Baker & McKenzie Consulting LLC is a subsidiary of Baker & McKenzie LLP, a member firm of Baker &...

31

Baker & McKenzie Consulting LLC is a subsidiary of Baker & McKenzie LLP, a member firm of Baker & McKenzie International, a Swiss Verein of member law firms around the world. In accordance with the common terminology used in professional service organizations, reference to a "partner" means a person who is a partner, or equivalent, in such a law firm. Similarly, reference to an "office" means an office of any such law firm. © 2013 Baker & McKenzie Consulting LLC It’s Worth the Effort: Targeting Awards to Ease Compliance Burdens and Maximize Plan Effectiveness Valerie Diamond -- Partner, Baker & McKenzie LLP June Anne Burke – Partner, Baker & McKenzie LLP CT/Boston NASPP Regional Meeting July 19, 2013

-

Upload

natalie-may -

Category

Documents

-

view

222 -

download

0

Transcript of Baker & McKenzie Consulting LLC is a subsidiary of Baker & McKenzie LLP, a member firm of Baker &...

Baker & McKenzie Consulting LLC is a subsidiary of Baker & McKenzie LLP, a member firm of Baker & McKenzie International, a Swiss Verein of member law firms around the world. In accordance with the common terminology used in professional service organizations, reference to a "partner" means a person who is a partner, or equivalent, in such a law firm. Similarly, reference to an "office" means an office of any such law firm.© 2013 Baker & McKenzie Consulting LLC

It’s Worth the Effort: Targeting Awards to Ease Compliance Burdens and Maximize Plan Effectiveness

Valerie Diamond -- Partner, Baker & McKenzie LLPJune Anne Burke – Partner, Baker & McKenzie LLP

CT/Boston NASPP Regional Meeting

July 19, 2013

© 2013 Baker & McKenzie Consulting LLC

Agenda

• Assessing the Compliance Burden• Award Structuring by Country

• Type of Awards• Tax-Qualified Programs

• Recharge Arrangements• Other Tax Saving Ideas• Other Compliance Considerations• Questions

2

© 2013 Baker & McKenzie Consulting LLC

Cost/Benefit Compliance Assessment

Assess by award and by country– Regulatory issues

Securities Offerings – generally territorial in nature / based on size of offering & headcounts Prospectus filings/registration statements (e.g., EU, Japan) Securities notices/reports (e.g., Malaysia, Thailand) Exemption confirmations (e.g., Australia, Philippines) Show-stoppers (e.g., Indonesia, Colombia)

Exchange Control Filings - for movement or holdings of foreign securities / funds Exchange control approvals (e.g., China, Vietnam) Notices (e.g., Italy) Show-stoppers (e.g., Ukraine)

Other filings (e.g., Singapore MoM approval)

© 2013 Baker & McKenzie Consulting LLC

Cost/Benefit Compliance Assessment (cont’d)

– Employer tax issues Tax withholding/reporting Employer social tax Favorable tax treatment (i.e., avoiding / minimizing social tax vs.

cost/burden to implement/maintain) Reimbursement/charge-back arrangements

– Employee taxation Timing of tax / deferral of income Social tax withholding Favorable tax treatment (and cost/burden to implement/maintain)

– Other issues (e.g., Danish Stock Option Act)

