©BANKSETA 2008 ENABLING SKILLS DEVELOPMENT IN THE BANKING SECTOR BANKSETA SME SERVICES AFRICA SMME...

13

©BANKSETA 2008 ENABLING SKILLS DEVELOPMENT IN THE BANKING SECTOR BANKSETA SME SERVICES AFRICA SMME CONFERENCE 15 September 2009

-

Upload

dominic-malone -

Category

Documents

-

view

216 -

download

0

Transcript of ©BANKSETA 2008 ENABLING SKILLS DEVELOPMENT IN THE BANKING SECTOR BANKSETA SME SERVICES AFRICA SMME...

©BANKSETA 2008ENABLING SKILLS DEVELOPMENT IN THE BANKING SECTOR

BANKSETA SME SERVICES

AFRICA SMME CONFERENCE

15 September 2009

Operating environment

©BANKSETA 2008

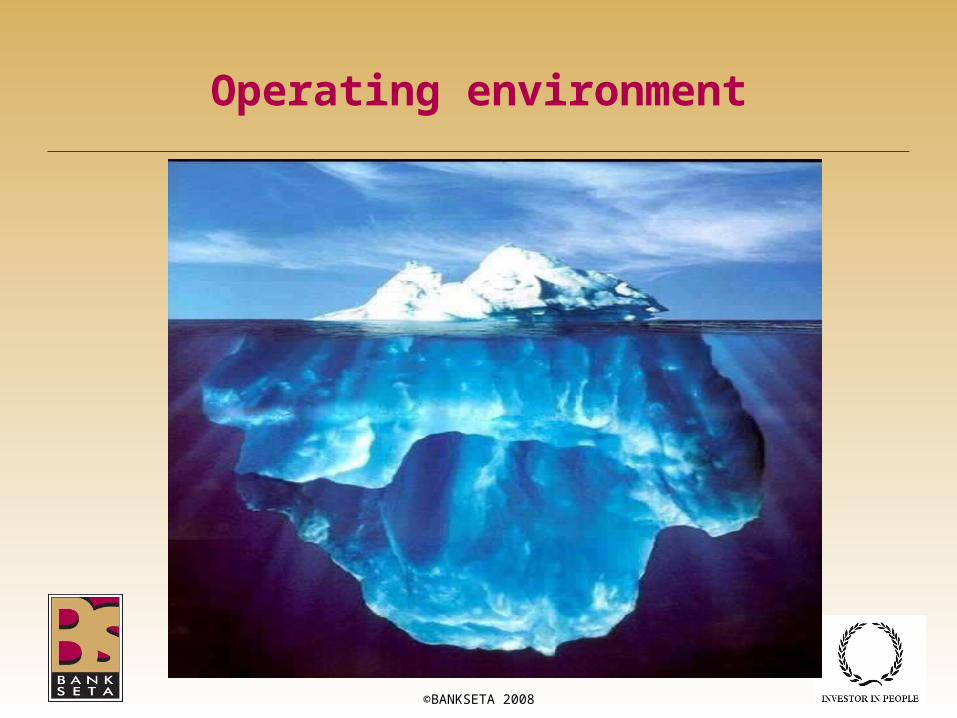

Operating environment: Finmark

• 8% of all small business owners in Gauteng are non-SA citizens – 70% male, 78% informal, 2 in 10 will employ other people, more negative outlook on life

• Majority of small business customers are private individuals (96%) • Largest problem across the board - finding capital to start business;

more problems in higher tiers linked to creating awareness of and registering the business, finding premises. Income tax + VAT regulations most troublesome due to compliance costs

• Majority (69%) are home-based, except and or no fixed location • 41% of small business owners are unbanked• Approximately 7 in 10 business owners are not aware of any

organisations that provide support, back up, advice or training to small businesses.

