Banking Report(3)

12

Banking Report: Interbank Rates Submitted by: Khadija Imam Murtaza Saba Irshad Maha Khalid

-

Upload

aicha-xaheer -

Category

Documents

-

view

221 -

download

0

Transcript of Banking Report(3)

8/6/2019 Banking Report(3)

http://slidepdf.com/reader/full/banking-report3 1/12

Banking Report: Interbank Rates

Submitted by:

Khadija Imam Murtaza

Saba Irshad

Maha Khalid

8/6/2019 Banking Report(3)

http://slidepdf.com/reader/full/banking-report3 2/12

Definition

` The rate of interest charged on short-term loans made between banks. Banks borrow

and lend money in the interbank market in order to manage liquidity and meet the

requirements placed on them.

` The interest rate charged depends on the availability of money in the market, on

prevailing rates and on the specific terms of the contract, such as length of term etc.

` Banks are required to hold an adequate amount of liquid assets, such as cash, to

manage any potential withdrawals from clients. If a bank can't meet these liquidity

requirements, it will need to borrow money in the interbank market to cover the

shortfall.

` Some banks, on the other hand, have excess liquid assets above and beyond theliquidity requirements.

` These banks will lend money in the interbank market, receiving interest on the assets.

Financial Markets-Pakistan scenario

` The Pakistan money market consists of the Interbank Market which is the Call market

and the Open market. In the Call market banks can lend or borrow funds up to theircredit limits without any security or guarantee.

` In the Open market there are repos in which holders of securities sell these securities to

an investor with an agreement to repurchase them at a fixed price on a fixed date.

` Participants in the interbank market consist of commercial banks and Development

Financial Institutions. Participants in the open market consist of commercial banks,

Development Financial Institutions, regional banks, corporate bodies, securities houses,

leasing companies, insurance companies, investment companies and individuals.

8/6/2019 Banking Report(3)

