Balanced Scorecard

88

BALANCED SCORECARD AS PERFORMANCE MANAGEMENT TOOL By VELUSAMY.NP (REG. NO. 0929170) A PROJECT REPORT Submitted to the CRESCENT BUSINESS SCHOOL in partial fulfillment of the requirements for the award of the degree of MASTER OF BUSINESS ADMINISTRATION APRIL 2011

Transcript of Balanced Scorecard

BALANCED SCORECARD AS PERFORMANCE MANAGEMENT TOOL

By

VELUSAMY.NP

(REG. NO. 0929170)

A PROJECT REPORT

Submitted to the

CRESCENT BUSINESS SCHOOL

in partial fulfillment of the requirements

for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

APRIL 2011

BONAFIDE CERTIFICATE

Certified that the project report titled “Balanced Scorecard as Performance

Management Tool” is the bonafide work of Velusamy.NP who carried out the research

under my supervision. Certified further, that to the best of my knowledge the work

reported herein does not form part of any other project report or dissertation on the basis

of which a degree or award was conferred on earlier occasion on this or any other

candidate.

L.ARAVIND KUMARAN Dr. MIRZA S. SAIYADAIN VIJAY SAMPATH

Associate professor, CBS Dean, CBS External Guide

Internal Guide

ACKNOWLEDGEMENT

I express my profound thanks to our respected Vice-Chancellor Dr. P.

KANNIAPPAN, M.Sc. Ph.D., and our Registrar Dr. V.M. PERIASAMY, B.E., M.E.,

Ph.D., for their enthusiastic support and help in providing all resources behind the scenes.

I wish to regard my sincere thanks to Dr. MIRZA S. SAIYADAIN, M.A., Ph.D.,

Professor and Dean, Crescent Business School, B.S. Abdur Rahman University,

Vandalur, Chennai – 600048.

I would like to thank to my guide L.ARAVIND KUMARAN, Assistant Professor,

Crescent Business School, for her full involvement in every part of my project.

My sincere thanks to SUVANDHU MAHAPATRA, Assistant vice President,

Operational Excellence, Zenta Knowledge Service for permitting me to pursue my

summer project at Company name. I would like to thank my external guide VIJAY

SAMPATH, Senior Manager, Operational Excellence, Zenta Knowledge Service. For his

morale support and encouragement, which helped me in carrying out the project

successfully.

I sincerely thank all the staff members of the Crescent Business School for their

valuable advice and kind cooperation, without which the project would not have emerged

as a successful one.

It is once again a pleasure to acknowledge to my parents, friends and family members

for their constructive and valuable suggestions towards improvement of this project.

VELUSAMY.NP

ABSTRACT

The Balanced Scorecard is the strategic planning and management system. It

helps to align business activities to the vision and strategy of the organization; it

improves internal and external communication, and monitor organization performance

against strategic goals. Zenta follows various metric to measure the overall performance

of the organization this project I am trying to fit all of the Zenta metric to a balanced

scorecard framework. This helps to measure and control and to align all business

activities into vision and strategy of the organization.

In balanced scorecard all the four perspectives of Kaplan and Norton is

considered and analysis is preceded according to these perspectives. In Zenta all

measured metrics are considered as strategic objective. And according to these strategic

objectives strategic measurement is done with the help Lagging and Leading indicator

As the balanced scorecard is the performance management tool it will consider

the Cause and Effect relationship for all the metric along with this performance drivers

and outcomes for each and every strategy which is formulated are measured, which will

show the performance of the strategy after it is implemented. So it makes mangers to

make right decision which results in organizational growth and development.

Normally balanced scorecard follows Top to Bottom approach of management all

the decisions are made at higher level and it is communicated to the lower level. Goals

framed according to the vision and it is classified and personal goals are aligned and

communicated to the employees. So in single scorecard all the aspects are considered and

performance of each and every strategy are measured this made to call balanced

scorecard as effective performance management tool. This entire project this is taken as

base line project is proceeded.

TABLE OF CONTENTS

CH NO CONTENTS PAGE NO

1 INTRODUCTION

1.1 company profile 1

1.1.1 Quality certification 2

1.1.2 Corporate philosophy 2

1.2 Introduction to balanced scorecard 4

1.2.1 History 4

1.3 Need of study 6

1.4 Objectives of balanced scorecard 7

1.5 Scope of balanced scorecard as performance Management tool 8

2 LITERATURE

2.1 Review of literature 9

2.1.1 Kaplan and Norton Approach of Balanced scorecard 9

2.1.1.1 Perspectives of Kaplan and Norton

11

2.1.1.2 Linking the Balanced Scorecard Measures

to Strategic Metric 13

2.1.1.3 Benefits of balanced scorecard 15

2.1.2 Performance Management system 16

2.1.2.1 Benefits of performance management system 17

3 MEASURING BUSINESS STRATEGIES

3.1 designs of balanced scorecard 19

3.1.1 Improved design method of Kaplan and Norton 20

3.2 Key measures of balanced scorecard 21

CH NO CONTENTS PAGE NO

3.3 Data collection method 25

3.4 Zenta business measurement System 26

3.4.1 Goal Flow 26

3.4.2 Translating Vision and Mission to Balanced scorecard 28

3.4.3 Metric analysis in Zenta 29

3.4.3.1 Seat Utilization 29

3.4.3.2 Transportation Cost 29

3.4.3.3 Employees Skill Effectiveness 30

3.4.3.4 Competency per FTE 31

3.4.3.5 Customer Satisfaction 33

3.4.3.6 Asset utilization 34

3.4.3.7 Employee Productivity 34

4 FORMULATING STRATEGIES

4.1 Zenta’s Approach on Balanced Scorecard 35

4.2 Balanced Scorecard to Zenta 38

4.2.1 Strategic Objective 38

4.2.2 Strategic Measurement 40

4.3 Achieving Strategic Alignment from Top to Bottom 43

5 CONCLUSION

5.1 Summary: Findings 45

5.2 Conclusion 46

6 APPENDIX

Bibliography 47

LIST OF FIGURES

Figure No TITLE PAGE NO

2.1 Balanced scorecard Approach by Kaplan and

Norton

11

2.2 Cause and Effect Relationship 13

3.1 Goal Flow in Zenta 27

3.2 Translating Vision and Mission to Balanced

Scorecard

28

3.3 Seat Utilization 29

3.4 Transportation Cost 30

3.5 Employee skill Effectiveness 31

3.6 Competency Per FTE 32

3.7 Employee Satisfaction 33

3.8 Asset Utilization 34

3.9 Employee Productivity 34

4.1 Zenta’s Approach On Balanced Scorecard 37

4.2 Employee Development relationship with

Balanced Scorecard

38

4.3 Top to Bottom Balanced Scorecard Approach 42

LIST OF TABLE:

Table no Content Page no

1 Balanced scorecard for Zenta 41

LIST OF ABBERIVATIONS

BSC – balanced scorecard

FTE – Full Time Employee

CU – capacity utilization

SU – seat utilization

CRM- customer relationship management

TQM – Total Quality Control

BG – Business Group

SBG - Sub Business group

RMS – Residential mortgage service

CSG – commercial servicing group

DD – Due Diligence

LA – Lease Administration

TAT – Turn Around Time

CSAT – Customer Satisfaction

FPY – First Pass Yield

CHAPTER – 1

1.1INDUSTRY PROFILE:

US Real Estate Industry:

Real estate in United States is one of the largest markets in the world. In fact, it is so

significant to world economic activity that the availability of easy money and the

subsequent Housing Bubble triggered the Sub-Prime Crisis and eventually the global

Financial Crisis of 2008 - 2009 that brought the world's economy to its knees. The US

real estate market is divided into 2 sectors: commercial real estate and residential real

estate. Most discussion tends to focus on residential real estate (i.e. houses), but

commercial real estate is also a critical sector of the economy, and is made up of offices,

shopping malls, factories, warehouses and other commercial buildings.

In order to be successful in real estate investment, an investor needs to understand house

price trends, assess the condition and value of the investment property, and secure a

suitable mortgage or other form of real estate finance. The US real estate industry has

been experiencing wonderful growth due to the relatively steady good economy. In

2006, some markets had major gains in occupied space, others saw record sales

transactions. The market has begun to tighten, developers remained cautious possibly

eye toward the future, particularly predictions of escalating rental rates.

Major Participants in the Real Estate Industry

Developers

Development is an idea that comes to fruition when consumers – tenants or

owner- occupants acquire and use the space put in place by the development team. Land,

labor, capital management and entrepreneurship are needed to transform an idea into

reality. Developers balance the needs of diverse providers and consumers of the real

estate product. The developers have to demonstrate the project's feasibility to the capital

markets and pay interest or assign Equity positions in return for funding.

Appraisers

Appraisers can be a part of every stage of the property development process.

Appraisers are primarily responsible for valuation of the project. They estimate the

market value of the property and typically prepare a formal document called appraisal.

Appraisal may be necessary when a developer transfers ownership, seeks financing and

credit, resolves tax matters, and establishes just compensation in condemnation

proceedings. Appraisers can also evaluate a project as input to market studies and

feasibility studies. Some of the familiar names in the US Real Estate markets include CB

Richard Ellis, Cushman and Wakefield and Grubb and Ellis.

