Barrick Nevada Investor Tour -...

53

Barrick Nevada Investor Tour | June 20-21, 2017 A Company of Owners

Transcript of Barrick Nevada Investor Tour -...

Barrick Nevada

Investor Tour | June 20-21, 2017

A Companyof Owners

Certain information contained or incorporated by reference in this presentation prepared by Barrick Gold Corporation ("Barrick" or the "Company"), including any information as to our strategy, projects, plans, or future financial or operating performance, constitutes "forward-looking statements". All statements, other than statements of historical fact, are forward-looking statements. The words"believe", "expect", "anticipate", "contemplate", "target", "plan", "objective" "aspiration", "aim", "intend", "project", "goal", "continue", "budget", "estimate", "potential", "may", "will", "can", "should", "could", "would", and similar expressions identify forward-lookingstatements. In particular, this presentation contains forward-looking statements including, without limitation, with respect to: (i) production rates; (ii) potential mineralization and metal or mineral recoveries; (iii) Barrick's Best-in-Class program (including potential improvements to financial and operating performance that may result from certain Best-in-Class initiatives); (iv) potential improvements to financial and operating performance and mine life at Barrick's Nevada operations; (v) potential developments in the Cortez district and at Barrick’s Fourmile project; (vi) the potential to identify new reserves and resources; (vii) the potential underground potential at Goldstrike; (viii) our pipeline of projects at or near existing Nevada operations; (ix) the potential impact and benefits from Barrick's digital enterprise transformation strategy; (x) the ability to achieve impact through short interval control at Cortez; (xi) the potential benefits from the acquisition of the Robertson Property; (xii) the benefits achievable from integrating the Cortez and Goldstrike operations; and (xiii) the estimated timing and conclusions of technical reports and other studies.

Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered reasonable by the Company as at the date of this presentation in light of management's experience and perception of current conditions and expecteddevelopments, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Known andunknown factors could cause actual results to differ materially from those projected in the forward-looking statements, and unduereliance should not be placed on such statements and information. Such factors include, but are not limited to: fluctuations in the spot and forward price of gold, copper, or certain other commodities (such as silver, diesel fuel, natural gas, and electricity); the speculative nature of mineral exploration and development; changes in mineral production performance, exploitation, and exploration successes; risks associated with the fact that certain Best-in-Class and other initiatives are still in the early stages of evaluation, and additional engineering and other analysis is required to fully assess their impact; risks associated with the implementation of Barrick's digital transformation initiative, and the ability of the projects under this initiative to meet the Company's capital allocation objectives; diminishing quantities or grades of reserves; increased costs, delays, suspensions, and technical challenges associated with theconstruction of capital projects; operating or technical difficulties in connection with mining or development activities, including geotechnical challenges, and disruptions in the maintenance or provision of required infrastructure and information technology systems; failure to comply with environmental and health and safety laws and regulations; timing of receipt of, or failure to comply with, necessary permits and approvals; uncertainty whether some or all of the Best-in-Class initiatives and targeted investments and projects will meet the Company's capital allocation objectives; the impact of inflation; fluctuations in the currency markets; changes in U.S. dollar interest rates; risks arising from holding derivative instruments; changes in national and local government legislation, taxation, controls or regulations, and/or changes in the administration of laws, policies, and practices, expropriation or nationalization of property and political or economic developments in the United States; damage to the Company’s reputation due to the actual or perceived occurrence of anynumber of events, including negative publicity with respect to the Company’s handling of environmental matters or dealings withcommunity groups, whether true or not; the possibility that future exploration results will not be consistent with the Company’sexpectations; risks that exploration data may be incomplete and considerable additional work may be required to complete furtherevaluation, including but not limited to drilling, engineering and socio-economic studies and investment; risk of loss due to acts of war, terrorism, sabotage and civil disturbances; litigation; contests over title to properties, particularly title to undeveloped properties, or over access to water, power and other required infrastructure; business opportunities that may be presented to, or pursued by, the Company; risks associated with working with partners in jointly controlled assets; our ability to successfully integrate acquisitions or complete divestitures; employee relations; increased costs and risks related to the potential impact of climate change; and availability and increased costs associated with mining inputs and labor. In addition, there are risks and hazards associated with the business of mineral exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations,pressures, cave-ins, flooding and gold bullion, copper cathode or gold or copper concentrate losses (and the risk of inadequate insurance, or inability to obtain insurance, to cover these risks).

Many of these uncertainties and contingencies can affect our actual results and could cause actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, us. Readers are cautioned that forward-lookingstatements are not guarantees of future performance. All of the forward-looking statements made in this presentation are qualified by these cautionary statements. Specific reference is made to the most recent Form 40-F/Annual Information Form on file with the SEC and Canadian provincial securities regulatory authorities for a more detailed discussion of some of the factors underlying forward- looking statements and the risks that may affect Barrick's ability to achieve the expectations set forth in the forward-looking statementscontained in this presentation.

The Company disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of newinformation, future events or otherwise, except as required by applicable law.

CAUTIONARY STATEMENT ON FORWARD-LOOKING INFORMATION

Barrick Nevada Investor Tour | 3

Elko, NevadaWelcome & Opening Remarks Kelvin Dushnisky

Operations Overview Richard Williams

Barrick Nevada Overview and Growth Bill MacNevin

Codemine Ed Humphries

Nevada Analytics and Operations Center Rob Neitzel

CortezDistrict

Range Front Declines, Continuous Miner Don Schumacher

Short Interval Control, Remote/Semi-Auto/Auto Demo Miguel Lamadrid

GoldstrikeOperations

TCM Circuit, Water Treatment Plant, Resin-in-Leach Circuit Paul Wilmot

Operations Center / Process Controls Holly Saucier

Open Pit Operations – Betze-Post and Arturo Julius Stieger

Barrick Nevada Investor Tour | 5

Largest industry presence in Nevada

Largest gold producer in Nevada and North America

Two mines: Goldstrike & Cortez “Barrick Nevada”

One joint venture: Turquoise Ridge

30 years of operationLas Vegas

Reno

Elko

Carson City

N E V A D A

Turquoise Ridge JV Goldstrike Operations

Cortez District

Barrick Nevada Investor Tour | 6

> $1 B new capital invested in Nevada past two years

> 500 Nevada-based suppliers goods/services

~$1.2 B annual spend with contractors and suppliers in rural and urban Nevada

Generates Nevada jobs (>3,000 employees) and annual state taxes (~$112M)

Barrick Nevada Investor Tour | 7

Enabler of Change

First Step – What? Vision – How? Drive – Why?

Barrick Nevada Investor Tour | 8

PARTNERSHIPSCommunity EngagementRegulatory PartnershipsStakeholder Relationships

PEOPLERecruitDevelop Retain

SafetyEnvironmentOutperform PlanBiC/Digital DeliveryInnovation

Capital Rigor & ExecutionMaintenance Management SystemStrategic SourcingCapitalize on Geological ResourcesUnite Barrick Nevada

OPERATIONAL EXCELLENCE

FINANCIAL FLEXIBILITYDeliver Free Cash Flow Disciplined Capital AllocationDeliver All in Sustaining Costs Integrated Planning

GROWTHTier IV PlanningGrowthExploring New Partnerships

Barrick Nevada Investor Tour | 9

100 Year Vision requires investment in exploration, innovation and partnerships

Close to Technical Limits

Step Changes

Innovation& Global EX

$ Investment withknown ROI

$ Investment with uncertain ROI

Leadership/Systems investment

(Optimization Process)

Impact on Productivity &Sustainability

Time

Barrick Nevada Investor Tour | 10

Imagine all of the decision making that is required to constantly deliver the optimum blend for each of the process plants as the grade, carbon contents, mining rates and other variables change while also balancing risk and opportunity within the operation!

