Azerbaijan presentation slides

87

BP in Azerbaijan Baku September 2006

Transcript of Azerbaijan presentation slides

BP in Azerbaijan

BakuSeptember 2006

Cautionary statement

Forward looking statements: This presentation and the associated slides and discussion contain forward-looking statements, particularly those regarding oil and gas prices; expected start-up of Thunderhorse; the timing of other projects and their contribution to expected production, their estimated reserves and production capacity; production; the expected movement of non-proven resources to proved reserves; divestments and their effect; capital expenditure; and cash flow. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that will or may occur in the future. Actual results may differ from those expressed in such statements, depending on a variety of factors, including the timing of bringing new fields on stream; future levels of industry product supply; demand and pricing; operational problems; general economic conditions; political stability and economic growth in relevant areas of the world; changes in laws and governmental regulations; exchange rate fluctuations; development and use of new technology; changes in public expectations and other changes in business conditions; the actions of competitors; natural disasters and adverse weather conditions; wars and acts of terrorism or sabotage; and other factors discussed elsewhere in this presentation.

Cautionary Note to US Investors - The United States Securities and Exchange Commission permits oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or formation tests to be economically and legally producible under existing economic and operating conditions. We use certain terms in this presentation, such as “resources” and “non-proven reserves”, that the SEC’s guidelines strictly prohibit us from including in our filings with the SEC. U.S. investors are urged to consider closely the disclosures in our Form 20-F, SEC File No. 1-6262, available from us at 1 St. James’s Square, London SW1Y 4PD. You can also obtain this form from the SEC by calling 1-800-SEC-0330.

September 2006

Introduction

Fergus MacLeodHead of Investor Relations

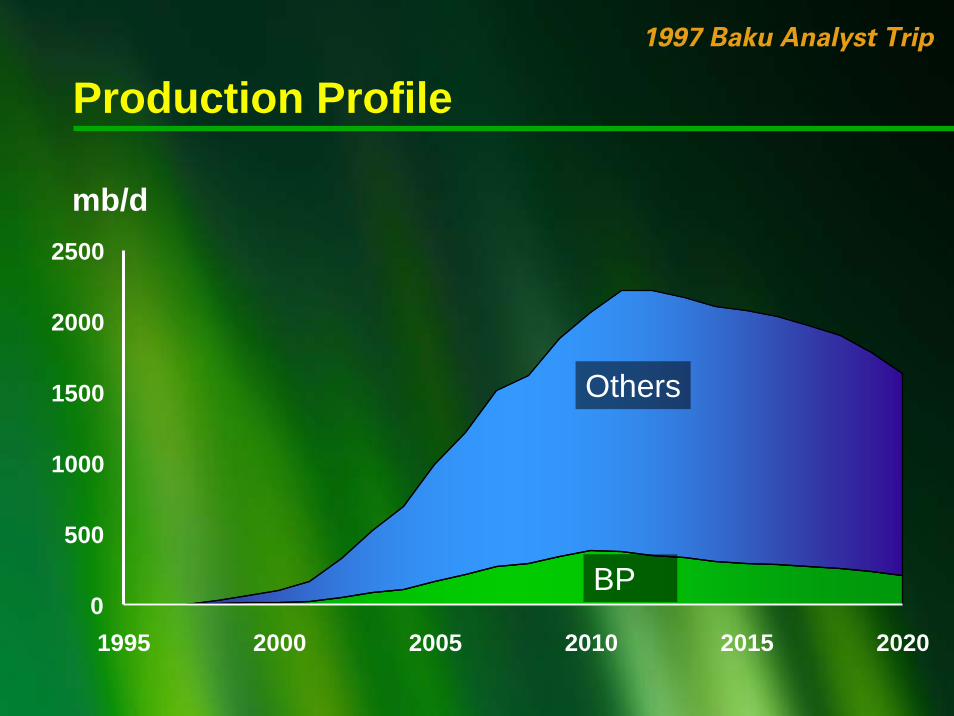

1989 Access Agenda1997 Baku Analyst Trip

E & W SiberiaE & W Siberia

CaspianCaspian

VietnamVietnam

NigeriaNigeriaVenezuela YemenVenezuela YemenLombokLombok

AngolaAngola

AlgeriaAlgeriaGOM GOM DeepwaterDeepwater

Current Environment1997 Baku Analyst Trip

Challenge to BPChallenge to BP

–– Keep ahead of pack Keep ahead of pack

–– Play to strengthsPlay to strengths–– Exploration track record Exploration track record –– Deepwater technologyDeepwater technology–– Relationship managementRelationship management–– Deepen existing posDeepen existing positionsitions–– Broaden into new posBroaden into new positionsitions

Competition Increasing

– Access competition

– New players

– Terms erosion

Production Profile

0

500

1000

1500

2000

2500

1995 2000 2005 2010 2015 2020

mb/d

BP

Others

1997 Baku Analyst Trip

E&P Strategy Update

Tony HaywardChief Executive, Exploration & Production

BP Azerbaijan organisation

Technical DirectorFereidoun Abbassian

BP Azerbaijan PresidentDavid Woodward / Bill Schrader*

Renewal VPPaul Clyne

Shah Deniz VPMike Skitmore

Major Projects VPBruce Luberski

Offshore Operations VPNeil McCleary

Onshore Operations VPRashid Javanshir

HR DirectorZarina Zeynalova

C&EA DirectorClare Bebbington

HSSE DirectorGunther Newcombe

Business Transformation

ManagerJudith Luberski*David Woodward will be retiring from BP on 1 January 2007,

Bill Schrader will be effective in this role from 10 November 2006

Commercial DirectorPhil Home

Georgia General ManagerHugh McDowell

Turkey E&P DirectorDjan Suphi

Chief of StaffErich Krumanocker

Executive AssistantKamala Husseynli

Project start-ups

2006Atlantis

King Sub-sea Pump

San Juan Coal Bed Methane

Greater Plutonio

Kizomba A Ph 2

Rosa

Red Mango

North West Area Development

Cannonball

TemsahRedevelopment

BTC

In Amenas

Wamsutter

Dalia

East Azeri

Shah Deniz

MagnusExtension

on stream in development under appraisal

Paz Flor

Egypt LNG T2

Browse

Io / Janz

Tangguh Phase 2

Vietnam Phase 2

Colombia Gas

Clair Ridge

Skarv

Kovykta Export

Rospan

North Rankin B

Kizomba D

Shah Deniz Phase 2

2007 2008 - 2009 2010 and beyondThunder HorseUrsa ExpansionKizomba CACG Phase 3AngelAustralia LNG T5Tangguh Phase 1SaqqaraDoradoGreat WhiteHorn Mountain NWMad Dog SW RidgeMars SouthCashimaChacalacaEgypt LNG T1Harding GasValhall RedevelopmentUvat (Demiansky Phase I)

