Banco Cruzeiro do Sul - MZGroup · Dividends and Interesent on own capital Banco Cruzeiro do Sul...

17

Banco Cruzeiro do Sul 2Q09/1H09 Earnings Release

Transcript of Banco Cruzeiro do Sul - MZGroup · Dividends and Interesent on own capital Banco Cruzeiro do Sul...

Banco Cruzeiro do Sul

2Q09/1H09

Earnings Release

2

2Q09 Highlights

On the 2Q09 the Bank privileged the asset growth, recovering the paycheck

deductible loans origination;

The 2Q09 net earnings was of R$ 23.2 million, posting a ROAE of 8.3%,

overcoming the 1Q09 loss (R$ 21.8 million) and presenting a net income for

the 1H09 of R$ 1.4 million;

The total payroll deductible loans origination, including the paycheck

deductible credit card, on the 2Q09 amounted to R$ 842.1 million, 28.5%

higher than the 1Q09 (R$ 655.5 million);

The total on-balance credit portfolio reached R$ 3.789 billion: R$ 3.439

billion in paycheck deductible loans, R$ 91.2 million in credit card

operations, and R$ 258.9 million in the SME business segment.

The term deposit base amounted to R$ 2,826 million, posting a growth of

49.6% if compared to 1Q09 (R$ 1,889.1 million), and 101.4% compared to

2Q08 (R$ 1,402.6 million).

3

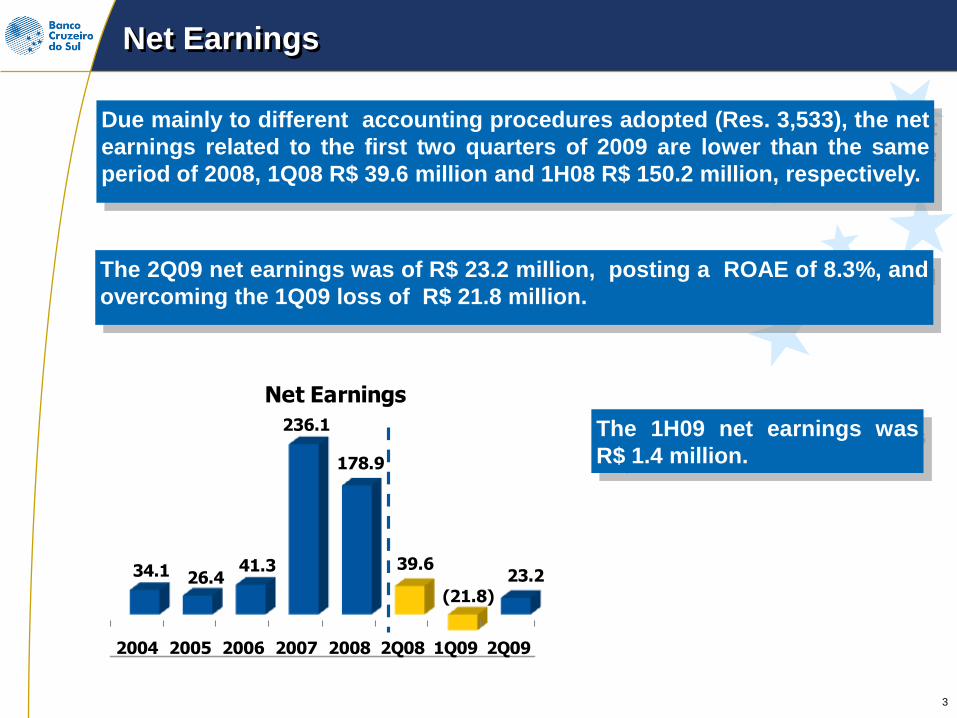

Net Earnings

Due mainly to different accounting procedures adopted (Res. 3,533), the net

earnings related to the first two quarters of 2009 are lower than the same

period of 2008, 1Q08 R$ 39.6 million and 1H08 R$ 150.2 million, respectively.

The 2Q09 net earnings was of R$ 23.2 million, posting a ROAE of 8.3%, and

overcoming the 1Q09 loss of R$ 21.8 million.

The 1H09 net earnings was

R$ 1.4 million.

