BÀI DỊCH ANH VĂN

30

4.3. RESOURCE ANALYSIS AND ADDING VALUE The fundamental role of resources in an organization is to add value. All organizations need to ensure that do not consistently lose value in the long term or they will not survive. For commercial organization, adding value is essential for their future. For non-profit organizations, adding value may only be a minor part of the reason for their existence, other purposes being centred on social, charitable or other goals. Resources add value by working on the raw materials that enter the factory gate and turning into a finished product. Added value can be defined as the difference between the market value of the output of an organization and the cost of its inputs. The concept is basically an economic one and is outlined, using GSK as an example, in Figure 4.5. for non-profit organizations, the concept of adding value can still be applied. The inputs to the organization may be similar to those of commercial organization electricity, telephones, etc.-and may be very different, particularly voluntary labour, which has a zero cost. Equally, the outputs may be difficult to define and measure-service to the community, help for sick people, etc. But the value added is real enough, just difficult to quantify. To explore the basic concepts, commercial explanations only are examined in this section. From the above definition of value added (i.e. outputs minus inputs), it follows that value can be added in an organizations: either by raising the value of outputs (sales) delivered to the customer; or by lowering the costs of its inputs (wages and salaries, capital and materials costs) into the company. Alternatively, both routes could be used simultaneously. Strategies therefore need to address these two areas.

-

Upload

horin-lata -

Category

Documents

-

view

102 -

download

1

Transcript of BÀI DỊCH ANH VĂN

4.3. RESOURCE ANALYSIS AND ADDING VALUEThe fundamental role of resources in an organization is to add value. All

organizations need to ensure that do not consistently lose value in the long term or they will not survive. For commercial organization, adding value is essential for their future. For non-profit organizations, adding value may only be a minor part of the reason for their existence, other purposes being centred on social, charitable or other goals. Resources add value by working on the raw materials that enter the factory gate and turning into a finished product. Added value can be defined as the difference between the market value of the output of an organization and the cost of its inputs.

The concept is basically an economic one and is outlined, using GSK as an example, in Figure 4.5. for non-profit organizations, the concept of adding value can still be applied. The inputs to the organization may be similar to those of commercial organization electricity, telephones, etc.-and may be very different, particularly voluntary labour, which has a zero cost. Equally, the outputs may be difficult to define and measure-service to the community, help for sick people, etc. But the value added is real enough, just difficult to quantify. To explore the basic concepts, commercial explanations only are examined in this section.

From the above definition of value added (i.e. outputs minus inputs), it follows that value can be added in an organizations:

either by raising the value of outputs (sales) delivered to the customer; or by lowering the costs of its inputs (wages and salaries, capital and

materials costs) into the company.

Alternatively, both routes could be used simultaneously. Strategies therefore need to address these two areas.

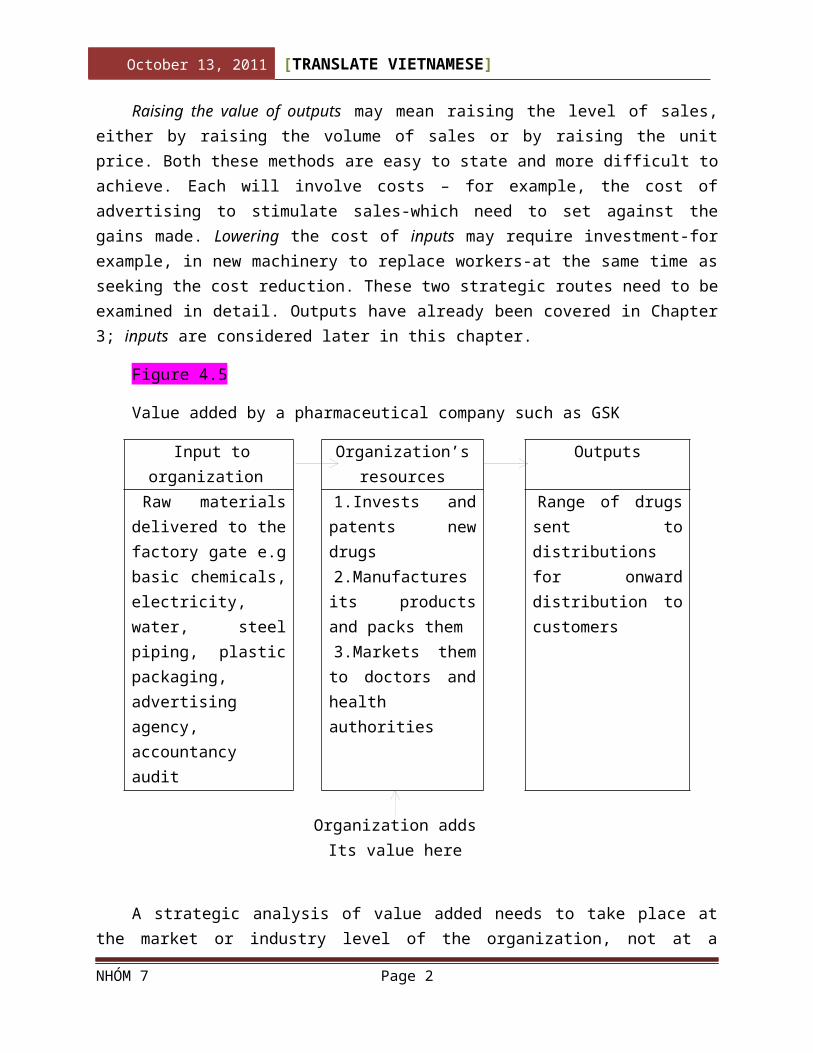

Raising the value of outputs may mean raising the level of sales, either by raising the volume of sales or by raising the unit price. Both these methods are easy to state and more difficult to achieve. Each will involve costs – for example, the cost of advertising to stimulate sales-which need to set against the gains made. Lowering the cost of inputs may require investment-for example, in new machinery to replace workers-at the same time as seeking the cost reduction. These two strategic routes need to be examined in detail. Outputs have already been covered in Chapter 3; inputs are considered later in this chapter.

Figure 4.5

Value added by a pharmaceutical company such as GSK

October 13, 2011 [ ]

Input to organization

Organization’s resources

Outputs

Raw materials delivered to the factory gate e.g basic chemicals, electricity, water, steel piping, plastic packaging, advertising agency, accountancy audit

1.Invests and patents new drugs2.Manufactures its

products and packs them3.Markets them to

doctors and health authorities

Range of drugs sent to distributions for onward distribution to customers

Organization addsIts value here

A strategic analysis of value added needs to take place at the market or industry level of the organization, not at a corporate or holding company level. If this analysis were to be undertaken at the general level, the performance of individual parts of the business would be masked. Value added is therefore calculated at the level of individual product groups.

Key strategic principles

The added value of a commercial organization is the difference between the market value of its output and the costs of its inputs.

The value added of a not-for-profit organization is the difference between the service provided and the costs of the inputs, some of which may be voluntary and have zero cost.

All organizations need to ensure that they do not consistently lose value in the long term or they will not survive. For commercial organizations, adding value is essential for their future. For non-profit organizations, adding value may only be a minor part of the reason for their existence, other purposes being centred on social, charitable or other goals.

In principle, there are only two strategies to raise value added in a commercial organization, increase the value of its outputs (sales) or lower the value of its inputs (the costs of labour, capital and materials). In practice, this implies detailed analysis of every aspect of sales and costs.

In companies with more than one product range, added value is best analysed by considering each group separately. Some groups may subsidise others in terms of added value. Not all groups are likely to perform equally.