Atlantis North Flank

Puma

Tubular Bells

Alaska Gas

Liberty

Point Thomson

Western Regional Development

Angola LNG

Block 18 West

Block 31 North

Block 31 South

Block 31 Central

2005Valhall Waterflood

Mad Dog

Central Azeri

Clair

Kizomba B

Trinidad LNG Train 4

Rhum

West Azeri

Mardi Gras Pipeline

Production to 2010

TNK-BP

New profit centres

Existing profit centres

Divestments closed in 2006

BP projection for ‘06-’10 updated to reflect closed ’06 divestments

mmboe/d

Actual prices and portfolio

Production at $40

0

1

2

3

4

5

2001 2002 2003 2004 2005 2010

Strategy – building profit centres

Existing Profit Centres

New Profit Centres

Russia / Kazakhstan

AlaskaAlaska

North America Gas

North America Gas

North Sea

North Sea RussiaRussia

EgyptEgypt

Latin America

Latin America

Middle East

Middle East

DeepwaterGulf of Mexico

DeepwaterGulf of Mexico

AngolaAngola

North AfricaNorth Africa

AzerbaijanAzerbaijan

Trinidad & TobagoTrinidad

& TobagoAsia

PacificAsia

Pacific

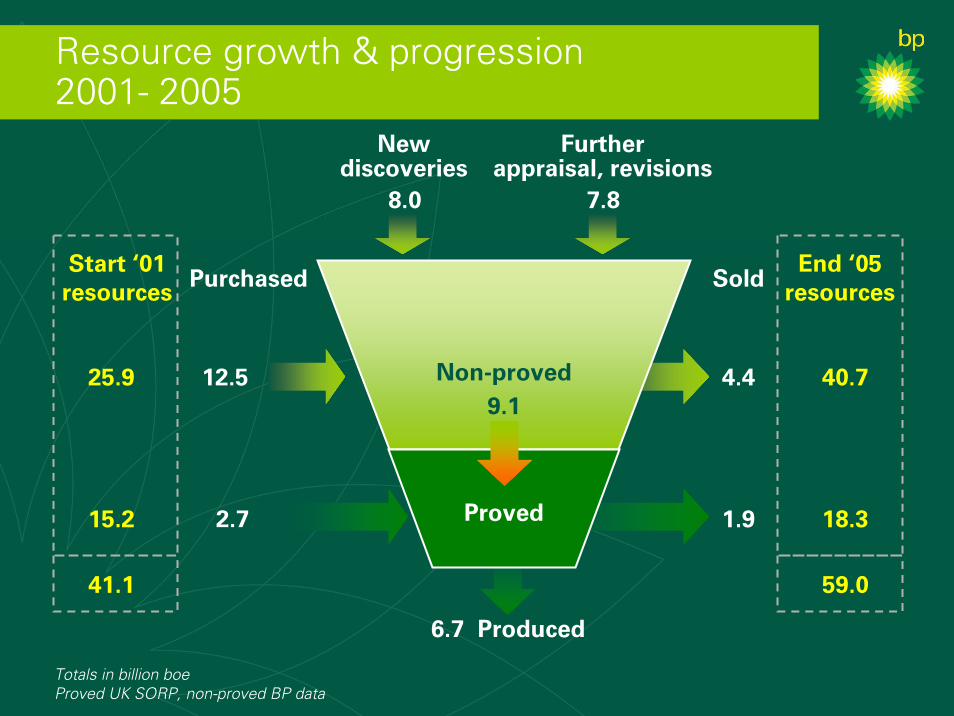

Resource growth & progression 2001- 2005

Non-proved

Proved

12.5

Newdiscoveries

2.7

9.1

6.7 Produced

7.88.0

Furtherappraisal, revisions

PurchasedStart ‘01

resources

25.9

15.2

41.1

Sold

4.4

1.9

End ‘05 resources

40.7

18.3

59.0

Totals in billion boeProved UK SORP, non-proved BP data

End 2005 resource by type

Between 2005 and 2010 11 bn boe of non-proved

resources are expected to be moved to proved reservesTotals in billion boe

Proved UK SORP, non-proved BP data

Non-Proved

Conventional Oil

Deepwater Oil

Water Flood Viscous and Heavy Oil

Conventional Gas

LNG Gas

Tight Gas

Coal Bed Methane

Proved

18 bn boe41 bn boe

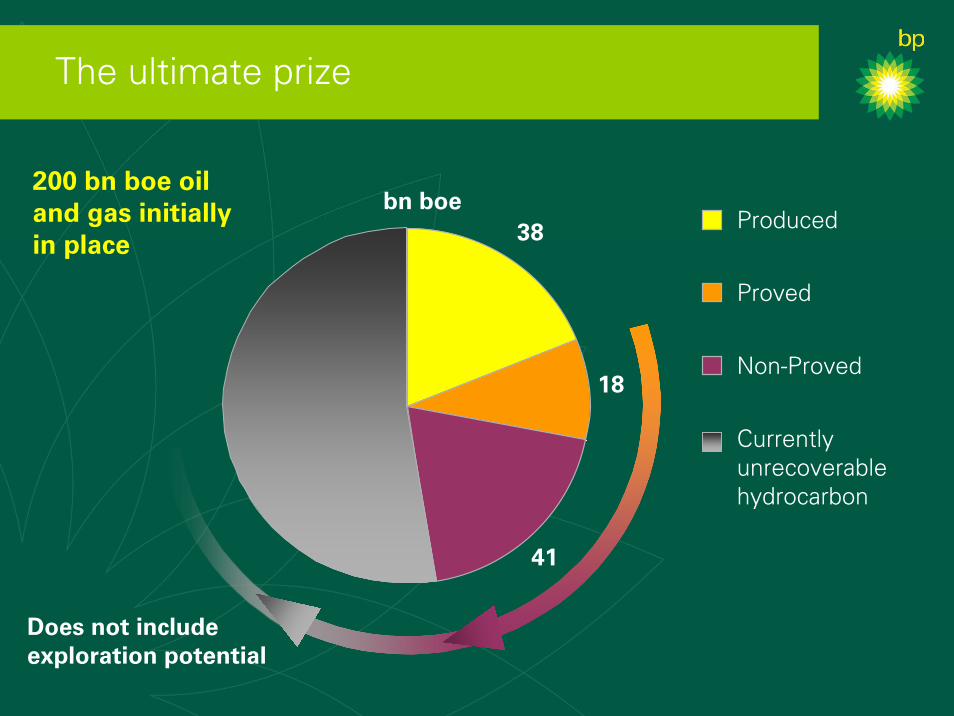

The ultimate prize

Does not include exploration potential

Produced

Proved

Non-Proved

Currently unrecoverable hydrocarbon

18

41

38bn boe

200 bn boe oil and gas initially in place

Summary

• New Profit Centres have arrived

− Major Projects underpin production growth through the end of the decade and beyond

• Power of incumbent positions

− Technology to unlock the resource base

Building a New Profit Centre:Azerbaijan

Andy InglisDeputy Chief Executive, Exploration & Production

Building a new profit centre: Azerbaijan

• Resource base

• Technology

• Project delivery

• Statecraft and diplomacy

• Sustainability through mutuality

Resource base: Azerbaijan

bn boe 0.4

6.1

7.6

ACG and Shah Deniz Gross Resource

Produced

Sanctioned

Non-Proved

Currently unrecoverable hydrocarbon

Source: BP data

Technology

Reserves pull-through

Maximising revenue

Capital efficiency

Project delivery

Dorado 2008

Go

M

Horn MountainNW 2008

Mad Dog SW Ridge 2009

Atlantis North Flank 2010+

Eg

ypt

Train 1 Supply 2008 Train 2 Supply – Ph1 2010+ Train 2 Supply – Ph2 2010+

Tri

nid

ad

Cannonball – 2006 Cashima – 2008Red Mango – 2007 Chachalaca -2009

An

go

la

G. Plutonio - 2007 Bk31 North – 2010+ Bk31 Central – 2010+ Bk31 South – 2010+ Bk18 West – 2010+

Aze

rbai

jan

Central Azeri - 2004 West Azeri - 2005 East Azeri – 2006 ACG3 - 2008

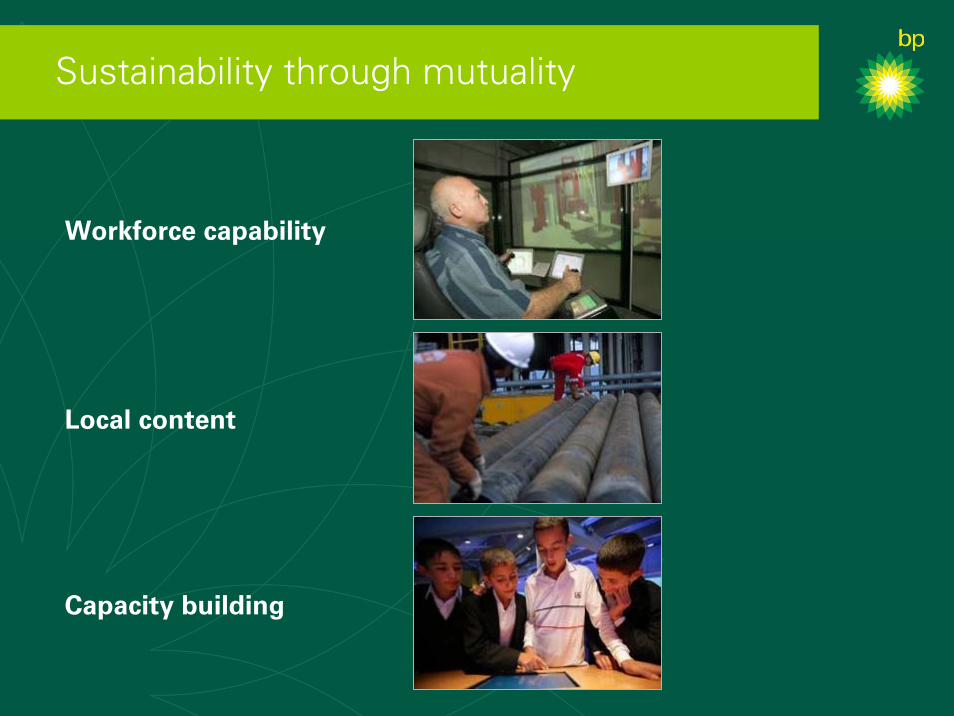

Statecraft and diplomacy

Sustainability through mutuality

Workforce capability

Local content

Capacity building

Overview of Azerbaijan and BP’s presence

Rashid JavanshirVice President, Onshore Operations

Geography

KAZAKHSTAN

RUSSIA

UKRAINE

AZERBAIJANTURKEY

SYRIA

IRAQ

IRAN

BULGARIA

MOLDOVA

Supsa

Novorossiysk

Ceyhan

Istanbul

Odessa

Constanta Black Sea

CaspianSea

Mediterranean Sea

Bosphorus

ARMENIA

TUR

KM

ENIST A

N

GEORGIA

Baku

150 years of oil production

0

200

400

600

800

1000

1200

1400

1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020

Historical peak 1941 (475 mmstb/d)

ACG 2010 (1200 mmb/d)

Future decline for other fields assumed 3% annual

Chirag online 1997

Azeri online 2005

Phase 3 online 2008

Oil

rate

(m

bd

)

Today

Chirag

Azeri

DW

G

Further Developments

Azerbaijan’s oil history

Oil wells in the vicinity of Baku pumping oil into reservoir lakes in 1880s.Photo: Azerbaijan National Archives.