2004 2005 2006 2007 2008 2Q08 1Q09 2Q09

34.1 26.441.3

236.1

178.9

39.6

(21.8)

23.2

Net Earnings

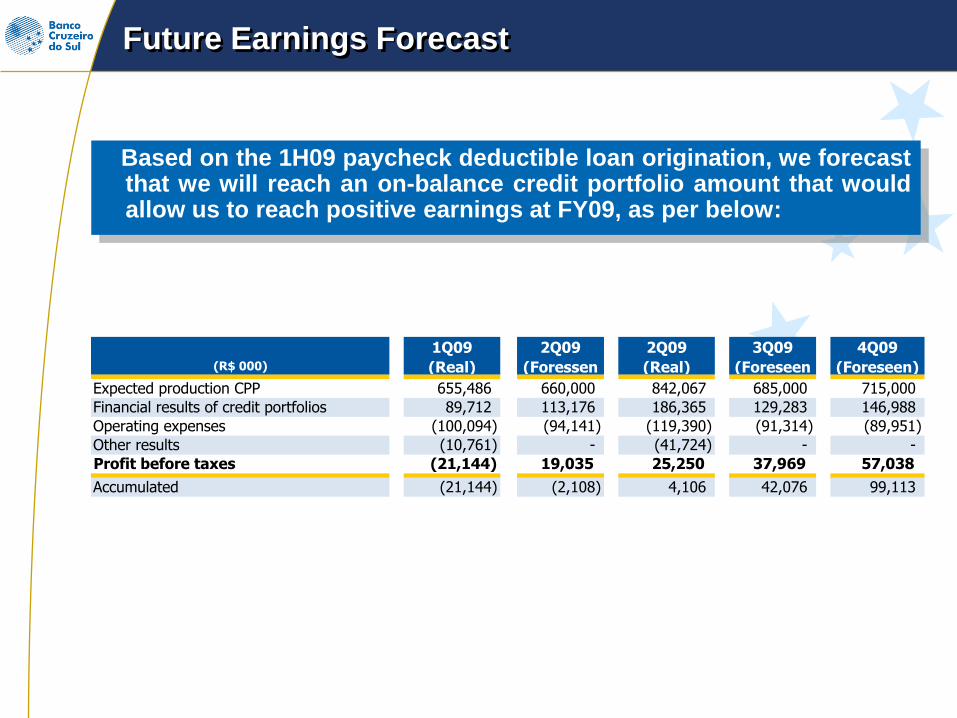

Future Earnings Forecast

Based on the 1H09 paycheck deductible loan origination, we forecastthat we will reach an on-balance credit portfolio amount that wouldallow us to reach positive earnings at FY09, as per below:

Expected production CPP 655,486 660,000 842,067 685,000 715,000

Financial results of credit portfolios 89,712 113,176 186,365 129,283 146,988

Operating expenses (100,094) (94,141) (119,390) (91,314) (89,951)

Other results (10,761) - (41,724) - -

Profit before taxes (21,144) 19,035 25,250 37,969 57,038

Accumulated (21,144) (2,108) 4,106 42,076 99,113

(R$ 000)

1Q09

(Real)

2Q09

(Foressen

2Q09

(Real)

4Q09

(Foreseen)

