IamSMEofIndia E circular- last date under black money act and balance sheet filing is nearing

Balance Sheet

This module provides an introduction to the balance

sheet, one of the essential financial statements in

accounting and includes an introduction to debits and

credits, and double entry accounting. We suggest doing

the Balance Sheet module prior to the Income Statement.

Author: Stu James

© 2014 Stu James and Management by the Numbers, Inc.

• The balance sheet is one of the essential financial

statements (reports) for a company and is a required filing

for all public companies.

• Understanding how to read and interpret a balance sheet

is an important skill for a business person or investor.

• The balance sheet provides important information about

the financial health of a company at a particular point in

time – a “snapshot”. This information includes:

• Assets (what the company owns)

• Liabilities (what the company owes)

• Shareholder’s Equity (what is left for

shareholders)

INT

RO

DU

CT

ION

TO

TH

E BA

LAN

CE S

HE

ET

2

Introduction to the Balance Sheet

MBTN | Management by the Numbers

SA

MP

LE BA

LAN

CE S

HE

ET

3

Sample Balance Sheet

MBTN | Management by the Numbers

Facebook, Inc. As of Sept 30, 2013

$Millions

Assets 14,933

Liabilities 1,885

Shareholder Equity 13,048

Here is a (very) simplified balance sheet for Facebook, Inc.

as of Sept 30, 2013. Facebook’s balance sheet consists of

three major categories. What else can we say?

First, note that

Assets = Liabilities +

Shareholder Equity

($14,933 = $1,885 + $13,048)

This must always be true!

Second, note that the figures

are as of Sept 30, 2013, a

particular moment in time.

We can also say that Facebook’s assets (what it owns) far outweighs its

liabilities (what it owes).

Now let’s look at these three parts of the balance sheet in more detail.

LE

GA

L RIG

HT

S

4

Legal Rights

MBTN | Management by the Numbers

Facebook, Inc. $Millions

Assets Property 14,933

Liabilities Primary Rights 1,885

Shareholder Equity Secondary Rights 13,048

Another way to look at this is a more formal legal definition

where we have property (assets) and two general classes of

property rights (liabilities and shareholder equity).

So we can also say that Facebook has $14,933 of property,

of which $1,885 is claimed through liabilities, and $13,048 is

left for shareholders. Legally, this is generally how it works.

AS

SE

TS

5

Assets

MBTN | Management by the Numbers

Facebook, Inc. Assets $Millions

Cash and Cash Equivalents 3,100

Short-Term Investments 6,228

Receivables 879

Inventory 0

Other Current Assets 342

Total Current Assets 10,549

Plant, Property and Equipment 2,685

Intangible Assets 1,609

Other Assets 90

Total Assets 14,933

Let’s look at Facebook’s assets in more detail:

First, note that assets are

divided into current assets

and non-current assets.

Examples of current assets

include cash, CDs,

marketable securities (stocks

and bonds), accounts

receivable (payments owed

to a company by customers),

inventory, and pre-paid

expenses (when a company

pays a bill in advance).

Definition: Current Assets are those assets which can reasonably be

expected to be converted into cash within one year.

AS

SE

TS

6

Assets

MBTN | Management by the Numbers

Facebook, Inc. Assets $Millions

Cash and Cash Equivalents 3,100

Short-Term Investments 6,228

Receivables 879

Inventory 0

Other Current Assets 342

Total Current Assets 10,549

Plant, Property and Equipment 2,685

Intangible Assets 1,609

Other Assets 90

Total Assets 14,933

Now let’s consider non-current assets:

Examples of non-current

assets include buildings,

vehicles, operating plants,

equipment, office furniture, and

intangible assets. Intangible

assets would include

intellectual property and

goodwill. Most long-term

assets are depreciated or

amortized over time.

Depreciation and amortization

represent how a long-term

asset gets used up over time.

Definition: Non-Current Assets are longer-term assets that are not

expected to be liquidated. These are depreciated or amortized over time.

