Barclays PLC · Barclays Plc (Barclays) ... PPI / Average RWA (%) 2.1 1.6 1.8 1.3 0.8 1.56 ......

13

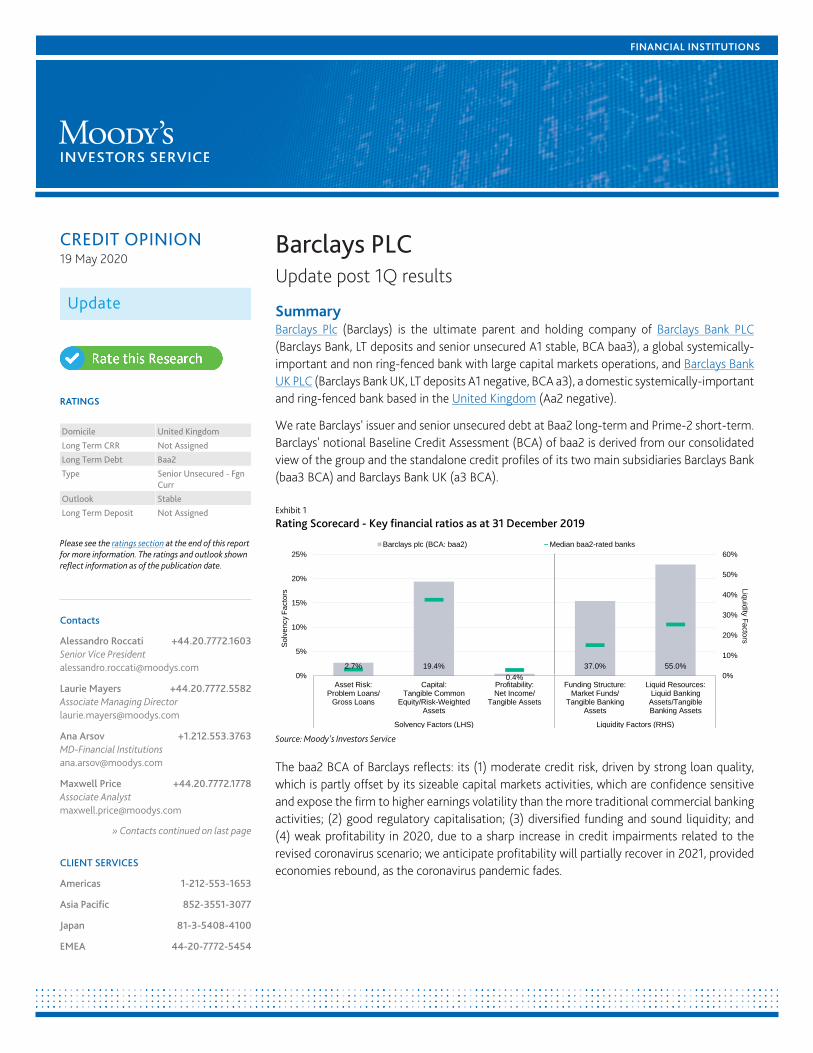

FINANCIAL INSTITUTIONS CREDIT OPINION 19 May 2020 Update RATINGS Domicile United Kingdom Long Term CRR Not Assigned Long Term Debt Baa2 Type Senior Unsecured - Fgn Curr Outlook Stable Long Term Deposit Not Assigned Please see the ratings section at the end of this report for more information. The ratings and outlook shown reflect information as of the publication date. Contacts Alessandro Roccati +44.20.7772.1603 Senior Vice President [email protected] Laurie Mayers +44.20.7772.5582 Associate Managing Director [email protected] Ana Arsov +1.212.553.3763 MD-Financial Institutions [email protected] Maxwell Price +44.20.7772.1778 Associate Analyst [email protected] » Contacts continued on last page CLIENT SERVICES Americas 1-212-553-1653 Asia Pacific 852-3551-3077 Japan 81-3-5408-4100 EMEA 44-20-7772-5454 Barclays PLC Update post 1Q results Summary Barclays Plc (Barclays) is the ultimate parent and holding company of Barclays Bank PLC (Barclays Bank, LT deposits and senior unsecured A1 stable, BCA baa3), a global systemically- important and non ring-fenced bank with large capital markets operations, and Barclays Bank UK PLC (Barclays Bank UK, LT deposits A1 negative, BCA a3), a domestic systemically-important and ring-fenced bank based in the United Kingdom (Aa2 negative). We rate Barclays' issuer and senior unsecured debt at Baa2 long-term and Prime-2 short-term. Barclays' notional Baseline Credit Assessment (BCA) of baa2 is derived from our consolidated view of the group and the standalone credit profiles of its two main subsidiaries Barclays Bank (baa3 BCA) and Barclays Bank UK (a3 BCA). Exhibit 1 Rating Scorecard - Key financial ratios as at 31 December 2019 2.7% 19.4% 0.4% 37.0% 55.0% 0% 10% 20% 30% 40% 50% 60% 0% 5% 10% 15% 20% 25% Asset Risk: Problem Loans/ Gross Loans Capital: Tangible Common Equity/Risk-Weighted Assets Profitability: Net Income/ Tangible Assets Funding Structure: Market Funds/ Tangible Banking Assets Liquid Resources: Liquid Banking Assets/Tangible Banking Assets Solvency Factors (LHS) Liquidity Factors (RHS) Barclays plc (BCA: baa2) Median baa2-rated banks Solvency Factors Liquidity Factors Source: Moody's Investors Service The baa2 BCA of Barclays reflects: its (1) moderate credit risk, driven by strong loan quality, which is partly offset by its sizeable capital markets activities, which are confidence sensitive and expose the firm to higher earnings volatility than the more traditional commercial banking activities; (2) good regulatory capitalisation; (3) diversified funding and sound liquidity; and (4) weak profitability in 2020, due to a sharp increase in credit impairments related to the revised coronavirus scenario; we anticipate profitability will partially recover in 2021, provided economies rebound, as the coronavirus pandemic fades.

