Royal Society for Rheumatology (KBVRGrève (Belgian Society of Medical Oncology (BSMO)), Sylvie Tenoutasse (Belgian Study Group for PediatricEndocrinology (BSGPE)), Jean-Michel Pochet (Groupement des néphrologues francophones de BelgiqueGNFB), Yves Beguin (Hematological Society - BHS), Bart De Moor (Nederlandstalige Belgische Vereniging voorNefrologie (NBVN)), Thomas De Rijdt (Vlaamse vereniging van ziekenhuisapotwho participated in the face-to face interviews and in the websurvey.

Francis Colardyn (UZ Gent), Jaime Espin (EASP- Spain), Steven Simoens (KU Leuven)

Jean Bury (Santhea), Rudy De Cock (Pfizer), Karen De Smet (FAGG –Gheuens (NBVN), Julie Gusman (Merck), Anne Hendrickx (Cabinet du Ministre Laurette Onkelinx), MarleenHoebus (Amgen), Michel Jadoul (GNFB), Philipe Jorens (RUZB), Myriam Nechelput (Roche(Pharma.be), Dominique Petit (Sandoz), François Sumkay (ANMC), SylvieAssche (Febelgen), Robert Vander Stichele (BCFI), Chris Van Hul (OZ), Luc Van Oevelen (Janssen), DirkVerschueren (Hospira),

Membership of a stakeholder group on which the results of this report could have an impact(Febelgen vzw, representative of biosimilars in the Belgian market. Memb

Owner of subscribed capital, options, shares or other financial instruments:action from J&J – Janssen Pharmaceutica), Luc Van Oevelen (employee

Pfizer)

Fees or other compensation for writing a publication or participating in its development:employee by Pfizer)

A grant, fees or funds for a member of staff or another form of compensation for the execution of research:Van Assche (Febelgen vzw, representative of biosimilars in the Belgian market

Barriers and opportunities for the uptake of biosimilar medIcines in Belgium - Synthesis

Nefkens, Sophie Gerkens, Imgard Vinck, Julien Piérart, Frank Hulstaert, María-Isabel Farfan-

onard, Raf Mertens

Pierre), Luc Hutsebaut (LCM)

Claudia Barth (Kuratorium für Dialyse und Nierentransplantation) , Gustaf Befrits (Tandvårds- ochIrene Kraemer (Johannes Gutenberg–Universität Mainz), Arnold Vulto

Roland Windt (Universität Bremen), To the scientific associations thatDominique Wouters (Association Francophone des Pharmaciens Hospitaliers de

Luc De Clercq (Belgian Royal Society for Rheumatology (KBVR – SRBR)), Jacques DeGrève (Belgian Society of Medical Oncology (BSMO)), Sylvie Tenoutasse (Belgian Study Group for Pediatric

Michel Pochet (Groupement des néphrologues francophones de Belgique -BHS), Bart De Moor (Nederlandstalige Belgische Vereniging voor

Nefrologie (NBVN)), Thomas De Rijdt (Vlaamse vereniging van ziekenhuisapothekers (VZA)), and to all persons

), Steven Simoens (KU Leuven)

– AFMPS), Patrick Durez (SRBR), Eric(Merck), Anne Hendrickx (Cabinet du Ministre Laurette Onkelinx), Marleen

Hoebus (Amgen), Michel Jadoul (GNFB), Philipe Jorens (RUZB), Myriam Nechelput (Roche ), Leo NeelsMC), Sylvie Tenoutasse (BSGPE), Joris Van

Assche (Febelgen), Robert Vander Stichele (BCFI), Chris Van Hul (OZ), Luc Van Oevelen (Janssen), Dirk

his report could have an impact: Joris Van AsscheMembers: Sandoz, Teva en Hospira),

Owner of subscribed capital, options, shares or other financial instruments: Eric Gheuens (NBVN) (owner ofby Janssen), Rudy De Cock (employee

ting a publication or participating in its development: Rudy De Cock

A grant, fees or funds for a member of staff or another form of compensation for the execution of research: Jorisbiosimilars in the Belgian market. Members: Sandoz, Teva en

Hospira), Rudy De Cock (pharmaceutical firms: Amgen, Janssen)

Consultancy or employment for a company, an association or andue to the results of this report:marketJulie Gusman (MerckNechelput (biopharmaceuticals

Payments to speak, training remunGheuens (NBVNBMS, Roche, Abbott, MSD, UCB, Pfizer), Michel Jadoul (GNFB)

Presidency oresults of this report could have an impact:Belgian market

Any other direct or indirect relationship with a producer, distributor or healthcare institution that could beinterpreted as a conflict of interests:companies), Rudy De Cock (employeepharmaceuticals), Myriam Nechelput (of originator biohospital)

Layout: Ine Verhulst, Sophie Vaes

Disclaimer: The external experts were consulted about a (preliminary) version of the scientific report. Theircomments were discussed during meetings. They did not conecessarily agree with its content.

Subsequently, a (final) version was submitted to the validators. The validation of the report results froma consensus or a voting process between the validators. The validators did not coreport and did not necessarily all three agree with its content.

Finally, this report has been approved

Only the KCE is responsible for errors or omissions that could persist. The policy recoalso under the full responsibility of the KCE.

Publication date: 28 March 2013

Hospira), Rudy De Cock (employee by Pfizer), Michel Jadoul (GNFBpharmaceutical firms: Amgen, Janssen)

Consultancy or employment for a company, an association or an organisation that may gain or lose financiallydue to the results of this report: Joris Van Assche (Febelgen vzw, representative of biosimilars in the Belgianmarket. Members: Sandoz, Teva en Hospira), Luc Van Oevelen (Janssen), Rudy De Cock (employee byJulie Gusman (Merck – company of originator pharmaceuticals), Michel Jadoul (GNFBNechelput (employee by Roche), Marleen Hoebus (employee by

pharmaceuticals)

Payments to speak, training remuneration, subsidised travel or payment for participation at a conference:Gheuens (NBVN – participation in medical conferences: Janssen, Roche), Patrick Durez (SRBRBMS, Roche, Abbott, MSD, UCB, Pfizer), Michel Jadoul (GNFB)

Presidency or accountable function within an institution, association, department or other entity on which theresults of this report could have an impact: Joris Van Assche (Febelgen vzw,Belgian market. Members: Sandoz, Teva en Hospira)

Any other direct or indirect relationship with a producer, distributor or healthcare institution that could beinterpreted as a conflict of interests: Leo Neels (Pharma.be, association of pharmaceutical originatorcompanies), Rudy De Cock (employee by Pfizer), Julie Gusman (Merckpharmaceuticals), Myriam Nechelput (employee by Roche), Marleen Hoebus (of originator biopharmaceuticals), Serge Van Praet (CHU Saint-Pierrehospital)

Ine Verhulst, Sophie Vaes

The external experts were consulted about a (preliminary) version of the scientific report. Theircomments were discussed during meetings. They did not co-author thenecessarily agree with its content.

Subsequently, a (final) version was submitted to the validators. The validation of the report results froma consensus or a voting process between the validators. The validators did not coreport and did not necessarily all three agree with its content.

Finally, this report has been approved by common assent by the Executive Board.

Only the KCE is responsible for errors or omissions that could persist. The policy recoalso under the full responsibility of the KCE.

28 March 2013

Michel Jadoul (GNFB – research funds from different

organisation that may gain or lose financiallyrepresentative of biosimilars in the Belgian

Members: Sandoz, Teva en Hospira), Luc Van Oevelen (Janssen), Rudy De Cock (employee by Pfizer),originator pharmaceuticals), Michel Jadoul (GNFB – consultant), Myriam

employee by Amgen – company of originator

eration, subsidised travel or payment for participation at a conference: Eric: Janssen, Roche), Patrick Durez (SRBR – speaker fee:

r accountable function within an institution, association, department or other entity on which the(Febelgen vzw, representative of biosimilars in the

Any other direct or indirect relationship with a producer, distributor or healthcare institution that could beLeo Neels (Pharma.be, association of pharmaceutical originator

Julie Gusman (Merck – company of originatorRoche), Marleen Hoebus (employee by Amgen – company

Pierre – negotiation of pharmaceuticals in a

The external experts were consulted about a (preliminary) version of the scientific report. Theirauthor the scientific report and did not

Subsequently, a (final) version was submitted to the validators. The validation of the report results froma consensus or a voting process between the validators. The validators did not co -author the scientific

by the Executive Board.

