Bankruptcy Fundamentals -...

64

Bankruptcy Fundamentals Erin M. McCartney John T. Turco & Associates, P.C., L.L.O., Omaha August 11, 2015 University of Nebraska College of Law, Lincoln

Transcript of Bankruptcy Fundamentals -...

Bankruptcy FundamentalsErin M. McCartney

John T. Turco & Associates, P.C., L.L.O., Omaha

August 11, 2015University of Nebraska College of Law, Lincoln

This page intentionally left blank.

8/4/2015

1

Bankruptcy Fundamentals

Erin M. McCartney

John T. Turco & Associates, P.C., L.L.O.

2580 S. 90th Street, Omaha, NE

402-933-8600; [email protected]

What is bankruptcy?• VIDEO

8/4/2015

2

What is bankruptcy?• Federal Court proceeding to discharge or reorganize debts

• Intended to provide a “fresh start” – making an individual look better to lenders

• Create a controlled crash landing rather than a fiery horrific crash landing

Bankruptcy Players• Debtor: individual who files a bankruptcy petition under Title 11. Person

looking for bankruptcy relief.

• Creditor: holder of secured, unsecured or priority claim.

• United States Trustee: this office reviews filings for bankruptcy eligibility and reports matters for investigation and possible criminal prosecution if appropriate (yikes!).

• Trustee: individual appointed by the United States Trustee’s Office in charge of administering a bankruptcy estate.

• Bankruptcy Judge: appointed for a term of 14 years by the United States Court of Appeals for the circuit in which the applicable district is located. Issues Court rulings if disputed matters.

8/4/2015

3

Bankruptcy Code• Governed under United States Constitution – Article 1, Section 8, Clause 4

Title 11 – referred to as the Bankruptcy Code Title 18 – bankruptcy crimes Title 26 – tax implications Title 28 – creation and jurisdiction of bankruptcy courts

• Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 (BAPCPA)

• Federal and state law apply – federal law govern procedure in bankruptcy cases / state law is applied when determining property rights.

• LOCAL RULES!! https://www.neb.uscourts.gov/Robohelp_Manuals/Local_Rules/index.htm

Intersection with Bankruptcy Law• Family Law/Divorce: property settlement v. support obligation

• Real Property: fee simple, life estate, future interest, contingent interest, lienholder,

• Contracts: validity of lien (real/personal property)

• Wills/Trusts: spendthrift provision

• Corporate/Business Associations

• Taxation Bankruptcy

Divorce

Will/Trusts

Real Property

Contracts

8/4/2015

4

Case Progression• Initial Consultation

• Pre-filing Credit Counseling Requirement

• Collect materials and prepare petition

• Follow-up Signing Appointment

• 11 U.S.C. § 341 hearing- Meeting of Creditors

• Post-filing Financial Management Requirement

• Judge involvement

• Discharge

Bankruptcy Estate• Estate – consists of all property interests of the debtor at the time of case

commencement, subject to certain exclusions and exemptions.

Exclusions: items the Debtor may keep no matter what. Exemptions: items the Debtor may keep if classified as protected under Federal

exemptions or applicable state exemptions.

Nebraska Exemptions: Homestead

Tools of the trade

Clothing

Household Goods

Wildcard

8/4/2015

5

Full Disclosure• Honesty is the BEST policy

• Disclosure of all information received through the provided documentation, independent research and information provided by the client is essential.

• Humans tend to hide things that may adversely affect a hoped-for outcome. Disclose all the facts because: a) they are invariably uncovered anyway; and, b) the advice from an informed attorney, considering all the details relevant, could drastically change the outcome.

Due Diligence Requirement• Paperwork:

Paystubs Bank statements Tax returns List of assets/liabilities Other: life insurance and retirement

• Research / Verify Credit Report Asset check Pacer Justice UCC/Judgment liens County Assessor KBB

8/4/2015

6

Outside Audits• U.S. Trustee may randomly select a case for an outside audit pursuant to 28

U.S.C § 586(f)(1)

• The audit firm looks for material misstatements

• Audits are simple when due diligence is performed

• Audit firm requests: bank statements, pay stubs, tax returns, all investment account, retirement accounts and life insurance statements covering the six months prior to filing, divorce decree and related orders

The Chapters of Bankruptcy – United States Code, Title 11, Bankruptcy

• Chapter 7: Liquidation “Complete” bankruptcy Liquidation of non-exempt assets Runs 3-4 months Keep secured loans if payments are current Must pass “means test”

• Chapter 13: Reorganization Plan 3-5 year repayment plan Based on disposable income “Super discharge” Gives homeowner a way of bringing past duemortgage payments current. Debt limitations

8/4/2015

7

Means Test- What is it?• The means test was added to the Bankruptcy Code in 2005 under 11 U.S.C.

§707(b) to create a way for determining which individuals qualify for relief in a Chapter 7 bankruptcy based on (1) the number of people in the household and (2) the average household income for the six months prior to filing.

• The means test is also designed to determine if an individual has “disposable monthly income” (“DMI”) after subtracting certain allowed expenses to make payments in a Chapter 13 plan. If an individual is determined to have DMI based on the means test, the individual does not qualify to file a Chapter 7 and must file for relief under a Chapter 13.

• The attorney must include the means test in the required forms within the bankruptcy petition. The forms are accessible at http://www.uscourts.gov/bkforms/bankruptcy_forms.html.

• On December 1, 2014, the official Bankruptcy Form 22C (B22C) was replaced with Form 22C-1 and Form 22C-2 (applicable if above median).

Means Test Income LimitsIn May 2015, the median income changed. The new threshold amounts in Nebraska are as follows*:

• 1 person household: $43,135

• 2 person household: $61,369

• 3 person household: $66,871

• 4 person household: $79,634

*http://www.justice.gov/ust/eo/bapcpa/20150515/bci_data/median_income_table.htm

8/4/2015

8

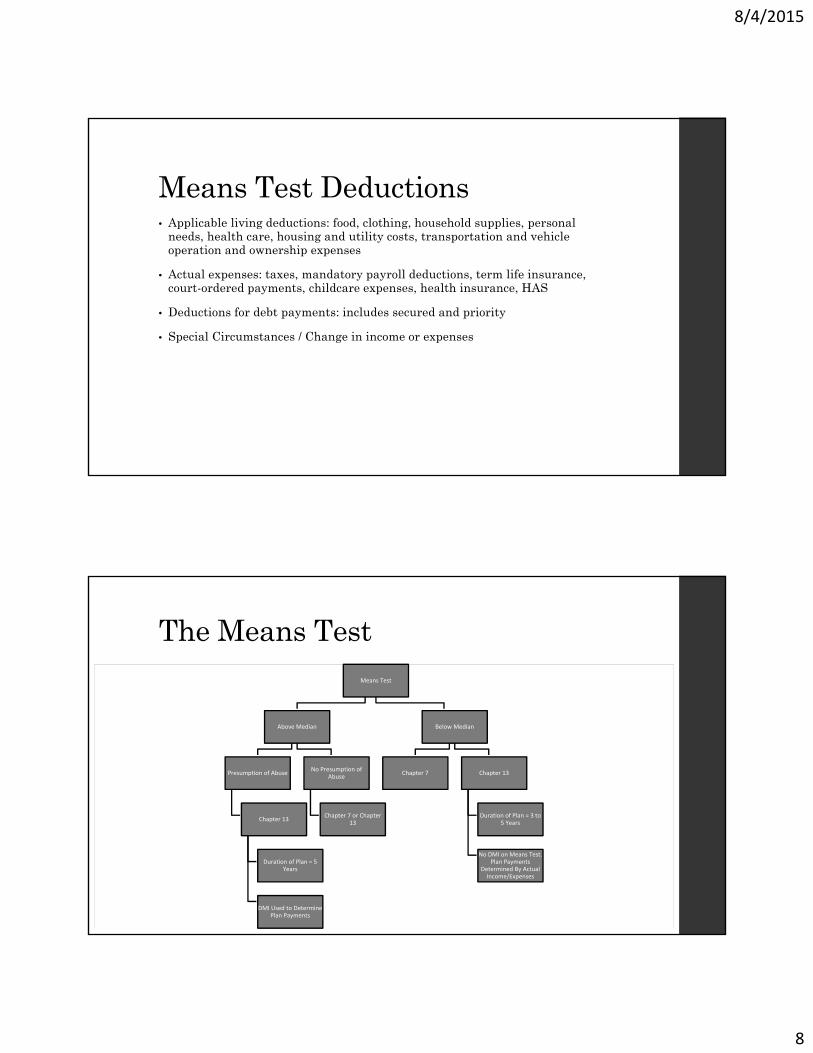

Means Test Deductions• Applicable living deductions: food, clothing, household supplies, personal

needs, health care, housing and utility costs, transportation and vehicle operation and ownership expenses

• Actual expenses: taxes, mandatory payroll deductions, term life insurance, court-ordered payments, childcare expenses, health insurance, HAS