3Q09

(Foreseen

5

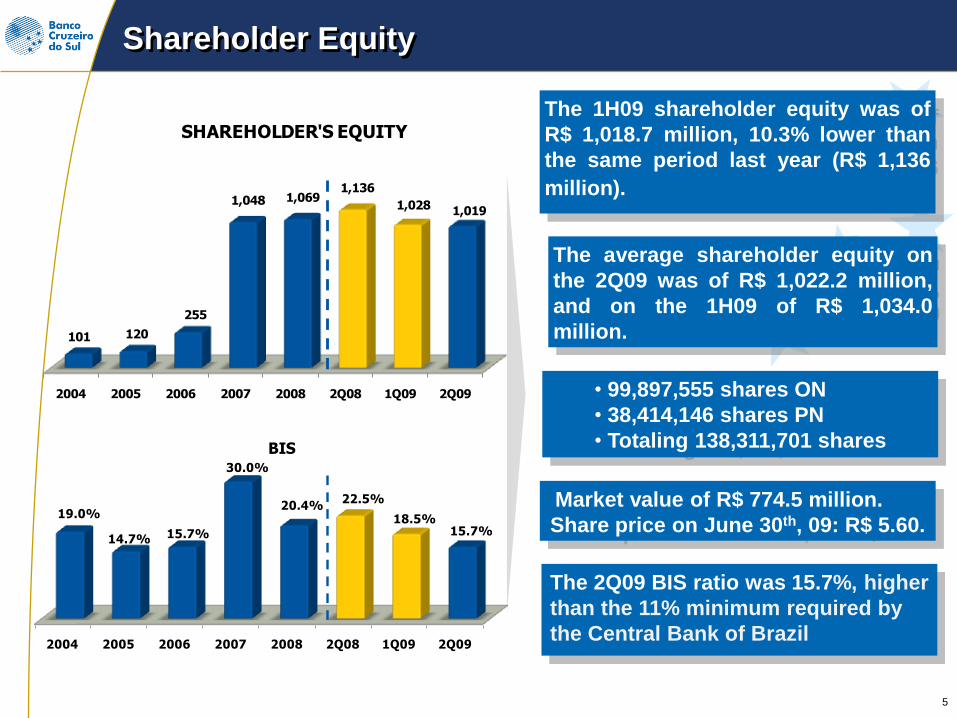

Shareholder Equity

The average shareholder equity on

the 2Q09 was of R$ 1,022.2 million,

and on the 1H09 of R$ 1,034.0

million.

Market value of R$ 774.5 million.

Share price on June 30th, 09: R$ 5.60.

• 99,897,555 shares ON

• 38,414,146 shares PN

• Totaling 138,311,701 shares

The 1H09 shareholder equity was of

R$ 1,018.7 million, 10.3% lower than

the same period last year (R$ 1,136

million).

The 2Q09 BIS ratio was 15.7%, higher

than the 11% minimum required by

the Central Bank of Brazil2004 2005 2006 2007 2008 2Q08 1Q09 2Q09

19.0%

14.7% 15.7%

30.0%

20.4%22.5%

18.5%15.7%

BIS

2004 2005 2006 2007 2008 2Q08 1Q09 2Q09

101 120

255

1,048 1,069 1,136

1,028 1,019

SHAREHOLDER'S EQUITY

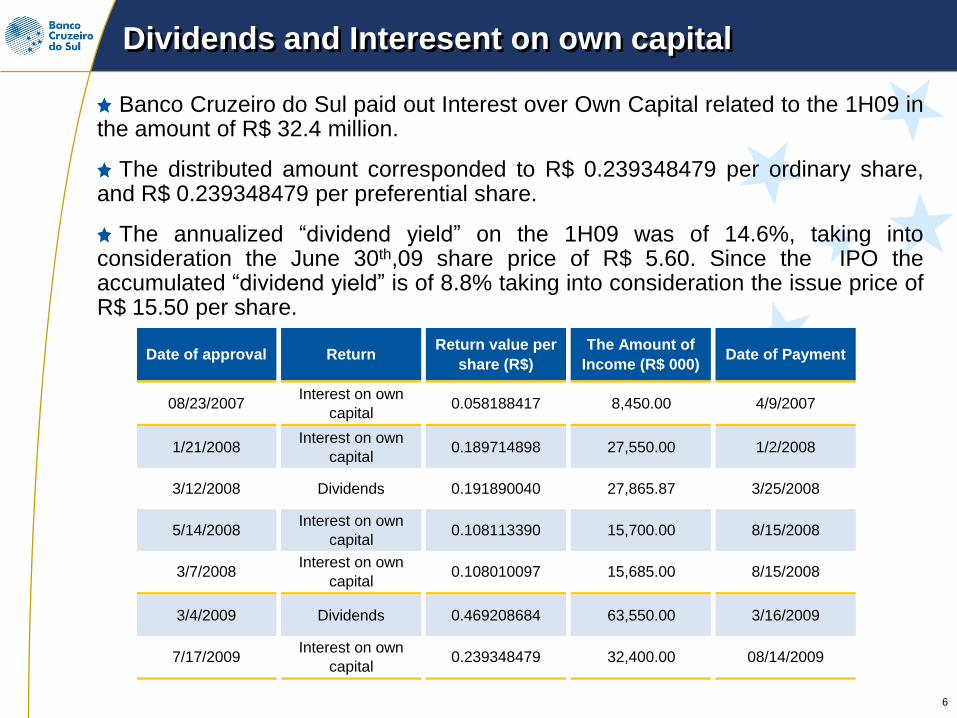

Dividends and Interesent on own capital

Banco Cruzeiro do Sul paid out Interest over Own Capital related to the 1H09 inthe amount of R$ 32.4 million.