http://slidepdf.com/reader/full/banking-report3 3/12

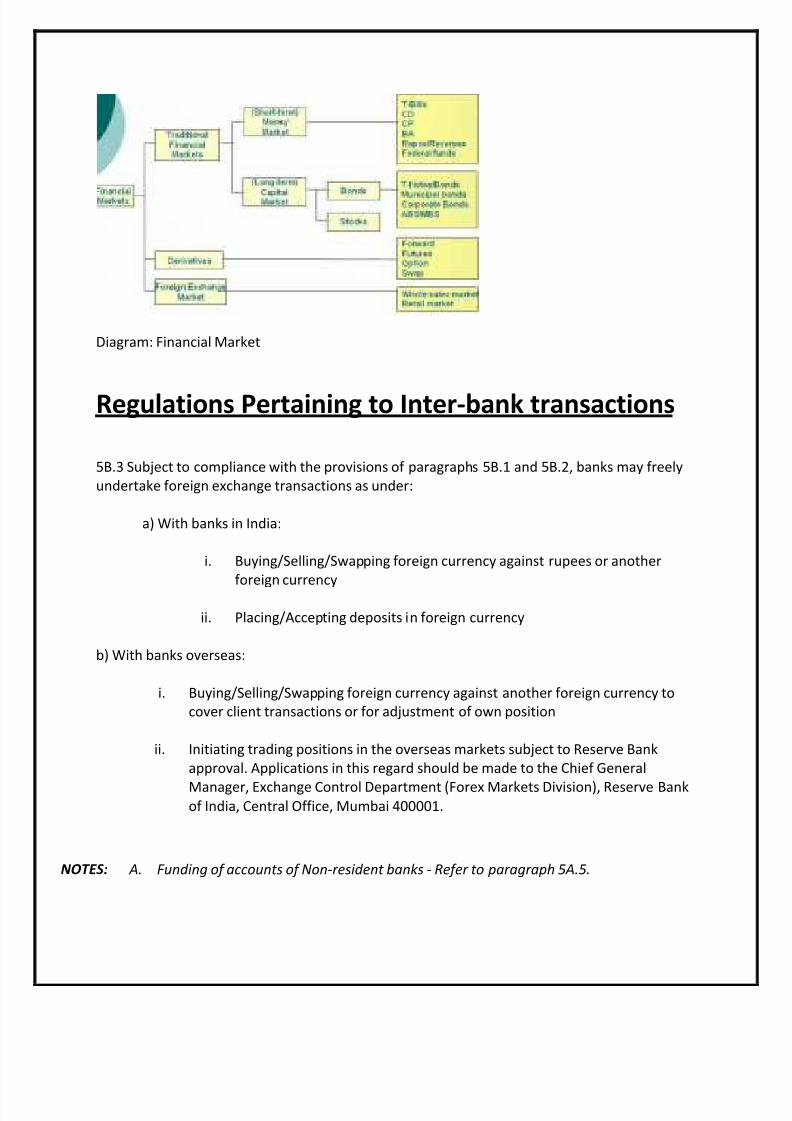

Diagram: Financial Market

Regulations Pertaining to Inter-bank transactions

5B.3 Subject to compliance with the provisions of paragraphs 5B.1 and 5B.2, banks may freely

undertake foreign exchange transactions as under:

a) With banks in India:

i. Buying/Selling/Swapping foreign currency against rupees or another

foreign currency

ii. Placing/Accepting deposits in foreign currency

b) With banks overseas:

i. Buying/Selling/Swapping foreign currency against another foreign currency to

cover client transactions or for adjustment of own position

ii. Initiating trading positions in the overseas markets subject to Reserve Bank

approval. Applications in this regard should be made to the Chief General

Manager, Exchange Control Department (Forex Markets Division), Reserve Bankof India, Central Office, Mumbai 400001.

NOTES: A. Funding of accounts of Non-resident banks - Refer to paragraph 5 A.5.

8/6/2019 Banking Report(3)

http://slidepdf.com/reader/full/banking-report3 4/12

B. Form A2 need not be completed for sales in the inter-bank market but all such transactions

should be reported to Reserve Bank in R Returns.

Foreign currency accounts

5B.4 (i) Inflows into foreign currency accounts arise primarily from client-related transactions,

swap deals, deposits, borrowings etc. Banks may maintain balances in foreign currencies upto

the levels approved by the Top Management. They are free to manage the surplus in these

accounts through overnight placement or investments with their overseas

branches/correspondents subject to adherence to the gap limits approved by Reserve Bank.

(ii) Banks may invest upto 15% of their unimpaired Tier I capital or US$ 10 million whichever is

higher, and the entire amount representing foreign currency deposit liabilities in overseas

money market instruments rated at least A1 + by Standard and Poor or P1 by Moody's.

(iii) Foreign currency funds representing deposit liabilities may be utilised for:

a. making loans to resident constituents for meeting their foreign exchange

requirements or for the rupee working capital/capital expenditure needs subject

to the prudential/interest-rate norms, credit discipline and credit monitoring

guidelines in force.

b. extending credit facilities to Indian wholly owned subsidiaries/ joint ventures inwhich at least 51% equity is held by a resident company, subject to the

guidelines issued by Reserve Bank (Department of Banking Operations &

Development).

(iv) Banks should regularly reconcile the balances in the foreign currency accounts as appearing

in their books with the balances advised by the correspondents and maintain records to show

that such reconciliation has been made.

(v) Banks may write off/transfer to unclaimed balances account, unreconciled debit/credit

entries up to the value of US.$.1,000 or its equivalent provided:

a. the entry has been outstanding in the books for two or more years and

b. approval from the Competent Authority has been obtained,

8/6/2019 Banking Report(3)

http://slidepdf.com/reader/full/banking-report3 5/12

c. a separate record of all such entries is maintained and the transactions reported

in the respective R Return.

Applications for adjustment of an entry in excess of US$ 1,000 or its equivalent should be

referred to the concerned Regional Office of Reserve Bank.

Loans/Overdrafts

5B.5 (i) Banks may avail of loans/overdrafts from their overseas branches and correspondents

up to 15% of their unimpaired Tier-I capital or US$ 10 million or its equivalent, whichever is

higher. The funds may be used for purposes other than lending in foreign currencies and repaid

without reference to Reserve Bank. The aforesaid limit applies to the aggregate amount availed

by all the offices and branches in India from all their branches/correspondents abroad.

