Banking 2016 New models of distribution - kbd.projektekf.pl · Retail Banking challenges Next...

11

Ambrogio Terrizzano Senior Executive - Head of Accenture Interactive Marketing Transformation Practice Banking 2016 New models of distribution October 25 th , 2012

Transcript of Banking 2016 New models of distribution - kbd.projektekf.pl · Retail Banking challenges Next...

Ambrogio Terrizzano Senior Executive - Head of Accenture Interactive Marketing Transformation Practice

Banking 2016New models of distribution

October 25th, 2012

Copyright © 2012 Accenture. All rights reserved. 2

Trend in revenues

Trend in costs

Trust &

confidence

15%

-1,5%

2008-2011 2011-2013

- 4,1%

2006-2008

+6%

2006-2008

- 0,5%

2008-2011

+3%

2011-2013

Trust for Food and

Beverage + Automotive

100%79%

Trust for Banks

10073

Confidencefor Banks in

2007

Confidencefor Banks in

2011

Strong evidences are pushing European retail banks to change

-21 p.p - 27%

Source: Domestic retail banks EU (DB Running the numbers august 2012)

Source: Source: DB Rtn, Sept 11

Source: Edelman, 2011; Nielsen Global Consumer Confidence Index, 2007 e 2011

Copyright © 2012 Accenture. All rights reserved. 3

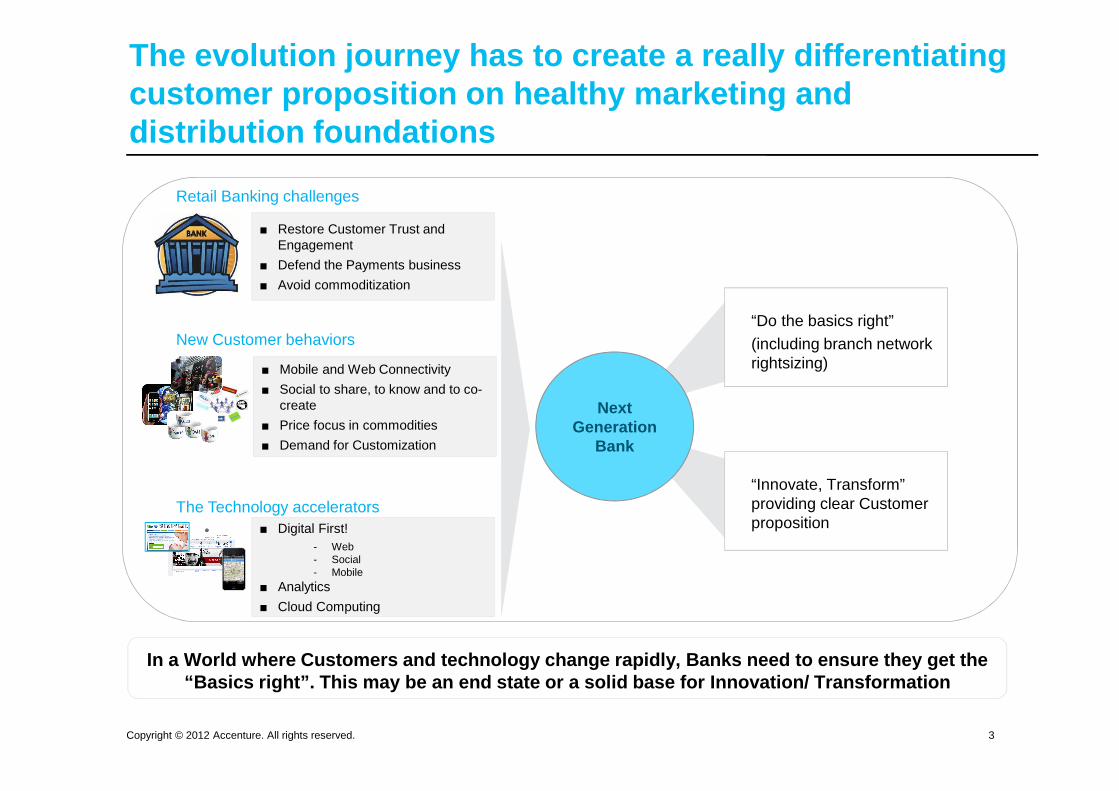

“Do the basics right”

