AZEEZ, Nurudeen Oyebamiji PG/M.SC/09/54079 WORKING …...PG/M.SC/09/54079 WORKING CAPITAL MANAGEMENT...

112

1 AZEEZ, Nurudeen Oyebamiji PG/M.SC/09/54079 WORKING CAPITAL MANAGEMENT AND FIRMS PERFORMANCE: A STUDY OF MANUFACTURING COMPANIES IN NIGERIA FACULTY OF BUSINESS ADMINISTRATION DEPARTMENT OF ACCOUNTANCY Azuka Ijomah Digitally Signed by: Content manager’s Name DN : CN = Webmaster’s name O= University of Nigeria, Nsukka OU = Innovation Centre

Transcript of AZEEZ, Nurudeen Oyebamiji PG/M.SC/09/54079 WORKING …...PG/M.SC/09/54079 WORKING CAPITAL MANAGEMENT...

1

AZEEZ, Nurudeen Oyebamiji

PG/M.SC/09/54079

WORKING CAPITAL MANAGEMENT AND

FIRMS PERFORMANCE: A STUDY OF

MANUFACTURING COMPANIES IN NIGERIA

FACULTY OF BUSINESS ADMINISTRATION

DEPARTMENT OF ACCOUNTANCY

Azuka Ijomah

Digitally Signed by: Content manager’s Name

DN : CN = Webmaster’s name

O= University of Nigeria, Nsukka

OU = Innovation Centre

2

WORKING CAPITAL MANAGEMENT AND FIRMS PERFORMANCE: A

STUDY OF MANUFACTURING COMPANIES IN NIGERIA

BY

AZEEZ, Nurudeen Oyebamiji

PG/M.SC/09/54079

3

DEPARTMENT OF ACCOUNTANCY,

FACULTY OF BUSINESS ADMINISTRATION,

UNIVERSITY OF NIGERIA, ENUGU CAMPUS

AUGUST, 2015

WORKING CAPITAL MANAGEMENT AND FIRMS PERFORMANCE.

A STUDY OF MANUFACTURING COMPANIES IN NIGERIA.

4

AZEEZ, Nurudeen Oyebamiji

PG/M.SC/09/54079

BEING A DISSERTATION PRESENTED TO THE DEPARTMENT OF

ACCOUNTANCY, FACULTY OF BUSINESS ADMINISTRATION

UNIVERSITY OF NIGERIA, ENUGU CAMPUS.

IN PARTIAL FULFILMENT OF THE AWARD OF MASTERS OF SCIENCE IN

ACCOUNTANCY

SUPERVISOR: PROFESSOR (MRS.) UCHE MODUM

AUGUST, 2015

5

DECLARATION

This is to certify that this dissertation is an original work written by AZEEZ

NURUDEEN OYEBAMIJI Registration number: PG/MSc/09/54079. The

dissertation was submitted in partial fulfillment for the award of MSc in

Accounting in the department of Accountancy, University of Nigeria, Enugu

Campus and has not been submitted in part or full for any other diploma or degree

of this or any other University.

-------------------------------------------------------------------

AZEEZ, Nurudeen Oyebamiyi

PG/M.Sc/09/54079

6

APPROVAL PAGE

This is to certify that AZEEZ, Nurudeen Oyebamiji , a post graduate student in the

department of accountancy, faculty of Business administration, university of

Nigeria Enugu Campus (UNEC) with Registration Number PG/M.SC/09/54079,

has satisfactorily completed the requirements of Dissertation research in partial

fulfillment of the award of M.sc in accountancy of the University of Nigeria.

---------------------------- ---------------------------

Prof (Mrs.) Uche Modum Date

Supervisor

--------------------------- ---------------------------

Osita Aguolu (Reader) Date

(Head of Department)

7

DEDICATION

This work is dedicated to Allah (SWT) for His infinite mercies and grace.

8

ACKNOWLEDGEMENTS

I wish to express my profound gratitude to God almighty for His providence,

guidance and divine provision in making this educational sojourn a reality. To Him

be the glory.

I sincerely acknowledge the efforts of my supervisor, Prof (Mrs) Uche Modum for

her patience, advice, suggestions and constructive criticism which has not only led

to the completion of this work but has also improved my knowledge in research.

My appreciation goes to my uncle; engineer T.A Shittu for his immense

contribution towards my educational career. To my elder sister Mrs Kazeem Seidat

I. for her encouragement. To my friends and colleagues Mr Iorpev Luper of Benue

State University, Makurdi, Benjamin Yio and others for their support, I say many

thanks to you all.

Finally, I wish to acknowledge my dearest wife Hajia Azeez Dolapo Omowumi for

her steadfastness, support and prayers in making this struggle a success.

May God bless you all (Amen).

9

ABSTRACT

This study investigated the relationship between working capital management

measured by account receivable period (ACRP), inventory period (INVP), cash

conversion cycle (CCC) and sales Growth (SG) and profitability performance

measured by returns on assets (ROA). The study utilized secondary data obtained

from the annual financial statements of Nigerian Manufacturing companies listed

on the Nigerian Stock Exchange (NSE) for period 2008 – 2012. Multiple

regression model were adopted for testing all the hypotheses and the study result

reveals that there was a negative significant relationship between the account

receivable period and profitability of the Nigerian Manufacturing companies. It

also reveals that the profit is significantly influenced by the number of days

inventory were held (INVP) and that the profitability performance negatively and

significantly related to the cash conversion cycle (CCC). These results suggest that