(ii) If drawals in excess of the above limit are not adjusted within five days, a report should be

submitted to the Forex Markets Division in the Central Office of Reserve Bank within 15 days

from the close of the month in which the limit was exceeded. Such a report is not necessary if

arrangements exist for value dating.

(iii) Banks may avail of loans in excess of the limits prescribed in sub-paragraph (i) above solely

for replenishing their rupee resources in India without prior approval of Reserve Bank. Such

rupee funds may be used only for financing the banks' normal business operations and should

not be deployed in the call money etc. markets. A report on each borrowing should be

immediately forwarded to the Forex Markets Division, in the Central Office of Reserve Bank

whose prior permission will be required for repayment of such loans. Such permission will be

given only if the bank has no borrowings outstanding either from Reserve Bank or otherbank/financial institution in India and is clear of all money market borrowings for a period of at

least four weeks before the repayment.

(iv) Interest on loans/overdrafts may be remitted (net of taxes) without the prior approval of

Reserve Bank.

Reports to Reserve Bank

5B.6 (i) The Head/Principal Office of each bank should submit to the Chief General Manager,

Exchange Control Department (Forex Markets Division), Reserve Bank of India, Central Office,Mumbai 400 001 the following:

(1) Daily statements of foreign exchange turnover in Form FTD and Gaps position

and cash balances in Form GPB. These statements should be transmitted online

through wide area network.

(2) Monthly statement ( in USD million) indicating:

8/6/2019 Banking Report(3)

http://slidepdf.com/reader/full/banking-report3 6/12

a. Aggregate Gap Limit (AGL) approved

b. Maximum AGL on any day in the month

c. Value at Risk (VaR) limit approved and

d. Maximum VaR on any day in the month

(ii) The Head/Principal Office of each bank should submit a statement in duplicate in form BAL

giving details of their holdings of all foreign currencies on fortnightly basis so as to reach the

Regional Office of Reserve Bank under whose jurisdiction the Head/Principal Office is situated

within seven calendar days from the close of the reporting period to which it relates. If the 15th

or the last day of the month is a holiday the statement should be submitted as at the close of

business on the preceding working day.

Direct Instruments and Indirect Instruments

` Direct instruments are typically directives given by the central bank to control the

quantity or price (interest rate) of money deposited with commercial banks (and

sometimes other financial institutions) and credit provided by them.

` Examples of Direct Instruments are:

y Interest Rate Controls

y Credit Ceilings

y Directed Lending

` Examples of Indirect Instruments are:

y T-bill and PIB Auctions

y Open-Market Operations

y Discounting Facility

y Foreign Exchange Management

y The instruments of money market are:

8/6/2019 Banking Report(3)

http://slidepdf.com/reader/full/banking-report3 7/12

y Treasury bill

y Federal Funds

y Repurchase Agreements

y Commercial Paper

y Certificates of Deposit (CD)

` Bankers Acceptance

Statuary Liquidity Requirements

` The SBP uses targeting monetary aggregates for its monetary management function so

Indirect instruments are used for controlling price or volume of the supply of its ownliabilities i.e. reserve money, which in turn affects interest rates and the quantity of

money and credit in the whole banking system.

Recent Developments in the Banking Sector

` During Q1-FY11, the money market witnessed large inflows due to heavy government

borrowings from SBP, expansion in net foreign assets and retirement of private sector

and commodity operations related credit (see Following Table). A significant portion of

these inflows, however, did not affect interbank market liquidity. This can be seen in a

relatively higher increase in currency in circulation and decline in bank deposits,

suggesting a rise in transaction demand for money.

Other than the seasonal pattern, these can be attributed to relief activities and

temporary disruptions of banking services in the flood affected areas. This explains the average

net injections of Rs21 billion by SBP in Q1-FY11.

8/6/2019 Banking Report(3)

http://slidepdf.com/reader/full/banking-report3 8/12

Table: Money Market

8/6/2019 Banking Report(3)

http://slidepdf.com/reader/full/banking-report3 9/12

KIBOR movements and Results

` Following the increase in KIBOR, which is used as a benchmark for most of the corporate

lending, the incremental weighted average lending rate (WALR) increased to 14.2

percent in December 2010 from 13.2 percent in June 2010. In real terms, the lendingrates are also increasing; however, these are still in the negative zone showing that the

desired impact of rise in interest rates has not yet materialized.