Only the KCE is responsible for errors or omissions that could persist. The policy reco mmendations are

Domain: Health Services Research (HSR)

MeSH: Biosimilar Pharmaceuticals

NLM Classification: QV241

Language: English

Format: Adobe® PDF™ (A4)

Legal depot: D/2013/10.273/

Copyright: KCE reports are published under a “by/nc/nd” Creative Commons Licencehttp://kce.fgov.be/content/about

How to refer to this document? Lepageuptake of biosimilar medIcines in BelgiumHealth Care Knowledge Centre (KCE). 2013. KCE Reports

This document is available on

Health Services Research (HSR)

Biosimilar Pharmaceuticals; Reimbursement Mechanisms; Cost Savings;

QV241

English

Adobe® PDF™ (A4)

D/2013/10.273/14

KCE reports are published under a “by/nc/nd” Creative Commons Licencehttp://kce.fgov.be/content/about-copyrights-for-kce-reports.

Lepage-Nefkens I, Gerkens S, Vinck I, Piérart J, Hulstaert F, Farfán-Portet Muptake of biosimilar medIcines in Belgium - Synthesis. Health Services Research (HSR)Health Care Knowledge Centre (KCE). 2013. KCE Reports 199Cs. D/2013/10.273/1

This document is available on the website of the Belgian Health Care Knowledge Centre.

Economics, Hospital

KCE reports are published under a “by/nc/nd” Creative Commons Licence

Portet M-I Barriers and opportunities for theHealth Services Research (HSR) Brussels: Belgian

. D/2013/10.273/13.

the website of the Belgian Health Care Knowledge Centre.

KCE Report 199Cs

FOREWORD Why the need for a KCE study on biosimilar medicines? Are they not simply the generics of biological medicines?Copies of hormones, growth factors or other molecules of biological origin that have lost their patent? Well no, thingsare not that simple. Cla

Firstly, it was a matter of checking whether biosimilars can be regarded as equivalent to generic medicines. Alreadyhere, appearancesmolecules, consisting in particular of chains of dozens if not hundreds of amino acids, possessing intrinsically a degreeof variation in their structure. This variability is also chadifferent to the original medicine. As a result, promoters of biosimilars probably encounter as many if not moredifficulties in gaining acceptance for their equivalence andmedicines.

Secondly, as these products are mainly for hospital use, they face the same obstacles as generics encountered inpenetrating this market. It is difficult to generalise, however, as each molecule has its oissues.

Finally, the market for biosimilars and generics is evolving rapidly and possesses great growth potentialyears.

Enough reasons for analysingsavings thatresearchers and we would like to thank them very warmly for this. Their contribution was essential in clearing up someof the mysteries that seemed to surround this complex and fascinating field.

Christian Léonard

Assistant Chief Executive Officer

Biosimilar medicines

Why the need for a KCE study on biosimilar medicines? Are they not simply the generics of biological medicines?Copies of hormones, growth factors or other molecules of biological origin that have lost their patent? Well no, thingsare not that simple. Clarifying this issue was one of the minister’s aims when commissioning this study

Firstly, it was a matter of checking whether biosimilars can be regarded as equivalent to generic medicines. Alreadyhere, appearances – or perhaps one should say similarities – are misleading. Biological medicines are in fact complexmolecules, consisting in particular of chains of dozens if not hundreds of amino acids, possessing intrinsically a degreeof variation in their structure. This variability is also characteristic of their “copies”. Biosimilars can therefore be slightlydifferent to the original medicine. As a result, promoters of biosimilars probably encounter as many if not moredifficulties in gaining acceptance for their equivalence and to gain market sharesmedicines.

, as these products are mainly for hospital use, they face the same obstacles as generics encountered inpenetrating this market. It is difficult to generalise, however, as each molecule has its o

, the market for biosimilars and generics is evolving rapidly and possesses great growth potential

Enough reasons for analysing the obstacles that have to date prevented biosimilars frsavings that have been expected. Many people generously shared their knowledge and expertise with our team ofresearchers and we would like to thank them very warmly for this. Their contribution was essential in clearing up someof the mysteries that seemed to surround this complex and fascinating field.

éonard

Chief Executive Officer

1

Why the need for a KCE study on biosimilar medicines? Are they not simply the generics of biological medicines?Copies of hormones, growth factors or other molecules of biological origin that have lost their patent? Well no, things

rifying this issue was one of the minister’s aims when commissioning this study to the KCE.

Firstly, it was a matter of checking whether biosimilars can be regarded as equivalent to generic medicines. Alreadyare misleading. Biological medicines are in fact complex

molecules, consisting in particular of chains of dozens if not hundreds of amino acids, possessing intrinsically a degreeracteristic of their “copies”. Biosimilars can therefore be slightly

different to the original medicine. As a result, promoters of biosimilars probably encounter as many if not moreshares than was the case for generic

, as these products are mainly for hospital use, they face the same obstacles as generics encountered inpenetrating this market. It is difficult to generalise, however, as each molecule has its own particularities and specific

, the market for biosimilars and generics is evolving rapidly and possesses great growth potential in the coming

the obstacles that have to date prevented biosimilars from generating the budgetaryhave been expected. Many people generously shared their knowledge and expertise with our team of

researchers and we would like to thank them very warmly for this. Their contribution was essential in clearing up some

Raf Mertens

Chief Executive Officer

2

ABSTRACT

Biosimilar medicines

Context

Biologicals are produced using “living organismtreatment of chronic and life-threatening diseases such as cancer, multiplesclerosis and rheumatoid arthritis. Treatment with biologicals is usuallyexpensive and represents ever-increasing pharmaceutical expenditures forthe National Institute for Health and DisabilThe apparition of first biosimilars, i.e.opportunity to improve access to needed treatments at a lower cost for thethird-party payer. Biosimilars are currently available in three productclasses: Erythropoiesis-stimulating agents (epoetins), granulocytestimulating factors (filgrastim) and growth hormones (somatropin).

Uptake of biosimilars varies among countriesEuropean countries, the clinical use of biosimilarsin Belgium and until today have not lead toexpiry of several blockbuster biologicalsnecrosis factor alfa inhibitors).

Objectives and methods

This report includes a description of biosimilar uptake, price reduction andrelated savings for the third-party payer in Europe as well as a closer lookat measures influencing biosimilar uptake in France, The Netherlands,Germany and Sweden.

For Belgium, a field screening was done based on semito-face interviews with stakeholders involved in the use of current andfuture biosimilars (pharmaceutical companies, specialists, hospitalpharmacists and concerned national authorities). Results and opinionswere cross verified in a websurveypharmacists.

International experience

Biosimilar uptake and price reduction vary among countries as well asamong product classes. However, lpotential saving related to biosimilar uptake was available. Policymeasures have been implemented in different countries to stimulatebiosimilar uptake, but it still too early to assess their overall impact.Moreover, countries with no specific policies for bio

KCE Report 199Cs

living organism”. They are used for thethreatening diseases such as cancer, multiple

sclerosis and rheumatoid arthritis. Treatment with biologicals is usuallyincreasing pharmaceutical expenditures for

National Institute for Health and Disability Insurance (RIZIV – INAMI).first biosimilars, i.e. biological “copies”, is seen as an

opportunity to improve access to needed treatments at a lower cost for theparty payer. Biosimilars are currently available in three product

stimulating agents (epoetins), granulocyte-colonystimulating factors (filgrastim) and growth hormones (somatropin).

among countries. Compared to otherEuropean countries, the clinical use of biosimilars has been particularly low

have not lead to substantial savings. The patentexpiry of several blockbuster biologicals is imminent (especially the tumor

a description of biosimilar uptake, price reduction andparty payer in Europe as well as a closer look

at measures influencing biosimilar uptake in France, The Netherlands,

as done based on semi-structured, face-face interviews with stakeholders involved in the use of current and

future biosimilars (pharmaceutical companies, specialists, hospitalnational authorities). Results and opinions

cross verified in a websurvey among specialists and chief hospital

iosimilar uptake and price reduction vary among countries as well asHowever, little reliable information on current and

ial saving related to biosimilar uptake was available. Policymeasures have been implemented in different countries to stimulatebiosimilar uptake, but it still too early to assess their overall impact.Moreover, countries with no specific policies for biosimilars (such as

KCE Report 199Cs

Sweden) have attained a large uptake. Consequently, biosimilar uptakeseems to be related to the larger nationalpharmaceutical use: acceptability of less expensive alternatives,procurement policies for pharmaceuticals as well as general pricing andreimbursement policies.

