BANK ISLAM MALAYSIA BERHAD Islam Malaysia Berhad 5 Bank Islam’sregional expansion plans include...

19

The credit rating is not a recommendation to purchase, sell or hold a security, inasmuch as it does not comment on the securi ty’s market price or its suitability for a particular investor, nor does it involve any audit by RAM Ratings. The credit rating also does not reflect the legality and enforceability of financial obligations, transfer and convertibility risks, repatriation risk, currency risk or any other risk apart from credit risk. NOVEMBER 2012 BANK ISLAM MALAYSIA BERHAD Financial Institution Ratings

Transcript of BANK ISLAM MALAYSIA BERHAD Islam Malaysia Berhad 5 Bank Islam’sregional expansion plans include...

The credit rating is not a recommendation to purchase, sell or hold a security, inasmuch as it does not comment on the securi ty’s market price or its suitability for a particular investor, nor does it involve any audit by RAM Ratings. The credit rating also does not reflect the legality and enforceability of financial obligations, transfer and convertibility risks, repatriation risk, currency risk or any other risk apart from credit risk.

NOVEMBER 2012

BANK ISLAM MALAYSIA BERHAD

Financial Institution Ratings

The credit rating is not a recommendation to purchase, sell or hold a security, inasmuch as it does not comment on the securi ty’s market price or its suitability for a particular investor, nor does it involve any audit by RAM Ratings. The credit rating also does not reflect the legality and enforceability of financial obligations, transfer and convertibility risks, repatriation risk, currency risk or any other risk apart from credit risk.

CREDIT RATING RATIONALE

FINANCIAL INSTITUTION RATINGS

NOVEMBER 2012

BANK ISLAM MALAYSIA BERHAD

– Rating Review

Summary

RAM Ratings has reaffirmed the respective long- and short-term financial

institution ratings of Bank Islam Malaysia Berhad (“Bank Islam” or “the Bank”) -

Malaysia’s first Islamic bank – at A1 and P1. The long-term rating has a stable

outlook.

The ratings consider Bank Islam’s strong branding in the Malaysian Islamic

banking sphere, although its franchise and market position within the overall

banking system (when compared to more-sizeable universal-banking groups) is

still limited. The Bank is primarily a retail-focused Islamic bank, with a high level

of concentration in unsecured retail financing; personal financing facilities make

up approximately 30% of its financing portfolio. The ratings also reflect the

backing of Lembaga Tabung Haji (“Tabung Haji”, Malaysia’s hajj pilgrims’ funds

board), i.e. the Bank’s ultimate controlling shareholder, in the form of capital

support and deposit placements. On this note, Bank Islam boasts a favourable

liquidity position and commendable funding profile, with an exceptionally low

financing-to-deposits ratio of 57% and a considerable proportion of low-cost

deposits. The Bank’s capitalisation position is also sturdy. As at end-June 2012,

its tier-1 and overall risk-weighted capital-adequacy ratios (“RWCARs”) stood at

14.4% and 15.6%, respectively (end-December 2011: 15.0% and 16.2%).

Bank Islam charted a 19% financing growth in FYE 31 December 2011 (“FY Dec

2011”). Its financing-quality indicators had improved, with a gross impaired-

financing (“GIF”) ratio of 2.0% as at end-June 2012. Although the Bank’s rapidly

expanding financing portfolio (with growth driven primarily by personal financing

facilities) may lack seasoning, salary deductions or salary transfers from

employers partially mitigate the risk of non-payment. Meanwhile, hefty write-offs

on legacy financing have eased, with the Bank’s credit-cost ratio moderating to

0.3% in FY Dec 2011. Last year, the Bank’s pre-tax profits grew 40% year-on-

year (“y-o-y”) to RM469.6 million1, supported by wide net financing margins.

1 With MFRS 139 restatements, Bank Islam’s pre-tax profits were RM492.5 million in FY Dec 2011 (an annualised 48% y-o-y growth). The Bank would have recorded a credit cost ratio of 0.2% while its tier-1 and overall RWCAR would have been 15.6% and 16.8% respectively, as at end-2011.

Analysts: Kwan Ji-Ling (603) 7628 1115 [email protected] Wong Yin Ching (603) 7628 1117 [email protected] Principal Activity: Islamic banking Rating Type: Financial Institution Ratings Ratings: A1/P1 [Reaffirmed] Rating Outlook: Stable Last Rating Action: 21 November 2011

Bank Islam Malaysia Berhad 2

Bank Profile

Figure 1: Bank Islam’s shareholding structure, with major subsidiaries & associate

Bank Islam Malaysia Berhad

Al-WakalahNominees

( Tempatan) Sdn Bhd

100%

BIMB Investment Management

Berhad

100%

Bank Islam Trust Company (Labuan)

Ltd

100%

Dubai Financial Group LLC BIMB Holdings Berhad

Lembaga Tabung Haji

30.5% 51% 18.5%

51%

BIMB Offshore Company

Management Services Sdn Bhd

100%20%

Amana Bank Limited

Source: Bank Islam

Bank Islam is Malaysia’s first Islamic bank. It commenced operations in 1983,

following the enactment of the Islamic Banking Act that same year. As at end-

September 2012, the Bank had 125 branches nationwide. Bank Islam is the third-

largest commercial Islamic bank in Malaysia, with an asset base of RM33.8

billion as at end-June 2012. In terms of financing and deposits, the Bank ranks a

respective 5th and 2

nd in the domestic Islamic banking industry, as at the same

date. While Bank Islam commands notable market shares in the Islamic banking

sphere, its market position and franchise are still limited in the overall industry

compared to the universal-banking groups.

Bank Islam’s business activities are segregated into consumer banking,

commercial and corporate banking, and treasury operations. Consumer banking

remains its largest earnings contributor, accounting for approximately half of the

Bank’s revenue and profits (before operating expenses and taxes). The Bank

also provides Ar-Rahnu (or pawnbroking) services.