Transcript of Barclays PLC · Barclays Plc (Barclays) ... PPI / Average RWA (%) 2.1 1.6 1.8 1.3 0.8 1.56 ......

FINANCIAL INSTITUTIONS

CREDIT OPINION19 May 2020

Update

RATINGS

Domicile United Kingdom

Long Term CRR Not Assigned

Long Term Debt Baa2

Type Senior Unsecured - FgnCurr

Outlook Stable

Long Term Deposit Not Assigned

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Contacts

Alessandro Roccati +44.20.7772.1603Senior Vice [email protected]

Laurie Mayers +44.20.7772.5582Associate Managing [email protected]

Ana Arsov +1.212.553.3763MD-Financial [email protected]

Maxwell Price +44.20.7772.1778Associate [email protected]

» Contacts continued on last page

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

Barclays PLCUpdate post 1Q results

SummaryBarclays Plc (Barclays) is the ultimate parent and holding company of Barclays Bank PLC(Barclays Bank, LT deposits and senior unsecured A1 stable, BCA baa3), a global systemically-important and non ring-fenced bank with large capital markets operations, and Barclays BankUK PLC (Barclays Bank UK, LT deposits A1 negative, BCA a3), a domestic systemically-importantand ring-fenced bank based in the United Kingdom (Aa2 negative).

We rate Barclays' issuer and senior unsecured debt at Baa2 long-term and Prime-2 short-term.Barclays' notional Baseline Credit Assessment (BCA) of baa2 is derived from our consolidatedview of the group and the standalone credit profiles of its two main subsidiaries Barclays Bank(baa3 BCA) and Barclays Bank UK (a3 BCA).

Exhibit 1

Rating Scorecard - Key financial ratios as at 31 December 2019

2.7% 19.4%

0.4%

37.0% 55.0%

0%

10%

20%

30%

40%

50%

60%

0%

5%

10%

15%

20%

25%

Asset Risk:Problem Loans/

Gross Loans

Capital:Tangible Common

Equity/Risk-WeightedAssets

Profitability:Net Income/

Tangible Assets

Funding Structure:Market Funds/

Tangible BankingAssets

Liquid Resources:Liquid BankingAssets/TangibleBanking Assets

Solvency Factors (LHS) Liquidity Factors (RHS)

Barclays plc (BCA: baa2) Median baa2-rated banks

So

lve

ncy F

acto

rs

Liq

uid

ity F

acto

rs

Source: Moody's Investors Service

The baa2 BCA of Barclays reflects: its (1) moderate credit risk, driven by strong loan quality,which is partly offset by its sizeable capital markets activities, which are confidence sensitiveand expose the firm to higher earnings volatility than the more traditional commercial bankingactivities; (2) good regulatory capitalisation; (3) diversified funding and sound liquidity; and(4) weak profitability in 2020, due to a sharp increase in credit impairments related to therevised coronavirus scenario; we anticipate profitability will partially recover in 2021, providedeconomies rebound, as the coronavirus pandemic fades.

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Credit strengths

» Capitalisation is slightly above the median of its global peers

» Ample liquidity protects against market shocks

» Strong credit quality and robust risk management

Credit challenges

» Profitability challenged by the current macroeconomic environment

» High reliance on inherently more volatile capital markets revenues

» High exposure to more confidence sensitive wholesale funding

» Capital markets and investment banking activities add opacity and complexity

Rating outlookThe stable outlook on Barclays' senior ratings reflects Moody’s expectation that its capital, finding and liquidity will only moderatelydeteriorate, despite profitability pressures. Our assessment of the volume of loss absorbing debt under our Advanced Loss Given Failureanalysis and our assumption of a moderate likelihood of government support have not changed.