The distributed amount corresponded to R$ 0.239348479 per ordinary share,and R$ 0.239348479 per preferential share.

The annualized “dividend yield” on the 1H09 was of 14.6%, taking intoconsideration the June 30th,09 share price of R$ 5.60. Since the IPO theaccumulated “dividend yield” is of 8.8% taking into consideration the issue price ofR$ 15.50 per share.

6

Date of approval ReturnReturn value per

share (R$)

The Amount of

Income (R$ 000)Date of Payment

08/23/2007Interest on own

capital0.058188417 8,450.00 4/9/2007

1/21/2008Interest on own

capital0.189714898 27,550.00 1/2/2008

3/12/2008 Dividends 0.191890040 27,865.87 3/25/2008

5/14/2008Interest on own

capital0.108113390 15,700.00 8/15/2008

3/7/2008Interest on own

capital0.108010097 15,685.00 8/15/2008

3/4/2009 Dividends 0.469208684 63,550.00 3/16/2009

7/17/2009Interest on own

capital0.239348479 32,400.00 08/14/2009

7

Main Business lines

Focused on low risk personal lending backed by payroll

deductible instrument, complemented by middle market

operations.

Notes:1 Total credit portfolio includes credit assignments

Segment Product

CR

ED

IT Payroll Loans

Middle Market

Loans to Public

Servants

Loans to

Beneficiaries of

INSS

Paycheck

Deductible

Credit Cards

Payroll Loan

Linked Credit

Card

Short term working capital

loans guaranteed by

receivables

% Total

Portfólio1

2Q09 – 2Q08

Growth¹ (%)

% Total

Assets

95.4% 11.3%

4.6% (37.4%)

78.4%

3.8%

8

Credit Portfolio

Source: Banco Cruzeiro do Sul

Portfolio Balance - R$ 3,788.6 mm

The total credit portfolio reached R$ 5.6

billion in 2Q09, a growth of 7.5%

compared to 2Q08 (R$ 5.2 billion), and a

negative growth of 0.3% compared to

the 1Q09 (R$ 5.6 billion).

The on-balance credit portfolio reached

R$ 3.789 billion in 2Q09, a growth of

9.9% compared to 1Q09 (R$ 3.447

billion), and a negative growth of 0.3%

compared to 2Q08 (R$ 3.800 billion).

The amount of assets assigned to other

financial institutions, and senior shares

in FIDC represented 32.5% of the

portfolio total in 2Q09 (R$ 5,611.0

million), against 38.7% in 1Q08.

Total Credit Portfolio (R$ mm)

3,438.690.8%

91.22.4%

258.96.8%

Portfolio Balance

R$ 3,788.6 mm

Paycheck-deductible¹ Paycheck-deductible Credit Card Middle Market

2004 2005 2006 2007 2008 2Q08 1Q09 2Q09

375 493 1,334

3,289 3,197 3,800 3,447 3,789

172 302

545

845 1,285 743 1,295

1,110

249 642

622

288

832 678 884 713

Balance Sheet Contracts of Loan with co-obligation Contracts of Loan without co-obligation

796

1,436

2,501

4,422

5,6265,222

5,6115,314

Origination (R$ mm) Paycheck – Deductible Loans (R$ Billion)