• Deductions for debt payments: includes secured and priority

• Special Circumstances / Change in income or expenses

The Means TestMeans Test

Above Median

Presumption of Abuse

Chapter 13

Duration of Plan = 5 Years

DMI Used to Determine Plan Payments

No Presumption of Abuse

Chapter 7 or Chapter 13

Below Median

Chapter 7 Chapter 13

Duration of Plan = 3 to 5 Years

No DMI on Means Test. Plan Payments

Determined By Actual Income/Expenses

8/4/2015

9

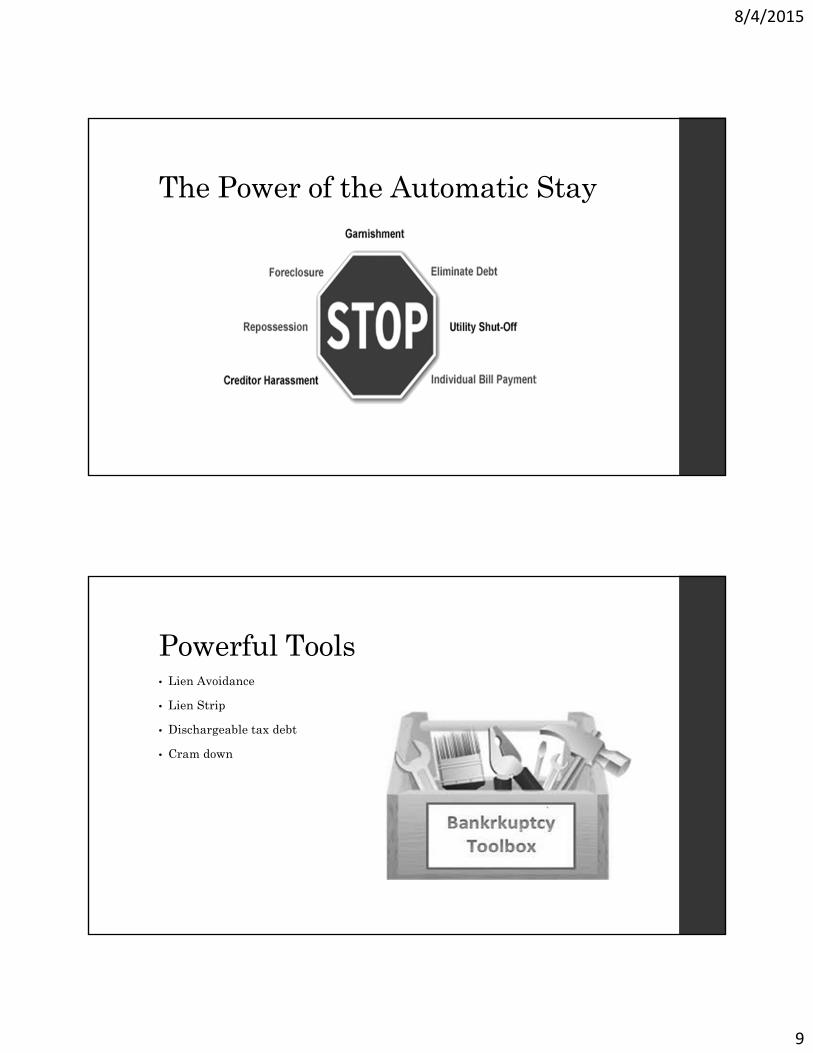

The Power of the Automatic Stay

Powerful Tools • Lien Avoidance

• Lien Strip

• Dischargeable tax debt

• Cram down

8/4/2015

10

Lien Avoidance • The bankruptcy code permits individuals going through bankruptcy to remove liens in

specific situations.

• Obtained by Motion to Avoid Lien

• Remove lien on non-PMSI security interest in household goods, furnishings, wearing apparel, jewelry, books, appliances that are held primarily for the personal use of the debtor

• Remove a lien on a vehicle if the lien is secured on a loan that was not used to purchase the vehicle, the vehicle is exempt and the vehicle is used as a “tool of the trade”

See In re Cleaver, 407 B.R. 354 (B.A.P. 8th Cir. 2009) See In re Cardwell, BK13-40623, 2013 WL 4874323 (Bank. D. Neb. Sept. 12, 2013)

• Remove judgment lien on a home that is the person’s primary residence and the judgment impairs an exemption Three requirements:

Lien resulted from money judgment issued by Court Entitled to an exemption Lien results in a loss of some or all exempt equity

Lien Strip• Tool that allows people who are upside down on their house to strip off the

junior liens (second or third mortgages) converting it to an unsecured loan.

• Must file an adversary proceeding with in the bankruptcy

• Effective upon discharge

• Lien Strip – Chapter 13 v. Chapter 7 Minnesota Housing Fin. Agency v. Schmidt, 765 F.3d 877 (8th Cir. 2014) – junior lien

upon Chapter 13 discharge may be stripped off and avoided. Dewsnup v. Timm, 502 U.S. 410, 1992 – partially underwater mortgage lien could

not be stripped down in Chapter 7. Bank of America, N.A. v. Caulkett, US Supreme Court, 2015 – junior lien may not be

stripped off (even if fully underwater) in Chapter 7 if both secured and allowed.

8/4/2015

11

Dischargeable TaxesThree scenarios:

• General Unsecured Tax Debt Tax return was filed over 2 years ago Tax return due date was over 3 years ago Tax return was assessed over 240 days ago

• Priority Tax Debt Tax return due date was within the past 3 years (watch due dates – sometimes weekends

pay a factor and extensions) Tax was assessed within the past 240 days

• Non-dischargeable Tax Debt (and not priority tax debt) Tax returns filed within the past 2 years Tax due date was over 3 years

**NOTE: watch offer in compromises and bankruptcy proceedings. They will toll the timeframe.

Cram Down• Applies in Chapter 13 proceedings only

• Allows someone to reduce the interest rate and stretch payments out over a longer term in order to lower monthly obligations Supreme Court’s decision in Till v. SCS Credit Corp., 541 U.S. 465 (2004)

• Allows someone to pay back the value of a piece of property opposed to the amount owed on the loan Vehicles

910-day rule

Cross-collateralized loans secured on personal residence Small mortgages/Real estate taxes Household goods and furnishings

One year rule

8/4/2015

12

Warning: Trustee’s Powers• Preference payments: any payment or transfer of value that a debtor makes

in the 90-day period before the debtor files for bankruptcy that is made in connection with a pre-existing debt > $600. Trustee MUST prove:

There was transfer of an interest in the debtor’s property

It was made within 90 days of the date that the debtor filed for bankruptcy

It was made in connection with a prior existing debt

It was made while the debtor was insolvent (the debtor, however, is presumed to have been insolvent during the 90-day period), and

It results in the creditor receiving more than it would otherwise receive if the debtor’s assets were sold off in a liquidating proceeded and the proceeds were distributed equally among all creditors.

Watch out for “insiders” – look back is 1 year

• Debtor gets the same power!

Warning: Trustee’s Powers• 544(b) of the Bankruptcy Code empowers a bankruptcy trustee to avoid any

transfer of an interest of the debtor in property that is voidable under "applicable law" by an unsecured creditor.

• Fraudulent transfers Two Types:

Actual Fraud: transfer made within two years AND made with intent to hinder or defraud a creditor Constructive Fraud: transfer for less than “reasonably equivalent value” AND debtor is unable to

pay debts either at the time or as a result of the transfer

• Watch out! – Under Nebraska State law – longer look back = 4 years Nebraska Fraudulent Transfer Act (UFTA) – 4 year look back

Dominguez v. Eppley Transp. Servs., Inc., 277 Neb. 531, 537, 763 N.W.2d 696, 701 (2009) Comcast of Illinois X v. Multi-Vision Elec., Inc., 504 F. Supp. 2d 740, 748 (D. Neb. 2007) Michael Blumenthal v. Jerry Cronk (In re M & M Mktg., LLC and Premier Fighter, LLC), invol. Ch.

7, BK09-81458-TJM, A11-8096-TJM (Jan. 15, 2013).

• NOTE: Creditor may have defenses (ordinary course of business, new value)

8/4/2015

13

The Power of the Discharge• A bankruptcy discharge releases the debtor from personal liability for

certain specified types of debts. In other words, the debtor is no longer legally required to pay any debts that are discharged.

• Most debts are discharged, but there are exceptions: Tax debts for certain years and other special kinds of tax. Child support or alimony Student loans (unless you can establish an undue hardship) Court fines and penalties Debts to government agencies for fines and penalties Debts intentionally not listed in the bankruptcy schedules

Creditor MAY Challenge the Discharge• Following debts may be contested and deemed non-dischargeable:

Debts obtained by fraud or false pretenses Debts obtained as a result of willful and malicious injury to another Debts obtained within 90 days of filing for bankruptcy if used for purchases of

luxury goods over $600 Cash advances aggregating more than $825 that are under an open end credit

obtained within 70 days of filing for bankruptcy

8/4/2015

14

Reasons for Denial of Discharge• False statements presented to the Court, perjury or other fraudulent acts

• Attempts to transfer or hide assets in order to defraud or hinder your creditors

• Violation of a court order

• Destruction or concealment of books/records

• Failure to complete the required post petition financial management course

• Failure to file necessary schedules or provide requested tax documents

• The debtor is not eligible for a discharge due to the eligibility requirements

Common Traps – Look Out!• Inheritances

• Trusts

• Sale dates

• Mortgage payments in Chapter 13

• Repossessions

• Business owners: corporations v. sole proprietorship

• Conflict of Interests

• Student loans

• Failure to report assets

1

BANKRUPTCY FUNDAMENTALS

Section 1: Chapter 7 v. Chapter 13

The Bankruptcy Code is located at Title 11 of the United States Code. There are

six types of bankruptcy under Title 11 but the most common types of personal

bankruptcy for individuals are Chapter 7 and Chapter 13.

Quick Overview:

• Chapter 7: Liquidation

• “Complete” bankruptcy

• Liquidation of non-exempt assets

• Runs 3-4 months

• Keep secured loans if payments are current

• Must pass “means test”

• Chapter 13: Reorganization Plan

• 3-5 year repayment plan

• Based on disposable income

• “Super discharge”

• Gives homeowner a way of bringing past due

mortgage payments current.

• Debt limitations

Chapter 7

The Chapter 7 is considered complete liquidation. It is the quickest and easiest

form of bankruptcy. In most cases, the process is completed after 90 days.

While the Chapter 7 may offer a quick result (debt free in 90 days) it does involve

a detailed analysis. Two main areas of interest involve: (1) the Debtor’s assets and (2)

the Debtor’s income.