(including branch network rightsizing)

“Innovate, Transform” providing clear Customer proposition

■ Restore Customer Trust and Engagement

■ Defend the Payments business

■ Avoid commoditization

Retail Banking challenges

Next Generation

Bank

In a World where Customers and technology change ra pidly, Banks need to ensure they get the “Basics right”. This may be an end state or a solid base for Innovation/ Transformation

■ Digital First!- Web- Social- Mobile

■ Analytics

■ Cloud Computing

The Technology accelerators

■ Mobile and Web Connectivity

■ Social to share, to know and to co-create

■ Price focus in commodities

■ Demand for Customization

New Customer behaviors

The evolution journey has to create a really differ entiating customer proposition on healthy marketing and distribution foundations

Copyright © 2012 Accenture. All rights reserved. 4

Video

Banking 2016 in a nutshell

Copyright © 2012 Accenture. All rights reserved. 5Source: Accenture analysis, 2011

Network Optimization

Today 2016

100

80

Number of Branches

Branch Operative Model Evolution

1. Optimized branch network , review network architecture (i.e. Hub & Spoke model)

2. Basic multichannel integration , for a real time banking

3. Proactive and reactive interaction management (Customer needs driving next offer, events management, etc)

3. Operational Customer segmentation driving a need based offering structure

4. Salesforce effectiveness powered by consistent sales behavior and sales tools

5. Simple and clear communication

6. Performance Management (new metrics Customer oriented) and tailored compensation schemes

The excellent Bank in the Basics

Today 2016

85%

15%

60%15%

25%

Full service Branch(>6 FTEs)

Light Branches(4-5 FTEs)

Kiosks(2-3 FTEs)

Employees

Average FTE/ Branch

∼∼∼∼ 6 ���� ∼∼∼∼ 4

-20%Of Branches

-2FTE

The “Do the basics right” Bank – key areas of focus

Copyright © 2012 Accenture. All rights reserved. 6

Prefilling

Unique contract

Digitalization

� Transfer operational branch activities to a centralized Back Office that provides support to the Commercial Network

� Let Customers do low value activities through online functionalities (e.g. internet banking, kiosks) or advanced ATM

� Set up a Unique Contract covering a list of products that customers can activate later through remote channels

� Use existing prefilled data to avoid the need for contract data entry at branches

� Introduce Paperless Processes for sales and service activities at branches by implementing digitalized tools (e.g. biometric signature)

Branch Time

Customer Experience

Do it yourself

Centralization

Key Levers Description

The “Do the basics right” Bank – levers enabling physi cal distribution network rightsizing

