Avoiding Two Common Tax Traps in Oil and Gas Conveyances · Avoiding Two Common Tax Traps in Oil...

33

#AICPAoil Avoiding Two Common Tax Traps in Oil and Gas Conveyances Vance Maultsby, CPA November 19, 2014 1

Transcript of Avoiding Two Common Tax Traps in Oil and Gas Conveyances · Avoiding Two Common Tax Traps in Oil...

#AICPAoil

Avoiding Two Common Tax Traps in Oil and Gas

Conveyances

Vance Maultsby, CPA November 19, 2014

1

American Institute of CPAs #AICPAoil

Vance Maultsby, CPA HM&M Shareholder, Vance Maultsby, CPA, entered the accounting profession at Peat Marwick Mitchell where he made partner early in his career and was later named National Director of the Petroleum Industry Practice. While at Peat Marwick, he was a Contributing Author and Senior Editor of Income Tax of Natural Resources, which was considered an authoritative resource in oil and gas taxation. Vance’s experiences also include executive corporate finance roles at investment bank Stephens Inc. and Ernst & Young. While at Ernst & Young, Vance was the Regional Director of Corporate Finance. He has also served as the Chief Executive Officer of Palex, Inc. (NASDAQ traded). Vance currently serves as Adjunct Professor at UNT where he teaches a graduate oil & gas taxation class. The experience Vance has gained in these roles gives him an exceptional perspective into the issues and challenges confronting his clients.

American Institute of CPAs #AICPAoil

Overview

Independent oil and gas producers are frequently engaged in farmout arrangements. • Farmout - a sharing arrangement that transfers some or all of

the working interest in a property or properties in exchange for undertaking some or all of the responsibilities for exploring, developing and operating the property or properties.

• These farmout arrangements are often classified as fully tax-free sharing arrangements or as divisible or mixed sharing arrangements having some tax-free elements and some taxable elements.

3

American Institute of CPAs #AICPAoil

Overview, cont.

With the increased activity in the U.S. oil patch, we see more farmout arrangements in recent years. Two types of transactions with almost always bad tax implications seem to arise frequently.

• Unintended subleases • Obligation well deals covered by Revenue Ruling 77-176

4

American Institute of CPAs #AICPAoil

Overview, cont.

We will look at each of these two types of transactions.

• We’ll lay out the fact pattern. • We’ll look at the tax treatment and the authority for

tax treatment of the fact patterns. • We’ll work through each of these situations with real

numbers. • We’ll identify ways to avoid these two tax traps.

5

American Institute of CPAs #AICPAoil

Inadvertent Sublease – Fact Pattern

Jones Partners, Ltd. (“JPL”) is formed to acquire and exploit leases in the Eagle Ford play. JPL acquires many new undeveloped leases and spends $10 million doing so.

JPL is approached by Gargantuan Oil Company (“GO”). After much negotiation, JPL receives $22 million in exchange for the leases. JPL retains an overriding royalty in each of the leases equal to a 25 percent net revenue interest, less the underlying landowners’ royalties net revenue interests.

6

American Institute of CPAs #AICPAoil

Inadvertent Sublease – Tax Treatment

The conveyance of a working interest and the retention of a continuing nonoperating interest (such as a royalty, overriding royalty, or net profits interest) in the conveyed property is a lease or sublease. Cash or property conveyed by the lessee or sublessee of the lease of undeveloped property is treated as leasehold cost by the lessee or sublessee. Cash or property received by the lessor or sublessor in connection with a lease or sublease in undeveloped property is treated as a lease bonus. The Supreme Court held that the receipt of a bonus payment by a lessor pursuant to an oil and gas lease is taxable as ordinary income, not as gain from the sale of capital assets. Burnet v. Harmel, 287 U.S. 103 (1932). See also Palmer v. Bender, 287 U.S. 551 (1933); Laudenslager v. Commissioner, 305 F. 2d 686 (3rd Cir. 1962); Cox v. U.S., 497 F. 2d 348 (4th Cir. 1974).

7

American Institute of CPAs #AICPAoil

Inadvertent Sublease – Tax Treatment, cont.

Theoretically, the lessor’s ordinary income may possibly be reduced by cost depletion.

It is very hard to justify cost depletion on undeveloped or unproven leases. • The IRS says that cost depletion cannot be computed. • However, there is one decision from a Wyoming District Court

stating that the entire cost in a lease could be offset against a sublease bonus, because there was not reasonable expectation of any future production at the time the sublease was executed. Collums v. U.S., 480 F. Supp. 864 (D.C. Wyo. 1979).

8

American Institute of CPAs #AICPAoil

Michael H. Dudek, et ux., TCM 2013-272 (12/2/2013)

A recent Tax Court Memorandum case is illustrative of the consequences of an unexpected lease or sublease

In 2008, the Dudeks entered into an oil and gas lease agreement with EOG Resources, Inc. covering 353.3 acres. The agreement provided for the Dudeks to receive 16% of the net profits of any oil and gas extracted from the property.