The rapid and widening spread of the coronavirus outbreak, deteriorating global economic outlook, falling oil prices, and asset pricedeclines are creating a severe and extensive credit shock across many sectors, regions and markets. The banking sector has been one of thesectors affected by the shock given the expected impact on asset quality and profitability. Although the initial shock from the coronavirushas been similar across countries, economic outcomes will differ because of different capacities to withstand the shock. The overall risksto our baseline forecasts1 for all countries are skewed to the downside.

Factors that could lead to an upgradeBarclays' baa2 notional BCA could be upgraded, following a sustained improvement in its asset risk, capital or liquidity profiles or animprovement of the standalone credit profile of its main subsidiary Barclays Bank. An upgrade of Barclays' baa2 notional BCA would likelylead to a ratings upgrade. Barclays' ratings could also be upgraded if the group were to issue a substantially higher amount of bail-in-ableliabilities or maintain excess financial resources at the level of the holding company, affording greater protection to its creditors.

Factors that could lead to a downgradeBarclays' baa2 notional BCA could be downgraded following a deterioration of the standalone credit profiles of its two main subsidiariesBarclays Bank and Barclays Bank UK. A lower notional BCA would likely lead to a downgrade of Barclays' ratings. Barclays' ratings couldalso be downgraded if we were to assess a lower degree of protection from the stock of bail-in-able liabilities, which we assess throughour advanced LGF analysis.

Key indicators

Exhibit 2

Barclays PLC (Consolidated Financials) [1]

12-192 12-182 12-172 12-162 12-152 CAGR/Avg.3

Total Assets (GBP Billion) 895.1 900.0 883.3 854.1 790.0 3.24

Total Assets (USD Billion) 1,185.8 1,146.3 1,194.9 1,055.4 1,164.5 0.54

Tangible Common Equity (GBP Billion) 57.2 55.6 56.6 57.6 51.9 2.44

Tangible Common Equity (USD Billion) 75.7 70.8 76.6 71.1 76.5 (0.3)4

Problem Loans / Gross Loans (%) 2.5 2.6 3.0 3.2 3.8 3.05

Tangible Common Equity / Risk Weighted Assets (%) 19.4 17.8 18.1 15.7 14.5 17.16

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 19 May 2020 Barclays PLC: Update post 1Q results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Problem Loans / (Tangible Common Equity + Loan Loss Reserve) (%) 12.5 13.6 14.8 19.4 25.8 17.25

Net Interest Margin (%) 1.1 1.1 1.2 1.4 1.3 1.25

PPI / Average RWA (%) 2.1 1.6 1.8 1.3 0.8 1.56

Net Income / Tangible Assets (%) 0.7 0.3 0.1 0.8 0.0 0.45

Cost / Income Ratio (%) 70.8 76.4 72.3 77.1 85.8 76.55

Market Funds / Tangible Banking Assets (%) 37.0 39.4 38.1 31.2 33.7 35.95

Liquid Banking Assets / Tangible Banking Assets (%) 55.0 57.5 60.6 41.3 41.5 51.25

Gross Loans / Due to Customers (%) 73.2 77.4 68.6 90.9 92.9 80.65

[1]All figures and ratios are adjusted using Moody's standard adjustments. [2]Basel III - fully loaded or transitional phase-in; IFRS. [3]May include rounding differences because of the scaleof reported amounts. [4]Compound annual growth rate (%) based on the periods for the latest accounting regime. [5]Simple average of periods for the latest accounting regime. [6]Simpleaverage of Basel III periods.Sources: Moody's Investors Service and company filings

ProfileBarclays is one of the market leaders in the UK, with strong franchises in the retail (including credit cards), business and corporate bankingmarket segments. The group also has overseas operations through its international credit card franchise (in continental Europe and theUS), international payments and its corporate and investment banking (CIB) activities, in around 40 countries. The group's activities focuson two main markets: the UK (around half of group revenues) and the US (around one third).

» Barclays Bank (the non ring-fenced bank) accounts for around 80% of group total assets and focuses on more confidence-sensitivecorporate banking and capital market activities, despite maintaining certain commercial activities, such as payments, wealthmanagement and international consumer and cards activities. The bulk of Barclays Bank's operations are split between the group'skey markets in the UK and the US but it also has presence in continental Europe and other major global financial centres.

» Barclays Bank UK (the ring-fenced bank) accounts for the remaining around 20% of the group's total assets and focuses on UKconsumer and small business banking. The firm's retail and commercial businesses are its key credit strengths, providing good shockabsorption capacity against potential earnings volatility stemming from the bank’s material capital market activities (see Exhibit 3).