2

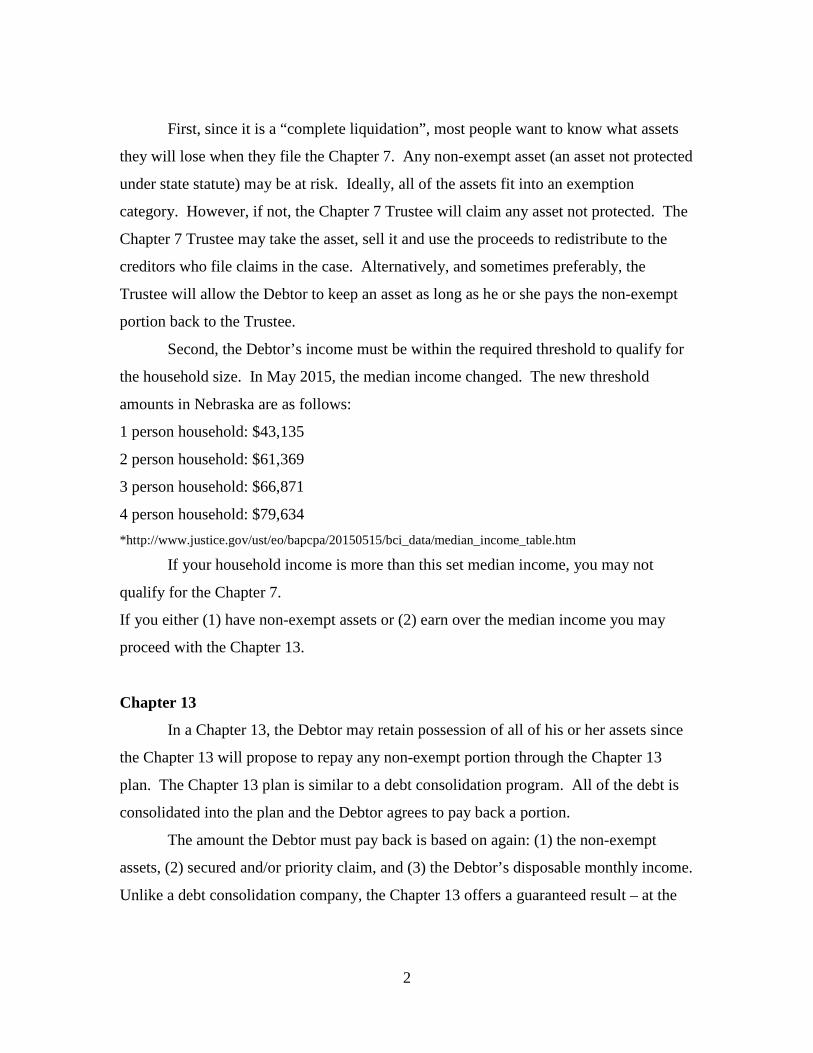

First, since it is a “complete liquidation”, most people want to know what assets

they will lose when they file the Chapter 7. Any non-exempt asset (an asset not protected

under state statute) may be at risk. Ideally, all of the assets fit into an exemption

category. However, if not, the Chapter 7 Trustee will claim any asset not protected. The

Chapter 7 Trustee may take the asset, sell it and use the proceeds to redistribute to the

creditors who file claims in the case. Alternatively, and sometimes preferably, the

Trustee will allow the Debtor to keep an asset as long as he or she pays the non-exempt

portion back to the Trustee.

Second, the Debtor’s income must be within the required threshold to qualify for

the household size. In May 2015, the median income changed. The new threshold

amounts in Nebraska are as follows:

1 person household: $43,135

2 person household: $61,369

3 person household: $66,871

4 person household: $79,634

*http://www.justice.gov/ust/eo/bapcpa/20150515/bci_data/median_income_table.htm

If your household income is more than this set median income, you may not

qualify for the Chapter 7.

If you either (1) have non-exempt assets or (2) earn over the median income you may

proceed with the Chapter 13.

Chapter 13

In a Chapter 13, the Debtor may retain possession of all of his or her assets since

the Chapter 13 will propose to repay any non-exempt portion through the Chapter 13

plan. The Chapter 13 plan is similar to a debt consolidation program. All of the debt is

consolidated into the plan and the Debtor agrees to pay back a portion.

The amount the Debtor must pay back is based on again: (1) the non-exempt

assets, (2) secured and/or priority claim, and (3) the Debtor’s disposable monthly income.

Unlike a debt consolidation company, the Chapter 13 offers a guaranteed result – at the

3

end of the plan, the Debtor is debt free (except if a mortgage is involved or the case

involved non-dischargeable debt like student loans).

Section 2:

The Means Test

The means test was added to the Bankruptcy Code in 2005 under 11 U.S.C.

§707(b) to create a way for determining which individuals qualify for relief in a Chapter

7 bankruptcy based on (1) the number of people in the household and (2) the average

household income for the six months prior to filing.

The means test is also designed to determine if an individual has “disposable

monthly income” (“DMI”) after subtracting certain allowed expenses to make payments

in a Chapter 13 plan. If an individual is determined to have DMI based on the means test,

the individual does not qualify to file a Chapter 7 and must file for relief under a Chapter

13.

The applicable code sections for calculating the means test are:

§707(b)(2)(A)- the means test and the deductions

§707(b)(2)(A)(i)- the formula

§707(b)(2)(A)(ii)-(iv)- the allowable expenses

§707(b)(2)(B)- adjustments for special circumstances.

The attorney must include the means test in the required forms within the

bankruptcy petition. The forms are accessible at

http://www.uscourts.gov/bkforms/bankruptcy_forms.html. The applicable form in a

Chapter 7 is B22A and the applicable form in a Chapter 13 is B22C. The purpose of

Form B22A is to determine if a presumption of abuse arises and the purpose of Form

B22C is to determine (1) the applicable commitment period in a Chapter 13 plan and (2)

the disposable income for an above-median individual.

The topics in this section include: (1) the mechanics of the means test, calculating

applicable income and allowed deductions (including possible special circumstance

4

deductions); (2) application in the Chapter 7 and the presumption of abuse; and, (3)

application in the Chapter 13.

1. Calculating the Applicable Income

In either a Chapter 7 or a Chapter 13 the same factors form the basis for

determining the applicable income. The means test requires a calculation of an

individual’s “current monthly income” (“CMI”). The code defines CMI under

§101(10A). CMI most commonly means “the average monthly income from all sources

that the debtor receives (or household receives if more than one member) without regard

to whether such income is taxable income during the 6-month period ending on the last

day of the calendar month immediately preceding the date of the commencement of the

case.” 11 U.S.C. 101(10A). This test assumes that this 6-month time period is an

accurate projection on an individual’s anticipated future income.

An individual’s income for means test calculation purposes consists of all

employment income, as well as additional household income that is received on a regular

basis. This may include contributions from a renter, unemployment compensation,

worker’s compensation benefits, regular pension/retirement distributions and regular

contributions from a family member (either in or outside of the household). An

individual whose income is from self-employment may report gross receipts less

necessary and reasonable expenses. However, it is extremely important to make sure the

business expenses for the self-employed are not part of the allowed standard deductions

already accounted for in the forms in an above-median case. Typically, irregular sources

of income are not counted towards the CMI including, IRA distributions, gambling

winnings, tax refunds and loans/gifts from family. The CMI also excludes benefits

received under the Social Security Act, payments to victims of war crimes or against

humanity and payments to victims of terrorism.

Once the CMI is calculated it is applied to the standard set by each state to

determine if the individual’s income puts him above or below the median income. The

median income is a figure set by each state and adjusted for inflation periodically.

5

If an individual’s income is below the applicable median income, or “below-

median,” they are determined to have zero disposable income on the means test and

would qualify for a Chapter 7 under this test. However, if an individual’s income is over

the median income, or “above-median,” he or she must then continue means test

calculations by deducting out certain statutorily defined living expenses and payment of

secured and priority debt.

2. Determining and calculating allowed deductions

Determining allowed deductions is similar in a Chapter 7 and a Chapter 13. If the

individual’s income classifies him as over the median income, the applicable deductions

must be applied to determine if an individual has disposable monthly income (“DMI”).

The applicable living deductions are set amounts based on the local and national IRS

standards. These deductions include: food, clothing, household supplies, personal needs,

health care, housing and utility costs, transportation and vehicle operation and ownership

expenses. These set amounts increase as the household size (number of dependants)

increases. The means test also accounts for other necessary expenses that are based on

actual expenses. These deductions include: taxes, mandatory payroll deductions, term

life insurance monthly payments, court-ordered payments, education expenses for

physically or mentally challenged children, childcare expenses (other than education),

health care costs (not insurance or health savings account) and telecommunication

services (internet service). Additional actual expenses allowed include health insurance,

disability insurance, health savings account, continued contributions to the care of

household or family members who are either elderly, chronically ill or disabled,

education expenses for dependent children less than 18 with a cap of $147.92 per child,

charitable contributions and additional justified food or household expenses not already

accounted for or above the IRS standards. Finally, the last section of permissible

deductions includes deductions for debt payment. This includes secured or priority debt

payments.

The means test also allows special circumstance deductions. These deductions

must be justified if they are taken in addition to the standard deductions provided for

6

under the IRS allotments. For example, special circumstance deductions may be allowed

for high commuting costs, married individuals maintaining separate households, special

needs for children or other legitimate expenses above those specifically allowed.

After accounting for all of the allowed deductions, an individual may qualify for a

Chapter 7 if the DMI is less than the presumption of abuse limit. If the DMI is

determined to be over the presumption of abuse limit, the debtor may only file a Chapter

13.

3. Application in a Chapter 7 and the Presumption of Abuse

If an individual is above-median and has DMI after the applicable expenses and

deductions are applied, the formula in §707(b)(2) must be utilized to determine if the case

is presumed abusive. Under §707(b)(2), the presumption of abuse arises and that

individual does not qualify to file a Chapter 7 if the debtor’s monthly disposable income

multiplied by 60 is either (1) greater than or equal to 25 percent of the debtor’s non-

priority unsecured claims or $7,025, whichever is greater; or (2) greater than or equal to

$11,725. Under §707(b)(3), the case may also be dismissed due to bad faith or based on

the totality of the circumstances (i.e. the individual has DMI according to their projected

income and expenses).