Notable market shares in the Malaysian Islamic banking sphere

Consumer-banking segment – largest earnings

contributor

Bank Islam Malaysia Berhad 3

Figure 2: Bank Islam’s segmental revenues in FY Dec 2011

Consumer Banking

50%

Corporate &

Commercial Banking

12%

Treasury29%

Others9%

Source: Bank Islam

The Bank’s current shareholding structure is a result of a recapitalisation

exercise, following sizeable losses that had wiped out its shareholders’ funds and

capital base in fiscal 2005 and 2006. Bank Islam had subsequently been

recapitalised through a RM1.01 billion infusion that had led to the issuance of

new shares to Tabung Haji and Dubai Financial Group LLC.2 Tabung Haji, the

hajj pilgrims’ funds board that in aggregate holds 44.5% of the Bank through

direct (18.5%) and indirect (through a 51%-stake in BIMB Holdings Berhad

(“BIMB Holdings”, an Islamic financial-services holding company) interests, is

Bank Islam’s ultimate majority shareholder. In October 2012, BIMB Holdings

received Bank Negara Malaysia’s approval to commence negotiations with Dubai

Financial Group LLC on the potential acquisition of the latter’s 30.5%-stake in

Bank Islam. Should this materialise, Tabung Haji’s effective interest in Bank

Islam will increase to approximately 60%.

RAM Ratings also notes plans for Bank Islam to assume the listed status of

BIMB Holdings. The Bank completed a corporate exercise in February 2012,

through which RM1.2 billion of historical accumulated losses had been written off

against balances in its share-premium account and regulatory reserves. We

understand that the listing exercise is expected to be completed in 2013, albeit

still subject to market conditions and the receipt of the necessary approvals. All

said, we do not envisage this to have any material credit impact on Bank Islam.

2 Dubai Financial LLC is the financial-services arm of Dubai Holdings, an investment-holding

company held by the Dubai government.

Tabung Haji may raise stake

Plans to assume parent’s listed status

Bank Islam Malaysia Berhad 4

Business Strategies

After a period of severe losses and a recapitalisation exercise, Bank Islam

embarked on a 3-year Turnaround Plan between June 2006 and June 2009. This

Turnaround Plan had involved the entry of a new management team, a large-

scale reorganisation exercise and a fundamental revamp of the Bank’s

processes. Bank Islam’s current Sustainable Growth Plan, which commenced in

2009 and ends in December this year, aims to position it for domestic and

regional growth through improvements in business innovation, risk management

and franchise development.

Bank Islam will implement its Hijrah to Excellence plan in 2013. This new

business plan focuses on the achievement of robust organic growth and service

excellence. Among others, the Bank targets to chart an annual financing growth

of 25% and to have its non-fund based income (which primarily comprises fee

income) account for 20% of its earnings by 2015. To improve service levels, the

management intends to inculcate a customer-centric business model and focus

on product innovation. The realignment of the Bank’s balance sheet will continue

next year, including the attainment of a higher composition of secured financing

and a 60:40 ratio between floating- and fixed-rate financing (from the present

38:62). From a liability-management perspective, the Bank plans to focus on

promoting retail deposits. Bank Islam is also making efforts to increase its

corporate and commercial banking franchise - these two segments are expected

to make up a larger 30% of its financing portfolio, going forward (end-June 2012:

24%). That said, the Bank will retain its consumer banking focus, with consumer

financing accounting for the remaining 70% of its financing portfolio.

Having been admitted to the Securities Commission’s panel of principal advisors,

Bank Islam is able to advise on and submit corporate proposals, such as initial

public offerings and acquisitions, to the regulator for approval.3 The Bank’s close

links with Tabung Haji have facilitated deal referrals and enhanced the placement

capabilities of its corporate- and investment-banking division, which offers a suite

of capital-market and advisory solutions to larger corporates by leveraging on its

Shariah-structuring capabilities. Within the retail segment, Bank Islam’s

relationship with Tabung Haji gives it access to cross-selling opportunities and

alternative distribution channels.

3 The Bank had participated in TNB Janamanjung Berhad’s RM5.0 billion Islamic Securities

Programme, Pembinaan BLT Sdn Bhd’s RM10.0 billion Islamic Medium-Term Notes Programme and DanaInfra Nasional Berhad’s RM8.0 billion Government-Guaranteed Islamic CP/MTN Programme.

Sustainable Growth

Plan ends this year

To continue realigning balance

sheet in 2013

Close ties with Tabung Haji sharpen competitive advantage

Bank Islam Malaysia Berhad 5

Bank Islam’s regional expansion plans include the acquisition of stakes in Islamic

financial institutions in Indonesia and Bangladesh. In particular, the Bank has

explored avenues to acquire a stake in an Indonesian Islamic bank. With the

release of Bank Indonesia’s Financial Institution Ownership Policy in July 2012,

the management is currently reassessing its planned inorganic growth in

Indonesia. Elsewhere, Bank Islam also has a 20%-stake in Amana Bank Ltd

(“Amana Bank”, the first Islamic financial institution in Sri Lanka);4 the Bank

provides technical advice on Shariah governance, product development and risk

management to the latter.

Risk Profile

As at end-December 2011, the Bank’s assets were valued at RM32.2 billion,

after having charted a 6% y-o-y increase. The Bank also charted a 19% (or

+RM2.3 billion) y-o-y financing growth last year, primarily driven by the expansion

of its retail financing portfolio. In aggregate, retail financing had expanded RM1.7

billion, supported by increases in personal financing (+RM722 million), residential

property financing (+RM532 million) and transport vehicle financing (+RM315

million).

In the 6-month period ending FY Dec 2012, the Bank’s financing assets added

another RM2.3 billion (+16%, from end-December 2011) to RM16.4 billion.

Financing extended for personal purposes had been the main driver of this

growth, having climbed RM1.1 billion during the same period. Following its

stronger financing growth of late, the Bank’s financing assets have been

accounting for an increasingly larger proportion of its assets (48% or RM16.4

billion as at end-June 2012 compared to 39% or RM11.9 billion as at end-

December 2010). RAM Ratings notes, however, that the Bank’s rapidly

expanding financing portfolio (with growth driven primarily by personal financing

facilities) may lack seasoning.

4 Bank Islam completed a share-subscription exercise for a 20%-stake in Amana Bank in February

2011. The 20%-interest had been paid for via RM21.3 million cash, along with a share swap, through which the Bank exchanged a 6.3%-stake in Amana Investment Limited for Amana Bank shares.