©BANKSETA 2008

BANKSETA strategic priorities

• Finance Sector Charter• Youth Development• SME Development• Continuous Professional Development/Life Long

Learning• Research and Benchmarking

Strategic priorities cont…

• The aim is to provide SME support through various initiatives and,

• to retain & attract organizations participating in skills development

• Categories of SMEs include:– Non Levy Paying (NLP) companies

– Levy Paying (LP) companies

• There is a particular focus on Microfinance Institutions

Strategic priorities cont…

The strategy aims to achieve SME support though:– A variety of skills development programmes to cater for different

needs of SMEs– Allocation of dedicated BANKSETA funding and other resources

to support SMEs– Building of partnerships with relevant organisations in order to

advance SME support– Research– Marketing and communications– Strategy measurement

SME Support snapshot

• Microfinance Skills Project• Training voucher scheme• Lifelong learning Initiatives • Building a Better Business • SME Support Multimedia toolkit• Mobile Learning Solution for SMEs• HIV/AIDS Training support• Research• Stakeholder forums/Road shows• New venture creation

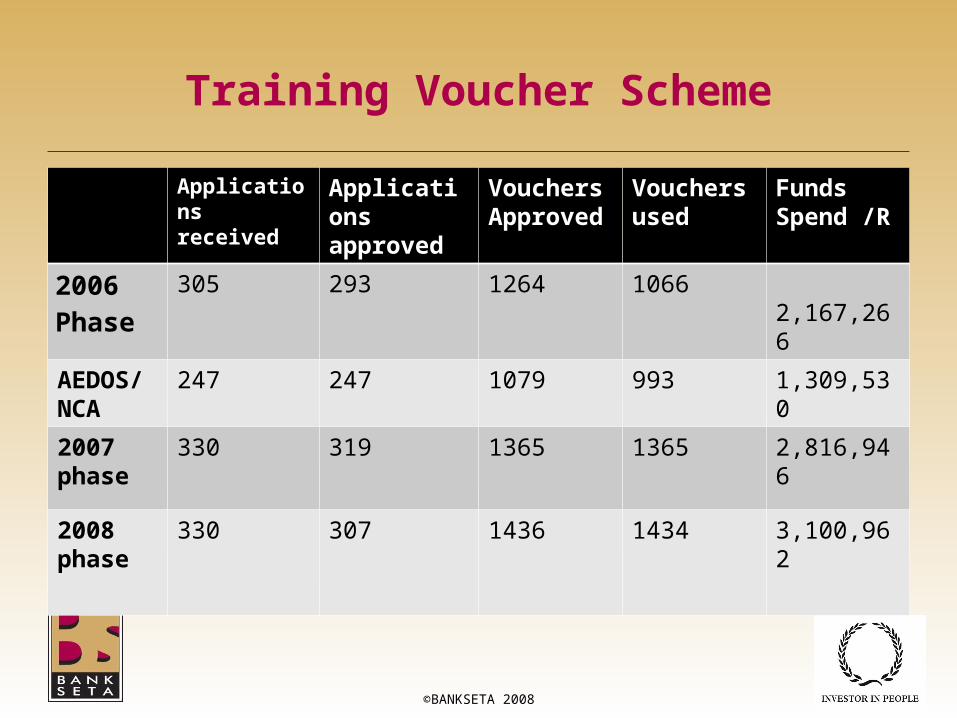

Training Voucher Scheme

Applications received