Imagine all of the decision making that is required to constantly deliver the optimum blend for each of the process plants as the grade, carbon contents, mining rates and other variables change while also balancing risk and opportunity within the operation!

Cortez OPCortez UG Goldrush Goldstrike OP Goldstrike UG

Heap Leach Oxide Mill/CIL Roaster Autoclave

Roaster

Oxide

Leach

Roaster

Autoclave

ORE SOURCES

PROCESS OPTIONS

CortezStockpiles

GoldstrikeStockpiles

On LeaseResources

Highest Value

LOM Plan

Sustaining ProjectSystem Evaluations

MINEX AcceleratedResource

Conversion

Global ExplorationNevada Projects

AcquisitionsEvaluations

Partnerships forOre Delivery

and Processing

Off LeaseOpportunities

New or expanded orebodies to feed production profileIntegrated Technical Growth and Organic GrowthInclusive of current sites and new opportunities

Barrick Nevada Investor Tour | 12

Stochastic model used to evaluate different scenarios to help identify areas of focus for the future

Base Case – optimize current plan on short term free cash flow without adding new reserves or infrastructure

“Re-Load” Option – Technical growth to reduce cutoff grades and organic growth through MINEX to fully use existing process infrastructure

Other “Re-Tool” Options assume differing capital spend on expanding processing and/or associated infrastructure

Barrick Nevada Investor Tour | 13

Barrick Nevada is not infrastructure constrained, particularly not post 2022

In the medium term (2017-2025), the best bang for Barrick’s buck comes from spending on MINEX and brownfield projects

Longer term (2025+), Best in Class/digital/innovation or bringing new assets into the portfolio through exploration, partnerships and acquisition to improve the economics to justify and catalyze significant one-off capital investment based on current economics

Barrick Nevada Investor Tour | 14

Increase oxide mill throughput and recovery through automation and improved carbon activity

Reach full potential for autoclave by maximizing benefit of acid and alkaline ores

Autoclave Throughput(tons per operating hour)

Oxide Mill Throughput(tons per operating hour)

488 473

526 539

562 554 558 546

576 566 566 593

571 565

620

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar2016 2017

500Jan/Feb 2017

(APC1)

593

634

654

PotentialOct/Nov 2016Jan/Feb 2016

Best-in-

Class

Innovation/Digitization

Partnership

1. Automated Process Control (APC)

Barrick Nevada Investor Tour | 15

Blend roaster feed for margin to maximize free cash flow

Increase production from bulk mining methods from 5% to 30% of total UG production

Cortez UG Tons Mined(tons thousands)

Roaster Tons Processed(tons thousands)

477

425

524

249

401

477

507 508 507 532 524

498

528

367

545

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar2016 2017

91

82

103

94 90

96 97

9188

100

94 96

106 102

126

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar2016 2017

Mai

nten

ance

Mai

nten

ance

Barrick Nevada Investor Tour | 16

Design and incorporate new, bespoke, and industry-leading digital systems to further enhance efficiencies

Digital Barrick Initiatives1. UG Short Interval Control2. UG Automation3. Digital Maintenance Work Management4. Digital Processing5. Predictive Maintenance6. Consolidated Data Platform7. Analytics and Unified Operations Center8. Integrated Planning

Barrick Nevada Investor Tour | 17

0

50

100

150

200

250

300

M A M J J A S O N D

Short Interval Control(additional tons per day)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

M A M J J A S O N D

Mill Uptime(additional hours per month)

0

50

100

150

200

250

300

M A M J J A S O N D

Automated Process Control(additional tons per day)

Barrick Nevada Investor Tour | 18

GET DATA

SUP GSMGR OPSGM

MAKE DECISIONS

LIBERATE DATA

UNIFIED OPERATIONSBARRICKNEVADA

BARRICKHEAD OFFICE

ANALYSTOPERATOR

MGR

GM

SUP

GS

ANALYZE DATA

Barrick Nevada Investor Tour | 19

80 miles southwest of Elko150 years of mining1,250 employeesNew discoveries

0 miles 1 2 3 4 5

Pipeline

Cortez Hills OP

Gold Acres

Cortez Pits

Cortez Hills UG

LasVegas

Reno

Elko

Carson City

N E V A D A

Cortez

2016 Reserves

Proven 0.8 Moz1

(1.52 g/t, 16M tonnes)

Probable 9.4 Moz1

(2.18 g/t, 135M tonnes)

1. See endnote #1

Barrick Nevada Investor Tour | 20

Identified 37 targets for Minex work: – target delineation– drill testing– advanced exploration– resource delineation– reserve conversion

0 miles 1 2 3 4 5

Pipeline

Gold Acres Window

Gold Acres

Cortez Pits

WestCortez

Window

Cortez Hills OP

Cortez Hills UG

LasVegas

Reno

Elko

Carson City

N E V A D A

Cortez

Barrick Nevada Investor Tour | 21

Access through Range Front Declines– Road header advancing ahead of schedule– 3,000 feet of advancement in east portal

and 800 feet in west portal

Feasibility Study – Added Renegade Zone to reserve– In progress, completion 3Q17– Completed geotechnical assessments– Optimized autonomous haulage

Water Management– EIS will include a focus on ground water – Extensive monitoring provides confidence

in ground water model

Permitting– Submitted Mine Plan of Operations – Record of decision (ROD) expected 2019/2020

Barrick Nevada Investor Tour | 22

Phase I FeasibilityOn track for YE 2017 completion

Underground surface infrastructure design work in progress

20 drill holes complete (6,075m)

– Program completed March 2017

2017 results to date (from 2016 drilling)

– Average grade vs. model: +44%

– Average thickness vs. model: +63%

Adding 60 holes in 2017 to complete Red Hill program

ExplorationDecline Portal

CHOPcomplex

Goldrush DepositUG Workings

Declines~3 mile haul road

Barrick Nevada Investor Tour | 23

Repetitive Tasks

Stationary:– Rail haulage– Automated chute delivery– Engineered bin systems– Automated hoisting– Smart conveyors– Auger feed systems– Ore pass delivery

In motion:– Autonomous drilling – Autonomous mucking

Barrick Nevada Investor Tour | 24

High grade, high value targets with small footprintTarget identification along 3km prospective corridorStep-out holes north of high grade interceptsTightened drilling within area of high grade

1. Potential quantities and grades in these preliminary results are conceptual in nature and there has been insufficient exploration to define a mineral resource at this time and it is uncertain that further exploration will result in the target being delineated as a mineral resource. See end note #1 and Appendix A for additional details including assay results for the significant intercepts.