Overseas expansion plans involve purchase of stakes in foreign Islamic banks

Rapidly expanding

financing portfolio

Personal financing main growth driver

Bank Islam Malaysia Berhad 6

Figure 4: Bank Islam’s financing profile (as at end-June 2012)

Primary agriculture1%

Mining & quarrying0%

Manufacturing 6%

Wholesale & retail trade, hotels, restaurants

3%

Construction7%

Real estate2%

Transport, storage & communications

1%

Finance, insurance &

business activities

1%

Education, health & others

1%

Other sectors

0%

House financing28%

Personal financing30%

Credit cards3%

Purchase of passenger cars13% Others

2%

Household sector76%

Source: Bank Islam

Financing facilities extended to individuals and the household sector (76%)

formed a large component of Bank Islam’s financing assets as at end-June 2012

and, in aggregate, showed a GIF ratio of 1.6% (end-June 2011: 2.4%). By

product type, personal financing facilities constituted the largest proportion of the

Bank’s financing assets, followed by home financing (28%) and financing for the

purchase of passenger cars (13%). Meanwhile, financing offered to corporates

and small and medium-sized enterprises (“SMEs”) only made up a respective

19% and 3% of its total gross financing portfolio. In total, these non-retail

portfolios had higher, albeit improving, GIF ratios. As at end-June 2012, the

Bank’s non-retail portfolio showed a GIF ratio of 3.3% (end-December 2011:

4.5%). Financing extended to the construction sector posted a somewhat higher

GIF ratio of 5.9%, partly due to a low-base effect and pre-2006 legacy financing.

At the same time, unsecured retail financing accounted for a third (33%) of Bank

Islam’s aggregate financing; these mainly comprised personal financing (30%).

While the concentration on unsecured personal financing exposes the Bank to

non-payment risk, salary deductions or salary transfers5 from employers partially

mitigate the risk of non-payment. A large portion (89%) of the Bank’s personal

financing portfolio was repaid through these methods, as at end-June 2012. The

personal financing facilities are mainly granted to employees of government-

linked entities and large corporates, and posted a low GIF ratio of 0.7% as at

end-June 2012 (end-June 2011: 1.7%).

5 Through the salary-deduction mechanism, the salaries of customers are paid into Bank Islam

accounts. The Bank uses a direct-debit arrangement to deduct repayment amounts once the salaries have been credited into their Bank Islam accounts. Under the salary-transfer mechanism, employers deduct repayments from the salaries of their employees and subsequently, the employers will send cheques to Bank Islam. As at end-June 2012, personal financing repaid through salary deductions had a GIF ratio of 0.41% while personal financing repaid through salary transfers had a GIF ratio of 0.30%.

Still primarily retail

bank...

...with sizeable proportion of unsecured retail

financing

Bank Islam Malaysia Berhad 7

The Bank’s clientele vis-a-vis residential property financing largely consists of

low-to-mid-end customers, with approximately 54% of the Bank’s outstanding

residential property facilities extended for the purchase of properties valued at

less than RM150,000 as at end-June 2012 (end-December 2011: 57%).

Nonetheless, the GIF ratio of Bank Islam’s residential property financing portfolio

has been easing, clocking in at 2.8% as at end-June 2012 (end-December 2011:

3.5%). The delinquency trends of this customer segment are likely to worsen in a

non-conducive economic environment. On this note, the Bank continues to

redirect its focus on higher-income customers.

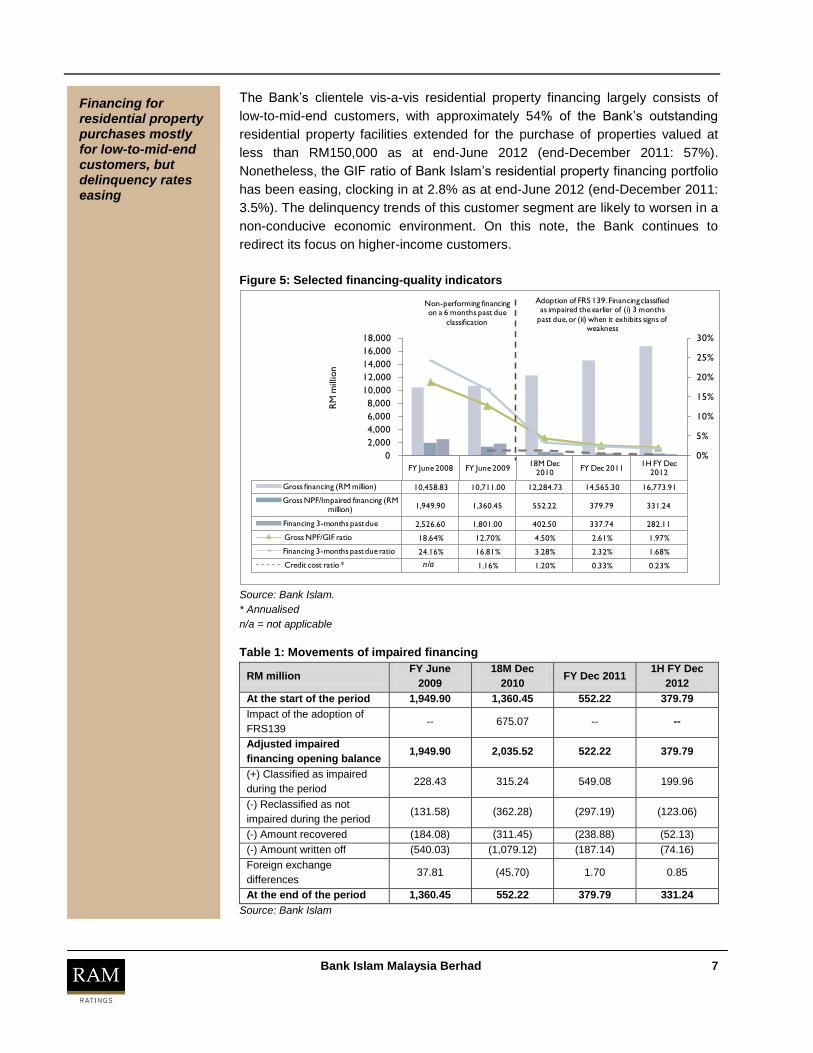

Figure 5: Selected financing-quality indicators

FY June 2008 FY June 200918M Dec

2010FY Dec 2011

1H FY Dec 2012

Gross financing (RM million) 10,458.83 10,711.00 12,284.73 14,565.30 16,773.91

Gross NPF/Impaired financing (RM million) 1,949.90 1,360.45 552.22 379.79 331.24

Financing 3-months past due 2,526.60 1,801.00 402.50 337.74 282.11

Gross NPF/GIF ratio 18.64% 12.70% 4.50% 2.61% 1.97%

Financing 3-months past due ratio 24.16% 16.81% 3.28% 2.32% 1.68%

Credit cost ratio * 1.16% 1.20% 0.33% 0.23%

0%

5%

10%

15%

20%

25%

30%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000 R

M m

illio

n

Adoption of FRS 139. Financing classified as impaired the earlier of (i) 3 months