The Nobel Brothers' oil wells in Balakhani, a suburb of Baku.

View of Oil Rocks c. 1950s 2006 Central Azeri platforms

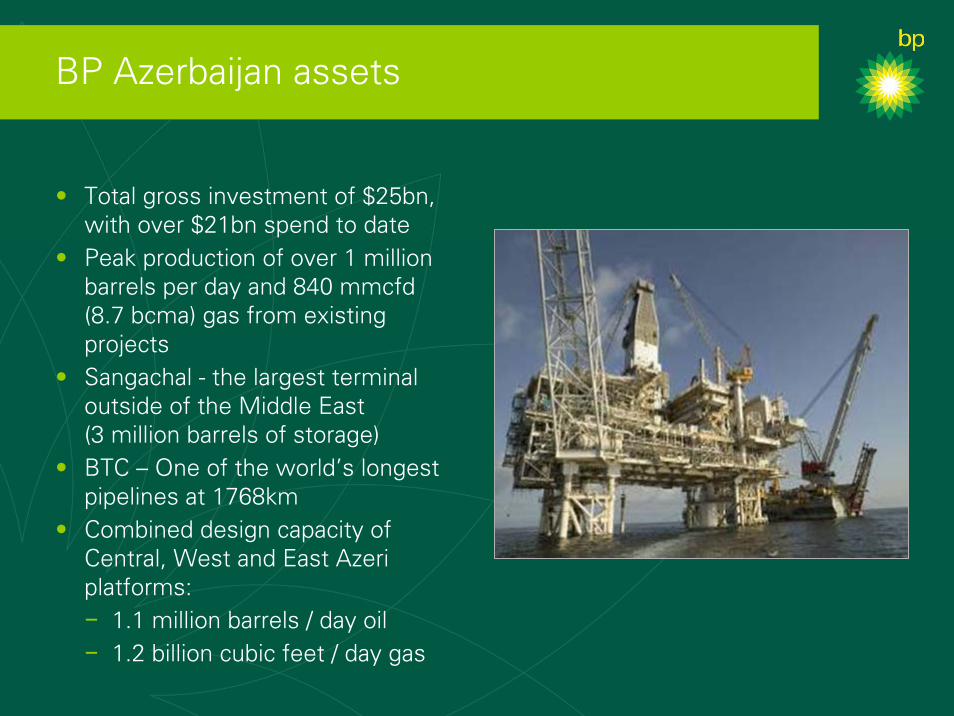

BP Azerbaijan assets

0 300 km200100

Turkey

IraqSyria

Russia

Georgia

Ceyhan

Erzurum

Black Sea

Tbilisi

Med.

Sea

South Caucasus

Pipeline Gas

South Caucasus

Pipeline Gas

WREPPipelineWREP

Pipeline

BTC Pipeline Oil

BTC Pipeline Oil

NREP PipelineNREP

Pipeline

Supsa

Novorossiysk

Caspian Sea

Iran

Kazakhstan

Turkmenistan

Azerbaijan

Inam Exploration

Inam Exploration

Shah Deniz Gas Development

Shah Deniz Gas Development

Alov Exploration

Alov Exploration

Baku

ACG Oil Production

& Development

ACG Oil Production

& Development

Sangachal Terminal

Sangachal Terminal

BP Azerbaijan assets

• Total gross investment of $25bn, with over $21bn spend to date

• Peak production of over 1 million barrels per day and 840 mmcfd (8.7 bcma) gas from existing projects

• Sangachal - the largest terminal outside of the Middle East (3 million barrels of storage)

• BTC – One of the world’s longest pipelines at 1768km

• Combined design capacity of Central, West and East Azeri platforms: − 1.1 million barrels / day oil − 1.2 billion cubic feet / day gas

Resources and Renewal

Paul ClyneVice President, Renewal

Resource base: Azerbaijan

Gross oil / gas resource potential

Non-proved

Sanctioned (incl. produced)

Exploration (risked)

1.1

5.4

2.2

3.1

4.5

0

1

2

3

4

5

6

7

8

9

ACG SD Exploration

Res

ou

rce

po

ten

tial

Bn

bo

e

Source: BP data (based on existing PSCs only)

BP Azerbaijan net resource progression 2001 - 2005

Non-proved

Proved

1.2

0.1 Produced

1.9

AdditionsCurrent PSC appraisal

and exploration

Start ‘01 resources

1.3

0.2

1.5

End ‘05 resources

2.0

1.3

3.3

*Totals in bn boeEnd ‘05 position based on UK SORP, non-proved BP data

Future potential

Potential gross oil + condensate production

0200400600800

1,0001,2001,4001,6001,800

2006 2009 2012 2015 2018 2021 2024 2027 2030

Oil

& c

on

den

sate

p

rod

uct

ion

(m

bd

)

PSC base production

Further develop existing PSCs

Further exploration & access

Potential gross gas production

2006 2009 2012 2015 2018 2021 2024 2027 20300123456789

Gas

pro

du

ctio

n (

bcf

d)

Forward projections: BP data

Major Projects Delivery (Offshore)

Bruce Luberski, Vice President, Major ProjectsMike Skitmore, Vice President, Shah Deniz

ACG field

ACG sanctioned resource 5.4 bn bbl

Peak production gross 1.2 mmbd

Capital cost gross $17 bn

BP working interest 34.1%

ACG gross production

Deepwater Gunashli

0

200

400

600

800

1000

1200

1400

2005 2008 2011 2014 2017 2020 2023

mb

d

Chirag

Azeri

Forward projections: BP data

BP Azerbaijan vision

The FutureSangachal

Chirag

East Azeri

Central Azeri

West Azeri

Shah Deniz 1

ACG Phase 32008

Inam Alov

Shah Deniz 2

End 2004

GROWTH Capital Spend 2004: $12m/ day

End 2006

Sangachal

Chirag l

Shah Deniz 1

Sangachal

West Azeri

ChiragCentral Azeri & C&WP

East Azeri2006

GROWTH Capital Spend 2006: $13m/day

Offshore: Chirag Chirag, CA/CWP, WA, SD,EA 8+ operating platforms + Projects

People: 4000 BP staff + agency >2000 BP staff3000 BP staff + agency

Infrastructure: ••

2 export pipelinesSangachal EOP Terminal

• 4 export pipelinesExpanded Sangachal Terminal•

• 4 export pipelinesOne of the biggest terminals in the world

•

Production:130 mbd

• 500 mbd Shah Deniz ramping up •

• 1 mmbd in 2009840 mmcfd in 2009•

Project schedule

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Appraise Select Define Execute PSC signed / Sanction Operation

ACG PSC

Early Oil Project

Central Azeri & C&WP

West & East Azeri

ACG Phase 3 (DWG)