There are cases where the presumption of abuse arises but the individual may still

qualify for relief under a Chapter 7. This occurs in rare situations where the means test

calculated CMI is not an accurate reflection of the expected CMI due to a loss of

employment or permanent change in income. In these cases the presumption must be

rebutted to prove the DMI is inaccurate based on actual anticipated income and expenses.

The means test does not apply to individuals with primarily non-consumer debt

(i.e. business debt). According to 11 U.S. C. §101(8), consumer debt is defined as debt

incurred for personal, family or household purposes. Tax debt is considered non-

consumer debt. Most courts look to the intention of the debt at the time it was incurred

and not the nature of the debt at the time of the bankruptcy filing.

4. Application in a Chapter 13

7

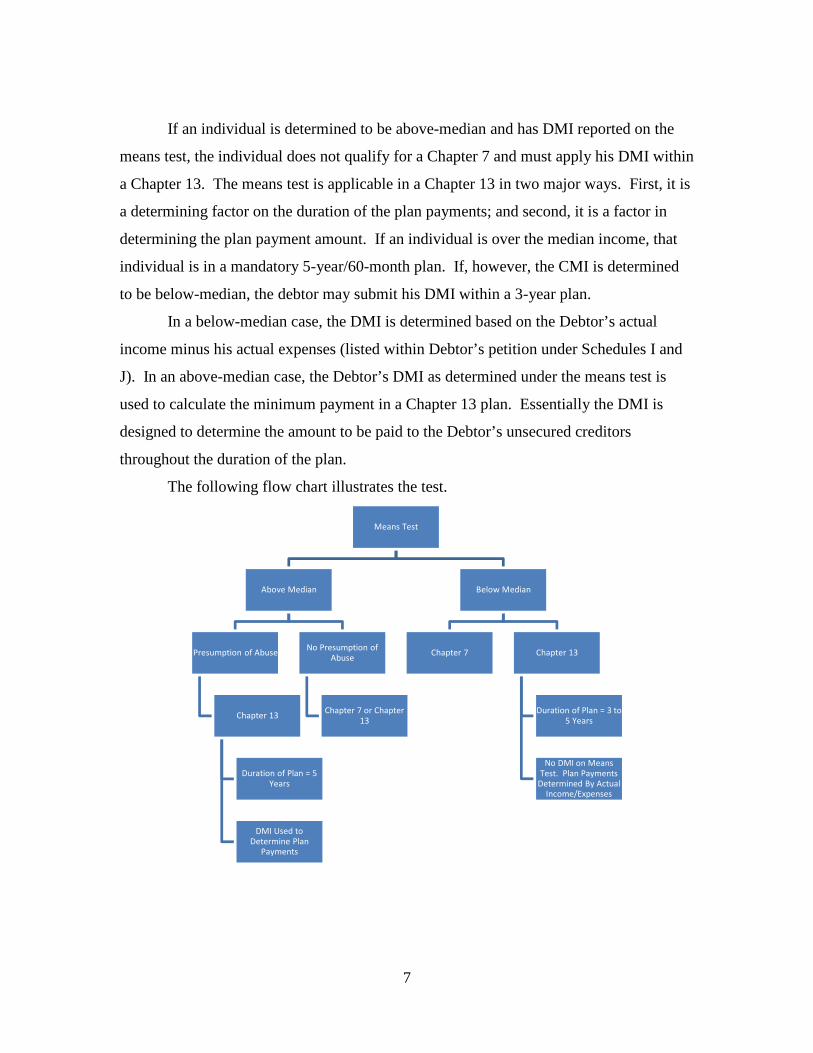

If an individual is determined to be above-median and has DMI reported on the

means test, the individual does not qualify for a Chapter 7 and must apply his DMI within

a Chapter 13. The means test is applicable in a Chapter 13 in two major ways. First, it is

a determining factor on the duration of the plan payments; and second, it is a factor in

determining the plan payment amount. If an individual is over the median income, that

individual is in a mandatory 5-year/60-month plan. If, however, the CMI is determined

to be below-median, the debtor may submit his DMI within a 3-year plan.

In a below-median case, the DMI is determined based on the Debtor’s actual

income minus his actual expenses (listed within Debtor’s petition under Schedules I and

J). In an above-median case, the Debtor’s DMI as determined under the means test is

used to calculate the minimum payment in a Chapter 13 plan. Essentially the DMI is

designed to determine the amount to be paid to the Debtor’s unsecured creditors

throughout the duration of the plan.

The following flow chart illustrates the test.

Means Test

Above Median

Presumption of Abuse

Chapter 13

Duration of Plan = 5Years

DMI Used toDetermine Plan

Payments

No Presumption ofAbuse

Chapter 7 or Chapter13

Below Median

Chapter 7 Chapter 13

Duration of Plan = 3 to5 Years

No DMI on MeansTest. Plan Payments

Determined By ActualIncome/Expenses

8

Section 3: Required Disclosures

The attorney should have a standard form or set of forms that is completed during

each potential new client interview and retained whether or not the client retains the firm

as counsel. At the conclusion of the client interview a checklist of documents should be

provided to the client. The checklist should include the paperwork required to prepare a

bankruptcy petition including, but not limited to:

• Last six months of pay stubs/income records;

• Last six months of bank statements;

• Tax returns and W-2s for last two years;

• Bills;

• Statement of assets.

In addition to the checklist, several disclosures are required to be provided to the

prospective client pursuant to the Bankruptcy Code. These disclosures provide important

information to the client, including basic bankruptcy information, a summary of the four

types of bankruptcy proceedings that may be commenced, the requirement of completing

a credit counseling session and receiving certification (must be completed at least one

calendar day before petition is filed), and briefly describes bankruptcy crimes and notifies

you that the Attorney General may examine all information you supply in connection

with a bankruptcy case. Examples of these disclosures appear below.

Sample Disclosure #1

NOTICE TO INDIVIDUAL CONSUMER DEBTOR UNDER § 342(b)OF THE BANKRUPTCY CODE

In accordance with §342(b) of the Bankruptcy Code, this notice: (1) Describes briefly the servicesavailable from credit counseling services; (2) Describes briefly the purposes, benefits and costs ofthe four types of bankruptcy proceedings you may commence; and (3) Informs you aboutbankruptcy crimes and notifies you that the Attorney General may examine all information yousupply in connection with a bankruptcy case. You are cautioned that bankruptcy law iscomplicated and not easily described. Thus, you may wish to seek the advice of an attorney tolearn of your rights and responsibilities should you decide to file a petition. Court employeescannot give you legal advice.

1. Services Available from Credit Counseling Agencies

9

With limited exceptions, § 109(h) of the Bankruptcy Code requires that all individualdebtors who file for bankruptcy relief on or after October 17, 2005, receive a briefing thatoutlines the available opportunities for credit counseling and provides assistance in performing abudget analysis. The briefing must be given within 180 days before the bankruptcy filing. Thebriefing may be provided individually or in a group (including briefings conducted by telephoneor on the Internet) and must be provided by a nonprofit budget and credit counseling agencyapproved by the United States trustee or bankruptcy administrator. The clerk of the bankruptcycourt has a list that you may consult of the approved budget and credit counseling agencies.

In addition, after filing a bankruptcy case, an individual debtor generally must complete afinancial management instructional course before he or she can receive a discharge. Theclerk also has a list of approved financial management instructional courses.

2. The Four Chapters of the Bankruptcy Code Available to Individual Consumer Debtors

Chapter 7: Liquidation: (Total Fee $299)1. Chapter 7 is designed for debtors in financial difficulties that do not have the ability to

pay their existing debts. Debtors whose debts are primarily consumer debts are subject to a"means test" designed to determine whether the case should be permitted to proceed underchapter 7. If your income is greater than the median income for your state of residence and familysize, in some cases, creditors have the right to file a motion requesting that the court dismiss yourcase under § 707(b) of the Code. It is up to the court to decide whether the case should bedismissed.

2. Under chapter 7, you may claim certain of your property as exempt under governinglaw. A trustee may have the right to take possession of and sell the remaining property that is notexempt and use the sale proceeds to pay your creditors.

3. The purpose of filing a chapter 7 case is to obtain a discharge of your existing debts.If, however, you are found to have committed certain kinds of improper conduct described in theBankruptcy Code, the court may deny your discharge and, if it does, the purpose for which youfiled the bankruptcy petition will be defeated.

4. Even if you receive a general discharge, some particular debts are not dischargedunder the law. Therefore, you may still be responsible for most taxes and student loans; debtsincurred to pay nondischargeable taxes; domestic support and property settlement obligations;most fines, penalties, forfeitures, and criminal restitution obligations; certain debts which are notproperly listed in your bankruptcy papers; and debts for death or personal injury caused byoperating a motor vehicle, vessel, or aircraft while intoxicated from alcohol or drugs. Also, if acreditor can prove that a debt arose from fraud, breach of fiduciary duty, or theft, or from awillful and malicious injury, the bankruptcy court may determine that the debt is not discharged.

Chapter 13: Repayment of All or Part of the Debts of an Individual with RegularIncome (Total fee $274)

1. Chapter 13 is designed for individuals with regular income who would like to pay allor part of their debts in installments over a period of time. You are only eligible for chapter 13 ifyour debts do not exceed certain dollar amounts set forth in the Bankruptcy Code.

2. Under chapter 13, you must file with the court a plan to repay your creditors all or partof the money that you owe them, using your future earnings. The period allowed by the court to

10

repay your debts may be three years or five years, depending upon your income and other factors.The court must approve your plan before it can take effect.

3. After completing the payments under your plan, your debts are generally dischargedexcept for domestic support obligations; most student loans; certain taxes; most criminal finesand restitution obligations; certain debts which are not properly listed in your bankruptcy papers;certain debts for acts that caused death or personal injury; and certain long term securedobligations.