9

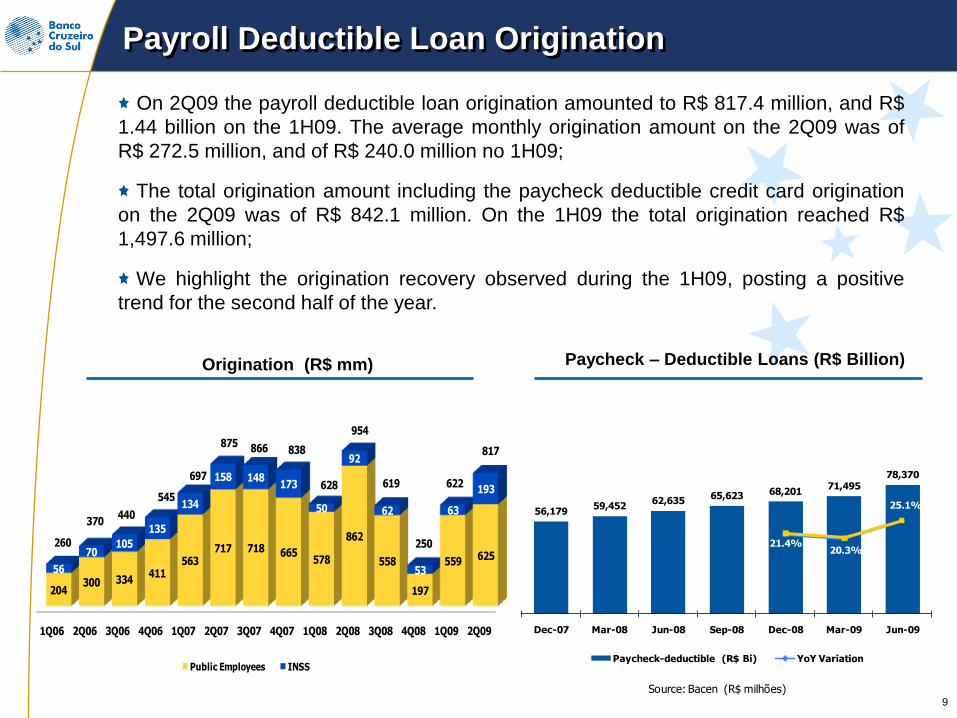

Payroll Deductible Loan Origination

On 2Q09 the payroll deductible loan origination amounted to R$ 817.4 million, and R$

1.44 billion on the 1H09. The average monthly origination amount on the 2Q09 was of

R$ 272.5 million, and of R$ 240.0 million no 1H09;

The total origination amount including the paycheck deductible credit card origination

on the 2Q09 was of R$ 842.1 million. On the 1H09 the total origination reached R$

1,497.6 million;

We highlight the origination recovery observed during the 1H09, posting a positive

trend for the second half of the year.

1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09

204 300 334

411 563

717 718 665 578

862

558

197

559 625 56

70 105

135

134

158 148 173

50

92

62

53

63

193

Public Employees INSS

370440

545

697

875 866

628

954

619

250

622

838

260

817

56,179 59,452

62,635 65,623 68,201

71,495 78,370

21.4%20.3%

25.1%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

90 000

Dec-07 Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09

Payroll Loans

Paycheck-deductible (R$ Bi) YoY Variation

Source: Bacen (R$ milhões)