EOG’s agent paid them $883,250 ($2,500 per acre) to enter into the lease and sent them a Form 1099-MISC for that amount.

9

American Institute of CPAs #AICPAoil

Dudek, cont.

The Dudeks reported the payment as long-term capital gain. • The court summarily rejected the Dudeks’ position, citing the

above-mentioned authorities.

The Dudeks argued alternatively that they should be able to receive percentage depletion. • The court pointed out that Section 613A(d)(5) specifically denied

percentage depletion on lease bonuses. • The court then noted that they did not argue for cost depletion.

10

American Institute of CPAs #AICPAoil

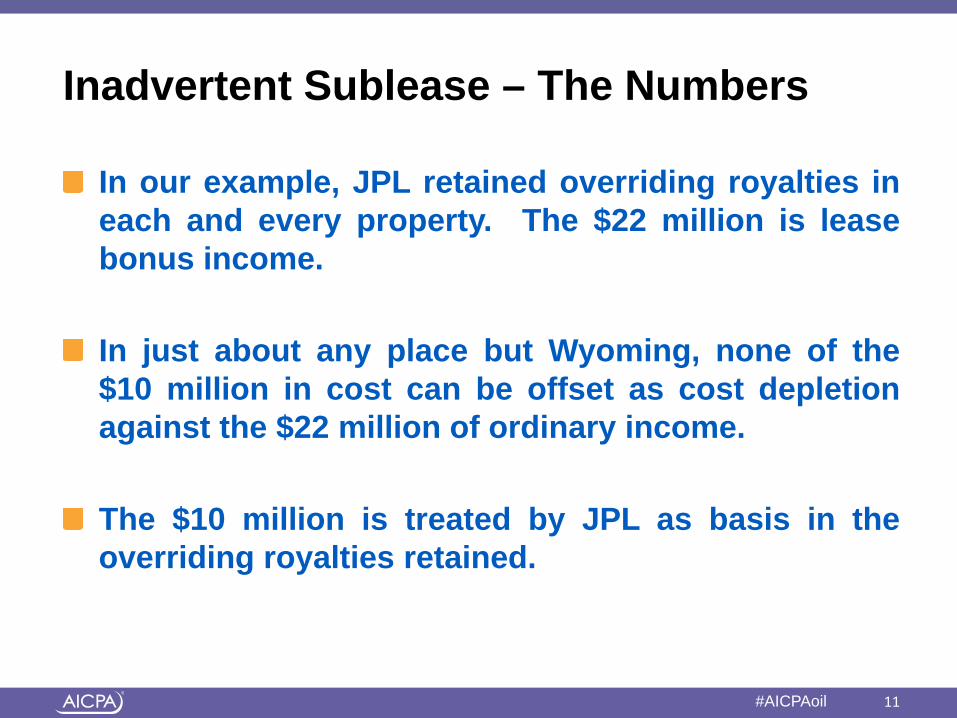

Inadvertent Sublease – The Numbers

In our example, JPL retained overriding royalties in each and every property. The $22 million is lease bonus income.

In just about any place but Wyoming, none of the $10 million in cost can be offset as cost depletion against the $22 million of ordinary income.

The $10 million is treated by JPL as basis in the overriding royalties retained.

11

American Institute of CPAs #AICPAoil

Avoiding Inadvertent Subleases

Just say no (to retention of overriding royalties).

• Instead of retaining a continuing nonoperating interest, retain a limited nonoperating interest – a production payment. - However, in the case of unproven properties,

it may be very difficult to prove that the production payment has a shorter life than the expected economic life of the properties burdened by the production payment.

12

American Institute of CPAs #AICPAoil

Avoiding Inadvertent Subleases, cont.

Before executing a lease, carve out the subject overriding royalties and assign them to a regarded entity, preferably an entity that is not owned in a manner identical to the entity receiving the consideration. • In a Field Service Advice (FSA (1992) 1992 WL 1355696 (cited

in Income Taxation of Natural Resources 2014, KPMG LLP) a taxpayer was apparently in the business of acquiring leases and reconveying them to third parties for a profit. The taxpayer established a trust for the benefit of his children. In connection with the conveyance to the third parties, he would simultaneously carve out and convey overriding royalties to his children’s trust. The FSA determined that “stepping these transactions together, the purchase and assignment of the lease interests and [overriding royalties] constitute sales of assets.”

American Institute of CPAs #AICPAoil

Avoiding Inadvertent Subleases, cont.

• Technical Advice Memorandum 8537007 offers some guidance, but following the roadmap too closely may not be advisable.

- In 1969, A entered into a lease to develop and operate mining properties.