2017 Step Out

Holes

Mill Canyon StockPre-mineral Intrusive Rock

5.2m @ 14.4 g/t

5.8m @ 10.9 g/t14.3m @ 31.7 g/t5.8m @ 49.6 g/t

8.4m @ 30.6 g/t

2017 Tightened

Drill spacing

GOLDRUSH

LegendDrillhole with >3m @ 5g/tDrillholeResource Footprint

Barrick Nevada Investor Tour | 25

0 miles 1 2 3 4 5

Pipeline

Cortez Hills OP

Gold Acres

Cortez Pits

Cortez Hills UG

Cortez Pits

Cortez HillsCrossroads

Gold Acres

Gold Acres Pit Expansion

Additional Pipeline andCrossroads Phases Expansion of Pediment

Area of Cortez Hills

Expansion of the Cortez/F-Canyon Pits

Current Optionality

Pipeline

Barrick Nevada Investor Tour | 26

Waste rock dump cutback at Crossroads open pit complete and stripping second 50 foot alluvial bench

Advancing Phase I of Crossroads

Barrick Nevada Investor Tour | 27

Acquisition from Coral GoldDeal closed June 7, 2017Cash consideration of US$15.75 MReturn of 4.15 M common shares Sliding scale 1% to 2.25% NSRShallow, open pit, non-refractory oreRobertson part of a large land package spanning ~8,480 acres

Robertson Property

Pipeline

Cortez Hills OP

Gold Acres

Cortez Pits

0 miles 1 2 3 4 5

Barrick Cortez Property

Barrick Cortez Property

Process Facilities

Barrick Nevada Investor Tour | 28

Growth, extends mining and milling life for Barrick NevadaRealize synergies with the neighboring Cortez operationRobertson deposit located 4 miles north of the Cortez Pipeline MillExpected to fill gap in mill feed to oxide Cortez Pipeline Mill in ~2025Extends Cortez Pipeline Mill life to enable processing of Deep South UG Oxide OrePotential for exploration upside in untested areasLow estimated construction capital

Cortez Hills Open Pit

Robertson Exploration

Barrick Nevada Investor Tour | 29

50 miles northeast of ElkoNorth America’s largest gold mining operation40 Moz produced to date1,700 jobsNew projects at Arturo and Meikle Expansion

Process, Autoclave,Truckshop and Admin.

Betze-PostOpen Pit

Roaster

Meikle UG

Arturo

0 miles 1 2 3

LasVegas

Reno

Elko

Carson City

N E V A D A

Goldstrike

2016 Reserves

Proven 6.1 Moz1

(3.29 g/t, 57.5M tonnes)

Probable 2.0 Moz1

(4.70 g/t, 13.2M tonnes)

1. See endnote #1

Barrick Nevada Investor Tour | 30

1918 Exploration activity in area for antimony1946 Bootstrap discovered as gold deposit (Newmont)1962 Goldstrike discovered by Atlas1975 Polar Res. delineates No. 9 and Diorite deposits 1976 Polar & Pancana start small heap leach 3,200 ozs.1978 Western States enters in 50/50 JV with Pancana1982 Post discovered, 110M tons containing 3.5M ozs.1987 American Barrick acquires Goldstrike for $62M 1987 Betze and Screamer discovered 1988 Rodeo and Meikle discovered1990 Commissioned first autoclaves1996 Underground production begins2000 Commissioned roaster2006 Goldstrike produced 30 millionth ounce2012 25th Anniversary – Produced 40 millionth ounce2015 TCM Commercial Production2016 20th Anniversary – Meikle production

Barrick Nevada Investor Tour | 31

Underground potential additions in color– East Banshee / Meikle Contact / Barrel Dike /

West Banshee / Griffin 3880 / Extension / Ren

Open pit potential additions– Arturo & Other near mine opportunities

Identified 30 targets for Minex work

A

A1

Long Section A – A1 Betze Post Open PitMeikle Underground

Barrick Nevada Investor Tour | 32

Permitting for Betze-Post 5NW layback underwayAdded production from Arturo open pit to mine planAdditional Phases of Arturo utilizing existing mine equipment Mining and process facilities are permittedUnder evaluation– Leach pad feasibility / Economics /

Recoveries / Mining costs / In-pit backfill (backfilling not permitted)

Mining will expose new geology and potential deep UG exploration targets

Phase 1 Expl. TargetPhase 2 Mining complete July 2017

Phase 3 Expl. Target

Arturo

Betze-Post

5NW3NW

4NW

Barrick Nevada Investor Tour | 33

Evolving ore types dictate changing processes– Oxide heap leach and milling – Autoclaving for single refractory– Roasting for double refractory– TCM circuit for lower grade double

refractory ore

Currently processing TCM-Acid and Double Refractory RoasterTCM developed to treat double refractory ore stockpiled to dateBrings production forward and improves total mine economics 1987 1992 1997 2002 2007 2012 2017 2022 2027

Oxide

Single RefractoryAutoclave Double

Refractory Roaster

TCM-Acid Ore

Annual Gold Production (by process)

TCM-Alkaline Ore

CURRENT

Barrick Nevada Investor Tour | 34

TechnicalCost efficienciesEnabling technologiesLogistical improvementsLOM planning

OrganicExtending existing minesAdding new ore bodies to plan

PartneringNew ore bodiesNew process infrastructureOre swapping and tolls

Barrick Nevada Investor Tour | 35

ADDITIONAL INFORMATION

Barrick Nevada Investor Tour | 36

Tonnes Grade Contained(as of Dec. 31/16) (000s) (g/t) (000s oz)

P&P Reserves 221,687 2.57 18,297

Proven Reserves 73,665 2.90 6,875

Probable Reserves 148,022 2.40 11,422

Measured Resources 4,512 4.36 632

Indicated Resources 35,055 2.63 2,967

Inferred Resources 15,651 2.21 1,112

1. See endnote #1. Based on Barrick’s Cortez and Goldstrike mines as reported on pages 25-35 of Barrick’s 2016 Form 40- F/Annual Information Form.

Barrick Nevada Investor Tour | 37

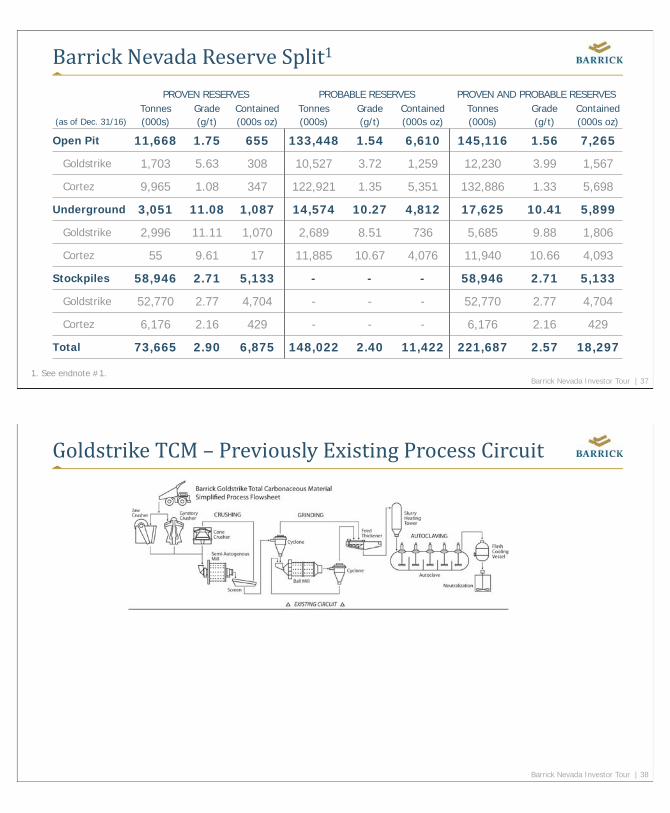

PROVEN RESERVES PROBABLE RESERVES PROVEN AND PROBABLE RESERVESTonnes Grade Contained Tonnes Grade Contained Tonnes Grade Contained