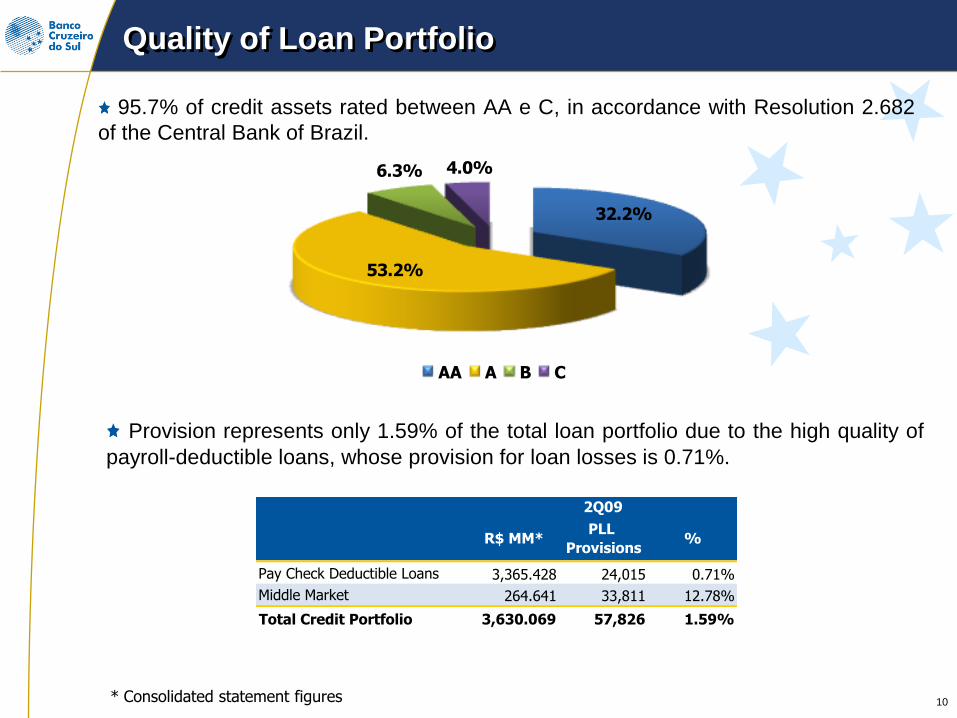

Quality of Loan Portfolio

95.7% of credit assets rated between AA e C, in accordance with Resolution 2.682

of the Central Bank of Brazil.

10* Consolidated statement figures

32.2%

53.2%

6.3% 4.0%

2Q09 Quality of Loan Portfolio

AA A B C

R$ MM*PLL

Provisions%

Pay Check Deductible Loans 3,365.428 24,015 0.71%

Middle Market 264.641 33,811 12.78%

Total Credit Portfolio 3,630.069 57,826 1.59%

2Q09

Provision represents only 1.59% of the total loan portfolio due to the high quality of

payroll-deductible loans, whose provision for loan losses is 0.71%.

11

Credit Card Operations

Issued card growth was of 69.2% if compared

to the 2Q08 (797,4 thousand).

The number of active customers grew 38%

between the 2Q08 (275.6 thousand) and the

2Q09 (380.4 thousand). The growth between

the 1Q09 (370.2 thousand) and the 2Q09 was of

2.8%.

The outstanding on-balance financed amount

on the 2Q09 was of R$ 91.2 million, 37.1%

higher than the 1Q09.

Financed Balance (R$ mm) Issued Cards (000)

Banco Cruzeiro do Sul has more than 100 agreements with government entities to offer the

Paycheck deductible loan credit card.

3,438.690.8%

91.22.4%

258.96.8%

Portfolio Balance

R$ 3,788.6 mm

Paycheck-deductible¹ Paycheck-deductible Credit Card Middle Market

2005 2006 2007 2008 2Q08 1Q09 2Q09

21.6

64.3

115.6

33.4

205.6

66.5

91.2

2005 2006 2007 2008 2Q08 1Q09 2Q09

107.3

334.2

604.1

1,224.2

797.4

1,293.21,349.0

12

Middle Market

In 2Q09 the credit portfolio on the

MME segment reached R$ 258.9

million, a negative growth of 37.4%

compared to same period of 2008

(R$ 413.4 million). Compared to

1Q09 the portfolio decrease 8.9%

(R$ 284.1 million).

•Average credit portfolio amount: R$

1.2 million.

•Average credit portfolio interest rate:

2.18% p.m.

•Average credit portfolio tenor: 151

days

131 active customers.

Conservative credit approach, with

collateral quality improvement, and

shorter tenor transactions was the

driver of the MME business strategy.