- In 1973, A subleased his property to S corporation P for 85% of the stock of P, retaining a 2.5% overriding royalty. A's three children owned the other 15% of P.

- In 1974, A transferred the entire ORRI to his three children by gift.

- In 1976, A transferred another 30% of the stock of P to the children by gift.

- In 1981, unrelated party Q purchased P's lease.

14

American Institute of CPAs #AICPAoil

Avoiding Inadvertent Subleases, cont.

• TAM 8537007, cont. - The IRS concluded that the ownership of the overriding

royalties by shareholders of P did not cause the sale to Q to be treated as a lease by P.

- The TAM does not address whether the 1973 sublease to P meets the requirements of a tax-free "transfer in exchange" for stock in Section 351.

- Do the principles set forth in E.I. DuPont De Nemours & Co. v. U.S., 471 F. 2d 1211 (Ct. Cl. 1973) yield a Section 351 transaction in the instant fact pattern? I wouldn't want to bet the ranch that they do.

15

American Institute of CPAs #AICPAoil

Avoiding Inadvertent Subleases, cont.

The FSA and the TAM to a lesser extent together offer a promising, but incomplete, roadmap for avoiding a subleasing transaction. • A meaningful time period between the overriding royalty carve-

out/transfer and the assignment of the lease for consideration may be helpful.

• The less identical the ownership in the entity receiving the carved-out ORRI and the entity assigning the lease for cash, the better.

• Good non-tax reasons for the separate entities and the transfers are important.

16

American Institute of CPAs #AICPAoil

Avoiding Inadvertent Subleases, cont.

Consider retaining a right to future income that does not qualify as an economic interest. • This solution should be approached with great care. • To achieve the desired, special attention should be paid in

drafting the conveyance to assure that it does not result in a divisible sharing arrangement – part lease and part taxable transaction.

• Neither the form nor the substance of the transaction should be that of a lease.

• A substantial alternative source of payment may take the transaction out of being classified as a lease or sublease.

- See Anderson v. Helvering, 310 US 404 (1940). Also, see C.B. Christie v. U.S., 436 F.2d 1216 (5th Cir. 1971). Both cases address the tax treatment of production payments before the enactment of Section 636.

17

American Institute of CPAs #AICPAoil

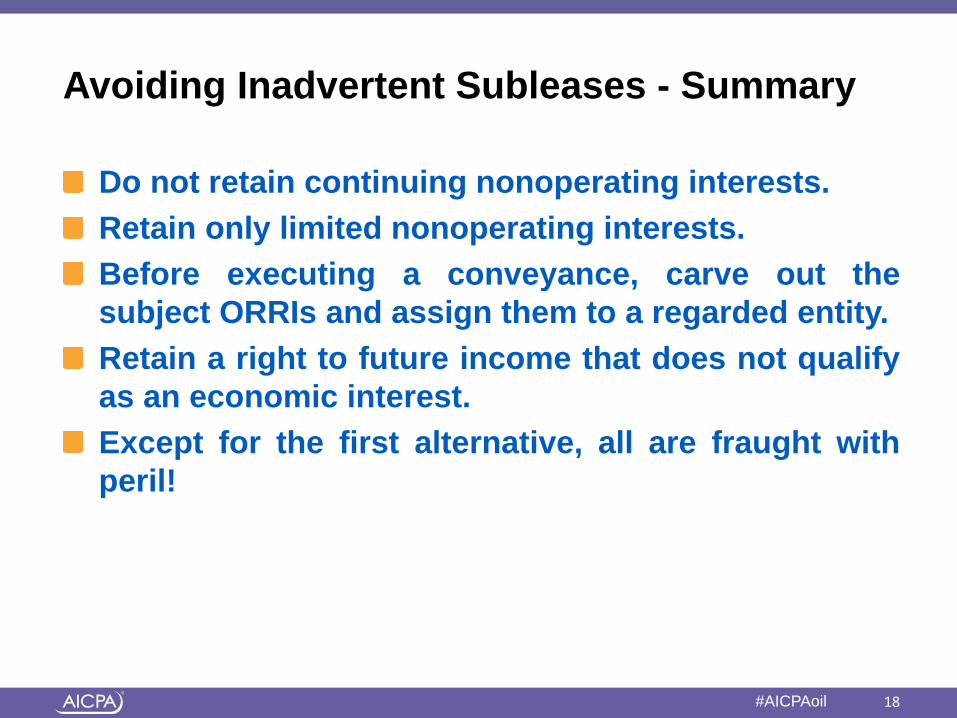

Avoiding Inadvertent Subleases - Summary

Do not retain continuing nonoperating interests. Retain only limited nonoperating interests. Before executing a conveyance, carve out the subject ORRIs and assign them to a regarded entity. Retain a right to future income that does not qualify as an economic interest. Except for the first alternative, all are fraught with peril!