Property managers

Property managers focus on the day operation of the asset. Property managers

carry responsibility for all respects of the physical space in accordance with the asset

manager's plan. The responsibilities of a property manager include:

Marketing and leasing

Maintenance and repair

Tenant relations including rent collection

Insurance

Accounting

Human resource management

Providing timely information to the asset manager about events affecting the

property.

Some of the major property managers include Trammel Crow Company and Grubb and

Ellis Company.

Brokers/ Leasing Agents

Real Estate brokers and leasing agents are hired to act in the name of the

developer or asset manager in leasing and selling space to prospective tenants or buyers.

Their function, particularly in leasing large industrial and commercial spaces is to carry

out one of the most complex financial negotiations in the development process. Leasing

agents must balance all the various uses' individual needs against the developer's

financial model.

Lenders

A) Construction Lenders are usually commercial banks, which are responsible

for financial during project construction and for seeing that the developer completes the

project within the budget and according to the specifications.

B) Permanent lenders seek to originate safe loans generating the maximum

possible return. The market value of the completed project is very critical in that it serves

as the primary collateral for the loan.

1.2 COMPANY PROFILE

Zenta Knowledge Services Pvt. Ltd.,

Zenta was founded in 2001, Zenta is a world-class knowledge process outsourcing

(KPO) and business process outsourcing (BPO) and Company, offering a full range of

back-office, voice and on-site support solutions such as Credit Card Servicing, Consumer

Lending Servicing, Accounts Receivable Management, Mortgage Servicing and Real

Estate Capital Market Analytics. The Company serves the following verticals:

Consumer Credit, Insurance and Financial Services, and Commercial and Residential

Real estate

With 4,500+ employees worldwide, Zenta has operations in six locations across

three continents. Zenta is a preferred employer in India.

SOLUTIONS PROVIDED BY ZENTA

From origination and throughout the customer lifecycle, Zenta delivers deep, end-

to-end servicing solutions. Zenta's specialized focus on the financial services industry and

our management expertise and experience, are the reasons we have been chosen to

provide high-end business processing for some of the world's most prestigious banks and

financial institutions.

Instead of coordinating multiple vendors, Zenta's complete solution set makes it

possible for clients to work with one company only - providing a single source for all

their business processing needs.

Zenta's end-to-end solutions include:

Credit card servicing

Commercial Realty Services

Residential Realty Services

Account Receivables management , and

Healthcare Revenue Cycle Management

Residential Mortgage Services

1.1.1 Quality Certification:

ISO 9001:2008 certified:

ISO 9001 is a quality management standard. It applies to all types of

organizations. It doesn't matter what size they are or what they do. It can help

both product and service organizations achieve standards of quality that are

recognized and respected throughout the world.

SAS 70 Type II Assessed

Statement on Auditing Standards (SAS) No. 70, Service Organizations, is a

widely recognized auditing standard developed by the American Institute of

Certified Public Accountants (AICPA). SAS 70 Type II is for operating

effectively

1.1.2 Corporate Philosophy

Client Focused:

We're passionate about our clients and are easy to do business with. We sell our

clients what they want to buy, how they want to buy it. We are flexible and responsive,

tailoring our solutions to our clients' unique needs. And we honor our commitments.

Employee Centric:

We provide our employees with rewarding and satisfying career opportunities

based on their personal performance and contribution.

Cultural Compatibility:

Our clients are primarily in North America and Europe. Our operations are

primarily in India. We must be adept at managing and leading in multiple cultures. We

have assembled a diverse management team that understands the Western business

environment and the needs, aspirations and motivations of our global work force.

Ethics:

The line between right and wrong is not gray or blurred. It is a bright line and we

will not cross it, nor will we tolerate anyone who does

Operational Excellence:

We are committed to operational excellence. We employ a global work force. We

capture work anywhere in the world, move it to wherever in the world we can find the

right blend of cost and quality to work and deliver it back to our clients, wherever in the

world they may be

Accountability:

We hold ourselves accountable for results. We push decision-making to the

lowest possible level. When approvals are required, they are given as rapidly as possible.

Our business leaders are experienced outsourcing industry professionals from global

companies. We have an exceptional track record of attracting and retaining senior talent

with both global exposure and domain expertise to meet our clients' unique business n?

ends.

1.3 NEED FOR STUDY

1. Creating a winning strategy is only the first part of your Balanced Scorecard

implementation. The next part is measuring the success (or "failure") of your

strategy.

2. Besides the Balanced Scorecard, performance measurement systems have mainly

focused on lagging financial indicators. Although non-financial measures have

existed for long, their link to strategy and financial results has been vague at best.

On the contrary, the Balanced Scorecard provides predictive, forward-looking

views of the overall business that go beyond a focus on short-term bottom-line

results

3. Measuring your strategy enables you to confirm or set aside the assumed causes

and effects you have based your strategy on. This is vital information. Your

strategy is based on what you believe influences the perspectives the most.

Keeping track of the right measures and communicating the success or failure to

achieve the target values of such measures help everyone focus on the issues that

matters most.

4. If this doesn't happen, then the assumption on which our strategy is based may be

wrong and we may have to rewrite our strategy. Getting this kind of information

to your desk fast may save you from total embarrassment. Confirm or disprove

your ability to achieve what you have planned to achieve. Had the desired effect

on your ability to deliver internal processes end objectives

1.4 OBJECTIVES OF THE STUDY

Balanced scorecard was the one the key control tool to manage the organization

effectively according to the strategy which is implemented. Objectives are diversified

into primary and secondary

PRIMARY OBJECTIVE

1. To improves the bottom line by reducing process cost and improving

productivity and mission effectiveness.

2. It helps in measurement of process efficiency provides a rational basis for

selecting what business process improvements to make first.

3. It allows managers to identify best practices in an organization and expand their

usage elsewhere.

4. The visibility provided by a measurement system supports better and faster

budget decisions and control of processes in the organization. This means it can

reduce risk.

5. Visibility provides accountability and incentives based on real data, not

anecdotes and subjective judgments. This serves for reinforcement and the

motivation that comes from competition.

SECONDARY OBJECTIVE

1. It permits benchmarking of process performance against outside

organizations.

2. It can raise you agency's Baldrige score, which can serve to increase its long-

term chances of survival.

1.5 SCOPE OF THE STUDY “BALANCED SCORECARD AS PERFORMANCE

MANAGEMENT TOOL”

1. The Balanced Scorecard enables organizations to bridge the gap between strategy

and actions, engage a broader range of users in organizational planning, reflect the

most important aspects of the business, and respond immediately to progress,

feedback and changing business conditions. The Balanced Scorecard can be a

great help used as a strategic tool, a management methodology or / and a

measurement system.

2. The Balanced Scorecard provides organizations with the ability to clarify vision

and strategy and translate them into action. By focusing on future potential

success it becomes a dynamic management system that is able to reinforce,

implement and drive corporate strategy forward.

3. The Balanced Scorecard is based on performance measurement and derives its

objectives from vision and strategy. It enables shared understanding of the links

between strategy, critical success factors and actions while establishing

accountability

4. The concept of the Balanced Scorecard has achieved increasing popularity in the

business world. Many businesses had previously built their objectives around

financial targets and goals of little relevance to a long-term strategic vision, thus

typically leaving a gap between strategy development and implementation.

5. The Balanced Scorecard is based on performance measurement and derives its

objectives from vision and strategy. It enables shared understanding of the links

between strategy, critical success factors and actions while establishing

accountability

6. The Balanced Scorecard focuses on creating and communicating a total

comprehensive picture to all members of the organization from the top down,

taking a long-term view of what the company's strategic objectives really are,

making good use of knowledge gained through experience and maintaining the

required flexibility of such a system to cope with the fast-changing business

environment.

1.6 STUDY METHOD

A qualitative study was chosen because metric to be analyzed was vast. The study

is focused on how Zenta’s internal metrics can be fitted to the balanced scorecard

concept.

1.7 DATA COLLECTION METHOD

Kaplan and Norton’s book “balanced scorecard” is taken as base and collected data for

this project

A “General Observation Study” was made to know about the measurement

method followed in the company.

Got help from my senior colleagues in the office to get some data’s about the

process

Internal metrics measured in Zenta is used for further analysis.

CHAPTER 2

LITERATURE REVIEW

2.1 INTRODUCTION TO BALANCED SCORECARD

HISTORY

Throughout the history of contemporary management theories starting from the

ones that were introduced between the intrusion of the mass production in the beginning

of the 20th century and until today, all the gurus of management have been trying to find

uniform solutions on more efficient allocation and use of very limited resources available

to businesses.

In the down of the century, Frederick W. Taylor established the very concepts of

resource allocation in his Principles of Scientific Management. In 1920 it went around

assembly line and motion studies as the first experience from systematic mass production

had given theorists quite a lot of materials to be analyzed from the point of view of using

traditional by blue-collar employees more efficiently. In the 1930, the main topic was

motivation of employees, as it turned out that human nature does not enable to work long

hours on a repetitive tasks without frustration level getting so high enough to diminish

productivity. In the 1940 and 1950, the first statistical and linear methods were

introduced in trying to measure logistics of the operations management and its

implications to overall company success in financial-analysis side.

In the beginning of 1980, partly because of introduction of electronic data

processing equipment and quick development of computers, the whole array of

management techniques were initiated. The particular reasons for the vast development of

the new theories were catalyzed mainly by ever growing competition generated through

more systematic use of computers, and of course also by rapid growth of the importance

of human capital.