(as of Dec. 31/16) (000s) (g/t) (000s oz) (000s) (g/t) (000s oz) (000s) (g/t) (000s oz)

Open Pit 11,668 1.75 655 133,448 1.54 6,610 145,116 1.56 7,265

Goldstrike 1,703 5.63 308 10,527 3.72 1,259 12,230 3.99 1,567

Cortez 9,965 1.08 347 122,921 1.35 5,351 132,886 1.33 5,698

Underground 3,051 11.08 1,087 14,574 10.27 4,812 17,625 10.41 5,899

Goldstrike 2,996 11.11 1,070 2,689 8.51 736 5,685 9.88 1,806

Cortez 55 9.61 17 11,885 10.67 4,076 11,940 10.66 4,093

Stockpiles 58,946 2.71 5,133 - - - 58,946 2.71 5,133

Goldstrike 52,770 2.77 4,704 - - - 52,770 2.77 4,704

Cortez 6,176 2.16 429 - - - 6,176 2.16 429

Total 73,665 2.90 6,875 148,022 2.40 11,422 221,687 2.57 18,297

1. See endnote #1.

Barrick Nevada Investor Tour | 38

Barrick Nevada Investor Tour | 39

Barrick Nevada Investor Tour | 40

Barrick Nevada Investor Tour | 41

Barrick Nevada Investor Tour | 42

Construction completed January 2015 at capital cost $610 million

Surpassed design production targets in Q2 2017– Currently processing acid ore, available

through Q2 2019– Trialling alkaline ore on a quarterly basis

starting in H2 2017

Alkaline ore impacts recovery negatively– Research ongoing at lab and plant scale

with respect to both autoclaving and CaTS leaching

– Alkaline ore variable cost per ton is ~34% lower than acid ore

Resin in leach Circuit

Reagent Recycle/Water Treatment

Thiosulphate Plant

AUTOCLAVES

Gold Elution

Barrick Nevada Investor Tour | 43

Mill Throughput(tons per operating hour)

562

554 558

546

576

566 566

593

571

565

620

May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar2016 2017

500May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2016 2017

TCM Recovery Rate(percent)

50

59.7

70.8

68.2 67.6

60.6

66.1 66.8

58.0

54.3

67.8

63.5

12 MonthRolling Avg.

Barrick Nevada Investor Tour | 44

Technology RefinementDesign defect eliminationMill throughput enhancementsReliability enhancementsStockpile analysis and validation

Best-in-ClassWTP modifications completeIncreased throughput by 80+ TPOH8.8% improvement in availabilityUnderstanding chemical impacts of acid vs alkaline ore

Barrick Nevada Investor Tour | 45

Cyanide free processing provides optionality to Barrick in jurisdictions where this is required

Allows Barrick to competitively explore for and exploit complex orebodies

Patented technology protects intellectual property and provides future revenue stream if leased

Barrick Nevada Investor Tour | 46

1 All significant intercepts calculated using a 5.0 g/t Au cutoff and are uncapped; internal dilution is less than 20% total width.2 True width of intercepts are uncertain at this stage.

A plan view DEM Hillshade image of Fourmile drilling showing significant intercepts as of February 9, 2017. Drill holes in red are high grade intercepts greater than 3.0 meters at greater than 5.0 gpt. The significant intercepts presented were calculated using a 5.0 g/t Au cutoff with internal dilution of no more than 20% included in the calculation. No capping grade was used to calculate the significant intercepts.

The drilling results for the Fourmile property contained in this presentation have been prepared in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects. All drill hole assay information has been manually reviewed and approved by staff geologists and re-checked by the project manager. Sample preparation and analyses are conducted by an independent laboratory. Procedures are employed to ensure security of samples during their delivery from the drill rig to the laboratory. The quality assurance procedures, data verification and assay protocols used in connection with drilling and sampling on the Fourmileproperty conform to industry accepted quality control methods.

Fourmile – Significant Intercepts1 GRC 0427D, GRC 0435D, FM16 05D, and FM16 10D

Core Drill Hole Azimuth Dip Interval (m) Width (m)2 Au (g/t)

GRC-0427D NA -90

666.9-672.7 5.8 10.9

695.3-709.6 14.3 31.8

921.4-927.2 5.8 49.6

GRC-0435D NA -90 702.2-707.4 5.2 14.4

FM16-05D NA -90 705.6-714.0 8.4 30.6

FM16-10D 357 -77 730.6-733.6 3.0 5.7

Barrick Nevada Investor Tour | 47

APPENDIX B –

Barrick Nevada Investor Tour | 48

Barrick Nevada

Tonnes Mined(000s)

Barrick NevadaTotal

Barrick NevadaGoldstrike

Barrick Nevada Cortez

2016 2015 2014 2016 2015 2014 2016 2015 2014

Total 192,753 223,661 233,556 67,834 72,304 81,410 124,919 151,357 152,146

Open Pit 189,941 221,501 231,369 66,040 70,836 79,807 123,901 150,665 151,562

Underground 2,812 2,160 2,187 1,794 1,468 1,603 1,018 692 584

APPENDIX B

Barrick Nevada Investor Tour | 49

Barrick Nevada

Average Mined Grade(grams/tonne)

Barrick NevadaTotal

Barrick NevadaGoldstrike

Barrick Nevada Cortez

2016 2015 2014 2016 2015 2014 2016 2015 2014

Open Pit Mined 1.74 1.87 1.43 5.74 4.17 4.67 1.30 1.06 0.62

Underground Mined 11.39 13.40 13.02 9.85 9.58 8.84 14.48 21.49 24.48

Processed 2.62 2.72 2.18 5.65 6.01 6.28 1.73 1.73 1.34

APPENDIX B

Barrick Nevada Investor Tour | 50

Barrick Nevada

Tonnes Processed (000s)

Barrick NevadaTotal

Barrick NevadaGoldstrike

Barrick Nevada Cortez

2016 2015 2014 2016 2015 2014 2016 2015 2014

Total 32,473 29,158 31,264 7,361 6,752 5,307 25,112 22,406 25,957

Oxide Mill 4,197 3,476 3,727 18 - - 4,179 3,476 3,727

Roasters 4,789 5,050 5,187 3,928 4,232 4,432 861 818 755

Autoclave 3,503 2,605 1,024 3,415 2,520 875 88 85 149

Heap Leach 19,984 18,027 21,326 - - - 19,984 18,027 21,326

APPENDIX B

Barrick Nevada Investor Tour | 51

Barrick Nevada

Cost per Tonnes Processed ($/tonnes)