NHÓM 7 Page 2

October 13, 2011 [ ]

4.4. ADDING VALUE: THE VALUE CHAIN AND THE VALUE SYSTEM – THE CONTRIBUTION OF PORTER

The concept of value added can be used to develop the organisation’s sustainable competitive advantage. There are two main routes – the value chain and the value system. Much of this approach was developed in the 1980s by Professor Michael Porter of the Harvard Business School.

Every organisation consists of activities that link together to develop the value of the business: purchasing supplies, manufacturing, distribution and marketing of its goods and services. These activities taken together form its value chain. The value chain identifies where the value is added in an organization and links the process with the main functional parts of the organisation. It is used for developing competitive advantage because such chains tend to be unique to an organisation.

When organisations supply, distribute, buy from or compete with each other, they form a broader group of value generation: the value system. The value system shows the wider routes in an industry that add value to incoming supplies and outgoing distributors and customers. It links the industry value chain to that of other industries. Again, it is used to identify and develop competitive advantage because such systems tend to be unique to companies.

The contributions of the value chain and value system to the development of competitive advantage, and the links between the two areas, which may also deliver competitive advantage, are explored in this section.

4.4.1. The value chain

The value chain links the value of activities of an organisation with its main functional parts. It then attempts to make an assessment of the contribution that it part make to the overall added value of the bussiness. The concept was used in acounting analysis for some years before Professor Micheal Porter suggeted that it could be applied to trategic analysis. Essentially, he links two areas together:

the added value that each part of the organisation contribute to the whole organisation and

the contribution to the competitive adventage of the whole oganisation that each of these parts might then make.

In a company with more than one product area, he said that the analysis should be conducted at the level of product groups, not of the level of company headquaters. The company is then spit into the primary activities of production, such as the production process itself, and the support activities, such as human resources management, that

NHÓM 7 Page 3

October 13, 2011 [ ]

give the necessary background to the running of the company but can’t be identified with any individual part. The analysis then examines how each part might be considered to contribute towards the generation of value in the company and how this differs from competitors.

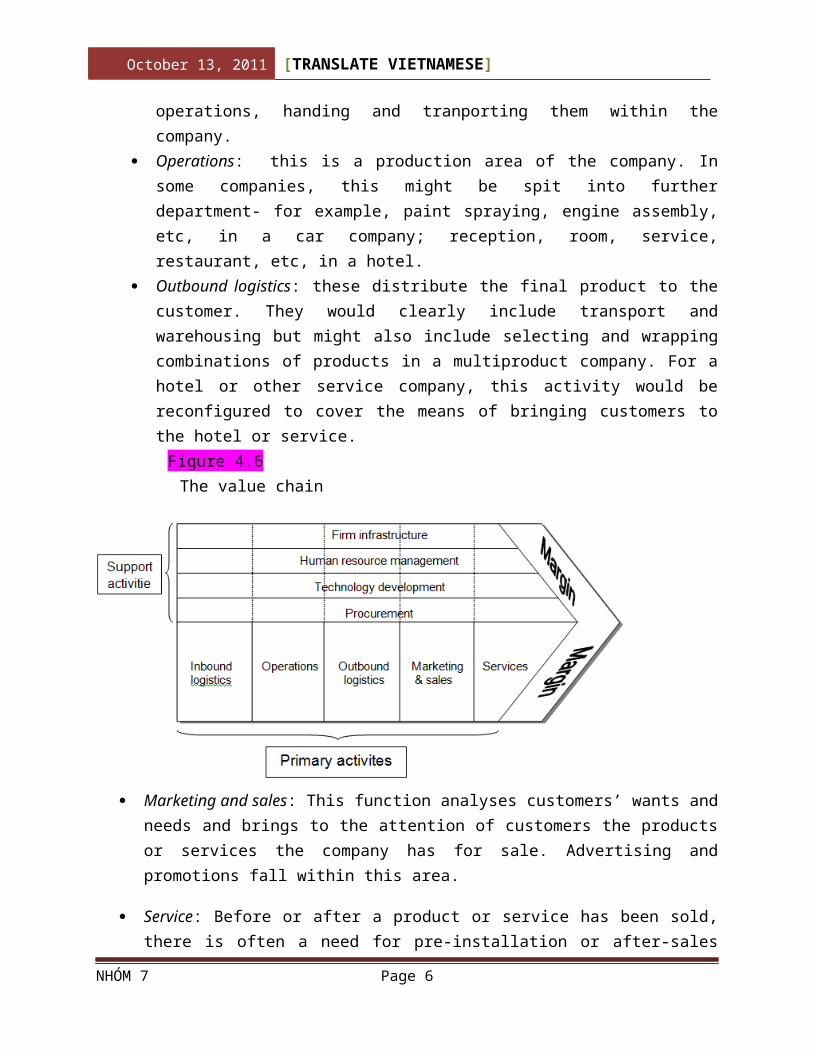

Porter‘s outline process is shown in Figure 4.6. He used the worg “margin” in the diagram to indicate what we defined as added value in section 4.4: “margin is the different between the total value and the collective cost of performing the value activities”.

According to the Porter, The primary activities of the company are: Inbound logistics: these are the areas concerned witn receiving the goods from

suppliers, storing them until required by operations, handing and tranporting them within the company.

Operations: this is a production area of the company. In some companies, this might be spit into further department- for example, paint spraying, engine assembly, etc, in a car company; reception, room, service, restaurant, etc, in a hotel.

Outbound logistics: these distribute the final product to the customer. They would clearly include transport and warehousing but might also include selecting and wrapping combinations of products in a multiproduct company. For a hotel or other service company, this activity would be reconfigured to cover the means of bringing customers to the hotel or service.

Figure 4.6The value chain

Marketing and sales: This function analyses customers’ wants and needs and brings to the attention of customers the products or services the company has for sale. Advertising and promotions fall within this area.

NHÓM 7 Page 4

October 13, 2011 [ ]

Service: Before or after a product or service has been sold, there is often a need for pre-installation or after-sales service. There may also be a requirement for training, answering customer queries, etc.

Each of the above categories will add value to the organisation in its own way. They may undertake this task better or worse than competitors: for example, with higher standards of service, lower production costs, faster and cheaper outbound delivery and so on. By this means, they provide the areas of competitive advantage of the organisation.

The support activities are:

Producement: In many companies, there will be a separate department (or group of managers) responsible for purchasing goods and materials that are then used in the operations of the company. The department’s function is to obtain the lowest prices and highest quality of goods for the activities of the company, but it is only responsible for purchasing, not for the subsequent production os the goods.

Technology development: This may be an important area for new products in the company. Even in a more mature industry, it will cover the existing technology, training and knowledge that will allow a company to remain efficient.

Human resource management: Recruitment, training, management development and the reward structures are vital elements in all companies.

Firm infrastructure: This inculdes the background planning and control sytems – for example, accounting, etc…that allow companies to administer and direct their development. It includes company headquarters.

These support activities add value, just as the primary activities do, but in a way that is more dificult to link with one particular part of organisation. A worked example of the primary part os a value chain is shown in Case 4.3 on Louis Vuitton and Gucci later in this chapter.

Comment

The problem with the value chain in strategic development is that it is designed to explore linkages and value-added areas of the business. By definition, it works within the existing structure. Real competitive strategy may require a revolution that moves outside the existing structure. Value chains may not be the means to achieve this

4.4.2. The value systemIn addition to the analysis of the company’s own value chain, Porter argued that an

addition analysis should also be undertaken. Organizations are part of wider system of adding value involving the supply and distribution value chains and the value chains of customers. This is known as the value system and is illustrated in Figure 4.7.

NHÓM 7 Page 5

October 13, 2011 [ ]

Except in very rare circumstances, every organization buys in some of its activities: advertising, product packaging design, management consultancy,electricity are all examples of items that are often acquired even by the largest companies. In the same way, many organizations do not distribute their products or services directly to the final consumer: travel agents, wholesalers, retail shops might all be involved in this role.