BTC

Shah Deniz PSC

Shah Deniz 1

First Oil WA

First Oil

First Gas to Turkey

Ceyhan Lifting

First Oil EA

First Oil C&WP Start-up

First Oil

First Oil WA

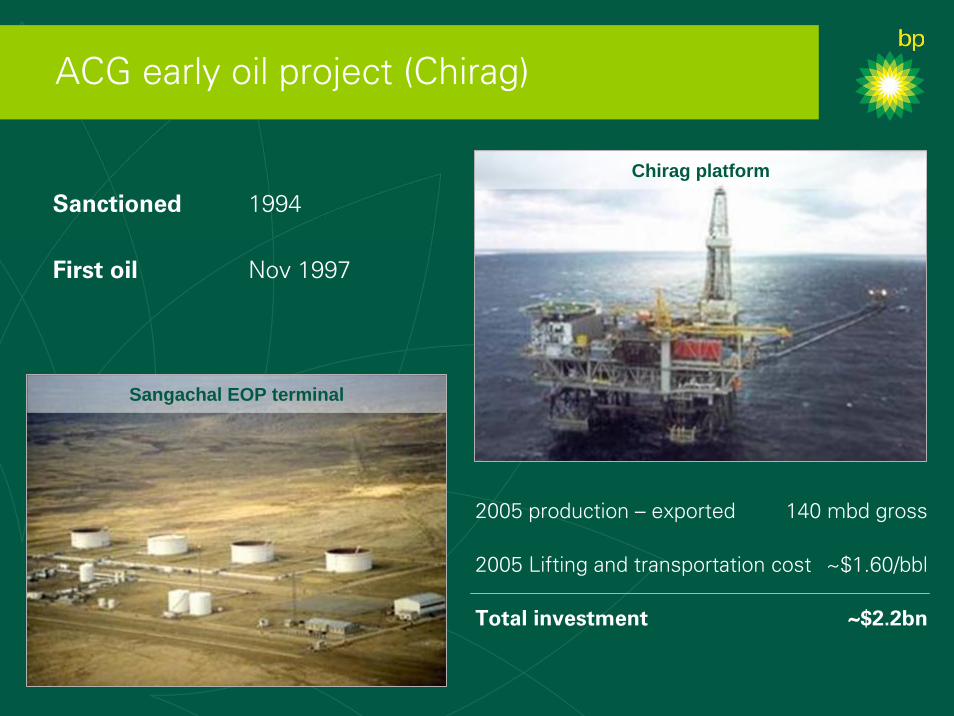

Chirag platform

Sangachal EOP terminal

ACG early oil project (Chirag)

Sanctioned 1994

First oil Nov 1997

2005 production – exported 140 mbd gross

2005 Lifting and transportation cost ~$1.60/bbl

Total investment ~$2.2bn

Sangachal Terminal

ACG full field development

Deepwater GunashliPhase 3

2008

ChiragEOP

Nov 1997

West AzeriPhase 2

Dec 2005

Central Azeri

Phase 1Mar 2005

East Azeri

Phase 24Q 2006

•••

90,000 te topsides90,000 te jackets1000 km offshore pipelines

••••

One of world’s largest terminals7 years of execute100 million man-hours to dateOver 3 million man-hours/month

•••

80% of man-hours in Azerbaijan20% across another 10 countriesNew Workforce - 8000 Azerbaijani

Sangachal history

Early Oil Project

2000

Sangachal history

Early Oil Project

2005

Shah Deniz

Projects production line

Production facilities engineering costs

Dir

ect

man

ho

urs

/te

CloneEA(15)CWP

(21)

CA(41)

WA(32)

Build duration

Mo

nth

s

30

28

27

26

25

CA

WA

29

EA

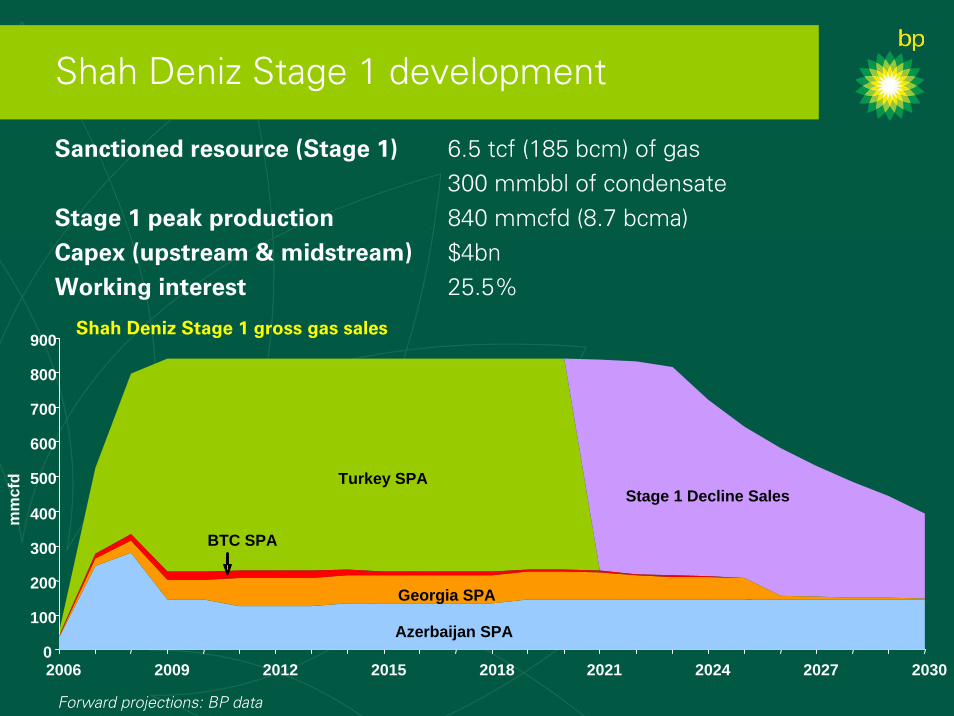

Shah Deniz Stage 1 development

Shah Deniz Stage 1 development

Sanctioned resource (Stage 1) 6.5 tcf (185 bcm) of gas 300 mmbbl of condensate

Stage 1 peak production 840 mmcfd (8.7 bcma) Capex (upstream & midstream) $4bnWorking interest 25.5%