Barrick Nevada

2016 2015 2014

Oxide Mill 12 13 12

Roasters 24 25 26

Autoclave 60 62 92

Heap Leach 0.97 1.17 1.40

APPENDIX B

Barrick Nevada Investor Tour | 52

Barrick Nevada

Recovery Rate(%)

Barrick Nevada

2016 2015 2014

Total 79% 80% 82%

Oxide Mill 88% 87% 84%

Roasters 90% 89% 86%

Autoclave 63% 59% 75%

APPENDIX B

Barrick Nevada Investor Tour | 53

Barrick Nevada

Production (k ounces)

Barrick Nevada

2016 2015 2014

Total 2,155 2,052 1,804

Oxide Mill 569 530 468

Roasters 1,115 1,177 963

Autoclave 242 204 148

Heap Leach 229 141 225

APPENDIX B

Barrick Nevada Investor Tour | 54

Barrick Nevada

Production Costs($/oz)

Barrick Nevada

2016 2015 2014

Cost of Sales 876 782 755

Operating Costs 477 477 505

Royalties and production taxes 25 27 31

Cash Cost1 502 504 536

Depreciation 372 270 219

Total Production Costs 874 774 755

All-in Sustaining Costs1 618 631 782

1. These are non-GAAP financial performance measures with no standardized meaning under IFRS and therefore may not be comparable to similar measures of performance presented by other issues. For further information and a detailed reconciliation of the non-GAAP measures used in this slide to the most directly comparable IFRS measure, please see Appendix C

APPENDIX B

Barrick Nevada Investor Tour | 55

Barrick Nevada

Capital Expenditures ($ millions)

Barrick Nevada

2016 2015 2014

Minesite Sustaining Capex 217 211 416

Project Capex 111 145 331

Total Capital Expenditures 328 356 747

APPENDIX B

Barrick Nevada Investor Tour | 56

1. Estimated in accordance with National Instrument 43-101 as required by Canadian securities regulatory authorities. Estimates are as of December 31, 2016, unlessotherwise noted. For United States reporting purposes, Industry Guide 7 under the Securities and Exchange Act of 1934 (as interpreted by Staff of the SEC),applies different standards in order to classify mineralization as a reserve. Complete mineral reserve and mineral resource data for all mines and projectsreferenced in this presentation, including tonnes, grades, and ounces, can be found on pages 25-35 of Barrick’s 2016 Form 40- F/Annual Information Form.

The following qualified persons, as that term is defined in National Instrument 43-101 – Standards of Disclosure for Mineral Projects, have reviewed and approved therelevant scientific and technical information contained in this presentation: Rob Krcmarov, Executive Vice President Exploration and Growth of Barrick, Rick Sims,Registered Member SME, Senior Director, Resources and Reserves of Barrick, Patrick Garretson, Registered Member SME, Senior Director, Life of Mine Planning ofBarrick and Steven Haggarty, P. Eng., Senior Director, Metallurgy of Barrick.

AAppendix C – Reconciliation of Gold Cost of Sales to Cash costs, All-in sustaining costs and All-in costs, including on a per ounce basis

"Cash costs" per ounce and "All-in sustaining costs" (also referred to as “AISC”) per ounce are non-GAAP financial performance measures. “Cash costs” start with our cost of sales related to gold production and removes depreciation, the non-controlling interest of cost of sales and includes by-product credits. “All-in sustaining costs” start with “cash costs” and include sustaining capital expenditures, general & administrative costs, minesite exploration and evaluation costs and reclamation cost accretion and amortization. Barrick believes that the use of "cash costs" per ounce and "all-in sustaining costs" per ounce will assist investors, analysts and other stakeholders in understanding the costs associated with producing gold, understanding the economics of gold mining, assessing our operating performance and also our ability to generate free cash flow from current operations and to generate free cash flow on an overall Company basis. "Cash costs" per ounce and "All-in sustaining costs" per ounce are intended to provide additional information only and do not have any standardized meaning under IFRS. Although a standardized definition of all-in sustaining costs was published in 2013 by the World Gold Council (a market development organization for the gold industry comprised of and funded by 18 gold mining companies from around the world, including Barrick), it is not a regulatory organization, and other companies may calculate this measure differently. These measures should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS. Further details on these non-GAAP measures are provided in the MD&A accompanying Barrick's financial statements filed from time to time on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

($ millions, except per ounce information in dollars) For the years ended December 31

Footnote 2016 2015 2014

Cost of sales related to gold production $ 1,896 $ 1,551 $ 1,340

Depreciation (807) (537) (389)

By-product credits 1 (2) (2) (1)

Non-recurring items 2 - (12) -

Non-controlling interests - - -

Cash costs $ 1,087 $ 1,000 $ 950

General & administrative costs - - -

Minesite exploration and evaluation costs 3 10 12 3

Minesite sustaining capital expenditures 4 217 211 415

Rehabilitation - accretion and amortization (operating sites) 5 26 27 19

Non-controlling interests (4) - -

All-in sustaining costs $ 1,336 $ 1,250 $ 1,387

Project exploration and evaluation and project costs 3 19 40 68

Project capital expenditures 4 141 159 319

Non-controlling interests (30) (31) (5)

All-in costs $ 1,466 $ 1,418 $ 1,769

Ounces sold - equity basis (000s ounces) 2,162 1,981 1,773

Cost of sales per ounce 6,7 $876 $782 $755

Cash costs per ounce 7 $ 502 $ 504 $ 536

Cash costs per ounce (on a co-product basis) 7,8 $ 503 $ 505 $ 537

All-in sustaining costs per ounce 7 $ 618 $ 631 $ 782

All-in sustaining costs per ounce (on a co-product basis) 7,8 $ 619 $ 632 $ 783

All-in costs per ounce 7 $ 678 $ 715 $ 998

All-in costs per ounce (on a co-product basis) 7,8 $ 679 $ 716 $ 999

1 By-product credits

Revenues include the sale of by-products for our gold mines.

2 Non-recurring items

Non-recurring items in 2015 consist of $12 million of costs arising from a change in our supplies inventory obsolescence provision. These costs are not indicative of our cost of production and have been excluded from the calculation of cash costs.

3 Exploration and evaluation costs

Exploration, evaluation and project expenses are presented as minesite sustaining if it supports current mine operations and project if it relates to future projects.

4 Capital expenditures

Capital expenditures are related to our gold sites only and are presented on a 100% accrued basis. They are split between minesite sustaining and project capital expenditures. Project capital expenditures are distinct projects designed to increase the net present value of the mine and are not related to current production. Significant projects in the current year are Arturo and Cortez Lower Zone.

5 Rehabilitation - accretion and amortization

Includes depreciation on the assets related to rehabilitation provisions of our gold operations and accretion on the rehabilitation provision of our gold operations, split between operating and non-operating sites.

6 Cost of sales per ounce

Cost of sales related to gold per ounce is calculated using cost of sales on an attributable basis (removing the non-controlling interest from cost of sales), divided by attributable gold ounces.

7 Per ounce figures

Cost of sales per ounce, cash costs per ounce, all-in sustaining costs per ounce and all-in costs per ounce may not calculate based on amounts presented in this table due to rounding.