© 2013 Baker & McKenzie Consulting LLC

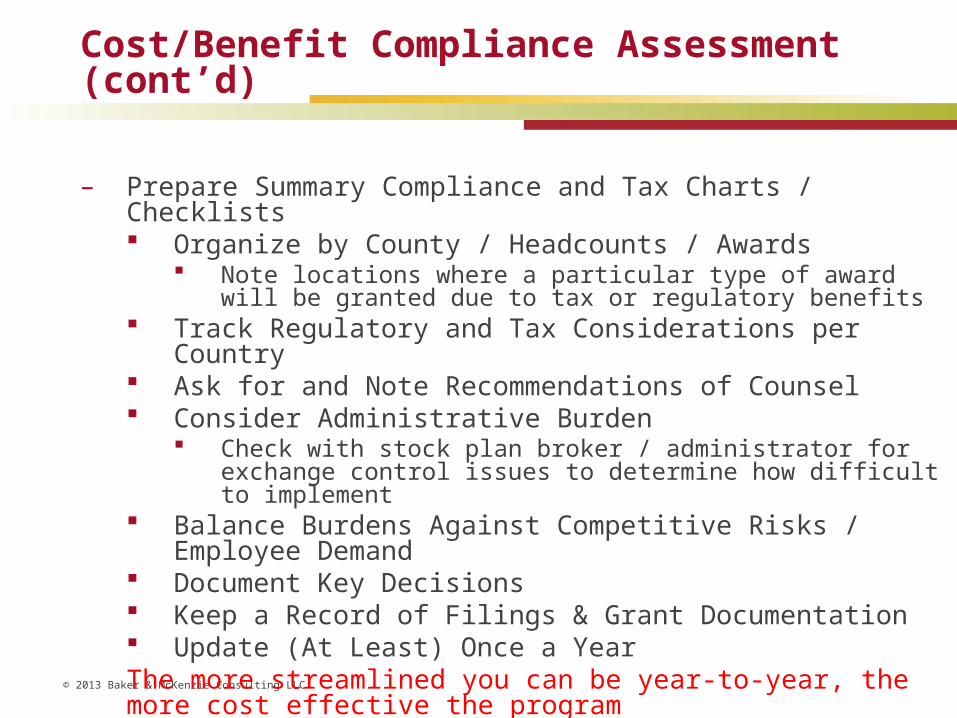

Cost/Benefit Compliance Assessment (cont’d)

– Prepare Summary Compliance and Tax Charts / Checklists Organize by County / Headcounts / Awards

Note locations where a particular type of award will be granted due to tax or regulatory benefits

Track Regulatory and Tax Considerations per Country Ask for and Note Recommendations of Counsel Consider Administrative Burden

Check with stock plan broker / administrator for exchange control issues to determine how difficult to implement

Balance Burdens Against Competitive Risks / Employee Demand Document Key Decisions Keep a Record of Filings & Grant Documentation Update (At Least) Once a YearThe more streamlined you can be year-to-year, the more cost effective the program

© 2013 Baker & McKenzie Consulting LLC

Award Structuring by Country

• Being Open to Grants of Different Kinds in a Country Can Save the Company (or the Employee) Money• Options vs. RSUs vs. RS vs. ESPP• Qualified vs. Non-Qualified

• Many Companies Feel One Size Should Fit All – Not willing to consider award variations

Watch for Hidden Costs of Managing Different Awards with Broker / Administrator, Duplicate Systems, etc.

© 2013 Baker & McKenzie Consulting LLC

Award Structuring by Country

• Canada: consider granting stock options rather than other forms of award– 50% tax exemption on spread at exercise– Primarily employee benefit, except for tax-equalized

expats• Brazil: consider granting stock options rather than other

forms of award (where no recharge)̶H Stock options taxed at sale of shares̶H Taxed as capital gains rather than salary income (15%