Chapter 11: Reorganization ($1000 filing fee, $39 administrative fee: Total fee$1039)

Chapter 11 is designed for the reorganization of a business but is also available toconsumer debtors. Its provisions are quite complicated, and any decision by an individual to file achapter 11 petition should be reviewed with an attorney.

Chapter 12: Family Farmer or Fisherman ($200 filing fee, $39 administrative fee:Total fee $239)

Chapter 12 is designed to permit family farmers and fishermen to repay their debts over aperiod of time from future earnings and is similar to chapter 13. The eligibility requirements arerestrictive, limiting its use to those whose income arises primarily from a family-owned farm orcommercial fishing operation.

3. Bankruptcy Crimes and Availability of Bankruptcy Papers to Law Enforcement Officials

A person who knowingly and fraudulently conceals assets or makes a false oath orstatement under penalty of perjury, either orally or in writing, in connection with a bankruptcycase is subject to a fine, imprisonment, or both. All information supplied by a debtor inconnection with a bankruptcy case is subject to examination by the Attorney General actingthrough the Office of the United States Trustee, the Office of the United States Attorney, andother components and employees of the Department of Justice.WARNING: Section 521(a)(1) of the Bankruptcy Code requires that you promptly file detailedinformation regarding your creditors, assets, liabilities, income, expenses and general financialcondition. Your bankruptcy case may be dismissed if this information is not filed with the courtwithin the time deadlines set by the Bankruptcy Code, the Bankruptcy Rules, and the local rulesof the court.

Sample Disclosure #2

STATEMENT OF INFORMATION REQUIRED BY 11 U.S.C. §341

BANKRUPTCY LAW IS A FEDERAL LAW. THIS SHEET GIVES YOU SOMEGENERAL INFORMATION ABOUT WHAT HAPPENS IN A BANKRUPTCY CASE.THE INFORMATION HERE IS NOT COMPLETE. YOU MAY NEED LEGAL ADVICE.WHEN YOU FILE BANKRUPTCY:

You can choose the kind of bankruptcy that best suits your needs:

• Chapter 7 - A trustee is appointed to take over your property. Any property of value will be soldor turned into money to pay your creditors. You may be able to keep some personal items and

11

possibly real estate depending on the law of the state where you live.

• Chapter 13 - You can usually keep your property, but you must earn wages or have some othersource of regular income and you must agree to pay part of your income to your creditors. TheCourt must approve your repayment plan and your budget. A trustee is appointed and will collectthe payments from you, pay your creditors, and make sure you live up to the terms of yourrepayment plan.

• Chapter 12 - Like chapter 13, but it is only for family farmers.

• Chapter 11 - This is used mostly by businesses. In chapter 11, you may continue to operate yourbusiness, but your creditors and the Court must approve a plan to repay your debts. There is notrustee unless the Judge decides that one is necessary; if a trustee is appointed, the trustee takescontrol of your business and property.If you have filed bankruptcy under one chapter, you may be able to change your case to anotherchapter.

Your bankruptcy may be reported on your credit record for as long as ten years. It can affect yourability to receive credit in the future.

WHAT IS A BANKRUPTCY DISCHARGE AND HOW DOES IT OPERATE?One of the reasons people file is to get a "discharge." A discharge is a Court order which statesthat you do not have to pay most of your debts. Some debts cannot be discharged. For example,you cannot discharge debts for --• child support;• alimony;• most student loans;• Court fines and criminal restitution; and• personal injury caused by drunk driving or under the influence of drugs.

The discharge only applies to debts that arose before the date you filed.

Also, if the Judge finds that you received money or property by fraud, that debt may not bedischarged.

It is important to list all your property and debts in your bankruptcy schedules. If you do not list adebt, for example, it is possible the debt will not be discharged.

The judge can also deny your discharge if you do something dishonest in connection with yourbankruptcy case, such as destroy or hide property, falsify records, or lie, or if you disobey a Courtorder.

You can only receive a chapter 7 discharge once every eight years. No one can make you pay adebt that has been discharged, but you can voluntarily pay any debt you wish to pay. You do nothave to sign a reaffirmation agreement or any other kind of document to do this.

12

Some creditors hold a secured claim (for example, the bank that holds the mortgage on yourhouse or the loan company that has a lien on your car). You do not have to pay a secured claim ifthe debt is discharged, but the creditor can still take the property.

WHAT IS A REAFFIRMATION AGREEMENT?Even if a debt can be discharged, you may have special reasons why you want to promise to payit. For example, you may want to work out a plan with the bank to keep your car. To promise topay the debt, you must sign and file a reaffirmation agreement with the Court. Reaffirmationagreements are under special rules and are voluntary. They are not required by bankruptcy law orby any other law. Reaffirmation agreements -• must be voluntary;• must not place too heavy a burden on you or your family;• must be in your best interest; and• can be cancelled anytime before the Court issues your discharge or within 60 days after theagreement is filed with the Court, whichever gives you the most time.

If you are an individual and you are not represented by an attorney, the Court must hold a hearingto decide whether to approve the reaffirmation agreement. You must file the agreement with theCourt and request a hearing. At the hearing, the court must find that the agreement is in your bestinterests and enter an order approving the agreement. The agreement will not be legally bindinguntil the Court approves it.

If you reaffirm a debt and then fail to pay it, you owe the debt the same as though there was nobankruptcy. The debt will not be discharged and the creditor can take action to recover anyproperty on which it has a lien or mortgage. The creditor can also take legal action to recover ajudgment against you.

IF YOU WANT MORE INFORMATION OR HAVE QUESTIONS ABOUT HOW THEBANKRUPTCY LAWS AFFECT YOU, YOU MAY NEED LEGAL ADVICE. THETRUSTEE IN YOUR CASE IS NOT RESPONSIBLE FOR GIVING YOU LEGALADVICE.

13

Sample Disclosure #3

DISCLOSURE REQUIRED PURSUANT TO11 U.S.C. §527(b)

IMPORTANT INFORMATION ABOUT BANKRUPTCY ASSISTANCE SERVICES FROMAN ATTORNEY OR BANKRUPTCY PETITION PREPARER.

If you decide to seek bankruptcy relief, you can represent yourself, you can hire anattorney to represent you, or you can get help in some localities from a bankruptcy petitionpreparer who is not an attorney. THE LAW REQUIRES AN ATTORNEY ORBANKRUPTCY PETITION PREPARER TO GIVE YOU A WRITTEN CONTRACTSPECIFYING WHAT THE ATTORNEY OR BANKRUPTCY PETITION PREPARERWILL DO FOR YOU AND HOW MUCH IT WILL COST. Ask to see the contract beforeyou hire anyone.

The following information helps you understand what must be done in a routinebankruptcy case to help you evaluate how much service you need. Although bankruptcy can becomplex, many cases are routine.

Before filing a bankruptcy case, either you or your attorney should analyze youreligibility for different forms of debt relief available under the Bankruptcy Code and which formof relief is most likely to be beneficial for you. Be sure you understand the relief you can obtainand its limitations. To file a bankruptcy case, documents called a Petition, Schedules andStatements of Financial Affairs, as well as in some cases a Statement of Intention need to beprepared correctly and filed with the bankruptcy court. You will have to pay a filing fee to thebankruptcy court. Once your case starts, you will have to attend the required first meeting ofcreditors where you may be questioned by a court official called a “trustee” and by creditors.

If you choose to file a chapter 7 case, you may be asked by a creditor to reaffirm a debt.You may want help deciding whether to do so. A creditor is not permitted to coerce you intoreaffirming your debts.

If you choose to file a chapter 13 case in which you repay your creditors what you canafford over 3 to 5 years, you may also want help with preparing your chapter 13 plan and with theconfirmation hearing on your plan which will be before a bankruptcy judge.

If you select another type of relief under the Bankruptcy Code other than chapter 7 orchapter 13, you will want to find out what should be done from someone familiar with that typeof relief.

Your bankruptcy case may also involve litigation. You are generally permitted torepresent yourself in litigation in bankruptcy court, but only attorneys, not bankruptcy petitionpreparers, can give you legal advice.

14

Section 4:

Due Diligence Requirement and Outside Audits

The main component in filing a bankruptcy is an accurate petition. An accurate

petition requires due diligence. Under 11 U.S.C. §707(b)(4), the attorney is required to

perform due diligence before filing a case. Filing an accurate bankruptcy petition is an

extremely difficult and extensive process that revolves around documentation, research

and proper disclosure. Since a bankruptcy petition has several parts it is imperative that

all of the parts coincide and create a cohesive description of each individual’s financial

story. A properly prepared petition requires due diligence and will almost always

guarantee a smooth and successful process.

1. Documentation

The first main component is proper documentation. This category is very case

specific since each individual’s situation is different. The most commonly required

documentation includes: pay stubs and bank statements for the previous six months, tax

returns for the previous two years, statements on all other sources of income including

pension, Social Security, VA benefits, workers’ compensation, unemployment and

disability benefits, life insurance statements, retirement account/investment statements,

divorce decree including property settlement agreements and child support orders, child

support payment history, vehicle title or registrations, bills, insurance declarations, and

loan documents.

These documents support the reported material in the petition and provide insight

into the debtor’s financial dealings. For example, reviewing a life insurance statement or

retirement account statement may provide important information regarding recent

contributions and account opening date. It will also provide the current value of the

account which is reported as an asset. Many times these documents will also verify

information of which the Debtor is either unaware or uncertain. An individual’s bank

statements can offer invaluable information regarding prior financial transactions.

Auditing deposits and withdrawals within a bank account will help determine recent

15

credit card activity, missing income and potential preference payments. The bank

statements may also be the only place to discover any potential possible wrong doing that

may be detrimental to a client’s case. An individual’s tax returns also offer information

required for a complete petition. A tax return may report income not previously

disclosed, and/or interest in a business or property. The returns will also help in

determining tax rates necessary for Form 22 means test calculations. Vehicle titles can

prove the validity of a lien.