Belgian experience

Different barriers that may hamper biosimilar uptake were identified forBelgium.

First, despite 20% to 34% price reduction compared to the list price of thereference product, biosimilars are not necessarily the least expensivealternative for the hospital. Indeed, direct negotiations between purchasersand providers may result in prices for reference products at substantiallylower level. In addition to these discounts, clinical recontinuing education of hospital pharmacists and physicians are alsofinanced by the producers of reference products.

Second, the lack of knowledge or the distrust of biosimilars amongspecialists, and to a lesser extent among hospital pharmacists is also a

Biosimilar medicines

Sweden) have attained a large uptake. Consequently, biosimilar uptakenational context regarding

pharmaceutical use: acceptability of less expensive alternatives,as well as general pricing and

Different barriers that may hamper biosimilar uptake were identified for

First, despite 20% to 34% price reduction compared to the list price of theimilars are not necessarily the least expensive

the hospital. Indeed, direct negotiations between purchasersand providers may result in prices for reference products at substantially

discounts, clinical research in hospitals andcontinuing education of hospital pharmacists and physicians are also

Second, the lack of knowledge or the distrust of biosimilars amongital pharmacists is also a

barrier for use of biosimilars. There is a gap between the expectationssurrounding current clinical data and the accessibility“sufficient” clinical data. Lack of confidenceservices provided by biosimilar companies (information) may also limit the use of biosimilars. In addition, lack of clearinformation on the use of biosimilars, originators and even on secondgeneration biological products for specifprescriber to stick to the product they are used to.

A broader problem

Low uptake of biosimilars in Belgium reflects thepharmaceutical use in hospital settingstransparency of costs, discounts and other advantagesgains constitute perfectly legal earningsmeaningful ways within the hospital, it disturbs competition and may makeit nearly impossible for the authoritiescost-containment policies.

3

barrier for use of biosimilars. There is a gap between the expectationssurrounding current clinical data and the accessibility to or availability of

clinical data. Lack of confidence by health care professionals inservices provided by biosimilar companies (especially in terms of

) may also limit the use of biosimilars. In addition, lack of clearinformation on the use of biosimilars, originators and even on second-

products for specific indications may lead theo the product they are used to.

Low uptake of biosimilars in Belgium reflects the broader problem ofpharmaceutical use in hospital settings, linked in particular to the lack of

and other advantages. Although theseconstitute perfectly legal earnings and may well be used in

meaningful ways within the hospital, it disturbs competition and may makeauthorities to set appropriate and long-term

4

SYNTHESIS

TABLE OF CONTENTS1.

2.

3.

3.1.

3.2.

3.3.

4.

4.1.

4.2.

4.3.

5.

5.1.

5.2.

5.3.

5.4.

6.

6.1.

6.2.

6.3.

6.4.

Biosimilar medicines

1. INTRODUCTION ................................................................ ................................

2. AVAILABLE BIOSIMILARS IN EUROPE ................................

3. BIOSIMILARS IN THE BELGIAN CONTEXT................................

3.1. PHARMACEUTICAL EXPENSES FOR BIOLOGICALS ................................

3.2. PRICE AND REIMBURSEMENT FOR BIOSIMILARS IN BELGIUM

3.3. MEASURES TO STIMULATE BIOSIMILAR UPTAKE ................................

4. BIOSIMILARS IN AN INTERNATIONAL PERSPECTIVE ................................

4.1. UPTAKE OF BIOSIMILARS IN EUROPE ................................ ................................

4.2. HOW MUCH PRICE REDUCTION AND SAVINGS CAN BE EXPECTED FROM THEBIOSIMILAR? ................................................................ ................................

4.3. FACTORS INFLUENCING BIOSIMILAR USE ................................

4.3.1. Physician prescription habits and loyalty to a reference product

4.3.2. Competition with second-generation products ................................

4.3.3. Policy decisions................................................................

5. ACTORS, ROLES, AND POSITIONS IN BIOSIMILAR UPTAKE IMPROVINGBELGIUM ................................................................................................

5.1. CLINICAL BARRIERS ................................................................

5.1.1. Lack of knowledge or confidence in efficacy and safety...

5.1.2. … but less so for newly initiated treatments ................................

5.1.3. Lack of available data or access to it ................................

5.2. BARRIERS TO ENTER THE HOSPITAL MARKET ................................

5.3. IMPACT OF THE RECENT POLICY MEASURES ................................

5.4. IMPACT OF OTHER FORTHCOMING OR POTENTIAL MEASURES

6. CONCLUSION AND DISCUSSION ................................................................

6.1. INFORMATION AND CLINICAL BARRIERS ................................

6.2. FINANCING OF PHARMACEUTICALS IN HOSPITALS: A PANDORA BOX FOR

6.3. LIMITATIONS AND RESEARCH AGENDA ................................

6.4. A LOOK INTO THE FUTURE................................................................

KCE Report 199Cs

................................................................... 5

............................................................................................ 6

....................................................................................... 8

..................................................................... 10

IN BELGIUM.................................................. 12

........................................................................ 12

................................................................. 14

........................................................... 14

BE EXPECTED FROM THE UPTAKE OF...................................................................... 15

.................................................................................... 15

Physician prescription habits and loyalty to a reference product .......................................... 15

...................................................................... 15

..................................................................................... 16

AR UPTAKE IMPROVING POLICIES IN............................................................................ 17

......................................................................................... 18

Lack of knowledge or confidence in efficacy and safety... .................................................... 18

......................................................................... 18

.................................................................................... 19

............................................................................ 19

............................................................................. 20

MEASURES .............................................. 21

.................................................................... 22

...................................................................................... 22

S: A PANDORA BOX FOR POLICY MAKERS22

........................................................................................ 23

.............................................................................. 23

KCE Report 199Cs

1. INTRODUCTIONTo control pharmaceutical expenditures in Belgium, a number of policiesfor pharmaceuticals in both ambulant and inpatient settings haveimplemented. Recent measures undertaken to curb expenditures includeamong others: higher price reductions for both pharmaceuticals wireference price system and pharmaceuticals reimbursed for periods over12 and 15 years and pharmacist substitution by less expensive alternativesfor International Non-proprietary Name (INN) prescription and forand antifungal prescriptions. It was also decided to claim a partdiscounts granted by pharmaceutical companies tovia a reduction of the hospital prospective budget for pharmaceuticals. It iswithin this context of need for cost-containment that the Minister of SocialAffairs and Public Health introduced during the summer of 2012 measuresthat offer an incentive to use biosimilars in Belgium.

When appropriate from a medical point of view, biosimilars offer analternative treatment to an already commercialized biological medicine at alower cost for the third-party payer (see Box 1). Yet, Belgium has one ofthe lowest uptake rates in Europe of currently available biosimilars. Lack ofcurrent market penetration of commercialised biosimilarnational authorities as a lost opportunity in terms of current savings as wellas a barrier for future savings. Indeed, patent expiry of major blockbusterbiologicals will create an opportunity for biosimilars in new product classes.

The Minister of Social Affairs and Public Health asked the KCE to identifyreasons for the low uptake of biosimilars in Belgium. The scope of thisreport is limited to the analysis of barriers and policy measures relating touptake of biosimilars in Belgium and abroad. We include a description ofuptake, price reduction and related savings for the thirdEurope as well as a closer look at measures influencing biosimilar uptakein France, The Netherlands, Germany and Sweden. For Belgium, weprovide a description of pricing and reimbursement rules encompassingbiosimilars as well as a field analysis of reasons leading to their lowuptake. Appraisal of the regulatory approval pathway of biosimilars,including the requirements for clinical data, are out ofand safety of biosimilars are considered as implicit in this report and are aprerequisite to promote the use of biosimilars.