vs. 27.5%)̶H No withholding or reporting obligation for employer

© 2013 Baker & McKenzie Consulting LLC

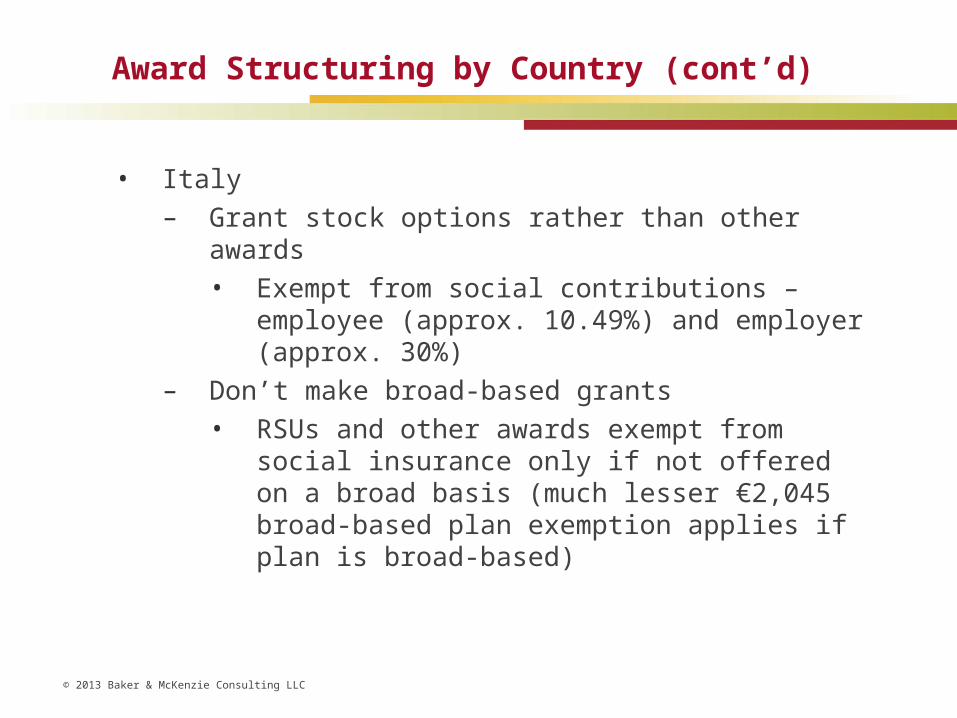

Award Structuring by Country (cont’d)

• Italy– Grant stock options rather than other awards

• Exempt from social contributions – employee (approx. 10.49%) and employer (approx. 30%)

– Don’t make broad-based grants• RSUs and other awards exempt from social

insurance only if not offered on a broad basis (much lesser €2,045 broad-based plan exemption applies if plan is broad-based)

© 2013 Baker & McKenzie Consulting LLC

Award Structuring by Country (cont’d)

• Generally avoid cash-settled awards– Often subject to social contributions that don’t apply to

equity awards, e.g., Brazil, Colombia, Japan, Malaysia, New Zealand, Portugal

– Special tax regimes available for equity often do not apply, e.g., French-qualified RSUs, Israeli trustee plans

– However, cash awards may allow for a local deduction not otherwise available, e.g., Canada, Netherlands

– Note that cash awards are subject to liability accounting treatment – additional burden/volatility