During the industrial age, the financial control systems were developed in major

companies to facilitate and monitor efficient allocations of financial and physical capital.

A summary financial measure such as return-on-capital-employed (ROCE) could both

direct a company’s internal capital to its most productive use and monitor the efficiency

by which operating divisions used financial and physical capital to create value for

shareholders.

The emergence of the information era, however, in the last decades of the 20 th

century, has made obsolete many of the fundamental assumptions of the industrial age

competition. The information age environment for both manufacturing and service

organizations requires new capabilities for competitive success. The ability of any

company to mobilize and exploit its intangible assets has become far more decisive that

investing and managing tangible, physical assets.

Today automation and productivity have increased the number of people

performing analytic functions: engineering, marketing, management and administration.

Therefore, these people are more viewed as problem solvers, not as variable costs. In

other words, information age ahs brought about the concept of knowledge management.

The shift to successful knowledge management has introduced a variety of improvement

initiatives such as; JIT, TQM, Lean enterprise, Time-based competition, Customer-

focused organizations etc. Some of those programmers have meant in practice real

breakthrough and improvement, others have proven to be in the best case just a short-

time disturbance, but in the worst cases total failures resulting in disarray or even

bankruptcy of a particular company. The main reason for that lies in five main

implementation problems:

1. Current performance measurement systems are based on the traditional financial

accounting model, which does not enable to objectively analyze information-age

companies;

2. If some non-financial performance measurement even is made, it is solely based

on employees’ tactical performance, not on strategic performance,

3. Majority of management and employee salary-based motivation schemes are only

short-run profit oriented, that does not enable to align towards long-run profit

oriented, that does not enable to align towards long-run goals;

4. Overall company strategy is not closely linked to organizational and personal

improvement programmers; and

5. Strategy is not generally linked to resource allocation, which results in under

financing some of the crucial parts of organization’s development.

As for today, superior financial performance and efficiency in production are just not

enough to gain sufficient competitive advantage but more and more attention needs to be

paid to intangible sides of business.

2.2 KAPLAN AND NORTAN APPORACH OF BALANCED SCORECARD

The balanced scorecard is a strategic planning and management system that is

used extensively in business and industry, government, and nonprofit organizations

worldwide to align business activities to the vision and strategy of the organization,

improve internal and external communications, and monitor organization performance

against strategic goals. It was originated by Drs. Robert Kaplan (Harvard Business

School) and David Norton as a performance measurement framework that added strategic

non-financial performance measures to traditional financial metrics to give managers and

executives a more 'balanced' view of organizational performance. While the phrase

balanced scorecard was coined in the early 1990s, the roots of the this type of approach

are deep, and include the pioneering work of General Electric on performance

measurement reporting in the 1950’s and the work of French process engineers (who

created the Tableau de Bord – literally, a "dashboard" of performance measures) in the

early part of the 20th century.

The balanced scorecard has evolved from its early use as a simple performance

measurement framework to a full strategic planning and management system. The “new”

balanced scorecard transforms an organization’s strategic plan from an attractive but

passive document into the "marching orders" for the organization on a daily basis. It

provides a framework that not only provides performance measurements, but helps

planners identify what should be done and measured. It enables executives to truly

execute their strategies.

This new approach to strategic management was first detailed in a series of

articles and books by Drs. Kaplan and Norton. Recognizing some of the weaknesses and

vagueness of previous management approaches, the balanced scorecard approach

provides a clear prescription as to what companies should measure in order to 'balance'

the financial perspective. The balanced scorecard is a management system (not only a

measurement system) that enables organizations to clarify their vision and strategy and

translate them into action. It provides feedback around both the internal business

processes and external outcomes in order to continuously improve strategic performance

and results. When fully deployed, the balanced scorecard transforms strategic planning

from an academic exercise into the nerve center of an enterprise.

Kaplan and Norton's first book, The Balanced Scorecard, remains their most

popular. The book reflects the earliest incarnations of Balanced Scorecard - effectively

restating the concept as described in the second Harvard Business Review article. Their

second book, The Strategy Focused Organization, echoed work by others (particularly in

Scandinavia) on the value of visually documenting the links between measures by

proposing the "Strategic Linkage Model" or “strategy map”. Since then Balanced

Scorecard books have become more common - in early 2010 Amazon was listing several

hundred titles in English which had Balanced Scorecard in the title.

Kaplan and Norton describe the innovation of the balanced scorecard as follows:

"The balanced scorecard retains traditional financial measures. But financial measures

tell the story of past events, an adequate story for industrial age companies for which

investments in long-term capabilities and customer relationships were not critical for

success. These financial measures are inadequate, however, for guiding and evaluating

the journey that information age companies must make to create future value through

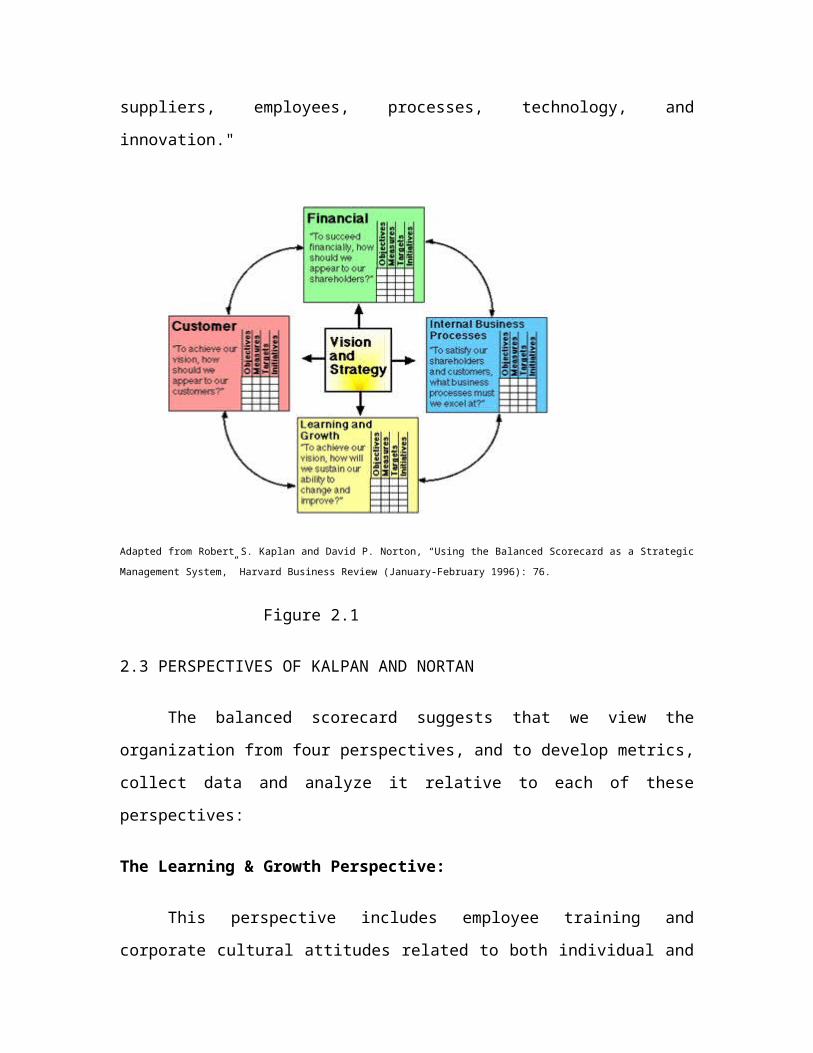

investment in customers, suppliers, employees, processes, technology, and innovation."

Adapted from Robert S. Kaplan and David P. Norton, “Using the Balanced Scorecard as a Strategic Management

System,” Harvard Business Review (January-February 1996): 76.

Figure 2.1

2.3 PERSPECTIVES OF KALPAN AND NORTAN

The balanced scorecard suggests that we view the organization from four

perspectives, and to develop metrics, collect data and analyze it relative to each of these

perspectives:

The Learning & Growth Perspective:

This perspective includes employee training and corporate cultural attitudes

related to both individual and corporate self-improvement. In a knowledge-worker

organization, people -- the only repository of knowledge -- are the main resource. In the

current climate of rapid technological change, it is becoming necessary for knowledge

workers to be in a continuous learning mode. Metrics can be put into place to guide

managers in focusing training funds where they can help the most. In any case, learning

and growth constitute the essential foundation for success of any knowledge-worker

organization.

Kaplan and Norton emphasize that 'learning' is more than 'training'; it also includes things

like mentors and tutors within the organization, as well as that ease of communication

among workers that allows them to readily get help on a problem when it is needed. It

also includes technological tools; what the Baldrige criteria call "high performance work

systems."

The Business Process Perspective:

This perspective refers to internal business processes. Metrics based on this

perspective allow the managers to know how well their business is running, and whether

its products and services conform to customer requirements (the mission). These metrics

have to be carefully designed by those who know these processes most intimately; with

our unique missions these are not something that can be developed by outside

consultants.

The Customer Perspective:

Recent management philosophy has shown an increasing realization of the

importance of customer focus and customer satisfaction in any business. These are

leading indicators: if customers are not satisfied, they will eventually find other suppliers

that will meet their needs. Poor performance from this perspective is thus a leading

indicator of future decline, even though the current financial picture may look good.