past due, or (ii) when it exhibits signs of weakness

Non-performing financing on a 6 months past due

classification

n/a

Source: Bank Islam.

* Annualised

n/a = not applicable

Table 1: Movements of impaired financing

RM million FY June

2009

18M Dec

2010 FY Dec 2011

1H FY Dec

2012

At the start of the period 1,949.90 1,360.45 552.22 379.79

Impact of the adoption of

FRS139 -- 675.07 -- --

Adjusted impaired

financing opening balance 1,949.90 2,035.52 522.22 379.79

(+) Classified as impaired

during the period 228.43 315.24 549.08 199.96

(-) Reclassified as not

impaired during the period (131.58) (362.28) (297.19) (123.06)

(-) Amount recovered (184.08) (311.45) (238.88) (52.13)

(-) Amount written off (540.03) (1,079.12) (187.14) (74.16)

Foreign exchange

differences 37.81 (45.70) 1.70 0.85

At the end of the period 1,360.45 552.22 379.79 331.24

Source: Bank Islam

Financing for residential property purchases mostly for low-to-mid-end customers, but delinquency rates easing

Bank Islam Malaysia Berhad 8

On the whole, the better credit quality of financing facilities extended to the

household sector is a plus for the overall credit quality of Bank Islam’s financing

portfolio. The Bank’s overall GIF ratio had eased to 2.0% as at end-June 2012

(end-December 2010: 4.5%), and now falls in line with the Malaysian banking

industry’s average6. In this respect, previously persistent write-offs on impaired

financing, mainly from its pre-2006 legacy financing facilities, have eased.

Meanwhile, the Bank’s credit-cost ratio had moderated from historically lofty

levels to a healthy 0.3%7 as at end-FY Dec 2011 (for the 18 months ended 31

December 2010: 1.2% annualised). The management expects a credit-cost ratio

of 0.3% for the current fiscal year.

Restructured and rescheduled accounts constitute about 4% of the Bank’s

aggregate financing portfolio. Residential property financing facilities accounted

for 56% of its total restructured and rescheduled facilities as at end-June 2012;

these were mainly financing programmes with rescheduled instalment payments.

As at end-June 2012, the Bank’s GIF coverage ratio stood at 126% (end-

December 2010: 77%), mainly due to large collective impairment allowances that

reflect historically elevated delinquency rates on the Bank’s financing portfolio,

before more recent revamping of its underwriting processes.

Securities still feature prominently in Bank Islam’s balance sheet, accounting for

39% of its total assets as at end-June 2012. The Bank’s securities portfolio is

generally viewed to be healthy. While Islamic private debt securities (“PDS”)

comprised about 65% of Bank Islam’s total securities portfolio, these primarily

consisted of government-guaranteed securities, quasi-government securities and

securities with AAA and AA ratings. The latter accounts for 51% of the Bank’s

PDS investments while government-guaranteed and quasi-government securities

accounted for 43% of Bank Islam’s PDS holdings. Malaysian government

investment issues and negotiable Islamic debt certificates were the second- and

third-largest components of the Bank’s securities portfolio, with respective shares

of 19% and 13% as at the same date. We note that the Bank has a policy of only

investing in PDS with AAA and AA ratings. Meanwhile, the Bank has a negligible

exposure to shares and unit trusts; these collectively make up less than 1% of its

total securities holdings.

6 As at end-June 2012, the Malaysian banking industry gross impaired loan/financing ratio was 2.2%.

7 Reflecting MFRS 139 restatements, the Bank’s credit cost ratio was 0.2% in FY Dec 2011.

Better financing-quality indicators

High GIF coverage levels

Healthy securities portfolio

Bank Islam Malaysia Berhad 9

Funding and Liquidity

Figure 6: Bank Islam’s funding and liquidity profiles

FY June 2008 FY June 200918M Dec

2010FY Dec 2011

1H FY Dec 2012

Total deposits (RM million) 20,754.3 25,204.6 26,866.6 28,279.7 28,685.8

Liquid asset ratio 62.26% 67.38% 65.30% 56.90% 52.09%

CASA deposits to total deposits 39.89% 35.95% 39.69% 43.42% 41.77%

Financing-to-deposits ratio 43.66% 38.33% 44.15% 50.00% 57.02%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

0%

10%

20%

30%

40%

50%

60%

70%

80%

RM

mill

ion

Source: Bank Islam

Bank Islam maintains robust funding and liquidity profiles, with a very liquid

balance sheet. The Bank’s liquid-asset ratio of 52% as at end-June 2012 is still

among the highest in RAM Ratings’ rated universe.

Bank Islam relies primarily on deposits for its funding needs; these made up 94%

of its profit-bearing funding as at end-June 2012. In FY Dec 2011, the Bank’s

deposit base added 5% to RM28 billion. With deposit growth trailing the

expansion of its financing portfolio, the Bank’s financing-to-deposits ratio had

increased to 57% as at end-June 2012. Nonetheless, this is still lower than the

management’s optimum financing-to-deposits ratio of 70%–80%, and lower than

the Islamic banking industry average financing-to-deposits ratio of 78% as at

end-June 2012. In the meantime, the Bank maintains a sizeable (42%) proportion

of low-cost current and savings account (“CASA”) deposits in its deposit base.