8 Co-product costs per ounce

Cash costs per ounce, all-in sustaining costs per ounce and all-in costs per ounce presented on a co-product basis remove the impact of by-product credits of our gold production (net of non-controlling interest) calculated as:

($ millions) For years ended December 31

2016 2015 2014

By-product credits $ 2 $ 2 $ 1

Non-controlling interest - - -

By-product credits (net of non-controlling interest) $ 2 $- $ 1

Barrick Nevada

Investor Tour | June 20-21, 2017

Digital EnterpriseTransformation

Strategy

Digital Enterprise Transformation Strategy

Investors Visit

20 June 2017

2Barrick

Our Strategic Intent is to transform Barrick into a Digital Enterprise

Substantial effort has been made in 2016 and Q1 2017 to initiate digital Barrick transformation

Multiple quick-wins achieved in Cortez test-site, under-time and under-budget.

Achieved significant levels of buy-in at every level of leadership.

Proven value of in-house product design system (CodeMine)

Early adoption of ‘Agile’ methods

Identified the value-adding and transformational potential of digital across the whole enterprise

An agile, highly productive, safe, environmentally friendly, socially responsible, and low cost digital enterprise that leverages technology and data as a competitive advantage.

“A tech company that does mining not a mining company that does tech”

3Barrick 3

Barrick is now moving from Digital Projects to Setting up the Digital Organization

SOURCE: Digital McKinsey

Digital Maturity for Companies

Initial initiatives Digital projects Derive vision and

overarching transformation roadmapCentralize projects Build up digital capabilities

Digital business contributes substantially to revenueDigital is integral to corporate design andoperations"Digital culture" is embraced

Digital is dominant corporate element Full digital organization with jointly drawn digital resources

DES

CR

IPTI

ON

Isolated initiatives in various areas Largely uncoor-dinated activities, no budgets

Set up digital orgEstablished digital org

Digital enterprise

Initial creation of transparency over existing initiatives Prioritization and first efforts to bundle activities into projects

OR

GA

NIZ

ATIO

N

Build up digital or-ganization including dedicated digital owners e.g. CDO Transform head-office functions, reducing central costs

Established digital organizationIncreased investment in innovation now possible

CDO organization removedDigital integral to all competency profiles

No dedicated digital unit

Small competence center Projects still managed by units

12

34

5

Moving from step to step in digital maturity requires transformational effort to succeed

4Barrick

What are our transformation

Principles1. 21st Century technology at every level

2. Built for miners by miners

3. Change the culture - every function will change.

4. Provide data and analytics insight at every level of the business

5. Achieve dominance of our data governance, privacy and security

6. Relentless pursuit of excellence

55

User-Centric Design Thinking ensures front-line input & buy-in

Design Thinking is a user-centered problem solving approach. It starts with an ideal or vision of what we need, and we work backwards to build a solution that gets us there. We balance user needs with business goals.

Here (1) Joe discusses the day’s plan with the team using paper maps of the mine. In the truck, Joe has a duplicate set of paper maps (2) that help him navigate from place to place to check progress. He has a planned route, but can get redirected via radio calls which are constant in the background. Joe describes his job as a Supervisor as being “open ended” after a certain point. After morning meetings and predefined planning for the day, anything can happen. This (3) was an impromptu meeting about how to address an issue in a heading.

1 2

3

By spending time with the frontline and creating ‘user councils’, we gain empathy for and a deep understanding of their daily pain points

77

Insights come from walkthroughs of major processes like Maintenance, seeing what workers experience every day

8

Start with the minimal viable product (covering 80% of customers)

Evolve over time for what we really need

Rapid digitization Agile approachTraditional “waterfall” project delivery

“This is a big and long project, let's make sure we capture everything, otherwise we are never going to get it”

What we want (and would originally build)

Solutions are created using an Agile approach: focusing on the “minimal requirements” onto which new features are progressively built

9

Agile is run on 2 week sprints ensuring constant prioritization of features and control of spend

Time-boxed “Sprint” Cycles

PRODUCT OWNER SCRUM MASTER

DEVELOPMENT TEAM DEVELOPMENT TEAM Development team

DEVELOPMENT TEAM

Time-boxedTest/Develop(No changes)

WORKING CODE READY FOR DEPLOYMENT

Sprint Planning Review product backlogEstimate sprint backlogCommit

Daily Stand upProgress since last stand upPlan for todayRoadblocks/Impediments?

Sprint Review Demo features to allRetrospective on the improving next sprintMake investment decision

Sprint RetrospectiveDone after each sprintAims to improve the process for next sprint

Sprint BacklogFeatures for a SprintEstimated by teamTeam commitment

Product BacklogUser-focused prioritized product features

Product Backlog Sprint Backlog

1011010011101000

The CodeMine creates a comfortable space for operators, executives and digital developers to collaborate in a natural way otherwise difficult in a traditional office or field context. In addition to facilitating collaboration, the CodeMine replicates a “Silicon Valley” environment that inspires innovation and creativity

11100001

We constructed this collaborative space to enable our digital transformation

s to collaborate in a natural way

Barrick Nevada

Investor Tour | June 20-21, 2017

Analytics andUnified Operations

Center

DIG

ITA

L TR

AN

SFO

RM

ATI

ON

AN

D

INN

OV

ATI

ON

IN N

EVA

DA

AN

ALY

TICS

AN

D U

NIF

IED

O

PERA

TIO

NS

CEN

TER

(AU

OPS

)

WH

AT

IS T

HE

AU

OPS

CEN

TER

?

The

Bar

rick

Nev

ada

An

alyt

ics

and

Un

ifi e

d

Ope

rati

ons

(AU

Ops

) C

ente

r w

ill g

et t

he r

ight

info

rmat

ion

to t

he r

ight

peo

ple

at t

he r

ight

tim

e to

en

hanc

e de

cisi

on-m

akin

g. It

wil

l

impr

ove

the

Com

pany

’s ab

ilit

y to

iden

tify

and

capi

tali

ze o

n o

ppor

tun

itie

s th

at m

itig

ate

risk

s

acro

ss o

pera

tion

s, h

ealt

h an

d sa

fety

and

the

envi

ron

men

t or

impr

ove

reve

nue

and

dri

ve

cost

-sav

ings

– a

ll in

rea

l or

near

-rea

l tim

e.

WH

AT

ARE

TH

E BE

NEF

ITS?

Eas

y-to

-rea

d vi

sual

s an

d gr

aph

ics

wil

l allo

w

anal

ysts

loca

ted

at t

he c

ente

r to

und

erst

and

how

min

ing

oper

atio

ns

are

perf

orm

ing

and

dri

ll do

wn

into

dat

a to

exa

min

e w

hat i

s d

rivi

ng

thos

e re

sult

s, d

evel

opin

g ac

tion

able

insi

ghts

muc

h m

ore

quic

kly.

An

alys

ts c

an t

hen

dec

ide

who

to c

onta

ct a

t the

ope

rati

ons,

fro

m f

ront

line

oper

ator

s to

sit

e ge

nera

l man

ager

s, w

ith

rele

vant

info

rmat

ion

and

adv

ise

them

acc

ord

ingl

y. T

his

give

s th

e C

ompa

ny r

eal-

tim

e ca

pabi

lity

to k

now

wha

t act

ion

s ar

e be

ing

take

n a

nd t

he p

oten

tial

impa

cts

of t

hose

act

ion

s.