LIA

BILIT

IES

7

Liabilities

MBTN | Management by the Numbers

Facebook, Inc. Liabilities $Millions

Accounts Payable 489

Short-Term Debt 459

Other Current Liabilities 36

Total Current Liabilities 984

Long Term Debt 287

Other Liabilities 614

Total Liabilities 1,885

Let’s look at Facebook’s liabilities in more detail:

Just like current assets, current

liabilities are those debts that

are expected to be paid during

the coming year. Examples of

current liabilities include

accounts payable (what a

company owes vendors for

products or services

purchased), taxes payable,

debt of less than one year or

debt coming due within a year

(bonds that mature in the

coming year).

Definition: Current Liabilities are those debts which are expected to

be paid within the coming year.

LIA

BILIT

IES

8

Liabilities

MBTN | Management by the Numbers

Facebook, Inc. Liabilities $Millions

Accounts Payable 489

Short-Term Debt 459

Other Current Liabilities 36

Total Current Liabilities 984

Long Term Debt 287

Other Liabilities 614

Total Liabilities 1,885

Now let’s consider Facebook’s long-term liabilities:

Long-term liabilities include

items such as long-term bonds

with a maturity date over a

year, real estate loans, and

other long-term bank loans.

Definition: Long-Term Liabilities are those debts which are expected

to be repaid more than a year in the future.

SH

AR

EH

OLD

ER

EQ

UIT

Y

9

Shareholder Equity

MBTN | Management by the Numbers

Facebook Shareholder Equity $Millions

Retained Earnings 2,636

Capital Surplus 10,399

Other Shareholder Equity 13

Total Shareholder Equity 13,048

Now let’s look at Facebook’s Shareholder Equity:

Shareholder equity includes

retained earnings (from the

Income Statement), Capital

Surplus (any initial or

subsequent investment in the

company by shareholders

beyond the par value of the

stock). In addition, the par

value of any preferred or

common stock would be listed

here separately.

Definition: Shareholder Equity accounts are the residual accounts –

what would be left for the shareholders after all liabilities are paid.

Insight Equity accounts represent the

(residual) value of the company (or,

assets minus liabilities)

TR

AN

SA

CT

ION

S

10

Transactions

MBTN | Management by the Numbers

An accounting transaction is an event that must be recorded

in a company’s accounting system that impacts the balance

sheet and/or income statement. These are also call journal

entries. Let’s look at a few simple transactions that impact

the balance sheet so you can better understand how the

balance sheet works in practice.

Consider the following transaction events:

• Receiving a 30 day loan as a $1,000 cash deposit from a bank

• Obtaining $5,000 from an investor

• Buying $3,000 of inventory with cash

• Paying a $3,000 bill owed to vendor

• Receiving a $500 wire payment from an international customer

How do these transactions impact the balance sheet?

TR

AN

SA

CT

ION

S

11

Transactions

MBTN | Management by the Numbers

Receiving a $1,000 loan will impact two areas as shown below. It will

increase your cash balance by $1,000 and increase your short-term

liabilities by $1,000 (maintains assets = liabilities + shareholder eq.).

Assets Liabilities Shareholder Equity

Cash S-T Liabilities

+$1000 = +$1000 + $0

Obtaining $5000 from an investor will also increase your cash

balance. But instead of a liability, the offsetting entry is capital surplus

under equity (maintains assets = liabilities + shareholder equity).

Assets Liabilities Shareholder Equity

Cash Capital Surplus

+$5000 = +$0 + $5000

TR

AN

SA

CT

ION

S

12

Transactions

MBTN | Management by the Numbers

Buying $3,000 of inventory with cash only impacts the asset side of

the balance sheet as shown, but the net effect maintains the equation.

Assets Liabilities Shareholder Equity

Inventory

+$3000 = +$0 +$0

Cash

-$3000 = +$0 +$0

$3000 -$3000 = +$0 +$0

What if the inventory is purchased on credit with the vendor, instead?

Assets Liabilities Shareholder Equity

Inventory Accounts Payable

$3000 = +$3000 +$0

TR

AN

SA

CT

ION

S

13

Transactions

MBTN | Management by the Numbers

When the vendor sends an invoice for the inventory and it is paid with

cash, cash will decrease and so will accounts payable.