Competitors may or may not use the same value system: some suppliers and distributors will be better than others in the sense that they offer lower prices, faster service, more reliable products, etc… Real competitive advantage may come from using the best suppliers or distributors. New competitive advantage may be gained by using a new distribution system or obtaining a new relationship with a supplier. An analysis of this value system may also therefore be required. This will involve a resource analysis that extends beyond the organization itself.

Figure 4.7

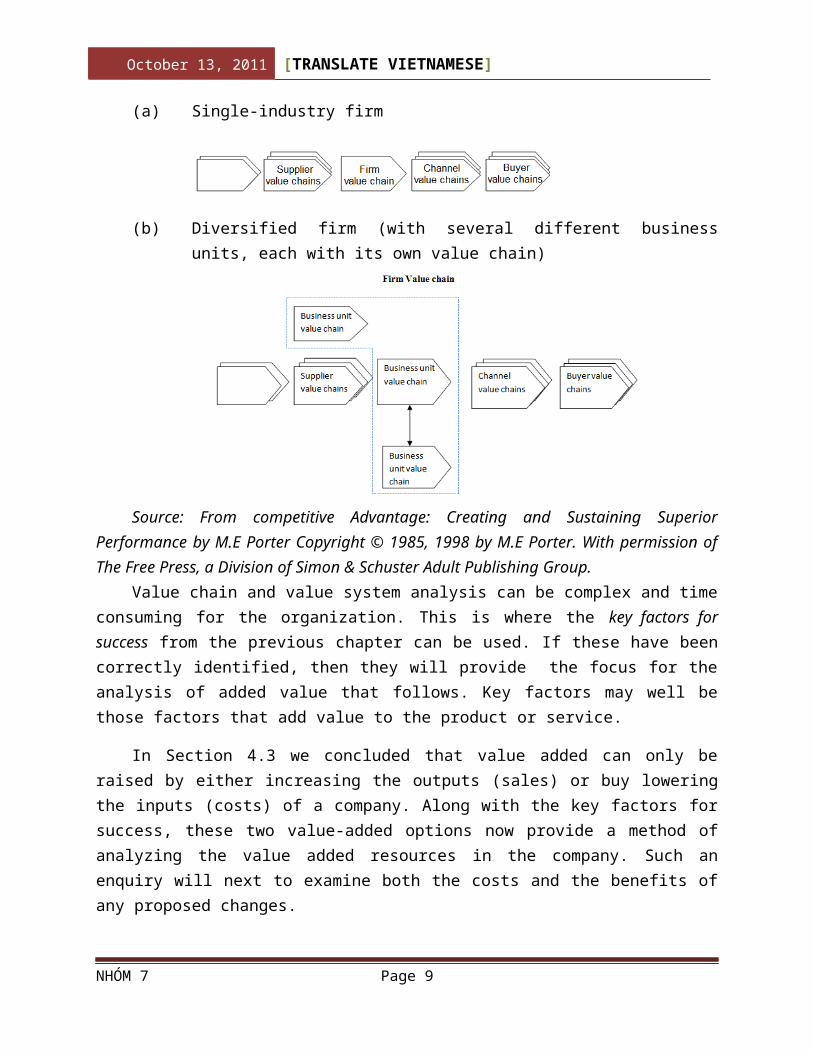

The value system

(a) Single-industry firm(b) Diversified firm (with several different business units, each with its own

value chain)

Source: From competitive Advantage: Creating and Sustaining Superior Performance by M.E Porter Copyright © 1985, 1998 by M.E Porter. With permission of The Free Press, a Division of Simon & Schuster Adult Publishing Group.

Value chain and value system analysis can be complex and time consuming for the organization. This is where the key factors for success from the previous chapter can be used. If these have been correctly identified, then they will provide the focus for

NHÓM 7 Page 6

October 13, 2011 [ ]

the analysis of added value that follows. Key factors may well be those factors that add value to the product or service.

In Section 4.3 we concluded that value added can only be raised by either increasing the outputs (sales) or buy lowering the inputs (costs) of a company. Along with the key factors for success, these two value-added options now provide a method of analyzing the value added resources in the company. Such an enquiry will next to examine both the costs and the benefits of any proposed changes.

In the case of Glaxo Smith Kline (GSK), the company might be advised to concentrate its value analysis initially at least on its identified key factors for success: R&D, marketing and product performance. In fact, the company’s strategy during recent years has been to invest very heavily in research and development- see Case 4.1. As already explored, GSK acquired the UK pharmaceutical company Wellcome in 1995 and merged with Smith Kline Becham in 2001. One of the main reasons for these activities was the strong range of new drugs that would complement the existing Glaxo product portfolio- another way of achieving R&D development. GSK might also usefully investigate ways of raising the value of key outputs and lowering key costs. The opening case showed that this is precisely the strategic activity undertaken by the company.

Comment

In common with the value chain, the value system is mainly concerned with the existing linkages and may miss totally new strategic opportunities.

4.4.3. Developing competive advantage linkages between the value chain and value system

Analysis of the value and the value system will provide information on value added in the company. For an organisation with a group of products, there may be some common item or common service the group, for example

a common raw material(such as sugar in various food products):or a common distributor (such as a car parts distrisbutor for a group with

subsidiary com - panies manufacturing various elements in car)...

Such common items may be linked to develop competitive advantage. Such possible linkages may be important to strategic development because they are often unique to that organisation. The linkages might therefore provide advantages over competitors who do not have such linkages, or who are unable to develop them easily.

It was Porter who suggested that value systems may not be sufficent in themselves to provide the competitive advantage needed by companies in developing

NHÓM 7 Page 7

October 13, 2011 [ ]

thier strategies. He argued that competitors can often imitate the individual moves made by an organisation; what competitors have much more difficulty in doing imitating the special and possibly unique linkages that exist between elements of the value chain and the value systems of the organization