2. Research

The second component in performing due diligence is research. Reviewing

reports and databases such as the credit report, Lexis Nexis asset check, Online Court

Case Searches and Pacer are useful tools when preparing a petition. The credit report

may help identify unknown creditors and tax liens. It will also supply contact addresses

necessary to guarantee the creditor receives proper notice. A Lexis Nexis asset check

will report all real property and vehicles registered in the debtor’s name. This helps assist

in reporting transfers and identifying missing assets. The asset check may also uncover

an interest in a trust account or unknown judgments, UCC and judgment liens.

Researching court cases online will help identify all pending legal action against an

individual. This information may produce additional creditors and additional contacts for

notice purposes. A Pacer check will verify any prior bankruptcy filing to analyze

eligibility requirements. Another helpful tool is the County Assessor’s public

information. This will help in determining the fair market value of real property with

supporting documentation. A simple search of the internet may also provide helpful

information regarding the value of assets.

3. Disclosure

Finally, the last component in preparing a complete petition is disclosure.

Disclosure of all information received through the provided documentation, independent

research and information provided by the client is essential. A debtor may report all of

his assets but may need assistance in obtaining values, determining what an asset consists

of and properly identifying his interest. For instance, a debtor may be owed money when

16

he files but may not consider the money owed an asset to include in his schedules. An

individual is also required to provide bank balances on the day of filing his case. It is

important to strategically plan the filing date based on the available balance of funds in a

bank account. Proper disclosure should also include information on expected tax refunds.

The proportional anticipated tax refund at the time of filing is an asset and should be

listed.

Outside Audits

The US Trustee’s office may randomly select a case for an outside audit. Outside

audits are easier to complete if due diligence is performed before the filing of the case.

The selected audit company reviews documents to determine if a material misstatement

was made within the petition. Obviously, reviewing this information prior to filing

creates a quick, simple and successful audit process. If an attorney conducted due

diligence prior to filing, the audit will produce the same substantive information

contained in the petition.

The documents requested by the audit company include: bank statements and pay

stubs for the prior six months through the filing date, tax returns for the two years prior to

the filing date, all investment, retirement and life insurance statements covering the six

months prior to filing, divorce decree and related property settlement or child support

orders within three years of filing and additional documents if self-employed. The audit

company also requires that all deposits and withdrawals from the bank statements

identify the source and recipient of funds over $500.00.

If these documents are requested prior to the filing, the audit company will not

uncover any substantive issues not already disclosed in the petition. Compiling the data

at this stage is also easier if these documents have been reviewed and analyzed prior to

the filing. Since being selected for an audit may be stressful for a client, reviewing and

addressing issues prior to filing will help prevent additional concerns.

Section 5:

Preparing for Filing: Petition, Schedules and Statements

17

All documents are filed using an Electronic Filing System. Once an attorney is

registered to use this system, filing a petition and related documents is quick and easy.

Preparing to file documents includes converting the documents into a PDF file, redacting

all security related information and reviewing the file to fit the size qualifications and

legibility. The PDF file should be no larger than 40 pages or 3MB, whichever is larger.

If the document is larger than 40 pages or 3MB the file should be separated and scanned

in portions for submission. A file should not be submitted without redacting security

information including Social Security numbers, minor children’s names and bank account

numbers. All files should also be reviewed for blank pages, unnecessary information and

clarity before filing.

The system allows for both an automatic upload of the complete petition, with all

related schedules and the option to file each schedule separately, this includes an

emergency petition, consisting of only the voluntary petition and a list of creditors. The

schedules and related documents may then be filed at a later time individually. The

system also allows electronic filing for all motions, pay stubs, credit counseling

certificates and supporting documents. The electronic filing system transmits notices of

all filings to interested registered parties via email. These electronic notices allow a

registered attorney to monitor a case and all filings within a case easily. If an interested

attorney would like to receive notices of filings within a case, the attorney may file a

notice of appearance and request for notices.

Section 6:

Transmitting Required Documents to the Trustee

Once the Chapter 7 or Chapter 13 petition has been filed there are still additional

documents to transmit to the Trustee.

Local rules and Trustee preferences may dictate what type of documents must be

sent, but the Bankruptcy Code states that the prior year tax returns must be provided at

least 7 days prior to the 341 hearing.

Pursuant to 11 U.S.C. 521-

18

(e)(2)(A) The debtor shall provide -

(i) not later than 7 days before the date first set for the first meeting of

creditors, to the trustee a copy of the Federal income tax return required under

applicable law (or at the election of the debtor, a transcript of such return) for

the most recent tax year ending immediately before the commencement of the

case and for which a Federal income tax return was filed; and

(ii) at the same time the debtor complies with clause (i), a copy of such return

(or if elected under clause (i), such transcript) to any creditor that timely

requests such copy.

(B) If the debtor fails to comply with clause (i) or (ii) of subparagraph (A), the

court shall dismiss the case unless the debtor demonstrates that the failure to so

comply is due to circumstances beyond the control of the debtor.

Pursuant to 11 U.S.C. 1308 –

(a) Not later than the day before the date on which the meeting of the creditors is

first scheduled to be held under section 341(a), if the debtor was required to file a

tax return under applicable nonbankruptcy law, the debtor shall file with

appropriate tax authorities all tax returns for all taxable periods ending during the

4-year period ending on the date of the filing of the petition.

United States Bankruptcy Appellate PanelFOR THE EIGHTH CIRCUIT

______

No. 08-6052______

In re: Jeremy Eugene Cleaver, *Formerly doing business as JC Auto * Repair; Michelle Ann Cleaver, *

*Debtors. *

*Jeremy Eugene Cleaver; Michelle *Ann Cleaver, *

*Debtors – Appellants, *

* Appeal from the United Statesv. * Bankruptcy Court for the

* Southern District of IowaAlbert Warford, *

*Trustee – Appellee, *

*Kris Earlywine, *

*Creditor – Appellee. *

______

Submitted: May 13, 2009Filed: June 11, 2009

______

Before KRESSEL, Chief Judge, MAHONEY and VENTERS, Bankruptcy Judges.______

KRESSEL, Chief Judge.

Case: 08-6052 Page: 1 Date Filed: 06/11/2009 Entry ID: 3556267

2

The debtors appeal an order of the bankruptcy court denying a motion for“reconsideration” of an order denying a motion to avoid a nonpossessory,nonpurchase-money security interest in a semi-tractor truck. Because we hold thatlien avoidance is a federal remedy to be determined under federal law, we reverse andremand for further proceedings consistent with this opinion.

BACKGROUND

Jeremy and Michelle Cleaver borrowed $42,381.93 from Kris Earlywine inearly 2008. To secure the loan, the Cleavers granted Earlywine a security interest intheir 2000 Kenworth W900B DS Semi-Tractor Truck that they already owned. TheCleavers filed a voluntary bankruptcy petition under chapter 13 on August 12, 2008.They listed the truck as an asset on their Schedule B, valuing it at $21,000.00. Theyclaimed an exemption in the truck on their Schedule C in the amount of $7,000 underIowa Code § 627.6(9), which provides for the exemption of “The debtor's interest inone motor vehicle, not to exceed in value seven thousand dollars.” No one objectedto the exemption claim. As a result, the exemption was allowed. 11 U.S.C. § 522(l).

On September 14, 2008, the Cleavers filed a motion to avoid Earlywine’snonpossessory, nonpurchase-money security interest in the truck under 11 U.S.C. §522(f)(1)(B)(ii). Earlywine did not object to the motion but the trustee, Albert C.Warford, did. A hearing was held on the motion on September 16, 2008, and thebankruptcy court denied the motion in an oral ruling. Consistent with its previousrulings in other cases, the bankruptcy court held that because the debtors could notexempt the truck as a “tool of the trade” under Iowa law, they were not permitted toavoid the lien as a “tool of the trade” under the Bankruptcy Code’s lien avoidanceprovisions. See Matter of Van Pelt, 83 B.R. 617 (S.D. Iowa 1987). The court notedthat although Iowa courts had not uniformly agreed with the Van Pelt decision, theappellate courts had not had occasion to review the issue. The Cleavers filed a motion

Case: 08-6052 Page: 2 Date Filed: 06/11/2009 Entry ID: 3556267

3

for relief from the September 16 order denying their motion to avoid Earlywine’s lien,and the court denied the motion for relief on November 13, 2008. The debtors appeal.

Standard of Review

The sole issue on appeal is a question of law, which we review de novo.DeBold v. Case, 452 F.3d 756, 761 (8th Cir. 2006); Green Tree Servicing, LLC v.Coleman (In re Coleman), 392 B.R. 767, 769 (B.A.P. 8th Cir. 2008).

DISCUSSION

The issue on appeal is whether the debtors, who have exempted a motor vehicleunder Iowa’s exemption statute, are entitled to prove that the vehicle is a tool of thetrade under 11 U.S.C. § 522(f)(1)(B)(ii) in order to avoid a nonpossessory,nonpurchase-money security interest in that vehicle. We hold that they are.

The Bankruptcy Code allows debtors to avoid liens on certain property thatCongress deemed “necessary to give substance to the concept of a fresh start. Thisproperty is required for the maintenance, health and welfare of the debtor and hisfamily, and avoids literal destitution.” Thorp Credit and Thrift Co. v. Pommerer (Inre Pommerer), 10 B.R. 935, 946 (Bankr. D. Minn. 1981). Congress included “toolsof the trade” in a class of property to receive the additional protection of lienavoidance. 11 U.S.C. § 522(f)(1) provides:

(f)(1) Notwithstanding any waiver of exemptions but subject toparagraph (3), the debtor may avoid the fixing of a lien on an interest ofthe debtor in property to the extent that such lien impairs an exemptionto which the debtor would have been entitled under subsection (b) of thissection, if such lien is—

. . .

Case: 08-6052 Page: 3 Date Filed: 06/11/2009 Entry ID: 3556267

4

(B) a nonpossessory, nonpurchase-money security interest in any—

. . .