Biosimilar medicines

To control pharmaceutical expenditures in Belgium, a number of policiesfor pharmaceuticals in both ambulant and inpatient settings have beenimplemented. Recent measures undertaken to curb expenditures include

h pharmaceuticals within thepharmaceuticals reimbursed for periods over

pharmacist substitution by less expensive alternativesprescription and for antibiotic

It was also decided to claim a part ofdiscounts granted by pharmaceutical companies to hospital pharmaciesvia a reduction of the hospital prospective budget for pharmaceuticals. It is

ment that the Minister of SocialAffairs and Public Health introduced during the summer of 2012 measuresthat offer an incentive to use biosimilars in Belgium.

When appropriate from a medical point of view, biosimilars offer analready commercialized biological medicine at a

party payer (see Box 1). Yet, Belgium has one ofthe lowest uptake rates in Europe of currently available biosimilars. Lack ofcurrent market penetration of commercialised biosimilars is seen bynational authorities as a lost opportunity in terms of current savings as well

barrier for future savings. Indeed, patent expiry of major blockbusterbiologicals will create an opportunity for biosimilars in new product classes.

ster of Social Affairs and Public Health asked the KCE to identifyreasons for the low uptake of biosimilars in Belgium. The scope of thisreport is limited to the analysis of barriers and policy measures relating to

We include a description ofprice reduction and related savings for the third-party payer in

Europe as well as a closer look at measures influencing biosimilar uptakeand Sweden. For Belgium, we

escription of pricing and reimbursement rules encompassingbiosimilars as well as a field analysis of reasons leading to their low

Appraisal of the regulatory approval pathway of biosimilars,including the requirements for clinical data, are out of scope. Effectivenessand safety of biosimilars are considered as implicit in this report and are a

In analogy with the introduction of generics forexpiration of patents for the first biologicals opened new hopes foraffordable copies and increased competition. Given the different nature ofthe active substance included in biosimilars and generics, the EuropeanMedicine Agency (EMA) developed a separate market authorization (MA)procedure for biosimilars.

The most important part of the evaluation of a biosimilar in the EuropeanUnion is the comparison of the product with the reference productto demonstrate that there is no significant difference between themcomparability exercise. The aim of thedemonstrate that the biosimilar and the reference product have similarprofiles in terms of quality, safety and efficacy.

Box 1 – Definitions

Biological medicines (biologicals) contain a biological substance that isproduced by or derived from a living organism.biologicals are usually larger and more complex than those of chemicallyderived medicines (non-biological medicine).

“A similar biological medicinal product, also knowproduct which is similar to a biological medicine that has already beenauthorised, the so-called “reference medicinal productsubstance of a biosimilar medicine is a known biological active substanceand similar to the one of the reference medicinal product. A similarbiological medicinal product and its reference medicinal product areexpected to have the same safety and efficacy profile and are generallyused to treat the same conditions”.

2

A biosimilar is not a generic. The development process of a biosimilar isusually more complex than for a generic, which usually has a simplerchemical structure and is considered to be identicalmedicine.

Biosimilars should not be confused with biogenerics, noncomparable biologics, me-too or secondSome biologicals marketed in countries such as China and India are

5

In analogy with the introduction of generics for chemical medicines, theexpiration of patents for the first biologicals opened new hopes foraffordable copies and increased competition. Given the different nature ofthe active substance included in biosimilars and generics, the European

veloped a separate market authorization (MA)

of the evaluation of a biosimilar in the Europeancomparison of the product with the reference product in order

nificant difference between them, i.e. theaim of the comparability exercise is to

demonstrate that the biosimilar and the reference product have similarprofiles in terms of quality, safety and efficacy.

(biologicals) contain a biological substance that isproduced by or derived from a living organism.

1The active substances of

biologicals are usually larger and more complex than those of chemicallybiological medicine).

dicinal product, also known as “biosimilar”, is aproduct which is similar to a biological medicine that has already been

reference medicinal product”. The activesubstance of a biosimilar medicine is a known biological active substance

one of the reference medicinal product. A similarbiological medicinal product and its reference medicinal product areexpected to have the same safety and efficacy profile and are generally

2

The development process of a biosimilar isusually more complex than for a generic, which usually has a simpler

tructure and is considered to be identical to the reference

Biosimilars should not be confused with biogenerics, non-too or second-generation biologicals.

marketed in countries such as China and India are often

6

referred as “biosimilars” without following the rigorous reguused in Europe.

Me-too biologicals and second-generation biologicalsthrough the normal full clinical development approval pathway forbiologics, while biosimilars have a scaled down procedure.biologicals” are approved after a pioneering (“firstare defined as comparable but not necessary clinically superior productA second-generation biological achieves an improved clinical performancecompared to a pioneering pharmaceutical (“first-generation

A therapeutic category can include a referencepharmaceutical), biosimilars and non-reference products (mebiologicals and second-generation products).

Biosimilar medicines

without following the rigorous regulatory scrutiny

biologicals are authorizedthrough the normal full clinical development approval pathway for

milars have a scaled down procedure. “Me-toofirst-generation”) product and

are defined as comparable but not necessary clinically superior products.an improved clinical performance

generation”).3

can include a reference-product (pioneeringreference products (me-too

2. AVAILABLE BIOSIMILARSThe first biosimilar was approved in Europe in 2006currently available in three product classes:agents (epoetins), granulocyte-colony stimulating factors (filgrastim) andgrowth hormones (somatropin) (seeepoetin on the market which are produced by tSeven biosimilars for filgrastim haveproduced by three manufacturers. Two biosimilars for somatropin haveobtained market authorization and are manufactured by differentcompanies.

KCE Report 199Cs

VAILABLE BIOSIMILARS IN EUROPEThe first biosimilar was approved in Europe in 2006. Biosimilars arecurrently available in three product classes: Erythropoiesis-stimulating

colony stimulating factors (filgrastim) andhormones (somatropin) (see Table 1). There are five biosimilars for

epoetin on the market which are produced by two different manufacturers.have obtained market authorization and are

manufacturers. Two biosimilars for somatropin haveobtained market authorization and are manufactured by different

KCE Report 199Cs

Table 1 – Biosimilars currently approved in the E

Product class Referenceproduct

Biosimilar

Somatropin

(Human growth factor)

Genotropin Omnitrope

Humatrope Valtropin

Epoetin

(Treatment of anemia,increases red bloodcell production)

Eprex Retacrit

Eprex Silapo

Eprex Abseamed

Eprex Binocrit

Eprex Epoetin alfa Hexal

Filgrastim

(Treatment ofneutropenia)

Neupogen Biograstim

Neupogen FilgrastimRatiopharm

Neupogen Ratiograstim

Neupogen Tevagrastim

Neupogen Nivestim

Neupogen Zarzio

Neupogen Filgrastim Hexal

Source: Adapted from Minghetti (2011)4

using official information from the European Medicine Agency (up to 29 January 2013).voluntary withdrawn from the market. INN: International Nonword.

Biosimilar medicines

Biosimilars currently approved in the European Union

Biosimilar INN MA holder Manufacturer of activesubstance

somatropin Sandoz Sandoz

somatropin BioPartners LG Life Sciences

epoetin zeta Hospira Norbitec

epoetin zeta Stada Norbitec

epoetin alfa Medice Rentschler Biotecnologie

epoetin alfa Sandoz Rentschler Biotecnologie

Epoetin alfa Hexal epoetin alfa Hexal (now Sandoz) Rentschler Biotecnologie

filgrastim CT Arzneimittel Sicor Biotech

Ratiopharmfilgrastim Ratiopharm (now Teva Generics) Sicor Biotech

Ratiograstim filgrastim Ratiopharm (now Teva Generics) Sicor Biotech

Tevagrastim filgrastim Teva Generics Sicor Biotech

filgrastim Hospira Hospira Zagreb

filgrastim Sandoz Sandoz

Hexal filgrastim Hexal Sandoz

using official information from the European Medicine Agency (up to 29 January 2013).1Valtropin and Filgrastim Ratiopharm were

voluntary withdrawn from the market. INN: International Non-proprietary Name. MA: market authorization. Brand names are written using an uppercase for the first letter of the