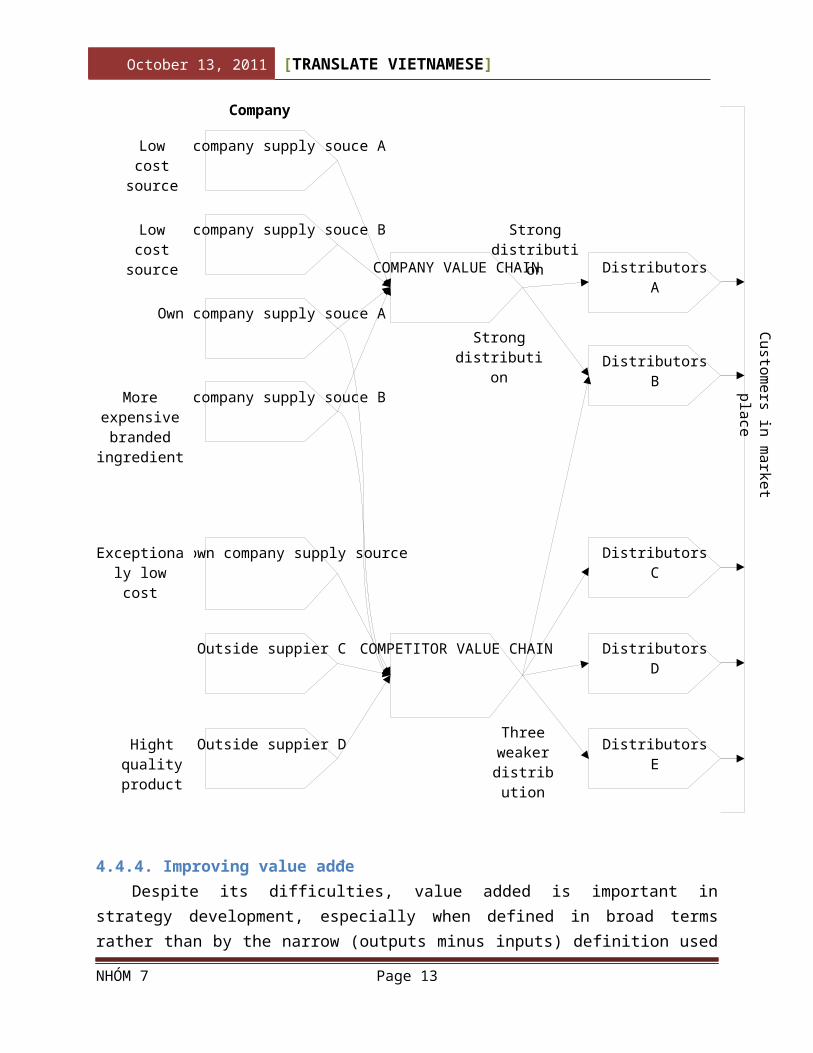

In addition to analysing resources for value chains and value systems, therefore, com-petitive strategy suggests that there is a third element. It is necessary to search for special and possibly unique linkages that either exist or might be developed between elements of the value chain and between value systems associated with the company. Figure 4.8 illus-trates this situation

Examples of such linkages abound

Common raw materials used in a variety of end-products: for example, petrochemical feedstocks are used widely to produce various products.

Common services, such as telecommunications or media buying, where a combined contract could be negotiated at a lower price than a series of individual local deals.

Linkages between technology development and production to facilitate new production methods that might be used in various parts of a group - for example, direct telecommunications links between large retail store chains such as marks & spencer and their suppliers.

Computer reservation systems that link airlines with travel ticket agents (proving to be so powerful that European commission has investigated their effects on airline competition).

Joint ventures, alliances and partnerships that often rely on different members to the agreement bringing their special areas of expertise to the relationship (see Chapter 9).

All the above suggest that linkage that enhance value added may provice significant ways for companies to improve their resources.

Comment

- One fundament problem with the value chain, value system and its linkages is their broad perspective across the range of the company's resources. They are sometimes rather value at indentifying the precise nature and scope of the advantage such resources possess against competitors. Sustainable competitive advantage is not the primary target of the value-added analysis. The remaining sections of this chapter explore more direct ways of tackling this issue.

- Another difficulty with value-added analysis is its focus on assets that can be clearly measured.This is a significant weakness because some of the organisation's

NHÓM 7 Page 8

October 13, 2011 [ ]

most valuable assets may be difficult to quantify - such as branding or specialist knowledge, moreover, some of the organisation's most important assets may be impossible to value, especially human resource assets like leadership and team building.

Figure 4.8Competitive advantage through linkages between the value chain and value system

NHÓM 7 Page 9

Own company supply souce ALow cost source

Own company supply souce BLow cost source

Own company supply souce A

Own company supply souce BMore expensive branded

ingredient

Major own company supply sourceExceptionaly low cost

Outside suppier C

Outside suppier DHight quality product

COMPANY VALUE CHAIN DistributorsA

DistributorsB

DistributorsC

DistributorsD

DistributorsE

COMPETITOR VALUE CHAIN

Strong distribution

Three weaker

distribution

Strong distribution

Company

Customers in m

arket placeOctober 13, 2011 [ ]

4.4.4. Improving value adđeDespite its difficulties, value added is important in strategy development, especially

when defined in broad terms rather than by the narrow (outputs minus inputs) definition used in the economic analysis explored in this chapter. The fundamental point remains that, unless organisations, this suggests that an important issue is how to capture the

NHÓM 7 Page 10

October 13, 2011 [ ]

value that is added by the organisation’s resource. We will pick up this theme in Chapters 8 and 9 after exploring resources in more detail.

Key strategic priciples

The value chain breaks down the activitives of the organisation into its main parts.

The contribution that each part makes can then be assessed for its contribution to sustainable competitive advantage.

The value chain is usually analysed without any detailed quantification of the added value that each elament contributes. It is undertaken at a broad general level and is compared with competitors.

Most organisations are part of a wider system of adding value anvolving supplier and distributor channels: the value system.

Analysing value chain and the value system can be complex. One way of reducing such difficulies is to employ the key factors for success as a means of selecting the items.

Possible linkages of elements of the value chain and value systems need to be analysed because they may be unique to the organisation and thus provide it with competitive advantage.

Significant weaknesses in the practical application pf value added include ia lack of precision in identifying areas of resource advantage and a inability to value clearly major assets like specialist knowledge and company leadership.

NHÓM 7 Page 11

October 13, 2011 [ ]

TRANSLATE

4.3. PHÂN TÍCH NGUỒN TÀI NGUYÊN VÀ GIÁ TRỊ GIA TĂNGVai trò cơ bản của nguồn tài nguyên trong một tổ chức là gia tăng thêm giá trị.Tất

cả các tổ chức cần phải đảm bảo giá trị không mất đi liên tục trong dài hạn nếu họ muốn tồn tại. Đối với một tổ chức thương mại, giá trị tăng thêm là điều cần thiết cho tương lai của họ. Đối với các tổ chức phi lợi nhuận, mục đích chính của họ là tập trung vào mục tiêu xã hội, từ thiện hoặc các mục tiêu khác, còn giá trị tăng thêm chỉ có thể là một phần nhỏ trong những lý do cho sự tồn tại của họ. Gia tăng giá trị nguồn lực bằng cách làm việc trên các nguyên liệu đầu vào nhà máy và tạo ra một sản phẩm hoàn chỉnh. Giá trị gia tăng có thể được định nghĩa là sự khác biệt giữa giá trị thị trường của một tổ chức và chi phí đầu vào của nó.

Khái niệm kinh tế cơ bản được trình bày, sử dụng GSK là một ví dụ (hình 4.5). Khái niệm về giá trị gia tăng vẫn có thể được áp dụng cho các tổ chức phi lợi nhuận. Đầu vào cho tổ chức này có thể tương tự như đối với những người của tổ chức thương mại điện tử, điện thoại,…và cũng có thể khác, đặc biệt là đối với lao động tự nguyện, tổ chức không phải bỏ ra chi phí nào. Tương tự, rất khó khăn để xác định các kết quả đầu ra và hiệu quả các dịch vụ cộng đồng, giúp đỡ cho người bệnh,...Tuy nhiên, rất khó để định lượng giá trị gia tăng đã thực sự đủ. Phần này sẽ giải thích và kiểm tra các nghiên cứu các khái niệm cơ bản này.

Từ định nghĩa trên về giá trị gia tăng (tức là kết quả đầu ra - đầu vào), nó chỉ ra giá trị thêm vào trong một tổ chức:

Nâng cao giá trị của kết quả đầu ra (bán hàng) giao cho khách hàng. Hoặc hạ thấp các chi phí đầu vào của nó (tiền lương, tiền vốn và các chi phí

vật liệu) vào công ty.

Ngoài ra, cả hai cách trên có thể được sử dụng đồng thời. Vì vậy, cần phải có chiến lược để giải quyết hai lĩnh vực này.

Nâng cao giá trị đầu ra có thể là nâng cao mức độ bán hàng, hoặc nâng cao doanh số bán hàng hay tăng giá bán. Cả hai phương pháp này đều dễ dàng để báo cáo và khó khăn hơn để đạt được. Mỗi chi phí liên quan đến- ví dụ như chi phí quảng cáo để kích thích bán hàng. Có thế yêu cầu giảm chi phí đầu vào, ví dụ như đầu tư máy móc mới để thay thế người lao động cùng một lúc để tìm kiếm sự giảm chi phí. Hai chiến lược này cần được nghiên cứu chi tiết. Đầu ra đã được bao gồm trong Chương 3, đầu vào được xem xét ở phần sau của chương này.