effective policies must be formulated for the individual components of working

capital. Furthermore, efficient management and financing of working capital

(current assets and liabilities) can increase the operating profitability of

manufacturing firms

10

TABLE OF CONTENTS

Content Page

Title page - - - - - - - - - - i

Declaration - - - - - - - - - - ii

Approval - - - - - - - - - - iii

Dedication - - - - - - - - - - iv

Acknowledgements - - - - - - - - - v

Abstract - - - - - - - - - - vi

List of tables - - - - - - - - - xi

List of figure - - - - - - - - - xi

CHAPTER ONE : INTRODUCTION

1.1 Background to the Study - - - - - - 1

1.2 Statement of the Problem - - - - - - - 3

1.3. Objectives of the Study - - - - - - - 4

1.4 Research Questions - - - - - - - - 5

1.5 Research Hypotheses - - - - - - - 5

1.6 Scope of the Study - - - - - - - 6

1.7 Significance of the Study - - - - - - - 7

References - - - - - - - - - 8

CHAPTER TWO: REVIEW OF LITERATURE

2.0. Introduction - - - - - - - - 10

2.1. Conceptual Review - - - - - - - 10

2.1.0. Concepts of Working Capital Management - - - - 10

11

2.1.1. Working Capital - - - - - - - - 10

2.1.2. Working Capital Management - - - - - - 12

2.1.3 Working Capital Management Efficiency - - - - - 13

2.1.4. Policy of Working Capital - - - - - - - 13

2.1.5. Working Capital Cycle - - - - -- - - 16

2.1.6. Components of Working Capital Management (WCM) - - - 18

2.1.7. Cash Management - - - - - - - - 19

2.1.8 Cash Positioning - - - -- - - - - 22

2.1.9 Cash Flow Volatility, Earnings Volatility and Firm Value. - - 23

2.1.10 Cash Budget - - - - - - - - - 25

2.1.11. Management of Cash Receivables - - - - - 26

2.1.12. Credit Standards - - - - - - - - 26

2.1.13. Credit Extension Policy - - - - - - - 27

2.1.14. Credit Collection Policy - - - - - - - 28

2.1.15. Inventory (Inv) Management - - - - - - 29

2.1.16. Need to Hold Inventory - - - - - - - 30

2.1.17 Inventory Control - - - - - - - - 31

2.1.18. The Economic Order Quantity (EOQ) - - - - - 31

2.1.19. Re-Order Point - - - - - - - - 32

2.1.20. Relation to Financial Management - - - - - 32

2.1.20.1. Payables Management - - - - - - - 33

2.1.21. Receivables Management - - - - - - - 33

2.1.22. Cash Conversion Cycle (CCC) Management - - - - 34

12

2.1.23. Measures of Profitability - - - - - - - 34

2.1.24. Liquidity - - - - - - - - - 36

2.1.25. Nature of Working Capital - - - -- - - - 37

2.1.26. Trade-Off between Profitability and Risk - - - - 37

2.1.27. The Efficient Management of Firm’s Working Capital - - 38

2.1.29 . The Consequences of Inefficient Management of Working Capital 39

2.1.30. The Costs and Benefits of Firm’s Investments in Working Capital - 44

2.1.31. The Nigerian Economy and Working Capital Management of Quoted

Firms in Nigeria =- - - - - - - - 46

2.20. Theoretical Review - - - - - - - - 47

2.2.1. The Operating Cycle Theory - - - - - - 48

2.2.2. The Cash Conversion Cycle (CCC) Theory - - - - 48

2.2.3. The Pecking Order Theory - - - - - - - 49

2.2.4 Agency Theory - - -- - - - - - 50

2.2.5. The Risk –Return Trade-Off Theory - - - - - 51

2.3.0. Review of Empirical Studies - - - - - - 51

2.3.1. Summary of Literature Review - - - - - 57

References - - - - - - - - - - 58

CHAPTER THREE: METHODOLOGY

3.0 Introduction - - - - - - - - - 60

3.1 Research Design - - - - - - - - 60

3.2 Population of the Study - - - - - - - 61

3.3 Sampling Techniques and Sample Size - - - - - 61

13

3.4 Sources of Data Collection - - - - - - - 61

3.5 Variables Used for the Study - - - - - - 62

3.5.1 Dependent Variable - - - - - - - - 62

2.5.2 Independent Variables - - - - - - - 63

3.6 Data Analysis Techniques - - - - - - - 65

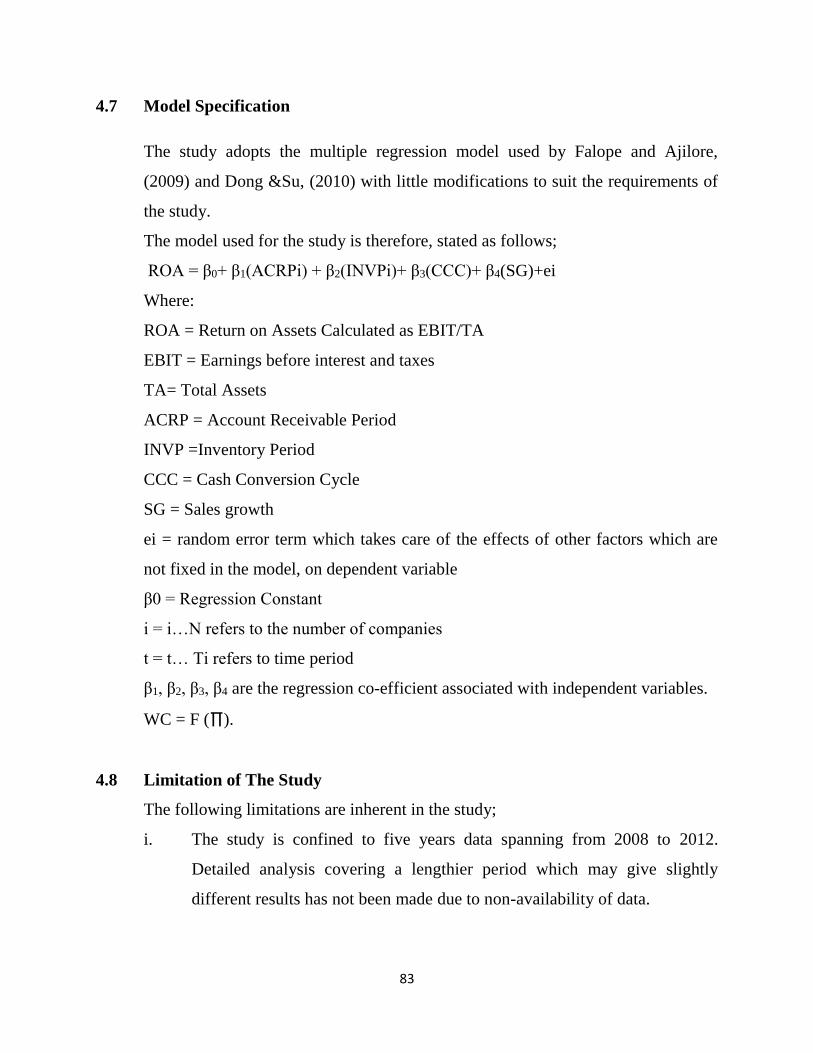

3.7 Model Specification - - - - - - - 66

3.8 Limitation of the Study - - - - - - - 66

References - - - - - - - - - 68

CHAPTER FOUR: DATA PRESENTATION, ANALYSIS AND

INTERPRETATION

4.0 Introduction - - - - - - - - 69

4.1. Presentation and Analysis of Multiple Regression Results - - 70

4.2. Data Validity Test - - - - - - - - 71

4.3. Summary of Regression Results - - - - - 72

4.4. Testing of Research Hypotheses - - - - - 73

4.5. Interpretation of results and discussion of findings - - - 75

4.5.1. The Impact of ACRP on Profitability - - - - 75

4.5.2. The Impact of Inventory Period (INVP) on Profitability - - - 75

4.5.3. The Impact of Cash Conversion Cycle (CCC) on Profitability - 76

4.5.4. The Impact of Sales Growth (SG) on Profitability - - - 76

CHAPTER FIVE: SUMMARY, CONCLUSIONS AND RECOMMENDATIONS

5.1. Introduction - - - - - - - - 78

5.2. Summary - - - - - - - - - 78

5.3. Conclusions - - - - - - - - - 80

5.3.1 Policy Implication - - - - - - - - 81

5.4. Recommendations - - - - - - - - 81

5.5. Suggestions for Further Research - - - - - - 82

14

Bibliography - - - - - - - - - 83

Appendices - - - - - - - - 86

15

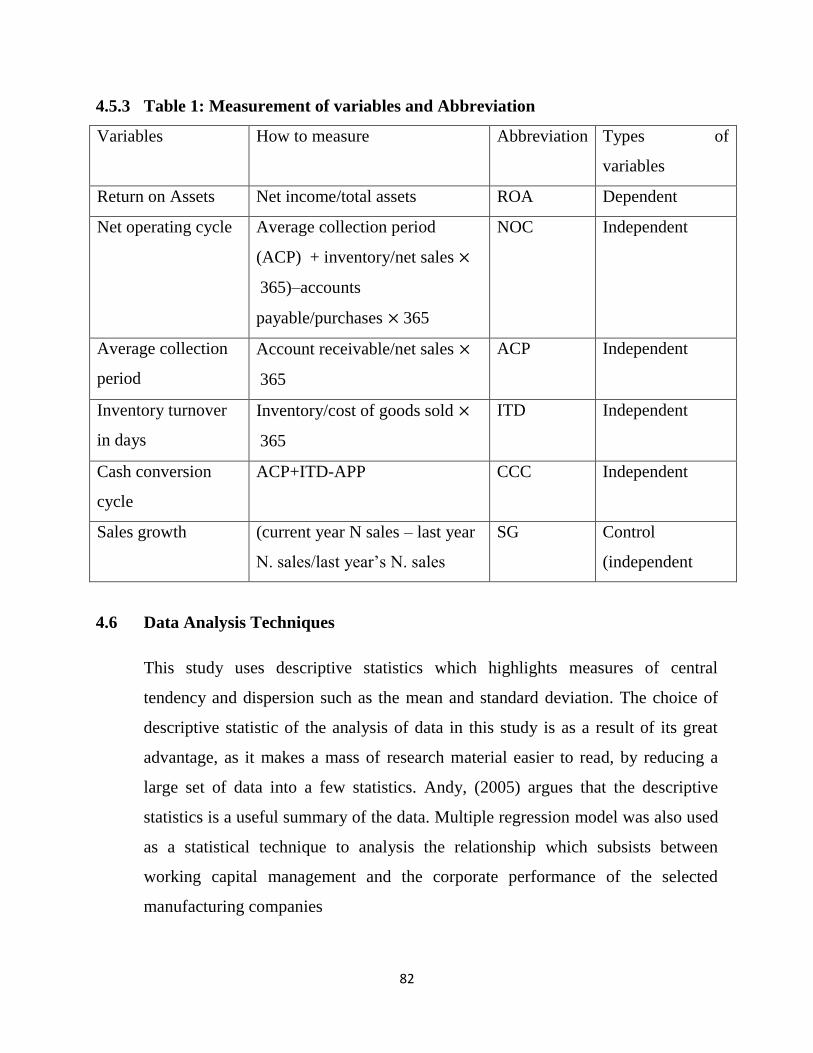

LIST OF TABLES

3.1.1.1 Table 1: Measurement of variables and Abbreviation - - 65

Table 1: Regression results showing Data Estimate effects of WCM on ROA 70

Table 2: Summary of Regression Results for the Study Model - - 72

16

LIST OF FIGURES

Fig. 2.1 Working Capital Cycle: Source from JPMorgan (2003)

Fleming International Cash Management Survey in

conjunction with the ACT - - - - - - 17

17

CHAPTER ONE

INTRODUCTION

1.1 Background To The Study

Working Capital management of a firm, which deals with the management of

current assets and current liabilities, has been recognized as an important area in

financial management. Working capital (WC) refers to the firm’s investment in

short-term assets. Pandey, (2005) classified working capital into gross and net

concepts. He defined gross working capital as the firm’s investment in current

assets. Current assets are the assets which can be converted into cash within an

accounting year and these include; cash, short-term securities, debtors, bills

receivables and stocks. He described net working capital as the difference between

current assets and current liabilities. Current liabilities are those claims of

outsiders, which are expected to mature for payment within an accounting year.