Exhibit 3

Barclays’ pre-tax profits by business line

(1.5)

(1.0)

(0.5)

-

0.5

1.0

1.5

2.0

1Q 2019 2Q 2019 3Q 2019 4Q 2019 1Q 2020

£ b

illio

ns

Barclays UK Barclays International Head Office

Source: Company data

Barclays is authorized and licensed to operate with its EEA clients and customers through its Irish subsidiary Barclays Bank IrelandPLC (BBI, not rated), which reported total assets of €69 billion at end-2019, including €13 billion of customer loans and €27 billion ofderivative assets. The subsidiary reported high levels of liquidity and capital, with an LCR of 187% and a CET1 capital ratio of 14.4%at the same time. BBI is under the supervision of the ECB’s Single Supervisory Mechanism and its operations are integrated within thegroup, with further transfer of business expected to continue taking place over the Brexit timeline.

3 19 May 2020 Barclays PLC: Update post 1Q results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Detailed credit considerationsPlease refer to the Credit Opinions of Barclays Bank and Barclays Bank UK for an analysis of the credit drivers for each of these entities.

Profitability challenged by the current macroeconomic environmentBarclays’ profitability, to which we assign a score of ba1 in our BCA scorecard, has improved in recent quarters. However, we expectweak profitability in 2020, due to a sharp increase in credit impairments and lower revenue related to the coronavirus environment; weanticipate profitability will partially recover in 2021, provided economies rebound, as the coronavirus pandemic fades.

Management reiterated their target to reduce the cost:income ratio to less than 60% over time, to mitigate the impact of a decrease inrevenue and an expectation of elevated credit charges and to achieve at RoTE of 10% over time.

In 1Q 2020, Barclays reported a net income of £842 million, and a return on tangible equity (RoTE) of 5.1%. Revenue increased 20% year-on-year, driven by a strong performance in capital markets. Operating costs were flat year-on-year, with the reported cost: income ratiodeclining to 52%. Credit impairment charges increased sharply to £2.1 billion, equal to a loan loss rate of 223 bps annualised.

The group is affected by Brexit, having a large presence in the UK (around half of total revenues). Our ratings incorporate the expectationof a “soft Brexit” (the exit of the UK from the EU with a negotiated agreement). We view that a “hard Brexit” (were no agreement tobe reached by the end of December) will result in a weaker growth outlook for the UK. The Coronavirus crisis will likely result in an evenweaker operating environment with lower economic growth and higher unemployment, resulting into lower revenue and higher creditcosts, which will translate into lower profitability than was previously expected.

Barclays' BCA does not include a positive qualitative adjustment for Business Diversification. Our assessments of the group's asset riskand profitability already capture the degree of diversification of the group's operations, and the extent to which they are expected todeliver higher and sustainable earnings over the cycle.

Capitalisation is slightly above the median of its global peersOur assigned score of aa3 for Capital reflects the group’s good regulatory capitalisation, slightly above the median of its global peer group(see Exhibit 4). We make a one notch negative adjustment from the initial score for our expectation of the trend in our Tangible CommonEquity (TCE) capital ratio over the outlook period.

The Common Equity Tier 1 (CET1) capital ratio of 13.1% at end-March 2020, around 160 bps above the Maximum Distributable Amount(MDA) requirement of 11.5% as of March 2020. Management stated that post-coronavirus, a CET1 level of around 13.5% is appropriate.The group's UK spot leverage ratio was 4.5%, above the minimum regulatory requirement, but below the 5.4% global peers' median.

Exhibit 4

Common Equity Tier 1 (CET1) and Tier 1 leverage ratios for Global Investment Banks, end-March 2020

15.3% 14.6%

13.1% 12.8% 12.8% 12.7%12.3% 12.3% 12.1% 12.0% 12.0%

11.2% 11.1%

6.2%5.3% 4.5% 5.4%

4.0% 4.2%

6.0% 5.9%5.3%

4.2%3.9%

6.0%6.4%

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

18.0%

baa2 a2 baa2 a3 ba1 baa2 a2 baa1 baa2 a3 baa1 baa1 a3

MS HSBC BCS** UBS* DB SG JPM GS CS* RBC BNP CITI BAC

CET1 ratio Tier 1 Leverage ratio Median CET1 ratio (12.3%) Median leverage ratio (5.3%)

Notes: (1) Basel III fully phased in advanced approach for all US banks; (2) Tier 1 leverage ratio for US banks is the supplemental leverage ratio (SLR). *UBS and CS leverage ratios reflectCommon Equity Tier plus Low Trigger Additional Tier 1 and High-Trigger Additional Tier 1 securities. For the computation of the leverage ratio, the Swiss regulator allowed for a temporaryexclusion of cash at central banks until 01 July 2020. The ratios shown here do not include this benefit.**Barclays (BCS) leverage is reflective of the spot UK leverage ratio.Source: Company data and Moody's Investors Service

4 19 May 2020 Barclays PLC: Update post 1Q results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

High exposure to more confidence sensitive wholesale funding mitigated by ample liquidityWe assign a baa2 Combined Liquidity Score, derived from an assigned aa2 Liquid Resources score and an assigned ba3 Funding Structurescore. The combined score reflects Barclays strong liquidity resources mitigating the high reliance on market funds.