BELO

W A

RE A

FEW

EX

AM

PLES

O

F H

OW

AU

OPS

WIL

L EN

HA

NCE

D

ECIS

ION

-MA

KIN

G.

•

Hea

lth

an

d s

afet

y al

erts

wil

l pop

up

on s

cree

n to

ind

icat

e th

e se

riou

snes

s of

a

situ

atio

n a

nd a

ctio

ns

requ

ired

to r

esol

ve

it. I

t wil

l dis

play

the

impa

ct to

cos

t and

tim

e an

d pr

oduc

e an

act

ion

log

for

use

as

a sy

stem

of r

ecor

d.

•

Pred

icti

ve a

nal

ysis

wil

l tri

gger

an

ala

rm

base

d on

the

pro

babi

lity

of e

quip

men

t

failu

re. I

t wil

l dis

play

the

cos

t to

repl

ace

equ

ipm

ent n

ow v

ersu

s th

e co

st to

rep

lace

it if

de-

prio

riti

zed.

•

Pred

icti

ve c

on

sum

able

s w

ill t

rigg

er

an a

larm

bas

ed o

n a

n o

verr

un

of a

mea

sure

d co

nsu

mab

le. T

his

wou

ld p

rom

pt

a d

iscu

ssio

n b

etw

een

an

an

alys

t and

an

oper

ator

or

supe

rvis

or to

und

erst

and

the

impa

ct o

f the

ir a

ctio

ns.

•

Pro

du

ctio

n s

tatu

s w

ill d

ispl

ay

perf

orm

ance

acr

oss

oper

atin

g te

ams,

iden

tify

the

equ

ipm

ent t

hey

are

usi

ng a

nd

mon

itor

key

per

form

ance

ind

icat

ors

and

perf

orm

ance

met

rics

. Th

is w

ill h

elp

to

iden

tify

team

s th

at a

re p

erfo

rmin

g w

ell a

nd

dri

ve b

est-

in-c

lass

ope

rato

r pe

rfor

man

ce.

To le

arn

mor

e ab

out

Barri

ck’s

digi

tal

trans

form

atio

n, p

leas

e sc

an th

e Q

R Co

de to

visi

t ou

r web

site.

HO

W A

U O

PS W

ORK

S

Barrick Nevada

Investor Tour | June 20-21, 2017

Cortez Hills Underground:Impact Drivers

IMPACT DRIVERS

Achieving impact through SIC at Cortez UG involves two main im-provements composed of several drivers

Beginning of shift Reduced time locating equipment Decrease length of lineout meeting Minimize time travelled from admin to UG

Effectiveshiftlength

Through-put

Impact

During shift Shorten of operator’s breaks

End of shiftEnsure operators are tasked until EOD Minimize travel from UG to admin

Improved bottleneck management

Improved reaction to unpredicted tasks

Increase traffic flow

a

b

c

d

f

e

PRODUCTION METRICS

UG – Total Feet Advanced

0

200

400

600

800

1000

1200

3/24/2017 3/31/2017 4/7/2017 4/14/2017 4/21/2017 4/28/2017 5/5/2017 5/12/2017 5/19/2017 5/26/2017 6/2/2017 6/9/2017

Feet

Adv

ance

d

Sum of Advance

Sum of Footage Target

4 per. Mov. Avg. (Sum of Advance)

UG – Development Feet

0

50

100

150

200

250

300

350

400

450

500

3/24/2017 3/31/2017 4/7/2017 4/14/2017 4/21/2017 4/28/2017 5/5/2017 5/12/2017 5/19/2017 5/26/2017 6/2/2017 6/9/2017

Development Feet

Sum of DevFeet

Sum of Dev Ft Target

4 per. Mov. Avg. (Sum of DevFeet)

UG – Mining Type

0

100

200

300

400

500

600

3/24/2017 3/31/2017 4/7/2017 4/14/2017 4/21/2017 4/28/2017 5/5/2017 5/12/2017 5/19/2017 5/26/2017 6/2/2017 6/9/2017

Sum of DrillFillFeet

4 per. Mov. Avg. (Sum of DrillFillFeet)

0

50

100

150

200

250

3/24/2017 3/31/2017 4/7/2017 4/14/2017 4/21/2017 4/28/2017 5/5/2017 5/12/2017 5/19/2017 5/26/2017 6/2/2017 6/9/2017

Stope Feet

Sum of StopeFeet

Sum of Stope Dev Target

4 per. Mov. Avg. (Sum of StopeFeet)

UG – Backfill (CRF)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

3/24/2017 3/31/2017 4/7/2017 4/14/2017 4/21/2017 4/28/2017 5/5/2017 5/12/2017 5/19/2017 5/26/2017 6/2/2017 6/9/2017

CRF

Tons

Sum of CRF

Sum of CRF Target

4 per. Mov.Avg. (Sum of CRF)

PRODUCTION METRICS

UG – Drill - Availability

0

10

20

30

40

50

60

70

80

90

100

3/24/2017 3/31/2017 4/7/2017 4/14/2017 4/21/2107 4/28/2017 5/5/2017 5/12/2017 5/19/2017 5/26/2017 6/2/2017 6/9/2017

% A

vaila

ble

Bolter

Average of BolterAvail

Average of BolterAvail

4 per. Mov. Avg. (Average of BolterAvail)

0

10

20

30

40

50

60

70

80

90

100

3/24/2017 3/31/2017 4/7/2017 4/14/2017 4/21/2107 4/28/2017 5/5/2017 5/12/2017 5/19/2017 5/26/2017 6/2/2017 6/9/2017

% A

vaila

ble

Jumbo

Average of JumboAvail

Average of Drill Avail Target

4 per. Mov. Avg. (Average of JumboAvail)

UG – Loader/Truck - Availability

75

80

85

90

95

100

3/24/2017 3/31/2017 4/7/2017 4/14/2017 4/21/2017 4/28/2017 5/5/2017 5/12/2017 5/19/2017 5/26/2017 6/2/2017 6/9/2017

% A

vaila

ble

Loader

Average of LoaderAvail

Average of Loader Avail Tgt

4 per. Mov. Avg. (Average of LoaderAvail)

0

10

20

30

40

50

60

70

80

90

100

3/24/2017 3/31/2017 4/7/2017 4/14/2017 4/21/2017 4/28/2017 5/5/2017 5/12/2017 5/19/2017 5/26/2017 6/2/2017 6/9/2017

% A

vaila

ble

Trucks

Average of TruckAvail

Average of Truck Avail Tgt

4 per. Mov. Avg. (Average of TruckAvail)

UG – Drill/Bolter – Utilization

0

10

20

30

40

50

60

70

80

90

100

3/24/2017 3/31/2017 4/7/2017 4/14/2017 4/21/2017 4/28/2017 5/5/2017 5/12/2017 5/19/2017 5/26/2017 6/2/2017 6/9/2017

Bolter

0

10

20

30

40

50

60

70

80

90

100

3/24/2017 3/31/2017 4/7/2017 4/14/2017 4/21/2017 4/28/2017 5/5/2017 5/12/2017 5/19/2017 5/26/2017 6/2/2017 6/9/2017

Jumbo

per/. Mov. Avg. (Average of

UG – Loader/Truck – Utilization

0

10

20

30

40

50

60

70

80

90

100

3/24/2017 3/31/2017 4/7/2017 4/14/2017 4/21/2017 4/28/2017 5/5/2017 5/12/2017 5/19/2017 5/26/2017 6/2/2017 6/9/2017

Loader

0

10

20

30

40

50

60

70

80

90

100

3/24/2017 3/31/2017 4/7/2017 4/14/2017 4/21/2017 4/28/2017 5/5/2017 5/12/2017 5/19/2017 5/26/2017 6/2/2017 6/9/2017

Truck

WHAT IS SIC?