© 2013 Baker & McKenzie Consulting LLC

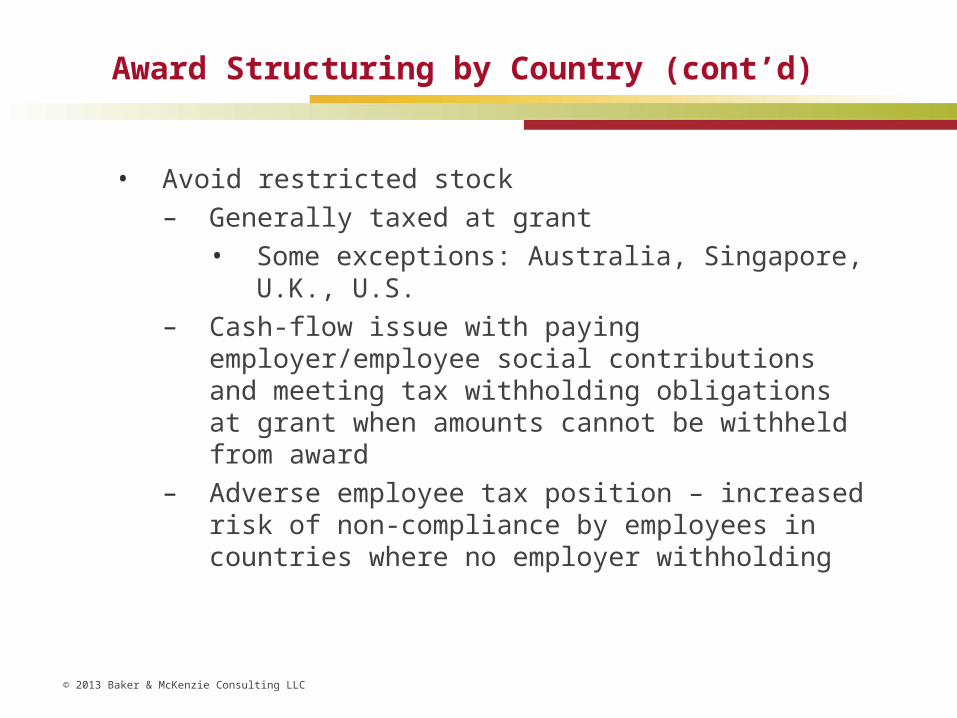

Award Structuring by Country (cont’d)

• Avoid restricted stock – Generally taxed at grant

• Some exceptions: Australia, Singapore, U.K., U.S.– Cash-flow issue with paying employer/employee social

contributions and meeting tax withholding obligations at grant when amounts cannot be withheld from award

– Adverse employee tax position – increased risk of non-compliance by employees in countries where no employer withholding

© 2013 Baker & McKenzie Consulting LLC

Tax-Qualified Plans

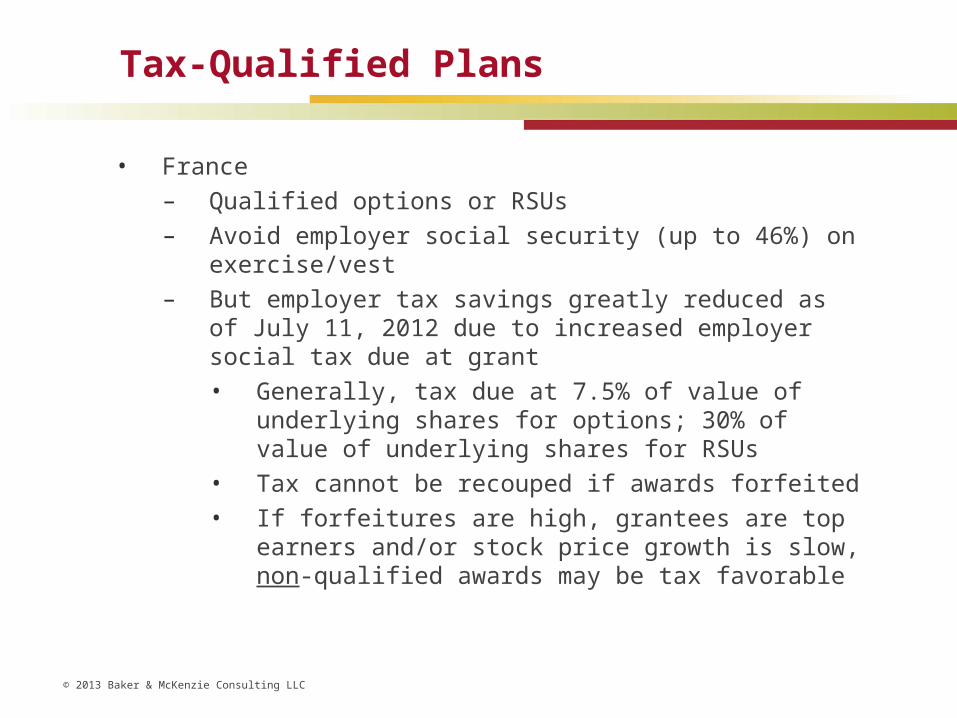

• France

– Qualified options or RSUs

– Avoid employer social security (up to 46%) on exercise/vest

– But employer tax savings greatly reduced as of July 11, 2012 due to increased employer social tax due at grant