These include trade creditors, bills payable, bank overdraft and short- term loan.

Home van, (2000) described working capital management as involving the

administration of these assets namely cash, marketable securities, receivables and

inventories and the administration of current liabilities.

Management of these short-term assets and liabilities is important to the financial

health of business of all sizes. This importance is hinged on the fact that the

amounts invested in working capital are often high in proportion to the total assets

employed and therefore warrants a careful investigation (Smith, 1980). Working

Capital therefore, should neither be more nor less, but just adequate for the smooth

running of a firm. While excess amount of working capital results in the reduction

of firm’s profitability, holding of inadequate amount of it leads to lower levels of

the firm’s liquidity and stock outs resulting in difficulties in maintaining smooth

operation (Krueger, 2002).

18

Business success, therefore, heavily depends on the ability of the financial

managers to effectively manage accounts receivable, inventory and account

payable (which are component of working capital) (Filbeck and Krueger, 2005).

Firm can reduce their financing costs and or increase the funds available for

expansion of project by minimizing the amount of investment tied up in current

assets (Home Van Wachowicz, 2004). For this reasons, most of the financial

manager’s time and efforts are spent in identifying the non-optimal levels of

current assets and liabilities and bringing them to optimal levels (Lamberson,

1995). An optimal level of working capital is the one in which a balance is

achieved between risk and efficiency. To maintain the optimal level of various

components of working capital, continuous monitoring is required (Afza and

Nazir, 2009).

A poor or inefficient working capital management leads to tie up funds in idle

assets and reduces the liquidity and profitability of a company (Reddy &

Kameswar, 2004). Siddart & Das (1993), states that the major reason for slow

progress of an undertaking is shortage or wrong management of working capital.

Deloot (2003: 573), states that “there is a significant relationship between gross

operating income and number of days of account receivable, inventories and

accounts payables”. The relationship between accounts payable and profitability is

consistent with the view that less profitable firms wait longer to pay their bills.

Considering the importance of Working Capital Management therefore, the

researcher focused on evaluating the Working Capital Management and

profitability relationship like other similar works such as Uyar, 2009; Samiloglu

and Demirgune 2008; Vishnani and Shah, 2007; Tervel and Solano, 2007;

Lazaridis and Tryfonidis, 2006; Padachi, 2006; Shin and Soenen, 1998; Smith et

al, 1997 and Jose et al, 1996. However, there are a few studies with reference to

19

Nigeria in respect of the subject. Like Akinsulire, 2005, Falope,, 2009, Ajilore,,

2009 etc.

Most of these studies focused on the Working Capital Management financing

policies. Shah and Sana (2006) concentrated on the oil and gas sector and

estimated the relationship using small sample of 7 firms. Raheman and Masr

(2007) analyzed profitability and Working Capital Management performance of

94 firms listed on Karachi Stock Exchange for the period 1999-2004 by using

ordinary least square and generalized least square. However, this study ignored the

fixed effect of each firm as each firm has its unique characteristics and also

ignores sector-wise analysis of Working Capital Management performance of

manufacturing firms. Insufficient evidences on the firm’s performance and

Working Capital management with reference to Nigeria therefore, provide a strong

motivation for evaluating the relationship between working capital management

and firm’s performance in detail. This study therefore, explores the various way of

measuring Working Capital components and relates them to the performance of

the Nigerian manufacturing sector.

1.2 Statement Of The Problem

There has been a growing number of studies that examined the relationship

between working capital and corporate profitability in the recent time (Shin and

Soenen, 1998; Deloof, 2003; Fildbeck and Krueger, 2005; Falope, 2009; .Jinadu,

2010). Justification for this common efforts centered on the relationship between

efficiency in working capital management and firms profitability and its

implications on shareholder’s value. Most of these studies were however, centered

on large firms operating within well developed money and capital market of

developed economies and did not consider the fact that the amount of working

capital required varies across industries and indeed firms depending on the nature

20

of business, scale of operation, production cycle, credit policy, availability of raw

materials etc (Ghosh and Maji; 2004).

It is regrettable to note that in spite of these huge literatures in this area, many

firms had crashed, more especially manufacturing sector of the Nigerian economy

in which application of working capital is more pronounced (Jinadu, 2009). In

addition, some promising investments with high rate of return are failing and

being frustrated out of business because of inadequacy of working capital. Many

factories had been either temporarily or completely shot down because they could

not meet their financial obligations as at when due because they were not liquid.

Many Nigerian workers had been forcefully thrown into unemployment market

and frustratingly became dependent on relations as a result of the aborted mission

of their organization caused by poor attention given to the management of working

capital . Unfortunately, Nigeria capital and money markets are not really helping

to ameliorate the problem, instead, more often than not; they compound the

problem by creating bottleneck with harsh conditions that could not be easily met

by the companies that are at the verge of collapse.

The problem then arises as to how managers of these manufacturing organization

could be encouraged to pay more attention to the management of their working

capital. In other words, how could working capital be managed in order to impact

positively on firms performance.

1.3 Objectives Of The Study

The main objective of this study is to investigate the relationship between working

capital management and the corporate performance (profitability) of the Nigerian

manufacturing companies. While the specific objectives of the study are to: -

i. investigate the relationship between the accounts receivable period (as a measure

of WCM) and profitability of manufacturing companies in Nigeria.

21

ii. investigate the relationship between inventory period (as a measure of WCM) and

profitability of manufacturing companies in Nigerian.

iii. investigate the relationship between cash conversion cycle period (as a

comprehensive measure of checking the efficiency of WCM) and profitability of

manufacturing companies in Nigeria.

1.4 Research Questions

In a bid to actualize the research objectives, the following research questions have

been formulated which serve as a guide in the researcher’s quest for answers.

These questions are;

i. What is the significant relationship between the accounts receivable period

(ACRP) and profitability of Nigerian manufacturing companies?

ii. What is the significant relationship between the inventory period (INVP)

and profitability of Nigerian manufacturing companies?

iii. To what extent is the relationship between cash conversion cycle (CCC)

and profitability of manufacturing companies in Nigeria?

iv. To what extent does the effective management of working capital affect the

profitability of the Nigerian manufacturing companies?

v. What level of working capital is optimal and desirable?

vi. To what extent has the inadequacy of working capital affect the profitability

of the Nigerian manufacturing companies

1.5 Research Hypotheses

A hypothesis is a conjecture or a prediction of what can be seen in the world of

reality and this prediction is made from the world of theory. It is a tentative

statement about the relationships that exist between two or among many variables

(Asika, 2005).

22

To provide an empirical support to the relationship between working capital

management and profitability of the Nigerian manufacturing companies, three

hypotheses have been formulated and stated in their null forms as follows:

HO1: There is no significant relationship between the accounts receivable

period (ACRP) and profitability of Nigerian Manufacturing

Companies

HO2: There is no significant relationship between the inventory period

(INVP) and profitability of Nigerian Manufacturing Companies

HO3: There is no significant relationship between the cash conventions

cycle (CCC) and profitability of Nigerian Manufacturing Companies

1.6 Scope Of Study

The scope of the study enables the researcher to circumscribe his/her research

within a manageable limit (Asika, 2005).

In this research work, an attempt is made to explore the relationship between

working capital management and firm’s performance for twenty (20)

manufacturing firms out of the 134 manufacturing firms listed on the Nigerian

stock exchange for the period 2008-2012. The twenty (20) manufacturing firms

were selected based on the following criteria:

Companies must remain listed on the Nigerian Stock Exchange (NSE)

during the 2008 – 2012 periods.

Companies must have complete financial statements for the period under

review.

Companies must be operational within the period under investigation.

Manufacturing organizations were so taken into consideration since they play a

very important role in the Nigerian economy.

23

1.7 Significance Of The Study

This study is very crucial as it will give the financial managers of these

manufacturing organizations, better insights on the need to pay particular attention

to the effective and efficient management of their working capital. They will be in

a better position to be able to design and implement strategies and policies that

are aim at stabilizing and managing the various components of working capital

especially as it significantly impact on the main aim of business which is creating

shareholders’ value.

The study would further, enable the management to know at what extend they

should increase their liquidity in order to make their performance up to the mark.

This is very important in improving the good will of their firms, since firms that

pay creditors as at when due are considered credit worthy and gains a good

reputation.