BTC SPA

Turkey SPAStage 1 Decline Sales

0

100

200

300

400

500

600

700

800

900

2006 2009 2012 2015 2018 2021 2024 2027 2030

mm

cfd

Shah Deniz Stage 1 gross gas sales

Azerbaijan SPA

Georgia SPA

Forward projections: BP data

Shah Deniz

Sangachal Terminal on track

Offshore pipeline – beach pull

Progress on SDX-04 appraisal

TPG500 installation

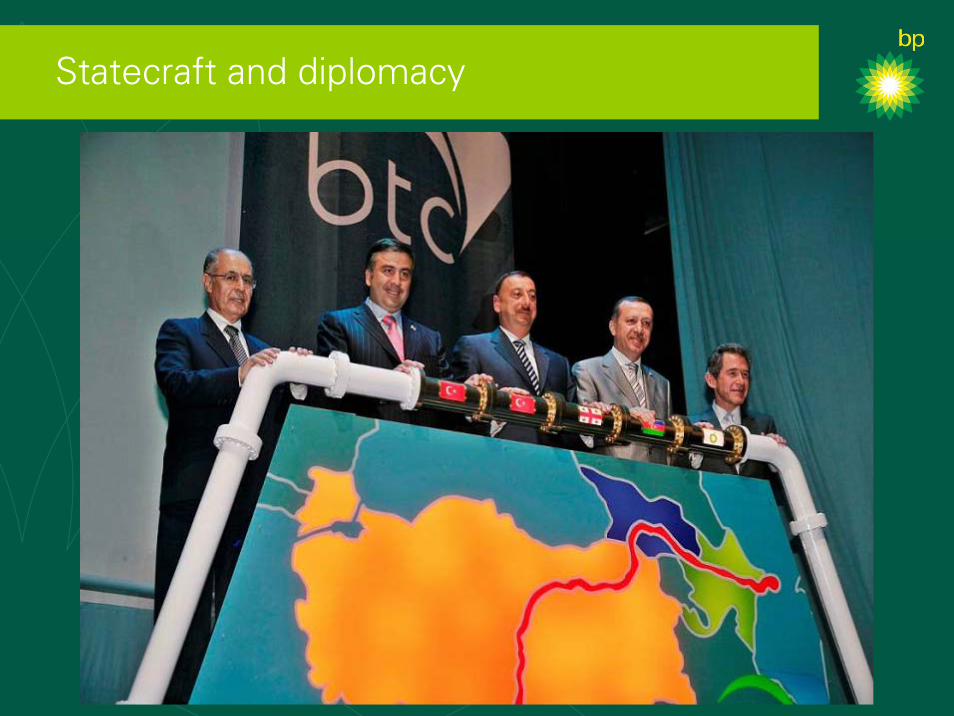

Statecraft and Diplomacy:The Story of BTC

Michael TownshendFormer Vice President, Onshore Operations & Projects

Regional context

`

Kazakhstan

Russia

Turkey

SyriaIraq

Iran

CaspianSea

Armenia

Tu

rkmen

istan

Georgia

Ukraine

Bulgaria

Moldova

Black Sea

Mediterranean Sea

Bosphorus

Ceyhan

Istanbul

Supsa

Novorossiysk

Baku

Odessa

Constanta

Azerbaijan

The politics of welding

Golden Weld Azerbaijan /Georgia – Oct 04 1st Oil Azerbaijan – May 05

1st Oil Georgia – Oct 05 Golden Weld Azerbaijan /Georgia – Oct 04

Social

Environmental

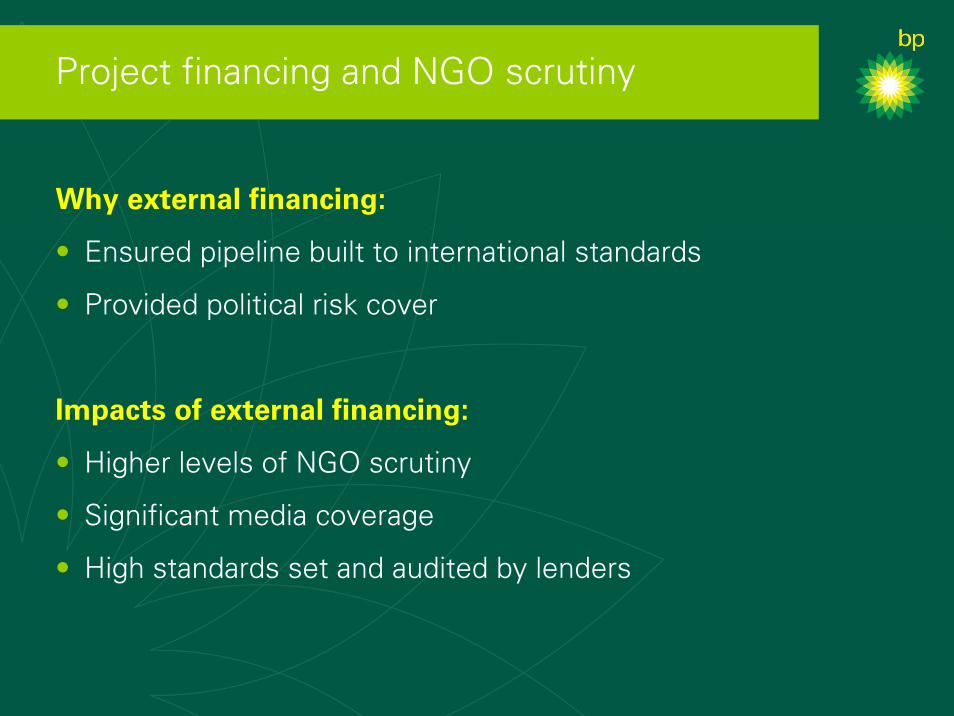

Project financing and NGO scrutiny

Why external financing:

•

•

Ensured pipeline built to international standards

Provided political risk cover

Impacts of external financing:

•

•

•

Higher levels of NGO scrutiny

Significant media coverage

High standards set and audited by lenders

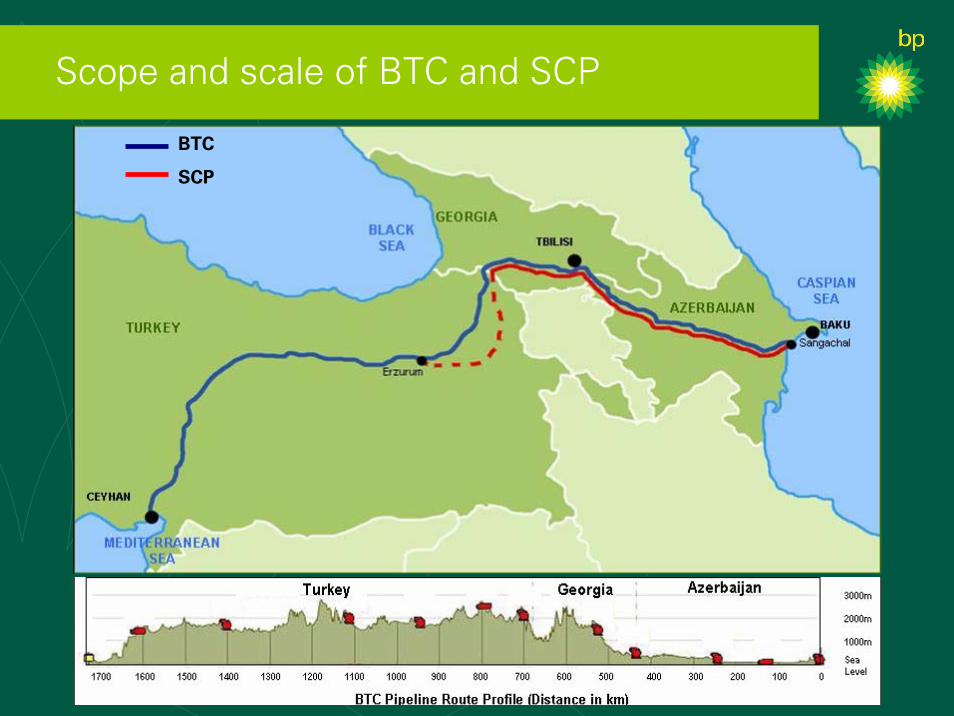

Scope and scale of BTC and SCP

BTC

SCP

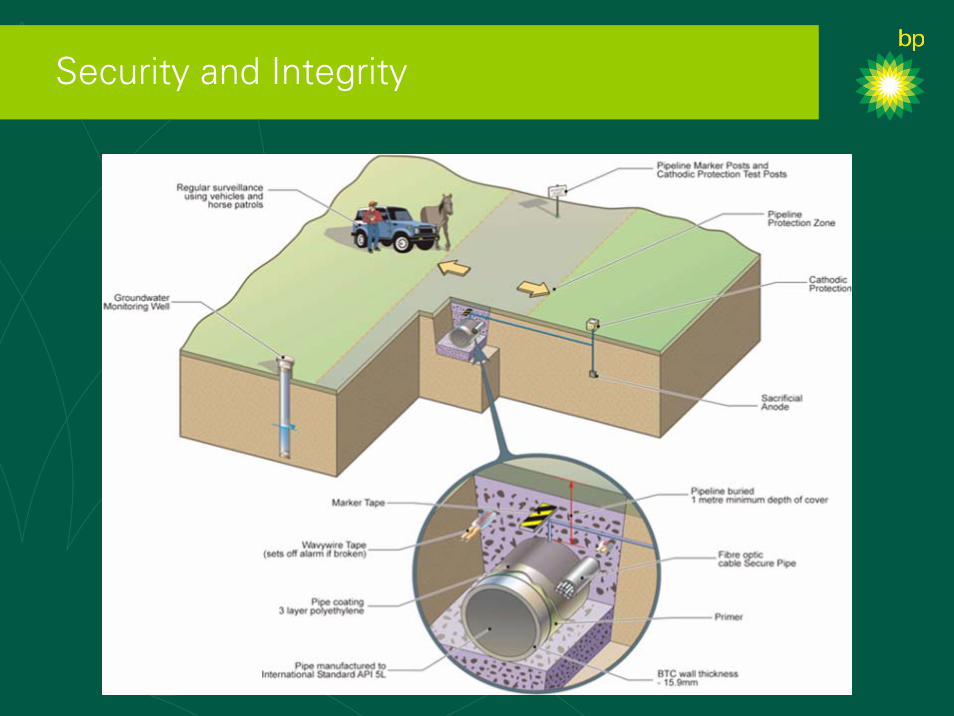

Security and Integrity

Unexploded ordinance on right of way

Mud volcano ridge

Digging for the pipe & block valve station

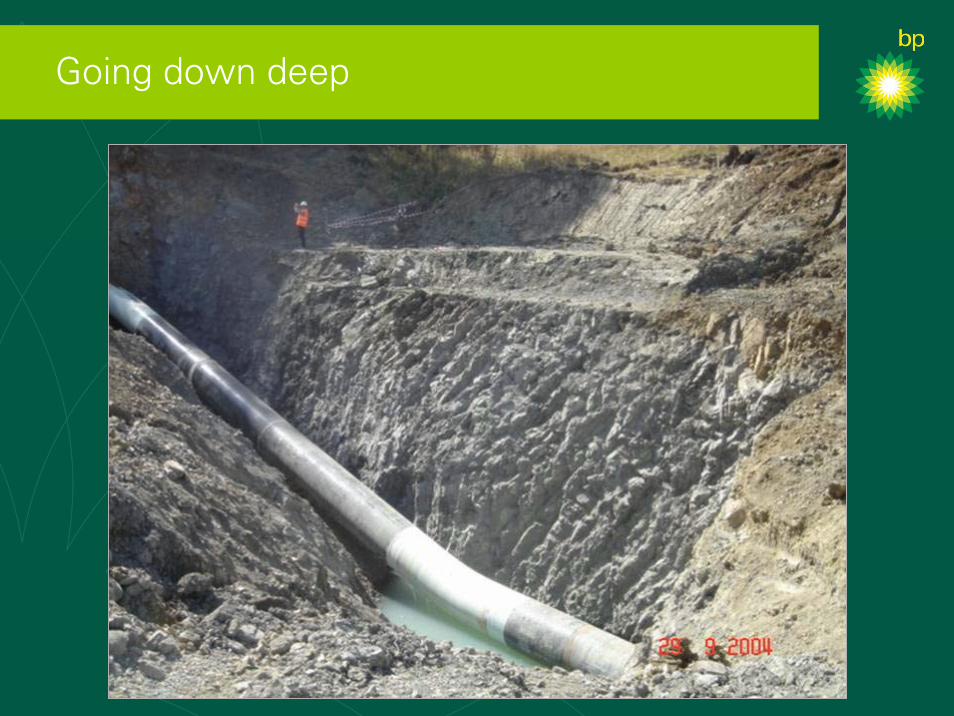

Going down deep

River crossing

Ridgeline construction – Turkey (and China)

Rock removal

Trench breakers and broken bones

Steep slope

Moving down

Nearly there…

The end in sight

The end in sight

Value through Technology

Fereidoun AbbassianTechnical Director

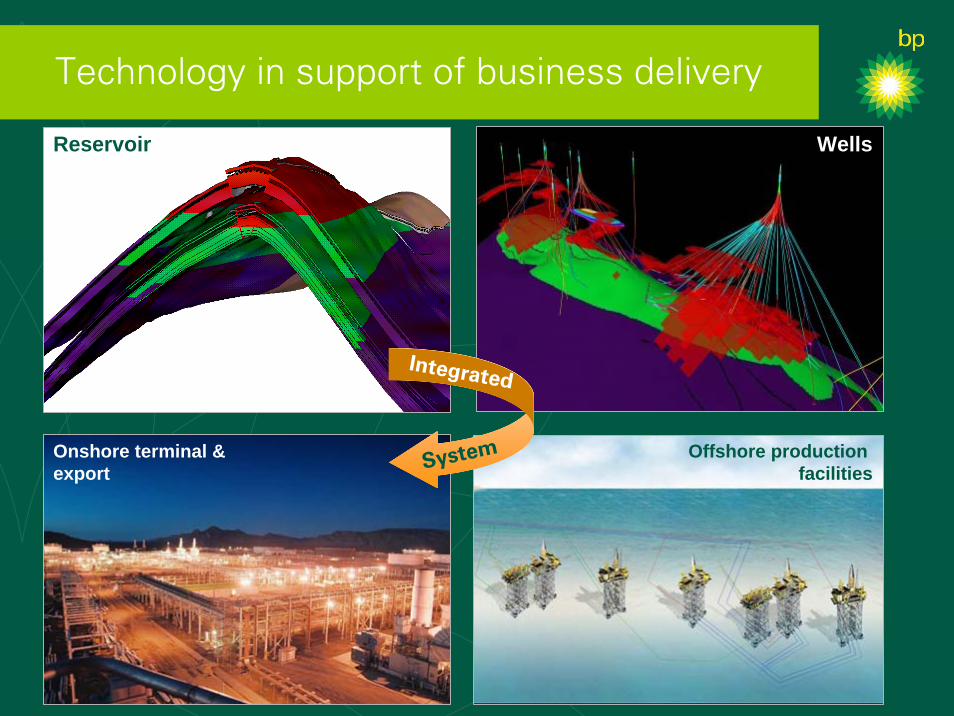

Technology in support of business delivery

Reserves pull-through

Maximising revenue

Capital efficiency

Technology in support of business delivery

Reservoir Wells

Onshore terminal &export

Offshore production facilities

Integrated

System

3500m

2000 -6000m

200-600 m

West Azeri Platform

Central Azeri Platform

Azeri reservoir structure

Well Trajectories3500m

2000 -6000m

200-600 m

West Azeri Platform

Central Azeri Platform

Azeri reservoir structure

Well Trajectories

Open hole gravel pack

Chirag 1 Platform ~ Well Profiles

A09zA06y

A12xA20 (plan)

A19 (plan)A18

A16 T3

A17 T2

A14zA09

A07

A11

A15z

A06

A08A10

A13

A05A12

A02A03

A04

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,0000 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000 5,500 6,000 6,500 7,000 7,500 8,000

Equivalent Departure (m)

TVD

BR

T (m

)

Conventional Well (Drilled)Conventional Well (Planned)ERD Well (Drilled)ERD Well (Planned)

ERD WellConventional Well

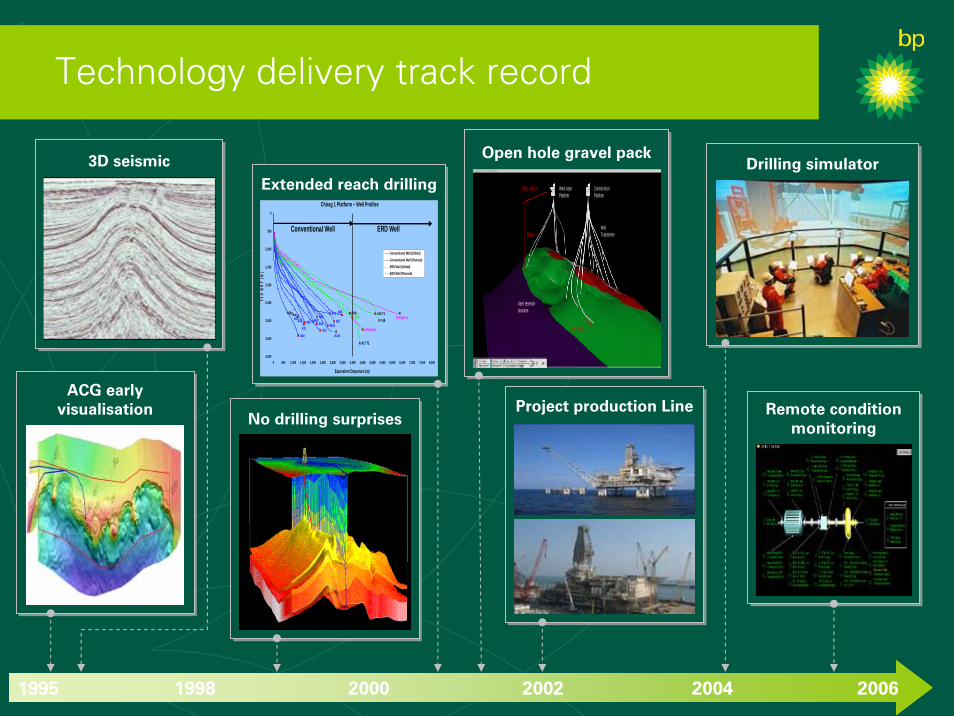

Extended reach drilling

ACG early visualisation

No drilling surprisesRemote condition

monitoring

Drilling simulator

Project production Line

1995 20061998 2000 2002 2004

3D seismic

Technology delivery track record

’’

Pereriv A

Pereriv B

Pereriv C

Pereriv D

Pereriv E

Water

Intelligent completions

Field of the Future™

ACE

Zonal flow monitoring

Zone ‘A’ Flow

Zone ‘B’ Flow

Zone ‘C’ Flow

Advanced seismic

Strategic technologies

Technology drivers

•

•

•

•

Reservoir management

New well delivery

D&C performance

Operating efficiency

Advanced seismic

Aim

• Monitor fluid movements inthe reservoir

BP’s position

• Technology leadership area

• Industry leader in 4-D life-of-field monitoring

Ocean bottom cable 4D seismic

Azeri reservoir management

CARSP: Phase 1Gas Cap

Water

OilDeep Water

Gunashli

Chirag Azeri

Depletion simulation for the Central Azeri

Water

Gas

Oil

’’