Barclays had a sizeable retail and corporate deposit funding book of £471 billion at end-March 2020, well in excess of the loan book(we calculate a gross loan-to-deposit ratio of 79% at the same date). However, the group is reliant on a large amount of confidence-sensitive wholesale funding because of its large stock of financial assets and to meet its Minimum Requirement for Own Funds andEligible Liabilities (MREL) requirements, albeit the group is now at its end-state requirements. The net stable funding ratio (NSFR) was>100% at end-March 2020.

We assign a Funding Structure score of ba3, one notch below the initial score. as a result of a two notch negative adjustment forexpected trend and a one notch positive adjustment for the group's quality of deposits. The positioning reflects our forward-lookingexpectation that our funding structure ratio will oscillate around 40%. We also incorporate the bank’s stable and diversified fundingbase provided by its national retail and corporate franchise.

Liquidity is a credit strength for Barclays, and the size and quality of its liquidity buffer are higher than those of some of its largeEuropean peers. This reflects the conservative UK liquidity standards and the bank's conservative liquidity risk management framework.Barclays’ sound liquidity position is also illustrated by its CRR II liquidity coverage ratio of 155% at end-March 2020. The liquid assetpool of £237 billion at the same date was well in excess of the stock of short-term wholesale funding, and most of the liquidity bufferqualified as high-quality liquid assets. The group also maintains a material amount of pre-positioned assets with the Bank of Englandproviding a ready source of contingent liquidity which is not factored into the Liquid Resources score. We view that keeping an elevatedliquidity level at times of uncertain market conditions is evidence of the group's conservative approach to liquidity management.

We assign a Liquid Resources score of aa2, in line with the initial score: The position reflects the bank’s very strong liquidity position.We take account of encumbrance on a sizable proportion of assets deemed liquid in our initial ratio, while positively considering thegroup’s conservative liquidity management.

Strong credit quality helps to mitigate risks from investment banking and capital market activitiesThe baa2 score for the Asset Risk factor of our BCA Scorecard reflects Barclays’ strong credit quality as well as the risks associated withthe group’s investment banking activities.

Barclays has a strong loan quality profile: we calculate a problem loan ratio of 2.2% as at end-March 2020. Barclays' conservativeunderwriting is stricter than that of its peers: as of end-2019, the bank's £143 billion UK mortgage book had an average loan-to-valueratio lower than that of its peers of 51%.

We view Barclays' investment banking and capital market businesses, which are the largest contributors to its group RWAs, as a creditweakness, owing to the tail risks associated with these activities. Market risk, counterparty credit risk and operational risk arise fromBarclays' capital market activities, in particular from its large stock of financial assets and derivatives, totaling £721 billion at end-March2020, corresponding to half of its total assets.

We consider capital markets activities as inherently riskier, susceptible to market conditions and more opaque than traditional retail andcommercial banking operations. These factors constrain the credit profile of Barclays and that of its global peers, and are reflected in aone-notch negative adjustment for Opacity and Complexity in the qualitative section of our BCA Scorecard.

Under Barclays’ strategic plan, the corporate and investment bank's risk profile will be largely unchanged, as measured by the allocatedRWAs as incremental earnings will be generated by customer flow-related activities, which consume less regulatory capital, thereforegenerating higher risk-adjusted returns. We believe that a greater proportion of CIB earnings could nevertheless lead to a higher degreeof volatility in the group's earnings, a credit negative.

Barclays' operating environment is driven mainly by its exposure to the UK and the US, to which we assign Strong+ and Very Strong-Macro Profiles respectively. UK banks benefit from operating in a wealthy and developed country, with a very high degree of economic,institutional and government financial strength, as well as low susceptibility to event risk. However, we believe that operating conditions

5 19 May 2020 Barclays PLC: Update post 1Q results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

for UK banks will deteriorate over the next 12-18 months, driven by an uncertain economic backdrop due to the coronavirus, as well asthe UK's preparation to leave the European Union (Aaa stable).

Environmental, social and governance considerationsThe global banking sector has been classified as “Low” risk in our environmental (E) risk heatmap2 and as “Moderate” risk in our social(S) risk heatmap3

Environmental risk exposure for Barclays is negatively impacted by its exposure to some high-carbon emission sectors, which are proneto environmental risks, including oil and gas (£16 billion credit risk exposure as at end-2019, equal to around 2.4% of total group).However, Barclays' exposures are well-diversified geographically and on a single name basis. We consider that such risk exposure isunlikely to translate into a meaningful credit impact in the outlook horizon.