7

Manufacturer of activesubstance

MA date

12/4/2006

LG Life Sciences 12/4/2006,withdrawn 12/05/2012

1

18/12/2007

18/12/2007

Rentschler Biotecnologie 28/08/2007

Rentschler Biotecnologie 28/08/2007

Rentschler Biotecnologie 28/08/2007

Sicor Biotech 15/09/2008

Sicor Biotech 15/09/2008,withdrawn 20/07/2011

1

Sicor Biotech 15/09/2008

Sicor Biotech 15/09/2008

Hospira Zagreb 08/06/2010

06/02/2009

06/02/2009

Valtropin and Filgrastim Ratiopharm were. Brand names are written using an uppercase for the first letter of the

8

3. BIOSIMILARS IN THE BELGIANCONTEXT

A brief overview of the context in which biosimilar competition takes placeis presented hereafter. First, prescription in ambulatory care of lowalternatives includes generics but also reference products (brandpharmaceuticals) having reduced their price. National authorities decidedto define low-cost prescription in this way to ensure savings for patientsand the third-party payer. Second, in hospital settings, direct negotiationsbetween purchasers (hospital pharmacists) and providers (pharmaceuticcompanies) lead in some cases to large discounts on list prices fixed bythe authorities. Discounted prices are not disclosed, neither to theauthorities nor among hospitals. As discounted prices are not known by allparties, the necessary conditions guaranteeing an open competition arelacking. In addition to discounts on list prices, clinical research in hospitalsand continuing education of hospital pharmacists and physicians are alsofinanced by the pharmaceutical sector. Whetherstrengthens the loyalty of pharmacists, physicians and hospitals toreference products is an open question. We may hypothesize thatbiosimilars enter a difficult arena.

Biosimilar medicines

ELGIAN

A brief overview of the context in which biosimilar competition takes placeis presented hereafter. First, prescription in ambulatory care of low-costalternatives includes generics but also reference products (brand

rice. National authorities decidedcost prescription in this way to ensure savings for patientsparty payer. Second, in hospital settings, direct negotiations

between purchasers (hospital pharmacists) and providers (pharmaceuticalcompanies) lead in some cases to large discounts on list prices fixed bythe authorities. Discounted prices are not disclosed, neither to theauthorities nor among hospitals. As discounted prices are not known by all

aranteeing an open competition arelacking. In addition to discounts on list prices, clinical research in hospitalsand continuing education of hospital pharmacists and physicians are alsofinanced by the pharmaceutical sector. Whether this conflict of intereststrengthens the loyalty of pharmacists, physicians and hospitals toreference products is an open question. We may hypothesize that

Box 2 – Key elements on the pricing and reimbursement syspharmaceuticals in Belgium

Pricing and reimbursement procedures

The request for reimbursement for medicinal products in inpatient andoutpatient settings follows the same pathway in Belgium. The DrugReimbursement Committee (CTG –request for reimbursement for any pharmaceutical. The CTGappraisal report includes the reimbursement basis, the list price, thereimbursement category (patient share in the cost of caresharing”) as well as any specific conditions for patient

The reimbursement basis usually corresponds to themainly concern pharmaceuticals included in the reference price system(RPS) and pharmaceuticals for which the reimbursement basis iscalculated as a flat rate that may differ from the list price.

The reimbursement basis takes into account the added therapeutic valueof the pharmaceutical. Therapeutic value is divided into three mainclasses.

Class 1 corresponds to pharmaceuticals for which the cadded therapeutic value and therefore, can claim a price premium.

Class 2 corresponds to pharmaceuticalstherapeutic value with respect to another product (comparator),prices cannot exceed that of the combiosimilars have been filed in class 2 (see more details in

Finally, class 3 includes generics and copies.copies must be reduced by at least by 31% (minimum mandatoryreduction) with respect to the ex-factory list price of the reference product

The reimbursement category reflects the therapeutic importance of thepharmaceutical and determines the patient share in the cost of care. Adistinction in patient cost-sharing is madefor serious and long-term illnesses (category Amedically useful pharmaceuticals (category Bmedically less useful pharmaceuticals (category C, Cs and Cx). It shouldbe noted that only for pharmaceuticals included in the category F (Fa and

KCE Report 199Cs

the pricing and reimbursement system of

Pricing and reimbursement procedures

The request for reimbursement for medicinal products in inpatient andoutpatient settings follows the same pathway in Belgium. The Drug

– CRM) gives the final appraisal of therequest for reimbursement for any pharmaceutical. The CTG – CRM

reimbursement basis, the list price, the(patient share in the cost of care or “cost-

conditions for patient reimbursement.

usually corresponds to the list price. Exceptionsmainly concern pharmaceuticals included in the reference price system(RPS) and pharmaceuticals for which the reimbursement basis is

may differ from the list price.

The reimbursement basis takes into account the added therapeutic valueof the pharmaceutical. Therapeutic value is divided into three main

Class 1 corresponds to pharmaceuticals for which the company claims anadded therapeutic value and therefore, can claim a price premium.

pharmaceuticals which have an analogoustherapeutic value with respect to another product (comparator), and theirprices cannot exceed that of the comparator. Reimbursement requests forbiosimilars have been filed in class 2 (see more details in section 3.2).

3 includes generics and copies. Prices of generics andat least by 31% (minimum mandatoryfactory list price of the reference product.

reflects the therapeutic importance of thepharmaceutical and determines the patient share in the cost of care. A

is made between vital pharmaceuticalsterm illnesses (category A and Fa), socially and

medically useful pharmaceuticals (category B and Fb), and socially andmedically less useful pharmaceuticals (category C, Cs and Cx). It should

for pharmaceuticals included in the category F (Fa and

KCE Report 199Cs

Fb alike) the reimbursement basis corresponds to a flat rate per treatment.Currently, only epoetins are included in category F (see sectiondetails). For each of these categories patient costa percentage (“coinsurance”) of the reimbursement basis limited to a fixedceiling.

Reference Price System (RPS)

A reference price system limits the reimbursement for pharmaceuticalsbelonging to clearly defined “clusters” (groups) to the level of the referenceprice. Within each cluster, if the price of a pharmaceutical exceeds thereference price, the patient pays the difference (namedsupplement”). In Belgium, a “generic reference price system2001. Clusters include pharmaceuticals having the same active substance(reference products and generics independent of dosage andadministration routes). The reference supplement is limited by a securitymargin of a maximum of 10.8 euros. Other countries ha“therapeutic reference price system” where clusters include therapeuticequivalent pharmaceuticals which may have a different active substance.

Quota of low-cost prescription

Belgium has a policy of quota of low-cost prescription pharmaceuticalsambulatory care. Before the summer of 2012 (see sectioninclusion of biosimilars) “low-cost” prescriptionmolecules when: (1) reference products (brand pharmaceuticalsa generic alternative exists and which reduced the list price so that patientsdo not have to pay the reference supplement, (2) generics and copies, (3)prescriptions under the International Non-proprietary Name (INN).Prescription quotas vary among different specialities and are monitored bythe RIZIV – INAMI.

Reimbursement (invoicing) of pharmaceuticals in hospital settings

Broadly, invoicing of pharmaceuticals from hospitals to the thirdpayer takes two forms. For pharmaceuticals integrated in the hospitalprospective budget, the hospital retrospectively charges 25% of thereimbursement basis of each delivered pharmaceutical and receives aprospective lump sum allocation per inpatient admission. Forpharmaceuticals not included in the hospital prospective budget,

Biosimilar medicines

Fb alike) the reimbursement basis corresponds to a flat rate per treatment.Currently, only epoetins are included in category F (see section 3.3 for

categories patient cost-sharing is calculated as) of the reimbursement basis limited to a fixed

A reference price system limits the reimbursement for pharmaceuticals(groups) to the level of the reference

price. Within each cluster, if the price of a pharmaceutical exceeds thethe patient pays the difference (named “reference

generic reference price system” exists since01. Clusters include pharmaceuticals having the same active substance

(reference products and generics independent of dosage andadministration routes). The reference supplement is limited by a securitymargin of a maximum of 10.8 euros. Other countries have set a

where clusters include therapeuticequivalent pharmaceuticals which may have a different active substance.

cost prescription pharmaceuticals in2012 (see section 3.3 for the

prescription included chemicalpharmaceuticals) for which

uced the list price so that patientsdo not have to pay the reference supplement, (2) generics and copies, (3)

proprietary Name (INN).uotas vary among different specialities and are monitored by

Reimbursement (invoicing) of pharmaceuticals in hospital settings

Broadly, invoicing of pharmaceuticals from hospitals to the third-partypayer takes two forms. For pharmaceuticals integrated in the hospital

retrospectively charges 25% of thereimbursement basis of each delivered pharmaceutical and receives aprospective lump sum allocation per inpatient admission. Forpharmaceuticals not included in the hospital prospective budget, the

hospital invoicing is based on the reimbursement basis taking into accountthe reimbursement category. Details on invoicing for biosimilars in hospitalsettings are provided in section 3.3.