Applications approved

Vouchers Approved

Vouchers used

FundsSpend /R

2006 Phase

305 293 1264 1066 2,167,266

AEDOS/NCA

247 247 1079 993 1,309,530

2007 phase

330 319 1365 1365 2,816,946

2008 phase

330 307 1436 1434 3,100,962

©BANKSETA 2008

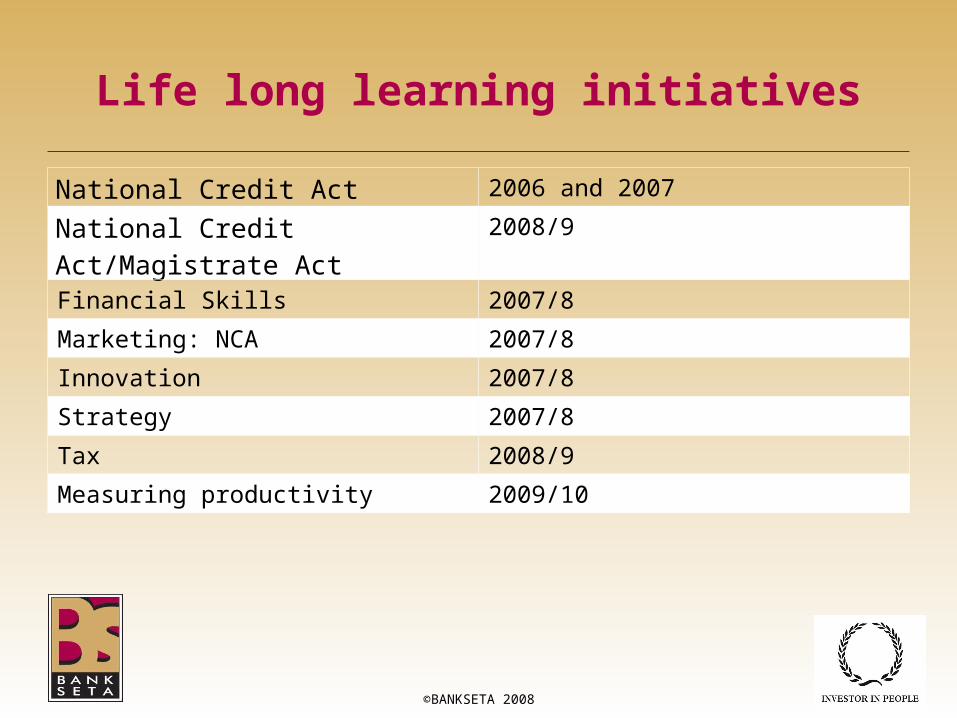

Life long learning initiatives

National Credit Act 2006 and 2007

National Credit Act/Magistrate Act 2008/9

Financial Skills 2007/8

Marketing: NCA 2007/8

Innovation 2007/8

Strategy 2007/8

Tax 2008/9

Measuring productivity 2009/10

©BANKSETA 2008

Building a Better Business

Provinces reached:

• Mpumalanga• Kwa-Zulu Natal• North West• Western Cape• Eastern Cape• Gauteng

More than 40 SME companies reached

©BANKSETA 2008

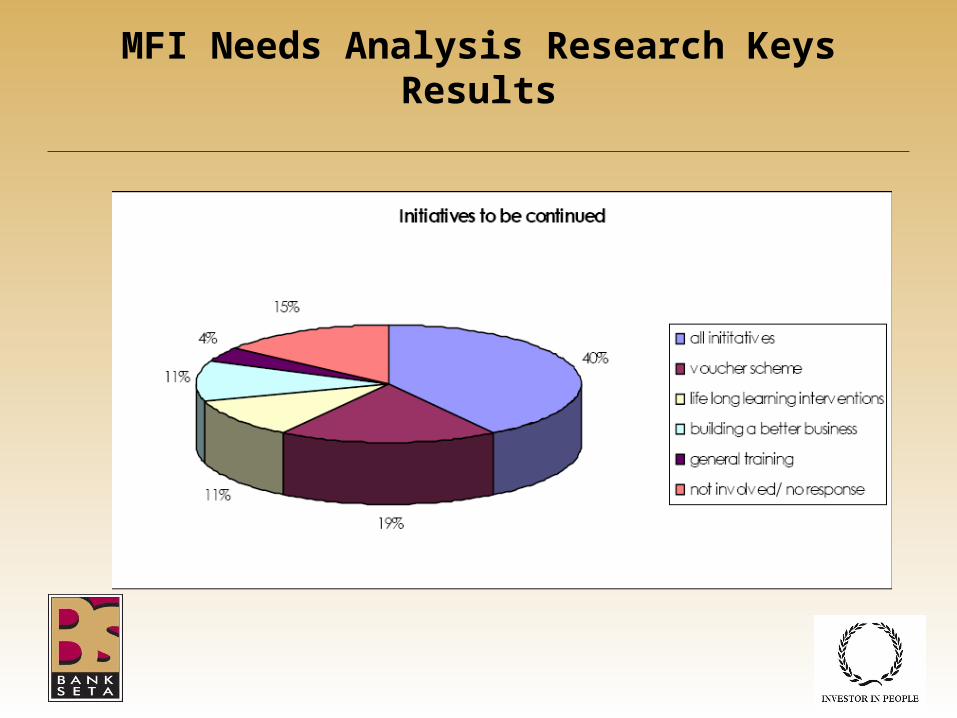

MFI Needs Analysis Research Keys Results

Impact imperatives

SMMEs including Microfinance play and important role in the economy through

• Creation of access to credit to the unbanked/un-bankable• Contribution to alleviation of poverty• Creation of sustainable livelihoods

‘ Not having enough money is only one part of being poor”

Jonathan Morduch et al: Portfolios of the poor

©BANKSETA 2008

Contact details

• Tel: 0118059661• Fax: 0118058348

• Call Centre: 0861020002• Website: www.bankseta.org.za