Social risk is moderate for Barclays, including considerations in relation to the coronavirus outbreak, given the substantial implicationsfor public health and safety and deteriorating global economic outlook, creating a severe and extensive credit shock across manysectors, regions and markets. The firm like other UK banks, is subject to regular investigations by the UK Financial Conduct Authority(FCA) on customer protection and fair treatment. Since the financial crisis, Barclays has made around £11 billion in provisions forconduct related to Payment Protection Insurance (PPI). Investigations represent significant reputational risk for banks.

Governance4 is highly relevant to B plc, as it is to all banks. Corporate governance weaknesses can lead to a deterioration in a bank’scredit quality, while governance strengths can benefit its credit profile. Governance risks are largely internal rather than externallydriven. The bank’s risk governance infrastructure is adequate and has not shown any shortfall in recent years.

Support and structural considerationsLoss given failure and additional notchingWe apply our advanced LGF analysis to Barclays because the bank is incorporated in the UK, which we consider to be an operationalresolution regime because it is subject to the EU Bank Recovery and Resolution Directive. For this analysis, we assume residual tangiblecommon equity of 3% and post-failure losses of 8% of tangible banking assets, a 25% run-off in junior wholesale deposits and a 5% run-off in preferred deposits. We assign a 25% probability to deposits being preferred to senior unsecured debt.

The introduction of UK ring-fencing has led us to perform separate advanced LGF analysis for Barclays, Barclays Bank and Barclays Bank UK.We consider that Barclays' creditors will benefit from Barclays' externally-issued debt as well as subordinated and junior debt externallyissued by Barclays Bank (Barclays Bank UK does not currently have outstanding debt).

We assume that UK holding company senior obligations benefit from the subordination of both holding and bank-subordinatedinstruments. However, we believe that UK holding company senior unsecured debt is economically junior to bank senior unsecureddebt, based on our forward-looking view that UK holding company senior unsecured debt, although legally pari passu to bank debt, willeventually fund bank senior unsecured debt, which is contractually, structurally or statutorily subordinated to operating company externalsenior debt.

Our advanced LGF analysis indicates a high loss given failure for senior unsecured creditors of Barclays, resulting in no rating uplift fromthe firm's adjusted BCA and a high loss given failure for junior creditors resulting in one notch negative adjustment from the firm's adjustedBCA. We also incorporate an additional notching for junior subordinated and preference share instruments, reflecting coupon suspensionrisk ahead of failure.

High-trigger contingent convertible capital (AT1) is not subject to the advanced LGF analysis because we include these securities intangible common equity, which is an input to the Capital score, part of the BCA.

Government supportWe assess a low probability of government support for the Barclays' creditors, given that this entity is the holding company of the group,resulting in no uplift for government support included in these ratings.

6 19 May 2020 Barclays PLC: Update post 1Q results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

About Moody's Bank ScorecardOur scorecard is designed to capture, express and explain in summary form our Rating Committee's judgement. When read in conjunctionwith our research, a fulsome presentation of our judgement is expressed. As a result, the output of our scorecard may materially differfrom that suggested by raw data alone (though it has been calibrated to avoid the frequent need for strong divergence). The scorecardoutput and the individual scores are discussed in rating committees and may be adjusted up or down to reflect conditions specific toeach rated entity.

7 19 May 2020 Barclays PLC: Update post 1Q results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