Bank Islam relies substantially on deposits from corporates and government-

linked entities; deposits from retail customers only account for 17% of its total

deposits. As at end-June 2012, the Bank’s top 3 depositors made up 12% of its

total deposits (end-December 2011: 11%). Tabung Haji is one of Bank Islam’s

largest depositors. While depositor-concentration risk still exists, the Bank’s very

liquid balance sheet and long-standing relationships with its depositors

somewhat alleviate our concerns.

Very liquid balance

sheet

Financing-to-deposits ratio inching closer to

optimum levels

Highly dependent on non-retail

deposits

Bank Islam Malaysia Berhad 10

Financial Performance

Figure 7: Selected profitability indicators

FY June 2008 FY June 200918M Dec

2010FY Dec 2011

1H FY Dec 2012

Pre-financing provision profits 309.40 359.16 709.19 513.59 296.30

Pre-tax profit 316.94 235.87 501.49 469.57 278.402

Net financing margins 3.10% 2.82% 3.08% 3.13% 3.31%

Returns on assets * 1.49% 0.92% 1.16% 1.50% 1.69%

Returns on equity * 27.11% 16.55% 16.44% 17.63% 19.32%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

-

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

RM

million

Source: Bank Islam

* Annualised

In FY Dec 2011, the Bank’s pre-tax profit surged 40% (annualised) to RM469.6

million8. The better showing was anchored by more robust financing income;

Bank Islam’s net financing margin of 3.1% for the year was underpinned by a

sizeable high-yielding personal financing portfolio and a large base of low-cost

CASA deposits. At the same time, the Bank’s fee income also strengthened, with

increases in gains from foreign-exchange-related transactions, gains from the

sale of financial assets, and higher fees and commissions. Financing income

continues to feature prominently in the Bank’s earnings profile, accounting for

80% of its gross income in FY Dec 2011.

On the back of its healthier profit performance, the Bank’s returns on assets and

equity climbed up to 1.5% and 17.6% in FY Dec 2011 (18 months ended 31

December 2010: 1.2% and 16.4% annualised). The Bank’s profitability is

expected to improve further this year, amid moderating credit costs and financing

growth.

8 With MFRS 139 restatements, Bank Islam’s 18M Dec 2010 and FY Dec 2011 pre-tax profits were

RM499.46 million and RM492.47 million, respectively. This represents an annualised 48% y-o-y pre-tax profit growth in the 2011 fiscal year.

Robust net financing margins

Bank Islam Malaysia Berhad 11

Capital Adequacy

Figure 8: Bank Islam’s capital base and capitalisation ratios

FY June 2008

FY June 2009

18M Dec 2010

FY Dec 2011

1H FY Dec 2012

Risk-weighted assets (RM million) 11,150.4 11,781.4 14,798.8 16,925.7 19,328.9

Capital base (RM million) 1,466.5 1,634.5 2,432.9 2,743.2 3,014.0

Tier-1 RWCAR 11.3% 12.3% 15.2% 15.0% 14.4%

Overall RWCAR 13.2% 13.9% 16.4% 16.2% 15.6%

0%

5%

10%

15%

20%

0

5,000

10,000

15,000

20,000

25,000

RM

mill

ion

Source: Bank Islam.

Note: Figures for capital base are net of proposed dividends.

Bank Islam’s capitalisation levels are considered sturdy, with a high proportion of

tier-1 capital. While slightly lower than the ratios as at end-December 2011 after

its proposed dividends, the Bank still posted strong tier-1 and overall RWCARs of

14.4% and 15.6% as at end-June 2012 (end-December 2011: 15.0% and

16.2%)9. These are expected to be able to adequately support its organic growth

over the medium term. We note that the Bank maintains internal overall and tier-

1 RWCARs of at least 13% and 10%, respectively. Bank Islam has also adopted

Bank Negara Malaysia’s Framework on Capital Adequacy for Islamic Banks - the

equivalent of the standardised Basel II approach for conventional banks.

9 With MFRS 139 restatements, the Bank’s tier-1 and overall RWCAR were 15.6% and 16.8%

respectively, as at end-December 2011.

Sturdy

capitalisation

Bank Islam Malaysia Berhad 12

Corporate Information – Bank Islam Malaysia Berhad

Date of Incorporation:

1 March 1983

Commencement of Business:

July 1983

Major Shareholders:

BIMB Holdings Berhad Dubai Financial Group LLC Lembaga Tabung Haji

51.0% 30.5% 18.5%

Directors:

Dato’ Zamani Abdul Ghabi Dato’ Sri Zukri Samat Dato’ Paduka Ismee Ismail Johan Abdullah Zahari @ Mohd Zin Idris Zaiton Mohd Hassan Mohamed Ridza Mohamed Abdulla Abdullah Abdulrahman Abdullah Sharafi Mohammed Abdul Ghaffar Ghualoom Hussain Abdulla

Auditor:

KPMG Desa Megat & Co

Listing:

Not listed

Key Management:

Dato’ Sri Zukri Samat Dato’ Wan Ismail Wan Yusoh Hizamuddin Jamalluddin Maria Mat Said Jamilah Abdul Sallam Khairul Kamarudin Mashitah Hj Osman Norashikin Mohd Kassim Abdul Rashid Abdul Hamid Jaafar Abu Mizan Masram Mohd Nazri Chik Mujibburahman Abd Rashid Wahid Ali Mohd Khalil Malkit Singh Maan Ryan Liew Choon Ching Dato’ Norasni Ayob Jeroen PMM Thijs Leong David @ Leong Sze Khiong

Managing Director General Manager, Strategic Relations General Manager, Strategic Planning General Manager, Legal & Secretarial General Manager, Human Resources Director, Business Development Director, Corporate Investment Banking Head, Treasury Head, Commercial Banking Head, Business Support Head, Recovery & Rehabilitation Head, Shariah Acting Head, Consumer Banking Chief Compliance Officer Chief Financial Officer Chief Technology Officer Chief Operating Officer Chief Risk Officer Chief Internal Audit

Major Subsidiaries/ Associates:

BIMB Investment Management Berhad Bank Islam Trust Company (Labuan) Ltd Amana Bank Limited

100% 100% 20%

Capital History:

Year Remarks Amount (RM million)

Cumulative Total (RM million)

2004 2005 2006

Balance brought forward Issuance of 100,000,000 shares Issuance of 280,000,000 shares