18

American Institute of CPAs #AICPAoil

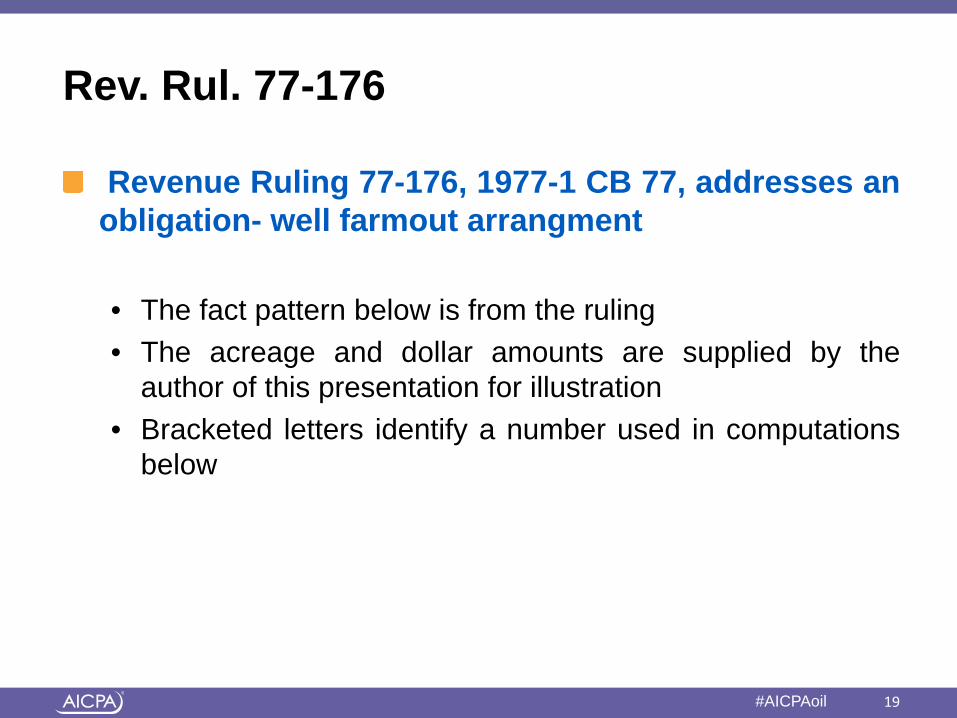

Rev. Rul. 77-176

Revenue Ruling 77-176, 1977-1 CB 77, addresses an obligation- well farmout arrangment

• The fact pattern below is from the ruling • The acreage and dollar amounts are supplied by the

author of this presentation for illustration • Bracketed letters identify a number used in computations

below

19

American Institute of CPAs #AICPAoil

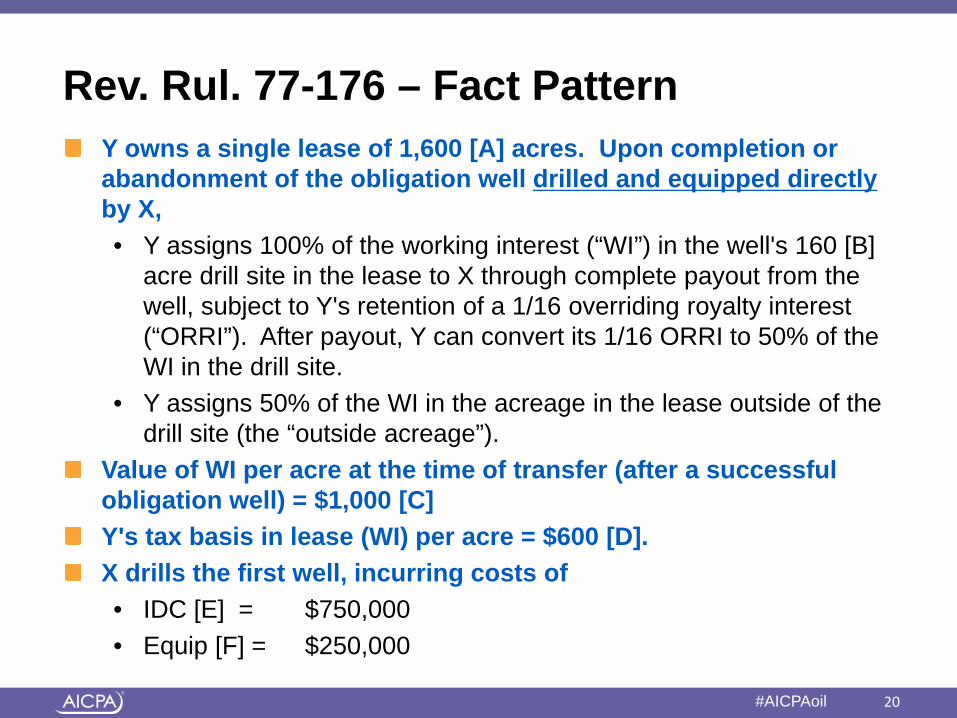

Rev. Rul. 77-176 – Fact Pattern Y owns a single lease of 1,600 [A] acres. Upon completion or abandonment of the obligation well drilled and equipped directly by X, • Y assigns 100% of the working interest (“WI”) in the well's 160 [B]

acre drill site in the lease to X through complete payout from the well, subject to Y's retention of a 1/16 overriding royalty interest (“ORRI”). After payout, Y can convert its 1/16 ORRI to 50% of the WI in the drill site.