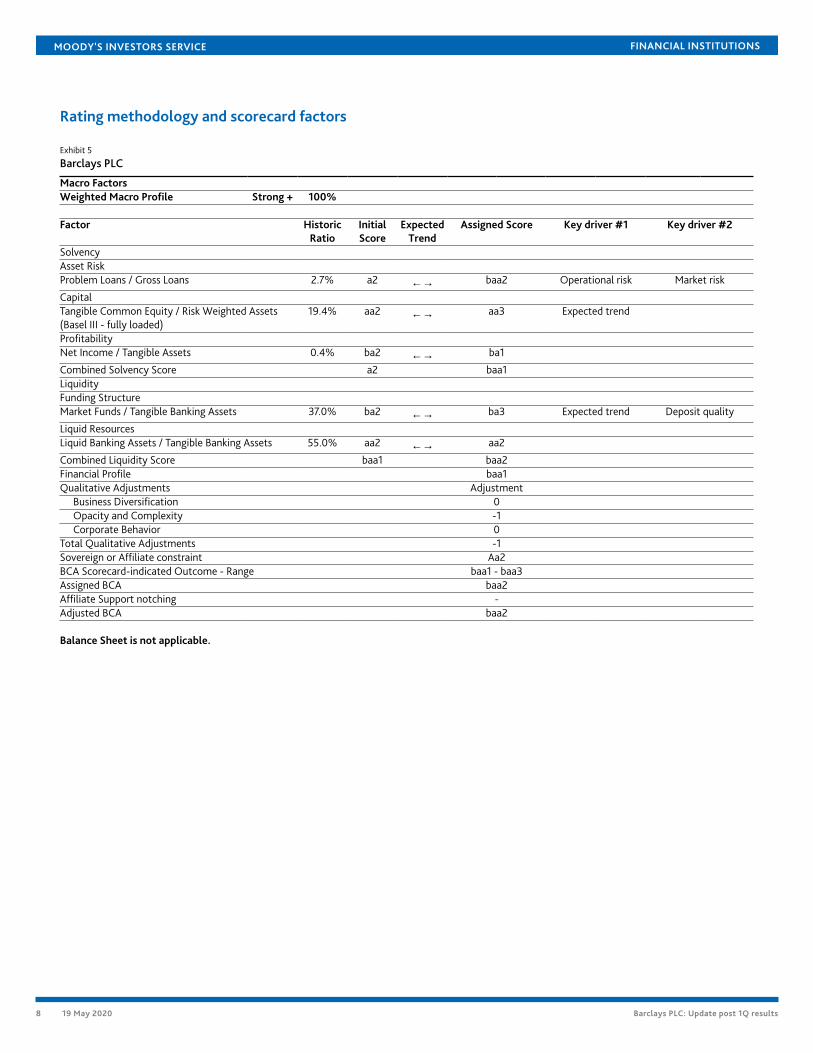

Rating methodology and scorecard factors

Exhibit 5

Barclays PLC

Macro FactorsWeighted Macro Profile Strong + 100%

Factor HistoricRatio

InitialScore

ExpectedTrend

Assigned Score Key driver #1 Key driver #2

SolvencyAsset RiskProblem Loans / Gross Loans 2.7% a2 ←→ baa2 Operational risk Market risk

CapitalTangible Common Equity / Risk Weighted Assets(Basel III - fully loaded)

19.4% aa2 ←→ aa3 Expected trend

ProfitabilityNet Income / Tangible Assets 0.4% ba2 ←→ ba1

Combined Solvency Score a2 baa1LiquidityFunding StructureMarket Funds / Tangible Banking Assets 37.0% ba2 ←→ ba3 Expected trend Deposit quality

Liquid ResourcesLiquid Banking Assets / Tangible Banking Assets 55.0% aa2 ←→ aa2

Combined Liquidity Score baa1 baa2Financial Profile baa1Qualitative Adjustments Adjustment

Business Diversification 0Opacity and Complexity -1Corporate Behavior 0

Total Qualitative Adjustments -1Sovereign or Affiliate constraint Aa2BCA Scorecard-indicated Outcome - Range baa1 - baa3Assigned BCA baa2Affiliate Support notching -Adjusted BCA baa2

Balance Sheet is not applicable.

8 19 May 2020 Barclays PLC: Update post 1Q results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

De Jure waterfall De Facto waterfall NotchingDebt ClassInstrumentvolume +

subordination

Sub-ordination

Instrumentvolume +

subordination

Sub-ordination

De Jure De FactoLGF

NotchingGuidance

vs.Adjusted

BCA

AssignedLGF

notching

AdditionalNotching

PreliminaryRating

Assessment

Senior unsecured holding company debt - - - - - - - 0 0 baa2Dated subordinated holding companydebt

- - - - - - - -1 0 baa3

Holding company non-cumulativepreference shares

- - - - - - - -1 -2 ba2

Instrument Class Loss GivenFailure notching

Additionalnotching

Preliminary RatingAssessment

GovernmentSupport notching

Local CurrencyRating

ForeignCurrency

RatingSenior unsecured holding company debt 0 0 baa2 0 Baa2 Baa2Dated subordinated holding companydebt

-1 0 baa3 0 (P)Baa3 Baa3

Holding company non-cumulativepreference shares

-1 -2 ba2 0 Ba2 (hyb) Ba2 (hyb)

[1]Where dashes are shown for a particular factor (or sub-factor), the score is based on non-public information.Source: Moody’s Investors Service

9 19 May 2020 Barclays PLC: Update post 1Q results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Ratings

Exhibit 6

Category Moody's RatingBARCLAYS PLC

Outlook StableBaseline Credit Assessment baa2Adjusted Baseline Credit Assessment baa2Issuer Rating -Dom Curr Baa2Senior Unsecured Baa2Subordinate Baa3Pref. Stock Non-cumulative Ba2 (hyb)Commercial Paper P-2Other Short Term -Dom Curr (P)P-2

BARCLAYS BANK PLC

Outlook StableCounterparty Risk Rating A1/P-1Bank Deposits A1/P-1Baseline Credit Assessment baa3Adjusted Baseline Credit Assessment baa2Counterparty Risk Assessment A1(cr)/P-1(cr)Issuer Rating A1Senior Unsecured A1Subordinate Baa3Jr Subordinate Ba1 (hyb)Pref. Stock Ba1 (hyb)Pref. Stock Non-cumulative Ba2 (hyb)Commercial Paper P-1Other Short Term -Fgn Curr P-1Other Short Term -Dom Curr (P)P-1