• Generally, tax due at 7.5% of value of underlying shares for options; 30% of value of underlying shares for RSUs

• Tax cannot be recouped if awards forfeited

• If forfeitures are high, grantees are top earners and/or stock price growth is slow, non-qualified awards may be tax favorable

© 2013 Baker & McKenzie Consulting LLC

Tax-Qualified Plans (cont’d)

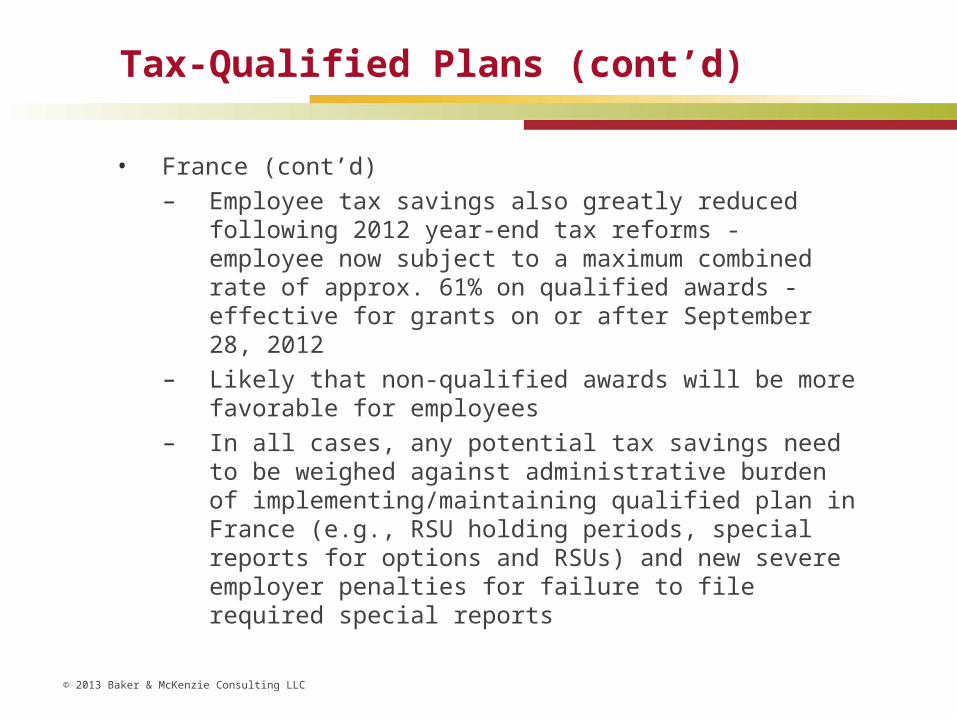

• France (cont’d)

– Employee tax savings also greatly reduced following 2012 year-end tax reforms - employee now subject to a maximum combined rate of approx. 61% on qualified awards - effective for grants on or after September 28, 2012

– Likely that non-qualified awards will be more favorable for employees

– In all cases, any potential tax savings need to be weighed against administrative burden of implementing/maintaining qualified plan in France (e.g., RSU holding periods, special reports for options and RSUs) and new severe employer penalties for failure to file required special reports

© 2013 Baker & McKenzie Consulting LLC

Tax-Qualified Plans (cont’d)

• Israel– Trustee plan options, RSUs or ESPP– Can avoid or reduce employer social security (5.9%,

capped at approx. $11K per month) on gain at sale– Local employer qualifies for tax deduction on

employee’s ordinary income – if recharge arrangement in place

– Requires Israeli trustee and lock-up of shares, but trustee handles withholding at sale of shares so ensures tax compliance

– New “deposit” requirements announced in July 2012 increase administrative burden

© 2013 Baker & McKenzie Consulting LLC

Tax-Qualified Plans (cont’d)

• United Kingdom– HMRC-approved options (CSOP)– Avoid employer NICs (13.8%, uncapped) on exercise– Substantial employee benefit – avoid income tax (up to