• Y assigns 50% of the WI in the acreage in the lease outside of the drill site (the “outside acreage”).

Value of WI per acre at the time of transfer (after a successful obligation well) = $1,000 [C] Y's tax basis in lease (WI) per acre = $600 [D]. X drills the first well, incurring costs of • IDC [E] = $750,000 • Equip [F] = $250,000

20

American Institute of CPAs #AICPAoil

Rev. Rul. 77-176 – The Ruling

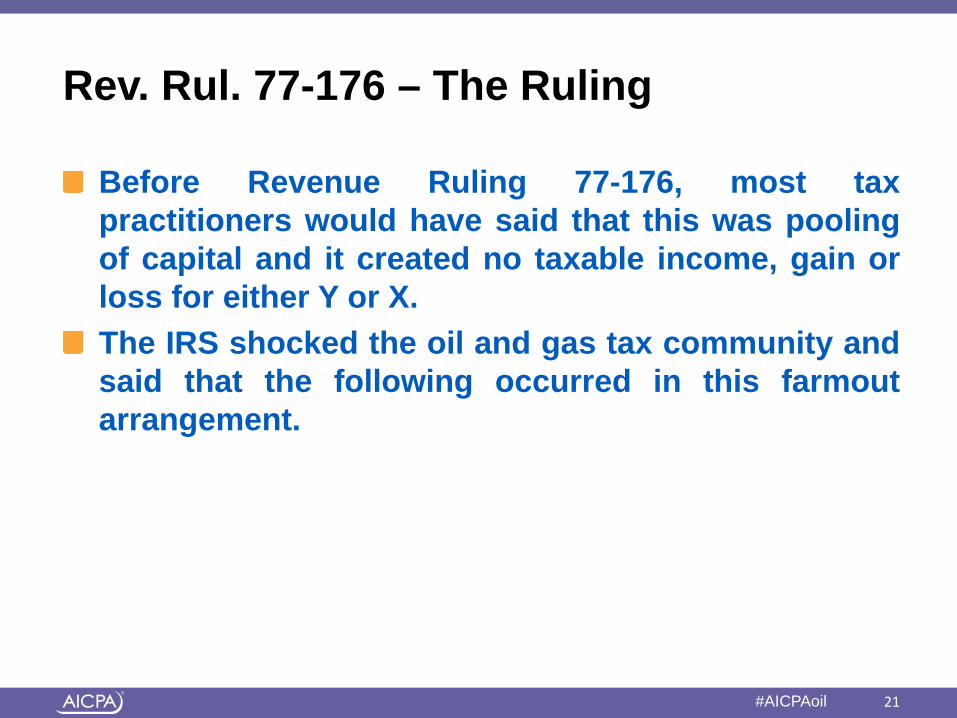

Before Revenue Ruling 77-176, most tax practitioners would have said that this was pooling of capital and it created no taxable income, gain or loss for either Y or X. The IRS shocked the oil and gas tax community and said that the following occurred in this farmout arrangement.