What is SIC?

Short Interval Control (SIC) is ensuring compliance to a detailed schedule of tasks and results. This is done by supervising the production in real-time and adjusting schedules as events occur during the shift.

Why are we doing this?

How is this going to affect me?

Higher production, lower costs, job security through extended mine life, developing a new skillset by being part of one of newest technological advances in mining, total familiarization with a system that soon will be a standard through-out mining and a safer work environment.

This system is just a tool to help safety, increase production,and efficiency. These are enhanced by availability of more accurate information, ability to make and communicate changes in real time, and reduced reaction time.

WAIT TIME

487

990

557282

1,649922

478

81

159 4422504773113

181233515

15:00-20:00

10:00-15:00

1,035

35:00-40:00

25:00-30:00

123

30:00-35:00

20:00-25:00

103

>40:00

69

147

194340

2,136

5:00-10:00

2:00-5:00

1,912

Number of Wait time for Haul trucks1

# - Count

1 Data excludes wait time under 2 min or above 2 hours

Average Daily Wait Time1 for Haul truck- 2017 Min

Wait time has been trending downward since MOC-C has been staffed and tablet issues have been minimized

2400+ instances where wait time has exceed more than 15 minutes

Avg wait at batch plant is 9:26

Avg. wait at loader 11:01

At Batchplant Other

0:00:00

0:02:53

0:05:46

0:08:38

0:11:31

0:14:24

0:17:17

0:20:10

0:23:02

5/17

/201

75/

18/2

017

5/19

/201

75/

20/2

017

5/21

/201

75/

22/2

017

5/23

/201

75/

24/2

017

5/25

/201

75/

26/2

017

5/27

/201

75/

28/2

017

5/29

/201

75/

30/2

017

5/31

/201

76/

1/20

176/

4/20

176/

5/20

176/

6/20

176/

7/20

176/

8/20

176/

9/20

176/

10/2

017

6/11

/201

7 6/

12/2

017

6/13

/201

7

Avg. wait time: 10:46

SHIFT EXTENDER

-

4/3/20

17

4/6/20

17

4/9/20

17

4/12/2

017

4/15/2

017

4/18/2

017

4/21/2

017

4/24/2

017

4/27/2

017

4/30/2

017

5/3/20

17

5/6/20

17

5/9/20

17

5/12/2

017

5/15/2

017

9:57:36

10:04:48

10:12:00

10:19:12

10:26:24

10:33:36

10:40:48

10:48:00

5/6/20

17

5/7/20

17

5/8/20

17

5/9/20

17

5/10/2

017

5/12/2

017

5/13/2

017

5/14/2

017

5/15/2

017

5/16/2

017

Avg. Shift Length for Haul TrucksTime

Daily production - 3 Day Rolling Avg. Tons per day

Avg. daily production has increased Inadequate data to monitor trends

Current avg. is same as avg. YTD shift length from Jigsaw

Avg. Shift length:10:22

OPERATOR EXCELLENCE: BOLTS BY CREW

5,490

3,384

4,3364,0474,475

3,954

2,673

3,994

7,280

5,9836,065

5,179

3,383

2,468

5,0694,876

AprFeb Mar May

Crew B Crew C Crew A Crew D Bolts1 installed by crew per month in 2017 Number of Bolts

1 8' bolts only. Excluding 12' & 16' bolts

OPERATOR EXCELLENCE: JUMBO

4,614

2,328

3,643

1,981

3,5553,400

2,336

3,608

4,844

4,0594,391

4,0634,423

3,556

4,662

3,354

AprFeb Mar May

Crew B Crew C Crew A Crew D Total Feet drilled by crew per month in 2017 Feet

List all operators

10

3040

60

80

50

0

70

20

Crew D Crew C Crew B Crew A

Buckets per operating hours Buckets per hour

By operator By crew

# of buckets # of buckets

OPERATOR EXCELLENCE: MUCKER

List alloperators

10

3040

60

80

50

0

70

20

Crew DCrew CCrew BCrew A

Buckets per operating hoursBuckets per hour

By operator By crew

# of buckets # of buckets

8

16

1210 10

18

1412

0

10

5

20

15

Miner 4 Miner 1 Miner 2 Miner 3

56

70

5450

6575

6260

OPERATOR EXCELLENCE: TRUCKS

8

1612

10 10

1814

1210

20

15

5

0Miner 4 Miner 3 Miner 1 Miner 2

5670

545065

756260

80

20

0

60

40

Crew A Crew C Crew D Crew B

Loads per operating hours Loads per hour

By operator By crew

Sample Charts for Mucker

# of loads # of loads

9

67

5

1

422 2

01

6 67

89

8

0

10

2

64

Miner 1 Miner 3 Miner 4 Miner 2

Ore to Surface Waste to Surface Wastefill CRF Backfill

90

6070

5026

40

9

4560

7090

4020

8060

100

0Crew B Crew C

4060

20

Crew A

1323

Crew D

OPERATOR EXCELLENCE: BOLTS BY OPERATOR

289

2,938

5,004

3,240

4,730

300726

3,510

5,505

387746

230

3,1513,057

5,503

359

2,113

941

4,312

323

3,0553,270

963

2,518

586

1,877

324364

387

3,8834,232

Min

er 6

Min

er 1

4

Min

er 1

1

Min

er 9

Min

er 1

0

Min

er 1

5

Min

er 1

2

Min

er 1

3

Min

er 8

Min

er 7

Min

er 1

6

Min

er 1

7

Min

er 1

8

Min

er 2

0

Min

er 2

2

Min

er 1

9

Min

er 2

5

Min

er 2

3

Min

er 2

6

Min

er 2

1

Min

er 2

4

Min

er 5

Min

er 2

9

Min

er 2

8

Min

er 3

2

Min

er 2

7

Min

er 3

3

Min

er 3

4

Min

er 3

0

Min

er 3

1

Min

er 3

5

656

2,237

Min

er 4

Min

er 1

Min

er 2

Min

er 3

1,861

Min

er 3

6

1,1811,608

Bolts1 installed by operator in Feb – May 2017 Number of Bolts2

1 8' bolts only. Excluding 12' & 16' bolts 2 Excludes all operators who installed under 200 bolts

OPERATOR EXCELLENCE: LOADER

551

1070

248

1,053

796

264

1,386

1,589

1,350

758935

584460482

914

AprFeb Mar May

Crew B Crew C Crew A Crew D Total bucket by crew per month in 2017 # of buckets