100.00 280.00

500.00 600.00 880.00

2007 2010

Issuance of 845,490,000 shares Conversion of 540,000,000 convertible redeemable non-cumulative preference shares

845.49

540.00

1,725.49

2,265.49

Bank Islam Malaysia Berhad 13

unaudited

STATEMENT OF FINANCIAL POSITION (RM million) 30-Jun-08 30-Jun-09 31-Dec-10 30-Dec-11 30-Jun-12

Cash & Short-Term Funds 9,948.77 8,448.21 2,519.70 3,364.18 2,753.77

Deposits & Placements with Financial Institutions 193.65 0.00 352.80 860.18 300.00

Securities Purchased Under Resale Agreements 0.00 0.00 0.00 0.00 0.00

Financial Investments at Fair Value Through Profit or Loss 54.51 287.68 2,279.45 1,228.95 741.04

Financial Investments Available-For-Sale 3,437.22 8,465.43 12,763.02 11,005.12 12,058.08

Financial Investments Held-To-Maturity 161.53 162.76 215.94 327.33 264.94

Gross Financing & Advances 10,458.83 10,711.00 12,284.73 14,565.30 16,773.91

Collective Impairment Provisions (169.38) (170.84) (345.04) (348.56) (345.64)

Individual Impairment Provisions (1,228.13) (878.30) (79.06) (75.77) (71.79)

Net Financing & Advances 9,061.32 9,661.86 11,860.63 14,140.97 16,356.47

Statutory Deposits 362.15 139.73 10.00 912.00 874.00

Investments in Subsidiaries/Associates/Jointly-Controlled Entities 0.00 0.00 0.00 21.18 23.52

Goodwill & Intangibles 0.00 0.00 0.00 0.00 0.00

Property, Plant & Equipment 127.78 127.71 181.49 200.85 211.40

Other Assets 209.51 197.75 167.25 125.68 252.62

Total Assets 23,556.44 27,491.13 30,350.27 32,186.45 33,835.85

Customer Deposits 20,754.32 25,204.63 26,866.56 28,279.68 28,685.84

Current Account Deposits 5,842.72 6,347.08 7,098.68 8,415.67 7,932.59

Savings Account Deposits 2,436.59 2,713.05 3,564.22 3,862.83 4,050.07

Investment Deposits 6,334.56 8,950.06 10,304.86 10,275.63 11,337.57

Negotiable Instruments of Deposits 6,098.74 7,133.79 5,819.88 5,622.29 5,178.38

Other Deposits 41.70 60.65 78.92 103.26 187.24

Interbank Deposits 58.44 8.08 378.13 384.63 1,430.98

Bills & Acceptances Payable 990.45 283.21 163.19 259.15 270.87

Securities Sold Under Repurchase Agreements 0.00 0.00 0.00 0.00 0.00

Senior Islamic Securities 0.00 0.00 0.00 0.00 0.00

Subordinated Islamic Securities 100.00 100.00 0.00 0.00 0.00

Hybrid Capital Islamic Securities 0.00 0.00 0.00 0.00 0.00

Other Sources of Funds 0.00 0.00 0.00 0.00 0.00

Other Liabilities 333.96 364.03 406.64 470.80 477.75

Total Liabilities 22,237.17 25,959.95 27,814.52 29,394.26 30,865.44

Equity Share Capital 1,725.49 1,725.49 2,265.49 2,265.49 2,265.49

Share Premium 500.02 500.02 500.02 500.02 0.00

Treasury Shares 0.00 0.00 0.00 0.00 0.00

Statutory Reserve 508.82 589.12 795.01 974.59 391.22

Revaluation Reserve 0.00 0.00 0.00 0.00 0.00

Available-For-Sale Reserve (82.61) (9.54) 83.43 117.46 127.25

Other Reserves 58.48 35.45 76.46 67.01 (10.55)

Retained Profits/(Accumulated Losses) (1,390.94) (1,309.36) (1,185.13) (1,132.38) 197.00

Non-Controlling Interests 0.00 0.00 0.48 0.00 0.00

Total Equity 1,319.27 1,531.18 2,535.75 2,792.19 2,970.41

Total Liabilities + Total Equity 23,556.44 27,491.13 30,350.27 32,186.45 33,835.85

Additional Disclosure:

Commitments & Contingencies 9,322.36 7,693.38 13,081.29 9,286.10 10,591.37

Risk-Weighted Assets 11,150.39 11,781.36 14,798.76 16,925.67 19,328.91

T ier-1 Capital Base * 1,257.11 1,443.61 2,250.46 2,539.65 2,779.35

Total Capital Base * 1,466.50 1,634.46 2,432.91 2,743.25 3,014.05

Notes:

* After proposed dividends

FINANCIAL SUMMARY Bank Islam Malaysia Berhad – Group

Bank Islam Malaysia Berhad 14

unaudited

STATEMENT OF COMPREHENSIVE INCOME (RM million) 30-Jun-08 30-Jun-09 31-Dec-10 30-Dec-11 30-Jun-12

18 months 6 months

Financing Income 1,065.54 1,137.35 1,939.74 1,429.81 795.72

Financing Expense (424.39) (434.00) (622.34) (477.11) (271.64)

Net Financing Income 641.15 703.36 1,317.40 952.71 524.08

Fee Income 70.45 86.46 164.68 131.12 72.94

Investment Income 4.65 18.30 51.69 67.98 23.89

Other Income 35.49 32.59 28.97 37.41 21.96

Gross Income 751.74 840.70 1,562.74 1,189.21 642.87

Personnel Expenses (216.46) (228.43) (430.97) (338.14) (182.20)

Other Operating Expenses (228.04) (248.45) (402.85) (305.45) (168.45)

Operating Income before Impairment Charges 307.23 363.82 728.92 545.61 292.21

Net Impairment Charges on Financing 7.55 (123.29) (207.70) (44.02) (17.90)

Net Impairment Charges on Financial Investments 2.16 (4.66) (19.73) (15.41) 0.39

Net Impairment Charges on Commitments, Contingencies & Other Assets 0.00 0.00 0.00 (15.23) 1.36