21

American Institute of CPAs #AICPAoil

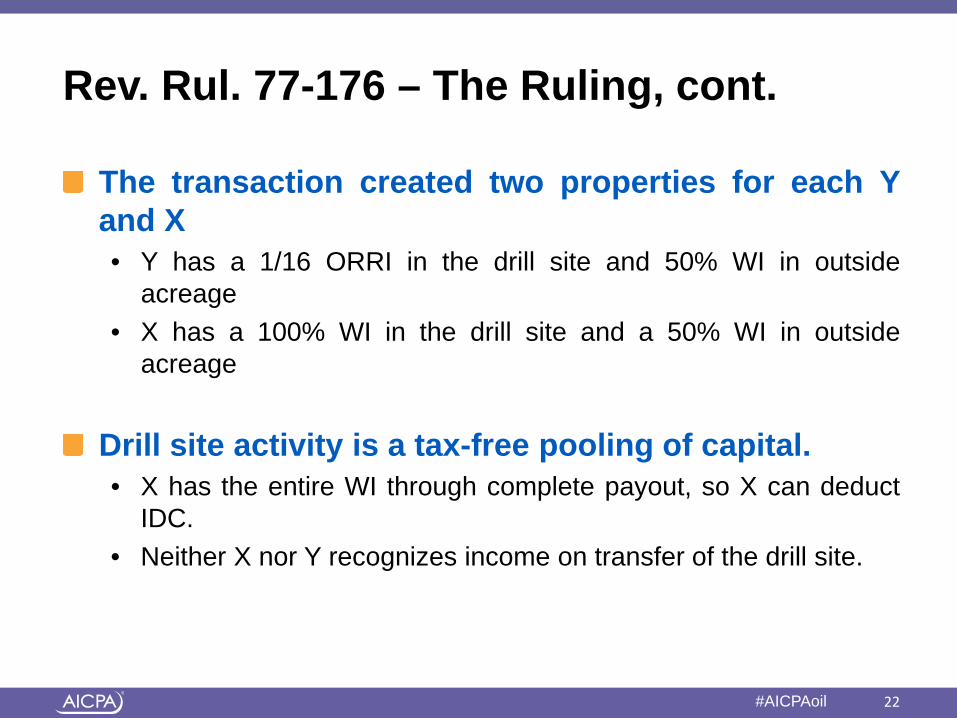

Rev. Rul. 77-176 – The Ruling, cont.

The transaction created two properties for each Y and X • Y has a 1/16 ORRI in the drill site and 50% WI in outside

acreage • X has a 100% WI in the drill site and a 50% WI in outside

acreage

Drill site activity is a tax-free pooling of capital. • X has the entire WI through complete payout, so X can deduct

IDC. • Neither X nor Y recognizes income on transfer of the drill site.

22

American Institute of CPAs #AICPAoil

Rev. Rul. 77-176 – The Ruling, cont.

Y is deemed to have sold the outside acreage for cash and transferred the cash to X "as additional compensation for undertaking by X of the development project on the drill site.“

• The adjusted basis in Y's ORRI in the drill site is increased by

the fair market value of the undivided 50% WI transferred to X. • Y has gain or loss depending on the value at the time of transfer

and Y's basis. • The gain or loss may be ordinary or Section 1231 gain or loss.

23

American Institute of CPAs #AICPAoil

Rev. Rul. 77-176 – The Ruling, cont.

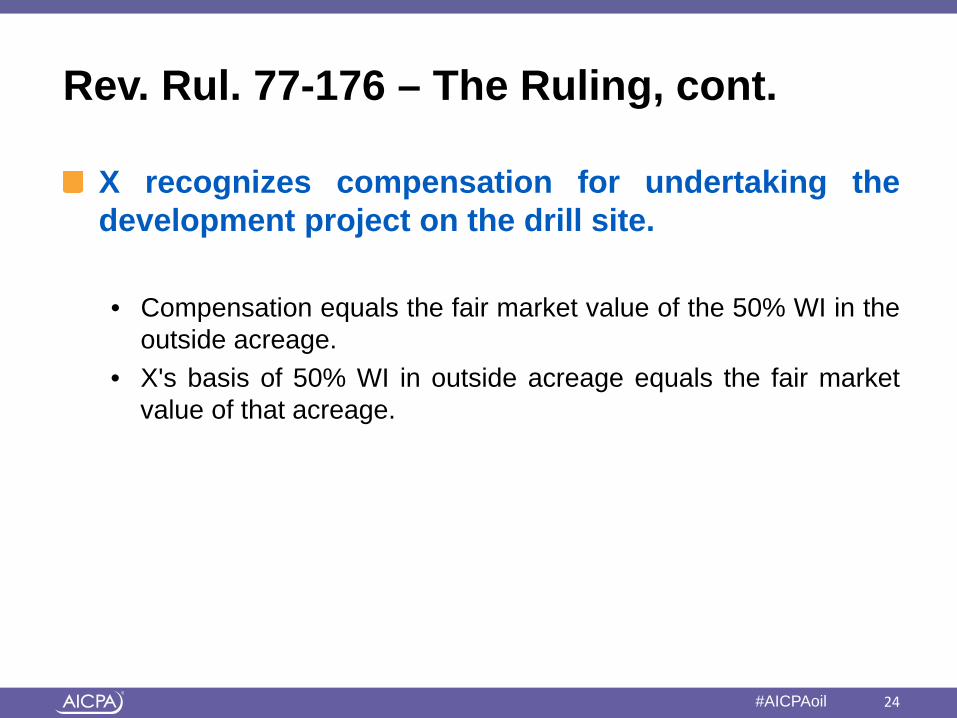

X recognizes compensation for undertaking the development project on the drill site.

• Compensation equals the fair market value of the 50% WI in the

outside acreage. • X's basis of 50% WI in outside acreage equals the fair market

value of that acreage.