Giản đồ 4,5

NHÓM 7 Page 12

October 13, 2011 [ ]

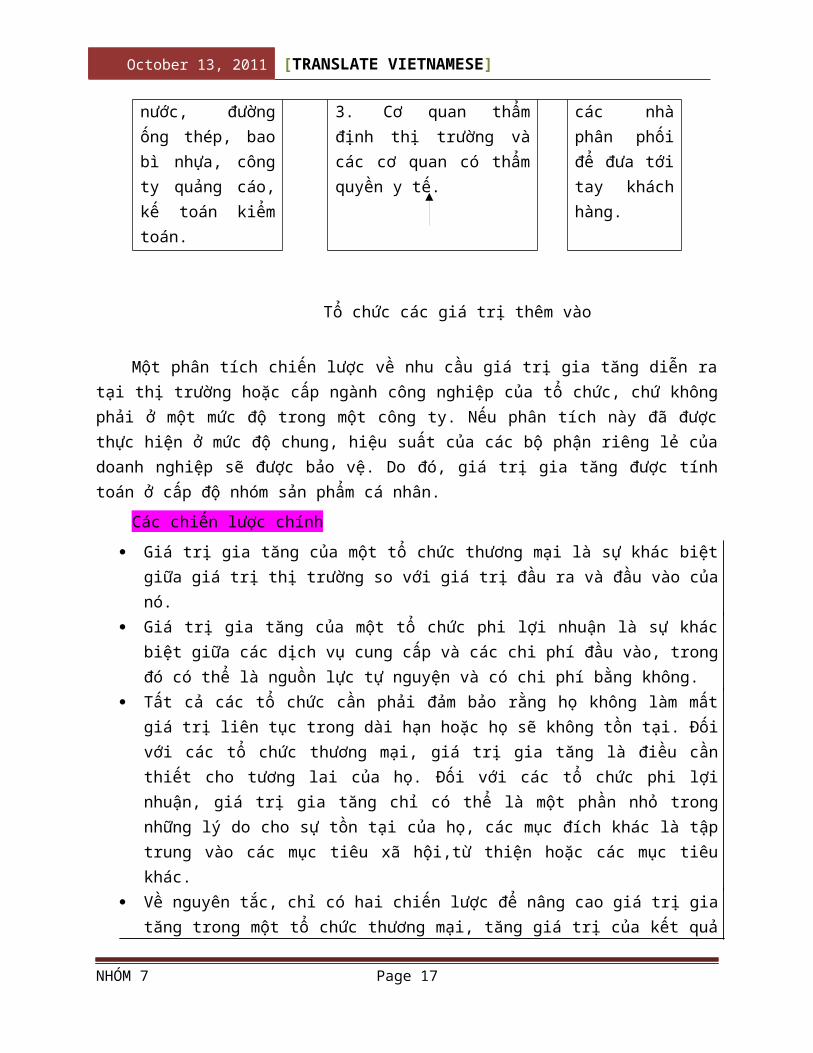

Đầu vào của tổ chức

Tổ chức nguồn lực Đầu ra

Nguyên liệu gửi đến, nhà máy ví dụ hoá chất cơ bản, điện, nước, đường ống thép, bao bì nhựa, công ty quảng cáo, kế toán kiểm toán.

1. Đầu tư và bằng sáng chế loại thuốc mới.2. Sản xuất sản phẩm và đóng gói.3. Cơ quan thẩm định thị trường và các cơ quan có thẩm quyền y tế.

Một loạt các loại thuốc được gửi đến cho các nhà phân phối để đưa tới tay khách hàng.

Tổ chức các giá trị thêm vào

Một phân tích chiến lược về nhu cầu giá trị gia tăng diễn ra tại thị trường hoặc cấp ngành công nghiệp của tổ chức, chứ không phải ở một mức độ trong một công ty. Nếu phân tích này đã được thực hiện ở mức độ chung, hiệu suất của các bộ phận riêng lẻ của doanh nghiệp sẽ được bảo vệ. Do đó, giá trị gia tăng được tính toán ở cấp độ nhóm sản phẩm cá nhân.

Các chiến lược chính

Giá trị gia tăng của một tổ chức thương mại là sự khác biệt giữa giá trị thị trường so với giá trị đầu ra và đầu vào của nó.

Giá trị gia tăng của một tổ chức phi lợi nhuận là sự khác biệt giữa các dịch vụ cung cấp và các chi phí đầu vào, trong đó có thể là nguồn lực tự nguyện và có chi phí bằng không.

Tất cả các tổ chức cần phải đảm bảo rằng họ không làm mất giá trị liên tục trong dài hạn hoặc họ sẽ không tồn tại. Đối với các tổ chức thương mại, giá trị gia tăng là điều cần thiết cho tương lai của họ. Đối với các tổ chức phi lợi nhuận, giá trị gia tăng chỉ có thể là một phần nhỏ trong những lý do cho sự tồn tại của họ, các mục đích khác là tập trung vào các mục tiêu xã hội,từ thiện hoặc các mục tiêu khác.

Về nguyên tắc, chỉ có hai chiến lược để nâng cao giá trị gia tăng trong một tổ chức thương mại, tăng giá trị của kết quả đầu ra (bán hàng) hoặc thấp hơn giá trị của yếu tố đầu vào (chi phí lao động, vốn và các nguồn nguyên liệu). Trong thực tế, điều này có nghĩa là phân tích chi tiết mọi khía cạnh của doanh số bán hàng và chi phí.

Đối với các công ty có nhiều hơn một dòng sản phẩm, giá trị gia tăng tốt nhất là phân tích bằng cách xem xét từng nhóm riêng biệt. Một số nhóm có thể trợ cấp

NHÓM 7 Page 13

October 13, 2011 [ ]

cho những giá trị gia tăng khác. Không phải tất cả các nhóm đều có thể thực hiện như nhau.

4.4. GIÁ TRỊ GIA TĂNG: CHUỖI GIÁ TRỊ VÀ HỆ THỐNG GIÁ TRỊ - ĐÓNG GÓP CỦA PORTER

Khái niệm giá trị gia tăng có thể được sử dụng để phát triển lợi thế cạnh tranh bền vững của tổ chức. Có hai con đường chính - chuỗi giá trị và hệ thống giá trị. Phần lớn phương pháp này đã được phát triển vào những năm 1980 bởi Giáo sư Michael Porter của Trường Kinh doanh Harvard.

Mỗi tổ chức bao gồm các hoạt động liên kết với nhau để phát triển giá trị của doanh nghiệp: mua vật tư, sản xuất, phân phối và tiếp thị hàng hóa và dịch vụ của mình. Những hoạt động này cùng thực hiện thống nhất hình thành nên chuỗi giá trị của nó. Chuỗi giá trị xác định nơi mà giá trị được thêm vào trong một tổ chức và liên kết quá trình với các bộ phận chức năng chính của tổ chức. Nó được sử dụng để phát triển lợi thế cạnh tranh bởi dây chuyền này có khuynh hướng là duy nhất cho một tổ chức.

Khi tổ chức cung ứng, phân phối, mua hoặc cạnh tranh với nhau, chúng tạo thành một nhóm rộng hơn của thế hệ giá trị: hệ thống giá trị. Hệ thống giá trị cho thấy các tuyến đường rộng hơn trong một ngành công nghiệp làm tăng thêm giá trị để cung cấp mà nhà phân phối và khách hàng đi đến. Nó liên kết các chuỗi giá trị ngành công nghiệp này với ngành công nghiệp khác. Một lần nữa, nó được sử dụng để xác định và phát triển lợi thế cạnh tranh bởi vì hệ thống như vậy có xu hướng là duy nhất cho các công ty.