Middle Market

3,438.690.8%

91.22.4%

258.96.8%

Portfolio Balance

R$ 3,788.6 mm

Paycheck-deductible¹ Paycheck-deductible Credit Card Middle Market

2004 2005 2006 2007 2008 2Q08 1Q09 2Q09

75.0121.5

161.2

358.4

281.5

413.4

284.1258.9

Middle Market

13

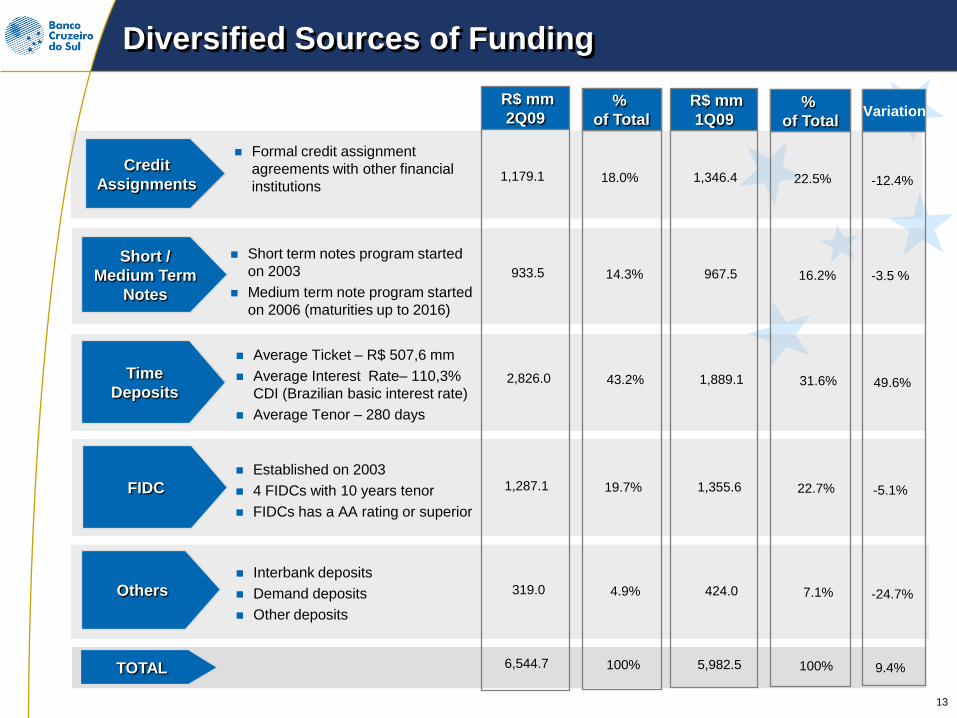

Diversified Sources of Funding

Short /

Medium Term

Notes

Short term notes program started

on 2003

Medium term note program started

on 2006 (maturities up to 2016)

Others

R$ mm

2Q09%

do Total

967.5 16.2%

1,355.6 22.7%

1,889.1 31.6%

Formal credit assignment

agreements with other financial

institutions1,346.4 22.5%

R$ mm

1Q09%

do Total

%

of Total%

of Total

%

do Total

-5.1%

49.6%

-12.4%

Variation

TOTAL 5,982.5 100% 9.4%

FIDC

424.0 7.1% -24.7%

933.5 14.3%

1,287.1 19.7%

2,826.0 43.2%

1,179.1 18.0%

6,544.7 100%

319.0 4.9%

Credit

Assignments

Time

Deposits

Average Ticket – R$ 507,6 mm

Average Interest Rate– 110,3%

CDI (Brazilian basic interest rate)

Average Tenor – 280 days

Established on 2003

4 FIDCs with 10 years tenor

FIDCs has a AA rating or superior

Interbank deposits

Demand deposits

Other deposits

-3.5 %

Contractual Liquidity

During the 1H09 Banco Cruzeiro do Sul maintained its liquidity and focus on asset

quality policy adopted in the past quarters.

The increase in guarantees for time deposits via the Fundo Garantidor de Crédito,

authorized by the National Monetary Council as of April 1, 2009, enabled the issue of

Time Deposits with Special Guarantee (DPGEs) in conditions favorable to our paycheck-

deductible loans requirements.

We continued our relationship with partner financial institutions, assigning credit assets

that generated resources at prices and maturity dates compatible with our operations, but

DPGEs funding reduced our dependence on the assignment of assets to other financial

institutions, and consequently the maintenance of a higher asset volume in the portfolio.

14

R$ 000.000

Assets 4,611.8

Cash 752.8

Cash equivalents 1

70.4

Credit assets for assignment (Paycheck Deductible + SME) 3,788.6

Liability 3,265.4

National currency 2,455.5

Foreign currency 809.9

Balance 1,346.4

¹Cash in FIDC's, Cash in other currencies, Pledged securities (BM&F)

15

341 operational agreements

covering more than 2,800 entities

on the 3 government levels as

follows: 149 federal, 91 state, and

101 municipalities.