24

American Institute of CPAs #AICPAoil

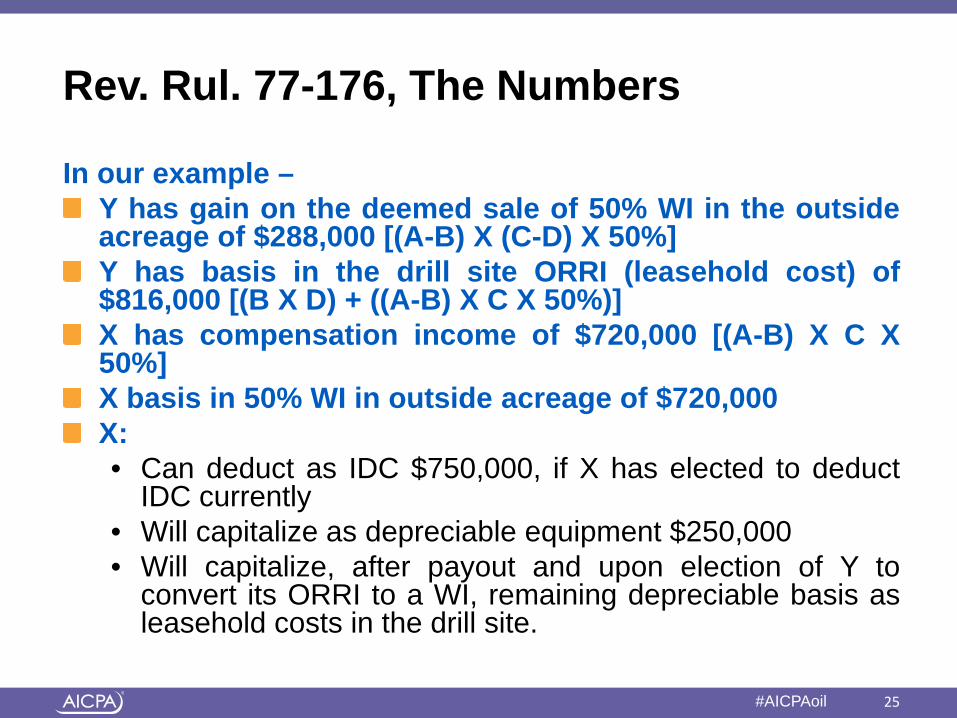

Rev. Rul. 77-176, The Numbers

In our example – Y has gain on the deemed sale of 50% WI in the outside acreage of $288,000 [(A-B) X (C-D) X 50%] Y has basis in the drill site ORRI (leasehold cost) of $816,000 [(B X D) + ((A-B) X C X 50%)] X has compensation income of $720,000 [(A-B) X C X 50%] X basis in 50% WI in outside acreage of $720,000 X: • Can deduct as IDC $750,000, if X has elected to deduct

IDC currently • Will capitalize as depreciable equipment $250,000 • Will capitalize, after payout and upon election of Y to

convert its ORRI to a WI, remaining depreciable basis as leasehold costs in the drill site.

25

American Institute of CPAs #AICPAoil

Rev. Rul. 77-176 - Analysis

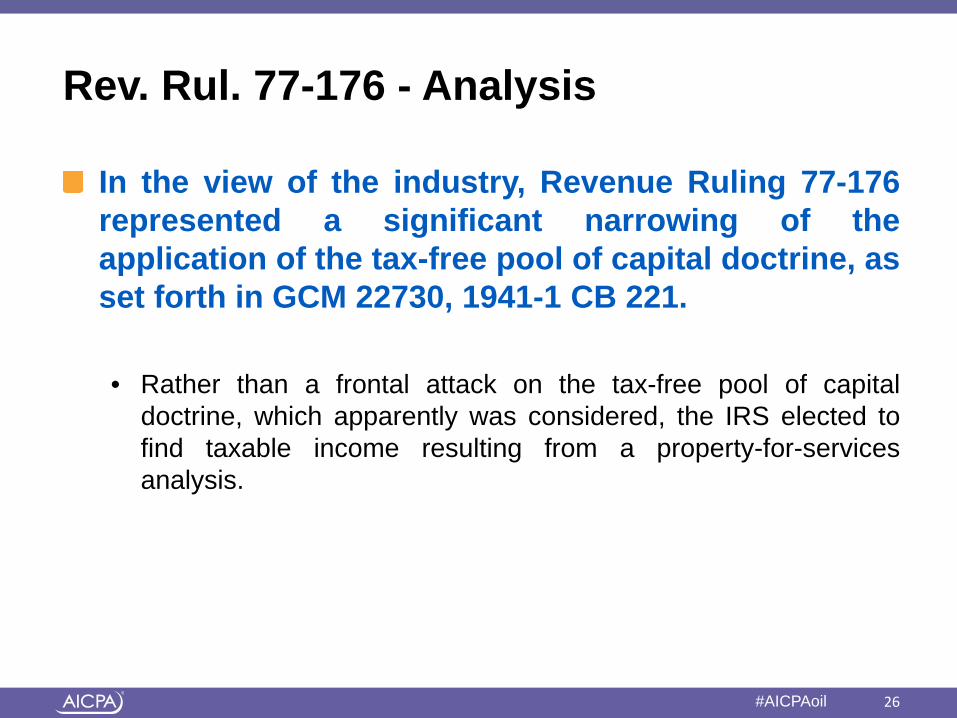

In the view of the industry, Revenue Ruling 77-176 represented a significant narrowing of the application of the tax-free pool of capital doctrine, as set forth in GCM 22730, 1941-1 CB 221.