Những đóng góp của chuỗi giá trị và hệ thống giá trị cho sự phát triển của lợi thế cạnh tranh, và các liên kết giữa hai khu vực, mà cũng có thể cung cấp lợi thế cạnh tranh, điều đó được làm rõ trong phần này.

4.4.1. Dây chuyền giá trị

Các dây chuyền giá trị liên kết giá trị của các hoạt động một tổ chức với các bộ phận chức năng chính của nó. Sau đó là nỗ lực đánh giá đóng góp của mỗi phần cho giá trị gia tăng của tổng thể kinh doanh. Khái niệm đã được sử dụng trong phân tích kế toán cho một số năm trước khi Michael Porter cho rằng nó có thể được áp dụng cho phân tích chiến lược. Về cơ bản, ông đã liên kết hai khu vực với nhau:

Giá trị gia tăng là một phần của một tổ chức đóng góp vào toàn bộ tổ chức và

Đóng góp vào lợi thế cạnh tranh của toàn bộ tổ chức khi gia tăng lợi thế cạnh tranh của tổ chức đã tạo ra nó.

NHÓM 7 Page 14

October 13, 2011 [ ]

Porter cho rằng đối với một công ty có nhiều hơn một lĩnh vực sản phẩm, phân tích cần được thực hiện ở cấp độ của các nhóm sản phẩm, không phải ở mức độ trụ sở công ty mẹ. Công ty được chia thành các hoạt động cơ bản của sản xuất, chẳng hạn như chính quá trình sản xuất của từng nhóm sản phẩm, và các hoạt động hỗ trợ, cũng như quản lý nguồn nhân lực, cung cấp cho các nền tảng cần thiết cho các hoạt động của công ty nhưng không thể xác định cho bất kỳ phần cá nhân nào. Sau đó xem xét làm thế nào mỗi phần có thể đóng góp vào việc tạo ra giá trị trong công ty và làm thế nào mà các điều này lại khác các đối thủ cạnh tranh.

Quá trình phác thảo của Porter được thể hiện trong giản đồ 4.6. Ông sử dụng từ "lợi nhuận" trong biểu đồ chỉ ra những gì chúng ta định nghĩa như giá trị gia tăng trong phần 4.4 “lợi nhuận là sự khác biệt giữa tổng giá trị và chi phí tập thể thực hiện các hoạt động giá trị”.

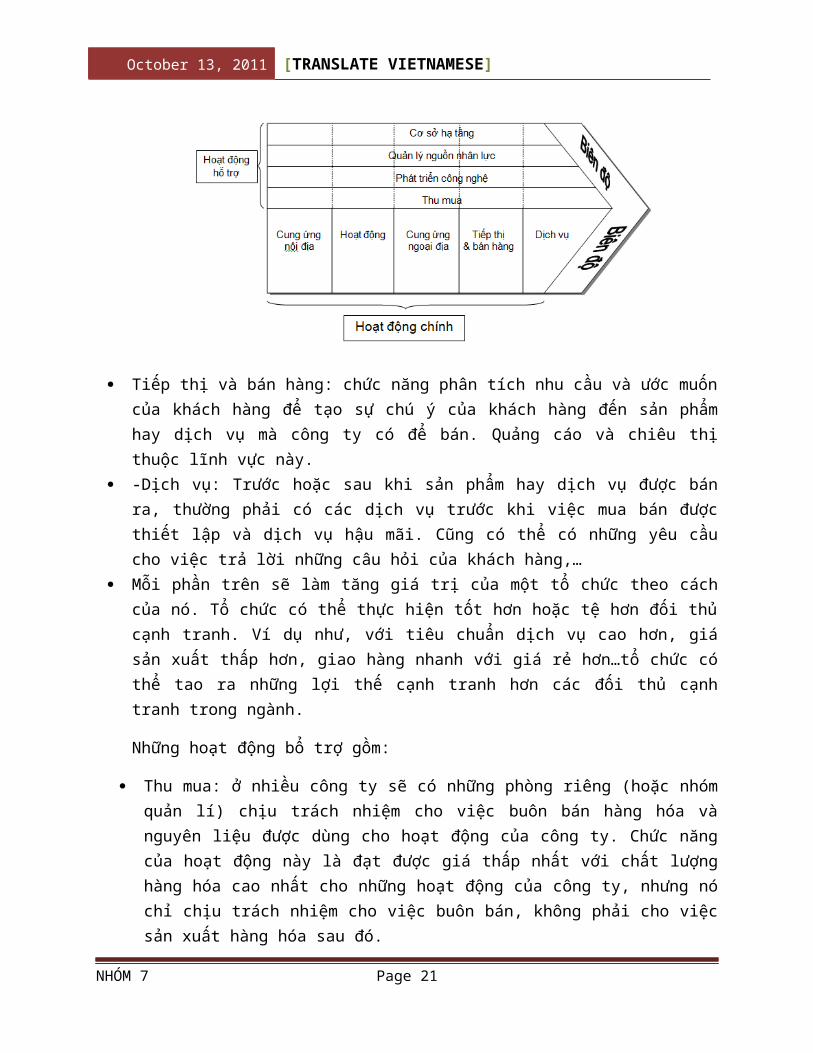

Theo Porter, các hoạt động cơ bản của công ty là:

Cung ứng nội địa: đây là những khu vực liên quan đến việc nhận được hàng hóa từ nhà cung cấp, lưu trữ chúng cho đến khi yêu cầu của hoạt động, bàn giao và vận chuyển trong công ty.

Hoạt động: đây là khu vực sản xuất của công ty.trong một số công ty, điều này có thể được chia thành các bộ phận. Ví dụ như sơn phun, động cơ, lắp ráp,...trong một chiếc xe hơi của công ty hoặc các dịch vụ tiếp nhận, dịch vụ phòng, nhà hàng,…trong một khách sạn.

Cung ứng ngoại địa: phân phối các sản phẩm cuối cùng đến khách hàng. Việc này rõ ràng sẽ bao gồm vận chuyển và kho bãi nhưng cũng có thể bao gồm việc lựa chọn và gói kết hợp của những sản phẩm trong một công ty đa sản phẩm. Đối với một khách sạn hoặc công ty dịch vụ khác, hoạt động này nên được định hình lại các phương pháp nhằm kích thích khách hàng đến sử dụng dịch vụ.

Giản đồ 4.6

NHÓM 7 Page 15

October 13, 2011 [ ]

Tiếp thị và bán hàng: chức năng phân tích nhu cầu và ước muốn của khách hàng để tạo sự chú ý của khách hàng đến sản phẩm hay dịch vụ mà công ty có để bán. Quảng cáo và chiêu thị thuộc lĩnh vực này.

-Dịch vụ: Trước hoặc sau khi sản phẩm hay dịch vụ được bán ra, thường phải có các dịch vụ trước khi việc mua bán được thiết lập và dịch vụ hậu mãi. Cũng có thể có những yêu cầu cho việc trả lời những câu hỏi của khách hàng,…

Mỗi phần trên sẽ làm tăng giá trị của một tổ chức theo cách của nó. Tổ chức có thể thực hiện tốt hơn hoặc tệ hơn đối thủ cạnh tranh. Ví dụ như, với tiêu chuẩn dịch vụ cao hơn, giá sản xuất thấp hơn, giao hàng nhanh với giá rẻ hơn…tổ chức có thể tao ra những lợi thế cạnh tranh hơn các đối thủ cạnh tranh trong ngành.

Những hoạt động bổ trợ gồm:

Thu mua: ở nhiều công ty sẽ có những phòng riêng (hoặc nhóm quản lí) chịu trách nhiệm cho việc buôn bán hàng hóa và nguyên liệu được dùng cho hoạt động của công ty. Chức năng của hoạt động này là đạt được giá thấp nhất với chất lượng hàng hóa cao nhất cho những hoạt động của công ty, nhưng nó chỉ chịu trách nhiệm cho việc buôn bán, không phải cho việc sản xuất hàng hóa sau đó.