Correspondent Banks

Agreements with government entities

National distribution coverage 410 correspondents;

Long lasting relationship with the correspondents;

Full IT support with in house technology

development;

Remuneration through commissions and incentive

plans based on effective net origination.

The average weighted commission paid to

correspondents on the 2Q09 was of 8,29%,

compared to 6,35% on the 1Q09 and 6,40% on the

2Q08;

Our 10 major correspondents were responsible for

18.4% of the total paycheck deductible loan

origination on the 2Q09 and for 20% on the 1H09.

2004 2005 2006 2007 2008 2Q08 1Q09 2Q09

95

207248

300

337 329 340 341

2004 2005 2006 2007 2008 2Q08 1Q09 2Q09

120

251281

297

360

306

397 410

Distribution Network and Franchise

16

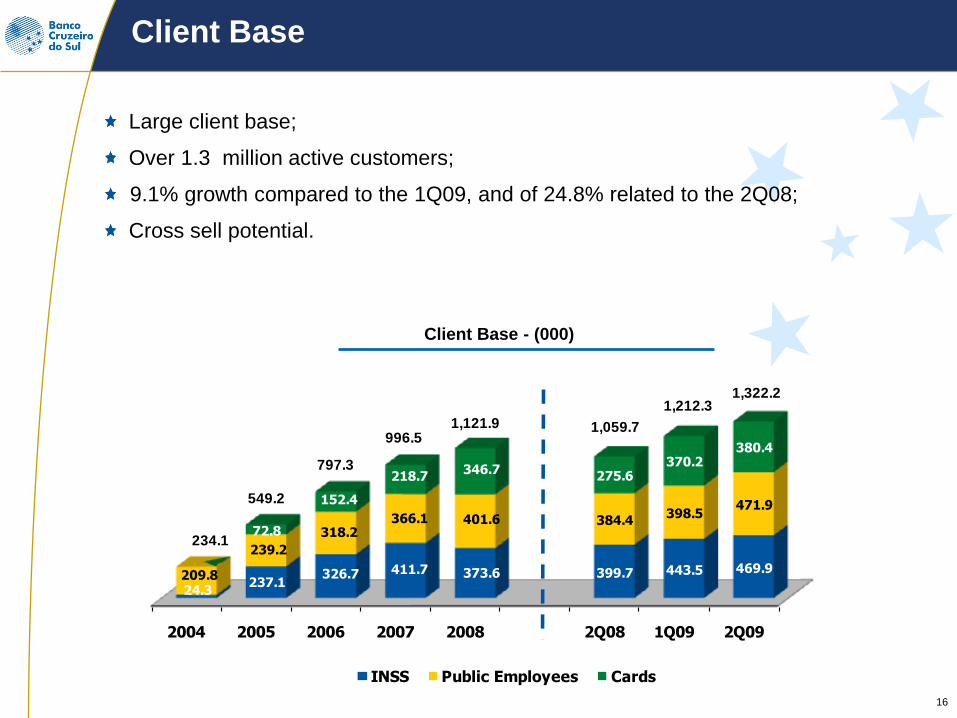

Client Base

Large client base;

Over 1.3 million active customers;

9.1% growth compared to the 1Q09, and of 24.8% related to the 2Q08;

Cross sell potential.

Client Base - (000)

2004 2005 2006 2007 2008 2Q08 1Q09 2Q09

24.3 237.1

326.7 411.7 373.6 399.7 443.5 469.9209.8

239.2

318.2 366.1 401.6 384.4

398.5 471.9

72.8

152.4

218.7 346.7

275.6 370.2

380.4

INSS Public Employees Cards

234.1

549.2

797.3

996.51,121.9

1,212.31,322.2

1,059.7

17

IR Contacts:

Fausto Vaz Guimarães Neto

Phone: +55 (11) 3848-2704

E-mail: [email protected]

João de Lacerda Soares

Phone: +55 (11) 3848-1563

E-mail: [email protected]

Roberto Coutinho

Phone: +55 (11) 3848-2739

E-mail: [email protected]

ri.bcsul.com.br

![Cruzeiro ..[1]](https://static.fdocuments.us/doc/165x107/558df7931a28ab60348b4571/cruzeiro-1.jpg)