In developing metrics for satisfaction, customers should be analyzed in terms of kinds of

customers and the kinds of processes for which we are providing a product or service to

those customer groups.

The Financial Perspective:

Kaplan and Norton do not disregard the traditional need for financial data. Timely

and accurate funding data will always be a priority, and managers will do whatever

necessary to provide it. In fact, often there is more than enough handling and processing

of financial data. With the implementation of a corporate database, it is hoped that more

of the processing can be centralized and automated. But the point is that the current

emphasis on financials leads to the "unbalanced" situation with regard to other

perspectives. There is perhaps a need to include additional financial-related data, such as

risk assessment and cost-benefit data, in this category.

2.4 LINKING THE BALANCED SCORECARD MEARSURES TO STRATEGIC

METRIC

There are three principles which will enable the organization’s balanced scorecard to be

linked to its strategy

Cause and effect relationship

Performance drivers

Linkage to financials

CAUSE AND EFFECT RELATIONSHIP

A properly constructed scorecard should tell the story of the business unit’s

strategy through such a sequence of cause and effect relationships. The measurement

system should make the relationships (hypotheses) among objectives (and measures) in

the various perspectives explicit the sequence of hypotheses about the cause and effect

relationships between outcome measures and the performance drivers of those outcomes.

Every measure selected for a balanced scorecard should be an element of a chain of cause

and effect relationships that communications the meaning of the business unit’s strategy

to the organization

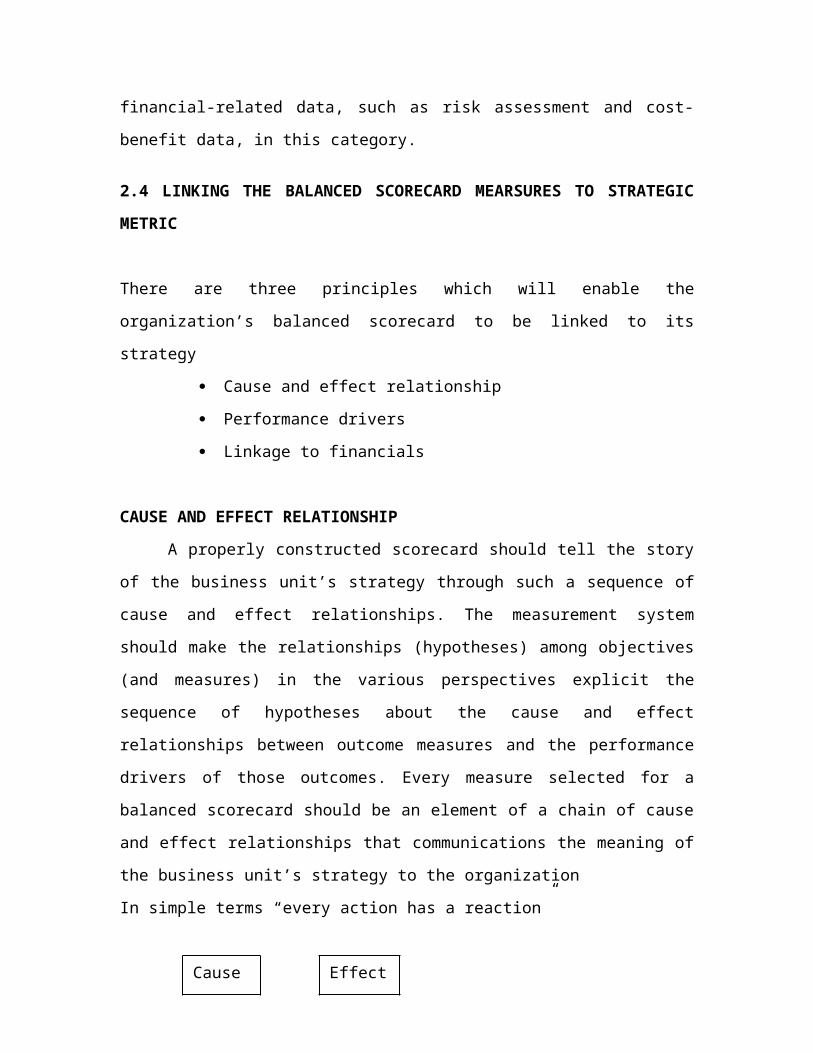

In simple terms “every action has a reaction”

Then

Cause and effect relationship for training

Figure 2.2

Cause Effect

Employee training(Cause)

Improvement in process (Effect)

PERFORMANCE DRIVERS AND OUTCOMES

All balanced scorecards use certain generic measures. These generic measures

tend to be core outcome measures, which reflect the common goals of many strategies as

well as similar structures across industries and companies. These generic outcome

measures tend to be lag indicators, such as profitability, market share, customer

satisfaction, customer retention, and employee skills. The performance drivers, the lead

indicators are the ones that tend to be unique for a particular business unit. The

performance driver reflect the uniqueness of the business unit strategy; for example, the

financial drivers of profitability, the market segments in which the unit chooses to

complete, and the particular internal processes and learning and growth objectives that

will deliver the value propositions to targeted customers and market segments.

A good balanced scorecard should have a mix of outcome measures and

performance drivers. Outcome measures without performance drivers do not

communicate how the outcomes are achieved. They also do not provide an earlier

indication about whether the strategy is being implemented successfully. Conversely, the

performance drivers – such as cycle time and part-per million defect rated – without

outcome measures enable the business unit to achieve short operational improvements,

but will fail to reveal whether the operational improvements have been translated into

expanded business with existing and new customers, and eventually, to enhance the

financial performance. A good balanced scorecard should have an appropriate mix of

outcome (lagging indicators) and performance drivers (leading indicators) that have been

customized to the business unit strategy.

LINKAGE TO FINANCIALS

With the proliferation of change programs under way in most organization today

it is easy to become preoccupied with such goals as quality, customer satisfaction,

innovation, and employee empowerment for their own sake. Will those goals can lead to

improved business unit performance, they may not if these goals are taken as ends in

themselves. The financial problems of some recent Baldrige award winners give

testimony to the need to link operational improvements to economical results.

A good balanced scorecard must retain a strong emphasis on outcomes, especially

financial ones like return–on–capital-employed or economic value added. Many

managers fail to link programs, quality management, cycle time reduction, reengineering,

and employee empowerment, to outcomes the directly influence customers and that

deliver future financial performance in such organizations the improvement programs

have incorrectly been taken as the ultimate objective they have not been linked to specific

targets and eventually financial performance. The inevitable result in that such

organization eventually become disillusioned about the lack of tangible payoffs from

their change programs. Ultimately, casual paths from all the measures on a scorecard

should be linked to financial objectives.

2.5 PERFORMANCE MANAGEMENT SYSTEM

Performance Management involves the entire gamut of processes in identifying critical

dimensions of performance - setting work plans against laid down objectives, reviewing

the work done against indicators of performance and developing and enhancing

competencies for improved performance.

An effective Performance Management System should be based on:-

Setting up KRAs for the Region/Theme/Unit/Department

Clarity of Individual Roles and Responsibilities

Laying down Plans and Performance Indicators for each position

Periodic assessment of performance of the individual against such Plans/

Performance Indicators

Identifying factors facilitating and hindering achievement of Plans - development

of action plans for overcoming hindering factors and strengthening facilitating

factors

Periodic review of role incumbents' behavior, which contributes to effective

functioning and working out action plans for developing such behavior.

Identification of role incumbents' developmental needs and preparing plans for

staff development through training and related activities.

Implementation and review.

2.6 DESIGNS OF BALANCED SCORECARD

Design of a Balanced Scorecard ultimately is about the identification of a small

number of financial and non-financial measures and attaching targets to them, so that

when they are reviewed it is possible to determine whether current performance 'meets

expectations'. The idea behind this is that by alerting managers to areas where

performance deviates from expectations, they can be encouraged to focus their attention

on these areas, and hopefully as a result trigger improved performance within the part of

the organization they lead.

The original thinking behind Balanced Scorecard was for it to be focused on

information relating to the implementation of a strategy, and perhaps unsurprisingly over

time there has been a blurring of the boundaries between conventional strategic planning

and control activities and those required to design a Balanced Scorecard. This is

illustrated well by the four steps required to design a Balanced Scorecard included in

Kaplan & Norton's writing on the subject in the late 1990s, where they assert four steps

as being part of the Balanced Scorecard design process:

1. Translating the vision into operational goals;

2. Communicating the vision and link it to individual performance;

3. Business planning; index setting

4. Feedback and learning, and adjusting the strategy accordingly.

These steps go far beyond the simple task of identifying a small number of financial

and non-financial measures, but illustrate the requirement for whatever design process is

used to fit within broader thinking about how the resulting Balanced Scorecard will

integrate with the wider business management process. This is also illustrated by books

and articles referring to balanced scorecards confusing the design process elements and

the balanced scorecard itself. In particular, it is common for people to refer to a “strategic

linkage model” or “strategy map” as being a balanced scorecard.

Although it helps focus managers' attention on strategic issues and the management

of the implementation of strategy, it is important to remember that the balanced scorecard

itself has no role in the formation of strategy. In fact, balanced scorecards can

comfortably co-exist with strategic planning systems and other tools.