9

ased on the reimbursement basis taking into accountDetails on invoicing for biosimilars in hospital

.

10

3.1. Pharmaceutical expenses for biologicalsIn 2010, 17.23% of total RIZIV – INAMI health care reimbursementconcerned pharmaceuticals. Table 2 includes forhighest reimbursement for biologicals in community and hospitalpharmacies as well as reimbursement for therapeutic classesbiosimilar is currently available. Besides biosimilars and referenceproducts containing epoetin, two second-generation products are availableon the market (Aranesp and Mircera). For granulocytefactors, one second-generation biological (Neulasta) is also available.

Biosimilar medicines

Pharmaceutical expenses for biologicalsINAMI health care reimbursement

ncludes for 2011, RIZIV – INAMIhighest reimbursement for biologicals in community and hospitalpharmacies as well as reimbursement for therapeutic classes where a

biosimilars and referencegeneration products are available

and Mircera). For granulocyte-colony stimulatingiological (Neulasta) is also available.

The largest reimbursements for biologicalsantibodies (mAb) of which three are anti(infliximab, adalimumab and etanercept) widely used to treat autoimmunepathologies in rheumatology (e.g., rblockbuster biologicals will see their patent expire in 2014 (infliximab,trastuzumab) and in 2015 (etanercept).infliximab are being evaluated by the European Medici

KCE Report 199Cs

for biologicals concern four monoclonalantibodies (mAb) of which three are anti-tumor necrosis factors (TNF)

and etanercept) widely used to treat autoimmunegies in rheumatology (e.g., rheumatoid arthritis). Several

blockbuster biologicals will see their patent expire in 2014 (infliximab,trastuzumab) and in 2015 (etanercept). Currently, two biosimilars for

the European Medicines Agency.

KCE Report 199Cs

Table 2 – RIZIV – INAMI expenses for selected biologicals (2011)

Group ATC

Most expensive biologicals (Top 5)

Monoclonal antibodies (anti-TNF) L04AB04

Monoclonal antibodies (anti-TNF) L04AA12

Monoclonal antibodies (anti-HER2) L01XC03

Monoclonal antibodies (anti-TNF) L04AB01

Epoetin B03XA02

Therapeutic class* where a biosimilar is available

Epoetin (long acting) B03XA02

(short acting) B03XA01

(long acting) B03XA03

Somatropin H01AC01

H01AC01

Filgrastim (long acting) L03AA13

(long acting) L03AA13

(short acting) L03AA02

(short acting) L03AA02

Source: RIZIV – INAMI data provisory for 2011. *Therapeutic classes include biosimilars, reference products and nonmolecules where a biosimilar is available. TNF: tumour

Biosimilar medicines

INAMI expenses for selected biologicals (2011)

ATC-5 INN Euros

L04AB04 Adalimumab 97

L04AA12 Infliximab 90

L01XC03 Trastuzumab 61

L04AB01 Etanercept 60

B03XA02 Darbepoetin alfa 53

Therapeutic class* where a biosimilar is available

B03XA02 Darbepoetin alfa 53

B03XA01 Erythropoietin 25

B03XA03 Methoxy-polyethylenglycol-epoetin beta 13

H01AC01 Somatropin 19

H01AC01 Somatropin 108

L03AA13 Pegfilgrastim 31

L03AA13 Pegfilgrastim 27

L03AA02 Filgrastim 4 903

L03AA02 Filgrastim 447

INAMI data provisory for 2011. *Therapeutic classes include biosimilars, reference products and non -reference products (see Box 1 for definitions). In italics:necrosis factors. ATC: Anatomical Therapeutic Chemical. HER2: Human epidermal growth factor receptor

11

Euros Pharmacy setting

673 654 Community

266 686 Hospital

337 274 Hospital

585 181 Community

457 323 Hospital

457 323 Hospital

771 878 Hospital

883 347 Hospital

512 592 Community

108 254 Hospital

981 299 Hospital

284 Community

903 752 Hospital

447 358 Community

reference products (see Box 1 for definitions). In italics:uman epidermal growth factor receptor-2

12

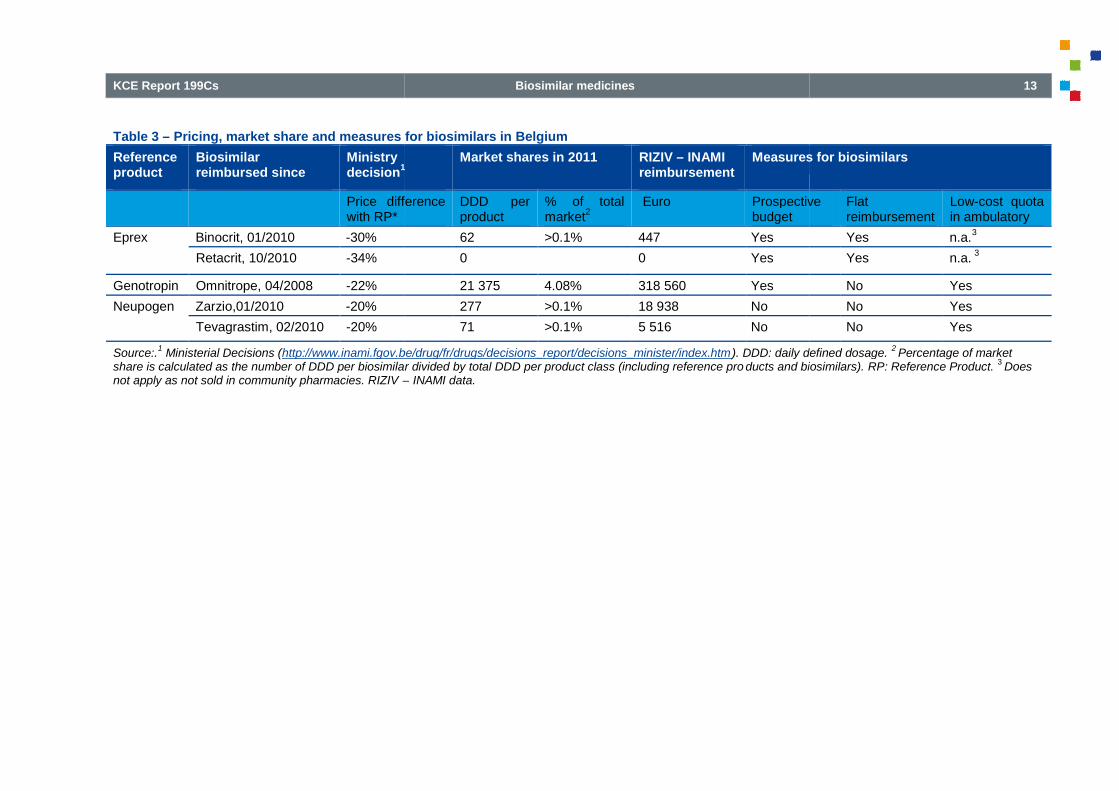

3.2. Price and reimbursement for biosimilars in BelgiumCurrently, companies producing biosimilars have submitted a marketingauthorization application via the centralised procedure at the EMA. Afterobtaining market authorization, companies can file a reimbursementrequest to national pricing and reimbursementreimbursement for biosimilars follow the same pathway as any otherpharmaceutical in Belgium. The current reimbursement framework doesneither contain clauses determining the reimbursement basis nor amandatory price reduction for biosimilars. All reimbursement claims forbiosimilars have been filed under class 2 probably because requirementsin class 1 or 3 do not encompass them. On the one hand, bcannot claim a therapeutic advantage over the reference product, ththe request for reimbursement is not likely to be accepted inthe other hand, class 3 only includes generics and copies.