And for the academic purposes, the research work will contribute to the existing

body of knowledge on working capital management and firm’s performance.

Finally, it is expected that the study will serve as a source of information to

students undergoing research work of this nature in the future.

24

REFERENCES

Afza, T. and Nazir, M. (2009). “Impact of aggressive working capital management policy

on firm’s profitability”. The IUP Journal of Applied Finance, 15 (8), 20 – 30.

Akinsulire, O. (2005). Financial management. Lagos: El-Toda Ventures.

Deloof, M. (2003). “Does working capital management affect profitability of Belgium

firms”? Journal of Business Finance and Accounting, 30 (3), 573-588.

Falope, O.I. and Ajilore, O.T. (2009). “Working capital management and corporate

profitability: Evidence from Panel Data Analysis of selected quoted companies in

Nigeria”. Research Journal of Business Management, 3(3)73-84.

Filbeck, G. and Krueger, T. (2005). “Industry related differences in working capital

management”. Mid-American of Business, 20(2), 11-18.

Filbeck, G., Krueger, T. and Preece, D. (2007). “CFO magazine’s working capital

surveys: Do selected firms work for shareholders”? Quarterly Journal of Business

and Economics, 46(2)3-22.

Krueger, T. (2002). “An analysis of working capital management results across

industries”. Mid-American Journal of Business, 20(2), 11 – 18.

Lamberson, M. (1995). “Changes in working capital of small firms in relation to changes

in economic activity”. Journal of Business, 10(2), 45-50.

Lazaridis, I. and Tryfonidis, D. (2006). “Relationship between working capital

management and profitability of listed companies in the Athens Stock Exchange”.

Journal of Financial Management and Analysis, 19(1)26-35.

Ohikhena, P. (2006). Research methodology in the social and management sciences.

Lagos, Nigeria: Bunmico Publishers.

Oxford (2005). A dictionary of accounting, 3 ed. Oxford University Press.

Pandey, I.M. (2005). Financial management, 9 ed. New Delhi Vikas Publishing House

PVT Ltd.

Padachi, K. (2006). “Trends in working capital management and its impact on firm’s

performance: An analysis of Mauritian small manufacturing firms”. International

Review Business Research Papers, 2(1), 45-56.

25

Prasad, R.S. (2001). “Working capital management in the paper industry”. Finance India,

15(1),185-188.

Shin, H.H. and Soenen, L. (1998). “Impact of working capital and corporate

profitability”. Journal of Finance Practice and Education, 8(2)37-45.

Smith, K. (1980). Profitability versus liquidity trade offs in working capital management,

in readings on the management of working capital. New York, St. Paul: West

Publishing Company.

VanHorne, J.C. (1977). “A risk-return analysi8s of a firm’s working capital position”.

Financial Economics, 2(1)71-88.

VanHorne, J.C. and Wachowiez, J.M. (2004). Fundamentals of financial management, 12

ed. New York: Prentice Hall.

26

CHAPTER TWO

REVIEW OF RELATED LITERATURE

2.0. Introduction

The aim of this research work is to examine the impact of Working Capital

Management on the performance of Nigerian manufacturing companies listed on

the Nigerian Stock Exchange (MSE). This chapter reviews the related literature in

respect of the subject matter under investigation and it is divided into five (5)

sections as shown below:

2.0. Introduction

2.1. Conceptual Review

2.2. Theoretical Review

2.3. Empirical Review

2.4. Summary

2.1. Conceptual Review

2.1.0. Concepts of Working Capital Management

2.1.1. Working Capital

Many authors have different perceptions about the concept “Working Capital”.

Falope and Ajilore (2009) regard working capital as the firm’s investment in short

term assets. To Akinsulire (2005), working capital is viewed as the items that are

required for the day to day production of goods to be sold by a company.

An understanding of the concept of working capital cycle will give appreciation

for the study of relationship between capital and firm’s performance. Weston

(1998) described working capital or cash operating cycle as the total length of time

required to complete the following sequence of events:

27

Conversion of cash into raw materials

Conversion of raw materials into work in progress

Conversion of work in progress into finished goods

Conversion of finished goods into debtors through sales and

Conversion of debtors into cash

Pandey (2005), however argues that working capital is a tow faced concept- gross

and net WC. He defined gross WC as the firm’s investment in current assets while

the net WC is the difference between current assets and current liabilities. Net WC

can be positive or negative. It will be positive if current assets are more than

current liabilities and negative when current assets are less than current liabilities.

Efficient management of working capital is very essential in the overall corporate

strategy in creating shareholders value (Afza & Nazir, 2009). Agreeing with the

view of Afza and Nazir, Eljelly (2004) states that working capital management

involves planning and controlling current assets and current liabilities in a manner

that eliminates the risk of inability to meet due short term obligations on one hand

and avoid excessive investment in current assets on the other hand.

Padachi (2006) opines that the management of working capital is important to the

financial health of businesses of all sizes. This is because, first, the amounts

invested in working capital are often high in proportion to the total assets

employed and so it is vital that these amounts are used efficiently. Secondary, the

management of working capital directly affects the liquidity and the profitability

of firms and consequently their net worth (Smith, 1980).

Agreeing with the view of Padachi (2006), Raheman and Nasir (2007) consider

working capital management as striking a balance between the two objectives of a

firm, that is, profitability and liquidity. They posited that firms must strive to

28

maximize profits and enhance shareholders wealth but at the same time not

sacrifice their liquidity which is necessary for smooth operations and most

importantly, corporate survival. To achieve this dual objective of working capital

management, most of the financial manager’s time and efforts are consumed in

identifying the non-optimal levels of the various components of working capital

and bringing them to optimal levels (Lamberson, 1995). The optimal level of

working capital components, which is a balance between risk and efficiency, is

maintained by continuous monitoring of the various components of working

capital (Afza & Nazir, 2009).

The basic objective of working capital management therefore is to ensure that a

firm’s current assets and current liabilities are maintained at a satisfactory level.

That is, to avoid neither more nor less working capital but to ensure that is just

adequate (Dong & Su, 2010). Agreeing with the view of Dong and Su, VanHorne

and Wachomicz (2004) observed that excessive level of current assets may have a

negative effect on a firm’s profitability; where as a low level of current assets may

lead to low level of liquidity and stock-outs thereby resulting in difficulties in

maintaining smooth operations.

For this work, suffice it to state that working capital management is all managerial

decisions taken by financial managers in maintaining a balance between liquidity

and profitability while conducting the day to day operations of a business concern.

The task of maintaining this balance, however, requires continuous monitoring of

the optimal levels of the various components of working capital.

2.1.2. Working Capital Management

Working capital management is the functional area of finance that covers all the

current accounts of the firm. It is concerned with the management of the levels of

29

the individual components of the working capital (Loneux, 2004). The basic

objective of working capital management is to manage firms’ current assets and

current liabilities in such a way that working capital is maintained at a satisfactory

level (Dong & Su, 2010).

Therefore, in this study, working capital management can be referred to as actions

taken by managers in maintaining a balance between liquidity and profitability

while conducting the day-to-day operations of a business concern.

2.1.3 Working Capital Management Efficiency

Efficient management of working capital has been defined by Ghosh and Maji

(2004) as the management of various components of working capital in such a

way that an adequate amount of working capital is maintained for the smooth

running of a firm and for fulfillment of twin objectives of liquidity and

profitability.

Modern financial management aims at reducing the level of current assets without

ignoring the risk of stock outs, to an optimal level (Bhattacharya, 1997).

2.1.4. Policy of Working Capital

The policy of working capital in accordance to Weston et al position is concerned

with two sets of relationship among balance sheet items. Firstly, the policy

question about the degree of total current assets to be held. Though current assets

vary with sales, it should be noted that the ratio of current assets to sales becomes

a policy issue. A company may hold relatively little proportion of stocks of current

assets if it elects to operate aggressively. Such move is to lower the required level

of investment and enhance the expected rate of return on investment. Thus, due to

excessive tough credit policy, such aggressive policy may as well enlarge the

possibility of running out of inventories and cash or sales loss.

30

The connection/relationship between types of assets and means such assets are

financed is the second policy question. One policy requests for harmonizing asset

and liability maturities: financing short term assets with short term debt, and long

term assets with long term debt or equity. If such policy is implemented, the

maturity formation of debt is resolved by considering fixed versus current assets.

Meanwhile, short-term debt is often less expensive to long term debt. This implies

that the expected rate of return may be more if short term debt is employed.

By offsetting the return advantage shows that huge proportion of short term credit

amplifies the risks as follows:

First, having to renew this debt at much higher interest rates

Second, not being able to renew the debt at all whenever the company goes

through tough times.