2.6.1 Improved design Method of Kaplan and Norton

In the mid 1990s, an improved design method emerged. In the new method,

measures are selected based on a set of "strategic objectives" plotted on a "strategic

linkage model" or "strategy map". With this modified approach, the strategic objectives

are distributed across the four measurement perspectives, so as to "connect the dots" to

form a visual presentation of strategy and measures.

To develop a strategy map, managers select a few strategic objectives within each

of the perspectives, and then define the cause-effect chain among these objectives by

drawing links between them. A balanced scorecard of strategic performance measures is

then derived directly from the strategic objectives. This type of approach provides greater

contextual justification for the measures chosen, and is generally easier for managers to

work through. This style of Balanced Scorecard has been commonly used since 1996 or

so: it is significantly different in approach to the methods originally proposed, and so can

be thought of as representing the "2nd Generation" of design approach adopted for

Balanced Scorecard since its introduction.

Several design issues still remain with this enhanced approach to Balanced Scorecard

design, but it has been much more successful than the design approach it superseded.

In the late 1990s, the design approach had evolved yet again. One problem with

the "2nd generation" design approach described above was that the plotting of causal

links amongst twenty or so medium-term strategic goals was still a relatively abstract

activity. In practice it ignored the fact that opportunities to intervene, to influence

strategic goals are, and need to be anchored in the "now;" in current and real management

activity. Secondly, the need to "roll forward" and test the impact of these goals

necessitated the creation of an additional design instrument; the Vision or Destination

Statement. This device was a statement of what "strategic success," or the "strategic end-

state" looked like. It was quickly realized, that if a Destination Statement was created at

the beginning of the design process then it was much easier to select strategic Activity

and Outcome objectives to respond to it. Measures and targets could then be selected to

track the achievement of these objectives. Design methods that incorporate a "Destination

Statement" or equivalent (e.g. the Results Based Management method proposed by the

UN in 2002) represent a tangibly different design approach to those that went before, and

have been proposed as representing a "3rd Generation" design method for Balanced

Scorecard.

Design methods for Balanced Scorecard continue to evolve and adapt to reflect

the deficiencies in the currently used methods, and the particular needs of communities of

interest (e.g. NGO's and Government Departments have found the 3rd Generation

methods embedded in Results Based Management more useful than 1st or 2nd

Generation design methods).

2.7 KEY MEASURES OF BALANCED SCORECARD

The Balanced Scorecard is currently a very trendy (and often misunderstood)

topic in business circles, but there are other measurement frameworks such as the

Performance Prism, the Quantum Performance Management Model and the Tableau de

Bord. All are useful, but none of them is the answer to everything despite what their

advocates may say.

Combining elements of various measurement frameworks yields the measurement model

below. It works as follows:

1. The needs and expectations of customers and stakeholders are the primary drivers

of strategies. Stakeholders include shareholders and employees, but suppliers, the

community, government entities and other organizations could also be important

stakeholders.

2. Strategy consists of defining your intended customers and how you are going to

compete for them. A company’s strategy is made up of individual strategies,

which are the key actions a company must take to achieve its vision and goals.

When developing strategies, all other elements of the model must be considered.

3. Operations include all direct and support business activities that execute strategies

and produce products and services for customers and stakeholders.

4. The capabilities of a company’s organization and infrastructure enable its

operations to efficiently satisfy customer and stakeholder requirements.

Stakeholder capabilities may also be important to a company’s operations. In the

short-term, capabilities can limit what strategies are feasible; in the long-term they

may need to be developed to implement certain strategies.

5. Stakeholder contributions include products or services that are essential to

operations. For example, suppliers may provide critical technical support for

designing products.

6. Products and services provided to customers create financial returns for

shareholders and perhaps other stakeholders as well.

Measurement and business success

All of the listed variables can be measured to a useful degree of accuracy and

some companies are doing it. Companies that have won the Baldrige Award or similar

state award have extensive measurement systems that include all of the above measures.

In reviewing numerous Baldrige-based quality award applications, I have found that a

good estimate of a company’s final score can be made by just examining the measures

being used. Why? Because the depth, breadth and underlying logic of a company’s

measures reflect management’s understanding of the business and how well it is being

managed.

Not surprisingly, over a five-year period ending in 1998, the winners of Baldrige and

similar awards did two to three times better than comparable companies in terms of their

growth in sales and operating income. That is a huge difference!

Determining what to measure

So how can you determine what your company should measure? As mentioned

before, there are several frameworks that can be used. Although they all have merit, some

have advantages in terms of their state of development, ease of use, and direct

relationship to common business practices.

I believe the best approach for developing company or business unit strategy and

related measures is to use the Balanced Scorecard methodology in conjunction with the

robust perspectives of the Performance Prism. Balanced Scorecard performance systems

have an established record of success, but one needs a disciplined way of building and

implementing the system to ensure that business strategies get executed and that the

necessary organization culture change gets implemented. One framework that is

becoming an international "best practice" is the Balanced Scorecard Institute's Nine-Step

Methodology for developing strategic themes, business strategies, strategic goals,

strategy maps, performance measures, targets, and new initiatives. The result is a

strategic management system that is comprehensive, logically sound, and supported by

the whole organization.

This does not assure the strategies will work, but the measures will provide timely

feedback about how well they are working so timely corrective action can be taken

regarding the strategies or their execution. Without the measures, a company’s strategy

and finances could get substantially off-track before any problems are even recognized.

But having good strategies is not enough to be successful. Operational excellence

is also needed to execute them. To achieve and maintain high levels of productivity,

quality, and customer service, comprehensive operations or process measurement

systems are needed to manage processes, departments and work units. These systems

would include the measures that are strategically important, but those measures alone are

insufficient for effectively managing operations.

For developing operational measures, I recommend the approach and model given

in my book Operational Performance Measurement: Increasing Total Productivity. No

doubt I am biased, but the book’s process measurement model is the only one I’ve seen

that meets three critical criteria: it is logically sound, it readily relates to real world

processes, and it has a record of successful application. The model is also consistent with

TQM and Six Sigma methodologies that contain many specialized techniques for

measuring and managing processes.

Becoming familiar with the Baldrige Criteria for Performance Excellence is also

recommended. Since it outlines general management best practices, it provides a very

helpful perspective on what a well-managed company should be measuring, as well as

what it should be doing.

Cascading measures

Corporate level measures are very important, but they aren’t going to have much

impact unless they are cascaded all the way down to front-line employees. The case for

cascading is simple: Do you want 10% of your employees working toward company

objectives or 100%?

With some exceptions, such as market share, what you measure at the top is what

must be measured at all levels. However, the specific measures will change with every

function and organizational level because managers doing different jobs need different

information to make different decisions.

The same methodologies used to develop measures at the corporate level can be

used to cascade the measures down to front-line managers, supervisors, and employees.

However, as you go down the organization chart, the focus is on operations or processes.

Strategy is incorporated into operational measures by giving more weight to the measures

that are strategically important. This communicates strategy to all employees by

translating it into operational terms - a primary objective of the Balanced Scorecard.

Implementing performance measures

Determining what to measure can take considerable effort, but it will probably be

less than one-third of the total effort required to implement an efficient and effective

measurement system. Data collection and processing systems will have to be

implemented to produce the measures; everyone will have to be trained in using the

systems and measures; and as the measures are used, some problems are sure to be

identified that will require changes to the system.

Perhaps the greatest challenge faced when implementing performance

measurement systems is changing an organization’s culture. Using performance measures

requires managers and employees to change the way they think and act. For most people,

this is relatively easy, but for some, changing old beliefs and habits is very difficult.

Overcoming such problems requires strong leadership to provide appropriate

direction and support. The best measurement system in the world will yield few benefits

if the right knowledge, skills, abilities, and values are not developed in a company. An

organization doesn’t just interface with a measurement system; it is part of the system.

CHAPTER 3

3.1 RESEARCH METHODOLOGY

Research Methodology is the way in which the data are collected for the research

project.

TYPE OF RESEARCH:

In this study, the type of research is “Qualitative Research”

QUALITATIVE RESEARCH MEANS:

Qualitative research seeks out the ‘why’, not the ‘how’ of its topic through the

analysis of unstructured information – things like interview transcripts, open ended

survey responses, emails, notes, feedback forms, photos and videos. It doesn’t just rely on

statistics or numbers, which are the domain of quantitative researchers.

Qualitative research is used to gain insight into people's attitudes, behaviors, value

systems, concerns, motivations, aspirations, culture or lifestyles. It’s used to inform

business decisions, policy formation, communication and research. Focus groups, in-

depth interviews, content analysis, ethnography, evaluation and semiotics are among the

many formal approaches that are used, but qualitative research also involves the analysis

of any unstructured material, including customer feedback forms, reports or media clips.

Collecting and analyzing this unstructured information can be messy and time

consuming using manual methods. When faced with volumes of materials, finding

themes and extracting meaning can be a daunting task.