Table 3 presents information on pricing, market share and measures forbiosimilars in Belgium. All reimbursement requesincluded a voluntary price reduction. The price negotiations occur on a percase basis for each new biosimilar, in contrast to generics where amandatory price reduction is fixed. Negotiations between authorities andbiosimilar producers led to a price reduction ranging from 20% to 34%respect to the price of the reference product. Not all available biosimilarsare currently commercialized in Belgium. Until December 2012, sixreimbursement request files were filed resulting in(Binocrit, Retacrit, Omnitrope, Zarzio, Tevagrastim) and in one negativedecision (Nivestim). In 2011, uptake of biosimilars for epoetin andfilgrastim was almost zero (less than 0.1% of total use as expressed indaily defined dosage (DDD)). A biosimilar for somatropin, mostlyprescribed in community pharmacies, achieved a market pe4.08% of total reimbursed DDDs. This percentage is lower than reportedsales (6% in terms of DDD) available in the IMS data (see figure 1).

3.3. Measures to stimulate biosimilar uptakeIn 2012, the Minister took a number of measures to increase the marketshare of biosimilars in Belgium. The objective was not only to generatesavings for RIZIV – INAMI but also to ensure that the Belgian market

Biosimilar medicines

Price and reimbursement for biosimilars in BelgiumCurrently, companies producing biosimilars have submitted a marketingauthorization application via the centralised procedure at the EMA. Afterobtaining market authorization, companies can file a reimbursement

authorities. Requests forreimbursement for biosimilars follow the same pathway as any other

reimbursement framework doesneither contain clauses determining the reimbursement basis nor a

ll reimbursement claims forprobably because requirements

On the one hand, biosimilarsclaim a therapeutic advantage over the reference product, therefore

request for reimbursement is not likely to be accepted in class 1. Onthe other hand, class 3 only includes generics and copies.

presents information on pricing, market share and measures forAll reimbursement requests for biosimilars have

The price negotiations occur on a percase basis for each new biosimilar, in contrast to generics where a

Negotiations between authorities anducers led to a price reduction ranging from 20% to 34% with

to the price of the reference product. Not all available biosimilarsare currently commercialized in Belgium. Until December 2012, six

filed resulting in five positive decisions(Binocrit, Retacrit, Omnitrope, Zarzio, Tevagrastim) and in one negativedecision (Nivestim). In 2011, uptake of biosimilars for epoetin andfilgrastim was almost zero (less than 0.1% of total use as expressed in

(DDD)). A biosimilar for somatropin, mostlyprescribed in community pharmacies, achieved a market penetration of

This percentage is lower than reportedsales (6% in terms of DDD) available in the IMS data (see figure 1).

biosimilar uptakeIn 2012, the Minister took a number of measures to increase the marketshare of biosimilars in Belgium. The objective was not only to generate

INAMI but also to ensure that the Belgian market

remains interesting for companies that will offer biosimilars in new productclasses. Measures to stimulate use of biosimilars included:

Inclusion of biosimilars in the quota for lowambulatory settings. Since 1enlarges the initial framework ofgeneral rule, the system previously only included chemical moleculeswhere a generic alternative is available. It should be noted that onlythe biosimilars themselves are nprescription quota. A biologicalwhich reduces its price to the level of the biosimilarthe quota of low-cost prescription

Inclusion of epoetin and somatropin in the hbudget. Since 1 July 2012, the hospital prospective budget forpharmaceuticals also includes all epoetins (shortwell as all pharmaceuticals containing somatropin. Before this date,these pharmaceuticals were invoiced by the hospital to the RIZIVINAMI based on actual consumption.filgrastim (reference product and biosimilars) are not included in thehospital prospective budget.

Flat rate reimbursement for epoetins (September 2012, all epoetins are also included inreimbursement basis for these pharmaceuticals (i.e. Aranesp, Binocrit,Eprex, Mircera, Neorecormon, Retacrit) is determined according to aflat rate per treatment. This flat rate was fixreimbursement basis of the least expensive reference product havinga biosimilar (Eprex) and covers prescriptions in inpatient andoutpatient settings. A difference between the list price and the flat rateis in charge of hospitals. In general, the payment from the thirdpayer to a hospital cannot exceed the reimbursement basis of apharmaceutical. However, as an exception to this rule, from 1February 2013, hospitals will receive this flat ratethe list price for the biosimilars Binocrit and Retacrit (i.e.reimbursement basis exceeds the list price for Binocrit and Retacrit).

KCE Report 199Cs

ains interesting for companies that will offer biosimilars in new productclasses. Measures to stimulate use of biosimilars included:

Inclusion of biosimilars in the quota for low-cost prescription inSince 1 July 2012, the inclusion of biosimilars

enlarges the initial framework of “low-cost” prescription quota. As ageneral rule, the system previously only included chemical moleculeswhere a generic alternative is available. It should be noted that onlythe biosimilars themselves are now included in the low-cost

iological for which a biosimilar is available andprice to the level of the biosimilar is not included in

cost prescription.

Inclusion of epoetin and somatropin in the hospital prospectiveJuly 2012, the hospital prospective budget for

pharmaceuticals also includes all epoetins (short- and long-acting) aswell as all pharmaceuticals containing somatropin. Before this date,

invoiced by the hospital to the RIZIV –INAMI based on actual consumption. Pharmaceuticals containingfilgrastim (reference product and biosimilars) are not included in the

Flat rate reimbursement for epoetins (category F). Since 1September 2012, all epoetins are also included in category F. Theeimbursement basis for these pharmaceuticals (i.e. Aranesp, Binocrit,

Eprex, Mircera, Neorecormon, Retacrit) is determined according to aflat rate per treatment. This flat rate was fixed according to the lowestreimbursement basis of the least expensive reference product having

and covers prescriptions in inpatient and. A difference between the list price and the flat rate

ls. In general, the payment from the third-partypayer to a hospital cannot exceed the reimbursement basis of apharmaceutical. However, as an exception to this rule, from 1February 2013, hospitals will receive this flat rate that is higher than

biosimilars Binocrit and Retacrit (i.e.reimbursement basis exceeds the list price for Binocrit and Retacrit).

KCE Report 199Cs

Table 3 – Pricing, market share and measures for biosimilars in Belgium

Referenceproduct

Biosimilarreimbursed since

Ministrydecision

1

Price differencewith RP*

Eprex Binocrit, 01/2010 -30%

Retacrit, 10/2010 -34%

Genotropin Omnitrope, 04/2008 -22%

Neupogen Zarzio,01/2010 -20%

Tevagrastim, 02/2010 -20%

Source:.1

Ministerial Decisions (http://www.inami.fgov.be/drug/fr/drugs/decisions_report/decisions_minister/index.htmshare is calculated as the number of DDD per biosimilar divided by total DDD per product class (including reference pronot apply as not sold in community pharmacies. RIZIV –

Biosimilar medicines

Pricing, market share and measures for biosimilars in Belgium

1Market shares in 2011 RIZIV – INAMI

reimbursementMeasures for biosimilars

Price difference DDD perproduct

% of totalmarket

2Euro Prospective

budget

62 >0.1% 447 Yes

0 0 Yes

21 375 4.08% 318 560 Yes

277 >0.1% 18 938 No

71 >0.1% 5 516 No

http://www.inami.fgov.be/drug/fr/drugs/decisions_report/decisions_minister/index.htm). DDD: daily defined dosage.share is calculated as the number of DDD per biosimilar divided by total DDD per product class (including reference pro ducts and biosimilars).

– INAMI data.