8/6/2019 Banking Report(3)

http://slidepdf.com/reader/full/banking-report3 10/12

Money Market Operations

Despite an increase in the policy rate and its transmission to market interest rates, the

growth in key monetary aggregates remains substantial. For instance, the reserve

money has grown by 16.6 percent (YoY) up till 15th January 2011. However, thisrepresents a favorable compositional change in reserve money in the form of a decline

in government borrowings from SBP since mid December 2010 and an increase in SBPs

NFA on the back of improved external current account position.

Similarly, the broad money grew by 15.1 percent during the same period despite a

modest growth of 4.8 percent in the credit to the private sector. This is due to the sharp

growth in credit to government 25.8 percent from the banking system. The continuation

of these trends can undermine efforts to bring inflation down and mitigate inflationary

expectations.

8/6/2019 Banking Report(3)

http://slidepdf.com/reader/full/banking-report3 11/12

Article:

Govt borrowing pushes money market towards liquidity

crunchBy Ismail Dilawar

KARACHI - The rupee blockade in the face of non-performing loans (NPLs) and the government's

focus on borrowing from the scheduled banks has created a liquidity crunch in the local money

market. The State Bank of Pakistan (SBP), for this reason, had to inject over Rs 92.35 billion intothe banking system in only 16 days during the current month.

The central bank injected Rs 32.6 billion, Rs 19.95 billion, Rs 33.85 billion and Rs 5.95 billion on

the sixth, 15th, 17th and 21st of January respectively. The State Bank instilled this money in the

inter-bank market by offering four, six, seven and eight days reverse repo in the Government of

Pakistan Market Treasury Bills and Pakistan Investment Bonds at a rate of return ranging from

12.81 to 12.85 percent.

The offers in the respective four auctions amounted to Rs 45.6 billion, Rs 33.7 billion, Rs 42.5

billion and Rs 28.25 billion, aggregating to over 150 billion. Contrarily, the State Bank had

injected only Rs 34.1 billion in December for MTBs and PIBs of six-days reverse repo. "We only

inject the money when they (banks) need it," SBP chief spokesman Syed Waseemuddin said.

Analysts believe that an increasing trend in the real inter-bank overnight borrowing rate was

indicative of the fact that the inter-bank market was falling short of the rupee.

Analysts viewed that inter-bank rates of 12.7 and 12 percent on last Saturday and Thursday

were "extremely high", hinting that there was a slight shortage of liquidity in the money

8/6/2019 Banking Report(3)

http://slidepdf.com/reader/full/banking-report3 12/12

market.

Liquidity crisis, analysts viewed, was natural given the fact that no fresh liquidity through public

savings and other means was coming to the banking system. Money in circulation is already

blocked in the face of NPLs and government borrowings.

"The money circulation process is not completing and is ultimately blocking in the face of banks

non-performing loans," Azfar Bin Shahid told Pakistan Today. Citing reasons for ever-increasingNPLs, the analyst said that soaring inflation had eroded purchasing power of the buyers that

had reflected negatively on the demand for saleable stocks, a major chunk of which was lying

unsold. "The borrowers are not able to generate the capacity to repay the bank loans," A B

Shahid said. He said that market players might find carrying out currency swap deals hard and

would depend on the central bank to cater their dire rupee need.

Market dealers are also said to have been wary of the rupee shortfall due to higher outflows

mainly going to the funds-strapped government that is now said to have shifted its borrowing

focus to the banks other than SBP. The rupee in the inter-bank market appears to be strong

nowadays due to a record inflow of workers' remittances that amounted to $5.3 billion during

first half of the current financial year. The country's foreign exchange reserves have also hit an

all time high of Rs 17.28 billion during the week ending on January 15. The recent inflow of

$633 million under US' Coalition Support Fund is another indicator that augurs well for the

rupee and its dealers in the country. Analysts foresee that reimbursement of a further $500-

700 as war expense during the second half of FY2010-11, would further rid the crises-hit

country of its woes emanating from currency exchange rate and balance-of-payment.