Copyright © 2012 Accenture. All rights reserved. 7

Personal DigitalAdvisory

The «Do the Basics right» bank

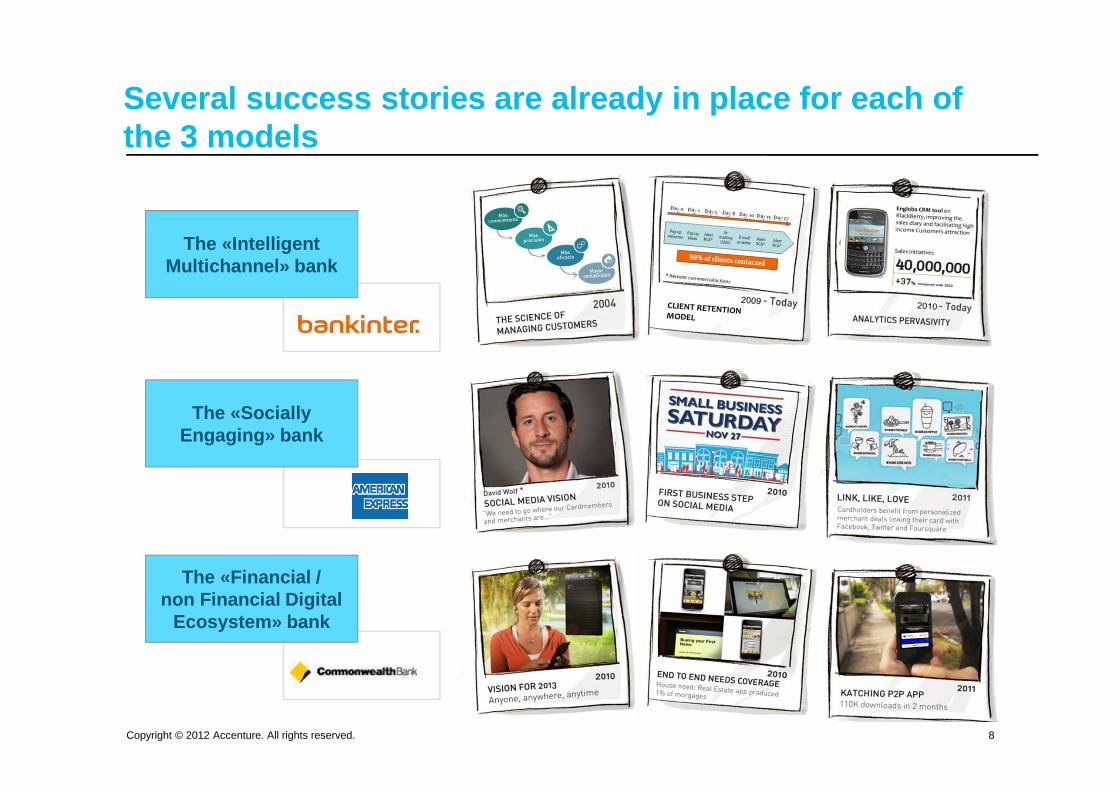

The «IntelligentMultichannel» bank

The «SociallyEngaging» bank

The «Financial / non Financial Digital

Ecosystem» bank

Key capabilities

3 possible models to create differentiation on the market

Copyright © 2012 Accenture. All rights reserved. 8

The «IntelligentMultichannel» bank

The «SociallyEngaging» bank

The «Financial / non Financial Digital

Ecosystem» bank

Several success stories are already in place for ea ch of the 3 models

Copyright © 2012 Accenture. All rights reserved. 9

“Do the Basics right” Bank

The “Intelligent Multichannel” Bank

The “Socially Engaging” Bank

The “ Financial/ Non Financial Digital

Ecosystem” Bank

Low Medium High

Each Bank North Star

Journey based on:

1. Market

2. Strategy pursued

3. Available capabilities

4. Investment affordability

Basic multichannel orchestration

Deep Customer understanding

Branch network optimization

Empowered Branch Front line & sales tools

Smart interaction with Customers

Web & Mobile channel marketing & effectiveness

Need based offering

Pervasive Analytics (next product, pricing, etc.)

Effective multichannel integration

Real time event management

Product offering optimization & scientific pricing

Mobile Marketing, M-Loyalty and Analytics

Partnership and Alliance management

M-payments

Mobile commerce ecosystem

Social Digital Marketing (clustering, client engagement)

Social CRM (data enrichment and optimized offering)

Social media listening & monitoring

Performance Management

Focus areas

Personal Digital Advisory

Each models can be activated working on specific capabilities

Copyright © 2012 Accenture. All rights reserved. 10

Trends Next Generation

Bank

Opportunities

Define appropriate

sourcing approach

Ensure focus on “Basics

right”

Define North Star model

Define Shared Vision on

future scenario/

opportunities

Create Digital Lab and foster “Test & Learn”

approach

“Digital Lab”

■ Involve Top Management assessing context and trends, “Next Generation Bank” models , required areas to focus on

■ Assess Customer base and prospects

■ Define “to be” model , related focus areas and capabilities, considering trends and Banking 2016 options

■ Define money on the table

■ Identify target KPIs and create a War Room to develop and monitor “Do the Basics right” focus areas

■ War Room should be temporary

■ Consider possible partners to scale fast capabilities

■ Digital Lab to monitor trends, manage chosen pilot initiatives in Social, Mobile, Digital

■ Pilot key initiatives with “ Test & Learn” approach

Note: similar experiences suggest it’s possible to activate a Transformation Program within 4-6 months

A robust execution approach is mandatory

Copyright © 2012 Accenture. All rights reserved. 11

For further info, please contact:[email protected]