45%) and employee NICs on spread at exercise; gain at sale taxed as capital gains (18% or 28%), subject to annual exemption (£10,900)

– Rules recently adopted to simplify approved plans– Savings limited by £30,000 cap on approved options– Note: same employer saving via transfer of employer

NICs to employee

© 2013 Baker & McKenzie Consulting LLC

Tax-Qualified Plans (cont’d)

• United States– Code Section 423 ESPP and 422 Incentive Stock

Options– Save employer FICA and FUTA costs– But forgo tax deduction on spread/discount unless

disqualifying disposition– Overall, not the best approach for employer tax savings– Note: requires shareholder approval within 12 months,

holding periods, special reporting

© 2013 Baker & McKenzie Consulting LLC

Tax-Qualified Plans (cont’d)

• Plans that provide significant employee benefit – indirect employer savings for tax-equalized expatriates:– Canada – 50% tax exemption on option spread

– Belgium – options – elect tax at grant and undertake not to exercise for 3+ years – tax on only 11.5% of FMV at grant of 10-year option

– China – Tax Circulars 35 and 902 – equity income taxed separately from monthly salary, usually at lower rate

– Singapore – ERIS – tax exemption up to SGD 1M (US$800K) over 10-year period (must offer awards to 25% of employees) – for grants prior to December 31, 2013 only

– U.K. – CSOP/SIP – as discussed previously

– U.S. – ISO/ESPP – as discussed previously

© 2013 Baker & McKenzie Consulting LLC

Recharge Arrangements

• Where equity plans are sponsored by a non-resident parent company, tax authorities generally will not permit a local tax deduction for the employer absent a recharge agreement– Exceptions where no agreement required: U.S. and

U.K.– Exceptions where no deduction permitted, even with

recharge: Netherlands and Canada • Other local requirements may apply, e.g., special signature

or local board approval requirements, requirement to use treasury shares, tracking of cost of shares issued to employees, etc.

© 2013 Baker & McKenzie Consulting LLC

Recharge Arrangements (cont’d)

• How does a recharge save taxes?– Foreign subsidiary may claim a corporate tax deduction

not otherwise available (most countries allow deduction):• Reduces foreign taxes paid by subsidiary on its

earnings• Thus, reduces global effective tax rate

© 2013 Baker & McKenzie Consulting LLC

Recharge Arrangements (cont’d)

• How does a recharge save taxes for a U.S. issuer?– Tax-free repatriation of cash from foreign sub to U.S.

parent under IRC § 1032:• 1032(a) – U.S. parent not required to recognize

gain or loss upon receipt of money for its stock• Need to ensure amount reimbursed by foreign sub

does not exceed cost to U.S. parent, i.e., FMV of share less amount paid by employee (“employee benefit”)

• Foreign subsidiary’s reimbursement to parent for employee benefit is thus not treated as dividend for U.S. tax purposes

© 2013 Baker & McKenzie Consulting LLC

Recharge Arrangements (cont’d)

• Key implementation considerations:– Foreign exchange controls may prevent recharge

• Argentina – Central bank prohibits transfer and conversion of funds

• Brazil – Local bank approval required for recharge• China – SAFE approval generally required for

recharge• South Africa – Reserve Bank approval required

and not likely to be granted• Intercompany book transfer of funds not permitted

in these countries

© 2013 Baker & McKenzie Consulting LLC

Recharge Arrangements (cont’d)

• Collateral issues to watch– Recharge/local tax deduction may trigger

withholding/reporting obligations and/or social contributions• Employer social insurance triggered in several

countries, mainly in Eastern Europe and Latin America, e.g., Brazil, Chile, Czech Republic, Mexico, Poland

• Thus, need to make sure recharge produces overall tax saving

• Note – Belgium – recharge triggers 35% uncapped employer social tax – likely negates tax savings of recharge

© 2013 Baker & McKenzie Consulting LLC

Recharge Arrangements (cont’d)