(ii) implements, professional books, or tools, of the trade of the debtoror the trade of a dependent of the debtor . . . .

“Tool of the trade” is not a term defined in the Bankruptcy Code. It is a term of art.The term also appears in § 522(d)(6), but § 522(d)(6) and § 522(f)(1) do not refer toeach other. The Bankruptcy Code’s use of this term of art creates conflicts where, ashere, a state has concluded that under its exemption scheme vehicles may never beconsidered tools of the trade, but the federal courts have interpreted the BankruptcyCode’s usage as sometimes extending to vehicles.

Iowa has opted out of the bankruptcy exemption scheme. See 11 U.S.C. §522(b)(2). As a result, a debtor in Iowa is limited to exemptions allowed by Iowa lawand federal non-bankruptcy law. The parties agree that, under Iowa law, a motorvehicle may not be exempted as a tool of the trade. The Iowa Supreme Court has heldthat because the Iowa exemption statute “mentions and classifies separately ‘theproper tools, instruments’ used in the operation of farm business, and ‘the wagon orother vehicle,’” trucks and automobiles “come within the latter classification and musttherefore be considered strictly as vehicles, and not as . . . tools.” Farmers’ Elevator& Live Stock Co. v. Satre, 195 N.W. 1011, 1013 (Iowa 1923).

Although Iowa has opted out of the federal exemption scheme, the opt-out onlypertains to the specific menu of exemptions to which a debtor is entitled. The IowaSupreme Court’s rulings on the exemption statute’s usage of the term “tools of thetrade” control for the purpose of determining Iowa debtors’ allowable exemptions.However, lien avoidance is a federal remedy to be interpreted by the federal courts.Heape v. Citadel Bank of Independence (In re Heape), 886 F.2d 280, 282 (10th Cir.1989); Matter of Thompson, 750 F.2d 628, 630 (8th Cir. 1984). “Although a statemay elect to control what property is exempt under state law, federal law determines

Case: 08-6052 Page: 4 Date Filed: 06/11/2009 Entry ID: 3556267

5

the availability of a lien avoidance.” Thompson at 630; see also Hart v. Crawford (Inre Hart), 332 B.R. 439, 444 (D. Wyo. 2005) (“federal law controls exemptionsgenerally and exemption procedures”). “[T]he ‘opt out’ provision of § 522(b)(2)(A)allows state law to determine only what property may be exempted from the estate.”In re Graettinger, 95 B.R. 632, 634 (Bankr. N.D. Iowa 1988).

While state law may govern the allowance of an exemption in the first instance,occasionally the Bankruptcy Code modifies some state exemption rights to preventabuse or overreaching by debtors or creditors. For instance, § 522(b)(3)’s domicileprovisions attempt to eliminate any incentive for debtors to move to another state onthe eve of bankruptcy in order to protect their assets under more generous exemptionstatutes. Section 522(o) reduces debtors’ homestead exemptions to the extent that the“value is attributable to . . . any property that the debtor disposed of in the 10-yearperiod ending on the date of the filing of the petition with the intent to hinder, delay,or defraud a creditor . . . .” 11 U.S.C. §522(o); see generally In re Maronde, 332 B.R.593 (Bankr. D. Minn. 2005). Section 522(p) places a ceiling on debtors’ state lawhomestead exemptions, where the debtor acquired the homestead within 1,215 daysof the petition, and § 522(q) limits the homestead exemption based on certain illegalor unlawful conduct.

Along with limiting exemptions, the Bankruptcy Code offers the remedy of lienavoidance to protect some property that might be essential to a debtor’s rehabilitationand fresh start. As expressed in the legislative history, Congress was concerned thata creditor might undermine a debtor’s fresh start by acquiring liens in property thatthe debtor had already purchased and that was essential to the debtor’s rehabilitationbut not necessarily of real value to creditors:

Creditors have developed techniques that enable them to avoid theeffects of a debtor’s bankruptcy, and bankrupts have sufferedaccordingly. Frequently they come through bankruptcy littler [sic]better off than they were before. Overbroad security interests on all of

Case: 08-6052 Page: 5 Date Filed: 06/11/2009 Entry ID: 3556267

1 As illustrated by this case, the Southern District of Iowa has adopted theposition that debtors seeking to avoid liens pursuant to § 522(d) must look to Iowastate law. Matter of Van Pelt, 83 B.R. 617 (Bankr. S.D. Iowa 1987) (applying statelaw and denying lien avoidance on vehicles). The Northern District has held that adebtor may avoid a lien on a vehicle that is a tool of the trade as a matter of federallaw even though state law does not allow a debtor to exempt a vehicle as a tool of thetrade. In re Graettinger, 95 B.R. 632, 634 (Bankr. N.D. Iowa 1988) (applying federallaw and granting lien avoidance on vehicle). The Van Pelt decision was issued oneday before the Northern District avoided a vehicle lien as a tool of the trade. The

6

a consumer’s household and personal goods, reaffirmations, limited stateexemption laws, and litigation over dischargeability of certain debts haveall contributed to the consumer debtor’s post-bankruptcy plight.

H.R.Rep. No. 95-595, at 117, reprinted in 1978 U.S.C.C.A.N. 5787, 6077. Thelegislative history indicates that Congress intended the lien avoidance provisions toprotect unsophisticated consumer debtors from overreaching creditors:

[T]he bill gives the debtor certain rights not available under current lawwith respect to exempt property . . . . Frequently, creditors lendingmoney to a consumer debtor take a security interest in all of the debtor’sbelongings, and obtain a waiver by the debtor of his exemptions. Inmost of these cases, the debtor is unaware of the consequences of theforms he signs. The creditor’s experience provides him with asubstantial advantage. If the debtor encounters financial difficulty,creditors often use threats of repossession of all of the debtor’shousehold goods as a means of obtaining payment.

. . .

Such security interests have too often been used by over-reachingcreditors. The bill eliminates any unfair advantage creditors have.

Id. at 6087-6088.

Iowa bankruptcy courts have split1 on the issue of whether a debtor can exempt

Case: 08-6052 Page: 6 Date Filed: 06/11/2009 Entry ID: 3556267

creditor in Graettinger appealed to the district court, which remanded to thebankruptcy court “for the limited purpose of determining the application of Van Peltto these facts.” Graettinger at 633. On remand, the bankruptcy court declined tofollow the Van Pelt reasoning, establishing a split that has apparently persisted forover twenty years.

7

a vehicle under state law and avoid the lien as a tool of the trade under federal law,where the vehicle could not be considered a tool of the trade under state law. The factthat an exemption claimed by debtors is in property that is not considered a “tool ofthe trade” under state law is irrelevant to the issue of whether the lien can be avoided.The Eighth Circuit has adopted a test to determine whether a vehicle is a tool of thetrade, and that is: “the reasonable necessity of the item to the debtor’s trade orbusiness.” Prod. Credit Assoc. of St. Cloud v. LaFond (In re LaFond), 791 F.2d 623,627 (8th Cir. 1986) (quoting Seacord v. Commerce Bank of Blue Hills (In re Seacord),7 B.R. 121 (Bankr. W.D. Mo. 1980)).

The plain language of the statute requires the application of federal bankruptcylaw to determine whether a lien may be avoided, but if there was any doubt, theSupreme Court resolved it in Owen v. Owen, 500 U.S. 305, 111 S. Ct. 1833, 114 L.Ed. 2d 350 (1991). In Owen, the Court held that judicial liens encumbering exemptproperty can be avoided under 11 U.S.C. § 522(f), even “when the State has definedthe exempt property in such a way as specifically to exclude property encumbered byjudicial liens.” Id. at 306, 111 S. Ct. at 1834. To determine whether a lien may beavoided under § 522(f), courts should ask whether the lien impairs an exemption towhich the debtor would have been entitled but for the lien at issue. The Courtconcluded that a state’s “exclusion of certain liens from the scope of its homesteadprotection does not achieve a similar exclusion from the Bankruptcy Code's lienavoidance provision.” Id. at 313-14, 111 S. Ct. at 1838. The Court reasoned, “Wehave no basis for pronouncing the opt-out policy absolute, but must apply it alongwith whatever other competing or limiting policies the statute contains.” Id. at 313,111 S. Ct. at 1838. Based on the plain meaning of the statute and the Owen decision,we conclude that the language of the statute, “exemption to which the debtor would

Case: 08-6052 Page: 7 Date Filed: 06/11/2009 Entry ID: 3556267

8

have been entitled under subsection (b),” does not require the exemption to be a “toolof the trade” exemption specifically, but rather any exemption under subsection (b)to which the debtor would have been entitled. 11 U.S.C. § 522(f)(1).

Conclusion

For the reasons stated, we reverse and remand to the bankruptcy court forfurther proceedings consistent with this opinion. On remand, the debtors are entitledto try to prove that the truck is a tool of the trade as a matter of federal law and thatthe lien impairs an exemption to which they would otherwise be entitled.

Case: 08-6052 Page: 8 Date Filed: 06/11/2009 Entry ID: 3556267

IN THE UNITED STATES BANKRUPTCY COURTFOR THE DISTRICT OF NEBRASKA

IN THE MATTER OF: ) CASE NO. BK13-40623-TLS)

GREGORY S. CARDWELL and ) CH. 13KIMBERLY D. CARDWELL, )

)Debtors. )

ORDER

Hearing was held in Lincoln, Nebraska, on August 14, 2013, on Debtors’ motion to avoidlien of First State Bank (Fil. #36) with an objection filed by creditor First State Bank (Fil. #41).Philip Kelly appeared for Debtors and Adam Hoesing appeared for First State Bank. Evidence andbriefs were submitted, and the matter was taken under advisement. This order contains findings offact and conclusions of law required by Federal Rule of Bankruptcy Procedure 7052 and FederalRule of Civil Procedure 52. This is a core proceeding as defined by 28 U.S.C. § 157(b)(2)(A) and(K).