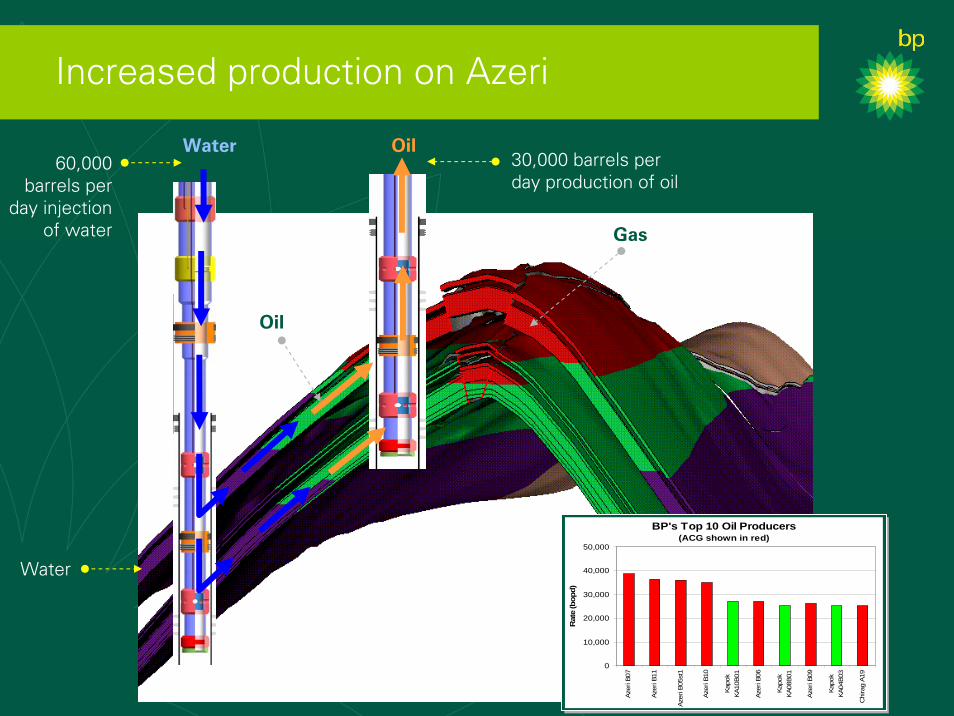

Down hole flow control valve

Expandable screen Pereriv A

Pereriv B

Pereriv C

Pereriv D

Pereriv E

Water

Intelligent completions

Aim

• Increased production with fewer wells

BP’s position

• Azerbaijan is leading BP and the Industry

Increased production on Azeri

Expandable Sand Screen

30,000 barrels per day production of oil

60,000 barrels per

day injection of water

Water Oil

Water

Oil

BP's Top 10 Oil Producers(ACG shown in red)

0

10,000

20,000

30,000

40,000

50,000

Azer

i B07

Azer

i B11

Azer

i B05

st1

Azer

i B10

Kapo

kKA

10B0

1

Azer

i B06

Kapo

kKA

08B0

1

Azer

i B09

Kapo

kKA

04B0

3

Chi

rag

A19

Rat

e (b

opd)

Gas

Zonal flow monitoring

Aim

• Real time monitoring of reservoir flow

BP’s position

• World leader in development and implementation of technology

Fibre-optic sensor technology

Time

Temperature

Dep

th

Real-time temperature data from Central Azeri well B04

Zone ‘A’ flow

Zone ‘B’ flow

Zone ‘C’ flow

Field of the Future TM

Cross discipline

collaboration

Monitoring real time data

Analysis/modeling

Offshore productionfacilities

Onshore terminals & exports

Wells

Reservoirs

Integration

Advanced CollaborationEnvironment

Decision making/people

BP’s Distinctive Caspian Presence

Rashid JavanshirVice President, Onshore Operations

Workforce capability

Professional Roles

ExpatsNational

2500

2000

1500

1000

500

02006 2007 2008 2009 2010

Forward projections: BP data

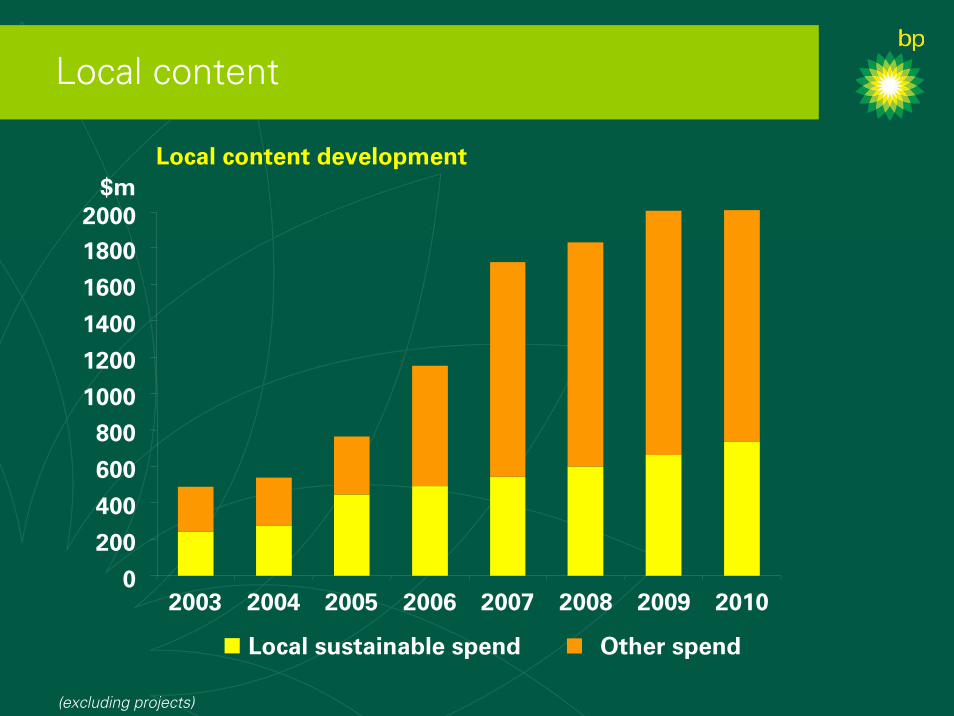

Local content

Other spend

$mLocal content development

Local sustainable spend

0

200

400

600

800

1000

1200

1400

1600

1800

2003 2004 2005 2006 2007 2008 2009 2010

2000

(excluding projects)

Capacity building

Commercial Structure &Financial Performance

Phil HomeCommercial Director

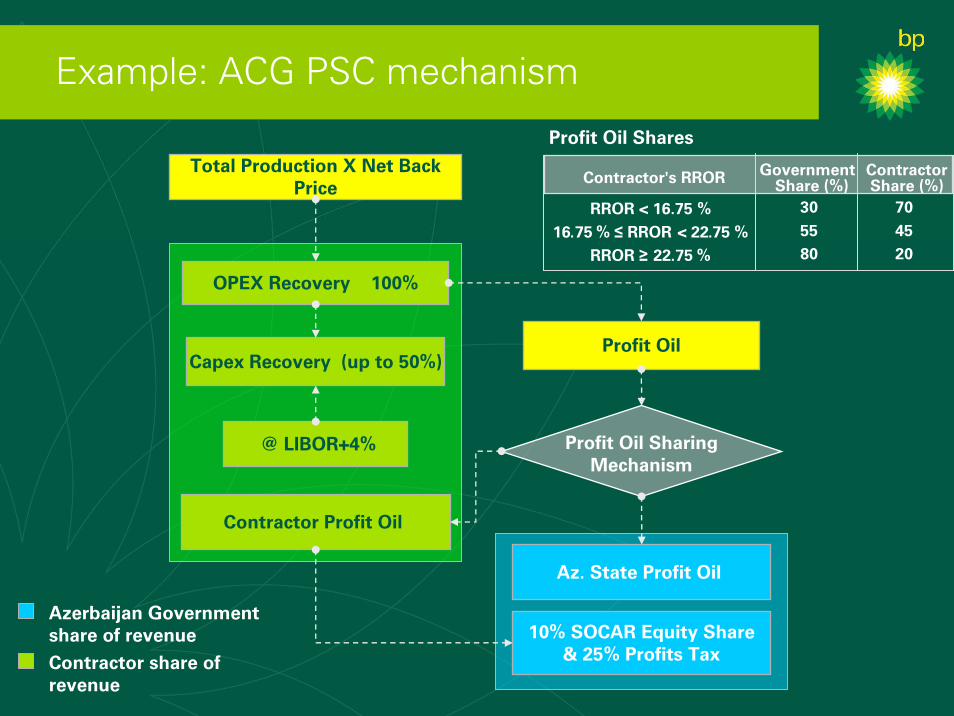

PSC terms – General principles

Duration• Exploration phase normally three years

with 2-3 well commitment• 25 year development phase with a five

year negotiable extension

Costs• FOCs (Foreign Oil Companies) pay all

costs, recovered as “cost oil”• Financing cost charged on unrecovered

Capex & Opex balances carried forward (e.g. @ LIBOR+4% in ACG PSC)