3.2 LIMITATIONS OF THE STUDY:

Lack of top management support

No access to confidential data

Complexity of the process

Time consuming process

CHAPTER 4

4.1 ZENTA BUSINESS MEASUREMENT SYSTEM

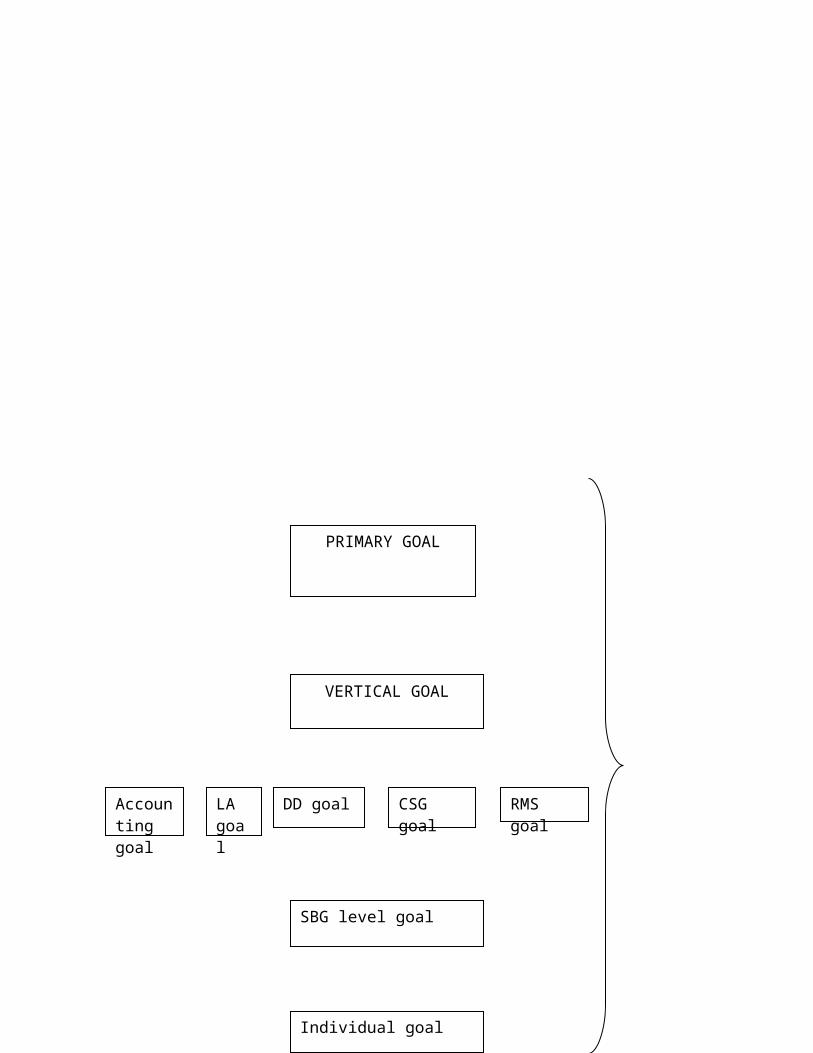

4.1.1 GOAL FLOW

In ZENTA all business process operates separately under different BG’s it is classified

according to the nature of business. In Zenta there are five business groups

Commercial Service group

Residential mortgage service

Due diligence

Financial service

Lease administration

All the business groups have separate goals but all the separate goals are linked with

corporate goal as shown the figure

Goal flow

Figure 3.1

Figure 4.1

Individual goal

PRIMARY GOAL

VERTICAL GOAL

SBG level goal

Accounting goal

DD goal CSG goal RMS goalLA goal

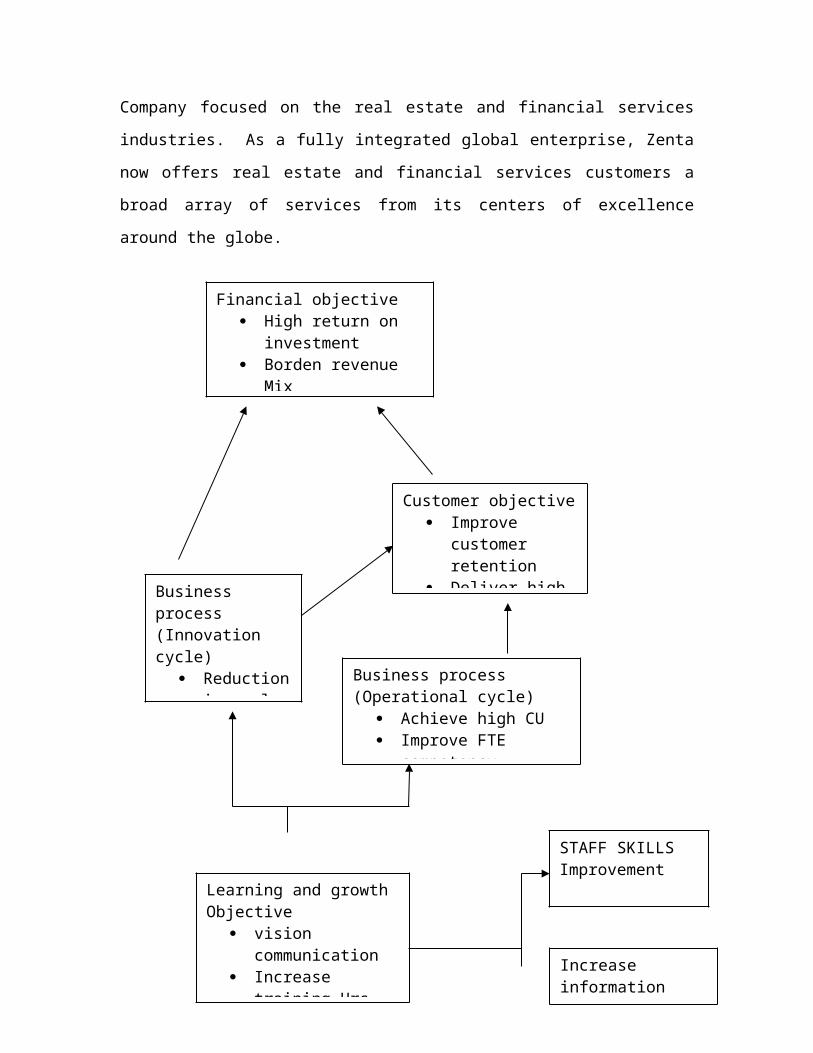

4.1.2 VISION AND MISSION BASED BALANCED SCORECARD

The May 2007 realignment of the Company’s services under the Zenta brand reflects the

new corporate vision of building a world-class Knowledge and Business Process

Outsourcing Company focused on the real estate and financial services industries. As a

fully integrated global enterprise, Zenta now offers real estate and financial services

customers a broad array of services from its centers of excellence around the globe.

Financial objective High return on

investment Borden revenue Mix

Customer objective Improve customer

retention Deliver high

quality serviceBusiness process(Innovation cycle)

Reduction in cycle time

Business process(Operational cycle)

Achieve high CU Improve FTE competency

Learning and growthObjective

vision communication Increase training Hrs

STAFF SKILLSImprovement

Figure 4.2

4.3 METRIC ANALYSIS IN ZENTA

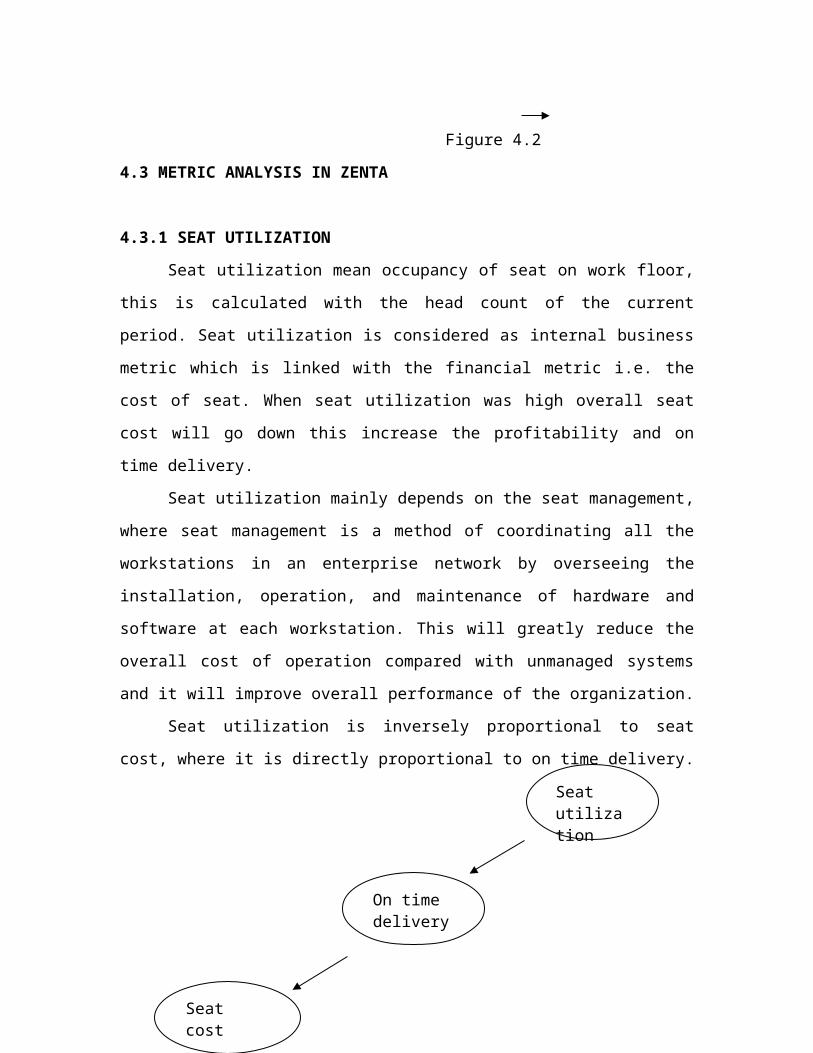

4.3.1 SEAT UTILIZATION

Seat utilization mean occupancy of seat on work floor, this is calculated with the

head count of the current period. Seat utilization is considered as internal business metric

which is linked with the financial metric i.e. the cost of seat. When seat utilization was

high overall seat cost will go down this increase the profitability and on time delivery.