Both areas of working capital policies entail risk/return tradeoffs. Therefore, the

need to work-out a modality to establish the best possible levels of each type of

current assets to hold, and the substitute methods to finance them is necessary. The

procedure of accomplishing these optimal conditions is what may be termed as

working capital management.

As pointed out by Shin and Soenen (1998) that Wal-Mart and K-Mart had

comparable capital formations in 1994, but K-Mart’s poor management of

working capital contributed to its going bankrupt. This is because K-Mart had a

cash conversion cycle of about 61 days whereas Wal-Mart had a shorter

conversion cycle of 40 days instead. K-Mart was with faced an extra $193.3

million per year financing costs arising from long-term conversion cycle.

31

As pointed out in their 2005 U.S. survey report, there is a high positive correlation

between the efficiency of a corporation’s working capital policies and its return on

invested capital.

Hence, Nunn (1981) employs the PIMS database to study the reason for some

product lines having small working capital requirements, whereas some product

lines are having large working capital requirements. Moreover, Nunn has much

interest in permanent rather than temporary working capital investment since he

employed data averaged over four years. By employing factor analysis, he’s able

to identify factors connected with the production, sales, competitive position and

industry.

While highlighting the function of industry practices on firm practices, Hawawini,

Viallet, and Vora (1986) observe the influence of a company’s industry on its

working capital management. They resolved that there is a greater industry

consequence on company working capital management practices which is stable

over time; having used data on 1,181 U.S companies over the period 1960 to 1979.

Their studies arrived at the conclusion that sales growth and industry practices are

essential issues that influence company’s investment in working capital.

The review above depicts that there are models to illustrate the way working

capital refers to a company’s investment in short term assets-cash, short-term

securities, accounts receivable, and inventories. Though, these assets are financed

by short- term liabilities. Thus, net working capital is current assets less current

liabilities.

Van Horne (1986) submitted that working capital management is a misnomer; if

the working capital of the company is not managed. The term he stressed describes

a set of management decisions that affect specific types of current assets and

32

current liabilities. In turn, those decisions should be rooted in the overall valuation

of the company.

This submission does not disagree with the substance of the postulations of

Weston et al. Thus, it strengthens their arguments that the idea of working capital

management must do with those management decisions which border on balancing

of risk/return tradeoffs for current asset holdings and the liabilities that create

those assets.

Weston et al then advised that working capital should be considered as an

investment no less important that equipment and materials. They both argued that

current assets embody more than half the total assets of a business, and since the

investment is relatively volatile, it is worthy of careful consideration.

They argued that it is even more so for the small business. The small business may

lower its investment in fixed assets by renting or leasing plant and equipment, but

there is no way it can avoid an investment in cash, inventories and receivables.

Further, since small and medium companies have relatively limited access to the

long-term capital markets, it must necessarily rely heavily on trade credit and

short- term bank loans, both of which affect net working capital by increasing

current liabilities

2.1.5. Working Capital Cycle

In a business cycle, cash flows into, around and out of the business. Cash is life

blood of a business, and a manager's key mission is to assist in keeping it to flow

and to take the advantage of the cash-flow in making profits. A business that is

operating profitably, in theory is generating cash surpluses. If it does not generate

surpluses, then the business ultimately will run out of cash and expire.

33

The more speedily the business gets bigger the further cash it will need for

working capital and investment. The cheapest and best sources of cash exist as

working capital right within business. Better management of working capital

generates cash, and will assist in improving profits and lessen risks. Hence, it is

imperative to note that the cost of offering credit to customers and holding stocks

may signify a significant percentage of a company's total profits.

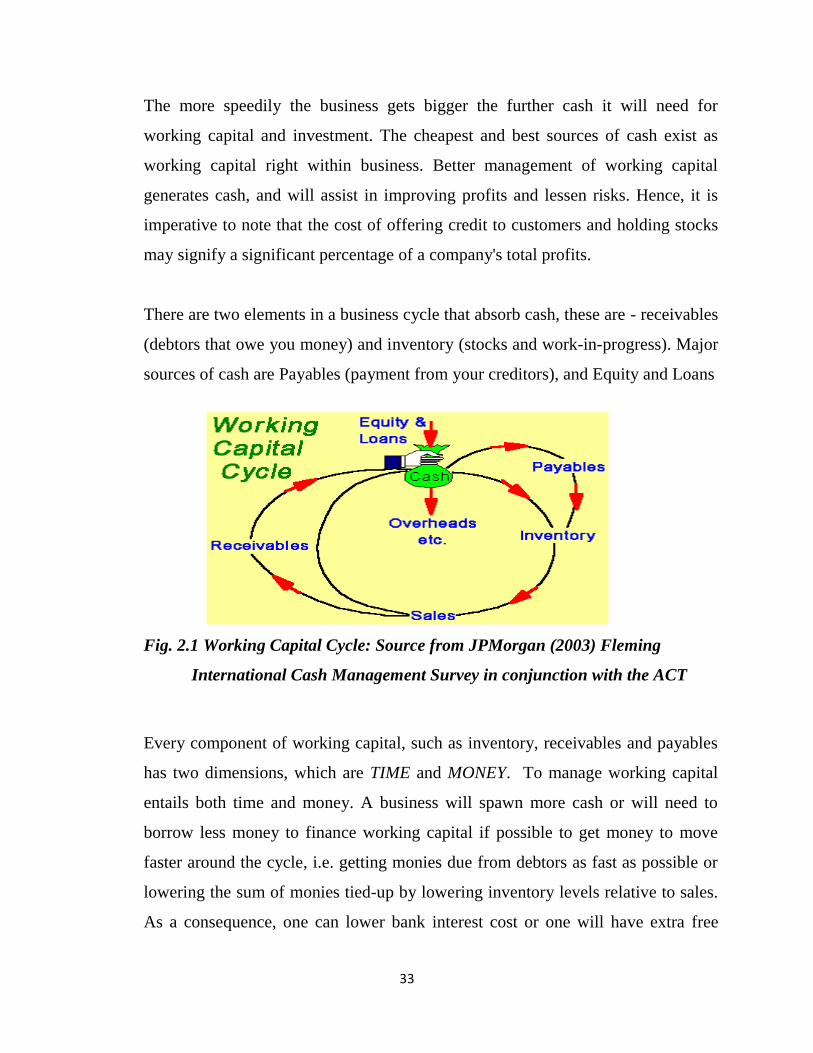

There are two elements in a business cycle that absorb cash, these are - receivables

(debtors that owe you money) and inventory (stocks and work-in-progress). Major

sources of cash are Payables (payment from your creditors), and Equity and Loans

Fig. 2.1 Working Capital Cycle: Source from JPMorgan (2003) Fleming

International Cash Management Survey in conjunction with the ACT

Every component of working capital, such as inventory, receivables and payables

has two dimensions, which are TIME and MONEY. To manage working capital

entails both time and money. A business will spawn more cash or will need to

borrow less money to finance working capital if possible to get money to move

faster around the cycle, i.e. getting monies due from debtors as fast as possible or

lowering the sum of monies tied-up by lowering inventory levels relative to sales.

As a consequence, one can lower bank interest cost or one will have extra free

34

money that will be available to enhance more sales growth or investment. In the

same way, negotiating improved terms with suppliers such as getting longer credit

or an increased credit limit will effectively create free finance to assist funding

future sales.

Working capital is referred to as the fuel powering global business activities, but

often a greater percentage of this fuel is constantly stuck in the pump; tied up in

aging invoices and lengthy Days Sales Outstanding (DSO) cycles. Those firms

that are looking to enhance cash flow have primarily focused on collections.

Whereas traditionally, collections have always been a reactive process i.e. picking

up on aging invoices after they are already late in payment, and then resolving the

underlying issues in an effort to collect. Since it is not easy to go up-stream and

systematically uncover and resolve the root causes of issues that actually drive the

delayed payments. Hence, most of the collections efforts normally end up squarely

emphasizing on dealing with symptoms, rather than addressing the real issues.

As a result of process automation built around innovative dispute prevention

technologies, it is now possible to take a more proactive approach to collections

that are proving to yield enormous dividends that include the unlocking of millions

in working capital, elimination of revenue leakage, and radical improvements in

overall customer satisfaction. Many companies have already seen significant

returns from their work in this area. As submitted by JP Morgan (2005); to

optimise working capital globally, payment and information components of a

transaction must be integrated.

2.1.6. Components of Working Capital Management (WCM)

Working capital management processes involve crucial decisions on multiple

aspects, including the investment of available cash, maintaining a certain level of

inventories, managing accounts receivable and accounts payable (Hadley, 2006).

35

However, WCM is not limited to these tasks, but is implicated in multiple levels of

interactions both internally and between external parties (supplier, customers,

distributors, bankers and retailers). For example, credit officers are required to

investigate credit history of their clients in order to understand their financial

worthiness.