BARCLAYS BANK UK PLC

Outlook NegativeCounterparty Risk Rating Aa2/P-1Bank Deposits A1/P-1Baseline Credit Assessment a3Adjusted Baseline Credit Assessment a3Counterparty Risk Assessment Aa2(cr)/P-1(cr)Commercial Paper P-1

Source: Moody's Investors Service

10 19 May 2020 Barclays PLC: Update post 1Q results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Endnotes1 Our latest macroeconomic forecasts are included in Global Macro Outlook 2020-21: Global recession is deepening rapidly as restrictions exact high

economic cost, published on 28 April 2020.

2 Environmental risks can be defined as environmental hazards encompassing the impacts of air pollution, soil/water pollution, water shortages and naturaland man-made hazards (physical risks). Additionally, regulatory or policy risks, like the impact of carbon regulation or other regulatory restrictions,including the related transition risks like policy, legal, technology and market shifts, that could impair the evaluation of assets are an important factor.Certain banks could face a higher risk from concentrated lending to individual sectors or operations exposed to the aforementioned risks.

3 Social risk considerations represent a broad spectrum, including customer relations, human capital, demographic and societal trends, health and safetyand responsible production. The most relevant social risks for banks arise from the way they interact with their customers. Social risks are particularly highin the area of data security and customer privacy, which is partly mitigated by sizeable technology investments and banks’ long track record of handlingsensitive client data. Fines and reputational damage because of product mis-selling or other types of misconduct is a further social risk. Societal trendsare also relevant in a number of areas, such as shifting customer preferences toward digital banking services increasing information technology costs,ageing population concerns in several countries affecting demand for financial services or socially driven policy agendas that may translate into regulationsthat affect banks’ revenue bases. Pressure on profitability can be particularly severe for small banks that have limited options to mitigate declines innet interest income, their main revenue source. By contrast, large institutions equipped with resources to invest in new businesses or technology will besomewhat able to overcome these challenges.

4 Corporate governance is a well-established key driver for banks and related risks are typically included in our evaluation of the banks' financial profile.Corporate governance is a well-established key driver for banks and related risks are typically included in our evaluation of the banks' financial profilemay be captured in individual adjustments to the BCA. Corporate governance weaknesses can lead to a deterioration in a company’s credit quality, whilegovernance strengths can benefit its credit profile. When credit quality deteriorates due to poor governance, such as break-down in controls resulting infinancial misconduct, it can take a long time to recover. Governance risks are also largely internal rather than externally driven.

11 19 May 2020 Barclays PLC: Update post 1Q results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

© 2020 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND/OR ITS CREDIT RATINGS AFFILIATES ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURECREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MATERIALS, PRODUCTS, SERVICES AND INFORMATION PUBLISHED BY MOODY’S(COLLECTIVELY, “PUBLICATIONS”) MAY INCLUDE SUCH CURRENT OPINIONS. MOODY’S INVESTORS SERVICE DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAYNOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEEMOODY’S RATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’SINVESTORS SERVICE CREDIT RATINGS. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, ORPRICE VOLATILITY. CREDIT RATINGS, NON-CREDIT ASSESSMENTS (“ASSESSMENTS”), AND OTHER OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTSOF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS ORCOMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. AND/OR ITS AFFILIATES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS DONOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOTAND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS ANDPUBLICATIONS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS, ASSESSMENTS ANDOTHER OPINIONS AND PUBLISHES ITS PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDYAND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS, AND PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESSAND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS OR PUBLICATIONS WHEN MAKING AN INVESTMENTDECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BYLAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHERTRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANYFORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM ISDEFINED FOR REGULATORY PURPOSES AND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing its Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY CREDITRATING, ASSESSMENT, OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any credit rating,agreed to pay to Moody’s Investors Service, Inc. for credit ratings opinions and services rendered by it fees ranging from $1,000 to approximately $2,700,000. MCO and Moody’sinvestors Service also maintain policies and procedures to address the independence of Moody’s Investors Service credit ratings and credit rating processes. Information regardingcertain affiliations that may exist between directors of MCO and rated entities, and between entities who hold credit ratings from Moody’s Investors Service and have also publiclyreported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance —Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as tothe creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any credit rating, agreed to pay to MJKK or MSFJ (as applicable) for credit ratings opinions and servicesrendered by it fees ranging from JPY125,000 to approximately JPY250,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1220981

12 19 May 2020 Barclays PLC: Update post 1Q results

MOODY'S INVESTORS SERVICE FINANCIAL INSTITUTIONS

Analyst Contacts

Maxwell Price +44.20.7772.1778Associate [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

13 19 May 2020 Barclays PLC: Update post 1Q results