Assets Liabilities Shareholder Equity

Cash Accounts Payable

-$3000 = -$3000 +$0

Note that the net on the accounts payable account is zero for the last

two transactions. Paying on credit, instead of using cash, basically

creates a temporary condition of a short-term liability, called accounts

payable (A/P).

Take a moment to recognize that the net impact of a cash purchase of

inventory is the same as a purchase on credit after paying the vendor.

The accounting system just records the fact that the company owes

the vendor a payment for the inventory, which is reflected in liabilities.

TR

AN

SA

CT

ION

S

14

Transactions

MBTN | Management by the Numbers

Receiving a $500 wire payment from a customer is kind of the flip side

of paying a vendor for inventory already received. Here, a customer

owes you money (recorded in accounts receivable), and pays it,

removing the expected, but not yet received, payment owed by the

customer.

Assets Liabilities Shareholder Equity

Cash

+$500 = +$0 +$0

Accounts Receivable

-$500 = +$0 +$0

+$500 - $500 = +$0 +$0

Just like the purchase of inventory earlier, this transaction only impacts

the balances on the asset side of the balance sheet.

DE

BIT

S AN

D C

RE

DIT

S

15

Debits and Credits

MBTN | Management by the Numbers

This module provides basic understanding of how balances

change with transactions. We’d be remiss if we didn’t mention

one additional dimension to transactions – credits and debits.

Every accounting transaction consists of one or more credits and

offsetting debits such that the balance sheet equation is

maintained (assets = liabilities + shareholder equity). You can

have debits and credits in each major category of the balance

sheet. What matters is that credits = debits and that change in

assets = change in liabilities + shareholder equity!

Definition:

For every transaction,

Credits = Debits

Assets = Liabilities + Shareholder Equity - and -

Net Change in Assets = Net Change in (Liabilities + Shareholder Equity)

DE

BIT

S AN

D C

RE

DIT

S

16

Debits and Credits

MBTN | Management by the Numbers

Account Category Debit / Credit Increase / Decrease

Asset Debit Increase

Asset Credit Decrease

Liability Debit Decrease

Liability Credit Increase

Equity Debit Decrease

Equity Credit Increase

The table below is a summary that you can use to determine if a

transaction is a debit or a credit, or whether it will increase or

decrease the balance of the account category.

So, rather than putting in a negative number to decrease an asset

account, we credit it. Rather than putting in a negative number to

decrease a liability account, we debit it.

DE

BIT

S AN

D C

RE

DIT

S

17

Debits and Credits

MBTN | Management by the Numbers

The system of using debits and credits, or double entry

bookkeeping, originated in Venice over 500 years ago. The

system is still in use today, though obviously modernized through

the use of computers. Computers have vastly improved on the

manual approach of “T” tables, but the approach is still the

backbone of the system.

Insight While the computer ensures that values balance, the data entered must be accurate and the right accounts must be chosen or the balance sheet will not be an accurate portrayal of the company’s position.

Assets Liabilities Shareholder Equity

Cash S-T Liabilities

Debits Credits Debits Credits Debits Credits

$1000 $1000

“T” Table

DE

BIT

S AN

D C

RE

DIT

S

18

Debits and Credits

MBTN | Management by the Numbers

Now let’s try our examples again, but using the full system of

debits and credits, as well as showing the impact on the account.

• Receiving a 30 day loan as a $1000 cash deposit from a bank

• Obtaining $5000 from an investor

• Buying $3000 of inventory with cash

• Paying a $3000 bill owed to vendor

• Receiving a $500 wire from an international customer

Here is the entry for the first transaction. Now try the others:

Assets Liabilities Shareholder Equity

Cash S-T Liabilities

Debits Credits Debits Credits Debits Credits

$1000 $1000

Increase Increase No change

DE

BIT

S AN

D C

RE

DIT

S

19

Debits and Credits

MBTN | Management by the Numbers

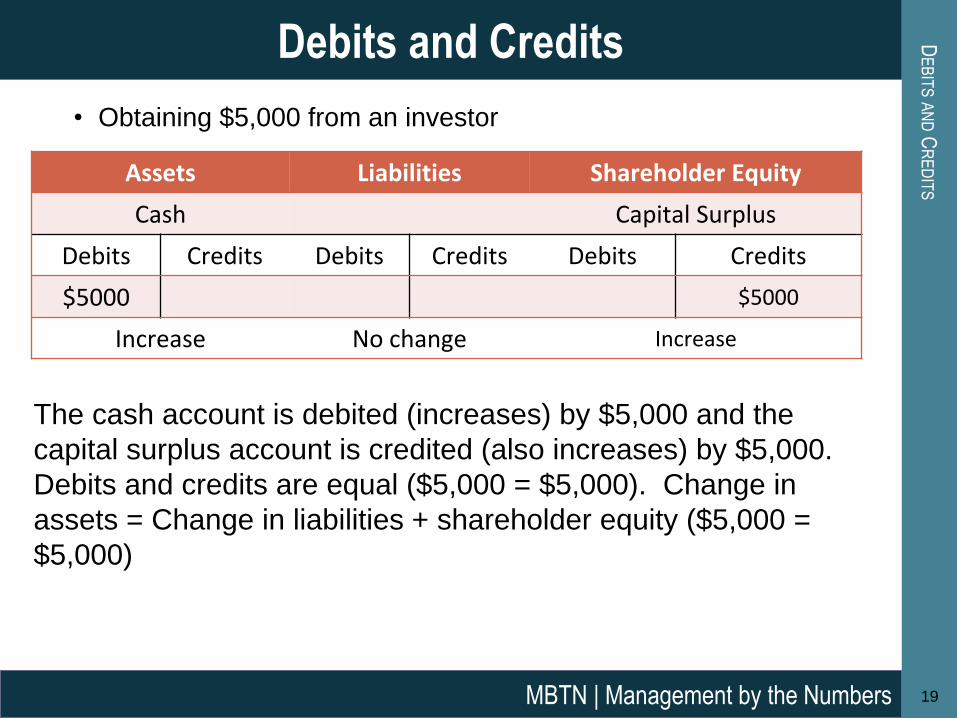

• Obtaining $5,000 from an investor

Assets Liabilities Shareholder Equity

Cash Capital Surplus

Debits Credits Debits Credits Debits Credits

$5000 $5000

Increase No change Increase

The cash account is debited (increases) by $5,000 and the

capital surplus account is credited (also increases) by $5,000.

Debits and credits are equal ($5,000 = $5,000). Change in

assets = Change in liabilities + shareholder equity ($5,000 =

$5,000)

DE

BIT

S AN

D C

RE

DIT

S

20

Debits and Credits

MBTN | Management by the Numbers

• Buying $3,000 of inventory with cash

Assets Liabilities Shareholder Equity

Cash

Debits Credits Debits Credits Debits Credits

$3000

Inventory

Debits Credits Debits Credits Debits Credits

$3000

Cash decreases (credit) and Inventory increases

(debit), but no net change in assets.

No change No change

DE

BIT

S AN

D C

RE

DIT

S

21

Debits and Credits

MBTN | Management by the Numbers

• If instead, the inventory had been purchased on credit (terms)…

Assets Liabilities Shareholder Equity

Inventory Accounts Payable

Debits Credits Debits Credits Debits Credits

$3000 $3000

Increase Increase No Change

• Later, paying the $3,000 bill owed to that same vendor

Assets Liabilities Shareholder Equity

Cash Accounts Payable

Debits Credits Debits Credits Debits Credits

$3000 $3000

Decrease Decrease No Change

DE

BIT

S AN

D C

RE

DIT

S

22

Debits and Credits

MBTN | Management by the Numbers

• Receiving a $500 wire payment from an international customer

Assets Liabilities Shareholder Equity

Cash

Debits Credits Debits Credits Debits Credits

$500

Accounts Receivable

Debits Credits Debits Credits Debits Credits

$500

Cash increases (debit) and Accounts Payable decreases (credit), but

no net change in assets.