For this study, WCM components can be narrowed to four important components,

namely; cash, receivables, inventory and payables management which are

explained as follows:

2.1.7. Cash Management

The purpose of cash management is to determine the optimal level of cash needed

for operations and investments in marketable securities, which is suitable for the

nature of business operations cycle (Hadley, 2006).

The challenge of cash management is to balance the appropriate level of cash and

marketable securities that will reduce the risk of insufficient funds for operations

and opportunity cost of holding excessively high level of these resources (Filbeck,

et al, 2007). Thus, a company’s competency to synchronize cash inflows with cash

out flows, by using cash budgeting and forecasting in formulating a cash

management strategy is important.

A consideration as to how organizations manage its current asset is quite

important. Though this did not cover marketable securities such as shares,

debentures etc rather, such current assets could be receivable (debtors) and

inventories (stock). Cash is known to be the most liquid of all current assets

needed to keep the business running while at the same time it is the ultimate

output expected to be selling services or products manufactured by the firm. Cash

is (legal tender) which the firm can disburse immediately without any restrictions.

36

The term “cash” include coins, currency notes and cheque held by the firm and

balance in its bank account. Sometimes near cash items such as marketable

securities are also included in cash. This is because near cash can readily be

converted into cash.

Generally, when a firm has excess cash, it invests it in marketable securities or

other investments. This kind of investment contributes some profit to the firm.

Cash management is concerned with management of the following;

i. Cash flow in and out of the firm.

ii. Cash flow within the firm

Cash management is assumed more important than most significant and

least productive assets that a firm holds. It is significant because it is used to pay

the firm obligations.

Therefore, the main aim of cash management is to maintain adequate cash position

to keep the firm sufficiently liquid, and to use excess cash in some profitable way.

It is also important because it is difficult to predict cash flow accurately and there

is no perfect coincidence between the inflows and outflow of cash. Thus during

some period, cash outflows will exceed cash inflows because of payment for taxes,

dividend, seasonal inventory buildup. Sometime because they may be large sums

promptly.

In order to resolve the uncertainty about cash flow prediction and lack of

synchronization between cash receipts and payments, some strategies for cash

management are developed. They include:

i. Cash Planning: This is planning of cash inflow and outflow to project cash

surplus or deficit for each period of the planning period. Cash budget is

prepare for this purpose

37

ii. Managing the Cash Inflow: The inflow and outflow of cash is properly

managed so as to delay the outflow of cash and for proper calculation of

cash flows.

iii. Optimal Cash Level: The firm decides about appointment level of cash

balance.

iv. Investing Idle Cash: Idle cash can be invested in marketable securities or

inform of bank deposit.

Reasons for Holding Cash

There are three major reasons for holding cash

i. Transaction Motive: Firm need cash to pay accounts payable, wages,

taxes, operating expenses, and other maturity current obligations. The

desire to hold cash to meet operating requirement is called the transaction

motive for holding cash. The amount of cash for transaction purpose is a

function of the viability of the firm’s cash flows. This cash flow is

principally affected by fluctuations in sale, the credit policies of raw

materials and the characteristics of the industry.

ii. Precautionary Motive: Cash is held under precautionary motive as a

buffer or cushion to meet unforeseen and unexpected cash requirements or

contingency. Firms with highly variable cash flow would generally have

cash reserves in excesses the need for transactions. Excess cash reserves

held to meet exceptional cash outflow requirements satisfies the

precautionary motive for holding cash reserves and thus allows the firm to

cope adequately with unexpected cash outflows. The need may however,

diminish whenever the cash flows of a business can be fairly predicted with

accuracy or where the business has the ready power to borrow to meet

contingency.

iii. Speculative Motive: This is relating to holding of cash in order to take

advantage of expected changes in security price. When interest rates are

38

expected to rise and security price to fall. The speculative motive would

suggest that the firm should wait until the rise in interest rate cease. When

interest rates are expected to fall, cash may be invested in securities; the

firm will benefit by any subsequent fall in interest rates and rise in security

prices.

There are some strategies for cash management, these include:

i. Cash disbursement should be based on plan and should be slow to avoid

shortage and production interruption.

ii. Loan negotiation and rescheduling of loan where appropriate.

iii. Accelerating collection from customers without adversely reducing future

sales and profit by requesting customers to pay promptly or through cash

discount or through a provided collection system.

iv. Idle or excess cash should be properly invested in short-term marketable

securities.

v. Prepayment should be avoided except in cases of insurance premium or

when necessary.

vi. Sound forecast for cash or short-term and long-term bases.

vii. There should be sound dividend policy

2.1.8 Cash Positioning

Whichever form of business and however volatile the cash flows, treasurers can

maximize the value of their cash holdings by more accurately identifying and

predicting positions throughout the day to enhance investment or borrowing

opportunities and therefore overall return.

Working capital expresses the liquidity of a business. A business with poor

liquidity will have difficulty in paying its everyday expenses, such as salaries and

wages, rent and telephone bills. If management refuses to constantly monitor,

39

control and manage a business's liquidity (its amount of working capital), then the

business may likely end up in a difficult situation with its creditors.

The following key points are important to working capital:

The current assets (cash, inventories/stock and accounts receivable/debtors)

in the business need to be monitored and kept at realistic levels.

Current liabilities constitute all the short-term payments that need to be met

by the business (obligations that need to be paid within one year). Short-

term loans and accounts payable are examples.

Most successful businesses keep the working capital ratio as low as

possible, and keep cash circulating, so as to maximize profit.

The size of the working capital ratio depends on the type of industry the

business operates in, and on financial arrangements such as overdrafts and

creditor policy. Ratios between 1.5:1 and 2:1 are acceptable for most

businesses.

2.1.9. Cash Flow Volatility, Earnings Volatility and Firm Value.

The theory of corporate risk management argues that shareholders are better off if

a firm maintains smooth cash flows. For instance, Froot, Scharfstein, and Stein

(1993) argued that smooth cash flows can add value by reducing a firm's reliance

on costly external finance. Empirically, Minton and Schrand (1999) showed that

cash flow volatility is costly as it affects a firm's investment policy by increasing

both the likelihood and the costs of raising external capital. One recurring theme in

this literature is that, all things being equal, firms with smoother financial

statements should be more highly valued. While previous research finds that cash

flow volatility is costly, no direct evidence exists linking financial statement

volatility to firm value. Such a link is important because, in order for risk

management to matter, smooth financials must be valued at a premium to more

40

volatile ones. Investors value firms with smooth cash flows at a premium relative

to firms with more volatile cash flows. Consistent with risk management theory,

strong evidence shows that cash flow volatility is negatively related to proxies for

firm value.

There are a number of reasons why earnings volatility may matter to the firm,

independent of cash flow volatility. For instance, prior empirical work suggests

that analysts tend to avoid covering firms with volatile earnings, as it increases the

likelihood of forecast errors Similarly, it is imperative that institutional investors

avoid companies that experience large variations in earnings. High earnings

volatility also increases the likelihood of negative earnings surprises; in response,

managers have engaged in extensive earnings smoothing. It should be noted that

earnings smoothing may likely reduce a company's perceived probability of

default and therefore a firm's borrowing costs. Goel and Thakor (2003) suggest

that a firm may smooth earnings so as to reduce the informational advantage of

informed investors over uninformed investors, and therefore protect these

investors who may need to trade for liquidity reasons. Last but not the least,

Francis, Lafond, Olsen, and Schipper (2004) find firms with greater earnings

smoothing have a lower cost of capital even after accounting for cash flow

volatility.

In fact, under certain specifications the market appears to punish firms for

undertaking smoothing behavior preferring earnings volatility mirror cash flow

volatility. These results are important and suggest Managers focus their actions on

smoothing cash flows rather than necessarily utilizing accruals to smooth earnings.

Of course, there are a number of other ways in which financial uncertainty

interacts with firm value. According to the CAPM, systematic risk should be

41

negatively related to value, since higher discount rates yield a lower value, all

things being equal.

Further, recent empirical work suggests that not only does systematic risk affect

value, but also idiosyncratic risk may be priced (Shin and Stulz, 2000). Empirical

evidence suggests that there is a negative relation between systematic risk and firm

value, as well as a negative and significant association between unsystematic risk

and firm value.

The two alternative types of risk, namely, cash flow and earnings volatility are of

primary importance since unlike financial market variables they reflect the actual

stability of the firms' financial statements and are directly affected by managerial

decisions and the firms' risk management policies.

2.1.10 Cash Budget

Cash budget is the most significant device to plan for control of cash receipt and

payment. Cash is summary statement of the firm expected cash inflows and

outflows over projected cash time period. It gives information on the timing and

magnitude of expected cash flows and cash balances over the projected period.