Production• “Profit oil” is shared between FOCs and

Azerbaijan State according to profit sharing mechanism [based on either RROR (Real rate of return) or R-factor]

• Unutilised associated gas is delivered at no cost to the State

Accounting & Fiscal• Accounting is in US Dollars• Azerbaijan profits tax rate is fixed for

duration of PSCs• No customs duty & VAT paid by FOCs

and contractors• PSCs contain Economic Stability clauses

Standards• PSCs apply international standards• Environmental and Social Impact

Assessments required for all projects

Example: ACG PSC mechanism

Total Production X Net Back Price

Profit Oil

@ LIBOR+4% Profit Oil SharingMechanism

Contractor Profit Oil

Az. State Profit Oil

10% SOCAR Equity Share& 25% Profits Tax

OPEX Recovery 100%

Capex Recovery (up to 50%)

Profit Oil Shares

Azerbaijan Government share of revenue

Contractor's RROR Government Share (%)

Contractor Share (%)

RROR < 16.75 % 30 70

16.75 % ≤ RROR < 22.75 % 55 45

RROR ≥ 22.75 % 80 20

Contractor share of revenue

Indicative price sensitivity: ACG

Gross production @ $25/bbl

FOC Profit Oil Share

Cost Oil

FOC Profit Oil

0

200

400

600

800

1000

1200

1400

1998 2001 2004 2007 2010 2013 2016 2019 2022

mb

d

0%

10%

20%

30%

40%

50%

60%

70%

80%

Az GovtProfit Oil

FOC Profit Oil

Cost Oil

Gross production @ $60/bbl

FOC Profit Oil Share

Cost Oil

FOC Profit Oil

0

200

400

600

800

1000

1200

1400

1998 2001 2004 2007 2010 2013 2016 2019 2022

mb

d

0%

10%

20%

30%

40%

50%

60%

70%

80%

Az GovtProfit Oil

FOC Profit Oil

Cost Oil

Source: BP data – indicative data based on current assumptions (currently sanctioned projects only)

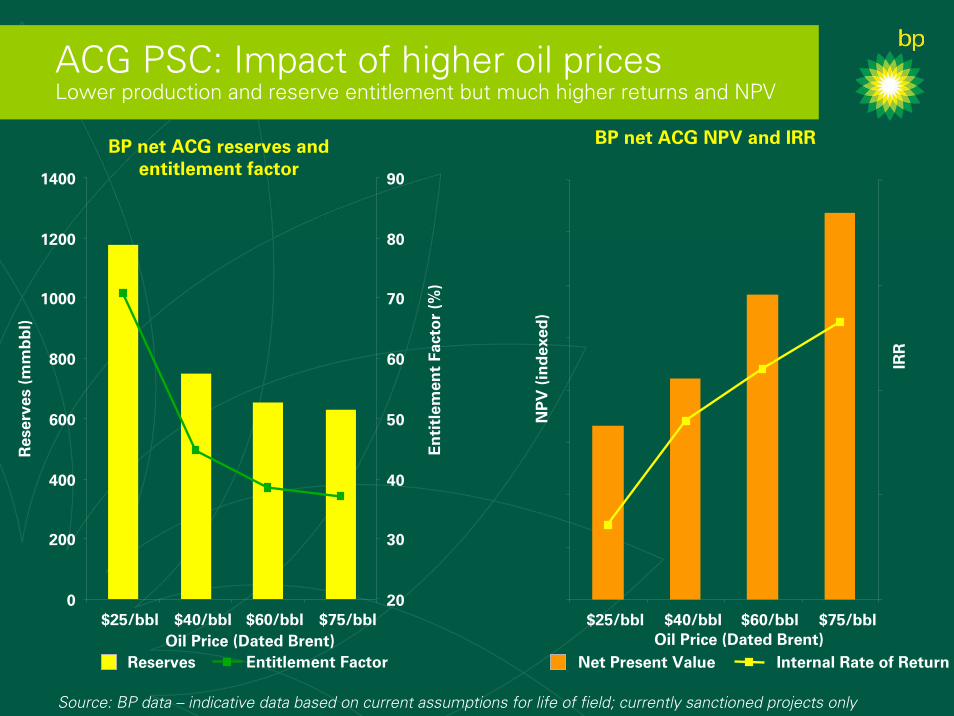

ACG PSC: Impact of higher oil pricesLower production and reserve entitlement but much higher returns and NPV

BP net ACG reserves and entitlement factor

$25/bbl $40/bbl $60/bbl $75/bblOil Price (Dated Brent)

Reserves Entitlement Factor

0

200

400

600

800

1000

1200

1400

Res

erve

s (m

mb

bl)

20

30

40

50

60

70

80

90

En

titl

emen

t Fa

cto

r (%

)

BP net ACG NPV and IRR

$25/bbl $40/bbl $60/bbl $75/bblOil Price (Dated Brent)

NP

V (

ind

exed

)

Net Present Value Internal Rate of Return

IRR

Source: BP data – indicative data based on current assumptions for life of field; currently sanctioned projects only

BP Azerbaijan net production

BP net production

@ $40/bbl @ $60/bbl

Production profiles include sanctioned developments only: Chirag, Central Azeri, West Azeri, East Azeri, Deep-Water Gunashli (DWG) and DWG East manifold in ACG, and Shah Deniz Stage 1

0

100

200

300

400

500

2005 2006 2007 2008 2009 2010

mbo

ed

Forward projections: BP data

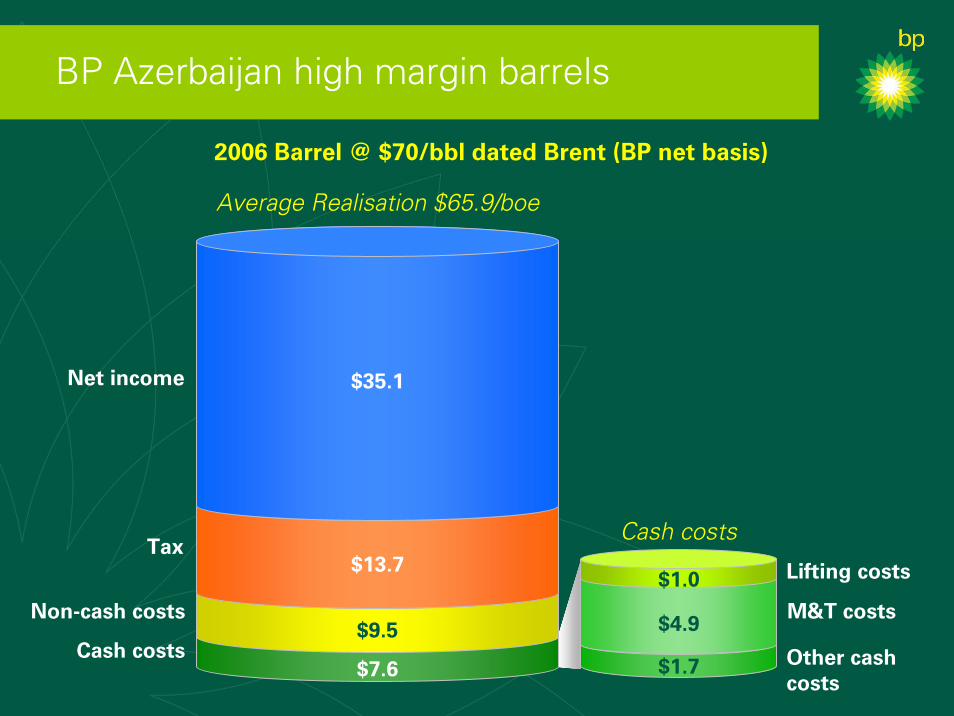

BP Azerbaijan high margin barrels

2006 Barrel @ $70/bbl dated Brent (BP net basis)

Net income

Tax

Non-cash costs

Cash costs$7.6

$9.5

$13.7

$35.1

Average Realisation $65.9/boe

$1.7

$4.9

$1.0 Lifting costs

M&T costs

Other cash costs

Cash costs

![[Waterworks] City Presentation - Baku(Azerbaijan)](https://static.fdocuments.us/doc/165x107/55862594d8b42a4c578b4632/waterworks-city-presentation-bakuazerbaijan.jpg)