13

Measures for biosimilars

Prospective Flatreimbursement

Low-cost quotain ambulatory

Yes n.a.3

Yes n.a.3

No Yes

No Yes

No Yes

DDD: daily defined dosage.2Percentage of market

and biosimilars). RP: Reference Product.3

Does

14

4. BIOSIMILARS IN AN INTERNATIONALPERSPECTIVE

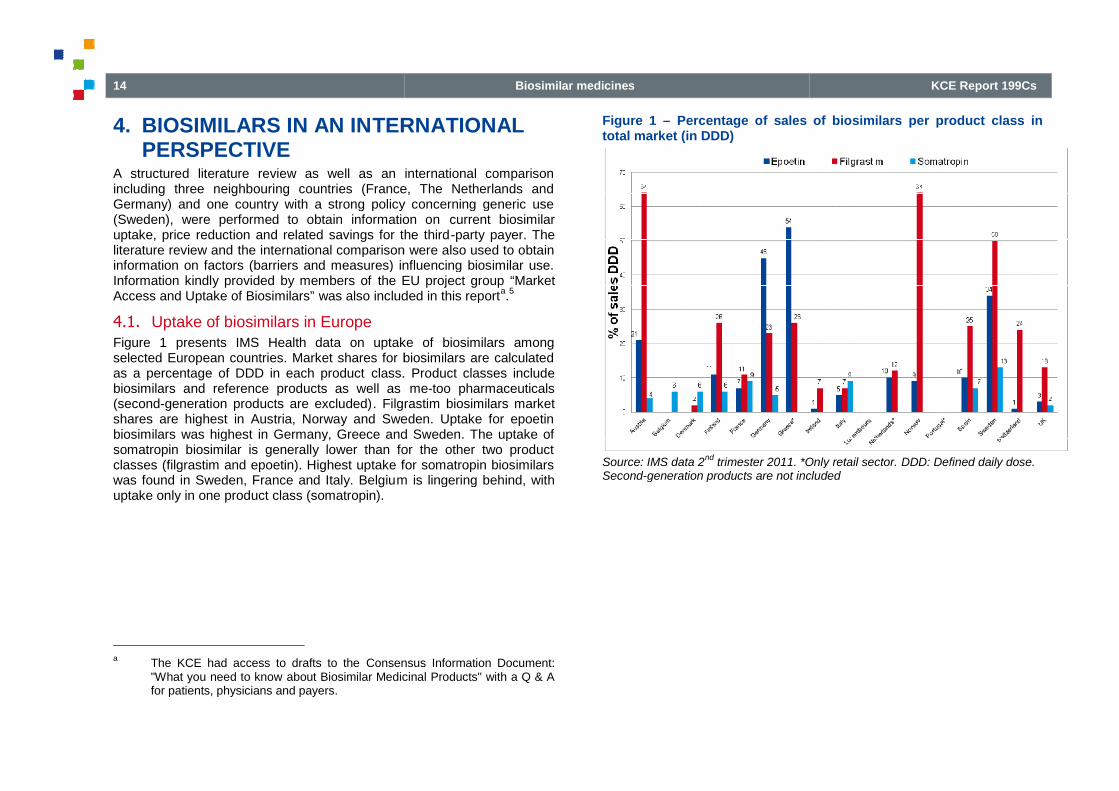

A structured literature review as well as an international comparisonincluding three neighbouring countries (France, The Netherlands andGermany) and one country with a strong policy concerning generic use(Sweden), were performed to obtain information onuptake, price reduction and related savings for the thirdliterature review and the international comparison were also used to obtaininformation on factors (barriers and measures) influencing biosimilar use.Information kindly provided by members of the EU project groupAccess and Uptake of Biosimilars” was also included in this report

4.1. Uptake of biosimilars in EuropeFigure 1 presents IMS Health data on uptake of biosimilars amongselected European countries. Market shares for biosimilars are calculatedas a percentage of DDD in each product class.biosimilars and reference products as well as(second-generation products are excluded). Filgrastim biosimilars marketshares are highest in Austria, Norway and Sweden. Uptake for epoetinbiosimilars was highest in Germany, Greece and Sweden. The uptake ofsomatropin biosimilar is generally lower than for the other two productclasses (filgrastim and epoetin). Highest uptake for somatropin biosimilarswas found in Sweden, France and Italy. Belgium is lingering behind, withuptake only in one product class (somatropin).

aThe KCE had access to drafts to the Consensus Information Document:"What you need to know about Biosimilar Medicinal Products" with a Q & Afor patients, physicians and payers.

Biosimilar medicines

TERNATIONAL

A structured literature review as well as an international comparisonincluding three neighbouring countries (France, The Netherlands andGermany) and one country with a strong policy concerning generic use(Sweden), were performed to obtain information on current biosimilaruptake, price reduction and related savings for the third-party payer. The

the international comparison were also used to obtaininformation on factors (barriers and measures) influencing biosimilar use.

the EU project group “Marketwas also included in this report

a.5

presents IMS Health data on uptake of biosimilars amongselected European countries. Market shares for biosimilars are calculated

class. Product classes includebiosimilars and reference products as well as me-too pharmaceuticals

. Filgrastim biosimilars marketshares are highest in Austria, Norway and Sweden. Uptake for epoetin

ilars was highest in Germany, Greece and Sweden. The uptake ofsomatropin biosimilar is generally lower than for the other two productclasses (filgrastim and epoetin). Highest uptake for somatropin biosimilars

m is lingering behind, with

Consensus Information Document:about Biosimilar Medicinal Products" with a Q & A

Figure 1 – Percentage of sales of biosimilars per product class intotal market (in DDD)

Source: IMS data 2nd

trimester 2011. *Only retail sector.Second-generation products are not included

KCE Report 199Cs

Percentage of sales of biosimilars per product class in

2011. *Only retail sector. DDD: Defined daily dose.generation products are not included

KCE Report 199Cs

4.2. How much price reduction and savings can be expectedfrom the uptake of biosimilar?

Most evidence seems to point out that competition will lead to smallerreductions on list prices between the reference product and the biosimilarthan is the case between generics and their reference products. This mayparticularly be true in countries such as the UK or Germany where pricesmay differ by up to 80% between the reference product and the generics.The lower price reduction between the reference product and the biosimilarhas been attributed to a higher production cost as well as to the strongerneed for marketing strategies for biosimilars than for generics. Moreover,high production costs may also result in fewer companies producingbiosimilars and therefore also to less price competition.

Most empirical information concerning price reductions (as well as uptake)is based on IMS data. Reported price reductions of biosimilars with respectto the reference product usually range between 10% and 35%. However,the figures vary from country to country and between the different productclasses. Mandatory price reductions have not been set in any country.Among the four countries studied in detail for thisprice reductions for epoetin and filgrastim exceeding the ranges reportedelsewhere (up to 40% for epoetins and 50% for filgrastim). Data forSweden comes from national authorities while for otherdata source is the IMS database. We cannot rule out that price reductionestimates are higher for Sweden compared to other countries becausethey are calculated using a different data sourceclasses where biosimilars are currently available, somatropin biosimilarsfeature the lowest price reduction (around 20%). It is noteworthy that onlyone biosimilar is available, providing some support to the hypothesis thatfewer competitors may lead to lower price discounts.

The available estimates on biosimilar-related savings are based ondifferent modelling strategies and hypotheses, making them difficult tocompare. In addition, estimates for Europe mostly come from thepharmaceutical sector itself. Consequently, there is a lack of independentanalyses of the current and future savings from the use of biosimilars.

Biosimilar medicines

How much price reduction and savings can be expected

Most evidence seems to point out that competition will lead to smallere reference product and the biosimilar

than is the case between generics and their reference products. This mayparticularly be true in countries such as the UK or Germany where pricesmay differ by up to 80% between the reference product and the generics.The lower price reduction between the reference product and the biosimilarhas been attributed to a higher production cost as well as to the strongerneed for marketing strategies for biosimilars than for generics. Moreover,

result in fewer companies producingbiosimilars and therefore also to less price competition.

Most empirical information concerning price reductions (as well as uptake)is based on IMS data. Reported price reductions of biosimilars with respect

ference product usually range between 10% and 35%. However,the figures vary from country to country and between the different productclasses. Mandatory price reductions have not been set in any country.Among the four countries studied in detail for this report, Sweden showedprice reductions for epoetin and filgrastim exceeding the ranges reportedelsewhere (up to 40% for epoetins and 50% for filgrastim). Data forSweden comes from national authorities while for other countries the main

e IMS database. We cannot rule out that price reductionestimates are higher for Sweden compared to other countries because

different data source. From the three productclasses where biosimilars are currently available, somatropin biosimilarsfeature the lowest price reduction (around 20%). It is noteworthy that onlyone biosimilar is available, providing some support to the hypothesis that

ompetitors may lead to lower price discounts.

related savings are based onmodelling strategies and hypotheses, making them difficult to

compare. In addition, estimates for Europe mostly come from theeutical sector itself. Consequently, there is a lack of independent

analyses of the current and future savings from the use of biosimilars.

4.3. Factors influencing biosimilar use

4.3.1. Physician prescription habits and loyalty to a referenceproduct