The operative facts are not in dispute. Debtors are the owners of two motor vehicles: a 2006Pontiac Montana and a 1992 Ford F-150 pickup. The vehicles are used by Debtors to travel to andfrom their respective places of employment. However, the vehicles are not otherwise used inconnection with their employment. Debtors have assigned a fair market value of $800.00 to the 1992Ford and $1,200.00 to the 2006 Pontiac. First State Bank holds a claim against Debtors in theamount of $24,466.44, which claim is secured in part by a nonpossessory, nonpurchase-moneysecurity interest in both vehicles. In amended Schedule C, Debtors claim exemptions in the vehiclesin the total amount of $2,000.00.

On July 8, 2013, Debtors filed their motion to avoid the lien of First State Bank in thevehicles pursuant to § 522(f)(1)(B)(ii) of the Bankruptcy Code. First State Bank resisted, assertingthat the vehicles do not constitute tools of the trade under federal law and, therefore, Debtors cannotuse § 522(f) to avoid its lien. For the reasons discussed below, I agree with First State Bank and themotion to avoid lien is denied.

11 U.S.C. § 522(f) provides in pertinent part:

(f)(1) Notwithstanding any waiver of exemptions but subject to paragraph (3),the debtor may avoid the fixing of a lien on an interest of the debtor in property tothe extent that such lien impairs an exemption to which the debtor would have beenentitled under subsection (b) of this section, if such lien is —

. . . (B) a nonpossessory, nonpurchase-money security interest in any —

. . . (ii) implements, professional books, or tools, of the trade of

the debtor or the trade of a dependent of the debtor[.]

Case 13-40623-TLS Doc 55 Filed 09/12/13 Entered 09/12/13 12:19:29 Desc Main Document Page 1 of 4

1Nebraska is an “opt-out” state and, therefore, debtors in bankruptcy can only elect state lawexemptions and exemptions under federal law other than bankruptcy law.

-2-

It is undisputed that First State Bank’s lien is a nonpossessory, nonpurchase-money securityinterest. It is also undisputed that the only subcategory of property listed in § 522(f)(1)(B)potentially applicable to motor vehicles would be tools of the trade as set forth in § 522(f)(1)(B)(ii).

The dispute in this case centers on the definition of “tools of the trade.” Debtors take theposition that since § 522(f) deals with avoiding a lien that impairs an exemption to which Debtorswould have been entitled, and since Nebraska state law exemptions apply,1 the court should look tostate exemption law to define tools of the trade. In the Nebraska exemption statute, a tool of thetrade is specifically defined to “include one motor vehicle used by the debtor . . . to commute to andfrom his or her principal place of trade or business[.]” Neb. Rev. Stat. § 25-1556(4). First StateBank, on the other hand, argues that the state law definition is irrelevant to the interpretation of theterm “tool of the trade” as used in § 522(f) of the Bankruptcy Code. Instead, First State Bank arguesthat the bankruptcy court should look to federal law in determining whether the motor vehiclesconstitute tools of the trade as contemplated by § 522(f). I agree.

A similar issue was faced by the Eighth Circuit Bankruptcy Appellate Panel in Cleaver v.Warford (In re Cleaver), 407 B.R. 354 (B.A.P. 8th Cir. 2009). There, the B.A.P. defined the issueas:

The issue on appeal is whether the debtors, who have exempted a motorvehicle under Iowa’s exemption statute, are entitled to prove that the vehicle is a toolof the trade under 11 U.S.C. § 522(f)(1)(B)(ii) in order to avoid a nonpossessory,nonpurchase-money security interest in that vehicle. We hold that they are.

Id. at 356.

In Cleaver, the B.A.P. began its analysis by noting that Congress included § 522(f) in theBankruptcy Code to allow “debtors to avoid liens on certain property that Congress deemed‘necessary to give substance to the concept of a fresh start. This property is required for themaintenance, health and welfare of the debtor and his family, and avoids literal destitution.’” Id.(quoting Thorp Credit and Thrift Co. v. Pommerer (In re Pommerer), 10 B.R. 935, 946 (Bankr. D.Minn. 1981)). Tools of the trade were included as a class of property receiving the protection of lienavoidance. 11 U.S.C. § 522(f)(1)(B)(ii). The B.A.P. recognized that Iowa (like Nebraska in thiscase) had opted out of the bankruptcy exemption scheme. As a result, a debtor in Iowa or Nebraskais limited to the exemptions allowed by that state’s law and federal non-bankruptcy law. Thus, theB.A.P. acknowledged that Iowa law regarding the Iowa exemption statute’s use of the term “toolsof the trade” would control for the purpose of determining the allowable exemptions available to anIowa debtor. Id. at 357. Similarly, Nebraska law would determine the allowable exemptions

Case 13-40623-TLS Doc 55 Filed 09/12/13 Entered 09/12/13 12:19:29 Desc Main Document Page 2 of 4

2Interestingly, Nebraska law clearly defines a tool of the trade to include a motor vehicle totravel to and from a place of employment while Iowa’s tool of the trade exemption has beeninterpreted to exclude motor vehicles.

-3-

available to the Nebraska debtors in this case.2 However, the B.A.P. determined that federal law, notstate law, determines the availability of a lien avoidance under § 522(f):

However, lien avoidance is a federal remedy to be interpreted by the federal courts.Heape v. Citadel Bank of Independence (In re Heape), 886 F.2d 280, 282 (10th Cir.1989); Matter of Thompson, 750 F.2d 628, 630 (8th Cir. 1984). “Although a statemay elect to control what property is exempt under state law, federal law determinesthe availability of a lien avoidance.” Thompson at 630; see also Hart v. Crawford (Inre Hart), 332 B.R. 439, 444 (D. Wyo. 2005) (“federal law controls exemptionsgenerally and exemption procedures”). “[T]he ‘opt out’ provision of § 522(b)(2)(A)allows state law to determine only what property may be exempted from the estate.”In re Graettinger, 95 B.R. 632, 634 (Bankr. N.D. Iowa 1988).

Cleaver at 357.

To support its position that federal bankruptcy law determines whether a lien may beavoided, the B.A.P. looked to the United States Supreme Court case of Owen v. Owen, 500 U.S. 305(1991). Owen held that judicial liens encumbering exempt property can be avoided under § 522(f)even “when the State has defined the exempt property in such a way as specifically to excludeproperty encumbered by judicial liens.” Id. at 306. Therefore, the B.A.P. held:

Based on the plain meaning of the statute and the Owen decision, we conclude thatthe language of the statute, “exemption to which the debtor would have been entitledunder subsection (b),” does not require the exemption to be a “tool of the trade”exemption specifically, but rather any exemption under subsection (b) to which thedebtor would have been entitled.

Cleaver, 407 B.R. at 359. More importantly, the B.A.P. stated “[t]he fact that an exemption claimedby debtors is in property that is not considered a ‘tool of the trade’ under state law is irrelevant tothe issue of whether the lien can be avoided.” Id. at 358. The B.A.P. remanded the case to thebankruptcy court to allow the debtors to “try to prove that the [vehicle] is a tool of the trade as amatter of federal law and that the lien impairs an exemption to which they would otherwise beentitled.” Id. at 359. At its essence, Cleaver holds that the bankruptcy court must first look to seeif the creditor has a nonpossessory, non-purchase money security interest in a tool of the trade asdefined by federal law. If so, the bankruptcy court then looks to state law to determine if the lienimpairs an exemption to which the debtors would have been entitled. The exemption can be anyexemption to which the debtors would have been entitled and does not need to be a tool of the tradeexemption.

Case 13-40623-TLS Doc 55 Filed 09/12/13 Entered 09/12/13 12:19:29 Desc Main Document Page 3 of 4

3I am well aware that this decision is contrary to existing lien avoidance practice in theDistrict of Nebraska. As a result, it has been reviewed by the other bankruptcy judge in this district,the Honorable Timothy J. Mahoney, who has concurred in the result.

-4-

Therefore, First State Bank is correct that Debtors must show that the vehicles are tools ofthe trade under federal law in order to avoid the bank’s lien. Although Cleaver did not reach theultimate issue of whether the vehicle in that case was in fact a tool of the trade, it did state “[t]heEighth Circuit has adopted a test to determine whether a vehicle is a tool of the trade, and that is:‘the reasonable necessity of the item to the debtor’s trade or business.’” 407 B.R. at 358 (citingProd. Credit Assoc. of St. Cloud v. LaFond (In re LaFond), 791 F.2d 623, 627 (8th Cir. 1986)(quoting Seacord v. Commerce Bank of Blue Hills (In re Seacord), 7 B.R. 121 (Bankr. W.D. Mo.1980)). In making that determination, a court should consider (1) the intensity of the debtor’s pastbusiness activities; (2) the sincerity of the debtor’s intention to continue the business; and (3)evidence that the debtor is “legitimately engaged in a trade which currently and regularly uses thespecific implements or tools . . . on which lien avoidance is sought.” LaFond, 791 F.2d at 626(citations omitted). A car that is used solely for commuting is not a tool of the trade. In re King, 451B.R. 884, 887 (Bankr. N.D. Iowa 2011) (stating, “It is fairly well settled that a car used only forcommuting purposes cannot be considered a tool of debtor’s trade.”) (citations omitted).

Here, Debtors have conceded that the vehicles are used solely for personal purposes and forcommuting to and from work, and are not necessary to Debtors’ trade or business. Therefore, thevehicles are not tools of the trade as that term has been defined under federal bankruptcy law.Because the vehicles are not tools of the trade under the lien avoidance statute, Debtors cannot avoidthe lien of First State Bank and this Court need not reach the issue of whether the lien impairs anexemption to which the Debtors are entitled.

IT IS, THEREFORE, ORDERED that the motion to avoid lien (Fil. #36) is denied.3

DATE: September 12, 2013.

BY THE COURT:

/s/ Thomas L. SaladinoChief Judge