No change No change

BU

ILDIN

G A B

ALA

NC

E SH

EE

T

23

Building a Balance Sheet

MBTN | Management by the Numbers

The last example we’ll use is to create a balance sheet from

scratch for a start-up coffee shop. While this is obviously a

very simplified exercise, it will help you understand how the

transactions build together to create the balance sheet.

On the next page, there are 7 transactions that you can use to

test your comprehension. Try to build it yourself before

checking the answer key. We’ve also provided the detail on all

the individual transactions so you can follow how the accounts

were updated.

BU

ILDIN

G A B

ALA

NC

E SH

EE

T

24

Building a Balance Sheet

MBTN | Management by the Numbers

Create a balance sheet from the following transactions:

• An investor starts the company with $25,000 of cash.

• The manager obtains a $15,000 long-term loan from a local

bank.

• The manager purchases an espresso maker for $1,500 on

credit.

• The manager purchases a computer for $1,000 for cash.

• The manager purchases $2,500 of goods to resell (inventory)

using cash.

• The manager signs a 3 year contract to rent a building space

that requires a $1,000 deposit and first month’s pre-paid rent of

$1,000.

• The manager writes the check for the deposit and rent.

Ready, set, go – don’t advance until you’ve tried it!

BU

ILDIN

G A B

ALA

NC

E SH

EE

T

25

Building a Balance Sheet

MBTN | Management by the Numbers

Assets $

Cash $34,500

Inventory $2,500

Pre-Paid Rent $1,000

Current Assets $38,000

Equipment $2,500

Deposit $1,000

Total Assets $41,500

Liabilities $

Accounts Payable $1,500

Current Liabilities $1,500

L-T Liabilities $15,000

Total Liabilities $16,500

Shareholder Equity $

Capital Surplus $25,000

Total SH Equity $25,000

Total Liab. + Equity $41,500

Though very simple (and only including transactions that

impact the balance sheet alone), this exercise provides a good

sense of how the balance sheet changes over time. The detail

of the transactions and T accounts are shown on the following

pages for reference.

BU

ILDIN

G A B

ALA

NC

E SH

EE

T

26

Building a Balance Sheet

MBTN | Management by the Numbers

Assets Liabilities Shareholder Equity

Cash Capital Surplus

Debits Credits Debits Credits Debits Credits

$25,000 $25,000

Increase No change Increase

Assets Liabilities Shareholder Equity

Cash Long-Term Liab.

Debits Credits Debits Credits Debits Credits

$15,000 $15,000

Increase Increase No Change

Assets Liabilities Shareholder Equity

Equipment (or PPE) Accounts Payable

Debits Credits Debits Credits Debits Credits

$1,500 $1,500

Increase Increase No Change

BU

ILDIN

G A B

ALA

NC

E SH

EE

T

27

Building a Balance Sheet

MBTN | Management by the Numbers

Assets Liabilities Shareholder Equity

Cash

Debits Credits Debits Credits Debits Credits

$1,000

Equipment

Debits Credits Debits Credits Debits Credits

$1,000

No net change in Assets No change No change

Assets Liabilities Shareholder Equity

Cash

Debits Credits Debits Credits Debits Credits

$2,500

Inventory

Debits Credits Debits Credits Debits Credits

$2,500

No net change in Assets No change No change

BU

ILDIN

G A B

ALA

NC

E SH

EE

T

28

Building a Balance Sheet

MBTN | Management by the Numbers

Assets Liabilities Shareholder Equity

Cash

Debits Credits Debits Credits Debits Credits

$2,000

Prepaid Rent

Debits Credits Debits Credits Debits Credits

$1,000

Deposits

Debits Credits Debits Credits Debits Credits

$1,000

No net change in Assets No change No change

Signing the contract generally does not create an accounting

transaction, only when the deposit and pre-paid rent is actually

paid.

MBTN Income Statement Module. This MBTN module

provides a similar introduction to the income statement.

FIN

AN

CIA

L ST

AT

EM

EN

TS– F

UR

TH

ER

RE

FE

RE

NC

E

29

Financial Statements - Further Reference

MBTN | Management by the Numbers