• Collateral issues to watch– Recharge/local tax deduction may increase labor law

risk• Increased risk that awards included in “salary” for

determination of severance payments, etc. (e.g., Argentina, Brazil)

• May increase acquired rights/entitlement risk (e.g., France, Italy, Spain)

• May trigger possible need to consult with works council (e.g., Czech Republic, Germany)

© 2013 Baker & McKenzie Consulting LLC

Other Tax Saving Ideas

• Reduce, limit or cap grants in high employer tax countries, e.g.,– Argentina – employer social contributions 23% or 27%

uncapped– Estonia – employer-paid FBT due at total rate of 68.4%

(limited exception if options not exercised/RSUs don’t vest for three years from grant)

– Sweden – employer social contributions 31.42% uncapped

© 2013 Baker & McKenzie Consulting LLC

Other Tax Saving Ideas

• Transfer employer social charges to employee– U.K. – transfer employer NICs at 13.8% to employee

• Need HMRC-approved joint election signed by employee prior to taxable event (transfers liability)

• Can also accomplish via unapproved agreement with employee (but no transfer of liability)

• Employee can deduct employer NICs paid from tax liability

– Israel – transfer of employer social charges (5.9% capped) likely permitted if included in award agreement/initial terms

© 2013 Baker & McKenzie Consulting LLC

Other Tax Saving Ideas (cont’d)

• Transfer employer social charges to employee (cont’d)– Romania – potentially transfer all income tax and

employer/employee social contributions to employee via agreement with the employee– Saves employer social contributions applicable to

“payor” of income (approx. 6.8% is uncapped)– Need to register the agreement

– Often not permitted in other countries, e.g., Sweden

© 2013 Baker & McKenzie Consulting LLC

Other Tax Saving Ideas (cont’d)

• Avoid tax penalties through strong ongoing compliance– Determine country employer withholding/reporting and

social insurance requirements when implementing equity awards and update annually

– Identify countries with special year-end equity award reports and set up compliance systems, e.g., Australia, France (qualified plans), Ireland, U.K.

© 2013 Baker & McKenzie Consulting LLC

Other Compliance Considerations

• Create a Global Form of Agreement to Address Mobile Employee Risks and Ease Administration– One form given to employees regardless of location

with a country-specific appendix– Easier to update and administer because clear what

country-specific terms apply– If employee moves from country A to country B over

the life of the award, it is clear that terms of country B apply

– Establish a tracking and compliance system for globally mobile employees – many countries currently stepping up enforcement in this area, e.g., Australia, Canada, Sweden, U.K., U.S.

© 2013 Baker & McKenzie Consulting LLC

Other Compliance Considerations

• Keep Equity Awards Out of Employment Agreements and Offer Letters– If employee work for separate subsidiary, then grant by

issuer is not a benefit offered by the employer– Document new hire equity offerings through equity side

letter on parent company letterhead– Keep to a consistent policy of separating employment

benefits and equity compensation to minimize exposure to entitlement claims and termination indemnities

© 2013 Baker & McKenzie Consulting LLC

Questions?

© 2013 Baker & McKenzie Consulting LLC

Contact Information

Valerie H. Diamond

415.576.3086

June Anne [email protected]

© 2013 Baker & McKenzie Consulting LLC

DisclaimersThis presentation was prepared for general information purposes for clients and friends of Baker & McKenzie LLP and should not be considered or relied on as legal advice or an opinion on specific facts. This presentation is not intended to create, and receipt of this presentation does not constitute, a lawyer-client relationship.IRS Circular 230 Disclosure: Pursuant to requirements related to practice before the Internal Revenue Service, any tax advice contained in this presentation (including any attachments) is not intended to be used, and cannot be used, for the purpose of (i) avoiding penalties imposed under the United States Internal Revenue Code or (ii) promoting, marketing or recommending to another person any tax-related matter, including, without limitation, any transaction or matter that is contained in this presentation.