This information is helpful to the financial manager to determine the future cash

need of the firm, plan for financing for those need and exercise control over cash

and liquidity of the firm. In preparing a cash budget, the financial manger has to

forecast receipts and payments.

The most important source of cash receipts is sales. Developing forecast is the first

step in preparing the cash budget. All precautions are taken to forecast sales as

accurately as possible, sales can be for cash or on credit.

42

Once the cash budget has been prepared and appropriate net cash flow is

established, the financial manger ensures that there does not exists a significant

deviation between projected cash flows and actual cash flows. To achieve this,

through collections and cash disbursement, this forms the objective of managing

the cash flow. One of the techniques used by companies to accelerate their cash

collections is concentration banking.

2.1.11. Management of Cash Receivables

Trade credit is known to be the most prominent force of the modern business. It is

considered as essential marketing tools, acting as a bridge for the movement of

goods through production and distribution stages to consumers. A firm grants

trade credit to protect its sales from the competitors and to attract potential

customers to buy its product at favorable terms. When a firm sells its product or

services and does not receive cash from it immediately, the firm is said to have

granted trade credit to customer. Trade credit, thus create receivables or book debt

and receivable arising from the credit had three characteristics which include

involvement of an element of risk which should be carefully analyzed.

Cash sales are totally risk less, but not credit sale, as the cash payments are yet to

be received.

2.1.12. Credit Standards

Credit standards are criteria that determine which customer will be granted credit

and to what event. First attempting to implement ideal credit standard may result

in a too stringent or too light policy that may eliminate the risk non-payment, but

also eliminate potential sales to those rejected customers who would have paid

their bill. At the other extreme, an excessively liberal policy may lead to higher

sales, but greater bad debt losses and collection cost would follow. Therefore, the

tradeoff between managerial benefit and cost dictate the balance between two

extremes.

43

Nevertheless, credit standards often revolve round five C’S of credit analysis.

i. Character: Has to do with the probability that a customer will try to honor

his/her obligation. This factor is of considerable importance between every

credit transaction which implies a promise to pay. Experience credit

managers frequently insist that character, is the most important issue in a

credit evaluation.

ii. Capital: This is measured by the general financial position of the firm as

indicated by a financial ratio analysis with a special emphasis on the

tangible net worth of the enterprises.

iii. Collateral: This is represented by assets the customers offer as a pledge for

security of the credit extends.

iv. Condition: This have to do with impact of general economic trends on the

firm or special development in certain area of the economy that affect the

customers’ ability to meet the obligation.

v. Capacity: This describes a subjective judgment of the customers’ ability to

pay. It is gauged by the customers past business performance record

supplemented by physical observation of the plant.

2.1.13. Credit Extension Policy

Credit extension policies provide guide lines for granting credit, the terms of

payment and amount of credit to extend to a customer. The cost of a credit

extension policy can be grouped into the following categories:

i. Cash Discount: A percentage of sales deducted as an incentive to

encourage early payment. Early payment not only reduces capital

requirement but also saves administrative cost of pursuing outstanding

debtors and may reduce the overall risk of bad debts as well. Cash discount

are a relative expensive way of improving the inflow of cash and most

companies would prefer to avoid them by raising extra working capital at a

44

more advantageous market rate. There may sometime be an element of

price reduction in the cash discount. It is a concealed way of offering lower

price to a sector of the market, which might otherwise go to competitions

(Brockingtion; 1287:273).

ii. Bad Debt Losses: These are usually accounts that are uncollectible and

written off as a charge against sales.

iii. Credit and Collection Expenses: Administrative cost for conducting in-

house credit operations are also charge against sales.

iv. Financing Cost: The opportunity cost of capital of funds tied up in a

receivable investment.

2.1.14. Credit Collection Policy

The overall debt collection policy of the firm should be that, the administrative

cost and other cost incurred in debt collection should not exceed the benefit

received from incurring those cost. The following are some of the best method to

be adopted in a debt collection department.

i. Polite reminder: This is done when a bad debt matured but the debtor has

done nothing about it.

ii. Strongly Worded Reminder: This is usually send when the debtor is

presumed to have received the polite reminder but still remains adamant.

iii. Tele-phone Call: This is a person to person contact employed as a step on

the debtor’s collection policy when the debtor does not need polite and

strongly worded reminder.

iv. Personal Call: When all the steps enumerated above fail to produce result,

staff of the credit company should be dispatched to the debtor to personally

persuade him/her to pay.

v. Collection Agencies: Collection agencies employ almost unlimited means

of collecting their customer’s funds, so businesses do not employ it readily

for fear of losing customers goodwill.

45

vi. Legal Action: This is last resort because it is costly both in terms of time

and money.

vii. Withdrawal of credit facilities: This is a situation whereby such credit

facilities are been withdrawn from the debtor’s form or possession for

default in payment.

2.1.15. Inventory (Inv) Management

Inventories are the product a company is manufacturing for sale and the

components that make up the product (Pandey, 2005). He classified the various

forms in which inventories exist in a manufacturing company as: raw materials,

work-in-progress facilitate production, while stock of finished goods is required

for smooth marketing operations (Hadley, 2006). Similarly the Oxford Dictionary

of Accounting (2005) defined inventory (stock) as the products or supplies of an

organization on hand or in transit at any point in time.

In the context of inventory management, Pandey (2005) opined that a firm is faced

with the problem of meeting two conflicting needs. First, to maintain a large size

of inventories of raw materials and work-in-progress for efficient and smooth

production and of finished goods for uninterrupted sales operations. Secondary, to

maintain a minimum investment in inventories to maximize profitability. The

objective of inventory management should be to determine and maintain optimum

level of inventory investment which should normally lie between the two danger

points of excessive and inadequate inventories.

According to Pandey (2005), the major dangers of over-investment are: the

unnecessary tie-up of the firm’s funds and loss of profit; the excessive carrying

costs (such as the costs of storage, handling, insurance, recording and inspection),

and the risk of liquidity. While the consequences of under-investment in

46

inventories are: the production hold-ups and the failure to meet delivery

commitments.

Inventory, therefore, plays an important role to determine the activities in

producing, marketing and purchasing. Since inventory determines the level of

activities in a company, managing it strategically contributes to profitability

(Filbeck, Krueger & Preece, 2007). A company’s ability to respond to demand is

largely dependent on how efficient the company manages inventories and how

committed its suppliers are to support a company’s production lines (Rafuse,

1996).

The number of days inventory are held (DINV) is used as a proxy for the

inventory policy and is calculated as (INV×365)/cost of goods sold (Dong & Su,

2010). DINV reflects the average number of days stock are held by the firm.

Longer storage days represent a greater investment in inventory for a particular

level of operations.

2.1.16. Need to Hold Inventory

There are three general reasons why inventory is held in manufacturing firms.

i. To maintain inventories to facilitate smooth sale operations.

ii. To guide against risk of unpredictable change in demand and supply forces

and factors.

iii. To take advantage of price fluctuation, which influence the decisions to

increase or reduce inventory level. Supply of raw materials may be delayed

due to such factors as transport disruption, short supply etc. Therefore, it is

necessary for a firm to maintain sufficient stock of raw materials at a given

streamline production.

47

2.1.17. Inventory Control

For a given level of inventory, the affectability of inventory control affects the

flexibility of the firm, inefficient inventory control result to unbalance inventory

and rigidity. The firm may sometimes be out of stock and sometimes pile up

unnecessary stock. This makes the firm unprofitable.

Better management of inventory has the following:

i. How much of the inventory should be order

ii. When should it be ordered?

The first problem relates to the problem of determining the economy order

quantity (EOQ) and is explain with analysis of the cost of maintaining certain

level inventories. On the other hand, when to order because of uncertainties and is

a problem of determining the re-order point.

2.1.18. The Economic Order Quantity (EOQ)

The problem of how much inventory should be added when inventory is

replenished or in case of raw materials, the lot which it has to purchase on each

replenishment are called “order quantity problem” and the task of the firm is to

determine optimum or economic order quantity and to determining the optimum

carrying cost.

Carrying costs are cost incurred for holding a given level of inventory they include

opportunity cost of funds invested in inventories, Insurance, Taxes, storage cost

and cost of deterioration. The carrying cost move in direct proportion to inventory

size. The optimum inventory size is commonly referred to as economic order

quantity (EOQ). It is that order size at which annual total cost of ordering and

holding are at minimum.

Economic order quantity is calculated by using the formulae below:

EOQ = √2𝐴𝑄

𝐶

48

Where: EOQ = Economic Order Quantity

A = Total Annual Requirement

O = Ordering cost per order

C = Carrying Cost per order

2 = Constant

2.1.19. Re-Order Point

This is the inventory level at which an order should be place to replenish the

inventory. To determine the re-order point under certainty, we should know the

lead time, the average usage and the economic order quantity. The lead time is the

time normally taken in receiving delivery of inventory after the order had been

placed.