Seat utilization mainly depends on the seat management, where seat management

is a method of coordinating all the workstations in an enterprise network by overseeing

the installation, operation, and maintenance of hardware and software at each

workstation. This will greatly reduce the overall cost of operation compared with

unmanaged systems and it will improve overall performance of the organization.

Seat utilization is inversely proportional to seat cost, where it is directly

proportional to on time delivery.

Internal business process

Customer perspective

Financial perspective

Increase information asset

Seat cost

On time delivery

Seat utilization

Figure 4.3

4.3.2 TRANSPORTATION COST

Transportation is simple metric but it will also impact in customer satisfaction and

retention. Transportation cost is considered as one of the key metric in financial

perspective of the company. Vehicle seat utilization is considered for knowing the total

number of employee using the company transport and how much the company paying for

it. Average travel time is calculated to identify to satisfaction level of the employee.

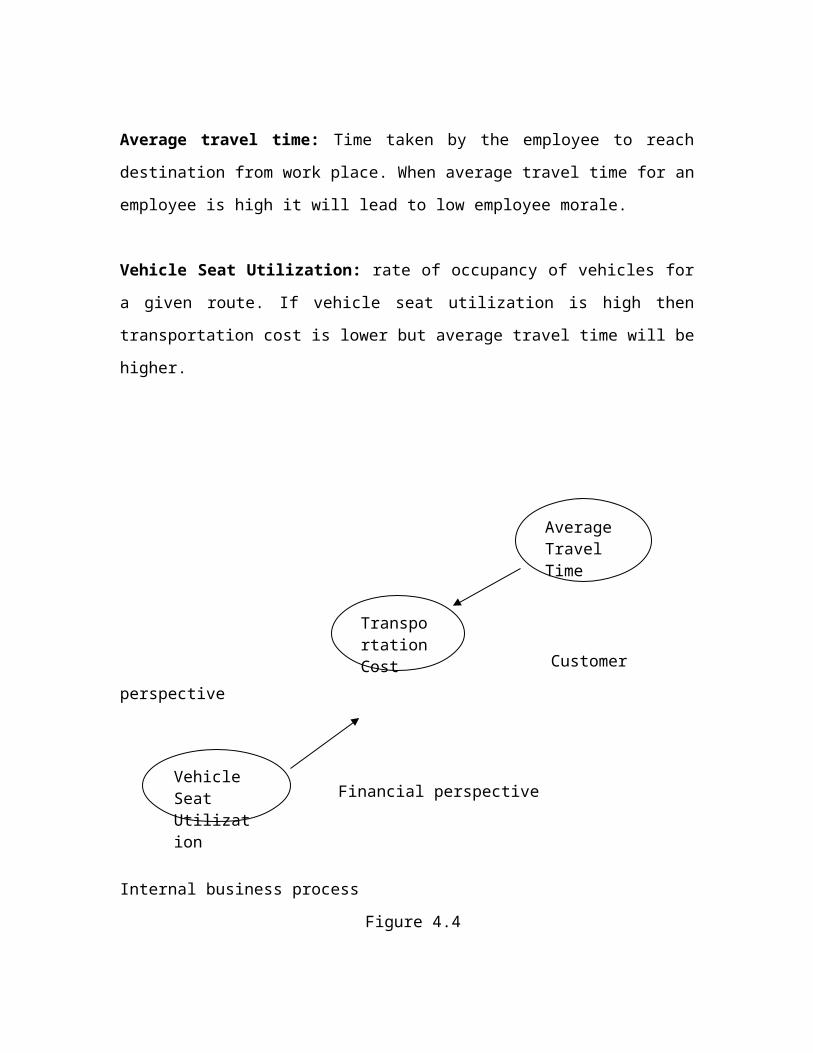

Average travel time: Time taken by the employee to reach destination from work place.

When average travel time for an employee is high it will lead to low employee morale.

Vehicle Seat Utilization: rate of occupancy of vehicles for a given route. If vehicle seat

utilization is high then transportation cost is lower but average travel time will be higher.

Customer perspective

Financial perspective

Internal business process

Figure 4.4

Vehicle Seat Utilization

Transportation Cost

Average Travel Time

4.3.3 EMPLOYEE SKILL EFFECTIVENESS

Employees are considered as important asset for any organization. Skill set for

any employee plays an important role in organizational development. All the employees

are trained according to the requirement of the respective business group. This training

makes the employee to be efficient in the work flow. Efficiency is considered as internal

business process metric when efficient employee is working in the process then there will

no deviation from turnaround time (TAT). With low skills of the FTE’s the process time

will be more and this will lead to increase in the TAT.

Learning and Growth

Internal business process

Customer perspective

Financial perspective

Skills per FTE (IT)

Efficiency of work

Deviation from TAT

RevenueGeneration

Figure 4.5

Skill per FTE (IT): the basic information technology skills which employees posses.

This will help in improving productivity or efficiency. The skill per FTE is increased

with help of training given by the organization.

Deviation from TAT: it refers to the increase in process time from the regular cycle

time. In order to meet desired TAT employees has to be trained as per requirement.

Revenue generation: Deviation from TAT is inversely proportional to revenue

generated. With the effective skills of employees the process time will get reduce, which

increases the workflow efficiency, which helps in revenue generation.

4.3.4 COMPETENCY PER FTE

Competence (or competency) is the ability of an individual to perform a job

properly. Some scholars see "competence" as a combination of knowledge, skills and

behavior used to improve performance; or as the state or quality of being adequately or

well qualified, having the ability to perform a specific role. Regardless of training,

competency would grow through experience and the extent of an individual to learn and

adapt.

Resource utilization: It is the process of utilizing the available resources with in the

organization effectively to increase efficiency of the work so that profitability of the

organization will be increased.

Profitability: It is a financial metrics that is used to assess a business's ability to

generate earnings as compared to its expenses and other relevant costs incurred during a

specific period of time. Profitability will be increased with increase in resource

utilization.

Learning and growth

Internal business process

Customer perspective

Financial perspective

Figure 4.6

4.3.5 CUSTOMER SATISFACTION

Customer satisfaction is a measure of how products and services supplied by a

company meet or surpass customer expectation. Customer satisfaction is defined as "the

number of customer or percentage of total customers, whose reported experience with a

firm, its products, or its services (ratings) exceeds specified satisfaction goals Customer

satisfaction provides a leading indicator of consumer purchase intentions and loyalty.

Customer satisfaction data are among the most frequently collected indicators of market

perceptions.

Profitability

Resource utilization

On time delivery

Competency per FTE

Remedial training : Specific remedial training for personnel may be required to

refresh and upgrade knowledge and skills related to their duties. A standard method of

implementing this training and evaluating the personnel involved should be established.

Zenta is following remedial training method to ensure efficiency in the process so that it

increases customer satisfaction.

Learning and Growth

Internal business process

Customer perspective

Financial perspective

Figure 4.7

Defective units

Cost of rework

Remedial training

CSAT

Cost of rework: Rework cost is the standard or actual cost that is spent on correcting

defective work. Rework cost is an unnecessary and additional cost for the organization,

which affects the overall operating cost.

4.3.6 ASSET UTILIZATION

Learning and growth Internal business process Customer perspective Financial

perspective

Figure 4.8

The term asset utilization means proper utilization of internal facilities to the greater

extent. Higher asset utilization increases the profitability and decreases the overall

expense incurred by the organization. All the internal facilities are more of IT related so

employees also should posses IT skills to use the facilities effectively. This will result in

increase in quality of service to the customer, which is the base line for any organization.

4.2 BALANCED SCORECARD ANALYSIS FOR ZENTA

The balanced scorecard framework for Zenta is formulated with the help of above

strategies given in the balanced scorecard approach figure. The final balanced scorecard

is shown in the table given below. This include two important strategies they are

Strategic objective

Strategic measurement

Strategic objective:

Asset utilization

IT skills per FTE

CSATBy quality of service Profitability

Strategic objective consist of four perspectives along with the metrics calculated

in Zenta this strategic objective is framed with help of vision and mission of the

company.

Financial perspective

In financial perspective balanced scorecard comprises of three important metric

which is considered in Zenta they are

Improve financial Returns

o Broaden Revenue Mix

o Reduce cost Structure

To achieve higher financial returns there should be more area for revenue generation

which also helps organization to grow. Reduce cost structure is productivity term to

control cost in organizational process high cost reduction will impact in quality of the

service provided to the customers this will the lagging indicator.

Customer perspective

In customer perspective table, increase in customer satisfaction through superior

execution is the strategic objective (These objectives are considered for Zenta). To

increase CSAT employee in the organization should be well trained how to handle the

customer. How to serve them but making proper relationship will be challenge so this

will be in lagging indicator. There should a proper execution of service this will result in

high customer retention so market share in the segment will go up this will the leading

indicator.