• Rather than a frontal attack on the tax-free pool of capital

doctrine, which apparently was considered, the IRS elected to find taxable income resulting from a property-for-services analysis.

26

American Institute of CPAs #AICPAoil

Rev. Rul. 77-176 – Analysis, cont.

• Somewhat surprisingly, there has been no substantive litigation and no further citations of Revenue Ruling 77-176 by the IRS.

• One possible reason for the lack of subsequent actions on Rev. Rul. 77-176 is that the fact pattern is actually fairly unique. - The farmee in the farmout, X, is a driller who accepts a working

interest in exchange for actually drilling the well. Most oil and gas exploration and production companies do not drill their own wells, but contract with drilling companies to do so.

- Some of the reasoning in Rev. Rul. 77-176 about the taxation of receipt of property for services does not translate so easily to the payment by the farmee of the costs of contractors to drill and equip a well.

27

American Institute of CPAs #AICPAoil

Avoiding Rev. Rul 77-176 application

- Most tax practitioners approach Rev. Rul. 77-176 with an appropriately cautious assumption that the IRS may try to apply the ruling to a wide variety of obligation-well farmouts, not only to the narrow facts in the ruling.

- The most commonly-suggested and probably the most effective alternative is for X and Y to create a partnership for Federal income tax purposes (a tax partnership).

- Another frequently-suggested method of mitigating the ill effects of Revenue Ruling 77-176 is to assign the working interest and give the farmee the option to purchase the outside acreage at the value as determined before the drilling.

28

American Institute of CPAs #AICPAoil

Avoiding Rev. Rul 77-176 application, cont.

- Both of the two suggested methods above may encounter the application of Section 83 to cause taxation at the time the right to receive or acquire the outside acreage, inside or outside of a tax partnership, actually vests. They also may alter the intended economics of the deal.

29

American Institute of CPAs #AICPAoil

Avoiding Rev. Rul 77-176 application, cont.

Another solution may be to carefully examine the facts of the obligation-well transaction with which you are confronted to see if there are elements of the subject transaction that distinguish it from the facts in Revenue Ruling 77-176.

• For example, what if Y retained no overriding royalty in the drill site,

but only a back-in interest? • Also, would an agreement for the farmee to pay cash to someone

else to drill the obligation well distinguish it sufficiently from Revenue Ruling 77-176, where X drilled the well itself? It would seem that principles underlying Section 83 and other property-for-services arguments would not be available to upset the tax-free pooling of capital doctrine.

• There are many other variations on the theme that might distinguish a transaction from the one addressed Revenue Ruling 77-176.

• Nevertheless, the fact that you can distinguish does not necessarily mean the IRS will agree.

30

American Institute of CPAs #AICPAoil

An Ace in the Hole: The Doctrine of Rescission

If you, as the tax advisor, learn of an inadvertent sublease or a significantly adverse application of Rev. Rul. 77-176 during the year in which the transaction occurs, you might be able to negotiate a "Do Over" in the form of a rescission. In effect, the IRS is acknowledging a basic tenet of accounting: Income or loss for the year is the difference between the beginning and ending balance sheets.

31

American Institute of CPAs #AICPAoil

Rescission, cont.

Based on Revenue Ruling 80-58, 1980-1 CB 181, the IRS generally requires all of the following elements for a valid rescission: (1) the transaction must be pursuant to an agreement or contract that (2) in the same tax year (3) is rescinded in a formal and proper manner (such as by agreement of the parties), so that (4) the parties are returned to the same position as if that transaction had never occurred. There is no prohibition of the parties then executing a different deal that achieves the desired tax results. The IRS has indicated that it may be reviewing its position on the elements required to effect a valid rescission. A private letter ruling may be in order.

32

American Institute of CPAs #AICPAoil

Conclusion

We have addressed two types of conveyances that are common in oil patch that can result in adverse tax consequences.

• We outlined the structure of the deals • We have identified the adverse tax consequences • We have discussed ways to eliminate or mitigate the adverse

consequences.

Every deal can be different. Whether or not the contents of this presentation apply to a particular conveyance depends on the deal structure and can turn on a single word or phrase.

33