Sự phát triển công nghệ: điều này là một yếu tố quan trọng cho những sản phẩm mới của công ty. Thậm chí trong nền công nghiệp phát triển hơn, nó bao gồm sự phát triển của công nghệ, chuyên môn và kiến thức để công ty duy trì tính hiệu quả.

Quản lí nguồn nhân lực: tuyển dụng, huấn luyện, phát triển quản lí và cấu trúc tiền thưởng là những yếu tố cần thiết cho sự sống còn của các tất cả các công ty.

NHÓM 7 Page 16

October 13, 2011 [ ]

Cơ sở hạ tầng của công ty: điều này bao gồm kế hoạch cơ bản và hệ thống kiểm soát (ví dụ: kế toán,…) điều này cho phép công ty quản lí và điều khiển sự phát triển của họ. Nó bao gổm cơ quan đầu não của công ty.

Những hoạt động bổ trợ giá trị gia tăng, chỉ là những hoạt động cơ bản, nhưng trong một cách nào đó có nhiều khó khăn để liên kết với một bộ phận đặc biệt của tổ chức. Một ví dụ công việc của phần cơ bản được chỉ ra trong 4.3 của Louis Vuiton và Gucci trong chương này.

Lời bình

Vấn đề dây chuyền giá trị trong chiến lược phát triển được thiết kế ra để khám phá những liên kết tồn tại và những khu vực giá trị gia tăng của doanh nghiệp. Theo định nghĩa, nó hoạt động bên trong cấu túc hiện có. Một chiến lược cạnh tranh thật sự có thể yêu cầu một cuộc cách mạng, một sự đổi mới bên ngoài cấu trúc hiện có. Chuỗi giá trị có thể không phải là cánh thức để đạt được thành tựu này.

4.4.2. Các hệ thống giá trị Ngoài việc phân tích hệ thống chuỗi giá trị của công ty, Porter lập luận rằng một

bảng phân tích bổ sung cũng nên được thực hiện. Tổ chức là một phần của hệ thống rộng lớn hơn về gia tăng giá trị liên quan đến các hệ thống cung cấp và phân phối thoả mãn nhu cầu thị trường và các chuỗi giá trị của khách hàng. Điều này được gọi là hệ thống giá trị và được minh họa trong hình 4.7.

Ngoại trừ những trường hợp rất hiếm, mọi tổ chức mua trữ một số hoạt động của mình: quảng cáo, thiết kế bao bì sản phẩm, tư vấn quản lý, điện là tất cả các ví dụ về các mặt hàng thường được mua lại, ngay cả bởi các công ty lớn nhất. Với cùng một cách thức, nhiều tổ chức không phân phối các sản phẩm hoặc dịch vụ của họ trực tiếp đến người tiêu dùng cuối cùng mà sử dụng các đại lý du lịch, bán buôn, cửa hàng bán lẻ để hoàn thành vai trò này.

Đối thủ cạnh tranh có thể có hoặc không thể sử dụng cùng một hệ thống giá trị: một số nhà cung cấp và nhà phân phối sẽ tốt hơn so với những người khác trong việc mà họ cung cấp mức giá thấp hơn, dịch vụ nhanh hơn, sản phẩm đáng tin cậy hơn,… Những lợi thế cạnh tranh thật sự có thể đến từ việc dùng các nhà cung cấp hoặc nhà phân phối tốt nhất. Lợi thế cạnh tranh mới có thể đạt được bằng cách sử dụng một hệ thống phân phối mới hoặc có được một mối quan hệ mới với một nhà cung cấp. Vì vậy, việc phân tích hệ thống giá trị này rất cần thiết. Điều này sẽ liên quan đến phân tích nguồn lực dành cho chính tổ chức .

Giản đồ 4.7Hệ thống giá trị(a) Công ty-công nghiệp đơn lẻ

NHÓM 7 Page 17

October 13, 2011 [ ]

(b) Công ty đa dạng hoá (với các đơn vị kinh doanh khác nhau, mỗi chuỗi giá trị riêng của mình)

Nguồn: Lợi thế cạnh tranh: Tạo và duy trì hiệu suất bởi ME PorterCopyright © 1985, 1998

ME Poter. Với sự cho phép của The Free Press một bộ phận của Tập đoàn Simon & Schuster xuất bản dành cho người lớn.

Chuỗi giá trị và phân tích hệ thống giá trị có thể phức tạp và mất thời gian đối với tổ chức. Điều này là yếu tố quan trọng cho sự thành công từ giai đoạn trước có thể được sử dụng. Nếu những việc này đã được xác định chính xác, họ sẽ cung cấp trọng điểm cho việc phân tích về những giá trị gia tăng vào những giai đoạn tiếp theo. Những yếu tố quan trọng cũng có thể là những yếu tố làm tăng giá trị sản phẩm hay dịch vụ.

Trong phần 4.3, chúng tôi kết luận rằng giá trị gia tăng chỉ có thể được nâng lên bằng cách tăng các kết quả đầu ra (bán hàng) hoặc mua giảm các yếu tố đầu vào (chi phí) của một công ty. Cùng với những yếu tố quan trọng cho sự thành công, hai lựa chọn giá trị gia tăng này cung cấp một phương pháp phân tích giá trị gia tăng nguồn lực trong công ty. Một cuộc điều tra tiếp theo để kiểm tra chi phí và lợi ích của bất kỳ sự thay đổi được đề xuất.

Trường hợp của Glaxo Smith Kline (GSK), công ty có thể được tư vấn để tập trung phân tích giá trị ban đầu, ít nhất là trên các yếu tố quan trọng mang lại sự thành công: R & D, tiếp thị và hiệu suất sản phẩm. Trong thực tế, chiến lược của công

NHÓM 7 Page 18

October 13, 2011 [ ]

ty trong những năm gần đây đã được đầu tư rất mạnh vào nghiên cứu và phát triển, nhìn ví dụ 4,1. Như đã được khám phá, GSK có được công ty dược phẩm Vương quốc Anh, Wellcome vào năm 1995 và sáp nhập với Smith Kline Becham vào năm 2001. Một trong những lý do chính cho các hoạt động này là các loại thuốc mới và mạnh này có thể bổ sung danh mục vốn đầu tư sản phẩm Glaxo hiện có, cách khác để đạt được sự phát triển R & D. GSK cũng có thể nghiên cứu những cách nâng cao giá trị của sản lượng và giảm chi phí chính một cách hiệu quả. Trường hợp mở đầu cho thấy rằng đây là các hoạt động chiến lược được thực hiện một cách chính xác bởi công ty.

Lời bìnhGiống như các phân tích hệ thống cung cấp, hệ thống giá trị đề cập chủ

yếu với các mối quan hệ hiện có và có thể bỏ lỡ những cơ hội chiến lược hoàn toàn mới.

4.4.3. Phát triển các mối liên kết cạnh tranh giữa các chuỗi giá trị và hệ thống giá trị

Phân tích giá trị và hệ thống giá trị sẽ cung cấp thông tin về giá trị gia tăng trong công ty. Một tổ chức với một nhóm sản phẩm, có thể có một số mặt hàng thông thường hoặc dịch vụ chung của nhóm, ví dụ:

Một nguyên liệu thông thường (chẳng hạn như đường trong các thực phẩm khác nhau):

Một nhà phân phối thông thường (chẳng hạn như một nhà phân phối phụ tùng xe hơi cho các công ty sản xuất các yếu tố khác nhau trong xe hơi) ..