TABLE: 1 (BALANCED SCORECARD OF ZENTA)

Strategic ObjectiveStrategic Measurement

Lagging Indicators Leading Indicators

FINANCIAL PERSPECTIVE

Improve returns ROI

Broaden revenue Mix Revenue growth Revenue mix

Reduce cost Structure Quality reduction Process Improvement Through

Kaizen and Lean tool

CUSTOMER PESPECTIVE

Increase Customer Satisfaction

Through Superior Execution

CRM Share of the segment

INTERNAL BUSINESS

PROCESS

Understand Customer Segments Meeting Client Targets

High capacity utilization Business volume

Asset utilization No Tracking system

FTE competency Remedial training

Cycle time reduction Application Tracking Statistical Measure

Provide Rapid

Response(internal)

Application

Tracking(Track IT)

LEARNING AND GROWTH

Increase Employee Productivity Efficiency Drivers Application Support

Develop Strategic Skills Attrition Effective Work force

Access to Strategic Information Application

Restriction

Align Personal Goals Good Performance Appraisal

.

Internal business process

In Zenta I am considering six internal businesses metric to measure balanced

scorecard. The considered metric are

Understand Customer Segments

High Capacity Utilization

Asset Utilization

FTE Competency

Cycle Time Reduction

Provide Rapid Response

These metrics are considered is to cover all the business area in the company. Provide

rapid response is only for internal communication purpose, not with external customers.

Learning and Growth perspective

Learning and growth is one the key perspective which helps to improve the

bottom line of the company. To increase employee productivity training is important only

with training employee cannot become competent to make employee competent some

key metric are considered they are

Develop strategic skills

Access to strategic information

Align personal goals

Develop strategic skills

In order to make process improvement employee should be trained according to

the business requirement. When there is lack of training employee cannot perform their

job well so it leads to attrition. For effective performance in their job employee should be

well motivated and trained this will increase overall efficiency of the organization.

Access to strategic information

In Zenta all the process is application oriented and application controlled. All

employees cannot access all files they have a limit but some of the strategic information’s

are common to all. This kind of systematic procedure of allowing access to data will

motivate employee to achieve more in their work process.

Align personal goals

Each and every employee in the organization will be aligned with specific goals

as assigned by the business head. With the proper communication of goal employee can

work on it and achieve it.

STRATEGIC MEASUREMENT

Strategic measurement has to main parts which will access the all the metric of

strategic objective the two parts of strategic measurement are

Lagging Indicator

Leading Indicator

Lagging Indicator

In balanced scorecard outcomes are called lagging indicators. It will determine

what to be improved in the company so that company can earn more. Lagging indicators

are not measured as leading but measuring lagging indicator will help organization to

change it to leading indicator

Leading indicator

In balanced scorecard leading indicators are the performance drivers which makes

company profitable. The leading indicator makes company to act according to the

strengths this will help them to achieve more in the market place. In strategic

measurement leading indicator will tell the strength of the company which was shown in

table below.

4.4 ZENTA APPROACH ON BALANCED SCORECARD

The process of developing a balanced scorecard at Zenta is translated each of

these strategies into objectives and measures in the four perspectives. Particular emphasis

was placed on understanding and describing the cause and effect relationships on which

the strategy was based. A simplified version of the results of this effort is shown in the

figure (4.1).

REVENUE GROWTH STRATEGY PRODUCTIVITY STRATEGY

Financial perspective

Customer Perspective

Internal Perspective

Learning and Growth Perspective

Improve returns

Broaden Revenue Mix

Improve Operating Efficiency

Increase Customer Confidence in Our Financial Advice

Increase Customer Satisfaction Through Superior Execution

Understand Customer Segments

High capacity utilization

Asset utilization

FTE competency

Shift to Appropriate Channel

Cycle time reduction

Reduce compliance

Increase Employee Productivity

Develop Strategic Skills Access to

Strategic Information

Align Personal Goals

On the job training

For the revenue growth strategy, the financial perspective is to broaden the

revenue mix for the company. Strategically it is meant to increase the business process by

acquiring new clients and identifying new processes. In case of customer perspective,

increase customer confidence will be the key factor for the Zenta in customer retention.

Then the scorecard design focused on the internal business process perspective, Zenta has

three main objectives first is understanding customer segments, Zenta is an outsourcing

company understanding the customer needs and wants is important for better servicing.

All customers are not same so segmenting them according to there requirement and work

accordingly will increase their confidence. Second was to improve capacity utilization of

the company, CU is one of key metric measured in the company which helps to measure

the performance of the business group, there will a CU target which is to be achieved by

the all BG’s in the company but the target will be different according to the work flow of

the BG’s. High CU leads to higher revenue. Third will be the asset utilization this will

measure the resource utilization i.e. the internal facilities provided by the company to

their employees.

The next scorecard measure will be the productivity strategy, the financial

perspective is to improve the operating efficiency this achieved by implanting new

techniques which reduce the cost Zenta follows Kaizen tool as technique which helps to

reduce the production hours due to that cost is reduced. These both revenue growth

financial measure and productivity strategic financial measure will lead to more returns to

the company which helps to achieve the financial goal.

For customer perspective in productivity strategy is to improve the customer

satisfaction through superior execution this suggest that fulfilling customer wants and

needs with help of facilities available. In internal business process I am considering three

important productivity improvement strategies are measured they are

Improve Competency of FTE

Cycle time reduction this applicable for all business process

Compliance to organizational policies

CYCLE TIME REDUCTION:

Cycle Time Reduction is identifying and implementing more efficient ways to do

things. Reducing cycle time requires eliminating or reducing non-value-added activity,

which is defined as any activity that does not add value to the product. Examples of non-

value- added activity in which cycle time can be reduced or eliminated include repair due

to defects, machine set-up, inspection, test and schedule delays. Reducing cycle time will

have a significant impact on a company's bottom line when implemented.

COMPLIANCE:

Conformity to the organizational policies or requirements to meet the overall

objectives. A system or framework developed internally to implement the above either

manually or application which will help in controlling and monitoring of key metrics.

All this metrics in balanced scorecard will help organization to measure the

performance and effectiveness of the work flow process. These three strategies gives way

to next set of questions on this that is what kind competency to be improved? And how

cycle time reduction can be done? To answer this question there will proper training

program will be given. In this balanced scorecard there will be another perspective that is

learning and growth. This perspective is common base for both the revenue growth

strategy and productivity strategy. Learning and growth three important metric they are

first is develop strategic skills this is achieved with help of proper on the job training.

Second will be Access to strategic information should ensure that all employees can

access to the common goals, financial status of the company then new deal. This helps

them to improve the knowledge about the work flow. Third will be alignment of personal

goals. Each employee in the company should have a goal this goal should be

communicated to the individual through training and development team in the company.

All these strategies lead to increase in employee productivity. This employee productivity

helps in improvement above mentioned strategies that is revenue growth and

productivity.

4.5 ACHIVING STRATEGIC ALIGNMENT: FROM TOP TO BOTTOM

Implementation of balanced scorecard begins by educating people who is

involving in executing it. Some organizations hold their strategy to top management to

make it secret that is shared among the senior executive and control group. Implement

group is controlled and commanded by top management but this is only for centralized

management company. Now a day’s all the organization is customer driven so all are

included in implementing and all are allocated with different strategy that is to be

implemented.

when balanced scorecard is implemented in an organization their management

system will get varied it will follow Top to Bottom level of management system. And a

different management system will be followed that is communicating and linking which

is shown in the figure

Figure 4.10

There are three distinct mechanisms are used in this method they are

Clarifying and

Translating the

Vision and Strategy

Strategic feedback

and learning System

Planning and Target

Setting

Communicating

and LinkingBalanced

scorecard

1. Communication and education programs. A prerequisite for implementing

strategy is that all employees, senior corporate executives, and the board of

directors understand the strategy and the required behavior to achieve the strategic

objectives. A consistent and continuing program to educate the organization on

the components of the strategy, as well as reinforcing this education with

feedback on actual performance.

2. Goal-setting programs. Once a base level of understanding exists, individuals and

teams throughout the business unit must translate the higher level strategic

objectives into personal and team objectives. The traditional management by

objectives (MBO) programs used by most organizations should be linked to the

objectives and measures articulated in the balanced scorecard.

3. Reward linkage system. Alignment of the organization towards the strategy must

ultimately be motivated through the incentives and reward. In this system its

incorporated in strategy itself

Key Features of this management strategy-

Goal alignment exists from top to bottom

Education and open communication about strategy are basis for employee

empowerment

Compensation is linked to strategy.

For formulating a balanced scorecard that links a business unit’s mission and strategy to

explicit objectives and measures is only the start of using the scorecard as a management

system. the balanced scorecard must be communicated to all the employees including top

level to bottom level reason for communicating this to all employees is to align all

employees with the organization as well as individuals to whom the business unit is

accountable to the strategy. The knowledge and alignment among these constituents will

facilitate local goal setting, feedback, and accountability to the SBG’s strategic path.

Alignment and accountability will clearly be enhanced when individual

contribution to achieving scorecard objectives are linked to recognition, promotion and

compensation programs. Whether such linkage should be explicit, based on