Operating Income after Impairment Charges 316.94 235.87 501.49 470.95 276.06

Non-Recurring Items 0.00 0.00 0.00 0.00 0.00

Share of Associates/Jointly-Controlled Entities Profits/(Losses) 0.00 0.00 0.00 (1.38) 2.34

Pre-Tax Profit/(Loss) 316.94 235.87 501.49 469.57 278.40

Taxation & Zakat 72.66 (73.99) (92.78) (111.42) (79.84)

Net Profit/(Loss) 389.60 161.88 408.71 358.15 198.56

Gain/(Loss) on Available-For-Sale Financial Investments 0.00 0.00 92.97 34.03 9.79

Changes in Cash Flow & Net Investment Hedges 0.00 0.00 0.00 0.00 0.00

Foreign Currency Translation Differences 0.00 0.00 41.01 (9.45) (1.10)

Share of Other Comprehensive Income/(Loss) of Associates/Jointly-Controlled Entities 0.00 0.00 0.00 0.00 0.00

Income Tax Relating to Other Comprehensive Income/(Loss) 0.00 0.00 0.00 0.00 0.00

Other Components of Comprehensive Income/(Loss) 0.00 0.00 0.00 0.00 0.00

Total Comprehensive Income/(Loss) 389.60 161.88 542.69 382.74 207.25

Additional Disclosure:

Net Profit/(Loss) Attributable to Non-Controlling Interests 0.00 0.00 (0.05) 0.06 0.00

Dividends - Ordinary Shares & Preference Shares 0.00 0.00 19.11 125.40 44.69

FINANCIAL SUMMARY Bank Islam Malaysia Berhad – Group

Bank Islam Malaysia Berhad 15

unaudited

KEY RATIOS 30-Jun-08 30-Jun-09 31-Dec-10 30-Dec-11 30-Jun-12

PROFITABILITY (%)

Net Financing Margin 3.10% 2.82% 3.08% * 3.13% 3.31% *

Non-Financing Income to Gross Income 14.71% 16.34% 15.70% 19.89% 18.48%

Cost to Income 59.13% 56.72% 53.36% 54.12% 54.55%

Return on Assets 1.49% 0.92% 1.16% * 1.50% 1.69% *

Return on Risk-Weighted Assets 3.03% 2.06% 2.52% * 2.96% 3.07% *

Return on Equity 27.11% 16.55% 16.44% * 17.63% 19.32% *

ASSET QUALITY (%)

Gross Impaired Financing Ratio 18.64% 12.70% 4.50% 2.61% 1.97%

Net Newly Classified Impaired Financing Ratio (1.44%) (0.82%) (2.08%) * 0.10% 0.32% *

Financing Credit Cost Ratio (0.07%) 1.16% 1.20% * 0.33% 0.23% *

Impairment Charge Ratio (0.07%) 0.76% 0.64% * 0.22% 0.12% *

Gross Impaired Financing Coverage Ratio 71.67% 77.12% 76.80% 111.73% 126.02%

LIQUIDITY & FUNDING (%)

Liquid Asset Ratio 62.26% 67.38% 65.30% 56.90% 52.09%

Interbank Deposits to Total Profit Bearing Funds 0.27% 0.03% 1.38% 1.33% 4.71%

Customer Deposits to Total Profit Bearing Funds 94.75% 98.47% 98.02% 97.77% 94.40%

CASA Deposits to Total Deposits 39.89% 35.95% 39.69% 43.42% 41.77%

Financing to Deposits Ratio 43.66% 38.33% 44.15% 50.00% 57.02%

CAPITALISATION & LEVERAGE (%)

Internal Rate of Capital Generation 33.32% 11.36% 12.77% 8.74% NA

Tier-1 Regulatory Risk-Weighted Capital Adequacy Ratio 11.27% 12.25% 15.21% 15.00% 14.38%

Overall Regulatory Risk-Weighted Capital Adequacy Ratio 13.15% 13.87% 16.44% 16.21% 15.59%

Notes:

* annualised

NA = Not Available / Not Applicable

Note: All figures prior to FY Dec 2012 are before MFRS 139 adjustments. Bank Islam had adopted the MFRS 139 accounting

policy with effect from 1 January 2012.

FINANCIAL RATIOS Bank Islam Malaysia Berhad – Group

Bank Islam Malaysia Berhad 16

KEY RATIOS FORMULAE

PROFITABILITY (%)

Net Financing Margin Net Finance Income / Average Profit Earning Assets

Non-Financing Income to Gross Income Non-Finance Income / Gross Income

Cost to Income (Personnel Expenses + Other Operating Expenses) / Gross Income

Return on Assets Pre-Tax Profit/(Loss) / Average Total Assets

Return on Risk-Weighted Assets Pre-Tax Profit/(Loss) / Average Total Risk-Weighted Assets

Return on Equity Pre-Tax Profit/(Loss) / Average Total Equity

Non-Finance Income Fee Income + Investment Income + Other Income

Profit Earning Assets Cash & Short-Term Funds + Deposits & Placements with Financial Institutions

+ Securities Purchased Under Resale Agreements + Total Financial Investments

+ Net Financing & Advances

Total Financial Investments Financial Investments at Fair Value Through Profit or Loss + Financial Investments Available-For-Sale

+ Financial Investments Held-To-Maturity

ASSET QUALITY (%)

Gross Impaired Financing Ratio Total Impaired Financing / Gross Financing & Advances

Net Newly Classified Impaired Financing Ratio Net Newly Classified Impaired Financing / Average Gross Financing & Advances

Financing Credit Cost Ratio Net Impairment Charges on Financing / Average Gross Financing & Advances

Impairment Charge Ratio (Net Impairment Charges on Financing + Net Impairment Charges on Financial Investments) /

(Average Gross Financing & Advances + Average Total Financial Investments)

Gross Impaired Financing Coverage Ratio Total Provisions / Gross Impaired Financing

Total Provisions Collective Impairment Provisions + Individual Impairment Provisions

Net Newly Classified Impaired Financing Newly Classified Impaired Financing - Recoveries on Impaired Financing

- Impaired Financing Reclassified As Performing

LIQUIDITY & FUNDING (%)

Liquid Asset Ratio Liquid Assets / (Customer Deposits + Short-Term Funds)