Các hạng mục thông thường có thể được liên kết để phát triển lợi thế cạnh tranh. Mối liên kết này có lẽ quan trọng để phát triển chiến lược vì chúng thường là duy nhất của tổ chức đó. Do đó các mối liên kết có thể cung cấp các lợi thế cạnh tranh so với các đối thủ cạnh tranh hay những người không có mối liên kết như vậy, hoặc những người không thể phát triển chúng một cách dễ dàng.

Porter đề nghị rằng hệ thống các giá trị có thể không hoàn toàn cung cấp đầy đủ các lợi thế cạnh tranh cần thiết cho các công ty trong việc phát triển chiến lược của họ. Ông lập luận rằng các đối thủ cạnh tranh có thể thường xuyên bắt chước tuỳ theo các hoạt động cá nhân được thực hiện bởi tổ chức, nhưng họ sẽ gặp khó khăn trong việc bắt chước các mối liên kết đặc biệt và các liên kết duy nhất giữa các yếu tố của chuỗi giá trị và hệ thống giá trị của tổ chức.

Ngoài ra để phân tích các nguồn lực của các chuỗi giá trị và hệ thống giá trị, chiến lược cạnh tranh chứa trong nó yếu tố thứ ba. Việc tìm kiếm các mối liên kết đặc biệt và độc đáo có thể tồn tại hoặc phát triển giữa các thành phần trong chuỗi giá trị và hệ thống giá trị liên quan đến công ty rất cần thiết. Giản đồ 4.8 thể hiện rõ điều này.

NHÓM 7 Page 19

October 13, 2011 [ ]

Một số ví dụ cho các liên kết trên:

Nguyên vật liệu được sử dụng phổ biến để hoàn thành các sản phẩm cuối cùng: ví dụ, nguyên liệu hóa dầu được sử dụng rộng rãi để sản xuất các sản phẩm khác nhau.

Dịch vụ thông thường, chẳng hạn như viễn thông, mua phương tiện truyền thông, nơi một hợp đồng kết hợp có thể được đàm phán ở một mức giá thấp hơn so với một loạt các giao dịch cá nhân địa phương.

Mối liên kết giữa phát triển công nghệ và sản xuất tạo điều kiện thuận lợi cho phương pháp sản xuất mới có thể được sử dụng trong các bộ phận khác nhau của một nhóm - ví dụ, viễn thông liên kết trực tiếp giữa các chuỗi cửa hàng bán lẻ lớn như Marks & Spencer và nhà cung cấp của họ.

Hệ thống các phòng máy tính của hãng hàng không liên kết với các đại lý vé máy bay du lịch (như vậy Ủy ban châu Âu đã điều tra được sự ảnh hưởng mạnh mẽ của chúng trong việc cạnh tranh của hãng hàng không).

Liên doanh, liên minh và quan hệ đối tác thường dựa vào các thành viên khác nhau để đạt được sự thỏa thuận trong các lĩnh vực chuyên môn đặc biệt của họ về mối quan hệ (xem Chương 9).

Tất cả các thành phần bên trên cho thấy mối liên kết nhằm nâng cao giá trị gia tăng có thể cung cấp các cách thức, dấu hiệu cho các công ty để cải thiện nguồn lực của họ.

Lời bình

Một trong những vấn đề cơ bản của các chuỗi giá trị, hệ thống giá trị và mối liên kết của nó là quan điểm rõ ràng trên phạm vi nguồn lực của công ty. Các công ty đôi khi xác định giá trị bản chất và phạm vi của các lợi thế nguồn lực như vậy để khống chế đối thủ cạnh tranh. Lợi thế cạnh tranh bền vững không phải là mục tiêu chính của phân tích giá trị gia tăng. Phần còn lại của chương này khám phá các cách thức trực tiếp hơn để giải quyết vấn đề này.

Một khó khăn khác với phân tích giá trị gia tăng là tập trung vào các tài sản có thể đo lường rõ ràng. Đây là một điểm yếu đáng kể bởi vì một số tài sản của tổ chức có giá trị nhất có thể rất khó để định lượng - chẳng hạn như xây dựng thương hiệu hoặc kiến thức chuyên môn. Hơn nữa, một số tài sản của tổ chức quan trọng nhất có thể không quy ra được giá trị, đặc biệt là nguồn nhân lực như là lãnh đạo và các đội nhóm mạnh.

Giản đồ 4.8

NHÓM 7 Page 20

Công ty cung cấp nguồn ANguồn chi phí thấp

Công ty cung cấp nguồn BNguồn chi phí cao

Bên ngoài cung cấp nguồn A

Bên ngoài cung cấp nguồn BThương hiệu mạnh

Các nguồn cung cấp chính từ công tyChi phí đặc biệt thấp

Bên ngoài cung cấp C

Bên ngoài cung cấp DChất lượng sản phẩm cao

Chuỗi giá trị của công ty Phân phối A

PHÂN PHỐIB

Phân phốiC

Phân phốiD

Phân phốiE

Chuỗi giá trị của đối thủ cạnh tranh

Phân phối mạnh

Ba yếu tố phân phối

Phân phối mạnh

Công ty

Khách hàng trong thị trường

October 13, 2011 [ ]

NHÓM 7 Page 21

October 13, 2011 [ ]

4.4.4. Cải thiện giá trị gia tăngMặc dù vẫn gặp phải những khó khăn, nhưng giá trị gia tăng vẫn là một yếu tố

quan trọng trong việc phát triển chiến lược, đặc biệt là khi đã định nghĩ rõ các thuật ngữ hơn là các định nghĩa hẹp (đầu ra trừ đầu vào) được sử dụng trong phân tích kinh tế được tìm hiểu ở chương này. Điểm cơ bản còn lại, nếu doanh nghiệp không thêm vào một vài giá trị đầu vào của họ, thì sự tồn tại của họ có lẽ là một dấu chấm hỏi. Với hầu hết các doanh nghiệp, điều này đưa ra một vấn đề quan trọng, đó là làm thế nào để nắm bắt được giá trị đưa ra bởi nguồn lực của doanh nghiệp. Chúng ta sẽ gặp chủ đề này ở chương 8 và 9 sau khi tìm hiểu chi tiết hơn.

Nguyên tắc chiến lược cốt lõi:

Phân tích hệ thống cung cấp làm đổ vỡ các hoạt động của doanh nghiệp vào các phần chính của nó.

Sự đóng góp của một nhóm tạo nên có thể được ước định cho sự đóng góp của nó để có thể tạo nên ưu thế cạnh tranh.

Phân trích hệ thống cung cấp không được phân tích với bất kỳ sự xác định số lượng tỉ mỉ của giá trị gia tăng mà mỗi yếu tố đóng góp. Nó được cam kết ở 1 cấp độ rộng và được so sánh với đối thủ cạnh tranh.

Hầu hết các doanh nghiệp là một phần của một hệ thống rộng hơn của giá trị gia tăng, bao gồm nhà cung cấp và kênh phân phối: hệ thống giá trị.

Phân tích chuỗi giá trị và hệ thống giá trị có thể phức tạp. Một cách để giảm thiểu khó khăn là làm những nhân tố chủ chốt thành công như một mục đích của việc lựa chọn các yếu tố.

Sự liên kết có thể của các yếu tố của chuỗi giá trị và hệ thống giá trị cần được phân tích vì chúng có thể khác với doanh nghiệp và qua đó cung cấp cho nó lợi thế cạnh tranh.

Điểm yếu quan trọng trong việc áp dụng thực tiễn của giá trị gia tăng bao gồm sự thiếu chính xác trong những khu vực xác định của lợi thế dự phòng và một sự bất lực để đánh giá rõ ràng tài sản chủ yếu, như sự kiến thức của chuyên gia và ban lãnh đạo công ty.

NHÓM 7 Page 22