Re-order Point = Lead Time + Average Usage

It is difficult to predict usage and the lead time accurately. Demand for materials

may be different from the normal lead time. These might lead to stock-out. To

guard against stock-out safety may be maintained. There are some minimum or

buffer inventories as cushion against expected increase usage and or delay in

delivery time.

When all uncertainties are taken into consideration, it means re-order point is

determined under uncertainty which thus give the following formulae.

Re-order Point (when safety is maintained) = Lead Time x Average usage + Safety

stock.

2.1.20. Relation to Financial Management

Techniques of inventory management are very useful in determining the optimum

level of inventory and finding solution to the problem of the economic order

quantity, the re-order point and the safety stock.

49

The investment of fund in an inventory is a very important aspect of financial

management therefore; the financial manager must be familiar with way to control

inventories effectively so that the allocation of capital will be done effectively.

When demand or usage of inventory is uncertain, the financial manager may try

lead time when an order is placed. The lower the average lead time, the lower the

safety stock needed and the lower the total investment.

In the case of purchases, the purchases department may look for a new vendor that

promise quicker delivery or put pressure in the case of finished goods. The

production runs may be scheduled by the production by producing smaller runs or

fast delivery. The greater the efficiency with which the firm manages its inventory,

the lower the inventory in it.

2.1.21. Payables Management

Falope and Ajilore (2009) view accounts payable (AP) as supplies whose invoices

for goods or services have been processed but have not yet been paid. While the

Oxford Dictionary of Accounting (2005) defined accounts payable, which is also

called trade creditors, as the amount owed by a business to suppliers. Accounts

payable are classed as current liabilities on the balance sheet but distinguished

from accruals and other non-trade creditors. Organizations often regard the

amount owing to creditors as a source of free credit because it has no identifiable

interest charges. It is in view of this that accounts payable are always regarded as a

major source of working capital financing for firms (Pandey, 2005). Therefore,

strong alliance between company and its suppliers will strategically improve

production lines and strengthen credit record for future expansion.

The number of days accounts payable (DAP) is used as a proxy for payment

policy. It reflects the average days it takes firms to pay their suppliers. DAP is

calculated as (AP×365)/cost of goods sold (Dong & Su, 2010).

50

2.1.22. Receivables Management

Refuse (1996) view accounts receivable (AR) as customers who have not yet made

payment for goods or services, which the firm has provided. While the Oxford

Dictionary of Accounting (2005) defined accounts receivable, which is also called

trade debtors, as the amounts owing to a business from customers for invoiced

amounts. AR are classed as current assets on the balance sheet, but distinguished

from prepayments and other non trade debtors.

The objective of debtors (receivables) management is to minimize the time-lapse

between completion of sales and receipt of payments (Hadley, 2006). Profits may

be called real profits after the receivables are turned into cash (Srivastarva, 2004)

refuse (1996) posited that the management of accounts receivable is largely

influence by the credit policy and collection procedure.

He maintained that a credit policy specifies requirements to value the worthiness

of customers and a collection procedure provides guidelines to collect unpaid

invoices that will reduce delays in outstanding receivables.

The number of days accounts receivable (DAR) is used as a proxy for the

collection policy. DAR is calculated as (AR×365)/sales (Dong Su, 2010), which

represents the average number of day that the firm takes to collect payments from

its customers. The shorter the DAR, the better the quality of debtors, since a short

DAR implies prompt payments by debtors. The DAR should be compared against

the firm’s credit terms and policy to ascertain its credit and collection efficiency

(Pandey, 2005).

2.1.23. Cash Conversion Cycle (CCC) Management

Working capital are the funds which are used to operate in the short term. If

receivables are postponed, there can be delays in payments and these could be

51

suspended causing a situation of illiquidity for the firm. Therefore, aligning the

receivables management between cash, inventory and payable management is

relatively challenging and important (Richards & Langhhin, 1980). In this context,

CCC is an important tool of analysis that enables us to establish more easily why

and how the business needs more cash to operate and when and how it will be in a

position to refund the negotiated resources (Elizalde, 2003). For Dong and Su

(2010), CCC is considered as a comprehensive measure of checking the efficiency

of working capital management. In their seminar paper, Richards and Laughhin

(1980) devised this method of working capital cycle which is considered as the

period between the payments of cash to creditors (cash out-flow) and the receipt of

cash from debtors (cash in-flow). They claimed that the method is superior to

other forms of working capital analysis that rely on ratio analysis.

A business can generate losses during a number of different periods, but it cannot

go on indefinitely with poor CCC Management. The activities that are directly

related to CCC management are:

i. The determination of the effective number of days to collect receivables.

ii. Determining the inventory needs and

iii. Determining the future growth of sales.

These activities must be integrated in such a way that the period of time in which

the cash is not being used to fund the working capital is minimized (Deloof, 2003).

The three activities are carried out through the implementation of credit policy,

inventory policy and cash management policy.

The CCC is calculated by subtracting the number of days accounts payable

(accounts payable×365/cost of goods sold) from the sum of the number of days

accounts receivable (accounts receivable×365/sales) and the number of days

inventory are held (inventories ×365/cost of goods sold). CCC has been

52

interpreted as a time interval between the cash outlays that arise during the

production of output and the cash inflows that result from the sale of the output

and the collection of accounts receivable (Falope & Ajilore, 2009). Padachi (2006)

posited that CCC is either negative or positive. A positive result indicates that a

company must borrow while awaiting payments from cutomers, if it must meet up

with its due obligations. A negative result indicates the number of days a company

has to receive cash from sales before it must pay its suppliers (Harris, 2005).

However, the ultimate goal is having low CCC, if possible negative, because the

shorter the CCC, the more efficient the company in managing its cash flows and

the better a firm profitability (Padachi, 2006).

2.1.24. Measures of Profitability

According to Eljelly (2004), profitability is the ability to create an excess of

revenue over expenses in order to attract and hold investment capital.

Four useful measures of firm’s profitability are the rate of return on firm’s assets

(ROA), the rate of return on firm’s equity (ROE), operating profit margin and net

firm income. The ROA measures the return to all firm’s assets and is often used as

an overall index of profitability, and the higher the value, the more profitable the

firm. ROA is an indicator of managerial efficiency and also shows how the firm’s

management converted the institution’s assets under its control into earnings

(Falope & Ajilore, 2009).

The ROE measures the rate of return on the owners equity employed in the firm

(Pandey, 2005). ROE indicates how well the firm has used the resources of

owners.

The operating profit margin measures the returns to capital per naira of gross firm

revenue. It focuses on the per unit produced component or earned profit and the

asset turnover ratio.

53

The net income comes directly on the income statement and it is calculated by

matching firm revenue with expenses incurred to create revenue, plus the gain or

loss on the sale of firm capital assets (Gitman, 2006).

2.1.25. Liquidity

Liquidity has been defined by Eljelly (2004) as the ability to convert an asset to

cash with relative speed and without significant loss in value. Liquidity measures

the ability of the firm to meet financial obligations as they fall due, without

disrupting the normal, ongoing operations of the business (Smith, 1980).

A frequent cause of liquidity problems occurs when debt maturities are not

matched with the rate at which the business assets are converted to cash (Eljelly,

2004).

Liquidity ratios measures the firm’s ability to meet current obligations, and are,

calculated by establishing relationships between current assets and current

liabilities (Pandey, 2005).

2.1.26. Nature of Working Capital

Working capital management is centred on problems arising in attempting to

manage the current assets, the current liabilities and the interrelationship that

exists between them. As explained earlier, the term current assets refer to those

assets which business will be converting into cash within one year without

experiencing a dwindling in value and upsetting the operations of the company.

Most major current assets are cash, marketable securities, accounts receivable and

inventory.

Current liabilities are referred to those liabilities that are intended at the beginning,

payable in the ordinary course of business, within a year, out of the current assets

54

or earnings of the concern. Among the essential current liabilities are accounts

payable, bills payable, bank overdraft, and outstanding expenses. The Principal

objective of working capital management is to manage the company’s current

assets and liabilities in such a way that a satisfactory level of working capital is

maintained. It is so due to the fact that if the company cannot sustain an acceptable

level of working capital, it is certainly may lead into what is termed insolvency

and may end up into bankruptcy.

Current assets must be large as much as necessary to be able to cover its current

liabilities to guarantee a reasonable margin of safety. All of the current assets are

to be managed efficiently so as to maintain the liquidity of the company; while not

keeping too high a level of any one of them. Every of the short-term bases of