Interbank Deposits to Total Profit Bearing Funds Interbank Deposits / Profit Bearing Funds

Customer Deposits to Total Profit Bearing Funds Customer Deposits / Profit Bearing Funds

CASA Deposits to Total Deposits (Current Account + Savings Account Deposits) / Customer Deposits

Financing to Deposits Ratio Net Financing & Advances / Customer Deposits

Liquid Assets Cash & Short-Term Funds + Deposits & Placements with Financial Institutions

+ Securities Purchased Under Resale Agreements

+ Quoted Financial Investments (excluding Financial Investments Held-To-Maturity)

Short-Term Funds Interbank Deposits + Bills & Acceptances Payable + Securities Sold Under Repurchase Agreements

Profit Bearing Funds Financial Institutions + Quoted Securities (Excluding Financial Investments Held-To-Maturity)Customer Deposits + Interbank Deposits + Bills & Acceptances Payable

+ Securities Sold Under Repurchase Agreements + Total Borrowings

Total Borrowings Senior Islamic Securities + Subordinated Islamic Securities

Hybrid Capital Islamic Securities + Other Borrowings

CAPITALISATION & LEVERAGE (%)

Internal Rate of Capital Generation (Net Profit/(Loss) - Dividends) / Average Total Equity

T ier-1 Regulatory Risk-Weighted Capital Adequacy Ratio (T ier-1 Capital Base - Proposed Dividends) / Risk-Weighted Assets

Overall Regulatory Risk-Weighted Capital Adequacy Ratio (Total Capital Base - Proposed Dividends) / Risk-Weighted Assets

FINANCIAL RATIOS Bank Islam Malaysia Berhad – Group

Bank Islam Malaysia Berhad 17

CREDIT RATING DEFINITIONS

Financial Institution Ratings

Long-Term Ratings

AAA

AA

A

BBB

BB

B

C

D

Short-Term Ratings

P1

P2

P3

NP

D

A financial institution rated AAA has a superior capacity to meet its financial obligations. This is the highest long-term FIRassigned by RAM Ratings.

A financial institution rated AA has a strong capacity to meet its financial obligations. The financial institution is resilientagainst adverse changes in circumstances, economic conditions and/or operating environments.

A financial institution rated A has an adequate capacity to meet its financial obligations. The financial institution is moresusceptible to adverse changes in circumstances, economic conditions and/or operating environments than those in

higher-rated categories.

A financial institution rated BBB has a moderate capacity to meet its financial obligations. The financial institution is morelikely to be weakened by adverse changes in circumstances, economic conditions and/or operating environments than

those in higher-rated categories. This is the lowest investment-grade category.

A financial institution rated BB has a weak capacity to meet its financial obligations. The financial institution is highlyvulnerable to adverse changes in circumstances, economic conditions and/or operating environments.

A financial institution rated B has a very weak capacity to meet its financial obligations. The financial institution has alimited ability to withstand adverse changes in circumstances, economic conditions and/oroperating environments.

A financial institution rated C has a high likelihood of defaulting on its financial obligations. The financial institution ishighly dependent on favourable changes in circumstances, economic conditions and/or operating environments, the lack

of which would likely result in it defaultingon its financial obligations.

A financial institution rated D is currently in default on either all or a substantial portion of its financial obligations, whetheror not formally declared. The D rating may also reflect the filing of bankruptcy and/or other actions pertaining to the

financial institution that could jeopardise the payment of financial obligations.

A financial institution rated P1 has a strong capacity to meet its short-term financial obligations. This is the highest short-term FIR assigned by RAM Ratings.

A financial institution rated P2 has an adequate capacity to meet its short-term financial obligations. The financialinstitution is more susceptible to the effectsof deteriorating circumstances than thosein the highest-rated category.

A financial institution rated P3 has a moderate capacity to meet its short-term financial obligations. The financialinstitution is more likely to be weakened by the effects of deteriorating circumstances than those in higher-rated

categories. This is the lowest investment-grade category.

A financial institution rated NP has a doubtful capacity to meet its short-term financial obligations. The financial institutionfaces major uncertainties that could compromise its capacity for payment of financial obligations.

A financial institution rated D is currently in default on either all or a substantial portion of its financial obligations, whetheror not formally declared. The D rating may also reflect the filing of bankruptcy and/or other actions pertaining to the

financial institution that could jeopardise the payment of financial obligations.

For long-term ratings, RAM Ratings applies subscripts 1, 2 or 3 in each rating category from AA to C. The subscript 1 indicates that thefinancial institution ranks at the higher end of its generic rating category; the subscript 2 indicates a mid-ranking; and the subscript 3

indicates that the financial institution ranks at the lower end of its generic rating category.

A Financial Institution Rating ("FIR") is RAM Ratings' current opinion on the overall capacity of a financial institution to meetits financial obligations. The opinion is not specific to any particular financial obligation, as it does not take into account theexpressed terms and conditions of any specific financial obligation.

Bank Islam Malaysia Berhad 18

RAM Ratings receives compensation for its rating services, normally paid by the issuers of such securities or the rated entity, and sometimes

third parties participating in marketing the securities, insurers, guarantors, other obligors, underwriters, etc. The receipt of this compensation has

no influence on RAM Ratings’ credit opinions or other analytical processes. In all instances, RAM Ratings is committed to preserving the

objectivity, integrity and independence of its ratings. Rating fees are communicated to clients prior to the issuance of rating opinions. While RAM

Ratings reserves the right to disseminate the ratings, it receives no payment for doing so, except for subscriptions to its publications.

RAM Ratings, its rating committee members and the analysts involved in the rating exercise have not encountered and/or are not aware of any

conflict of interest relating to the rating exercise. RAM Ratings will adequately disclose all related information in the report if there are such

instances.

Published by RAM Rating Services Berhad

Reproduction or transmission in any form is prohibited except by

permission from RAM Ratings.

Copyright 2012 by RAM Ratings

RAM Rating Services Berhad

Suite 20.01, Level 20

The Gardens South Tower

Mid Valley City, Lingkaran Syed Putra

59200 Kuala Lumpur

Tel: (603) 7628 1000 / (603) 2299 1000 Fax: (603) 7620 8251

E-mail: [email protected] Website: http://www.ram.com.my